Asia-Pacific Guar Market Analysis by ���ϲ�����

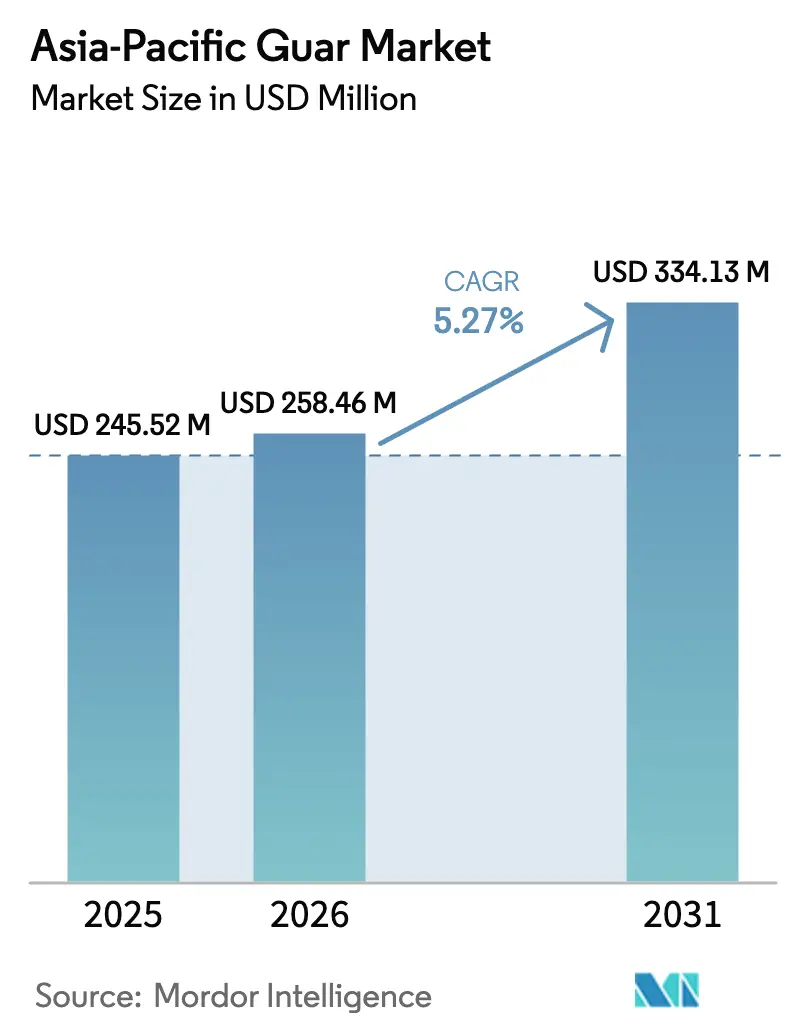

The Asia Pacific guar market size is projected to grow from USD 245.52 million in 2025 to USD 258.46 million in 2026 and is forecast to reach USD 334.13 million by 2031 at a 5.27% CAGR over 2026-2031. The expansion reflects shifting end-use priorities, particularly the pivot from hydraulic fracturing toward premium food, beverage, and biodegradable packaging applications. India supplies nearly 80% of global guar and anchors regional availability, but its concentration in Rajasthan introduces acute weather-related procurement risk. China’s rising shale activity adds volume demand yet increasingly substitutes polyacrylamide in high-temperature wells, tempering guar growth in the oil and gas segment. Urban consumers across China, India, and Japan favor clean-label foods and beverages, driving formulators to select guar over costlier xanthan or cellulose, while Japanese regulations on single-use plastics have opened a pathway for biodegradable guar-based films.

Key Report Takeaways

- By geography, India led with 71.20% of the Asia Pacific guar market share in 2025, while Australia is projected to advance at a 7.60% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Guar Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising export-oriented demand for processed foods | +0.8% | India, China, and Japan | Medium term (2-4 years) |

| Growing use of guar gum as a clean-label thickener in premium dairy and plant-based beverages | +0.9% | China, India, Australia, and Japan | Short term (≤ 2 years) |

| Uptick in shale stimulation projects in China’s Sichuan and Tarim basins | +0.6% | China with spillover to India exports | Medium term (2-4 years) |

| Emergence of biodegradable guar-based films replacing single-use plastics in Japan | +0.4% | Japan, early adoption in urban China | Long term (≥ 4 years) |

| Rapid expansion of e-commerce cosmetics that favor natural rheology modifiers | +0.5% | China, India, and Japan | Short term (≤ 2 years) |

| Government incentives for drought-resilient crops in Australia’s dryland farming belts | +0.3% | Australia | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising Export-Oriented Demand for Processed Foods

Exports of processed foods from India reached USD 7.8 billion in 2025, with government programs targeting USD 100 billion by 2030, which sustains demand for hydrocolloid stabilizers in export-grade products [1]Source: Volza, “India Guar Gum Export Data,” volza.com. China shipped significant amount of processed foods in 2023, during which seafood processors deployed guar to improve freeze-thaw stability. Japan exported JPY 1.45 trillion (approximately USD 9.7 billion) of food products in 2024, targeting premium positioning that aligns with clean-label ingredient trends and natural thickener preferences [2]Source: Ministry of Agriculture, Forestry and Fisheries, “2024 Food Export Statistics,” maff.go.jp. Regional food-thickener demand is growing, outpacing global averages, as processors seek lower-cost alternatives to xanthan. India’s guar gum shipments have grown since 2021 while rising faster in value, indicating premiumization and derivative innovation.

Growing Use of Guar Gum as a Clean-Label Thickener in Premium Dairy and Plant-Based Beverages

The global plant-based milk segment surpass in 2024, with Asia Pacific posting the fastest gain as urban consumers adopt dairy alternatives. Guar’s neutral taste and quick hydration enhance mouthfeel at 0.1-0.3% inclusion, making it preferable to cellulose in premium oat and almond beverages. A 2024 peer-reviewed study confirmed guar represents 90% of global galactomannan supply and delivers superior swelling ratios compared with synthetic thickeners. Syensqo launched blockchain-enabled traceability in 2025, adding supply-chain transparency that appeals to premium brands [3]Source: Syensqo, “The Sustainable Guar Initiative,” syensqo.com. Formulators blend guar with locust bean gum to achieve synergistic viscosity at lower total hydrocolloid loadings, saving 10-15% on ingredient costs.

Uptick in Shale Stimulation Projects in China’s Sichuan and Tarim Basins

China consumed 422.2 billion cubic meters of natural gas in 2024, up 7.8%, with shale output expanding in Sichuan and Tarim. Deep reservoirs above 150 °C prompt operators to substitute guar with polyacrylamide for higher thermal stability, compressing guar’s share even as well count rises. Indian exporters shipped guar gum to China in 2024, so any substitution would directly affect trade volumes. Environmental codes are tightening residue limits for fracturing fluids, favoring synthetic polymers that reduce formation damage. Guar demand linked to Chinese shale is growing more slowly due to limited shale development in the region.

Emergence of Biodegradable Guar-Based Films Replacing Single-Use Plastics in Japan

Japan’s Plastic Resource Circulation Act (PRCA) from 2022 drives the shift from single-use plastics toward biodegradable alternatives. Guar’s cost of USD 2-5 per kilogram is lower than cellulose substitutes, positioning it for mid-tier applications. Technical hurdles involve achieving tensile strength and moisture resistance without chemical modifications that undermine biodegradability. Ingredient suppliers and converters aim to commercialize films targeting urban markets where consumers are willing to pay premiums for sustainable packaging.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material supply concentration in Rajasthan leading to procurement risk | -0.7% | Global with acute impact on China, Japan, and Australia importers | Short term (≤ 2 years) |

| High year-on-year price volatility tied to monsoon variability | -0.8% | Global | Short term (≤ 2 years) |

| Availability of cheaper cellulose and xanthan substitutes for thickening | -0.6% | China, Japan, and Australia | Medium term (2-4 years) |

| Stringent residue limits on hydro-fracturing additives in environmental codes | -0.4% | China with regulatory spillover to Australia | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Raw-Material Supply Concentration in Rajasthan Leading to Procurement Risk

Rajasthan produces 70-72% of India’s guar, accounting for about 56% of global output, so a localized weather shock reverberates across global supply. A weak monsoon can reduce yields by up to 30%, sparking double-digit price moves within weeks. India exported USD 568.96 million and 453,612 metric tons of guar gum in 2024. and disruptions therefore ripple to leading buyers in the United States, Germany, and China. Alternative origins remain marginal, as Australia is experimental and Pakistan contributes modest volumes. Blockchain traceability under Syensqo’s initiative improves transparency but does not hedge physical supply risk.

High Year-on-Year Price Volatility Tied to Monsoon Variability

Guar is predominantly rain-fed, making yields highly sensitive to monsoon timing and distribution. Prices averaged INR 10,300-10,800 (USD 123-129) per 100 kgs in early 2025 but have historically spiked, as in 2012 when rates exceeded USD 12,000 per metric ton. In 2024, the instability index ranked guar as the most volatile Indian export commodity. During price spikes, buyers reformulate with xanthan, cellulose, or tara gum, eroding guar share where functional parity exists. Futures markets remain undeveloped, so most users stay exposed to spot volatility.

Geography Analysis

India’s dominance rests on Rajasthan’s arid climate and Kandosol soils that suit guar, along with decades of seed improvement and agronomic knowledge. Processing hubs near Jodhpur convert beans into splits and powder, supporting rapid shipment to global buyers. The Asia-Pacific guar market size linked to Indian deliveries will grow as exporters introduce certified sustainable grades to win premium contracts. Yet monsoon dependency exposes the supply chain to yield swings, which can send prices sharply higher, as seen in recent seasons with 10-15% volatility.

Australia aims to build a secondary supply base. Trials in the Northern Territory show promising yields under supplemental irrigation and could enable local processors to capture value from milling and derivative production. Government water-infrastructure incentives make on-farm dams and low-pressure systems viable, potentially integrating guar into crop rotations that include sorghum and chickpeas. If processing plants come online, Australia could supply close-to-market volumes to East Asian clients, reinforcing regional resilience.

China and Japan play outsized roles on the demand side. Chinese shale stimulation once used significant amounts of guar but now prefers polyacrylamide in high-temperature reservoirs. Nonetheless, China’s packaged food and e-commerce cosmetics industries continue to import guar for viscosity and texture. Japan’s Plastic Resource Circulation Act (PRCA) accelerates research into biodegradable guar films, and its premium processed food exports pull in clean-label stabilizers. Together, these demand nodes counterbalance the supply risk that stems from India’s geographic concentration.

Competitive Landscape

The Asia-Pacific guar market shows moderate concentration. Hindustan Gum leads with a major share, leveraging integrated farming programs and in-house testing to ensure batch consistency. Jai Bharat Gum, Neelkanth Polymers, and Vikas WSP constitute the organized mid-tier, focusing on export logistics and derivative innovation such as fast-hydrating guar for energy drilling and high-protein meal for animal feed.

The unorganized segment, comprising small-scale, traditional, and informal business units operating outside systematic corporate oversight and industrial standardization, accounts for 90% of processors by number but lacks quality certification, limiting participation in pharmaceutical and premium food applications. Organized exporters invest in precision agriculture, including remote sensing to monitor crop health and schedule harvests, thereby stabilizing quality and reducing waste. Global ingredient majors are reshaping the landscape. Tate and Lyle completed the USD 1.8 billion CP Kelco acquisition in 2024, adding pectin and specialty gums to its portfolio and integrating seven regional plants and nine application centers across the Asia-Pacific.

The combined entity can cross-sell hydrocolloid blends and offer technical formulation support, potentially raising competitive pressure on regional guar processors. Syensqo’s Sustainable Guar Initiative, launched with L’Oréal, Procter & Gamble, and Henkel in 2025, sets a precedent for blockchain-based traceability that could split the market into commodity and certified supply streams. Processors that adopt transparent sourcing may command price premiums of 5-10% in cosmetics and premium foods.

Recent Industry Developments

- March 2025: India's guar gum prices stabilized in the range of INR 10,300 to INR 10,800 per quintal during January-March 2025, reflecting balanced supply-demand dynamics following a moderate monsoon season in Rajasthan. The pricing stability enabled exporters to secure medium-term contracts with European and North American buyers seeking predictable input costs for food and industrial applications.

- December 2024: Japan's food exports reached JPY 1.507 trillion (approximately USD 9.7 billion) in 2024, with premium product positioning driving sustained demand for clean-label thickeners such as guar in export-oriented processed foods, particularly in sauces, dressings, and frozen desserts.

- November 2024: Tate & Lyle PLC completed its USD 1.8 billion acquisition of CP Kelco from J.M. Huber Corporation, combining Tate & Lyle's sweetening and mouthfeel platforms with CP Kelco's pectin and speciality gums portfolio, included guar, to create a global speciality food and beverage solutions business.

Asia-Pacific Guar Market Report Scope

Asia Pacific Guar Market Report is Segmented by Geography (India, China, Japan, and Australia). The Report Includes Production (Volume), Consumption (Value and Volume), Imports (Value and Volume), Exports (Value and Volume), Wholesale Price Trend Analysis and Forecast, Regulatory Framework, List of Key Players, Logistics and Infrastructure, and Seasonality Analysis. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Geography

| China | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Australia | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| India | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Japan | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis |

| By Geography | China | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Australia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| India | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Japan | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

Key Questions Answered in the Report

How large is the Asia-Pacific guar market in 2026?

The Asia-Pacific guar market size is estimated at USD 258.46 million in 2026.

What is the forecast growth rate through 2031?

The market is projected to register a 5.27% CAGR from 2026 to 2031.

Which country contributes the most supply?

India accounts for 71.20% of regional value in 2025, reflecting its dominant production in Rajasthan.

Why is Australia considered the fastest-growing country segment?

Government incentives for drought-resilient crops and Commonwealth Scientific and Industrial Research Organisation (CSIRO) agronomy trials support a 7.60% CAGR through 2031.

What drives rising guar usage in premium dairy and plant-based beverages?

Consumers favor clean-label formulations, and guar provides efficient mouthfeel and stability at low inclusion rates.

How does the Tate and Lyle-CP Kelco deal affect market competition?

The combined entity offers broader hydrocolloid portfolios and application support, intensifying competition for regional processors.

Page last updated on: