Asia-Pacific Maize Market Analysis by ���ϲ�����

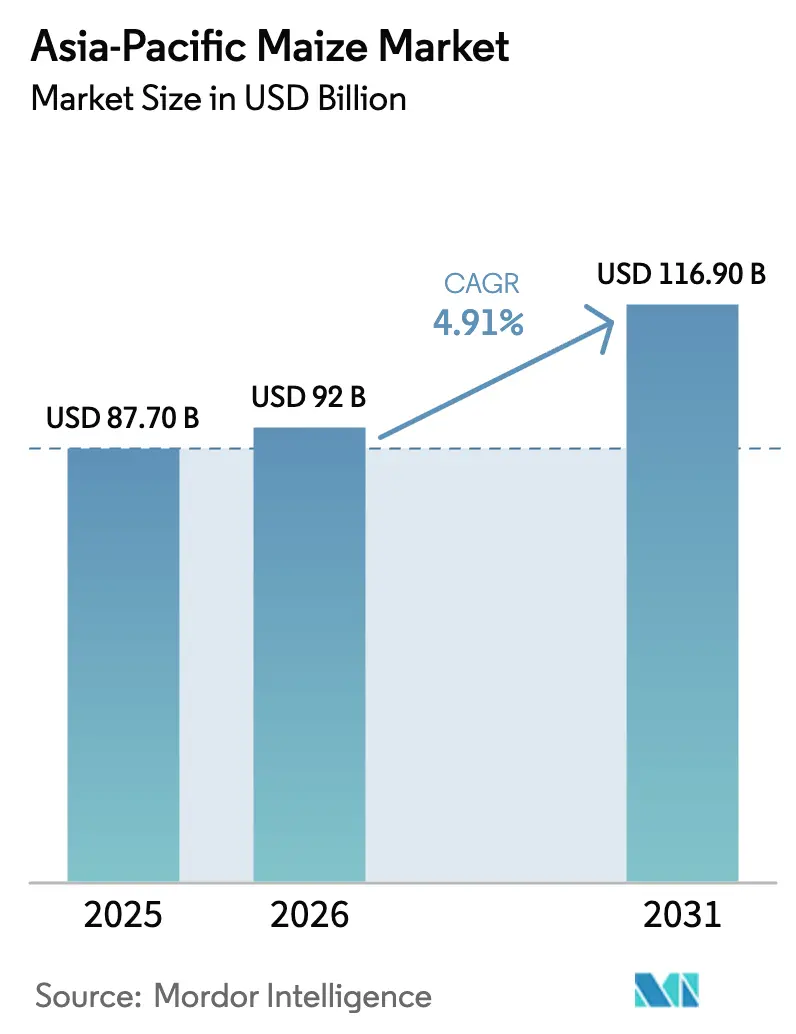

The Asia-Pacific maize market is projected to grow from USD 87.70 billion in 2025 to USD 92.00 billion in 2026, and is forecast to reach USD 116.90 billion by 2031, with a 4.91% CAGR over 2026-2031. Feed intensification across poultry and aquaculture remains the core structural driver, reinforced by deep-processing capacity additions in China and Southeast Asia that lift starch and sweetener throughput and widen downstream value pools. India’s ethanol blending policy continues to reallocate grain toward fuel in priority districts, which supports farm-gate prices, encourages acreage, and reshapes trade flows [2]Agricultural and Processed Food Products Export Development Authority, “Monthly Dashboard – Maize,” APEDA, apeda.gov.in. Processing enterprises are investing in higher operating rates as profitability improved in late 2025, which expands industrial demand for maize-derived starches, sweeteners, and amino acids in China [1]National Food and Strategic Reserves Administration, “Accelerated Progress, Rising Prices-Maize Market Sales Booming,” National Food and Strategic Reserves Administration, lswz.gov.cn. Policy and regulatory signals around feed efficiency and grain-saving in large consuming markets also influence ration formulas and sustain the resilience of the Asia-Pacific maize market across cycles.

Key Report Takeaways

By geography, China accounted for 66.0% of the Asia-Pacific maize market size in 2025, while India is projected to grow at a 6.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Maize Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feed demand expansion from poultry, aquaculture and dairy sector | +1.8% | Global, with core growth in China, India, and Southeast Asia | Medium term (2-4 years) |

| Industrial maize deep processing capacity build-out in China and Southeast Asia | +1.2% | China (primary), Indonesia, Thailand, and Vietnam | Long term (≥ 4 years) |

| India ethanol blending policy pull for grain-based ethanol | +0.9% | National (India), with early gains in Maharashtra, Karnataka, and Uttar Pradesh | Short term (≤ 2 years) |

| Hybrid seed adoption and mechanization improving yields in South and Southeast Asia | +0.7% | India, Indonesia, and Philippines, spillover to Myanmar and Cambodia | Medium term (2-4 years) |

| Trade facilitation and tariff adjustments under RCEP benefiting maize derivatives | +0.2% | Regional Comprehensive Economic Partnership (RCEP) signatories (The Association of Southeast Asian Nations (ASEAN)), China, Japan, South Korea, Australia, and New Zealand) | Long term (≥ 4 years) |

| Diversification of feed formulations increasing corn inclusion where competitive | +0.1% | China, Vietnam, and Thailand, and secondary markets in South Asia | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Feed demand expansion from poultry, aquaculture and dairy sector

China’s feed maize absorption reached 193.5 million metric tons in the 2025/26 marketing year, which anchored base demand despite profit-pressure periods for breeders during late 2025. Livestock and poultry inventories remained elevated by the end of 2025, which supported steady compound feed use and sustained corn inclusion within least-cost formulations. India’s poultry and cattle segments together absorbed large maize volumes in 2024–25, with official dashboards showing sustained pull from poultry integrators and dairy ration programs in key clusters. Aquaculture feed is expanding in Vietnam as stocking densities rise in priority basins and integrators scale higher performance formulas for shrimp and finfish. Corporate feed leaders have added capacity and digital traceability in recent years, with Charoen Pokphand Foods operating significant regional feed manufacturing and maintaining verified 100% traceable corn sourcing for Thailand, which reinforces procurement standards across the Asia-Pacific maize market. Policy programs in large consuming markets promote grain-saving actions and precision nutrition, which together sustain disciplined use of maize while protecting feed efficiency targets within the Asia-Pacific maize market.

Industrial maize deep processing capacity build-out in China and Southeast Asia

China's corn-starch and deep-processing system is projected to operate with an installed capacity exceeding 125 million metric tons by 2025. Throughput and operating rates are projected to improve, supported by better margins later in the year. In 2024, China's corn starch output reached 37.99 million metric tons, representing 63.3% of the global share. Additionally, nearly two-thirds of the national output was concentrated among top processors, highlighting scale advantages in energy and water management. Demand for high-fructose corn syrup (HFCS) across the Asia-Pacific region is anticipated to grow significantly during the forecast period. This growth supports steady corn demand for starch-sugar conversion in beverage and processed food channels. Multinational companies continue to invest in integrated processing hubs to secure feedstock and serve regional customers. For instance, Cargill’s Songyuan complex in Jilin converts corn into starches, HFCS, industrial alcohols, and feed coproducts, while also piloting water and fertilizer programs with contract growers. The extensive processing ecosystem in China allows for flexible product switching across starch derivatives and amino acids, enabling adaptability to shifting demand. This flexibility strengthens the Asia-Pacific maize market during fluctuations in commodity prices. Meanwhile, Southeast Asian facilities in Indonesia and Thailand are enhancing their capabilities to cater to halal and regional buyers. These developments gradually diversify sourcing away from China while anchoring regional value addition within the Asia-Pacific maize market.

India ethanol blending policy pull for grain-based ethanol

India advanced toward higher petrol blending targets in 2025 and continued to draw grain for ethanol, which supported acreage and local procurement in maize-growing belts. Official dashboards show that domestic users have absorbed more supply, while exports moderated as feed and industrial channels expanded their pull on available grain. Policy adjustments for the 2025/26 supply year widened allowable feedstocks for ethanol, which helps balance sugar-cycle swings and provides a hedge for distilleries that also procure maize. The alignment of oil marketing company tenders, quality standards, and state-level incentives is improving procurement visibility for maize belts linked to grain-based ethanol plants, which feeds into a predictable offtake and steadier farmer realization in the Asia-Pacific maize market [3]Press Information Bureau, “Foodgrain Production Breaks Records,” Ministry of Agriculture and Farmers Welfare, pib.gov.in. The ethanol corridor has emerged as a structural buffer that can smooth maize demand variability alongside feed and starch channels, which reinforces the Asia-Pacific maize market across seasons [2].

Hybrid seed adoption and mechanization improving yields in South and Southeast Asia

The ongoing adoption of hybrid seeds and a shift toward traited products, where regulations permit, are shaping the Asia-Pacific maize market. Government and industry initiatives are promoting traits such as drought tolerance, pest resistance, and improved standability, aligning with the region's increasing mechanization of planting and harvesting processes. These advancements contribute to greater yield stability for smallholders and mid-size farms. In Indonesia, the seed industry is expanding distribution and extension efforts in key provinces, supported by association-led programs that enhance access to quality seeds and agronomic guidance. Similarly, the Philippines has allocated funding for seed research and development while maintaining floor-price support mechanisms. These measures mitigate risks for growers adopting improved varieties, encouraging seasonal adoption and reducing input investment risks. The combination of hybrid seed adoption and precision services, such as optimized planting density and nutrient management, continues to close the yield gap compared to global benchmarks, strengthening the Asia-Pacific maize market in the medium term.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited access to agricultural finance among smallholders | -0.5% | India, Indonesia, and Philippines, rural zones in Myanmar and Cambodia | Medium term (2-4 years) |

| Limited access to quality inputs (certified seed and balanced fertilizers) | -0.4% | India (eastern states), Indonesia (outer islands), and Philippines (Mindanao) | Medium term (2-4 years) |

| Sanitary and Phytosanitary (SPS) and Genetically Modified Organism (GMO) regulatory frictions limiting cross-border trade and planting | -0.3% | China (import controls), India (GM planting ban), ASEAN (varied GMO approvals) | Long term (≥ 4 years) |

| Substitution pressure from wheat, cassava and Distillers Dried Grains with Solubles (DDGS) in feed during price spreads | -0.2% | China (wheat), Southeast Asia (cassava), Vietnam and South Korea (DDGS) | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Limited access to quality inputs (certified seed and balanced fertilizers)

Certified seed use and balanced fertilizer application remain inconsistent across parts of South and Southeast Asia, which constrains yield gains in rain-fed zones and keeps productivity below global front-runners in several belts of the Asia-Pacific maize market. Public programs are attempting to improve input access and extension, but logistics constraints slow last-mile delivery for smallholders in outer islands and remote districts. The Philippines has rolled out funding for seed R&D and price protection schemes for growers, which support hybrid adoption and help stabilize returns during market swings. Regional variability in credit access also limits farmers’ ability to upgrade inputs and mechanize at scale, which slows the pace of agronomic gains in the Asia-Pacific maize market. Over time, better extension, seed quality assurance, and nutrient stewardship are projected to lift the input baseline and reduce yield dispersion across districts.

Substitution pressure from wheat, cassava and Distillers Dried Grains with Solubles (DDGS) in feed during price spreads

China's feed wheat consumption is projected to reach 36 million metric tons in MY2025/26 as narrowing price spreads reduce corn inclusion in feed rations during those periods. The introduction of Brazilian DDGS imports in May 2025, enabled by new phytosanitary protocols, expands protein and energy options, potentially reducing corn usage if delivered costs are competitive. In Southeast Asia, cassava chips and pellets continue to serve as energy substitutes when economically viable. Controlled trials indicate that fermented cassava byproducts can replace substantial portions of maize in duck diets without affecting performance. Vietnam's cassava supply to feed channels is projected to grow in 2026 following a weaker 2025, supporting flexible rationing in the aquaculture and livestock industries. The use of least-cost formulation tools enables feed mills to alternate between wheat, cassava, DDGS, and corn, highlighting the significance of price spreads and policy changes in influencing short-term corn demand within the Asia-Pacific maize market.

Geography Analysis

China is projected to maintain a dominant position in the Asia-Pacific maize market by 2025, accounting for 66.0% of the market value. The country anchors both feed and processing demand. This highlights China's significant influence on the regional maize market. Production gains have been concentrated in the Northeast, driven by increased mechanization and favorable moisture conditions, which have supported higher productivity in recent years and ensured a steady supply for feed mills and starch plants. Industrial processing activity strengthened toward the end of 2025, supported by improved profitability and higher operating rates. This led to increased production of starches, sweeteners, and fermentation outputs, further reinforcing China's influence on regional maize flows. Imports, however, declined sharply in 2024/25 and remained below 6 million metric tons in 2025/26 due to strict quota enforcement. This reflects a continued emphasis on domestic supply and a narrower import window compared to earlier in the decade. Policy measures aimed at promoting grain-saving in feed are projected to reduce maize intensity per unit of animal product by 2030. This is projected to moderate long-term demand growth and emphasize the role of co-products and alternative proteins in feed formulations within the Asia-Pacific maize market.

India is the fastest-growing country in the Asia-Pacific maize market, with a CAGR of 6.0% during the forecast period of 2026–2031. This growth is driven by the expansion of the poultry sector and ethanol blending initiatives, which redirect grain flows to domestic users and help stabilize farm incomes in several regions. Between 2023–24 and 2025–26, production increased due to acreage expansion and favorable seasonal conditions in key states. Official crop updates and global production data confirm the supply growth, which supports feed mills, starch plants, and distilleries. Export shipments to neighboring countries declined as domestic demand grew, while targeted imports increased in 2024–25 to address localized requirements. This highlights how strategic trade adjustments complement the domestic supply-demand balance in the Asia-Pacific maize market. Feed and industrial sectors continue to benefit from coordinated policies and crop support measures, which promote mechanization and the adoption of improved seeds across several states in the region.

Indonesia achieved self-sufficiency in 2025, producing 16.11 million metric tons of maize, exceeding consumption by 470,000 metric tons, with carry-over stocks reaching approximately 4.5 million metric tons. This enabled a zero-import position for 2026 and allowed tentative export tenders without compromising domestic supply security in the Asia-Pacific maize market. Government-set farm-gate and warehouse floor prices have supported planting decisions and encouraged the adoption of mechanization and certified seeds in priority provinces, enhancing on-farm resilience. In contrast, the Philippines remains structurally dependent on imports, with MY2025/26 imports projected at 1.85 million metric tons to bridge the gap between production and consumption. This reliance continues to expose the country to import prices and quality standards enforced by national agencies. During the first half of 2025, maize output increased significantly. However, typhoon-related losses in parts of the Cagayan Valley later in the year highlighted the need for post-harvest investments and resilient agronomic practices in the Asia-Pacific maize market.

Competitive Landscape

The Asia-Pacific maize market features a bifurcated structure where seed and deep-processing segments show moderate consolidation while feed manufacturing and farm production remain fragmented. In seeds, the combined share of leading global and regional firms is meaningful but leaves room for local champions to compete on germplasm fit and distribution reach in price-sensitive smallholder segments across the Asia-Pacific maize market. The starch industry in China displays a higher concentration among top processors, which leverage scale for energy and water efficiency and integrate into amino acids and modified starches to smooth margins across price cycles. These structures support steady throughput for corn-based derivatives that flow into food, beverage, and industrial channels in the Asia-Pacific maize market.

Global supply-chain players continue to reshape origination and logistics, which influences availability and pricing for buyers across the Asia-Pacific. The merger of Bunge and Viterra in July 2025 consolidated export and crush networks that connect South America and the Black Sea with Asia, and it came with regulatory conditions to protect supply reliability in China, confirming the strategic weight of Asian demand. Cargill’s integrated corn-processing hub in Jilin highlights a model where feedstock contracting, processing, and customer channels co-locate to reduce logistics risk and serve domestic and export markets efficiently within the Asia-Pacific maize market. These moves complement country-level policy efforts that emphasize domestic supply security while keeping trade lanes adaptable during crop shocks or policy swings in the Asia-Pacific maize market.

In feed, regional champions remain influential while the long tail of mills preserves a decentralized landscape. Charoen Pokphand Foods maintains large regional capacity and continues to invest in smart-factory upgrades and traceable sourcing that reduce contamination risk and align with emerging Environmental, Social, and Governance (ESG) requirements, which strengthens customer confidence across Southeast Asia in the Asia-Pacific maize market. National feed markets remain fragmented beyond the leading groups, which slows the adoption of software-enabled precision nutrition in certain provinces and maintains variability in corn inclusion practices. As a result, competitive strategy revolves around scale, integration, and traceability in some nodes and around localized service, credit, and input bundling in others, which together define the current dynamics of the Asia-Pacific maize market.

Recent Industry Developments

- December 2025: China’s National Development and Reform Commission (NDRC) plans to expand the cultivation of high-quality forage crops, including silage corn and alfalfa, while implementing large-scale yield improvement programs for major crops. The initiative aims to increase the production of specialty crop varieties and align agricultural output with domestic demand. It also focuses on protecting arable land, ensuring balanced land use, and optimizing the allocation of agricultural land.

- March 2025: Cargill has opened a new corn milling plant in Gwalior, Madhya Pradesh, to address the growing demand for safe and high-quality food solutions in India. This facility has been established in collaboration with Saatvik Agro Processors. Under a business agreement with Cargill, Saatvik has developed this dedicated production facility for starch derivatives, with an initial production capacity of 500 metric tons per day, which can be expanded to 1,000 metric tons per day.

- May 2025: The approval of Brazilian DDGS imports into China in 2025, priced competitively at approximately USD 317 per metric ton compared to higher-cost US imports (USD 496 per metric ton), is projected to reduce feed costs for Chinese producers. This development is anticipated to increase demand for cost-effective alternatives to soybean meal. The shift towards a "United States + Brazil" trade model enhances regional supply security and promotes the availability of stable, lower-cost animal feed. This is anticipated to drive growth in the Asia-Pacific feed and maize market.

Asia-Pacific Maize Market Report Scope

The Asia-Pacific Maize Market Report is Segmented by Geography (India, China, Indonesia, and More). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Import Analysis (Value and Volume), Export Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecast, List of Key Players, Regulatory Framework, Logistics and Infrastructure, and Seasonality Analysis. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Geography

| India | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| China | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Indonesia | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Philippines | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis |

| By Geography | India | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| China | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Indonesia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Philippines | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

Key Questions Answered in the Report

What is the size and growth outlook for the Asia-Pacific maize market to 2031?

The Asia-Pacific maize market size is USD 92.0 billion in 2026 and is expected to reach USD 116.9 billion by 2031 at a 4.91% CAGR.

Which country holds the largest share in the Asia-Pacific maize market?

China held 66.0% of the regional value in 2025, anchored by strong feed demand and deep-processing throughput.

Which country is the fastest growing within the Asia-Pacific maize market through 2031?

India is projected to grow at a 6.0% CAGR to 2031, supported by ethanol blending, poultry expansion, and steady rotation to domestic users.

What are the main demand pillars sustaining the Asia-Pacific maize market?

The core pillars are compound feed for poultry and aquaculture and industrial conversion into starches, sweeteners, and amino acids, with ethanol blending creating an additional buffer in India.

How are policy and trade changes affecting near-term balance in the Asia-Pacific maize market?

China's quota enforcement reduces imports, Indonesia's zero-import stance tightens local balances, and Philippine imports bridge structural gaps under strict quality controls, while Brazil-origin DDGS entry into China increases formulation flexibility.

What supply-side upgrades are improving resilience across the region?

Hybrid seed expansion, mechanization, and traceability programs in large integrators are lifting yield stability and procurement quality, which support consistent supply to feed mills and processors.

Page last updated on: