Wood Fiber Insulation Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

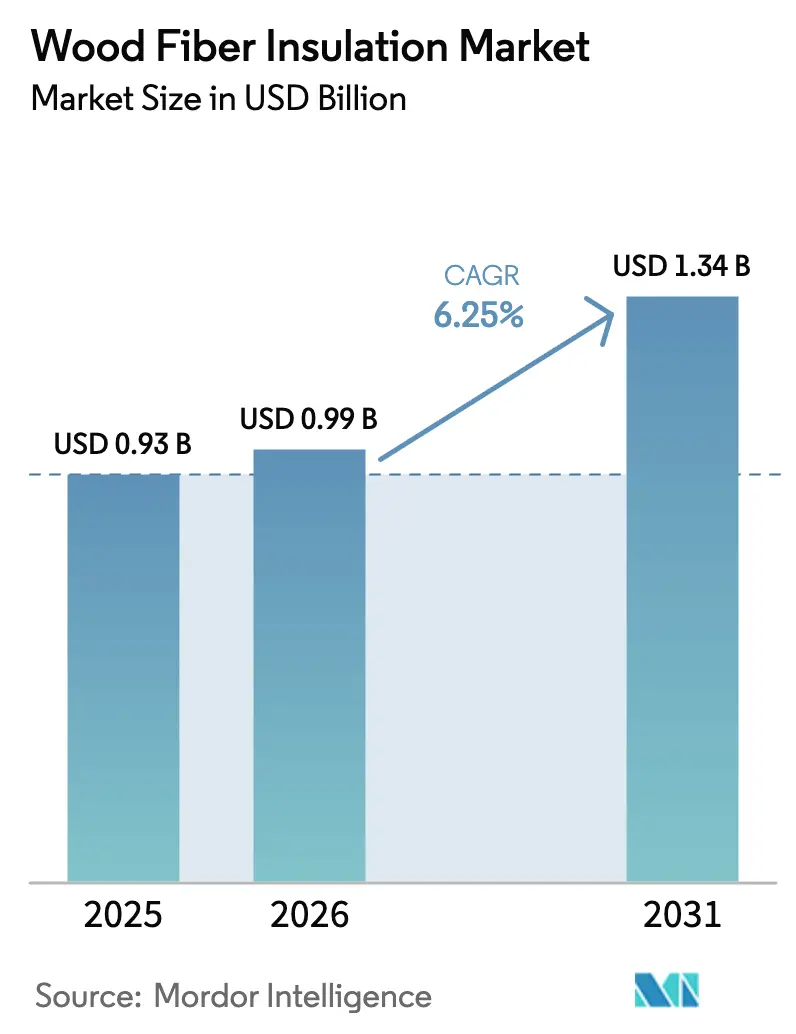

| Market Size (2026) | USD 0.99 Billion |

| Market Size (2031) | USD 1.34 Billion |

| Growth Rate (2026 - 2031) | 6.25% CAGR |

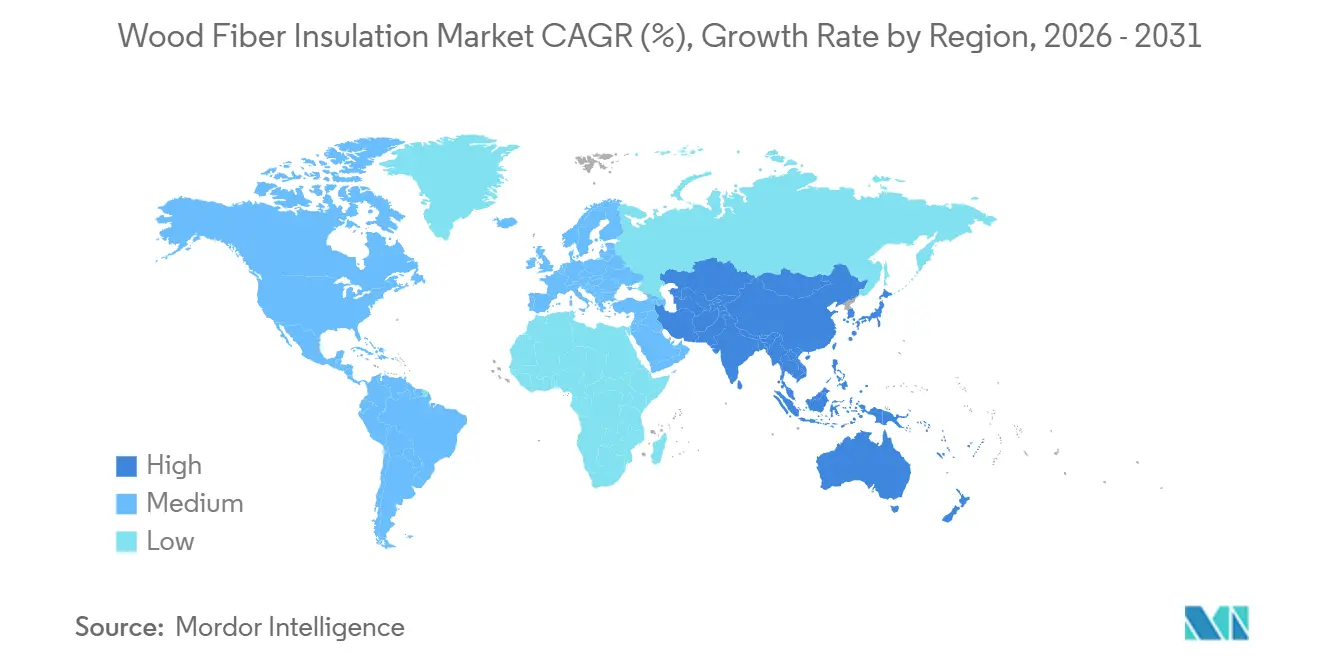

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

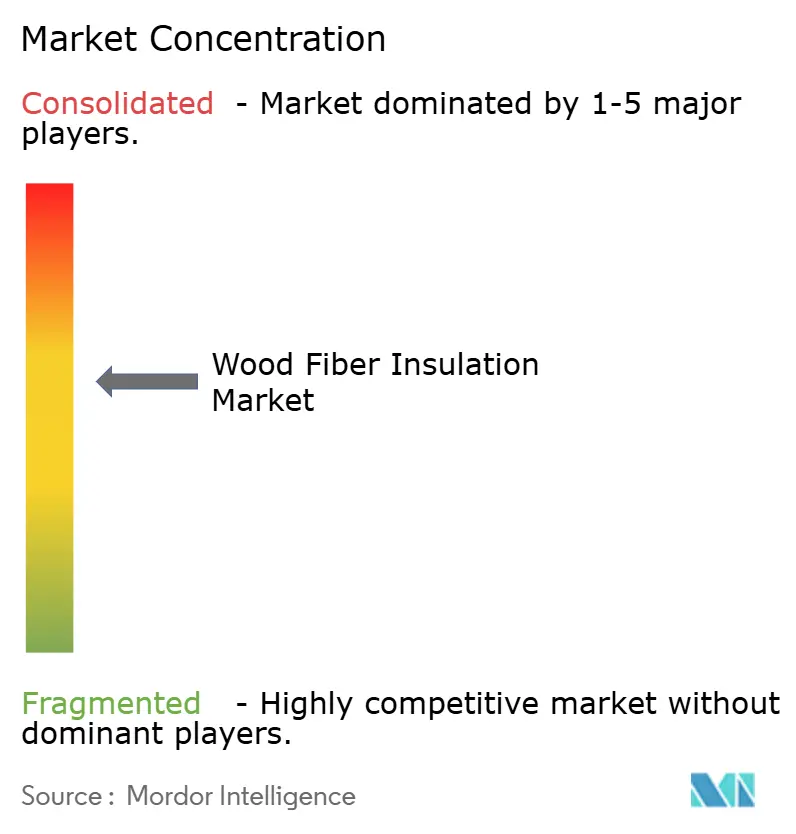

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Wood Fiber Insulation Market Analysis by ���ϲ�����

The Wood Fiber Insulation Market size is projected to be USD 0.93 billion in 2025, USD 0.99 billion in 2026, and reach USD 1.34 billion by 2031, growing at a CAGR of 6.25% from 2026 to 2031. Carbon-intensity limits written into building codes, coupled with mandatory whole-life carbon accounting in public procurement, are underpinning the expansion of the wood fiber insulation market. Retrofit subsidies in North America, notably New York’s USD 500 million allocation for envelope upgrades, are accelerating demand for vapor-open boards that mitigate thermal bridging. Europe continues to anchor volume on the back of decades-old installer training programs, yet North America is now the fastest-growing region as state and provincial incentives remove initial cost barriers. Corporate net-zero pledges are spilling into tenant-improvement specifications, lifting commercial uptake and signaling a structural shift away from petrochemical incumbents toward bio-based alternatives.

Key Report Takeaways

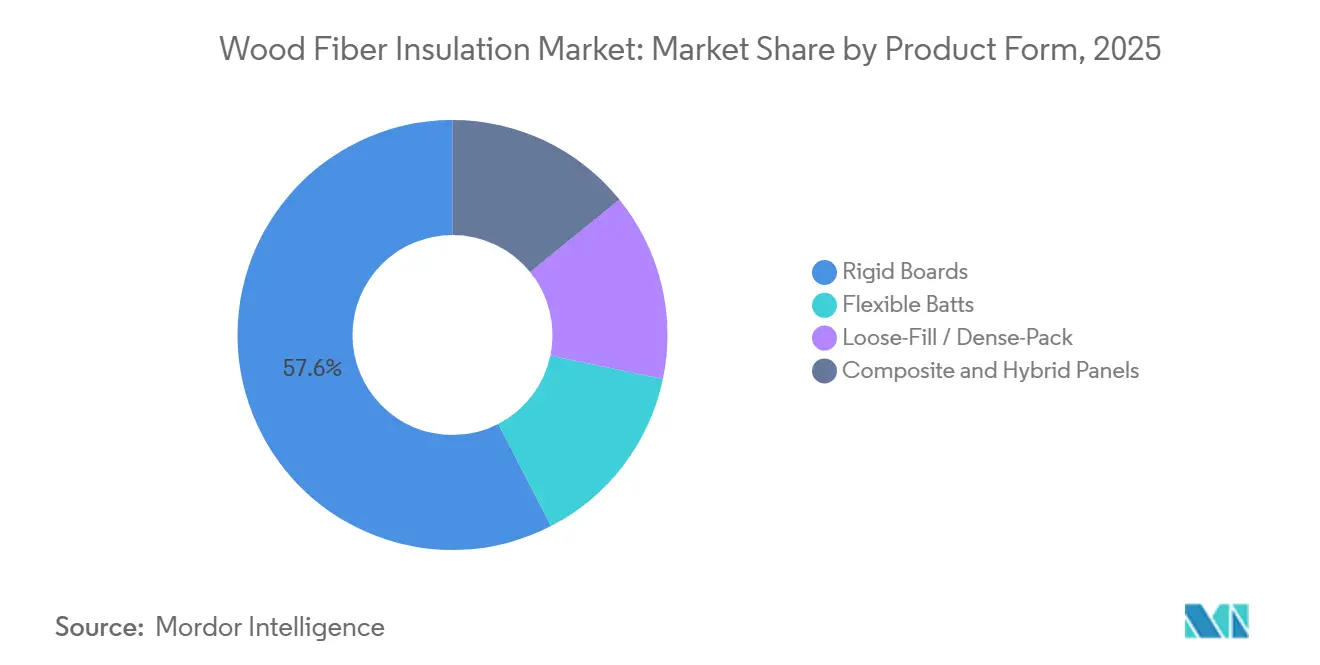

- By product form, rigid boards captured 57.57% of the wood fiber insulation market share in 2025, while loose-fill and dense-pack products are expanding at a 6.97% CAGR through 2031.

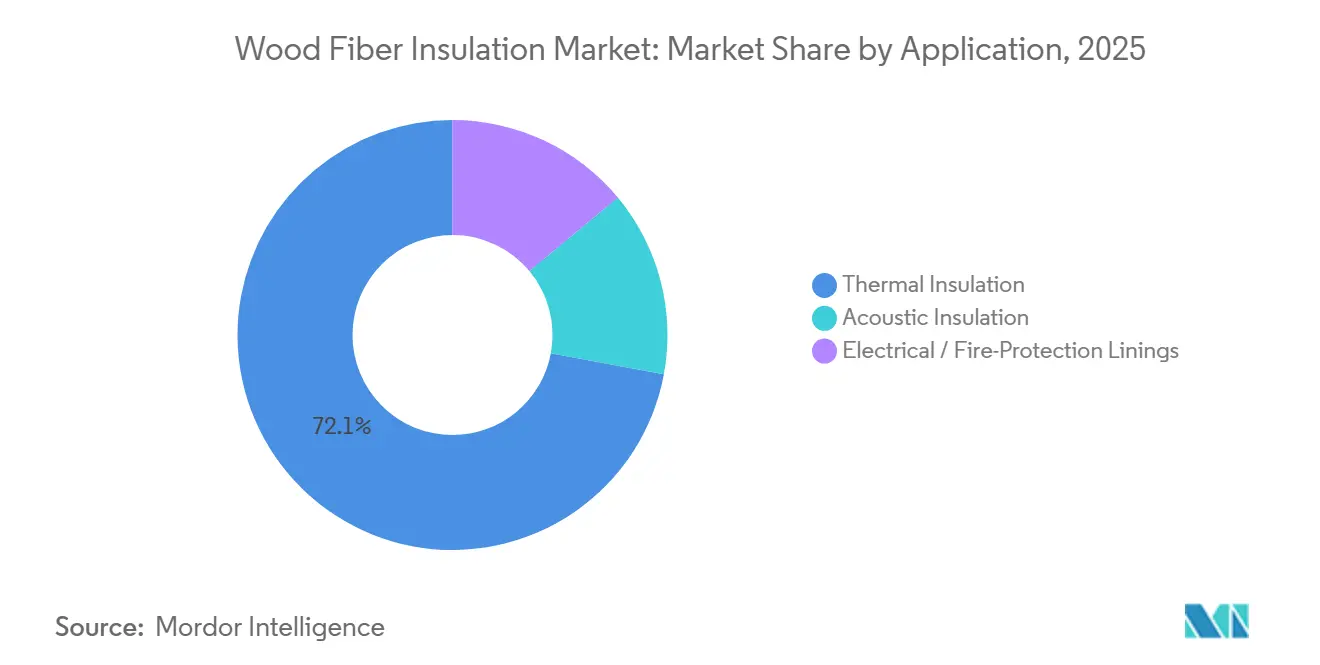

- By application, thermal insulation commanded 72.08% of the wood fiber insulation market size in 2025. However, acoustic insulation is advancing at the fastest 7.05% CAGR through 2031.

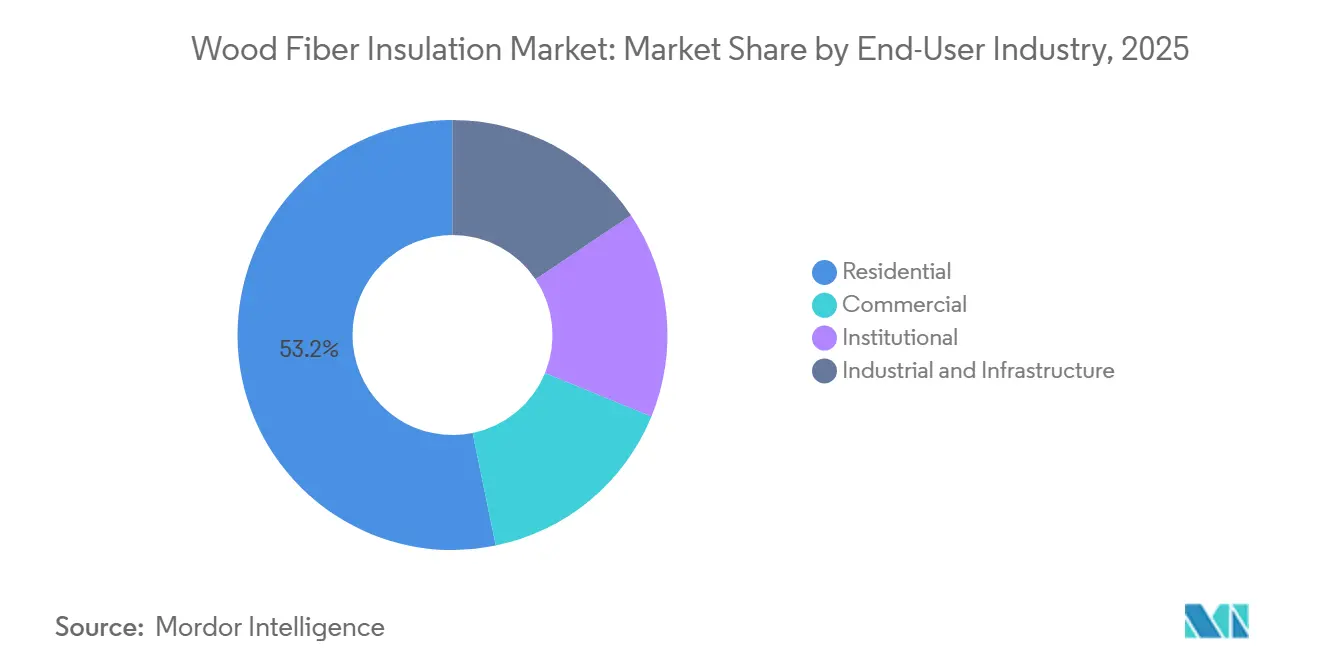

- By end-user industry, residential projects held 53.22% of 2025 demand while commercial construction is growing at a 6.86% CAGR through 2031.

- By geography, Asia-Pacific retained the largest 51.19% revenue share in 2025, recording the fastest regional CAGR at 6.19% during 2026-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wood Fiber Insulation Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter net-zero building energy codes | +1.2% | North America and Europe, early adoption in select APAC cities | Medium term (2-4 years) |

| Surge in residential deep-retrofit programs | +1.5% | North America and Europe, with pilot programs in Australia and New Zealand | Short term (≤ 2 years) |

| Embodied-carbon rules in public procurement | +1.8% | Global, led by North America and Europe, gradual APAC uptake | Long term (≥ 4 years) |

| Off-site modular growth driving vapor-open materials | +0.9% | North America and Europe, emerging in Japan and South Korea | Medium term (2-4 years) |

| Supply-chain localization for circular-economy compliance | +0.7% | Europe and North America, with regional clusters in APAC | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Stricter Net-Zero Building Energy Codes

Mandatory upgrades to wall R-values and carbon-budget ceilings are compressing payback periods for bio-based insulation. California’s 2025 Title 24 amendments raised wall R-values by 15%, disqualifying single-layer fiberglass in climate zones 3–16 and steering architects toward continuous exterior wood fiber boards that satisfy vapor-open requirements[1]California Energy Commission, “2025 Title 24 Building Energy Efficiency Standards,” energy.ca.gov. Norway’s 2025 Technical Building Regulation capped operational plus embodied emissions at 8 kg CO₂-equivalent per m² annually, adding explicit carbon budgets to permit reviews. Irish and German net-zero standards likewise embed whole-life-carbon modules in compliance software, making the biogenic carbon of wood fiber visible at early design stages. As permit officers and energy-modeling consultants align on carbon ceilings, wood fiber moves from niche eco-choice to mainstream compliance route, especially in temperate and cold-climate envelopes. The driver’s influence is expected to intensify once U.S. states beyond California and New York harmonize codes with ASHRAE’s forthcoming CH-36 carbon appendix.

Surge in Residential Deep-Retrofit Programs

Public funding has reached record levels, unlocking latent demand for cavity-infilling materials that combine insulation and air-sealing in a single work step. New York’s EmPower+ weatherization mandate pegs blower-door performance at 0.25 cfm50 per ft², a threshold dense-pack wood fiber satisfies without formaldehyde-based binders. Canada’s Greener Homes Loan lifted its ceiling to CAD 40,000 (USD 29,600) in 2025, and application volume exceeded forecasts by 40% after homeowners paired heat pumps with attic re-insulation. Germany’s BEG grant now covers 45% of material costs for Efficiency House 55 retrofits, a target that vapor-open wood fiber helps achieve by preventing interstitial condensation. Funding milestones have forced contractors to invest in blower-door testing and thermal imaging, creating a feedback loop where verified air-sealing performance cements future wood fiber specifications. The retrofit surge is therefore both a volume catalyst and a skills-development accelerator.

Embodied-Carbon Rules in Public Procurement

Federal and state agencies are turning carbon intensity into a bid pass-fail criterion rather than a tiebreaker. The U.S. Environmental Protection Agency’s Buy Clean guidance prioritizes materials with cradle-to-gate Environmental Product Declarations, and wood fiber’s negative carbon footprint—minus 1.2 to minus 1.8 kg CO₂-e/kg—ranks it ahead of mineral wool and extruded polystyrene[2]U.S. EPA, “Federal Buy Clean Guidance 2024,” epa.gov. California’s 2025 Buy Clean Act now covers insulation packages in projects above USD 1 million, and early data show a 60% year-on-year rise in wood fiber specifications in state university dormitory renovations. New York Executive Order 22 demands whole-life-carbon assessment for state-funded buildings, normalizing the use of biogenic materials during tender evaluation. As ISO 14067 and EN 15804 become de facto gatekeepers, manufacturers lacking accredited EPDs face exclusion from institutional projects, reinforcing first-mover advantages for incumbent wood fiber producers.

Off-Site Modular Growth Driving Vapor-Open Materials

Modular factories value materials that can dry to both sides without additional membranes, and wood fiber boards meet that performance brief. Modular housing captured 6% of U.S. residential starts in 2025, and leading factories reported 40% fewer mold-related callbacks when switching from closed-cell spray foam to wood fiber sheathing. The 2025 International Residential Code Appendix AW legalized vapor-open assemblies in climate zones 4-8, directly validating wood fiber layers in panelized systems. Japanese prefab leader Sekisui House initiated pilot projects that embed European-made boards into steel frames, citing fire-class B-s1, d0 ratings under EN 13501-1. With factories retrofitting CNC lines for wood-fiber board machining, long-term material contracts lock in demand and limit spot-market volatility. The modular channel is therefore both a growth vector and a stabilization mechanism for production runs.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price competition vs. mineral wool and fiberglass | -0.8% | Global, most acute in cost-sensitive residential segments | Short term (≤ 2 years) |

| Limited installer familiarity outside Europe | -0.6% | North America, APAC, and emerging markets | Medium term (2-4 years) |

| High logistics cost from low bulk density | -0.4% | Long-haul markets in APAC, Middle East, and remote regions | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Price Competition vs. Mineral Wool and Fiberglass

Delivered cost remains 10-20% higher than commodity mineral wool in U.S. and APAC housing markets where embodied-carbon premiums have yet to translate into mandatory specifications. Fiberglass batts retailed at USD 0.45 per board-foot R-value in 2025 big-box channels, compared with USD 0.55 for rigid wood fiber boards. Mineral wool keeps share in fire-rated assemblies because its non-combustible ASTM E136 classification eliminates extra coatings, whereas wood fiber boards sometimes require hybrid constructs to meet the same rating. Although deep-retrofit labor synergies close part of the gap, rebate structures in many jurisdictions cap reimbursements at commodity pricing, leaving homeowners to self-fund the premium. Until subsidy frameworks reward low-carbon materials directly, price tension will cap penetration in budget-constrained projects.

Limited Installer Familiarity Outside Europe

A 2025 survey showed only 18% of U.S. insulation contractors had hands-on experience with wood fiber compared with 94% for fiberglass. Certification programs are sparse—fewer than 50 installers across Canada as of 2025—so distributors hesitate to stock products with limited labor capacity. European manufacturers are funding mobile training units, yet ramp-up timelines extend into 2027, risking missed windows as retrofit grants sunset. The learning curve also includes unfamiliar fastener patterns and thicker wall sections, elements that slow jobsite productivity until crews gain repetition. Knowledge gaps, therefore, restrain volume, particularly in regions where retrofit backlogs already outstrip qualified labor pools.

Segment Analysis

By Product Form: Rigid Boards Anchor Share, Loose-Fill Gains in Retrofit

Rigid boards commanded 57.57% of 2025 revenue, underscoring their fit with rain-screen and continuous-insulation assemblies that require dimensional stability. Prefab plants value boards that double as structural sheathing, trimming SKUs, and installation steps. Flexible batts remain niche where stud cavities vary, but mineral wool still dominates that channel, keeping batt uptake modest. Loose-fill and dense-pack products, however, are growing at a 6.97% CAGR because retrofit contractors blow material into irregular bays without settling risk, a durability edge verified in Canadian field studies. Composite panels pairing wood fiber facings with mineral wool or PIR cores are the fastest-evolving line, allowing EN 13501-2 fire ratings without intumescent sprays. As Kingspan’s 2025 vacuum-panel joint venture with Gutex matures, hybrid solutions will erode rigid-board share in passive-house retrofits, though single-material boards will stay dominant in code-minimum residential builds.

Second-generation wet-process lines reduce embodied energy by 18% versus legacy systems, enabling price cuts that buttress rigid-board market position. Meanwhile, loose-fill producers are investing in fiber-conditioning mills that raise bulk density by 12%, paring freight cost and smoothing blown coverage. The product-form landscape is therefore bifurcating: high-performance composite offerings target commercial retrofits where wall thickness is at a premium, while streamlined rigid boards defend core residential volume. Across both channels, digital modeling tools now include hygrothermal modules that highlight wood fiber’s buffering advantage, nudging architects to specify vapor-open layers early in schematic design.

By Application: Thermal Dominates, Acoustic Surges in Multi-Family

Thermal insulation held 72.08% of the 2025 value because building codes universally dictate minimum R-values, and wood fiber boards fit continuous exterior applications without separate weather-resistive barriers. Acoustic usage is expanding at a 7.05% CAGR as mixed-use urban buildings chase 50-dB party-wall and 60-IIC floor-ceiling thresholds. Lab tests record a 52-dB weighted sound-reduction index for 100-mm wood fiber batts, outperforming closed-cell foams that peak in high frequencies but trail in mid-band attenuation. Developers now specify wood fiber in office fit-outs where open-plan acoustics drive tenant satisfaction metrics. Electrical and fire-protection linings remain small but strategic, with ammonium-polyphosphate-treated boards maintaining integrity for 90 minutes at 800 °C, three times longer than conventional OSB. Uptake depends on harmonizing ASTM and EN fire-test protocols, a work-in-progress for multinational data-center projects.

On the thermal front, updated software such as PHPP 10 now models dynamic vapor transport, revealing that wood fiber boards eliminate dew-point risks in climate zones 5-8 when combined with smart-vapor retarder membranes. As codes add hygrothermal checks to compliance paths, wood fiber’s ability to buffer humidity becomes a quantifiable asset. This technical edge offsets partial price premiums, sustaining thermal-segment dominance while acoustic and specialty niches provide margin diversification.

By End-User Industry: Residential Leads, Commercial Accelerates

Residential accounted for 53.22% of 2025 revenue, buoyed by deep-retrofit grants and stricter prescriptive codes in single-family construction. Homebuilders in California, New York, and British Columbia now use software that integrates whole-life carbon into Title 24 and Step-Code workflows, making wood fiber a default selection in high-performance subdivisions. Commercial demand is growing at 6.86% as landlords pursue LEED v4.1 and WELL credits; wood fiber’s zero VOC emissions and moisture buffering score points across multiple categories. An East Coast study of LEED projects showed that swapping spray foam for wood fiber adds four certification points at negligible cost, tilting default specifications in Class A refurbishments.

Institutional buildings—schools, hospitals, government offices—are pivoting as procurement officers adopt embodied-carbon thresholds. Germany now requires life-cycle carbon accounting on public projects above EUR 2 million, and municipal planners report lower compliance costs when they specify wood fiber rather than purchase offsets. Cold-storage operators are piloting the material in high-humidity warehouses, leveraging its hygroscopic properties to curb condensation. Fast-growing commercial and institutional uptake signals a power shift from facilities managers to sustainability officers who rank carbon metrics alongside cost and schedule, sustaining above-trend growth relative to the still-dominant residential segment.

Geography Analysis

Asia-Pacific retained the largest revenue share at 51.19% of the global wood fiber insulation market in 2025, and is also estimated to be the fastest-growing region with a CAGR of 6.19% from 2026-2031. Wood fiber insulation adoption in the region is still developing in many markets due to sparse installer training and freight cost penalties. Japan’s 2025 Building Standard Law now caps embodied carbon in public buildings above 2,000 m², and Sekisui House is testing European-sourced boards in modular steel frames. Australia’s National Construction Code 2025 tightened R-values in alpine zones, creating niche demand in Tasmania and high-altitude New South Wales. Freight costs add USD 0.10-0.12 per board-foot, limiting wood fiber to premium green-build projects until regional plants emerge.

Europe accounted for a significant regional share in 2025, underpinned by Germany, France, and the United Kingdom. The United Kingdom’s Future Homes Standard, effective 2026, requires 75% operational-carbon reductions; passive-house architects wield continuous wood fiber layers to eliminate thermal bridges. Although Europe’s penetration rate nears 40% in Alpine and Nordic new-builds, retrofit programs sustain modest growth even as new-construction upside narrows.

In North America, California, Oregon, and Washington integrate embodied-carbon tables into energy-code compliance, while New York funds deep-energy retrofits that pair heat pumps with continuous exterior insulation. Canada’s Greener Homes loan boost to CAD 40,000 (USD 29,600) sparked provincial bulk-purchase programs that shaved 12-15% off wood fiber board pricing. Mexico’s NOM-020-ENER update set envelope requirements that wood fiber fulfills, birthing an early-adopter cluster in Monterrey and Guadalajara luxury projects.

South America and the Middle East and Africa trail, though Dubai’s Al Sa’fat rating system grants low-carbon credits that tilt high-end hospitality projects toward wood fiber.

Competitive Landscape

The wood fiber insulation market is moderately consolidated. Barriers include integrated forestry assets, specialized defibration lines, and code-approval dossiers. STEICO’s vertical supply chain, from sawmill residuals to finished boards, insulated margins during 2025 resin-price spikes. The 30,000-m³ expansion at its Polish plant targets Central European tenders that now require carbon disclosure on public projects above EUR 5 million.

White-space lies in hybrid laminates that marry fire-resistant cores with vapor-open facings. Patent filings for composite panels climbed 40% year-on-year, centered on structural load-bearing and fire-resistant designs. Agricultural-residue challengers (hemp, straw) test the waters but still lack the code acceptance and long-term durability data amassed by wood fiber over three decades of European field performance. Mergers and acquisitions momentum is likely to intensify as adjacent insulation majors license technology rather than commit to greenfield mills, consolidating know-how and accelerating product approvals in new geographies.

Wood Fiber Insulation Industry Leaders

STEICO SE

Gutex Holzfaserplattenwerk H. Henselmann GmbH + Co. KG

TimberHP

Knauf Insulation

Soprema

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: STEICO SE completed a EUR 22 million expansion of its Czarnków plant, adding 30,000 m³ of rigid-board capacity and installing a wet-process line that cuts energy use by 18%.

- March 2025: TimberHP inaugurated a second facility in Madison, Maine, with 40,000 m³ annual capacity, sourcing 95% of fiber from in-state sawmills and qualifying for Maine Green Building Tax Credits

Global Wood Fiber Insulation Market Report Scope

Wood fiber insulation is manufactured from wood fibers such as sawdust, wood chips, or wood shavings. It is commonly used to create thermal insulation and soundproofing in walls and ceilings. Because it is made from a renewable resource and is biodegradable, wood fiber insulation is an environmentally beneficial solution. It is also fire-resistant and can help you save money on energy. The wood fiber insulation market is segmented by product form, application, end-user industry, and geography. BY product form, the market is segmented into rigid boards, flexible batts, loose-fill / dense-pack, and composite and hybrid panels. The market is segmented by application into thermal, acoustic insulation, and electrical / fire-protection linings. The end-user industry segments the market into residential, commercial, institutional, and industrial and infrastructure. The report also covers the market size and forecasts for around 20 countries. For each segment, the market sizing and forecasts have been done based on value (USD).

| Rigid Boards |

| Flexible Batts |

| Loose-Fill / Dense-Pack |

| Composite and Hybrid Panels |

| Thermal Insulation |

| Acoustic Insulation |

| Electrical / Fire-Protection Linings |

| Residential |

| Commercial |

| Institutional |

| Industrial and Infrastructure |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Product Form | Rigid Boards | |

| Flexible Batts | ||

| Loose-Fill / Dense-Pack | ||

| Composite and Hybrid Panels | ||

| By Application | Thermal Insulation | |

| Acoustic Insulation | ||

| Electrical / Fire-Protection Linings | ||

| By End-User Industry | Residential | |

| Commercial | ||

| Institutional | ||

| Industrial and Infrastructure | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the global wood fiber insulation market and what value is expected by 2031?

Global outlay is estimated to reach USD 0.99 billion in 2026 and is projected to climb to USD 1.34 billion by 2031, reflecting a 6.25% CAGR.

Which geographic region is growing fastest for wood fiber insulation deployments?

Asia-Pacific leads in growth with a 6.19% forecast CAGR for 2026-2031, driven by tightening energy codes and incentive programs.

Why do builders favor rigid wood fiber boards for new-build envelopes?

Rigid boards provide dimensional stability, double as structural sheathing, and meet vapor-open requirements that simplify continuous-insulation assemblies.

What policy measures are accelerating the use of wood fiber insulation in public projects?

Buy Clean rules and embodied-carbon thresholds now make low-carbon materials a pass-fail criterion in bids, giving wood fiber an edge due to its negative cradle-to-gate footprint.

How does wood fiber insulation compare to mineral wool on carbon impact and upfront cost?

Wood fiber carries a negative carbon footprint but still costs 10-20% more delivered than commodity mineral wool in regions lacking carbon-based subsidies.

Which companies hold the largest production capacity for wood fiber insulation?

Leading producers include STEICO, Gutex, Pavatex (Soprema), and TimberHP, and Knauf Insulation together the top five account for roughly 60% of European and 35% of North American capacity.

Page last updated on: