Wholesale Voice Carrier Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 44.53 Billion |

| Market Size (2031) | USD 73.63 Billion |

| Growth Rate (2026 - 2031) | 10.58% CAGR |

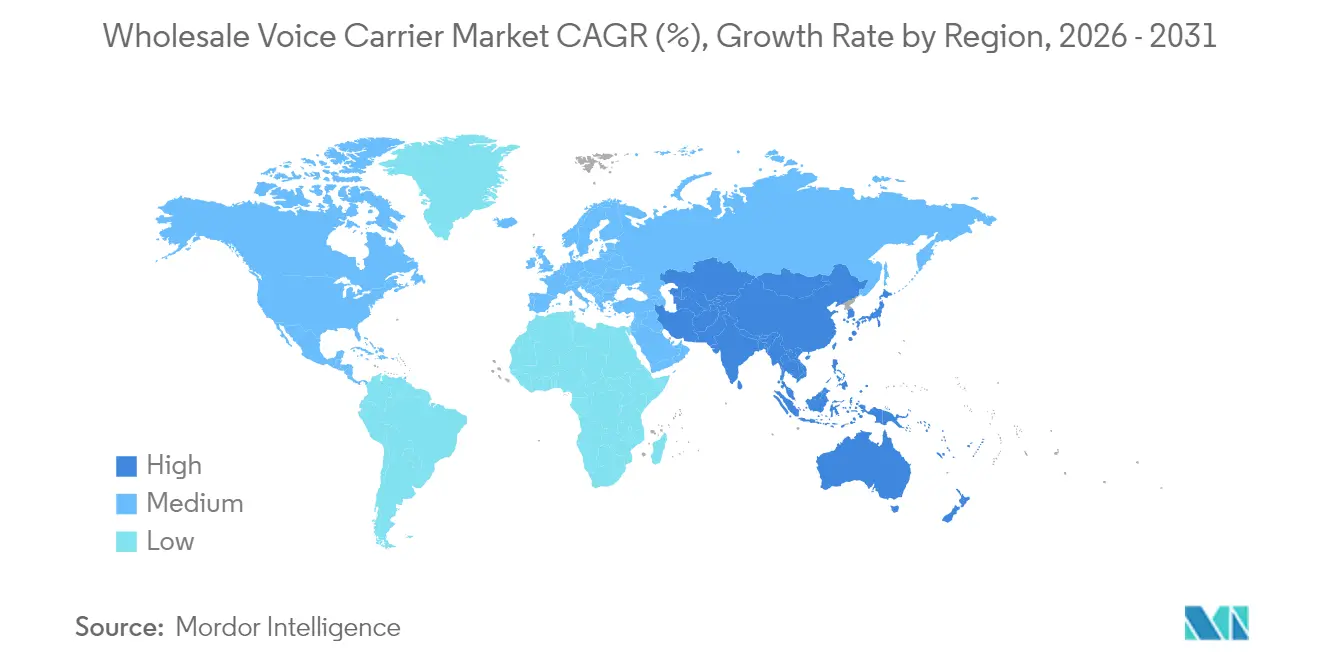

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Wholesale Voice Carrier Market Analysis by ���ϲ�����

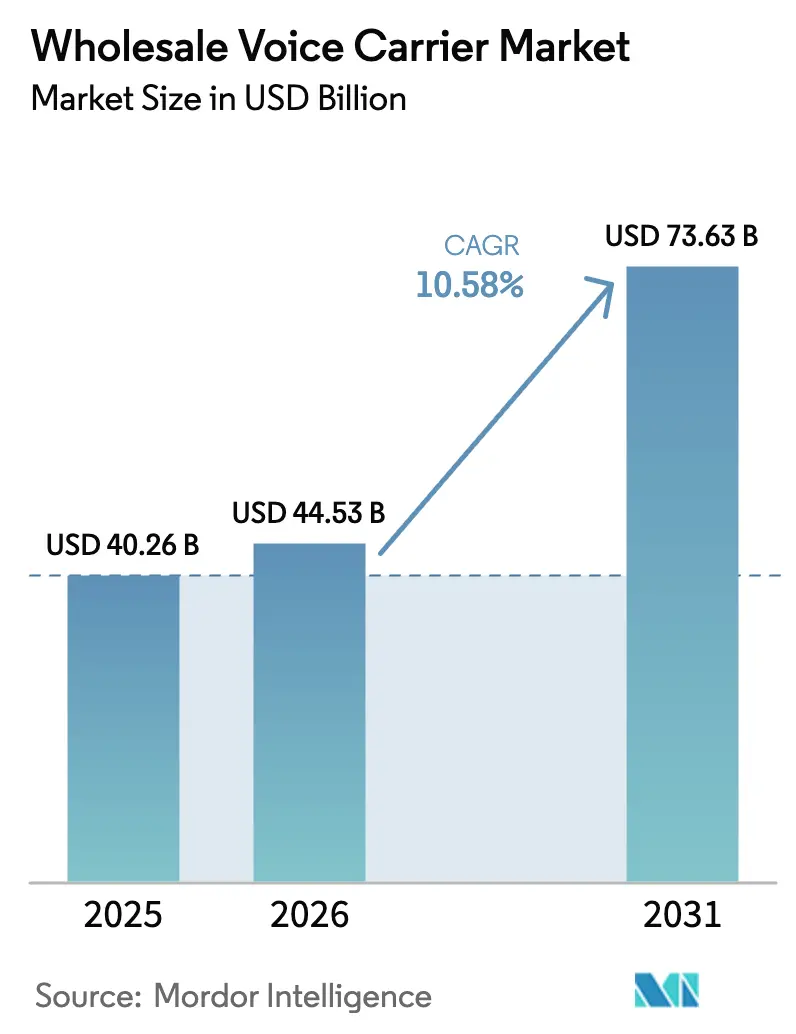

wholesale voice carrier market size in 2026 is estimated at USD 44.53 billion, growing from 2025 value of USD 40.26 billion with 2031 projections showing USD 73.63 billion, growing at 10.58% CAGR over 2026-2031. Migration from circuit-switched to IP-based architectures, rapid expansion of VoIP traffic, and growing demand for programmable voice services place the wholesale voice carrier market at the center of global connectivity. Europe keeps a commanding position thanks to harmonized interconnection rules, while Asia Pacific delivers the highest growth as 5G roll-outs accelerate voice-over-data usage. Consolidation, illustrated by large-scale acquisitions, continues to reshape competitive dynamics as operators seek scale, fiber reach, and advanced routing technologies. Fraud management, AI-driven least-cost routing, and inter-carrier blockchain pilots emerge as high-value niches within the overall wholesale voice carrier market, rewarding providers that pair infrastructure modernization with service innovation.

Key Report Takeaways

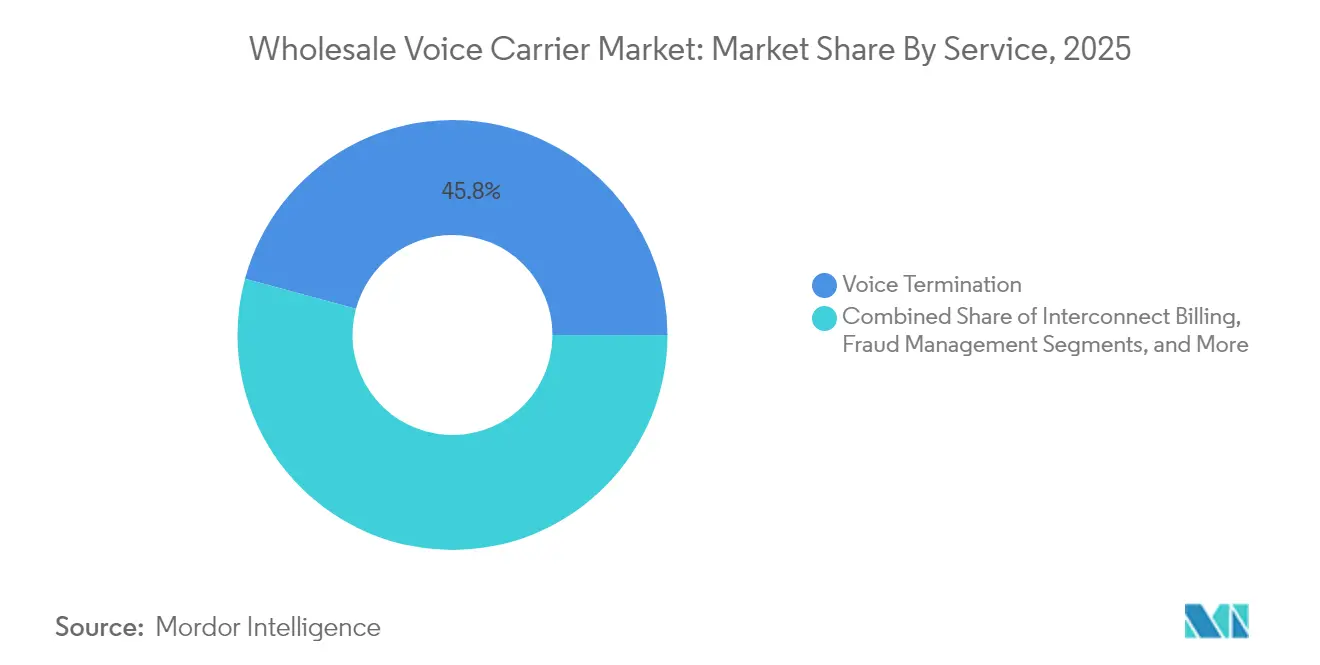

- By service, Voice Termination led with 45.78% revenue share in 2025; Fraud Management is projected to expand at a 13.55% CAGR during 2026-2031.

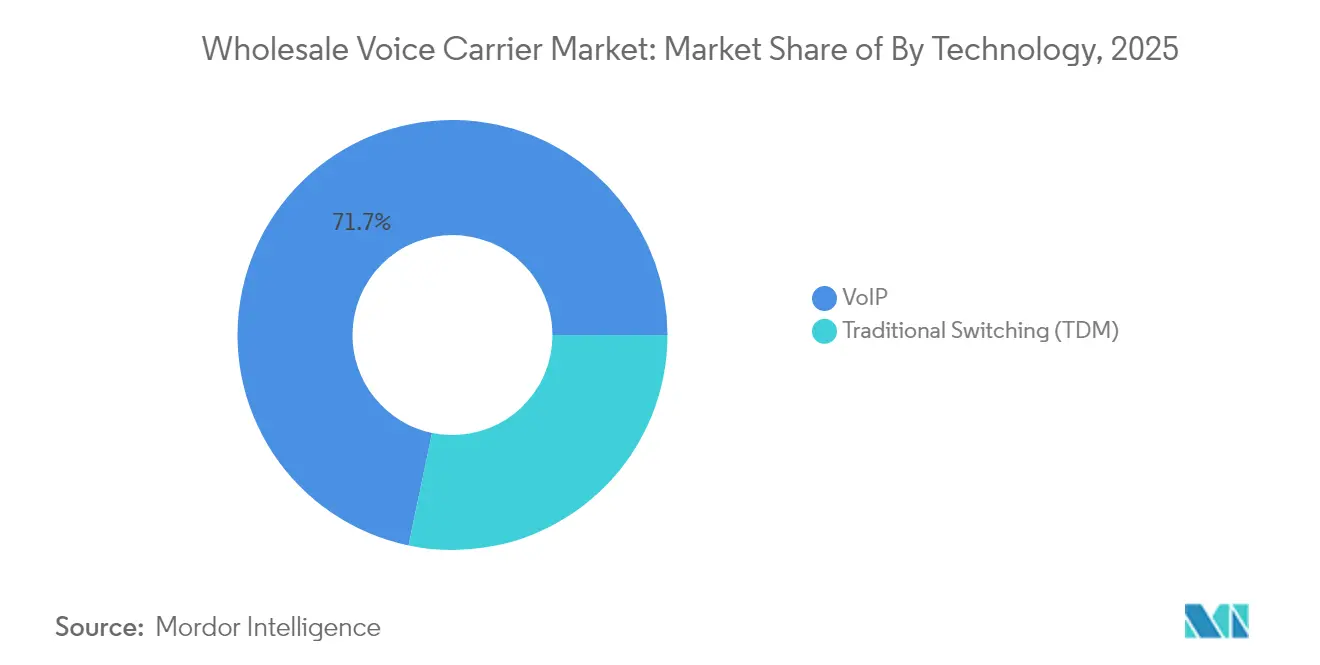

- By technology, VoIP accounted for 71.72% of the wholesale voice carrier market share in 2025, while SIP-based implementations are set to grow at 11.95% CAGR through 2031.

- By end user, Tier-1 and Tier-2 telcos captured 53.35% of demand in 2025, whereas OTT and CPaaS providers registered the fastest pace at 11.45% CAGR to 2031.

- By geography, Europe held 27.95% of 2025 revenue, yet Asia Pacific is forecast to post the highest regional CAGR of 13.72% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wholesale Voice Carrier Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid migration from TDM to SIP and VoIP trunking | +3.2% | Global, acceleration in Europe and North America | Medium term (2-4 years) |

| Cloud-based communication (UCaaS / CPaaS) uptake | +2.8% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Emerging voice-over-5G roaming agreements | +1.9% | Asia Pacific core, spill-over to Europe and North America | Long term (≥ 4 years) |

| AI-enabled dynamic least-cost routing | +1.4% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rapid Migration from TDM to SIP and VoIP Trunking

Mandatory phase-outs of PSTN networks, such as the 2027 switch-off timetable set by Ofcom in the United Kingdom, compel operators to decommission legacy exchanges and invest in IP cores.[1]Ofcom, “Preparing for the PSTN Switch Off,” Ofcom, ofcom.org.ukThe transition compresses maintenance costs, enables flexible capacity scaling, and supports feature expansion even as carriers temporarily operate parallel systems that elevate opex. Early adopters leverage improved latency and advanced codec support to differentiate on call quality, while lagging providers confront regulatory penalties and higher churn risk.

Cloud-based Communication (UCaaS / CPaaS) Uptake

Enterprise preference for unified cloud platforms shifts wholesale demand from fixed trunks to API-centric voice enablement. Operators that expose programmable voice, recording, and analytics capabilities through white-label CPaaS offerings gain new revenue while safeguarding traffic volumes. Funding milestones, such as IntelePeer’s USD 110 million growth investment, signal heightened capital flow toward providers that bridge traditional termination with cloud‐native orchestration.

Emerging Voice-over-5G Roaming Agreements

Standalone 5G cores create opportunities for high-definition voice roaming and network slicing. Trials by Vodafone, A1 Group, and Ericsson deliver full-stack 5G roaming with lower latency and service-based charging, underscoring wholesale relevance in the 5G era.[2]Ericsson, “A1 and Vodafone Complete 5G SA Roaming Call,” Ericsson, ericsson.com China’s nationwide 5G roaming collaboration among its four major carriers further validates the model’s scalability for traffic exchange across heterogeneous infrastructures.

AI-enabled Dynamic Least-cost Routing Boosts Margins

AI integration replaces static routing tables with real-time quality and cost optimization. Nokia’s extension of its voice-core contract with AT&T embeds machine-learning analysis of call completion rates and customer experience metrics, redirecting traffic away from under-performing routes and lifting gross margin while sustaining service-level agreements. Capital-light carriers can now access comparable intelligence, narrowing performance gaps with incumbents.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened fraud (CLI spoofing, robocalls) | -2.1% | Global, particularly severe in North America | Short term (≤ 2 years) |

| Declining voice ARPU due to OTT substitution | -1.8% | Global, accelerated in developed markets | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Heightened Fraud (CLI Spoofing, Robocalls)

Escalating vishing attacks that generated USD 1.2 billion in losses during 2024 undermine consumer trust and trigger stricter compliance mandates. Wholesale carriers invest heavily in analytics-driven fraud detection, yet must balance protection costs against thin per-minute margins. International fraud, estimated at USD 17 billion annually, includes False Answer Supervision and Traffic Pumping schemes that erode profitability while damaging brand reputation.

Declining Voice ARPU due to OTT Substitution

Voice minutes shrink as consumers migrate to data-rich messaging platforms. Germany’s fixed voice traffic fell 20% to 64 billion minutes in 2024, and mobile outgoing calls dipped to 153.5 billion minutes. Carriers bundle voice with data and introduce verified caller solutions to preserve value, yet wholesale rates remain under pressure as OTT offerings set new price benchmarks.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Fraud Management Drives Innovation

Voice Termination accounted for 45.78% of revenue in 2025, maintaining its role as the cornerstone of inter-carrier exchange. However, Fraud Management delivers the swiftest expansion at 13.55% CAGR to 2031 as enterprises demand authenticated caller identities and regulators mandate robocall mitigation. Higher-margin Premium CLI products outperform commoditized Standard Best-Effort traffic thanks to guaranteed delivery and origin validation. Interconnect Billing splits between customizable on-premise modules preferred by large incumbents and SaaS suites adopted by smaller operators seeking opex flexibility. The wholesale voice carrier market benefits when revenue-assurance platforms integrate machine-learning pattern recognition, enabling predictive blocking of anomalous traffic bursts.

Fraud Management momentum stems from regulatory frameworks such as STIR/SHAKEN in North America, compelling carriers to certify calling party numbers before termination. Leading vendors package signaling firewalls with real-time analytics dashboards that flag suspicious answer-seizure ratios. As these capabilities mature, smaller solution providers encounter entry barriers while established players consolidate share through end-to-end fraud stacks. For carriers, premium anti-fraud service uptake supports average-revenue-per-minute lift that partially offsets unit price compression in the wider wholesale voice carrier market.

By Technology: VoIP Transformation Accelerates

VoIP held 71.72% adoption in 2025 and is advancing at 11.95% CAGR, confirming its dominance over residual TDM traffic. SIP’s maturity simplifies interconnect negotiations and supports codec agility, creating a virtuous cycle of quality improvement and cost efficiency. The wholesale voice carrier market size for VoIP-based traffic is set to widen materially as operators deactivate legacy TDM switches following national PSTN retirement schedules. Demonstrations such as Nokia’s three-dimensional Immersive Voice at MWC 2025 show how spatial audio can become a premium layer atop existing VoIP frameworks.

Sustained protocol innovation benefits from AI-assisted transcoding that minimizes packet loss and latency. NTT Corporation’s real-time voice conversion prototype highlights a future where voice characteristics, accent localization, and emotion filtering personalize caller interactions without compromising network performance. These advances reinforce VoIP’s position as the foundation for next-generation services, elevating the wholesale voice carrier market as an essential backbone for immersive voice communication.

By End User: OTT Providers Reshape Demand

Tier-1 and Tier-2 telcos represented 53.35% of traffic demand in 2025, relying on wholesale partners to extend geographic coverage and optimize least-cost routing. Yet the fastest growth comes from OTT and CPaaS providers at 11.45% CAGR through 2031. These application-layer firms lease wholesale voice routes and wrap them with programmable APIs that power customer engagement, two-factor authentication, and AI voice agents. KORE Wireless’s MVNE platform enabling Simpel’s rapid subscriber growth shows how virtual operators depend on wholesale infrastructure to scale cost-effectively.

The end-user mix signals a value-shift from infrastructure ownership toward service orchestration. CPaaS deployments, such as IntelePeer’s generative-AI agent for a Fortune 100 fintech client, consume substantial voice minutes while requiring integration simplicity and granular analytics. The wholesale voice carrier market adapts by offering white-label routing, real-time provisioning, and billing APIs that let digital-native brands embed voice functionality while abstracting network complexity.

Geography Analysis

Europe maintained a 27.95% revenue share in 2025, underpinned by robust cross-border interconnection regulations and widespread fiber backbones. Market maturity prompts a pivot toward efficiency and value-added services, illustrated by Deutsche Telekom’s EUR 115.8 billion revenue and 6.2% EBITDA uplift in 2024.Consolidation discussions between major incumbents such as Orange and Telefónica underline a strategic need to counter hyperscale cloud rivals and OTT disruptors.

Asia Pacific delivers the fastest regional trajectory at 13.72% CAGR through 2031, propelled by soaring 5G subscriptions, rising enterprise digitization, and inter-regional trade flows. The GSMA values the mobile economy contribution at USD 880 billion in 2024, with China alone recording RMB 1.74 trillion telecommunications revenue and double-digit growth in cloud and big-data services. Such momentum enlarges the wholesale voice carrier market size across the region as operators deploy standalone 5G cores that require new interconnect and roaming frameworks.

North America exhibits technological leadership but slower traffic growth. The region enforces stringent STIR/SHAKEN frameworks, compelling carriers to invest in call authentication before termination. Verizon’s USD 20 billion purchase of Frontier Communications extends fiber reach across 25 states and consolidates voice and broadband assets. Latin America presents divergent strategies: Telefónica accelerates divestments in Argentina, Chile, and Mexico to refocus capital on higher-return European markets while maintaining selective presence where regulatory conditions support profitability.

Competitive Landscape

The wholesale voice carrier market combines infrastructure-heavy incumbents with asset-light disruptors, resulting in moderate fragmentation. Strategic initiatives cluster into three categories. First, horizontal consolidation aims to aggregate scale and fiber footprints, as demonstrated by Verizon-Frontier and Sinch-Inteliquent transactions. Second, technology differentiation emphasizes AI routing, blockchain settlements, and immersive audio; Nokia’s digital operations suite for AT&T exemplifies this path. Third, vertical service expansion positions carriers in adjacent fraud management and CPaaS arenas, blurring lines between wholesale transport and application enablement.

Incumbent operators leverage extensive interconnect agreements and capital reserves, yet face margin squeeze from OTT substitution and regulatory price oversight. New entrants exploit programmable interfaces, cloud deployment, and specialized fraud solutions to win traffic from digital-native enterprises. Patent filings by Samsung, Apple, and other technology firms indicate convergence between telecom networks and machine-learning voice processing, foreshadowing competition that extends beyond traditional carriers.

White-space prospects materialize wherever quality-sensitive enterprises require guaranteed termination, verified caller identity, or low-latency 5G voice. Providers that integrate AI-driven routing, dynamic settlement ledgers, and advanced codec support strengthen bargaining power with both legacy telcos and OTT customers. Conversely, carriers that delay modernization risk traffic outflow to global aggregators that can terminate at scale with validated caller signatures.

Wholesale Voice Carrier Industry Leaders

Verizon

AT&T

������

Deutsche Telekom AG

Tata Communications

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Verizon secured FCC approval for its USD 20 billion Frontier Communications acquisition, enabling expansion of fiber broadband capabilities across 25 states and positioning the company to compete more effectively with AT&T’s fiber infrastructure investments.

- February 2025: Deutsche Telekom reported record 2024 financial results with EUR 115.8 billion revenue and raised 2025 outlook for adjusted EBITDA to approximately EUR 45.0 billion, demonstrating sustained growth momentum in European telecommunications markets.

- February 2025: Nokia, Vodafone, and RingCentral showcased Immersive Voice and Audio Services at MWC 2025, introducing three-dimensional sound experiences that enhance business communications through metadata-assisted spatial audio technology

- February 2025: AT&T expanded its voice core partnership with Nokia through a multi-year deal focused on network security, automation, and Voice-over-New-Radio capabilities, including deployment of Nokia’s Digital Operations software for automated service delivery

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

���ϲ����� defines the wholesale voice carrier market as the total annual value of voice minutes exchanged between licensed network operators and service providers, whether routed through traditional TDM switches or session-based VoIP interconnects. The study captures revenues from voice termination, interconnect billing, and fraud-management services that enable cross-network delivery of calls for fixed, mobile, MVNO, and CPaaS players.

Scope exclusion: consumer over-the-top calling apps that bypass carrier interconnect arrangements are not sized within this market.

Segmentation Overview

- By Service

- Voice Termination

- Premium (CLI Guaranteed)

- Standard (Best-Effort)

- Interconnect Billing

- On-premise Solutions

- SaaS-based Solutions

- Fraud Management

- Revenue-Assurance and Analytics

- Signalling-Based Firewalls

- Voice Termination

- By Technology

- VoIP

- SIP (IMS)

- H.323 and Other Protocols

- Traditional Switching (TDM)

- VoIP

- By End User

- Tier-1 and Tier-2 Telcos

- Mobile Virtual Network Operators (MVNO)

- OTT and CPaaS Providers

- Enterprises and BPOs

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed wholesale product heads at regional carriers, switch vendors, and fraud-management specialists across North America, Europe, Asia-Pacific, and the Middle East. Dialogues tested preliminary assumptions on minute growth, VoIP migration speed, and price-erosion curves, and then filled information gaps that public filings do not disclose.

Desk Research

Our analysts began with telecommunications statistics from tier-one public sources such as the International Telecommunication Union, the Federal Communications Commission, GSMA Intelligence, Eurostat, and UN Comtrade, which outline traffic minutes, subscriber bases, and interconnect rate trends. Company 10-Ks, wholesale rate cards, and investor presentations supplied blended average-selling-price indicators, while news wires from Dow Jones Factiva and shipment logs on Volza offered timely signals on route tariffs and bilateral agreements. These examples illustrate, rather than exhaust, the secondary sources consulted during data collection and verification.

Market-Sizing & Forecasting

A top down and bottom up hybrid model converts regional minutes of use into revenue through sampled interconnect rates that are weighted by call destination mix. Supplier roll-ups of major hub carriers act as a reasonableness cross-check. Key model drivers include international outbound minutes per subscriber, VoIP share of wholesale traffic, average settlement rate per minute, smartphone penetration, and adoption of CPaaS voice platforms. Multivariate regression projects each driver, and scenario analysis tests sensitivity to tariff regulation or rapid OTT substitution before consolidated forecasts are produced for 2019-2030.

Data Validation & Update Cycle

Outputs pass a multi-step review that screens anomalies against traffic statistics, carrier disclosures, and peer signals. Senior analysts sign off after reconciling variances. Reports refresh every twelve months, with interim revisions when material events, such as a major hub acquisition, shift baseline assumptions.

Why Our Wholesale Voice Carrier Baseline Commands Reliability

Published estimates often diverge because firms apply different traffic pools, price assumptions, and refresh cadences.

Key gap drivers include varying treatment of on-net minutes, some studies using global averages instead of route-specific tariffs, and others extrapolating historic declines without validating current VoIP migration rates or currency conversions updated quarterly by Mordor analysts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 40.26 bn (2025) | ���ϲ����� | - |

| USD 39.6 bn (2023) | Global Consultancy A | excludes interconnect billing revenue and applies flat regional tariffs |

| USD 25.32 bn (2023) | Trade Journal B | focuses on Tier-1 routes only and uses conservative VoIP penetration |

| USD 43.27 bn (2024) | Regional Consultancy C | inflates totals by counting retail OTT traffic alongside carrier minutes |

The comparison shows that figures swing widely when scope or price logic shifts. By anchoring estimates to verified minutes, route-level tariffs, and an annual refresh cycle, ���ϲ����� delivers a balanced, transparent baseline that decision-makers can reproduce and trust.

Key Questions Answered in the Report

What is the current size of the wholesale voice carrier market?

The wholesale voice carrier market is valued at USD 44.53 billion in 2026 and is projected to reach USD 73.63 billion by 2031.

Which region grows fastest in wholesale voice services?

Asia Pacific registers the quickest pace with a forecast 13.72% CAGR to 2031, driven by 5G adoption and expanding mobile subscriber bases.

What segment records the highest growth?

Fraud Management services are expected to grow at 13.55% CAGR between 2026 and 2031 as enterprises seek verified caller solutions.

How dominant is VoIP in wholesale traffic?

VoIP commands 71.72% of 2025 traffic and is set to strengthen further with a 11.95% CAGR as operators phase out TDM networks.

Which end-user group is expanding most rapidly?

OTT and CPaaS providers lead demand growth, advancing at 11.45% CAGR through 2031, as they embed voice APIs into digital applications.

What key risk affects wholesale voice revenues?

Heightened fraud through CLI spoofing and robocalls is projected to shave 2.1% off CAGR forecasts unless carriers deploy advanced mitigation tools.

Page last updated on: