Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

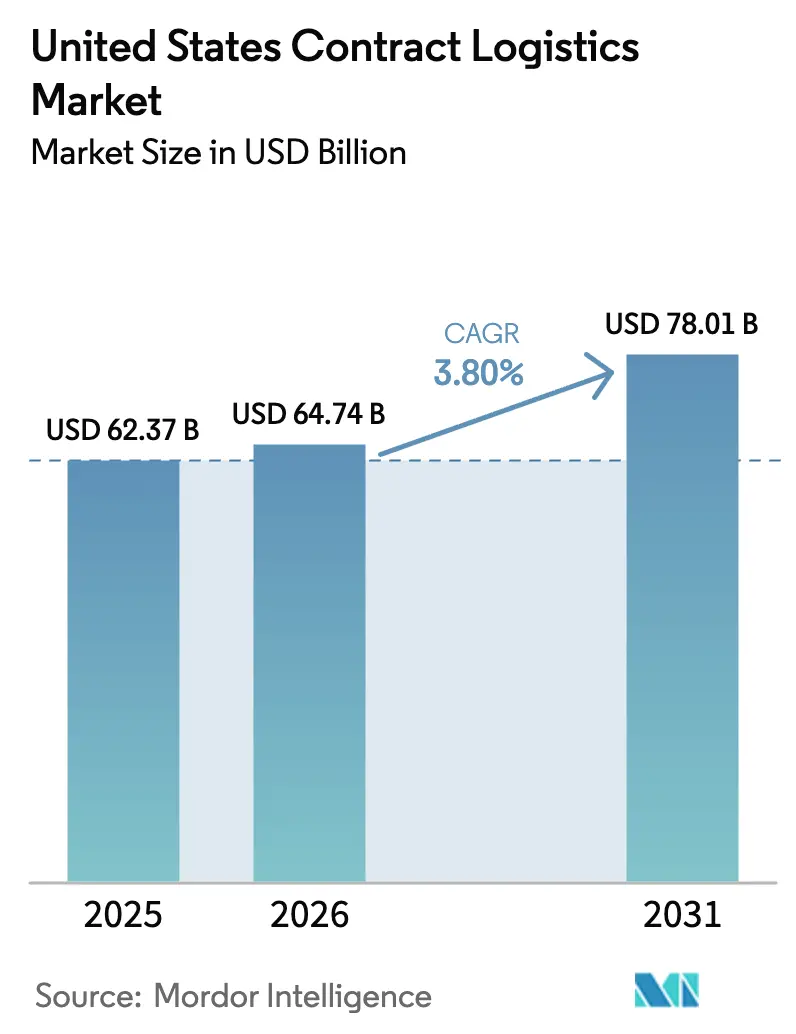

| Base Year Market Size (2025) | USD 62.37 Billion |

| Market Size (2026) | USD 64.74 Billion |

| Market Size (2031) | USD 78.01 Billion |

| Growth Rate (2026 - 2031) | 3.80% CAGR |

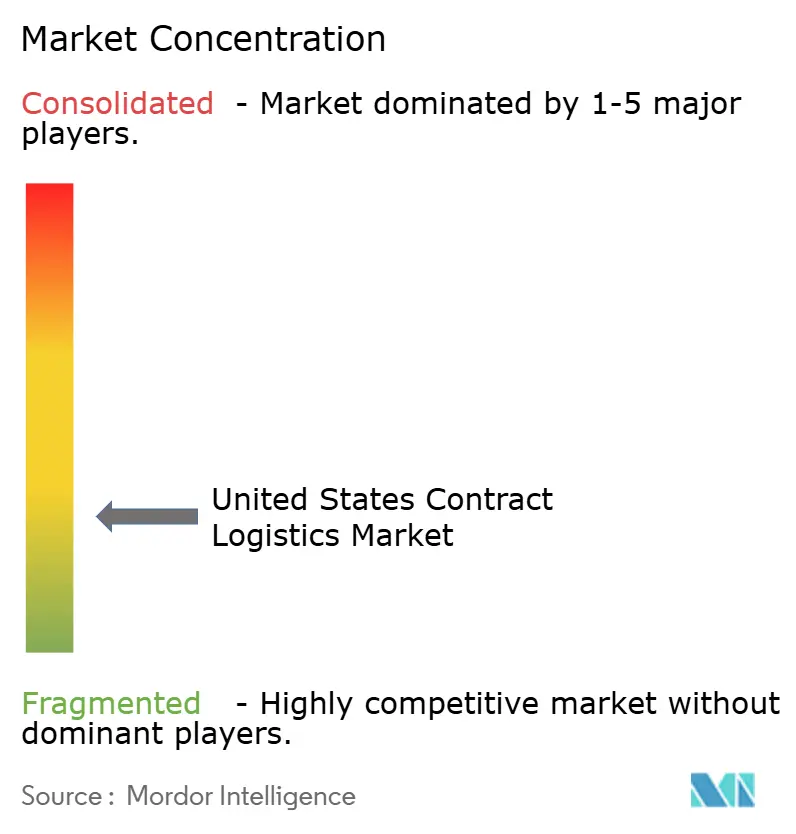

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

United States Contract Logistics Market Analysis by ���ϲ�����

The United States Contract Logistics Market size was valued at USD 62.37 billion in 2025 and estimated to grow from USD 64.74 billion in 2026 to reach USD 78.01 billion by 2031, at a CAGR of 3.80% during the forecast period (2026-2031).

The United States contract logistics market as a maturing arena where profitability hinges more on efficiency than on sheer shipment volume. Ongoing migration from in-house operations to outsourced models accelerates demand, especially as manufacturers adopt Build-to-Order strategies and retailers confront an unrelenting wave of reverse-logistics traffic sparked by e-commerce returns. Near-shoring to Mexico, the largest U.S. trading partner in 2024 with USD 839.9 billion in bilateral flows, reconfigures cross-border networks and underscores the geographic breadth of the United States contract logistics market. Simultaneously, Amazon’s USD 4 billion rural-delivery build-out, slated to triple its delivery-station count by 2026, is redefining last-mile economics in non-urban zones. Automation investments—from warehouse robotics to AI-enabled orchestration—now generate the lion’s share of productivity gains as providers anticipate labor shortages and rising cybersecurity compliance costs.

Key Report Takeaways

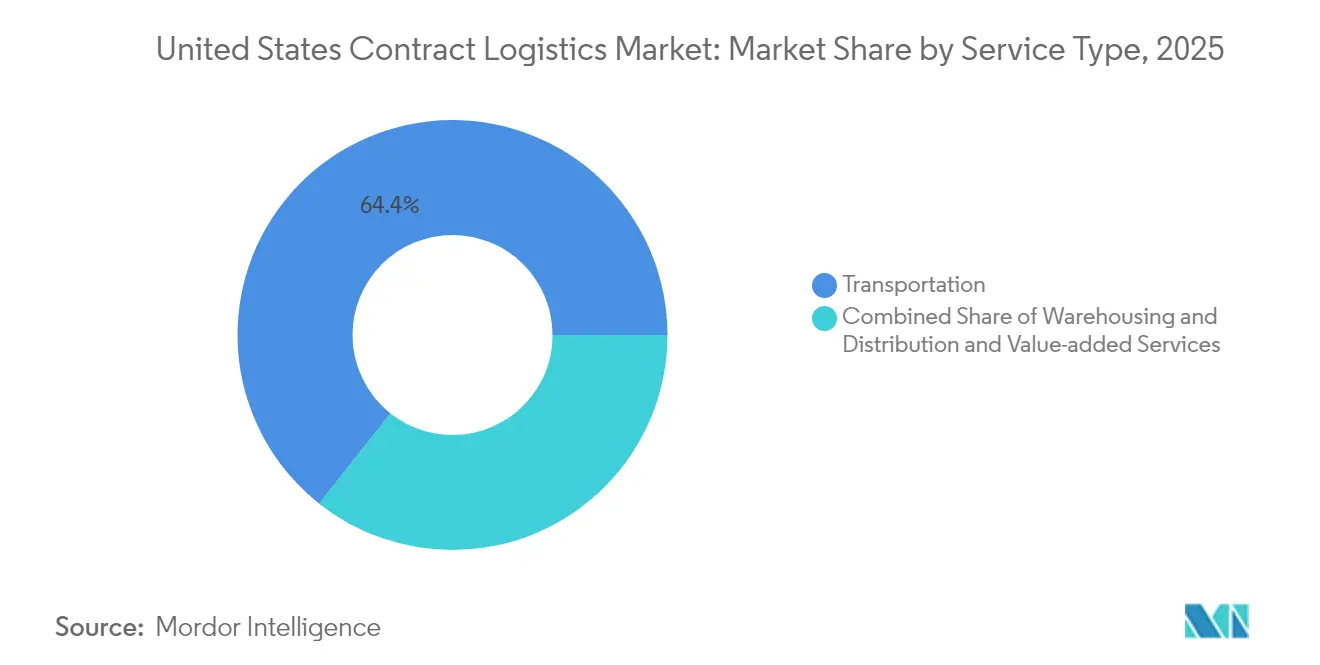

- By service type, transportation captured 64.35% of the United States contract logistics market share in 2025. Warehousing & Distribution is projected to advance at a 3.12% CAGR through 2031.

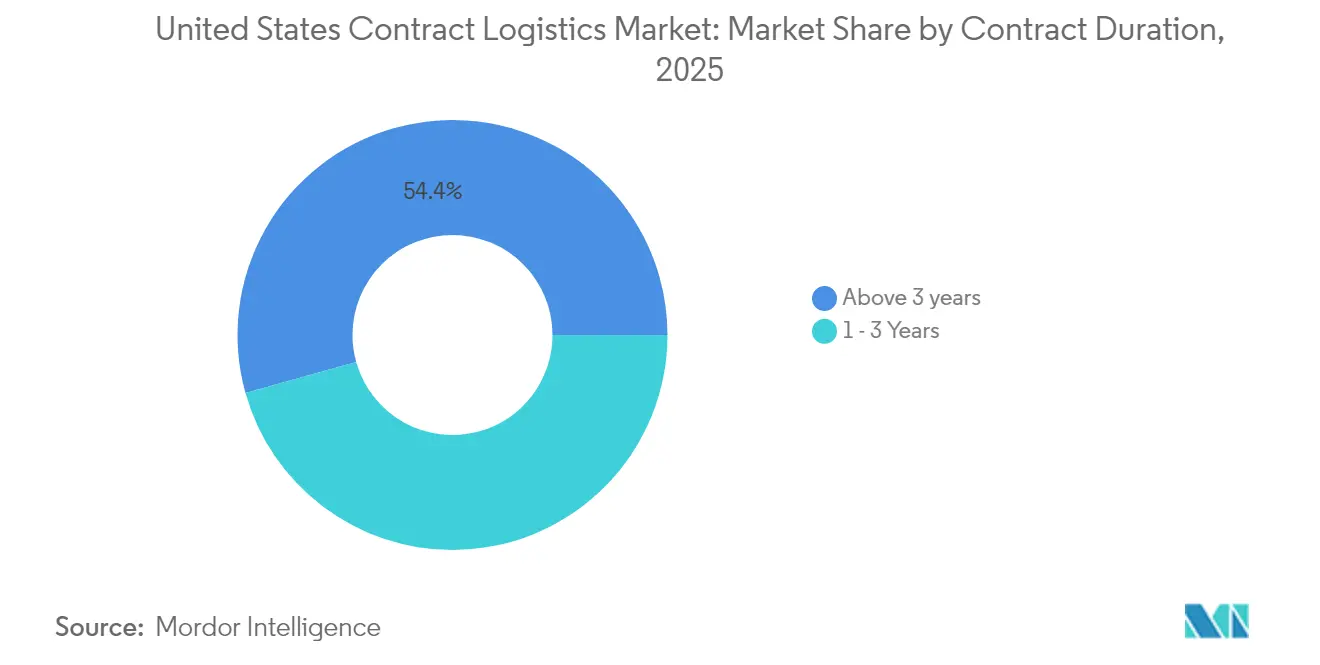

- By contract duration, above-3-year agreements accounted for 54.35% of the United States contract logistics market size in 2025 and are forecast to grow at a 3.63% CAGR through 2031.

- By end user, retail & e-commerce maintained 25.60% revenue share in 2025; healthcare & pharmaceuticals are poised to expand at 4.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Contract Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive e-commerce fulfillment demand | +1.2% | National; Southeast Golden Triangle | Short term (≤ 2 years) |

| Surge in cold-chain & healthcare logistics | +0.8% | National metros | Medium term (2-4 years) |

| Automation-first warehouses & AI orchestration | +0.6% | National hubs | Long term (≥ 4 years) |

| Near-shoring to Mexico boosting cross-border flows | +0.5% | Southwest border corridor | Medium term (2-4 years) |

| OEM shift to Build-to-Order models | +0.4% | Midwest and Southeast | Medium term (2-4 years) |

| Exploding reverse-logistics volumes | +0.3% | National e-commerce nodes | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Explosive e-commerce fulfillment demand

Persistent online shopping makes inventory velocity a year-round constraint. Amazon delivered more than 9 billion items via same-day and next-day services in 2024, a 30% year-over-year jump[1]Lauren Forristal, “Amazon to Spend over $4B to Expand Prime Delivery,” techcrunch.com. Rural penetration covering 4,000+ small towns reshapes network topology, compelling contractors to craft micro-fulfillment and flexible capacity models. Walmart’s closure of a legacy fulfillment site while opening automated centers that cut 12 process steps to 5 shows how speed trumps footprint. DOT hours-of-service regulations further dictate route planning, forcing compliance-aligned shifts in facility location. The United States contract logistics market continues to funnel capital into real-time visibility and short-haul transport solutions that shrink order-to-delivery windows.

Surge in cold-chain & healthcare logistics

DHL’s USD 1.1 billion North American outlay illustrates how temperature-controlled know-how has evolved into an entry barrier[2]Keiron Greenhalgh, “DHL to Invest $1.1B in Health Care Logistics,” ttnews.com. Acquisitions such as Cryopdp, which handles 600,000 clinical-trial moves yearly, exemplify the push toward white-glove services for cell-and-gene therapies requiring sub-zero maintenance. The FDA Good Distribution Practice mandates now attach steep penalties to temperature excursions, compelling providers to deploy IoT sensors and redundant power. The United States contract logistics market, therefore, prizes GDP-certified space and trained personnel, with cold-chain square footage like Cold Zone’s 170,000-sq-ft Springfield site signaling further expansion.

Automation-first warehouses & AI orchestration

Productivity gains stem from orchestration software that blends people, mobile robots, and fixed automation. Amazon’s Proteus AMRs and Cardinal sorters illustrate multi-class robotics integration. GXO’s partnership with Blue Yonder spans 1,000+ sites and underlines the software’s role in lowering variable cost per unit. Robotics-as-a-Service models open the technology door for mid-tier firms, although technical-integration talent remains scarce. The United States contract logistics market increasingly rewards providers that convert automation data into real-time labor, cube, and routing optimization.

Near-shoring to Mexico boosting cross-border flows

U.S.–Mexico trade volumes underscore structural supply-chain realignment, lifting cross-border trucking and intermodal demand. BMW’s USD 800 million battery plant adjacent to San Luis Potosí assembly lines typifies OEMs co-locating parts and final-assembly sites across the border. The CP-KC rail merger provides a single-line network from Canada to Mexico, further integrating North American freight paths. Compliance with USMCA rules of origin plus Mexican labor standards favors incumbents that already field bilingual brokerage and bonded-warehouse capacity within the United States contract logistics market.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute warehouse & driver labor shortages | -0.9% | Midwest and Southeast | Short term (≤ 2 years) |

| Fuel-price and freight-rate volatility | -0.6% | National | Short term (≤ 2 years) |

| Coastal port realignments creating network risk | -0.4% | East and West Coast | Medium term (2-4 years) |

| Rising cybersecurity & data-privacy costs | -0.3% | Major logistics hubs | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Acute warehouse & driver labor shortages

FMCSA English-proficiency rules, effective June 2025, risk sidelining 10% of drivers, lifting tender rejections, and tightening capacity. Transportation and warehousing hiring added 14,000 positions in July 2024, yet 51% driver turnover undermined headcount stability. Wage inflation persists as Amazon’s rural delivery wages far exceed federal minimums. Shortfalls are profound in CDL-A and hazmat-certified positions, directly constraining healthcare and chemical freight lanes within the United States contract logistics market.

Fuel-price and freight-rate volatility

Despite 2024 diesel falling to USD 0.553 per mile, total operating cost hit USD 2.26 per mile as equipment and financing expenses climbed[3]David Hollis, “Operating Costs Reach Record High,” truckersnews.com. California diesel could top USD 6.00 per gallon after July 2025 tax hikes, adding regional complexity. Flat tonnage indices curb carriers’ ability to levy surcharges, compressing margins for contract logistics operators locked into fixed-rate agreements scattered across the United States contract logistics market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominance Faces Automation Pressure

Transportation claims 64.35% of the United States contract logistics market share in 2025, buoyed by road carriers that moved 72.2% of U.S.–Mexico freight. Yet, warehousing & distribution is growing faster at 3.12% CAGR as e-commerce demands distributed inventory that elevates storage-and-pick services. Rail’s single-line Canada-to-Mexico network following the CP-KC merger improves intermodal reliability, although market power concentration may raise rates. Air lifts time-sensitive cargo but remains vulnerable to fuel swings. Sea lanes gain from port upgrades but confront labor-automation gridlock.

Warehouse square footage receives disproportionate capital as automation boosts pick rates and slot-density. Amazon’s shift from March Air Reserve Base to San Bernardino proves network fluidity. Veritiv’s USD 60 million AmeriPac buy points to a strong appetite for value-added kitting, assembly, and postponement processes that lock in customers during seasonal bursts. These services carry higher margins than pure transport and reduce revenue volatility across the United States contract logistics market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Contract Duration: Long-term Partnerships Accelerate

Above-3-year contracts held 54.35% share of the United States contract logistics market size in 2025 and are tracking 3.63% CAGR, demonstrating shippers’ appetite for strategic continuity under supply-chain volatility. DHL’s multi-year Blue Yonder deployment exemplifies long-cycle automation ROI that only extended deals justify. Capital-intensive cold-chain nodes also rely on durable revenue streams.

Contracts of 1-3 years still attract firms piloting new regions or coping with cyclical peaks, yet growth lags as performance risk looms. DoD’s cancellation of its Global Household Goods Contract illustrates the disruption risk in shorter deals. OEM margin pressures push Build-to-Order strategies, needing deep provider collaboration over multiple years. The tilt toward longer commitments effectively raises market entry barriers within the United States contract logistics market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Healthcare Leads Growth Acceleration

Healthcare & pharmaceuticals is the fastest riser at 4.02% CAGR, propelled by biologics and aging demographics that require GDP-certified storage. DHL’s plan to grow healthcare revenue 50% by 2030 through USD 1.1 billion in regional investments validates the sector’s pull. Cryogenic therapies demand constant -150 °C environments, compelling real-time telemetry and specialized packaging.

Retail & e-commerce retains the highest revenue at 25.60%, driven by omni-channel fulfillment complexity. Manufacturing & automotive gains from near-shored component flows, yet compressing OEM margins spur cost-sharing models. Food & beverage benefits from cold-chain densification, such as Coca-Cola’s USD 17 million Waco hub. Chemicals trade bolsters hazmat niches where compliance acumen matters. Together, these trends diversify the United States contract logistics market and cushion sectoral slowdowns.

Geography Analysis

The Southeast “Golden Triangle” dominates the United States contract logistics market, lying within a day’s drive of 70% of the population and over half of the national GDP. Five of seven Class I railroads cross the region, underpinning resilient intermodal options. Favorable labor costs and proliferating manufacturing projects make the corridor a magnet for warehouse construction and automation integrations.

Texas anchors Southwest momentum as the principal gateway for USD 839.9 billion in U.S.–Mexico trade, reinforcing demand for customs-bonded facilities and bilingual brokerage. Load balancing between Laredo and alternative ports of entry strains drayage capacity, triggering Ryder’s expanded yard supporting 250,000 annual border moves.

Competitive Landscape

Market concentration remains moderate, with global integrators and technologically advanced specialists setting the competitive agenda. DHL’s acquisition of Inmar catapults it atop reverse-logistics rankings while its healthcare outlays deepen vertical integration. GXO’s enterprise-wide Blue Yonder rollout showcases software-centric competitiveness, whereas Amazon’s robotics stack demonstrates scale advantages in multi-class automation.

DSV’s EUR 14.3 billion (USD 14.9 billion) purchase of DB Schenker doubles revenue, forging the world’s largest logistics provider and raising competitive benchmarks for integrated services. FedEx’s planned spinoff of its LTL unit indicates a strategic refocus, potentially inviting acquirers to consolidate line-haul capacity. Regional operators, exemplified by Patton Logistics Group, continue bolt-on acquisitions to reach density thresholds that enable dedicated fleets and shared automation.

Strategic whitespace surfaces in cold-chain, hazardous materials, and AI-orchestrated micro-fulfillment. UPS’s MedSpeed buyout augments its healthcare footprint. Penske and Werner expand dedicated automotive and regional facilities to secure OEM contracts. The United States contract logistics market consequently rewards providers that blend compliance readiness, technology acumen, and geographic reach.

United States Contract Logistics Industry Leaders

DHL Supply Chain

XPO Logistics

GXO Logistics

Ryder Supply Chain Solutions

FedEx Logistics

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: GXO Logistics entered a multi-year strategic partnership with Blue Yonder to deploy advanced warehouse-management software across more than 1,000 sites.

- April 2025: DSV completed its EUR 14.3 billion (USD 14.9 billion) purchase of DB Schenker, creating the world’s largest logistics company by revenue.

- April 2025: DHL unveiled a USD 1.1 billion five-year outlay to scale North American healthcare logistics infrastructure.

- June 2024: Ryder opened a 228,000-sq-ft warehouse and expanded its Nuevo Laredo drayage yard to manage 250,000 annual border moves.

United States Contract Logistics Market Report Scope

Contract logistics refers to the process of outsourcing resource management tasks to a third-party company. In addition, the companies involved in this market handle activities such as designing and planning supply chains, designing facilities, warehousing, transporting and distributing goods, processing orders and collecting payments, managing inventory, etc. The report provides a comprehensive background analysis of the United States contract logistics market. It covers the assessment of the economy and the contribution of various sectors, offers an overview of the market, estimates the market size for key segments, highlights emerging trends, and discusses market dynamics and geographical trends.

The United States contract logistics market is segmented by type (outsourced and insourced), by end user (manufacturing and automotive, consumer goods and retail, high-tech, healthcare, and pharmaceuticals other end users (energy, construction, aerospace, etc.)). The report offers market size and forecasts in value (USD) for all the above segments.

By Service Type

| Transportation | Road |

| Rail | |

| Air | |

| Sea | |

| Warehousing & Distribution | |

| Value-added Services (Assembly, Labelling, Kitting) |

By Contract Duration

| 1 – 3 Years |

| Above 3 years |

By End-user Industry

| Manufacturing & Automotive |

| Food & Beverage |

| Retail & E-commerce |

| Healthcare & Pharmaceuticals |

| Chemicals |

| Other Industries |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea | ||

| Warehousing & Distribution | ||

| Value-added Services (Assembly, Labelling, Kitting) | ||

| By Contract Duration | 1 – 3 Years | |

| Above 3 years | ||

| By End-user Industry | Manufacturing & Automotive | |

| Food & Beverage | ||

| Retail & E-commerce | ||

| Healthcare & Pharmaceuticals | ||

| Chemicals | ||

| Other Industries |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the United States contract logistics market?

The sector is valued at USD 64.74 billion in 2026.

How fast is the sector expected to grow through 2031?

A forecast CAGR of 3.80% should lift revenue to USD 78.01 billion by 2031.

Which service type is expanding quickest?

Warehousing & distribution is projected to post the fastest growth at 3.12% CAGR.

Why are longer-term contracts gaining traction?

Shippers seek supply-chain stability and ROI on automation, boosting above-3-year agreements to 54.35% share.

Which end-user vertical shows the strongest momentum?

Healthcare & pharmaceuticals leads with an anticipated 4.02% CAGR, reflecting cold-chain demand.

How is near-shoring influencing U.S. logistics networks?

U.S.–Mexico trade of USD 839.9 billion in 2024 is shifting capacity toward the Southwest corridor.