Market Overview

| Study Period | 2021 - 2031 |

|---|---|

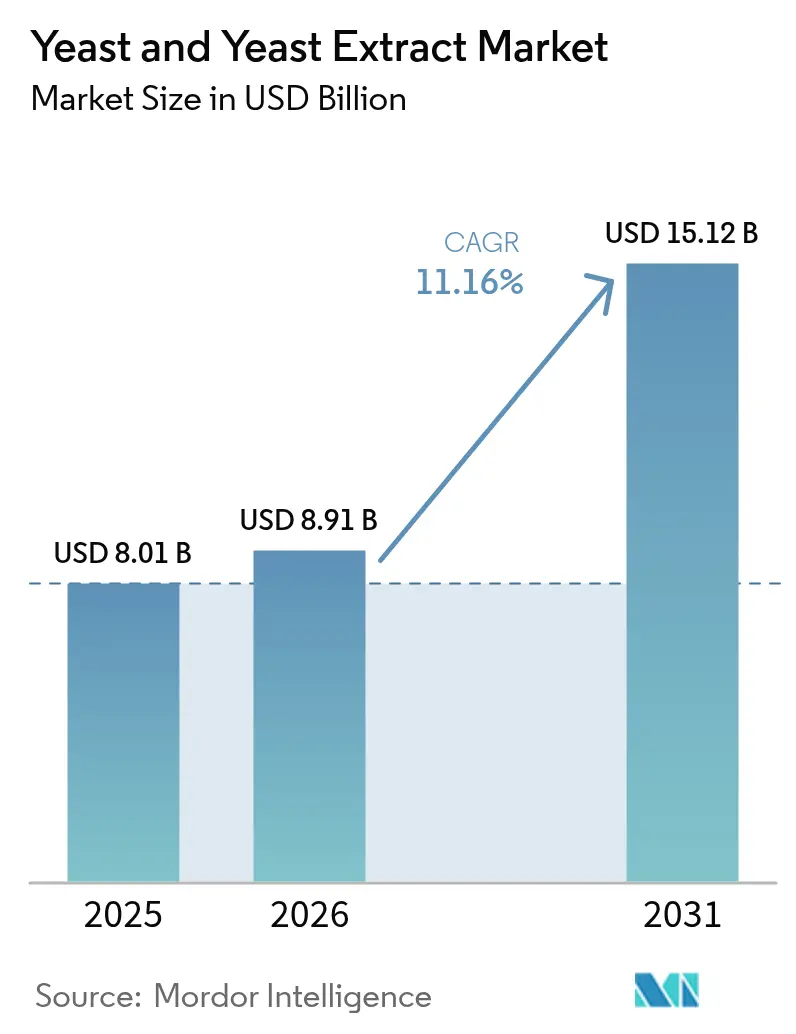

| Market Size (2026) | USD 8.91 Billion |

| Market Size (2031) | USD 15.12 Billion |

| Growth Rate (2026 - 2031) | 11.16% CAGR |

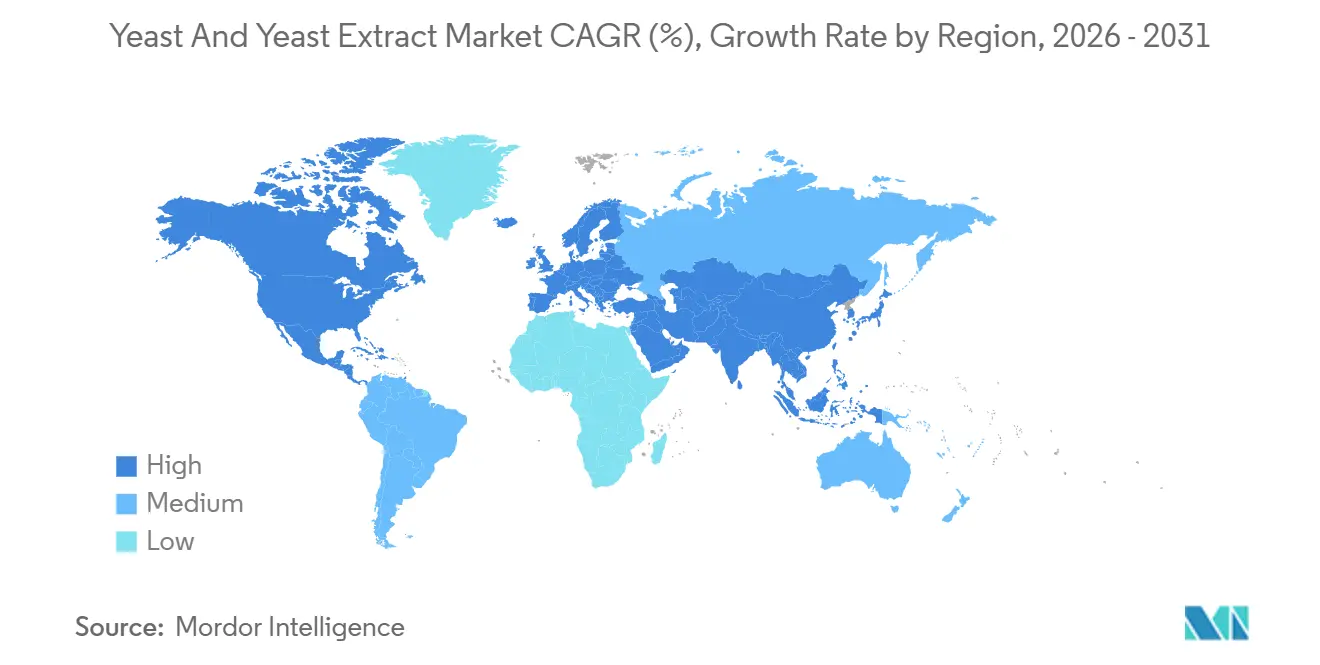

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

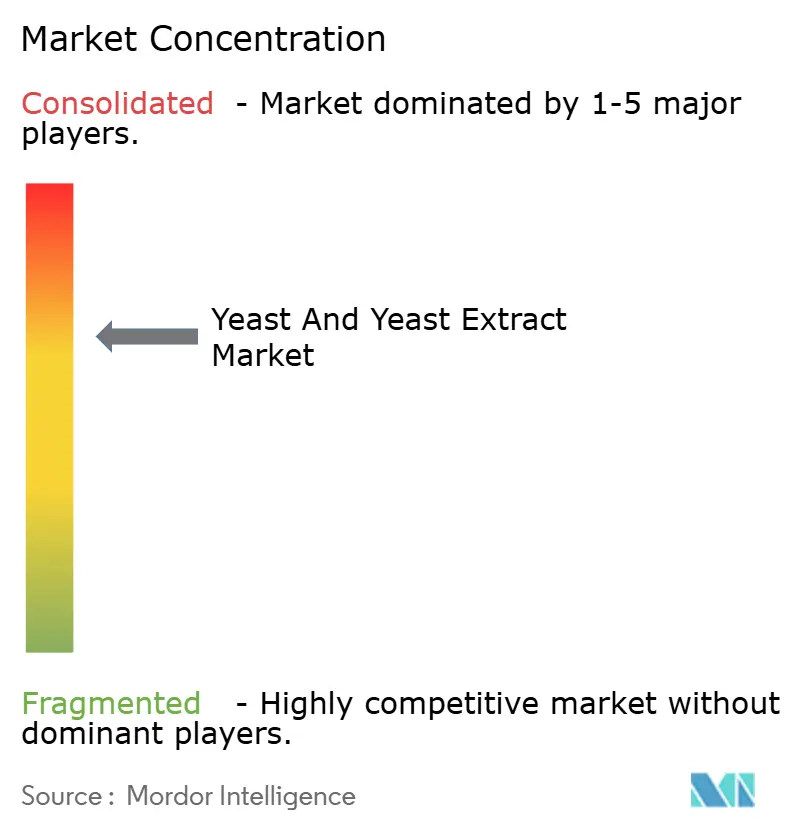

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Yeast And Yeast Extract Market Analysis by ���ϲ�����

The yeast and yeast extracts market size in 2026 is estimated at USD 8.91 billion, growing from the 2025 value of USD 8.01 billion, with 2031 projections showing USD 15.12 billion, growing at 11.16% CAGR over 2026-2031. Clean-label reformulation, antibiotic-free livestock production, and bioethanol capacity additions are synchronizing to expand total addressable demand, while premium applications such as artisan bakery and precision-fermented nutraceuticals strengthen margins. Baker’s yeast retained the largest volume share in 2025 and continues to anchor industrial bread lines across Asia-Pacific, even as probiotic and nutritional strains outpace the broader yeast and yeast extract market on the strength of gut-health positioning. Europe supplied over one-third of 2025 revenue, yet Asia-Pacific remains the fastest-growing geography as China and India scale biofuel mandates and modernize refrigerated distribution. Competitive intensity sits at the upper-mid range, with three global leaders controlling roughly half of installed capacity but dozens of agile specialists filling white-space niches in organic, non-GMO, and designer strains.

Key Report Takeaways

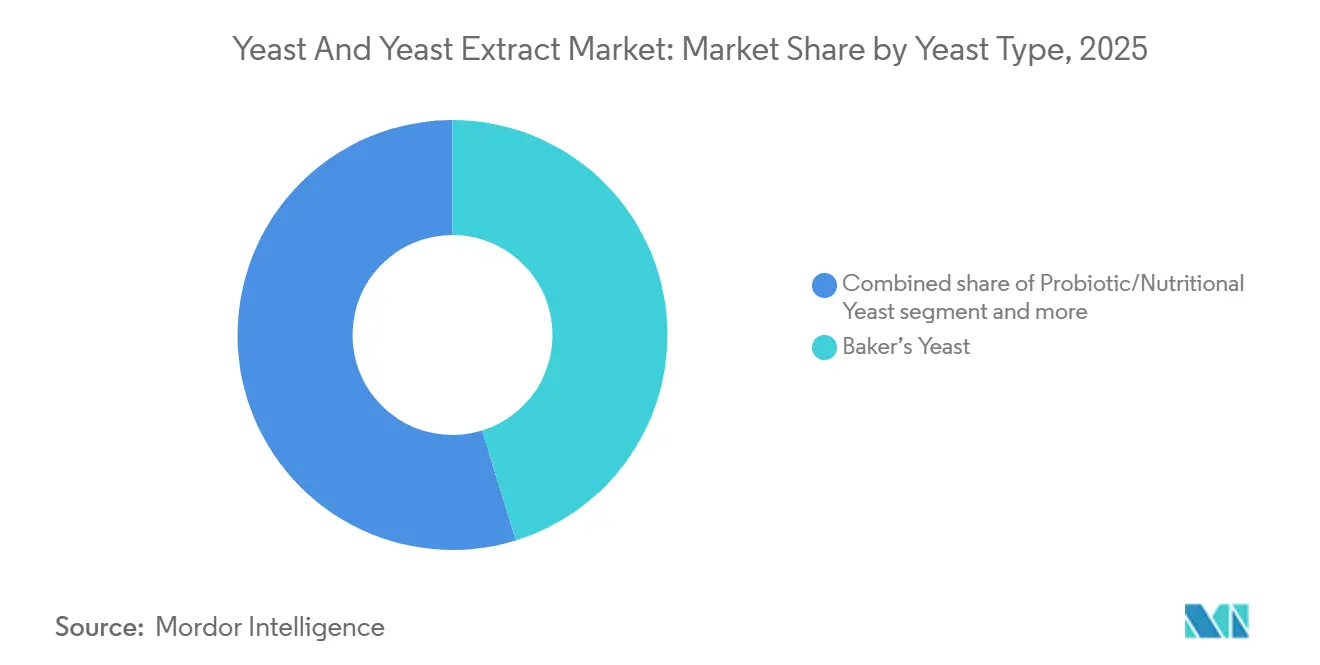

- By yeast type, baker’s yeast commanded 45.23% of 2025 volume, whereas probiotic/nutritional yeast is forecast to grow at 13.49% CAGR from 2026 to 2031.

- By product, autolyzed extracts captured 62.59% of 2025 revenue; hydrolyzed extracts are projected to expand at 12.87% CAGR through 2031.

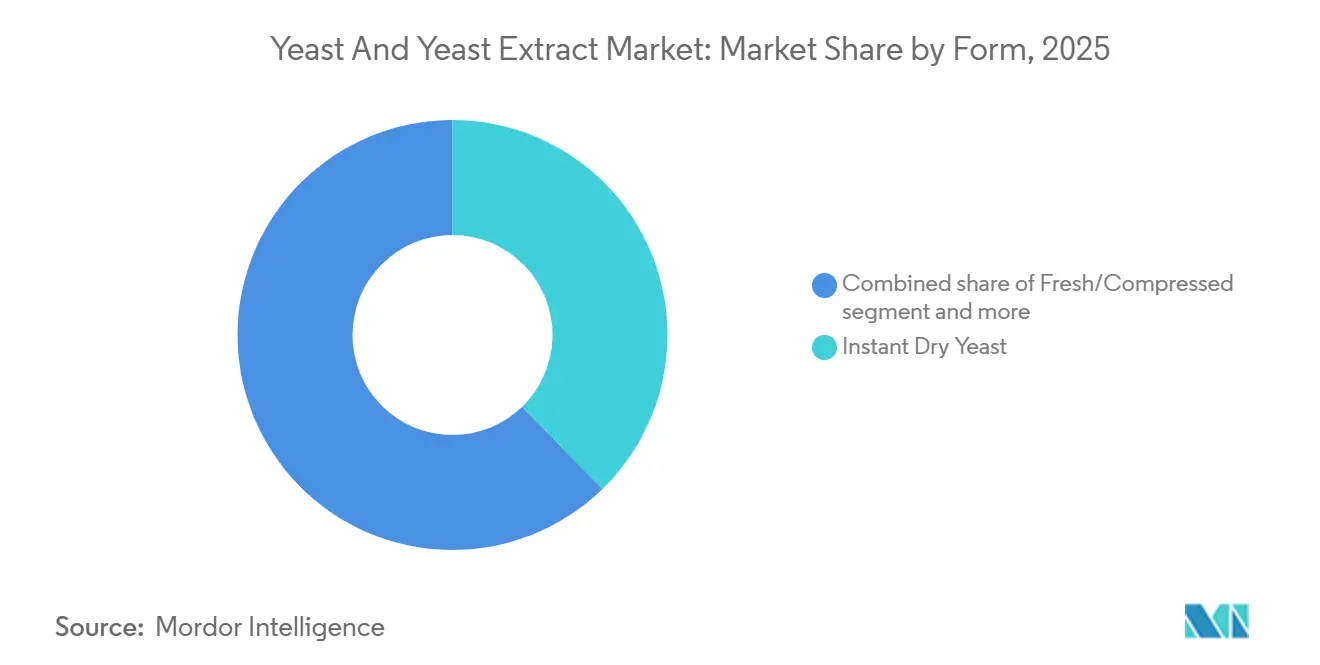

- By form, instant dry yeast led with 37.71% of 2025 sales, while fresh yeast is set to grow at 13.72% CAGR over the forecast horizon.

- By source, conventional supply represented 78.13% in 2025, yet organic and free-form strains are advancing at 14.35% CAGR.

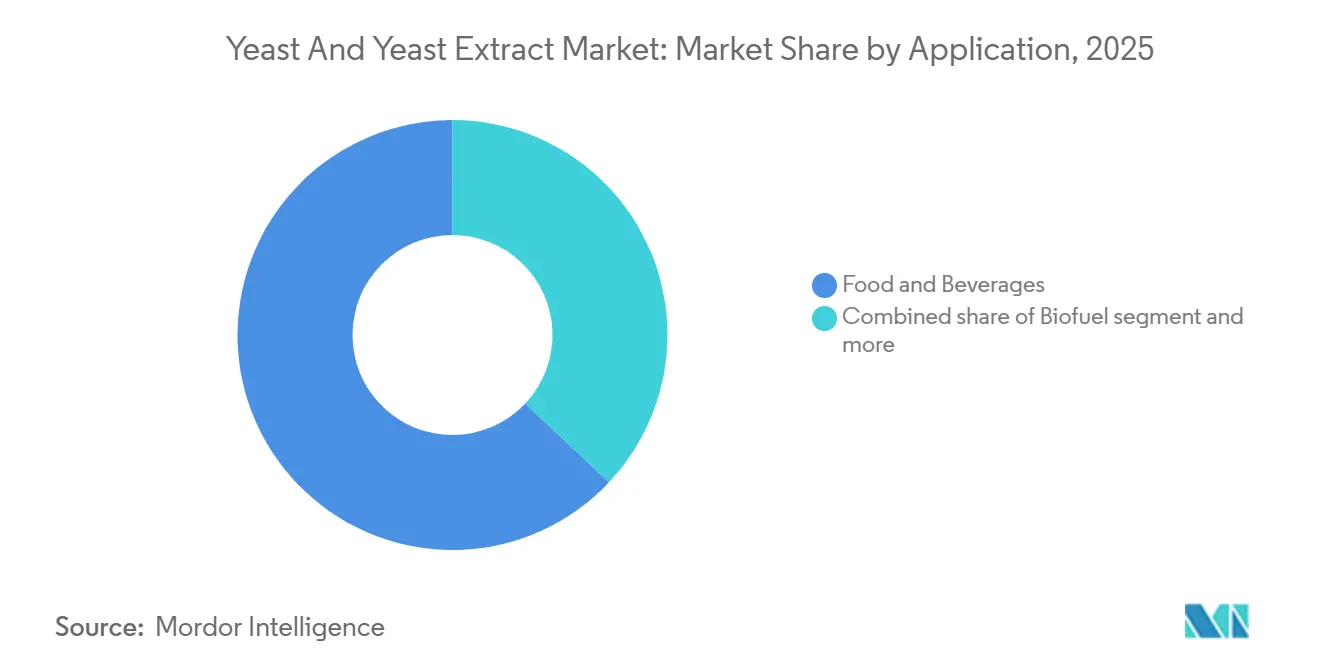

- By application, food and beverages accounted for 62.98% of 2025 demand, whereas biofuel use is accelerating at 15.22% CAGR.

- By geography, Europe held 35.65% of 2025 revenue, but Asia-Pacific is poised to grow at 12.83% CAGR on rising bakery consumption and ethanol blending targets.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Yeast And Yeast Extract Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in bakery and fermented food consumption | +1.8% | Global, with concentration in Asia-Pacific (China, India) and Europe (Germany, France) | Medium term (2-4 years) |

| Expansion of craft brewing and alcoholic beverages | +1.5% | North America (United States, Canada) and Europe (Germany, United Kingdom, Belgium) | Short term (≤ 2 years) |

| Clean-label and natural-ingredient momentum | +2.1% | Global, with early adoption in North America and Europe, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Adoption of yeast as an antibiotic-free feed additive | +1.6% | Global, with core demand in Asia-Pacific (China, Thailand, Indonesia) and North America | Medium term (2-4 years) |

| Rising demand for bioethanol and biofuel production | +2.3% | Brazil, United States, China, India; emerging in Southeast Asia and Middle East | Long term (≥ 4 years) |

| Precision-fermentation–enabled designer strains | +1.9% | North America and Europe (research and development hubs), scaling to Asia-Pacific manufacturing | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Growth in bakery and fermented food consumption

Bakery and fermented food consumption is expanding at an accelerated pace, particularly in the Asia-Pacific region, where urbanization and rising disposable incomes are driving demand for packaged bread, buns, and traditional fermented products. China's annual per capita consumption of baked foods stands at a modest 7-8 kg. This highlights a significant growth potential for China's baked food market[1]Source: United States Department of Agriculture, "China: Food Processing Ingredients Annual, 2025" usda.gov. India's bakery sector is witnessing similar momentum, with organized retail chains launching fresh-baked bread lines that require consistent yeast performance and extended shelf life. Europe's artisan bakery revival is creating parallel demand for specialty yeast strains that deliver complex flavor profiles and slower fermentation cycles, a trend particularly pronounced in France and Germany, where sourdough and heritage grain breads command premium pricing. The popularity of kimchi, kombucha, and kefir likewise amplifies demand for yeast extracts as clean-label flavor enhancers.

Expansion of craft brewing and alcoholic beverages

Craft brewing's resurgence is reshaping yeast demand dynamics, with microbreweries and regional brewers prioritizing proprietary strains that differentiate flavor, aroma, and mouthfeel. The United States craft beer segment grew in volume during 2025, driven by consumer preference for locally sourced ingredients and experimental hop-yeast pairings. In 2025, the United States boasted a total of 9,778 operational small and independent breweries[2]Source: Brewers Association, "Brewers Association Reports 2025 U.S. Craft Brewing Industry Figures," brewersassociation.org . Germany's craft brewing sector expanded, supported by relaxed licensing regulations and the entry of younger brewers experimenting with Belgian and American yeast strains traditionally absent from German lagers. The United Kingdom's ale revival and Belgium's continued dominance in specialty fermentation are sustaining demand for brewer's yeast, while wine producers in France, Italy, and Spain are adopting commercial yeast strains to ensure fermentation consistency amid climate-induced vintage variability.

Clean-label and natural-ingredient momentum

Clean-label mandates are compelling food manufacturers to replace synthetic additives with yeast extracts that deliver umami, texture, and shelf stability. The 2024 revision of EU Regulation 1333/2008 tightened disclosure for flavor modifiers, pushing food processors to swap synthetic enhancers for autolyzed yeast extracts. Asia-Pacific markets are following suit, with Japan's Ministry of Health, Labour and Welfare proposing stricter labeling for fermentation-derived ingredients in 2025, a move that favors yeast extracts over chemically synthesized alternatives. The International Food Information Council's 2024 Food and Health Survey reveals that 26% of U.S. respondents consider "natural" as the primary indicator of healthy food, indicating growing wariness toward synthetic additives[3]Source: IFIC, "2024 IFIC Food & Health Survey," ific.org . This shift has increased the use of yeast extracts as replacements for artificial flavor enhancers, particularly in savory applications, helping food manufacturers meet both regulatory requirements and consumer preferences for natural ingredients.

Adoption of yeast as an antibiotic-free feed additive

Livestock producers are integrating yeast-based feed additives to replace growth-promoting antibiotics, driven by regulatory bans and consumer backlash against antimicrobial resistance. China's Ministry of Agriculture and Rural Affairs prohibited the use of colistin and other medically important antibiotics in animal feed starting January 2025, prompting poultry and swine producers to adopt Saccharomyces cerevisiae-based probiotics that enhance gut health and nutrient absorption. Similar policies in the EU aquaculture sector and North American poultry supply chains drive volume gains, with documented 4%-6% feed-conversion improvements supporting on-farm economics. Thailand and Indonesia's shrimp farming sectors are piloting yeast-based immunostimulants to reduce white spot syndrome mortality, a development that could unlock significant volume if efficacy is validated at a commercial scale. This driver is projected to add 1.6 percentage points to the CAGR, with medium-term impact as producers complete transition cycles and regulatory frameworks harmonize across regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile molasses and sugar feedstock prices | -0.8% | Global, with acute impact in Brazil, India, Thailand (cane-sugar producers) | Short term (≤ 2 years) |

| Stringent GMO and food-safety regulations | -0.6% | Europe (EU regulations), North America (FDA, USDA), Asia-Pacific (China, Japan) | Medium term (2-4 years) |

| Cold-chain energy intensity for fresh yeast | -0.5% | Asia-Pacific, Middle East, Africa (grid reliability challenges) | Medium term (2-4 years) |

| Substitution risk from next-gen microbial proteins | -0.4% | North America and Europe (venture capital concentration), early spillover to Asia-Pacific | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Fluctuating raw material prices

Molasses and cane-sugar prices surged 18% during the first half of 2025, driven by drought conditions in Brazil's Center-South region and India's decision to restrict sugar exports to stabilize domestic food inflation. This volatility directly pressures yeast producers, as molasses typically accounts for 25% to 35% of variable production costs, and long-term supply contracts are scarce in regions where smallholder cane farmers dominate. Brazil's 2025 ethanol mandate increases diverted additional cane tonnage away from sugar refining, tightening molasses availability and forcing yeast manufacturers to either absorb margin compression or pass costs downstream to bakery and brewing customers. Producers without vertical integration into cane processing or diversified feedstock portfolios such as beet molasses or corn steep liquor are particularly exposed. This restraint is estimated to subtract 0.8 percentage points from the CAGR, with the short-term impact concentrated in cane-dependent geographies.

Stringent GMO and food-safety regulations

Regulatory scrutiny of genetically modified yeast strains is intensifying, particularly in jurisdictions where gene-editing techniques occupy a legal gray zone. The European Union's Court of Justice reaffirmed in 2024 that CRISPR-edited organisms fall under Directive 2001/18/EC, requiring full GMO authorization and labeling even when no foreign DNA is introduced. This interpretation has delayed the commercialization of precision-fermented yeast strains engineered for enhanced bioethanol yield or probiotic efficacy, as developers face multi-year approval timelines and public consultation requirements. China's National Health Commission tightened safety assessment protocols for fermentation-derived ingredients in 2025, mandating toxicological studies and allergenicity testing. These regulatory barriers favor incumbents with established strain libraries and in-house regulatory affairs teams, while constraining innovation from smaller biotech entrants.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Yeast Type: Probiotic Innovation Drives Transformation

Baker's yeast captured 45.23% of market share in 2025, underpinned by its indispensable role in bread, buns, and pastry fermentation across industrial and artisan bakeries. Europe's consumption is concentrated, where per-capita bread intake exceeds 50 kilograms annually. Asia-Pacific's baker's yeast demand is accelerating as China's urban middle class adopts Western-style breakfast routines and India's organized retail sector expands fresh-baked bread offerings, with both markets favoring instant dry formats for ease of handling and extended shelf life. North America's industrial bakeries continue to dominate volume, that require consistent yeast performance and minimal batch-to-batch variability.

Probiotic and nutritional yeast are expanding at 13.49% CAGR from 2026 to 2031, propelled by consumer prioritization of gut health, immune support, and plant-based protein fortification. North America leads adoption with probiotic yeast strains gaining traction in dietary supplements targeting digestive wellness. Asia-Pacific's probiotic yeast market is nascent but growing, with Japan and South Korea incorporating yeast-based supplements into functional food portfolios and China's e-commerce platforms driving direct-to-consumer sales of imported nutritional yeast products.

By Product: Autolyzed Extracts Dominate Savory, Hydrolyzed Variants Gain in Meat Alternatives

In 2025, autolyzed yeast extracts held a 62.59% share of product revenue, highlighting their critical role in savory seasonings, bouillon cubes, soups, and sauces. These extracts enhance umami flavor and reduce salt without triggering allergen labeling. Europe's food processing sector is the largest consumer, using autolyzed extracts in ready meals and snack coatings to meet clean-label requirements and improve flavor cost-effectively. In Asia-Pacific, instant noodle and soup manufacturers, especially in China and Indonesia, are replacing monosodium glutamate with autolyzed extracts due to health concerns and regulatory pressures. North America's snack food industry incorporates autolyzed extracts in potato chip seasonings and popcorn flavorings to boost savory notes and mask off-flavors in reduced-sodium products.

Hydrolyzed yeast extracts are projected to grow at a 12.87% CAGR from 2026 to 2031, driven by their superior solubility and flavor intensity in meat alternatives, plant-based broths, and premium sauces. The hydrolysis process, which breaks down yeast proteins into smaller peptides and free amino acids, enhances the umami profile, making it valuable in plant-based burger patties and sausages to replicate meat's savoriness. In North America, the meat-alternative sector, led by brands like Beyond Meat and Impossible Foods, increasingly uses hydrolyzed yeast extracts to improve mouthfeel and flavor complexity, targeting flexitarians seeking taste parity with traditional meat.

By Form: Instant Dry Yeast Leads Industrial Bakery, Fresh Yeast Gains in Artisan Channels

In 2025, instant dry yeast accounted for 37.71% of form-based sales, favored by industrial bakeries for its shelf stability, seamless integration into automated mixing systems, and reliable fermentation across various doughs. Large-scale bread producers in North America turn to instant dry yeast to simplify handling and cut down on cold-storage needs. With a 12-month ambient shelf life, this yeast format allows for centralized purchasing and bulk inventory management. Similarly, industrial bakeries in Europe prefer instant dry yeast for producing sandwich bread, burger buns, and pizza dough, where consistent fermentation and minimal batch variability are essential for smooth production schedules.

Fresh yeast is growing at a 13.72% CAGR from 2026 to 2031, driven by artisan bakeries' preference for its consistent fermentation and the rich flavors it brings to sourdough, baguettes, and heritage grain breads. Europe's artisan bakery revival, particularly in France, Germany, and Italy, is boosting fresh yeast demand as bakers adopt traditional fermentation methods for open crumb structures and distinct flavors. North America's premium bread market is following suit, with urban bakeries and farmers' market vendors using fresh yeast fermentation and longer proofing times to enhance digestibility and shelf life. In Asia-Pacific, cold-chain challenges limit fresh yeast growth, but urban areas with improving refrigerated distribution networks are seeing expansion.

By Source: Organic Certification Drives Premium Growth

In 2025, conventional yeast accounted for 78.13% of the market, driven by its cost efficiency and scalability. Industrial bakeries, large-scale breweries, and bioethanol producers prefer conventional yeast due to its lower cost compared to organic alternatives and its reliable supply chain. In the Asia-Pacific region, producers like China's Angel Yeast and India's regional manufacturers focus on high-volume strategies for price-sensitive markets. Europe’s conventional yeast supply is concentrated in France, Germany, and the Netherlands, leveraging proximity to sugar beet processing and fermentation infrastructure. In North America, companies like AB Mauri and Lallemand serve industrial clients prioritizing consistency and availability.

From 2026 to 2031, the free-form/rganic yeast market is expected to grow at a 14.35% CAGR, driven by non-GMO certification mandates and clean-label requirements in North America and Europe. In 2025, the Non-GMO Project verified 38 new yeast products, reflecting consumer demand for transparency. Regulation (EU) 2018/848 supports Europe’s organic yeast market by mandating certification for organic bread and beer, creating a less price-sensitive demand base. In North America, brands like Dave's Killer Bread and Alvarado Street Bakery use organic yeast to maintain certification and appeal to health-conscious consumers willing to pay premiums. Asia-Pacific’s organic yeast market is emerging, led by Japan and Australia, while China faces challenges with fragmented certification and inconsistent enforcement.

By Application: Biofuel Surge Reshapes Demand Patterns

In 2025, food and beverages dominated applications, accounting for 62.98%. This included bakery, beverages, meat alternatives, soups, sauces, snacks, and noodles, leveraging yeast's fermentation, flavor-enhancement, and nutritional benefits. Bakery applications led the major share of the food and beverage volume, driven by bread, buns, pastries, and pizza dough. Meat and meat alternatives are growing rapidly, with yeast extracts enhancing umami and texture in plant-based products for flexitarian consumers. Snacks and noodles, especially in Asia-Pacific's instant noodle markets, utilized yeast extracts in seasonings and coatings for savory depth and monosodium glutamate replacement.

Biofuel applications are growing at a 15.22% CAGR from 2026 to 2031, driven by ethanol-blending mandates in Brazil, the United States., China, and India. Brazil's RenovaBio program promotes second-generation ethanol from sugarcane bagasse and lignocellulosic feedstocks, increasing demand for robust yeast strains. China's E10 ethanol mandate, requiring 10% ethanol blending in gasoline, is driving capacity expansions in key provinces, with state-owned enterprises partnering with yeast suppliers. India's ethanol-blending program targets 20% blending by 2025, pushing sugar mills to install distillation units and procure yeast strains for molasses and sugarcane juice.

Geography Analysis

Europe held 35.65% of the global market share in 2025, driven by Germany's industrial bakery sector, France's artisan bread tradition, and the Netherlands' role as a yeast production and export hub. Germany's high per-capita bread consumption sustains demand for baker's yeast, while its craft brewing sector boosts specialty brewer's yeast sales. France's regulations supporting natural fermentation aids promote autolyzed yeast extract adoption in clean-label bakery formulations. The United Kingdom’s plant-based food sector integrates hydrolyzed yeast extracts into meat alternatives and vegan ready meals. Europe's yeast production benefits from proximity to sugar beet processing and fermentation expertise, ensuring cost competitiveness and adaptability to customer needs.

Asia-Pacific is projected to grow at a 12.83% CAGR from 2026 to 2031, driven by bioethanol capacity expansions in China and India, rising bakery consumption, and improved cold-chain infrastructure enabling fresh yeast distribution. China's E10 ethanol mandate boosts yeast demand in key provinces, while urban bakery growth aligns with changing consumer habits. India's ethanol-blending program and organized retail bakeries create demand for bioethanol and baker's yeast, supported by cold-chain investments. Japan's mature probiotic yeast market targets aging consumers, while South Korea's premium bread chains adopt fresh yeast for artisanal differentiation. Australia's craft brewing sector sustains demand for specialty brewer's yeast. Regional growth depends on infrastructure investment, regulatory harmonization, and feedstock price stability.

North America also accounted for a good share of global revenue in 2025, led by the United States' bioethanol production, Canada's bakery sector, and Mexico's tortilla and bread markets. The United States Renewable Fuel Standard drives bioethanol yeast demand, while its craft brewing sector supports specialty brewer's yeast sales. Canada's industrial bakeries prefer instant dry yeast for its stability, while organic bakeries adopt USDA Organic-certified yeast. Mexico's tortilla industry modernizes production and incorporates yeast extracts for flavor and texture enhancement. The Middle East and Africa account for 8% to 10% of revenue, with regional hubs in the United Arab Emirates, Saudi Arabia, and Turkey supporting bakery and brewing applications, while South Africa and Nigeria's bakery sectors favor instant dry yeast due to cold-chain limitations.

Competitive Landscape

The yeast and yeast extract market reflects a consolidated core where Lesaffre Group, Angel Yeast Co Ltd, and Lallemand Inc. control approximately major share of global production capacity and command fermentation intellectual property that spans strain development, bioprocess optimization, and application-specific formulations. Angel Yeast's collaboration with a Chinese animal-nutrition conglomerate is extending its reach into antibiotic-free feed additives, a segment where margin profiles exceed traditional bakery applications by 8 to 12 percentage points, while Lallemand's investment in probiotic yeast research is targeting pharmaceutical and nutraceutical channels that value clinical validation and regulatory dossiers.

Associated British Foods' AB Mauri division and Kerry Group plc are leveraging their global distribution networks and technical service capabilities to lock in industrial bakery and food processing customers, offering formulation support and fermentation troubleshooting that smaller regional producers cannot replicate at scale. White-space opportunities are emerging in precision-fermented designer strains that deliver enhanced bioethanol yield, targeted probiotic benefits, or novel flavor compounds, with venture-backed entrants such as Ginkgo Bioworks and Zymergen exploring yeast engineering for applications beyond traditional food and fuel.

However, the capital intensity of scaling fermentation infrastructure estimated at USD 50 million to USD 100 million per facility and the multi-year timelines required to secure regulatory approvals are tempering near-term disruption risks and favoring incumbents with established production footprints and regulatory affairs expertise. Smaller players are carving niche positions in organic and non-GMO certified yeast, regional specialty strains for artisan bakeries and craft breweries, and application-specific formulations for plant-based meat alternatives, segments where customer intimacy and rapid formulation iteration confer competitive advantages over scale-driven cost leadership.

Yeast And Yeast Extract Industry Leaders

-

Associated British Foods plc

-

Lesaffre Group

-

Angel Yeast Co Ltd

-

Lallemand Inc.

-

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Lesaffre acquired a bioethanol yeast facility in Brazil namely Zilor. This resulted in the establishment of a joint venture combining the complementary expertise of Biospringer by Lesaffre and Biorigin to provide improved yeast derivatives and savory ingredient solutions for the food and feed markets.

- June 2025: MicroBioGen, an Australian yeast biotechnology company, and Lesaffre entered into licensing and collaboration agreement to develop yeast solutions for the baking, food, and biochemicals markets. This partnership combines MicroBioGen's yeast strain platform and 20-year genetic library with Lesaffre's bioengineering expertise.

- December 2024: Lesaffre acquired DSM-Firmenich's yeast extract business, integrating its sales organization, processing technologies, and 46 employees into Lesaffre's Biospringer division. This acquisition aligns with Lesaffre's objective to enhance its position as a global leader in yeast extracts and derivatives within the savory ingredients market.

Global Yeast And Yeast Extract Market Report Scope

Yeast can be described as a microscopic fungus that consists of specific oval cells that reproduce by budding and are proficient in converting sugar into carbon dioxide and alcohol. Yeast extracts are the cell culture of yeast that is being utilized as a flavoring agent and a food additive. By Yeast Type, the market is segmented into baker’s yeast, brewer’s yeast, distiller’s and wine yeast, bioethanol yeast, probiotic/nutritional yeast, and others. By Product, the market is segmented into autolyzed and hydrolyzed. By Form, the market is segmented into fresh/compressed, active dry, instant dry, and others. By Source, the market is segmented into conventional and free-form/organic. By Application, the market is segmented into food and beverages, animal feed and pet food, biofuel, pharmaceuticals, dietary supplements, and other applications. The food and beverage category is further bifurcated into bakery, beverages, meat and meat alternatives, soups, sauces, and bouillons, snacks and noodles, and other categories. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value (USD) and volume (Tons) for all the abovementioned segments.

By Yeast Type

| Baker's Yeast |

| Brewer's Yeast |

| Distiller's and Wine Yeast |

| Bioethanol Yeast |

| Probiotic/Nutritional Yeast |

| Others |

By Product

| Autolyzed |

| Hydrolyzed |

By Form

| Fresh/Compressed |

| Active Dry |

| Instant Dry |

| Others |

By Source

| Conventional |

| Free-form/Organic |

By Application

| Food and Beverages | Bakery |

| Beverages | |

| Meat and Meat Alternatives | |

| Soups, Sauces, and Bouillons | |

| Snacks and Noodles | |

| Others | |

| Animal Feed and Pet Food | |

| Biofuel | |

| Pharmaceuticals | |

| Dietary Supplements | |

| Other Applications |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Morocco | |

| Rest of Middle East and Africa |

| By Yeast Type | Baker's Yeast | |

| Brewer's Yeast | ||

| Distiller's and Wine Yeast | ||

| Bioethanol Yeast | ||

| Probiotic/Nutritional Yeast | ||

| Others | ||

| By Product | Autolyzed | |

| Hydrolyzed | ||

| By Form | Fresh/Compressed | |

| Active Dry | ||

| Instant Dry | ||

| Others | ||

| By Source | Conventional | |

| Free-form/Organic | ||

| By Application | Food and Beverages | Bakery |

| Beverages | ||

| Meat and Meat Alternatives | ||

| Soups, Sauces, and Bouillons | ||

| Snacks and Noodles | ||

| Others | ||

| Animal Feed and Pet Food | ||

| Biofuel | ||

| Pharmaceuticals | ||

| Dietary Supplements | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the yeast market?

The yeast market is valued at USD 8.91 billion in 2026 and is projected to reach USD 15.12 billion by 2031.

Which region leads the yeast market?

Europe holds the largest share at 35.65% in 2025, driven by bakery, brewing, and stringent clean-label regulations.

What application segment is growing the fastest?

Biofuel applications record the highest CAGR at 15.22% for 2026-2031 due to renewable-energy mandates.

How do biofuel policies in major economies affect yeast demand?

Ethanol mandates in Brazil, the United States, China, and India are pushing bioethanol yeast applications to a 15.22% CAGR, boosting overall volume.

Page last updated on: