Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.74 Billion |

| Market Size (2031) | USD 8.95 Billion |

| Growth Rate (2026 - 2031) | 2.95% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

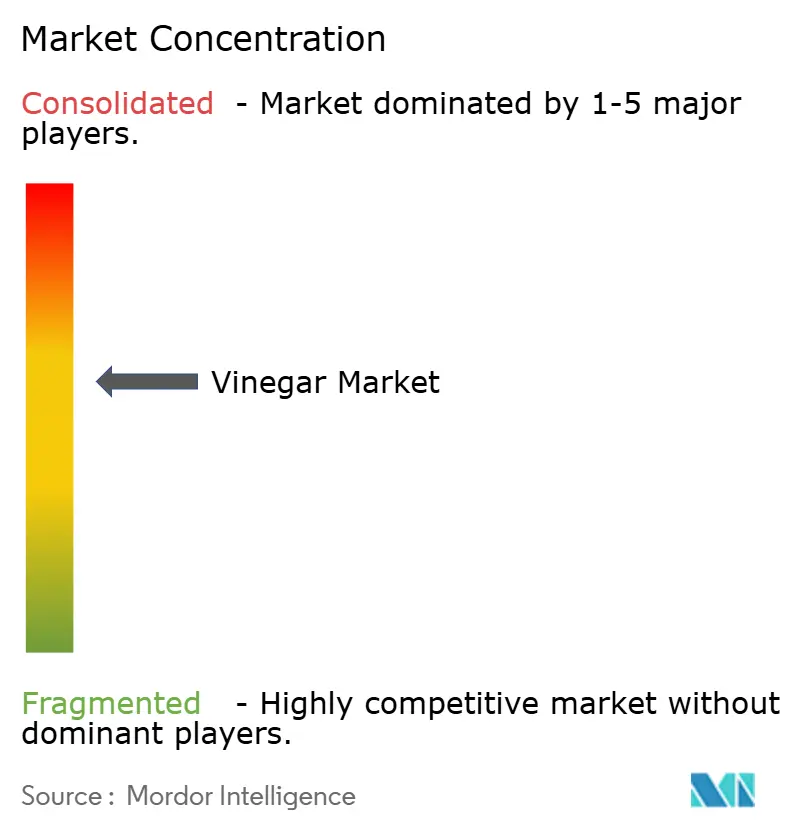

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Vinegar Market Analysis by ���ϲ�����

The Vinegar Market size was valued at USD 7.66 billion in 2025 and is estimated to grow from USD 7.74 billion in 2026 to reach USD 8.95 billion by 2031, at a CAGR of 2.95% during the forecast period (2026-2031). While overall growth appears moderate, notable shifts are occurring beneath the surface. Millennials and Gen Z are increasingly adopting ready-to-drink and functional vinegar beverages, redefining vinegar from a basic condiment to a wellness-focused drink. Advances in fermentation technologies, such as genomic strain selection, dry-gelatinization of starches, and controlled aging, enable producers to ensure consistent acidity and longer shelf life without relying on synthetic preservatives, thereby improving profit margins. Asia-Pacific currently accounts for one-third of global demand, while Europe is witnessing the fastest growth, supported by Protected Geographical Indication rules that enhance premium balsamic exports. Additionally, consistent bulk purchases from foodservice chains provide stability to the vinegar market, even during retail slowdowns. However, agricultural price fluctuations and competition from industrial acetic acid are driving operators to hedge feedstock contracts and prioritize authenticity to strengthen their market positioning.

Key Report Takeaways

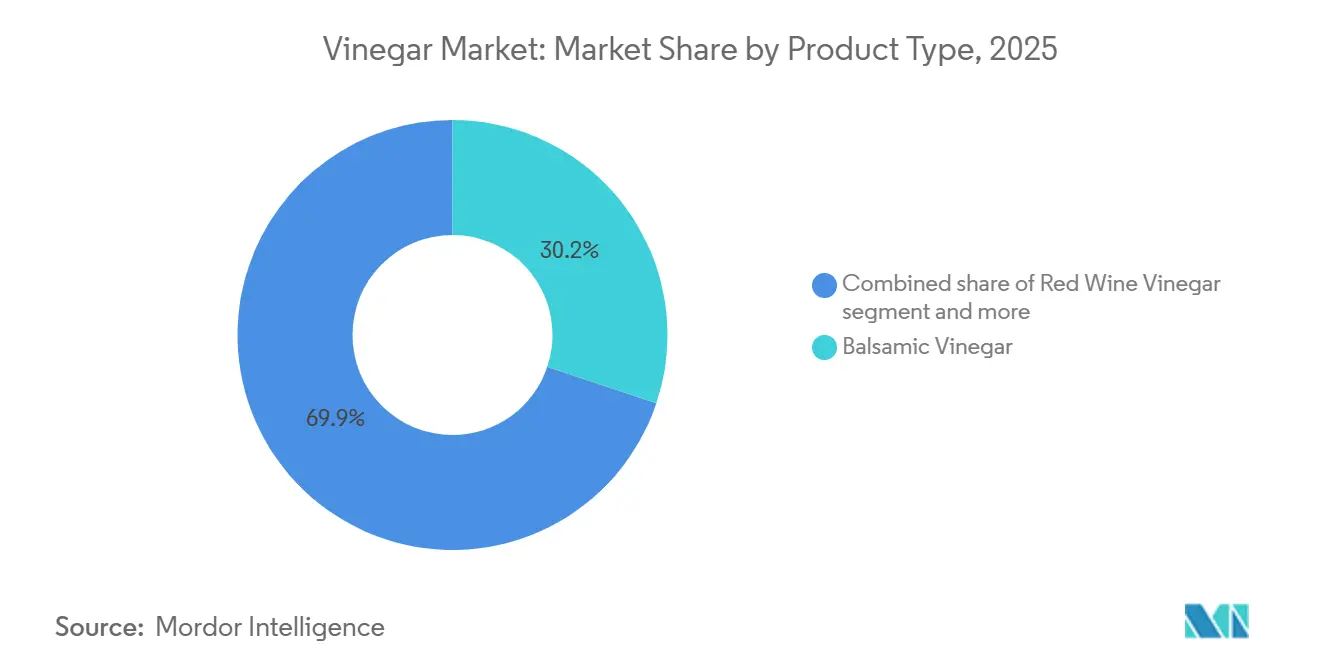

- By product type, balsamic vinegar led with 30.15% of the vinegar market share in 2025, while cider vinegar is forecast to expand at a 3.18% CAGR to 2031.

- By source, conventional variants accounted for 66.83% of the vinegar market size in 2025, whereas organic vinegar is projected to rise at a 3.66% CAGR through 2031.

- By flavor, unflavored formats captured 75.97% of revenue in 2025; flavored vinegar is advancing at a 3.84% CAGR over 2026-2031.

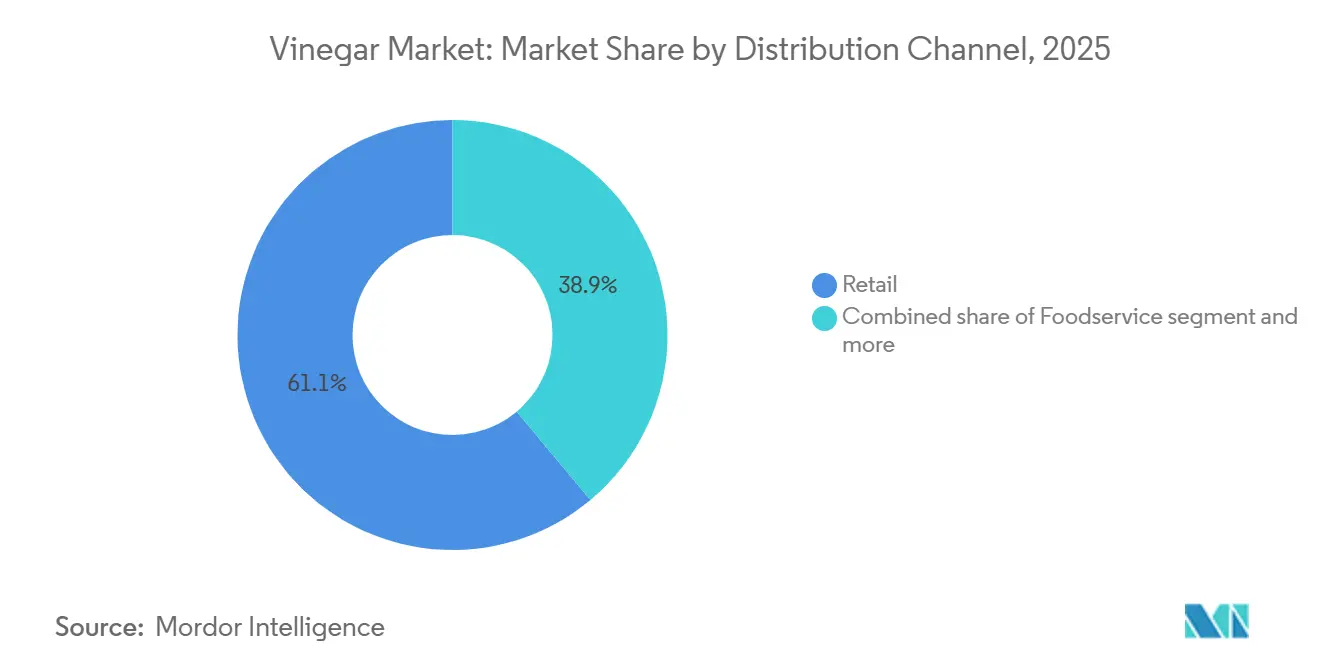

- By distribution channel, retail controlled 61.08% of 2025 sales, and foodservice is growing at 3.85% CAGR to 2031.

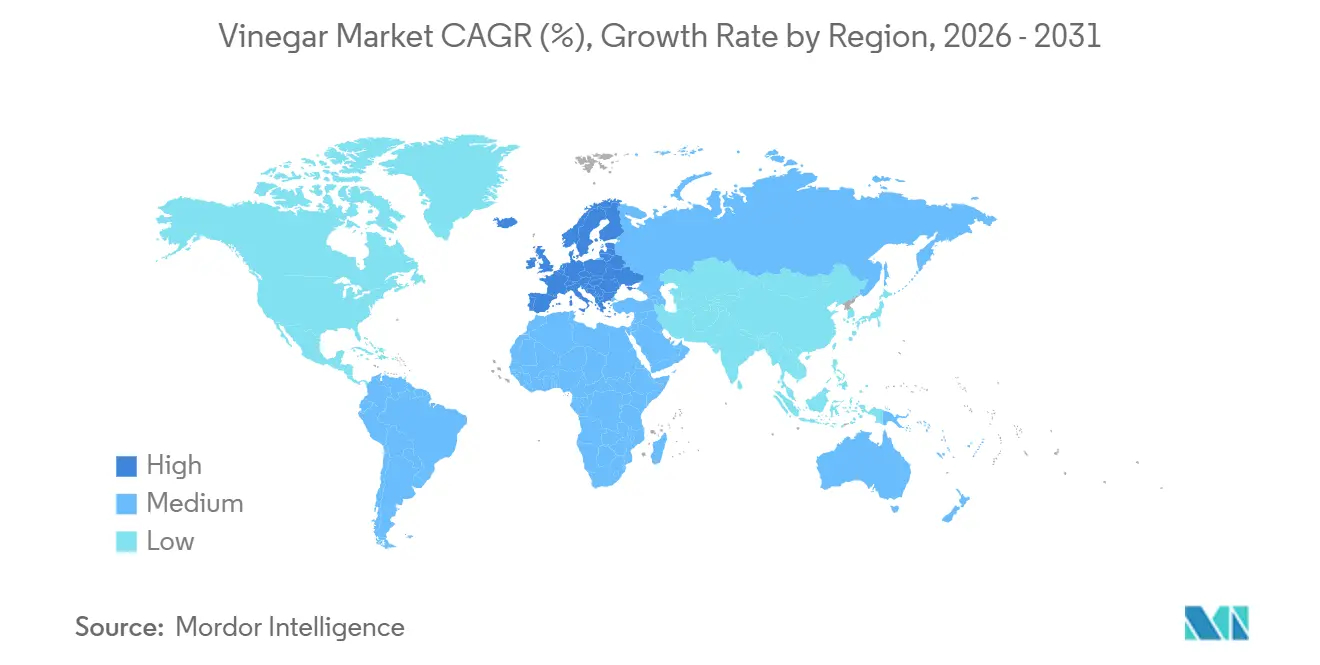

- By geography, Asia-Pacific accounted for 33.98% of the vinegar market size in 2025, whereas Europe is projected to rise at a 3.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vinegar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Innovation in flavored, low-sugar, and ready-to-drink vinegar beverages attracts younger consumers | +0.6% | North America and Europe, spillover to urban Asia-Pacific | Medium term (2-4 years) |

| Rising health awareness is driving apple cider vinegar consumption globally | +0.7% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Growing popularity of organic and clean-label food ingredients | +0.5% | Europe and North America, expanding to Asia-Pacific urban centers | Long term (≥ 4 years) |

| Growth of the foodservice industry boosting bulk vinegar demand worldwide | +0.4% | Global, led by North America and Europe post-pandemic recovery | Short term (≤ 2 years) |

| Rising demand for natural preservatives in processed food products | +0.3% | Global, particularly Europe and North America due to regulatory push | Long term (≥ 4 years) |

| Technological advancements in fermentation enhancing product quality and shelf life | +0.3% | Global, with early adoption in Japan, Europe, and North America | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Innovation in flavored, low-sugar, and ready-to-drink vinegar beverages attracts younger consumers

Brands such as Apeal World and Acid League are transforming the perception of vinegar by introducing sparkling vinegar drinks with reduced sugar content. These products cater to health-conscious millennials and Gen Z consumers, providing a healthier alternative to sugary sodas and energy drinks. The UK Food Standards Agency's High in Fat, Salt, and Sugar regulations, set to take effect in October 2025, will restrict the promotional placement of products exceeding specific nutrient thresholds. This regulation is expected to create shelf space for low-sugar vinegar beverages that comply with these standards. Flavor innovations are expanding beyond traditional fruit infusions to include botanical blends, chili-infused variants, and seasonal options. For instance, De Nigris launched its pumpkin spice vinegar in 2024. This premiumization approach enables producers to achieve higher margins while distinguishing their products from commodity white vinegar, which faces significant price competition. As diabetes becomes more prevalent, low-sugar vinegar beverages are gaining traction among younger consumers, driving market growth. According to the latest International Diabetes Federation (IDF) Diabetes Atlas (2025), 11.1% of adults aged 20-79 are currently living with diabetes[1]Source: International Diabetes Federation, "Diabetes Facts and Figures", idf.or.

Rising health awareness driving apple cider vinegar consumption globally

Apple cider vinegar, which originated as a folk remedy, is now recognized as a functional ingredient, supported by peer-reviewed research that highlights its impact on postprandial glucose and lipid profiles. A review by Harvard T.H. Chan School of Public Health indicated that consuming 1-2 tablespoons of vinegar before meals can improve insulin sensitivity and help reduce blood sugar spikes. However, the review also cautioned against overconsumption due to potential risks such as enamel erosion and gastrointestinal discomfort. With this scientific backing, brands are expanding their product offerings. For example, Bragg introduced apple cider vinegar gummies at Sprouts Farmers Market in February 2025, targeting the supplement aisle to attract consumers who prefer convenient dosing over traditional liquid forms. Furthermore, the antimicrobial properties of acetic acid appeal to consumers looking for natural alternatives to synthetic preservatives, aligning with the broader clean-label trend. Despite its growing popularity, regulatory bodies have not yet established standardized health claims for vinegar, leaving producers to navigate varying national guidelines with differing levels of permissiveness.

Growing popularity of organic and clean-label food ingredients

Organic vinegar sales are growing as consumers focus on ingredient transparency and demand clarity in sourcing. Urban millennials, in particular, favor clean-label products with minimal additives and are willing to pay a premium for certified organic goods. A 2025 report from the India Brand Equity Foundation underscores this trend, showing that 60% of Indian consumers are prepared to spend more on organic products[2]Source: India Brand Equity Foundation, "Future of Food Processing in India", ibef.org. To obtain organic certification, vinegar producers must source raw materials from farms that avoid synthetic pesticides and fertilizers. While this increases production costs, it also helps producers differentiate themselves in competitive retail markets. A 2024 OECD study revealed that 40% of online sustainability claims lacked evidence, prompting stricter regulatory enforcement. This has raised compliance challenges, particularly for smaller producers. Consequently, established brands with strong certification systems are better positioned to adapt, potentially consolidating their market share as they navigate these changing standards.

Growth of the foodservice industry boosting bulk vinegar demand worldwide

Foodservice channels significantly drive vinegar consumption in North America. This structural characteristic protects producers from retail price wars but links their growth to restaurant traffic and the recovery of quick-service dining. The post-pandemic resurgence in dining has increased bulk vinegar demand for applications such as salad dressings, marinades, and pickling. In response, major suppliers have expanded their capacities. For example, Mizkan Holdings invested USD 156 million to enhance its Kentucky facility, targeting foodservice distributors that serve chain restaurants and contract caterers. Additionally, the growth of ghost kitchens and delivery-only models has diversified demand. These operators prioritize shelf-stable ingredients with consistent flavor profiles, reducing the focus on artisanal small-batch vinegars. This trend benefits large-scale fermenters capable of producing uniform quality across multi-thousand-liter batches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong competition from synthetic acids and alternative condiments | -0.4% | Global, particularly in industrial and cost-sensitive segments | Medium term (2-4 years) |

| Fluctuations in raw material prices | -0.3% | Global, with acute impact in regions dependent on imported feedstocks | Short term (≤ 2 years) |

| Inconsistent quality across local and unorganized vinegar manufacturers | -0.2% | Asia-Pacific, Middle East and Africa, and South America | Long term (≥ 4 years) |

| Vinegar's sharp flavor limits use in certain culinary applications | -0.1% | Global, particularly in sweet and delicate flavor profiles | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Strong competition from synthetic acids and alternative condiments

Global supply of industrial acetic acid is primarily driven by methanol carbonylation. While regulatory standards mandate that food-grade vinegar be produced through fermentation, synthetic acetic acid is extensively utilized in non-food sectors. These include textile processing, pharmaceuticals, and chemical synthesis, establishing a cost benchmark that influences vinegar pricing in related markets. Moreover, alternative condiments like lemon juice, citric acid, and proprietary blends are increasingly encroaching on vinegar's territory in salad dressings and marinades. This trend is especially pronounced among budget-conscious foodservice operators. The growing popularity of plant-based and ethnic cuisines has ushered in new flavor profiles vying for attention. Ingredients such as tamarind paste, pomegranate molasses, and yuzu juice provide acidity without the distinct aroma of vinegar. This shift poses a significant risk, especially in upscale dining, where chefs emphasize ingredient novelty and sensory distinction over traditional condiments.

Fluctuations in raw material prices

Vinegar production depends on agricultural feedstocks, apples, grapes, grains, and sugarcane, whose prices show cyclical volatility influenced by weather patterns, geopolitical disruptions, and biofuel demand. In 2024, the World Bank's commodity price index for agriculture increased by 12%, with grains and oilseeds experiencing significant price hikes due to droughts in critical growing regions and export restrictions by major suppliers. Apple cider vinegar producers are particularly affected by the availability of cider apples, which compete with fresh fruit and juice markets. A poor harvest in areas like Washington State or Normandy can quickly reduce supply and drive up costs. Similarly, grape-based vinegar producers must navigate the dynamics of the wine industry, where premium varietals command higher prices for winemaking, leaving only lower-grade or surplus grapes for vinegar production. Currency fluctuations further exacerbate challenges for producers relying on imported feedstocks. For example, a stronger dollar raises input costs for European and Asian manufacturers sourcing grains from North America.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Balsamic vinegar, renowned for its centuries-old barrel aging process, captured a significant 30.15% share of the 2025 revenue. This traditional aging method not only enhances its flavor profile but also allows it to command double-digit price premiums in the market. The balsamic segment within the vinegar market is anticipated to experience steady growth, driven by the enforcement of geographic indications that protect its authenticity and the increasing popularity of tourism-driven gifting. In contrast, commodity red- and white-wine vinegars continue to serve as cost-effective options, primarily utilized in salad dressings. Malt vinegar, on the other hand, remains deeply rooted in its association with the traditional fish-and-chips culture, while rice vinegar caters specifically to the culinary traditions and preferences of East Asian cuisine.

Cider vinegar stands out as the fastest-growing segment in the vinegar market, propelled by its strong positioning within the wellness trend. It is projected to grow at a compound annual growth rate (CAGR) of 3.18% through 2031. Innovations such as Bragg’s cider vinegar gummies are expanding the scope of vinegar consumption, transforming it from a cooking ingredient to a popular dietary supplement. This shift is being increasingly adopted by private-label retailers, further driving growth in this segment. Although specialty vinegars, including fruit, coconut, and sherry varieties, currently hold a smaller share of the market, they offer significant potential for higher margins through their unique and compelling narratives. These evolving dynamics not only intensify competition within the vinegar market but also encourage continuous experimentation and innovation in flavor development.

By Source: Conventional Scale Versus Organic Premiumization

In 2025, conventional manufacturing accounted for 66.83% of the total output, primarily driven by the strong demand from fast-food chains and private-label clients that prioritize cost efficiency. This significant market share is supported by the adoption of bulk ethanol sourcing and industrial farming practices, which effectively lower production costs and enable manufacturers to dominate high-volume distribution channels.

Organic vinegar recorded a 3.66% growth, propelled by the rising consumer preference for clean-label products. Certified organic farms, which strictly avoid synthetic inputs, incur higher production costs. Despite this, retail studies indicate that consumers are willing to pay a premium of 20-40% for products with organic certification, reflecting the growing value placed on sustainability and health-conscious choices. While the market share for organic vinegar is projected to expand, smaller producers face considerable challenges, including the high costs associated with obtaining certification and the increasingly stringent regulations surrounding green claims. These factors could limit their ability to compete effectively in the market.

By Flavor: Unflavored Utility Versus Flavored Innovation

In 2025, unflavored varieties captured a dominant 75.97% share of the market, primarily driven by the widespread use of white distilled and rice vinegars. These vinegar types are highly valued for their neutral acidity, making them a preferred choice in gallon jug formats, particularly among foodservice operators who rely on them for various culinary applications. Despite their strong market presence, the segment faces challenges in achieving higher profitability due to the high level of price transparency, which restricts margin expansion opportunities.

Flavored vinegar is witnessing a consistent growth rate of 3.84% CAGR, fueled by millennials' growing preference for unique and experiential dining experiences. Infused varieties, such as pumpkin-spice, Meyer-lemon, chili, and herb flavors, are increasingly popular and command premium shelf prices that are three to five times higher than those of plain white vinegar. The long-term growth of this segment will depend on the continuous introduction of innovative flavor profiles and economic conditions that support consumer willingness to invest in premium, high-value products.

By Distribution Channel: Retail Reach Versus Foodservice Scale

In 2025, retail contributed 61.08% to global revenue, highlighting its dominant role in the market. Supermarkets are actively leveraging promotional strategies to drive the sales of mainstream brands, while e-commerce platforms are expanding their product offerings to include a wider variety of items, particularly catering to niche markets. Online sales are experiencing the fastest growth, fueled by the increasing penetration of the internet worldwide. For instance, in 2025, 74% of the global population had internet access, an increase from 71% in the previous year, according to data from the International Telecommunication Union[3]Source: International Telecommunication Union, "Key Figure", itu.int.

Foodservice distribution is projected to grow at a faster pace than retail, with a compound annual growth rate (CAGR) of 3.85%. The vinegar market, which supplies products to restaurants, commissaries, and institutional kitchens, is expected to expand further as dine-in traffic rises and quick-service restaurant chains continue to proliferate. The recent capacity expansions by Kikkoman and Mizkan in the United States reflect strong confidence in the long-term growth and resilience of this distribution channel.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 33.98% of the market share, driven by China and Japan. In these countries, rice vinegar has a long-standing tradition, used in applications ranging from sushi seasoning to medicinal tonics. Jiangsu Hengshun Vinegar Industry, a major producer in China, operates traditional fermentation facilities in Zhenjiang. These facilities use time-honored solid-state methods to produce aromatic black vinegar, a key ingredient for dipping and braising. Rising urbanization and increasing disposable incomes are encouraging consumers in cities like Shanghai, Beijing, and Tokyo to upgrade from standard commodity vinegar to premium organic and flavored options. However, the region faces challenges due to its fragmented production base. Thousands of small-scale manufacturers, often lacking modern quality controls, contribute to inconsistencies that hinder export growth and complicate retail assortment strategies.

Europe is projected to grow at a 3.79% CAGR through 2031, the fastest among major regions. This growth is primarily driven by balsamic vinegar exports and strict enforcement of the Protected Geographical Indication, which ensures authenticity. The Consorzio Tutela Aceto Balsamico Tradizionale di Modena monitors compliance with aging and production standards, certifying that only vinegars aged in wooden barrels for at least 12 years can carry the Tradizionale label. Germany and France represent mature markets with stable per-capita consumption, while Eastern European countries are experiencing faster growth due to modernizing retail infrastructures and the adoption of Western food habits. Additionally, the European Food Safety Authority's regulations on organic acids (E260-E263) provide a clear pathway for vinegar's use as a natural preservative, supporting its integration into processed foods.

North America, South America, and the Middle East and Africa collectively represent the remaining market share, each with distinct growth drivers. In North America, the market benefits from a recovery in foodservice and capacity expansions by major players like Kikkoman, with a USD 560 million plant in Wisconsin, and Mizkan's USD 156 million facility in Kentucky. These expansions address bulk demand from chain restaurants and institutional kitchens. The region's well-established retail landscape and strong e-commerce penetration further drive premiumization. Specialty brands such as Bragg and Acid League are gaining significant shelf space in natural food stores and online platforms. In South America, the vinegar market remains underdeveloped relative to its population size, constrained by lower per-capita consumption and competition from alternatives like lime juice and tamarind. Brazil and Argentina are the largest markets, with local producers catering to regional cuisines that emphasize fresh ingredients over preserved condiments. In the Middle East and Africa, demand is gradually emerging. Expatriate communities, Western foodservice chains, and the slow adoption of Mediterranean and Asian cuisines are contributing to this growth. However, challenges such as infrastructure gaps, import tariffs, and limited cold-chain logistics restrict distribution, confining growth mainly to urban centers with established retail networks.

Competitive Landscape

The Global Vinegar Market is moderately fragmented, with multinational players like Mizkan Holdings Co., Ltd., The Kraft Heinz Company, Burg Group B.V., Acetum S.p.A., and Ponti S.p.A. holding a significant share due to their scale economies, extensive distribution networks, and strong brand recognition. At the same time, numerous regional and artisanal producers compete by focusing on authenticity, organic certification, and flavor innovation. Leading producers are increasingly adopting vertical integration strategies, managing fermentation, bottling, and distribution to maximize margins across the value chain. Premiumization is particularly evident in balsamic vinegar, where Protected Geographical Indication enforcement enables Modena producers to command premium pricing. Similarly, in the organic segment, certification costs create barriers that favor established brands with robust compliance capabilities.

Growth opportunities are concentrated in functional beverages, innovative formats, and underserved regions. Ready-to-drink vinegar beverages are still in their early stages outside North America and Europe, offering first-mover advantages to brands that can effectively address regulatory claims and taste challenges. Alternative formats such as gummies, capsules, and powders are expanding vinegar's use beyond cooking, as demonstrated by Bragg's February 2025 gummy launch at Sprouts Farmers Market.

Emerging players like Acid League and Apeal World are utilizing direct-to-consumer channels and social media storytelling to bypass traditional retail barriers, appealing to millennial and Gen Z consumers who prioritize experiential eating over standard condiments. Producers are adopting advanced fermentation technologies, including genomic strain selection, microbial fuel cells, and dry gelatinization. These innovations enhance yield, reduce cycle times, and minimize off-flavors, providing cost and quality advantages that drive market share growth. However, the industry's reliance on agricultural feedstocks and fermentation processes limits the potential for disruptive innovations. Consequently, competition is centered on incremental improvements and brand differentiation rather than transformative breakthroughs.

Vinegar Industry Leaders

-

Mizkan Holdings Co., Ltd.

-

The Kraft Heinz Company

-

Burg Group B.V.

-

Acetum S.p.A.

-

Ponti S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Daily Dose has introduced a cold-pressed Apple Cider Vinegar Shot. The newly unveiled 60ml shot from Daily Dose combines apples, lemon, ginger, agave syrup, and thyme with apple cider vinegar.

- May 2025: Mizkan America invested USD 156 million to expand its Owensboro, Kentucky plant by an additional 320,000 sq. ft. This expanded facility will bolster the production of pasta sauces and vinegar products, featuring well-known brands such as Ragú, Bertolli, and Holland House.

- May 2024: Bragg Live Food Products has rolled out a new 10 oz. size of its Apple Cider Vinegar (ACV) in all 20,000 Dollar General stores across the United States. This move boosts the accessibility of Bragg's ACV, reinforcing the brand's commitment to promoting wellness. In addition to the new size, Bragg also provides ACV in 16-, 32-, 64-, and 128-ounce variants.

- May 2024: De Nigris 1889, a renowned name in the vinegar and glaze industry, introduced the first-ever pumpkin spice vinegar and glaze products to the U.S. market. This launch highlights the company's commitment to innovation in seasonal flavor development and its strategic focus on specialty product positioning.

Global Vinegar Market Report Scope

Vinegar refers to an acidic liquid that is produced by the fermentation of ethanol. The vinegar market is segmented by product type, source, flavor, distribution channel, and geography. By product type, the market is segmented into balsamic, red wine, white, cider, rice, malt, and other. By source, the market is segmented into organic and conventional. By flavor, the market is segmented into flavored and unflavored. By distribution channel, the market is segmented into retail, foodservice, and industrial. By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD) and volume (tons).

By Product Type

| Balsamic Vinegar |

| Red Wine Vinegar |

| White Vinegar |

| Cider Vinegar |

| Rice Vinegar |

| Malt Vinegar |

| Other Product types |

By Source

| Organic |

| Conventional |

By Flavor

| Flavored |

| Unflavored |

By Distribution Channel

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| Foodservice | |

| Industrial |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Balsamic Vinegar | |

| Red Wine Vinegar | ||

| White Vinegar | ||

| Cider Vinegar | ||

| Rice Vinegar | ||

| Malt Vinegar | ||

| Other Product types | ||

| By Source | Organic | |

| Conventional | ||

| By Flavor | Flavored | |

| Unflavored | ||

| By Distribution Channel | Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Foodservice | ||

| Industrial | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the global vinegar market in 2031?

The vinegar market size is forecast to reach USD 8.95 billion by 2031.

Which vinegar type is growing fastest through 2031?

Apple cider vinegar is expected to post a 3.18% CAGR, the quickest among major product categories.

Why is Europe expanding faster than other regions?

Protected Geographical Indication rules that safeguard authentic balsamic vinegar and rising demand for organic condiments are together pushing Europe’s CAGR to 3.79%.

How are companies addressing younger consumer preferences?

Brands are launching low-sugar sparkling vinegar beverages, botanical infusions, and supplement gummies to appeal to millennial and Gen Z shoppers.

Page last updated on: