Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

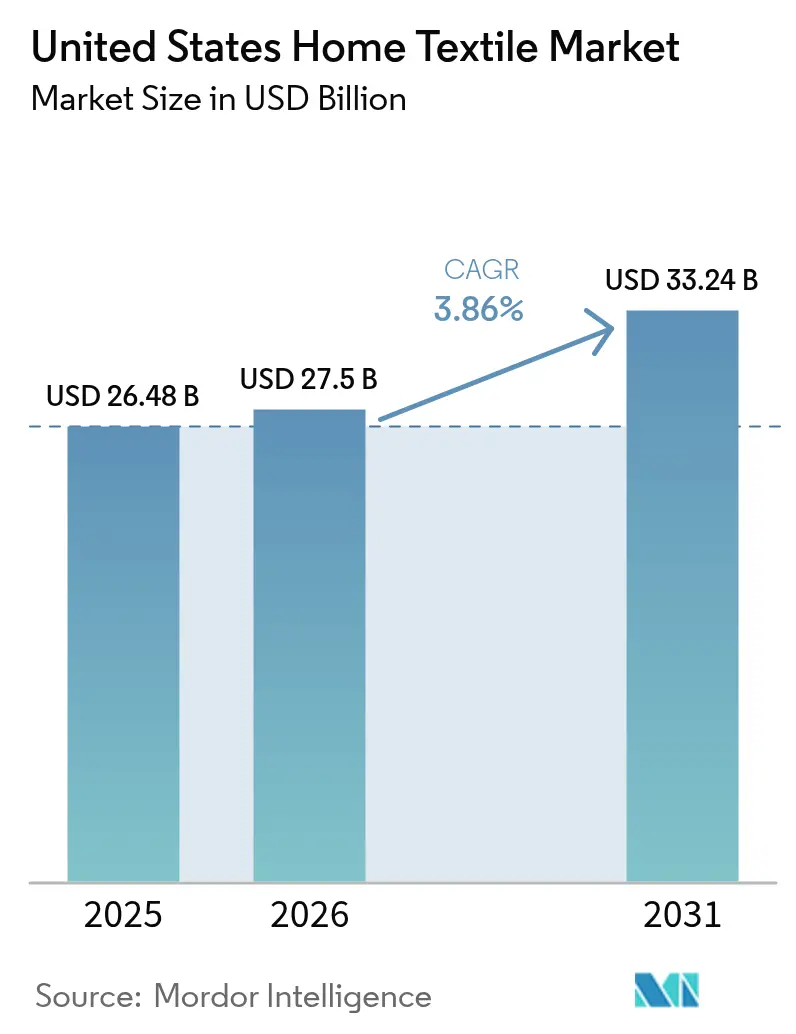

| Base Year Market Size (2025) | USD 26.48 Billion |

| Market Size (2026) | USD 27.5 Billion |

| Market Size (2031) | USD 33.24 Billion |

| Growth Rate (2026 - 2031) | 3.86% CAGR |

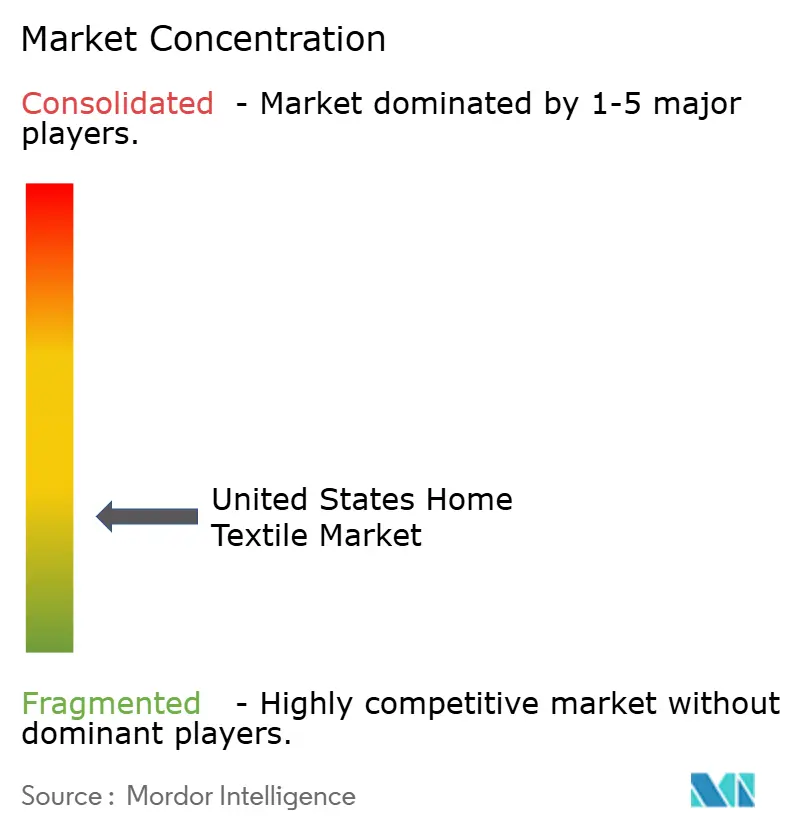

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

United States Home Textile Market Analysis by ���ϲ�����

The United States home textile market size is expected to increase from USD 26.48 billion in 2025 to USD 27.5 billion in 2026 and reach USD 33.24 billion by 2031, growing at a CAGR of 3.86% over 2026-2031. The growth profile reflects a transition from pandemic-era remodeling saturation to steadier replacement-driven demand supported by longer-stay hospitality formats and professional short-term rental operators. Compliance pressures from PFAS restrictions in several states and evolving forced-labor enforcement under the UFLPA are accelerating PFAS-free reformulation and onshore capacity additions across towels, sheets, and upholstery substrates[1]Minnesota Pollution Control Agency Editorial Team, “PFAS in Products Reporting,” Minnesota Pollution Control Agency, pca.state.mn.us. Volatile cotton and input costs continue to complicate pricing and sourcing decisions, keeping procurement cycles disciplined across both retail and institutional channels. At the same time, brands and mills with verified traceability and active sustainability roadmaps are seeing improved access to hospitality contracts and premium retail placements as the United States home textile market rewards compliant and reliable partners.

Key Report Takeaways

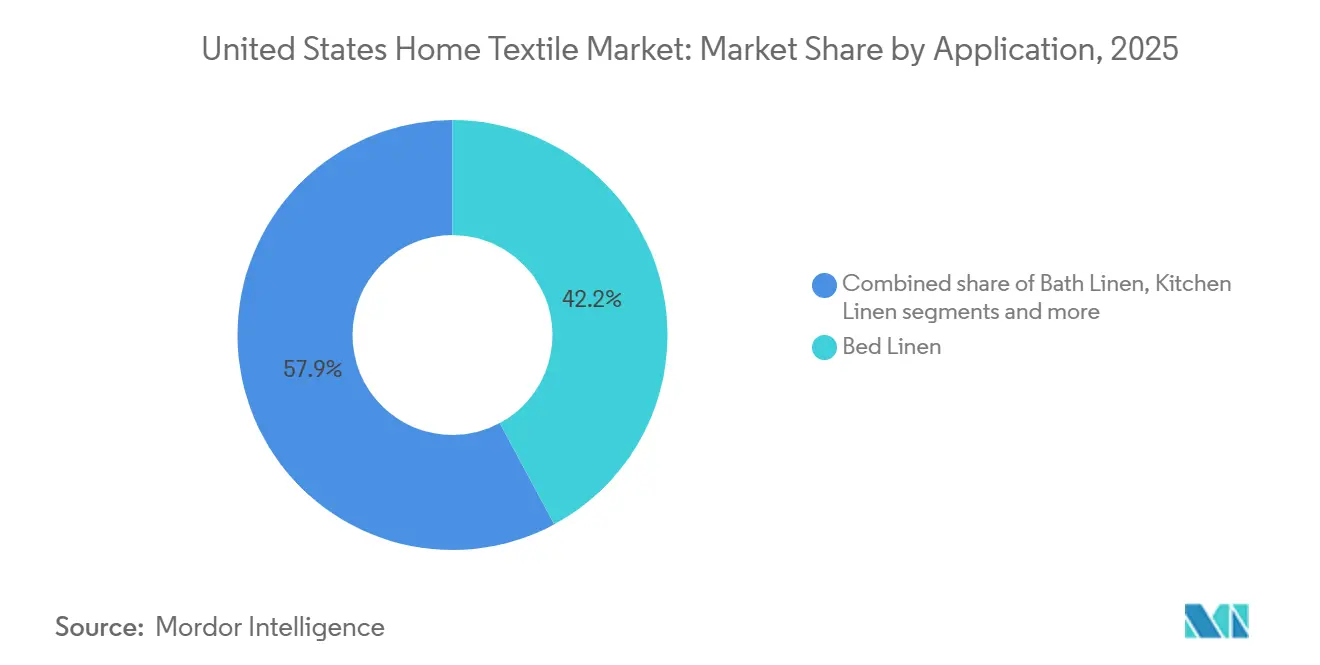

- By application, bed linen led with 42.15% revenue share in 2025 in the United States home textile market, while upholstery is forecast to expand at a 5.31% CAGR through 2031.

- By material, cotton accounted for a 65.90% share in 2025 in the United States home textile market, and linen is projected to grow at a 5.63% CAGR through 2031.

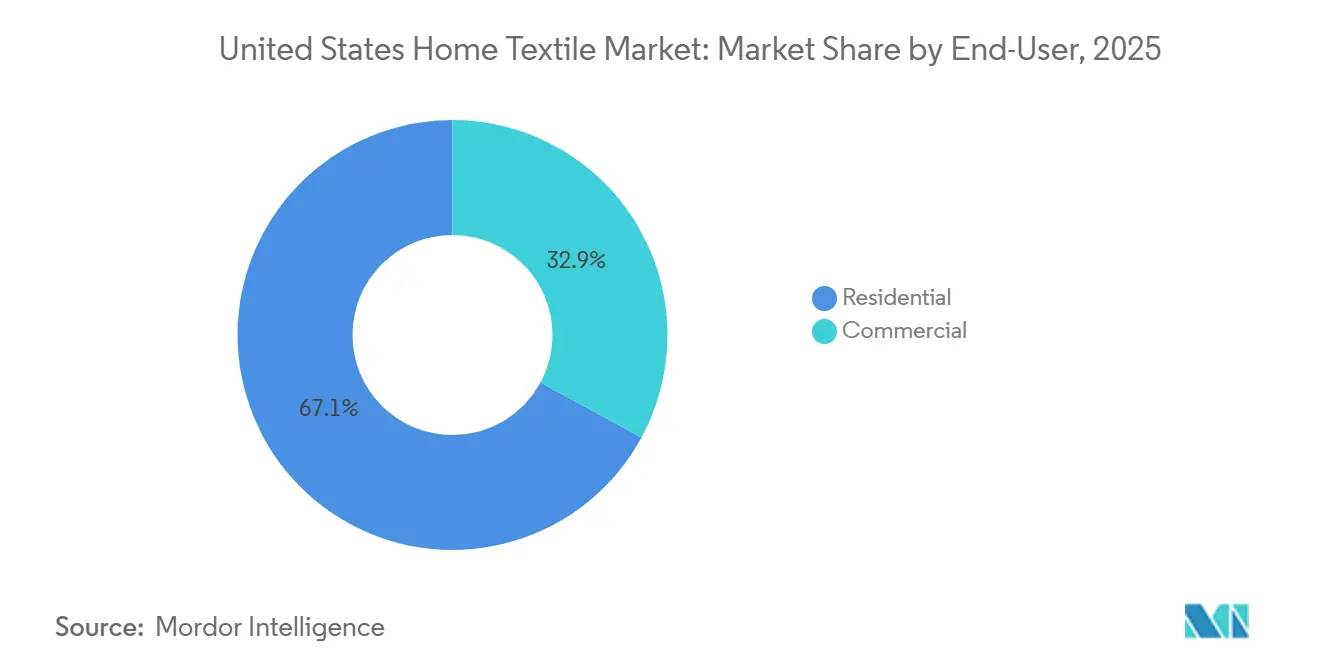

- By end-user, residential held 67.10% of the United States home textile market share in 2025, while commercial is expected to record the highest CAGR at 5.39% through 2031.

- By distribution channel, offline retail held 66.30% of the United States home textile market share in 2025, and online is projected to grow at a 6.20% CAGR through 2031.

- By geography, the Southeast accounted for 28.05% of the United States home textile market in 2025, while the West is expected to grow at a 5.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Home Textile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce and omnichannel adoption accelerate home textile access and convenience | +0.8% | National, with concentration in urban metros and tech-savvy demographics | Medium term (2-4 years) |

| Hospitality pipeline (extended-stay mix) sustains durable bed & bath linen demand | +1.2% | National, with hotspots in Sunbelt metros and gateway cities | Long term (≥ 4 years) |

| Consumer shifts toward natural fibers and certified sustainable textiles | +0.7% | National, early gains in coastal metros and the Western United States | Medium term (2-4 years) |

| PFAS restrictions catalyze PFAS-free finishes and material substitution in home textiles | +0.9% | Multi-state enforcement, cascading to national brands | Short term (≤ 2 years) |

| Climate- and income-driven premiumization pockets in the Western United States bedding | +0.4% | West and select Northeast affluent submarkets | Long term (≥ 4 years) |

| Short-term rental growth increases the frequent turnover of bed & bath linens | +0.6% | National with vacation-rental hubs and urban centers | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

E-commerce And Omnichannel Adoption Accelerate Home Textile Access and Convenience

Direct engagement models in the United States home textile market have set new expectations for product discovery, fulfillment speed, and hassle-free returns, leading to omnichannel rollouts by leading direct-to-consumer brands. Flagship stores that provide tactile product experiences now complement digital storefronts where full assortments and customization options reside, supporting higher conversion while keeping inventory lean. Institutional buyers have also shifted many replenishment orders to online portals, strengthening the role of order management systems and regional warehouse networks in meeting short lead times for hospitality and healthcare accounts. Investments in demand planning, automation, and robotics at United States manufacturing sites are improving service reliability and mitigating disruption risks tied to forced-labor enforcement and import delays. As omnichannel operations mature, subscription programs, curated bundles, and monogramming are driving average order value gains, especially in premium sheets and towels, where the United States home textile market supports repeat purchase behavior and gifting use cases.

Hospitality Pipeline Sustains Durable Bed and Bath Linen Demand

Steady development in longer-stay and select-service hospitality continues to underpin institutional demand for durable cotton-rich sheets, quick-drying towels, and easy-care basics suited to frequent laundering cycles. Procurement outlooks for 2026 indicate modest cost inflation for linens and towels as freight and labor normalize at higher baselines than pre-pandemic levels, which encourages volume commitments and multi-year contracts with integrated suppliers. Suppliers with vertically integrated operations have expanded capacity to serve multinational hotel brands, exemplified by onshore and nearshore investments that reduce transit time and allow faster response to seasonal peaks and room-opening schedules. Domestic manufacturing footprints in facilities across Georgia, Ohio, Texas, and other states are enabling quick prototyping and small-batch runs for hospitality collections that meet sustainability and performance standards without PFAS chemistry. These advantages position integrated players to capture a larger share of bed and bath linen replacements as the United States home textile market prioritizes durability, consistency, and compliance in institutional settings.

Consumer Shift Toward Natural Fibers and Certified Sustainable Textiles

Organic cotton and linen continue to gain traction as consumers seek breathable, low-impact fibers for bedding and bath products, supported by the growing availability of certified options across retail channels. United States organic cotton product sales reached USD 2.5 billion in 2024, up 7.4% year over year, indicating strong consumer acceptance in categories such as sheets and towels, where certification can be clearly communicated. Supply chain readiness has improved as OCS- and GOTS-certified facilities have expanded worldwide through 2023, supporting traceability and labeling needs for brands targeting eco-conscious segments in the United States home textile market. Premium labels have leaned into narratives that combine craftsmanship with natural materials, reinforcing the appeal of linen blends and organic cotton in curated home collections[2]Ralph Lauren Corporate Affairs, “Home Collections and Sustainability,” Ralph Lauren Corporation, corporate.ralphlauren.com. Institutional buyers are also aligning with third-party procurement standards, raising the bar for mills and converters participating in hospitality and healthcare programs that require verified materials. As these certified assortments expand, brands can segment by climate, lifestyle, and aesthetic preferences without sacrificing performance, supporting premiumization within the United States home textile market.

PFAS Restrictions Catalyze PFAS-Free Finishes and Material Substitution

New state-level requirements are forcing suppliers to eliminate intentionally added PFAS in categories such as textile furnishings and upholstered furniture, accelerating reformulation programs and supplier audits for bed, bath, and upholstery lines. Minnesota’s 2026 reporting mandate requires manufacturers to disclose PFAS-containing products and submit ongoing reports, which has driven early testing, supply chain mapping, and documentation protocols. Leading manufacturers have already transitioned away from PFAS in fibers and finishes across multiple product lines, demonstrating the technical feasibility of alternatives for both professional protective and consumer textile applications. In 2025, PFAS- and PVC-free healthcare textiles that match or exceed disposable product performance advanced in the market, giving institutional buyers practical options that meet compliance goals without sacrificing durability. These changes require upfront investments in product development and quality assurance, but they also create space for performance claims that resonate with retailers and hospitality procurement teams, who are moving quickly to meet deadlines. Compliance wins are likely to carry over to national assortments as the United States home textile market consolidates around PFAS-free baselines and verifiable material claims.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cotton and input-cost volatility compress margins and complicate pricing | -0.9% | National, acute for vertically integrated domestic mills | Short term (≤ 2 years) |

| UFLPA forced-labor enforcement disrupts cotton/textile supply chains and leads times | -0.7% | National, concentrated in brands sourcing from China/Southeast Asia intermediaries. | Medium term (2-4 years) |

| Compliance and reformulation costs from chemical restrictions | -0.5% | Multi-state, cascading to national supply chains | Short term (≤ 2 years) |

| Demand cyclicality with remodeling slowdown | -0.6% | National, pronounced in high-mortgage-rate metros | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Cotton And Input-Cost Volatility Compress Margins and Complicate Pricing

Price swings in key fibers and continued increases in freight and labor have introduced uncertainty into cost models for sheets, towels, and upholstery, complicating promotional planning and replenishment strategies. The global cotton balance has been governed by moderate consumption growth and ample inventories, keeping prices range-bound and limiting the pass-through of mill cost relief to retail pricing in the United States home textile market[3]USDA ERS Cotton and Wool Outlook Team, “Cotton and Wool Outlook,” USDA Economic Research Service, ers.usda.gov. These dynamics affect vertically integrated domestic mills most acutely because they must align sourcing, spinning, weaving, and finishing with order cycles that often lock prices six months in advance. Hedging strategies help, but they do not fully offset the combined impact of fiber, wage, and logistics inputs when demand signals are uneven across retail and institutional channels. Brands are therefore prioritizing reliable quality and service levels over aggressive discounting to protect margins in the United States home textile market, which keeps the growth profile steady but limits upside in discretionary categories.

UFLPA Forced-Labor Enforcement Disrupts Cotton/Textile Supply Chains and Lead Times

The Uyghur Forced Labor Prevention Act imposes a rebuttable presumption that goods mined, produced, or manufactured wholly or in part in Xinjiang are ineligible for entry into the United States, requiring importers to document traceability to the fiber level. On January 15, 2025, the Entity List was expanded to add 35 entities across categories that include textile manufacturing and cotton trading, tightening compliance expectations for the United States home textile market. Many importers have adapted by mapping multi-tier suppliers and obtaining origin certificates, production records, and logistics documentation that can withstand review, which has added weeks to procurement cycles in some instances. As a hedge against clearance delays and detention risk, mills and brands have increased onshore or nearshore production and diversified away from higher-risk nodes, which helps stabilize assortments while compliance frameworks mature. This compliance-centric sourcing approach is now embedded in vendor selection and contract renewals across the United States home textile market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Upholstery Outpaces Bed Linen on Multifamily and Compliance Tailwinds

Bed linen accounted for 42.15% of revenue share in 2025, while upholstery is projected to grow the fastest at a 5.31% CAGR through 2031, supported by sustained housing formation and furniture fabric reformulations ahead of PFAS-related deadlines. The bed category remains the anchor of replenishment cycles in the United States home textile market because it spans residential, hospitality, and healthcare settings where replacement frequency is predictable, and hygiene standards are non-negotiable. Hospitality buyers have increased their focus on durability and laundering performance, which keeps cotton-rich percale and sateen constructions central to property standards, with mills leveraging onshore lines for responsive supply. In upholstery and soft furnishings, PFAS-free stain- and soil-resistance technologies are moving from pilot runs into scaled production, prompting accelerated refreshes that are boosting fabric-yardage demand. These dynamics favor integrated suppliers that combine compliant chemistry, strong weaving capacity, and the ability to provide documentation at the article level across bed and furniture textiles in the United States home textile market.

The United States home textile market size concentration in bed products remains high because bed basics are gateway purchases for new households and hospitality openings. Towels, robes, and bathmats continue to ride institutional replacement cycles that value fast-drying characteristics and consistent hand-feel, aligning with the move to PFAS-free baselines in public and private facilities. Category performance is also tied to omnichannel merchandising, where bedding bundles, sheet quality cues, and return-friendly policies support steady sell-through. Upholstery demand benefits from multifamily turnover and living-room refreshes where durable, easy-care fabrics with improved repellency and cleanability are prioritized, even without fluorinated chemistries[4]Milliken Corporate Communications, “PFAS-Free Performance Textiles,” Milliken & Company, milliken.com. Collectively, these factors keep application-level growth diversified across bedrooms, bathrooms, and living spaces, with upholstery set to expand faster than other segments as PFAS-free fabric systems scale in the United States home textile market.

By Material: Linen’s Climate Edge Challenges Cotton’s Volume Lock

Cotton held 65.90% material share in 2025, reflecting cost competitiveness, fabric familiarity, and established spinning and weaving infrastructure, while linen is expected to post the fastest growth through 2031 as premium buyers favor breathable, natural aesthetics. Stable global cotton stocks have tempered price spikes even as mills adjust their order books, keeping cotton the workhorse fiber in sheets and towels within the United States home textile market. Certified organic cotton remains a compelling proposition as consumer education improves and brands invest in merchandising that highlights verifiable product-level benefits. United States organic cotton product sales reached USD 2.5 billion in 2024, which supports further assortment expansion in bedding and bath. At the same time, linen’s appeal is reinforced by its breathability and low-input agronomy profile, which aligns with premium-tier brand stories and climate-adaptive product design. Together, these trends are reshaping material mixes in favor of natural fibers at the premium end of the United States home textile market, while cotton continues to anchor volume at opening and mid-tier price points.

The United States home textile market's size distribution by material also reflects institutional procurement standards that prioritize performance and audit-ready supply chains. Certifications such as GOTS and OCS have expanded their facility footprints, enhanced supply security, and enabled clearer labeling, which supports retail and hospitality compliance goals. Innovation in PFAS-free repellents is closing the performance gap that previously favored synthetics in stain resistance, improving the competitiveness of cotton and linen upholstery. Testing and verification by third-party labs have become routine in material qualification, raising the bar for suppliers and reassuring institutional buyers evaluating large linen programs. As a result, material choices are increasingly tied to climate comfort, certification eligibility, and lifecycle performance, reinforcing a balanced but evolving mix across the United States home textile market.

By End-User: Commercial Gains Traction Via Extended-Stay and Healthcare Replacement Cycles

Residential captured 67.10% of 2025 revenue, while commercial channels are forecast to grow faster through 2031 as extended-stay hotels and healthcare facilities continue to refresh bed and bath textiles at disciplined intervals. Extended-stay formats impose frequent laundering, and durability demands that favor cotton-rich sheets and lower-GSM towel constructions with consistent hand and quick-dry properties, which benefits integrated suppliers that can support property-level standards. Healthcare institutions are adopting PFAS- and PVC-free reusable solutions that meet or exceed disposables on performance, signaling a durable shift in procurement directives and product development. As these institutional preferences harden, vendors with United States manufacturing and rapid-fulfillment capabilities are better positioned to win multi-year contracts in the United States home textile market. Residential channels remain stable as omnichannel retail increases convenience, with premium sheets and towels often serving as focal categories for upgrades and gifting.

Commercial growth is supported by ongoing capacity additions and digitalization across domestic operations, which shorten lead times and reduce logistics complexity. Strategic investments by mills and converters in robotics, AI-driven planning, and warehouse modernization have improved service levels for high-volume accounts in hospitality and healthcare. The United States home textile market reflects this diversification as vendors balance consumer-facing assortment strategies with institutional product lines that emphasize performance specifications and compliance documentation. Residential cycles, however, remain sensitive to mortgage rates and remodeling sentiment, which influences discretionary upgrades in fashion bedding and decorative textiles. Over the forecast window, the net effect is a resilient commercial cadence that steadies overall demand even when consumer spending softens.

By Distribution Channel: Online Gains Share Despite Offline's Entrenched Convenience

Offline channels commanded 66.30% market share in 2025 as mass merchandisers leveraged private-label scale, home centers benefited from project bundling, and specialty stores maintained tactile showroom appeal. Online is forecast to expand at a 6.20% CAGR through 2031, the fastest pace among distribution routes in the United States home textile market, supported by direct-to-consumer store rollouts and regional warehousing that improve service speed. Subscription models that encourage repeat purchases and B2B e-commerce options that enable quick-turn bulk orders are lifting digital throughput even as offline retains strong local presence for urgent replacements. Within offline, mass merchandisers held an estimated 35-40% sub-segment share in 2025, helped by value-focused natural-fiber programs, including 1888 Mills’ October 2025 cotton line that carries the Seal of Cotton, which 79% of consumers trust and 82% associate with sustainability. Home centers captured a mid-teens sub-segment share but are advancing at only 2-3% growth as remodeling slows and large flooring-adjacent categories report softer trends, reflected in Mohawk’s flat net sales of USD 2.8 billion in Q2 2025. Specialty stores hold a low-teens share with 3-4% growth, while other offline formats, such as boutique retailers and outlet malls, together account for a sub-5% aggregate share.

Online penetration reached 33.70% by 2025 after several years of rapid adoption, and while growth moderates, the channel is still projected to expand at a 6.20% CAGR through 2031. In-store evaluation remains influential for premium sheets and plush towels where feel and fit matter, yet digital storefronts manage broader assortments, custom sizing, monogramming, and personalized recommendations at scale. This pairing allows showrooms to serve as high-intent touchpoints while online platforms carry extended variants that are difficult to stock in physical stores.

Geography Analysis

The Southeast accounted for 28.05% of 2025 revenue and remains a high-demand region given population inflows and hospitality exposure, while the West is projected to grow the fastest, with a 5.97% CAGR through 2031. Western states continue to favor natural, breathable materials, which benefits premium-certified lines in bedding and bath, and supports linen’s ascent as a climate-adaptive fiber within the United States home textile market. The Northeast sustains robust demand through luxury retail corridors and hospitality concentration, with premium heritage brands maintaining strong shelf presence across curated home assortments. The Midwest shows steady institutional demand anchored by healthcare and hospitality clients that value domestic manufacturing footprints and short lead times. As compliance with PFAS restrictions and UFLPA documentation requirements intensifies, domestic production nodes across the South and Midwest offer attractive alternatives for category expansion and replenishment.

Regional growth differences also reflect the distribution of premium retail formats and direct-to-consumer showrooms that enable tactile experiences for higher-ticket bedding purchases. Hospitality procurement patterns vary by region, depending on the mix of property types, with extended-stay options driving steady replacement cycles in warm-weather destinations and transit hubs. The Southeast’s scale advantage across both residential and institutional segments secures its leading revenue position in the United States home textile market, while Western momentum is driven by premiumization and climate-aligned product design. The Northeast benefits from international tourism and downtown recovery dynamics that keep hotel assortment standards high, which favors suppliers with luxury-grade programs and reliable logistics. Across regions, verified fiber content and PFAS-free performance have become baseline expectations in new collections, shaping assortments in both retail and institutional channels.

In the forecast window, the West’s outperformance is expected to persist as income growth supports premium bedding and bath purchases and as home fashion trends lean toward lighter, breathable constructions. The Southeast will continue to contribute the largest share of replacement-driven demand tied to population growth and hospitality exposure in key metros. The Northeast and Midwest will benefit from ongoing procurement modernization and nearshore sourcing that reduce cycle times and enhance resilience in the United States home textile market. Regional differences in sustainability adoption rates will narrow as national brands scale certified programs and expand PFAS-free offerings. The net result is a geographically diversified growth pattern that supports steady national expansion through 2031.

Competitive Landscape

The United States home textile market remains fragmented, with leadership concentrated at the category level rather than across the full bed, bath, kitchen, upholstery, and area rug portfolio. Vertically integrated manufacturers have emphasized onshore and nearshore capacity to reduce lead times and improve service reliability for both retail and institutional accounts. Investments in robotics, automation, and analytics are streamlining production and fulfillment, supporting margin defense amid volatility in cotton prices and rising compliance costs. In rugs and flooring-adjacent soft surfaces, scale players continue to optimize networks and product portfolios to align with consumer preferences for performance and value. These moves collectively reflect a focus on operational agility and product credibility as procurement teams and consumers demand verifiable materials and PFAS-free finishes across the United States home textile market.

Strategy has bifurcated into cost leadership and sustainability-led premiumization. Cost leaders leverage integrated mill operations and proximity to end markets to offer competitive pricing and dependable service while maintaining the documentation required for UFLPA and state chemical regulations. Premium-focused brands elevate natural fiber stories and craftsmanship through curated collections and selective distribution, underscoring longevity and traceability. Supplier partnerships with procurement groups and hospitality brands remain a key channel for growth, where demonstrated manufacturing depth and standardized quality protocols win multi-year linen and towel programs in the United States home textile market. At the same time, bundle strategies and personalization in consumer channels support higher average order values while keeping returns manageable through consistent quality and fit.

Several firms have announced or completed capacity additions that expand domestic utility bedding production, enhance fulfillment, or increase product development velocity. One example is a greenfield facility investment in North Carolina that scales pillow output and diversifies United States manufacturing for a global bed linen specialist. Another is the steady push toward robotics and digitalization at major United States bedding producers, which has improved throughput while maintaining stringent quality standards. Category-focused innovation and restructuring continue at scale players in rugs and flooring-adjacent textiles, with targeted savings reinvested in equipment and logistics optimization. In bath and hospitality textiles, new product lines feature recycled content or PFAS-free constructions that meet institutional performance tests, signaling the direction of product development in the United States home textile market.

United States Home Textile Industry Leaders

Welspun Living (Welspun USA)

Mohawk Industries

American Textile Company

Standard Textile

WestPoint Home

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Standard Textile launched a Terry Collection with recycled cotton content in partnership with a UK laundry services provider to advance circularity in hospitality.

- October 2025: 1888 Mills and Cotton Incorporated unveiled a 100% cotton bath and bedding collection targeting opening price points and highlighting the Seal of Cotton trademark to address consumer interest in natural fiber alternatives.

United States Home Textile Market Report Scope

Home textiles can be defined as textiles used for home furnishing. It consists of a various range of functional as well as decorative products mainly used in decorating our houses. The fabrics used for home textiles consist of both natural and man-made fibers. This report aims to provide a detailed analysis of the US Home Textile Industry. The report focuses on the market dynamics, emerging trends in the segments, and insights into various product and application types. Also, it analyzes the key players and competitive landscape. The United States Home Textile Market is segmented by product (Bed Linen, Bath Linen, Kitchen Linen, Upholstery, and Floor Covering) and by distribution channel (Supermarkets & Hypermarkets, Specialty Stores, Online, and other distribution channels). The report offers market size and values in (USD million) during the forecast years for the above segments.

By Application

| Bed Linen |

| Bath Linen |

| Kitchen Linen |

| Upholstery |

| Others (Carpets & Area Rugs) |

By Material

| Cotton |

| Linen |

| Synthetic Fibres |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| Offline | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | |

| Specialty Stores | |

| Other Offline Channels | |

| Online |

By Region

| Northeast |

| Midwest |

| Southeast |

| Southwest |

| West |

| By Application | Bed Linen | |

| Bath Linen | ||

| Kitchen Linen | ||

| Upholstery | ||

| Others (Carpets & Area Rugs) | ||

| By Material | Cotton | |

| Linen | ||

| Synthetic Fibres | ||

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | Offline | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | ||

| Specialty Stores | ||

| Other Offline Channels | ||

| Online | ||

| By Region | Northeast | |

| Midwest | ||

| Southeast | ||

| Southwest | ||

| West | ||

Key Questions Answered in the Report

What is the current size and growth outlook of the United States home textile market to 2031?

The United States home textile market size was USD 26.48 billion in 2025 and is projected to reach USD 33.24 billion by 2031 at a 3.86% CAGR during 2026-2031.

Which product categories are leading, and which are growing fastest in the United States home textile market?

Bed linen led with 42.15% market share in 2025, while upholstery is forecast to expand at the fastest pace with a 5.31% CAGR through 2031.

How are PFAS regulations changing sourcing and product development for the United States home textiles?

State reporting and restrictions are pushing PFAS-free finishes and material substitution, leading brands and mills to reformulate chemistries, expand testing, and document compliance across bed, bath, and upholstery lines.

What end-user channels are driving growth in the United States home textile market?

Residential accounted for 67.10% of 2025 revenue, while commercial channels, led by extended-stay hospitality and healthcare replacement cycles, are projected to grow faster at 5.39% through 2031.

What materials trends are most important for United States home textile buyers?

Cotton remains the volume leader at 65.90% share, while certified organic cotton and linen are rising, driven by verified sustainability claims and climate-adaptive comfort, particularly in premium bedding and bath.

Page last updated on: