Africa Lime Market Analysis by ���ϲ�����

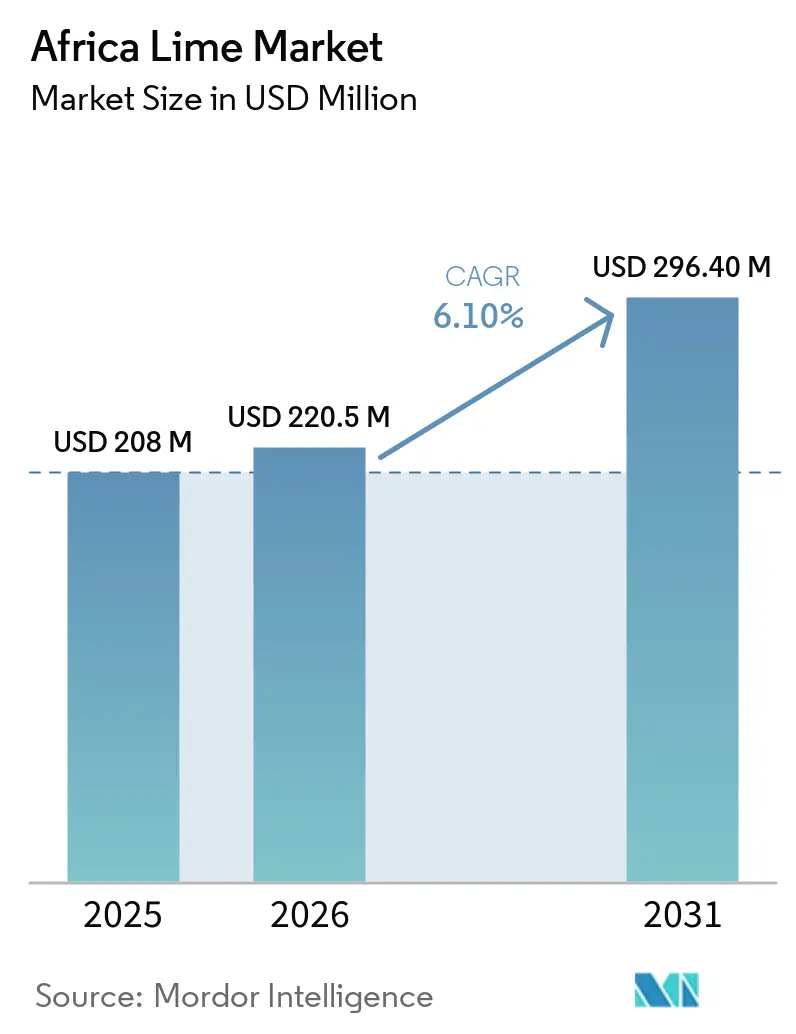

The Africa lime market size is projected to grow from USD 208 million in 2025 to USD 220.5 million in 2026 and is forecast to reach USD 296.4 million by 2031, registering a CAGR of 6.1% during 2026-2031. Reduced intra-African tariffs, expanding citrus replanting initiatives, and increasing demand for natural preservatives in ready-to-drink beverages are driving regional trade flows, particularly between Southern and North Africa. Carbon-credit funding for lime agroforestry is assisting smallholders in covering establishment costs, while investments in value-added processing are strengthening the connection between fresh fruit supply and industrial applications. However, pest outbreaks, particularly Huanglongbing (HLB), and inadequate cold-chain infrastructure continue to constrain effective supply in several production regions. Nevertheless, ongoing public-private investments in orchard revitalization and logistics are gradually alleviating these challenges. Competitive intensity remains moderate, as fragmented smallholder production coexists with a limited number of vertically integrated processors that dominate export-grade volumes.

Key Report Takeaways

By geography, South Africa led with the largest 32% of the Africa lime market share in 2025, and Egypt's market size is forecast to record the fastest growth, advancing at a 7.8% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Lime Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing use of lime preservatives in ready-to-drink beverages | +0.8% | North, West, and Southern Africa | Medium term (2-4 years) |

| Rising demand from pharmaceutical and nutraceutical applications | +0.6% | South Africa, Egypt, and Tunisia | Long term (≥4 years) |

| Government support for citrus orchard revitalization programs | +1.2% | Egypt, Tunisia, Algeria, and Sudan | Medium term (2-4 years) |

| Export tariff reductions under the African Continental Free Trade Area (AfCFTA) | +1.5% | Continental member states | Long term (≥4 years) |

| Vertical farming enabling year-round lime seedling supply | +0.4% | Kenya, Nigeria, and South Africa | Long term (≥4 years) |

| Carbon-credit funding for lime agroforestry expansion | +0.7% | Kenya, Tanzania, and Southern Africa | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Growing Use of Lime Preservatives in Ready-to-Drink Beverages

A study conducted by researchers from Universitas Airlangga, Indonesia, published in 2026, demonstrated that lime juice exhibits significant antimicrobial activity. The study reported inhibition zones of 23–12 mm against Staphylococcus aureus, 21–13 mm against Pseudomonas aeruginosa, and 18–10 mm against Escherichia coli across tested concentrations [1]Source: World Journal of Advanced Research and Reviews (WJARR), Comparison of Antibacterial Activity of Lime and Lemon Juices on Common Bacteria, wjarr.com . These results highlight lime juice's effectiveness in inhibiting key spoilage and pathogenic bacteria, confirming its potential as a natural preservative. This evidence aligns with the growing use of lime-based ingredients in clean-label ready-to-drink beverages, particularly in regions where manufacturers are transitioning away from synthetic preservatives.

Rising Demand from Pharmaceutical and Nutraceutical Applications

A 2024 study by researchers from Pukyong National University, Korea Food Research Institute, and the University of Southern California revealed that lime peel-derived extracts contain hesperidin at 66.44 mg/g, eriocitrin at 46.17 mg/g, and narirutin at 86.77 mg/g. These results demonstrate the high concentration of bioactive flavonoids in lime peel, which are extensively used in pharmaceutical and nutraceutical applications. The findings support the increasing industrial use of lime by-products for value-added extraction, encouraging processors to improve recovery efficiency and driving the growing demand for secondary lime products in global and African markets.

Government Support for Citrus Orchard Revitalization Programs

The revitalization of citrus orchards in North Africa is bolstering the structural foundation of the African lime market. Enhancements in irrigation efficiency, orchard renewal, and farm management practices are improving productivity, fruit quality, and yield consistency. Efforts to address aging plantations and fragmented landholdings are facilitating more efficient and scalable cultivation, along with improved supply chain integration. Additionally, the increased adoption of advanced agronomic techniques by growers is contributing to higher output and greater resilience to climate variability. Consequently, citrus production is becoming more stable and reliable, ensuring a consistent supply of raw materials for both fresh and processed applications, thereby supporting sustained growth in the regional lime market.

Export Tariff Reductions Under The African Continental Free Trade Area (AfCFTA)

A study published by the United Nations Economic Commission for Africa in 2025 projected that the implementation of the African Continental Free Trade Area would increase intra-African trade by 45% by 2045 [2]Source: United Nations Economic Commission for Africa, AfCFTA Benefits Will Be Across Sectors – Economic Report on Africa 2025, uneca.org. This growth is attributed to tariff reductions and improved trade facilitation. The findings emphasize that reduced trade barriers and more efficient customs processes enhance regional market access while lowering transaction costs. This development supports the increasing focus on intra-African trade of agricultural commodities, such as citrus and lime derivatives, encouraging exporters to diversify beyond traditional markets and bolstering regional supply chains among participating countries.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pest pressure from Huanglongbing (HLB) and fruit fly | -1.3% | South Africa, East Africa, and Sudan | Short term (≤2 years) |

| Volatile farm-gate prices beyond peak export seasons | -0.9% | South Africa, Egypt, and Tunisia | Short term (≤2 years) |

| High post-harvest losses from weak cold-chain infrastructure | -1.6% | Sub-Saharan Africa (ex. South Africa) | Medium term (2-4 years) |

| Competition from synthetic citric acid alternatives | -0.7% | Continental industrial buyers | Long term (≥4 years) |

| Source: ���ϲ����� | |||

Pest Pressure from Huanglongbing (HLB) and Fruit Fly

A 2025 study by researchers from the University of Technology and Applied Sciences, Oman, revealed that Huanglongbing (HLB) infection in lime results in substantial yield losses, increased fruit drop, and eventual tree mortality, significantly diminishing production capacity. The study also noted that HLB has already been identified in lime-growing regions of Oman, presenting a critical threat to citrus productivity. These findings underscore the severe impact of the disease on lime cultivation, as it degrades fruit quality, hastens orchard decline, and heightens management challenges and production risks.

Volatile Farm-Gate Prices Beyond Peak Export Seasons

Volatility in farm-gate prices outside peak export windows remains a significant constraint for the Africa lime market. Seasonal supply gluts, combined with limited cold storage and weak post-harvest infrastructure, force many smallholders to sell immediately after harvest at lower prices. This reduces income stability and discourages long-term investment in orchard management and productivity improvements. Inconsistent access to structured trading mechanisms, such as forward contracts, further exposes growers to sudden price fluctuations. Additionally, the absence of formal hedging tools limits risk management options, making producers highly vulnerable to market swings and demand variability across domestic and export channels.

Geography Analysis

South Africa led with the largest 32% of the Africa lime market share in 2025, driven by its well-established citrus infrastructure and export capacity. Its robust logistics network and integration into global markets support its leading position in the regional citrus trade. However, challenges such as increasing disease pressure and stricter export standards persist. Meanwhile, Egypt is expanding its citrus export presence through advancements in cold-chain logistics and improved port connectivity, which enhance product quality, shelf life, and access to international markets.

Egypt's market size is projected to achieve the fastest growth, with a forecasted CAGR of 7.8% from 2026 to 2031. Tunisia's emphasis on organic and GlobalGAP-certified citrus production facilitates entry into premium export markets. Algeria is working to stabilize output by expanding cultivation beyond traditional regions. In contrast, Sudan's production potential remains underutilized due to logistical and geopolitical challenges, limiting its participation in exports. In East Africa, emerging citrus cultivation is being supported by sustainability-linked financing. Meanwhile, Morocco is gradually expanding its established citrus export infrastructure to include diversified fruit categories, such as lime production.

Regional variations in infrastructure, certification, and logistics significantly impact supply dynamics across Africa. Countries with developed cold-chain systems and strong export compliance capabilities are better equipped to meet international demand, while others face challenges due to inadequate post-harvest systems and restricted market access. According to the Food and Agriculture Organization, Africa produced 2.15 million metric tons of limes and lemons in 2024, underscoring the continent's increasing importance in the global lime supply [3]Source: Food and Agriculture Organization (FAO), FAOSTAT Database – Crops and Livestock Products (Limes and Lemons Production), fao.org. These disparities in production affect trade flows, investment trends, and regional competitiveness.

Competitive Landscape

The competitive landscape comprises a mix of smallholder cultivation and larger integrated operations engaged in processing and export activities. Companies with established supply chains and processing infrastructure are better equipped to cater to high-value segments, including juice concentrates and essential oils. In contrast, smaller growers often encounter challenges related to storage, certification, and financing, which restrict their access to premium export markets. This results in variations in market participation based on scale, infrastructure, and compliance capabilities.

Technology adoption differs across regions, with advanced producers utilizing precision agriculture tools to enhance efficiency and reduce input costs. Techniques such as satellite-based irrigation monitoring and digital pest surveillance are improving yield stability for larger farms. Meanwhile, smallholders are gradually gaining access to financial and technical support through sustainability-focused initiatives, though scalability remains constrained by cost and coordination challenges. Adherence to international phytosanitary standards continues to play a critical role in determining participation in export-oriented supply chains.

Processing and export-oriented activities are playing a significant role in shaping competitive positioning within the market, particularly for participants with established logistics and compliance capabilities. According to the Food and Agriculture Organization, Africa exported 0.83 million metric tons of lemons and limes in 2024, demonstrating strong engagement in the global citrus trade (FAOSTAT, 2024). This export volume underscores the importance of efficient post-harvest handling, standardized quality, and compliance with international phytosanitary requirements. Producers with greater integration across harvesting, processing, and export logistics are better equipped to leverage the growing cross-border demand.

Recent Industry Developments

- December 2025: San Miguel invested approximately R490 million (USD 26.5 million) in a lemon processing facility at the Coega Special Economic Zone, South Africa, with capacity to process 100,000 metric tons annually by 2030.

- April 2025: The United States has implemented new trade measures, imposing a 30% tariff on South African citrus imports. This policy change has significantly increased export costs for South African producers, reducing their ability to compete effectively in the United States market.

- April 2024: South Africa escalated a dispute at the World Trade Organization against European Union citrus import rules, citing stricter cold-treatment requirements for pests such as false codling moth. These measures increase compliance costs and reduce export competitiveness, affecting citrus trade dynamics in the Africa lime market.

Africa Lime Market Report Scope

Lime, a small green citrus fruit from the species (Citrus aurantifolia), is recognized for its sour taste and high vitamin C content. It is extensively utilized in food, beverages, and traditional remedies. Additionally, lime possesses natural antimicrobial and preservative properties. The Africa lime market report includes production analysis (area harvested, yield, and volume), consumption analysis (value and volume), import analysis (value and volume), export analysis (value and volume), wholesale price trend analysis and forecast, regulatory framework, list of key players, logistics and infrastructure, and seasonality analysis. The market is segmented by country (South Africa, Egypt, Sudan, Algeria, Tunisia, and the Rest of Africa). The market forecasts are provided in terms of value (USD) and volume (metric tons).

By Geography

| Africa | South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Egypt | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Sudan | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Algeria | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Tunisia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Rest of Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| By Geography | Africa | South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Egypt | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Sudan | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Algeria | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Tunisia | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Rest of Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

What is the projected value of the Africa Lime market by 2031?

The Africa Lime market size is forecast to reach USD 296.4 million by 2031, expanding at a 6.1% CAGR from 2026 to 2031.

Which country currently holds the largest Africa Lime market share?

South Africa led with the largest 32.0% of the Africa Lime market share in 2025.

Which geography is projected to be the fastest growing through 2031?

Egypt market size is projected to grow at the fastest 7.8% CAGR from 2026 to 2031.

How are carbon credits influencing lime orchard expansion?

Programs such as the Kenya Agricultural Carbon Project pay up to USD 177 per metric tons of sequestered carbon, covering roughly 40% of orchard establishment costs and accelerating plantings in East Africa.

Page last updated on: