Africa Peas Market Analysis by ���ϲ�����

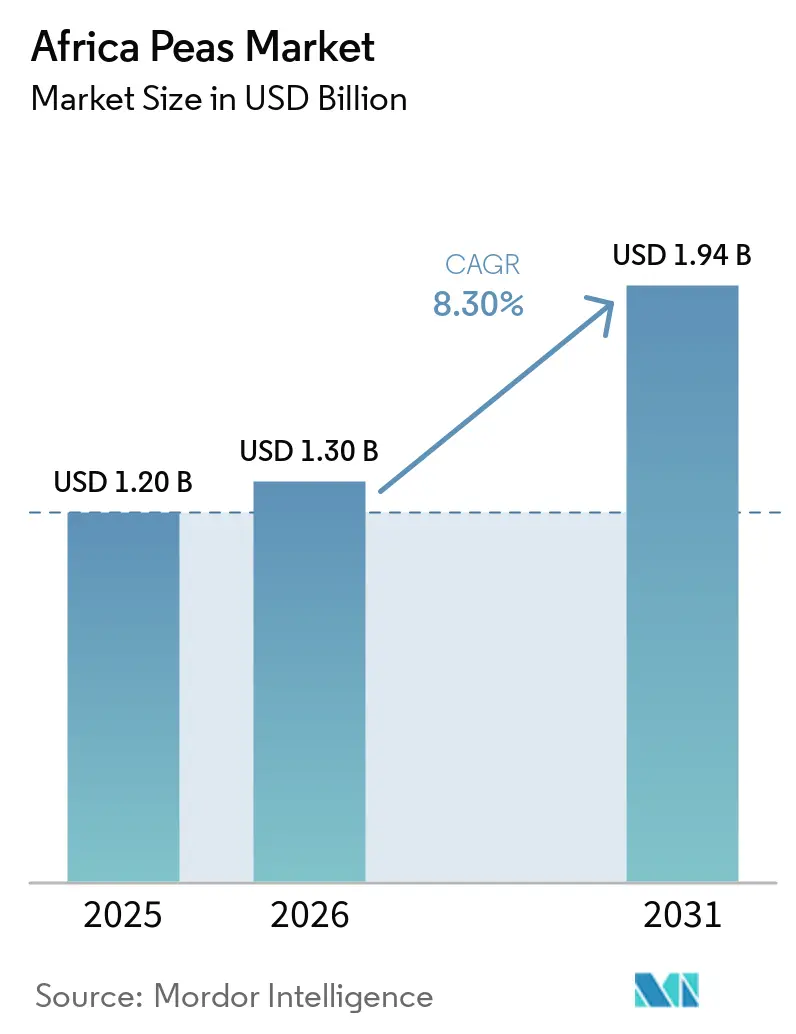

The Africa peas market size is projected to grow from USD 1.20 billion in 2025 to USD 1.30 billion in 2026 and is projected to reach USD 1.94 billion by 2031, registering a CAGR of 8.3% during 2026-2031. The growth is driven by expanding intra-African trade under the African Continental Free Trade Area, a shift from bulk exports to branded canned and ingredient formats, and the increasing adoption of ag-fintech credit products for smallholders, which are enhancing both demand and supply channels. In Kenya, field pea and green pea cultivation primarily occurs within highland mixed farming systems, where legumes like peas are combined with cereals to enhance soil fertility and diversify farm income. According to the Food and Agriculture Organization (FAO), peas are a staple in highland farming systems across East Africa, particularly in Kenya and neighboring countries, contributing to both subsistence farming and local market supply. Furthermore, the growing demand for plant-based protein and sustainable agricultural practices is driving the use of field peas in crop rotation systems and food processing applications.

Key Report Takeaways

By geography, Ethiopia accounted for the largest 30% of Africa peas market share in 2025, and Kenya's market size is projected to grow at the fastest 5.5% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Peas Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Plant-Based Protein | +1.5% | Ethiopia, Kenya, and Tanzania | Medium term (2–4 years) |

| Government Crop-Diversification Incentives | +1.2% | Ethiopia, Kenya, and Tanzania | Short term (≤ 2 years) |

| Expansion of Pea Ingredients in Bakery and Snack Products | +0.9% | Urban Kenya | Medium term (2–4 years) |

| Adoption of Solar-Powered Micro-Irrigation | +0.8% | Ethiopia, Kenya, and Tanzania | Long term (≥ 4 years) |

| Ag-Fintech Input-Credit Platforms for Pulse Growers | +1.0% | Kenya, Nigeria, and Tanzania | Short term (≤ 2 years) |

| African Continental Free Trade Area (AfCFTA) Boosting Intra-African Pulse Trade | +1.4% | Ethiopia, Kenya, and Tanzania | Medium term (2–4 years) |

| Source: ���ϲ����� | |||

Rising Demand for Plant-Based Protein

Urban consumers in Africa are gradually adopting plant-based diets, driven by increasing awareness of nutrition, affordability, and sustainability. Pea protein is emerging as a favored choice due to its high protein content, digestibility, and suitability for processed foods like snacks and bakery products. Food manufacturers are incorporating pea protein into their formulations to address clean-label and allergen-free demands. This shift in consumption patterns is boosting domestic demand and aligning African supply with global plant-based food trends, creating more stable and diversified opportunities for pea producers.

Government Crop-Diversification Incentives

Government-supported crop diversification initiatives across Africa are promoting the inclusion of field peas in cereal-based farming systems to enhance soil fertility and support sustainable agricultural practices. These initiatives emphasize pulse-based crop rotations to reduce reliance on monocropping and strengthen climate-resilient farming systems. According to AGRA’s Agrifood Systems Transformation 2024 report, published in 2025, Eastern Africa experienced a 26% increase in pulse crop yield performance compared to the previous decade, driven by improved seed adoption and enhanced agronomic practices[1]Source: AGRA, “Africa Food Systems Report 2025,” agra.org.. The growing emphasis on diversification and improving pulse productivity is fostering expanded field pea cultivation and contributing to the long-term growth of the Africa peas market.

Expansion of Pea Ingredients in Bakery and Snack Products

The use of pea ingredients in bakery and snack products is growing across Africa, fueled by increasing demand for cost-effective, plant-based protein and clean-label formulations. Food manufacturers are utilizing pea flour and pea protein in products such as biscuits, extruded snacks, and fortified baked goods to enhance nutritional content and functional properties like binding and texture. Urbanization and evolving dietary preferences are also driving the demand for convenient, high-protein snack options. This trend is prompting local food producers to expand their product offerings, leading to consistent downstream demand for peas beyond traditional household use and bulk trade markets.

Adoption of Solar-Powered Micro-Irrigation

The adoption of solar-powered irrigation systems is enhancing pulse cultivation in water-stressed farming regions of Ethiopia and Kenya by providing reliable irrigation during dry periods. According to the International Water Management Institute’s 2025 SoLAR Phase II program update, initiatives in these countries are advancing the use of solar-powered irrigation technologies to make irrigation more affordable and promote climate-resilient agriculture for smallholder farmers[2]Source: International Water Management Institute, “Solar Energy for Agricultural Resilience (SoLAR) Phase II,” solar.iwmi.org . Improved irrigation access is contributing to more consistent pea production cycles and strengthening supply reliability in African agricultural regions.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Volatility Tied to Global Trade Swings | -1.1% | Ethiopia, Kenya, and Tanzania | Short term (≤ 2 years) |

| Limited Pest-Proof Storage Infrastructure | -0.9% | Ethiopia, Kenya, and Tanzania | Medium term (2–4 years) |

| Slow Release of Heat-Tolerant Pea Varieties | -0.7% | Semi-arid Ethiopia, Kenya, and Tanzania | Long term (≥ 4 years) |

| Land Competition from Other Faster-Maturing Crops | -0.6% | Nigeria and Northern Tanzania | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Price Volatility Tied to Global Trade Swings

Price volatility in the Africa peas market is significantly impacted by sudden changes in global trade policies and supply conditions. Export demand is heavily concentrated in a limited number of key international markets, leaving producers susceptible to abrupt tariff adjustments, import restrictions, and policy reversals. Variations in supply from major producing countries further exacerbate price instability in global markets. Due to the lack of well-established commodity exchanges and hedging mechanisms in many African regions, farmers and traders face exposure to unpredictable price fluctuations. This uncertainty hinders long-term investments in productivity-enhancing inputs and restricts producers' ability to plan consistent production cycles.

Limited Pest-Proof Storage Infrastructure

Insufficient pest-proof storage infrastructure continues to be a significant challenge for supply efficiency and quality maintenance. Smallholder farmers predominantly depend on traditional storage methods, which provide minimal protection against insect infestations, moisture accumulation, and fungal contamination. This leads to a decline in grain quality and reduces the marketable value of stored peas. To avoid storage losses, farmers frequently sell their produce immediately after harvest, when prices are at their lowest, thereby limiting their income potential. Additionally, the absence of structured warehousing and cold-chain systems undermines supply chain reliability and restricts access to higher-value processing and export markets.

Geography Analysis

Ethiopia accounted for the largest 30% of Africa peas market share in 2025. The country's highland farming systems ensure consistent output, while contract farming enhances traceability and stabilizes pricing. According to the Food and Agriculture Organization (FAO), Ethiopia produced 399,812 metric tons of dry peas in 2024, based on officially reported national statistics[3]Source: Food and Agriculture Organization (FAO), “FAOSTAT Crop Production Data – Dry Peas (Pisum sativum),” fao.org. This production supports both domestic consumption and regional trade. Kenya and Tanzania also contribute to supply through expanding pulse cultivation and the adoption of improved agronomic practices. Together, these countries form a key East African production cluster, enhancing supply stability and facilitating the integration of peas into regional food and trade systems.

Regional trade integration and infrastructure improvements are significantly influencing market dynamics across East Africa. The African Continental Free Trade Area (AfCFTA) is facilitating the cross-border movement of agricultural commodities by reducing tariff barriers and improving market access. Kenya's market size is projected to grow at the fastest 5.5% CAGR from 2026 to 2031, supported by its robust logistics network and access to ports. Meanwhile, Tanzania and Ethiopia are strengthening their domestic value chains through investments in irrigation and storage systems. These advancements collectively improve supply chain efficiency and diversify end markets for peas across the region.

Tanzania continues to play a pivotal role in regional pulse supply systems, benefiting from favorable agro-climatic conditions and established farming practices. The Southern Highlands remain a key production area where pulses are integrated into mixed cropping systems, promoting soil fertility and risk diversification for farmers. Strengthening regional trade linkages is driving a gradual shift toward intra-African markets alongside traditional export destinations. This transition fosters more stable demand patterns and reduces exposure to global trade fluctuations. Consequently, Tanzania contributes to enhancing regional supply resilience and improving overall market balance within East Africa.

Competitive Landscape

The Africa peas sector features a diverse structure, with smallholder farmers serving as the primary production base and supplying raw materials to cooperatives and regional processors. Mid-sized processing companies are increasingly focusing on branded and value-added products, such as packaged pulses and ingredient-grade flour. The involvement of agri-technology firms is enhancing access to inputs, advisory services, and financing. These advancements are strengthening connections between farmers and markets, improving productivity and traceability, and supporting the gradual formalization of the value chain in key producing countries.

Digital agriculture platforms and input financing models are becoming significant in shaping competitive dynamics. Ag-fintech companies are offering bundled services, including credit, insurance, and agronomic guidance, which enable farmers to adopt improved practices and achieve higher yields. Expanding partnerships between processors and farmer groups are ensuring consistent supply and adherence to quality standards. Additionally, investments in storage and logistics infrastructure are reducing post-harvest losses and improving price realization. These integrated approaches are enhancing efficiency and competitiveness within the regional pea value chain.

Technology integration and vertical coordination are emerging as critical factors in the competitive landscape. Companies that combine input supply, financing, processing, and market access are gaining greater control over value chains. This integrated approach enhances operational efficiency, reduces reliance on intermediaries, and enables better price realization for both producers and processors. Simultaneously, the adoption of traceability systems and quality standards is increasing to meet the demands of international and regional buyers. As competition intensifies, market participants are focusing on differentiation through value addition, branding, and supply chain reliability.

Recent Industry Developments

- April 2026: India has extended duty-free yellow pea imports until March 2027 to stabilize domestic pulse supplies and manage food inflation. This policy is anticipated to maintain export opportunities for Africa pea-producing countries by supporting global demand for yellow peas in international trade markets.

- June 2025: Export Trading Group (ETG) partnered with the International Finance Corporation (IFC) to enhance smallholder farming capabilities across Africa. The collaboration focused on pulse crops, including peas, through initiatives such as productivity improvement programs and farmer training measures to boost regional agricultural trade and market access.

- September 2024: The Alliance for a Green Revolution in Africa (AGRA) organized a cross-border pulses trade forum in Nairobi, which facilitated USD 12.8 million in trade agreements between Ethiopia and Kenya. This initiative supported the expansion of regional trade for pulse crops, such as peas, and strengthened the integration of Africa's pulse supply chain.

Africa Peas Market Report Scope

Peas are small, spherical edible seeds from the plant, which belongs to the legume family and is widely cultivated for food. They are used in fresh, frozen, and processed foods; plant-based protein products; animal feed; and soil enrichment through nitrogen fixation in agriculture.

The Africa Peas Market Report includes production analysis by volume, consumption analysis by value and volume, import analysis by value and volume, export analysis by value and volume, wholesale price trend analysis and forecast, regulatory framework analysis, key player analysis, logistics and infrastructure analysis, and seasonality analysis. The market is segmented by country, including Ethiopia, Kenya, South Africa, and Tanzania. The market forecasts are provided in terms of value (USD) and volume (metric tons).

By Geography

| Africa | Ethiopia | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Kenya | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Tanzania | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| By Geography | Africa | Ethiopia | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Kenya | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Tanzania | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

What is the forecast value of the Africa pea market by 2031?

The Africa pea market is projected to reach USD 1.94 billion by 2031.

Which country held the largest share of the Africa pea market in 2025?

Ethiopia led with the largest 30% market share in 2025.

Which geography is projected to record the fastest growth through 2031?

Kenya is projected to register the fastest CAGR of 5.5% during 2026-2031.

What portion of the Africa pea market does Ethiopia contribute in 2025?

Ethiopia held the largest 30% of the Africa pea market share in 2025.

Page last updated on: