Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

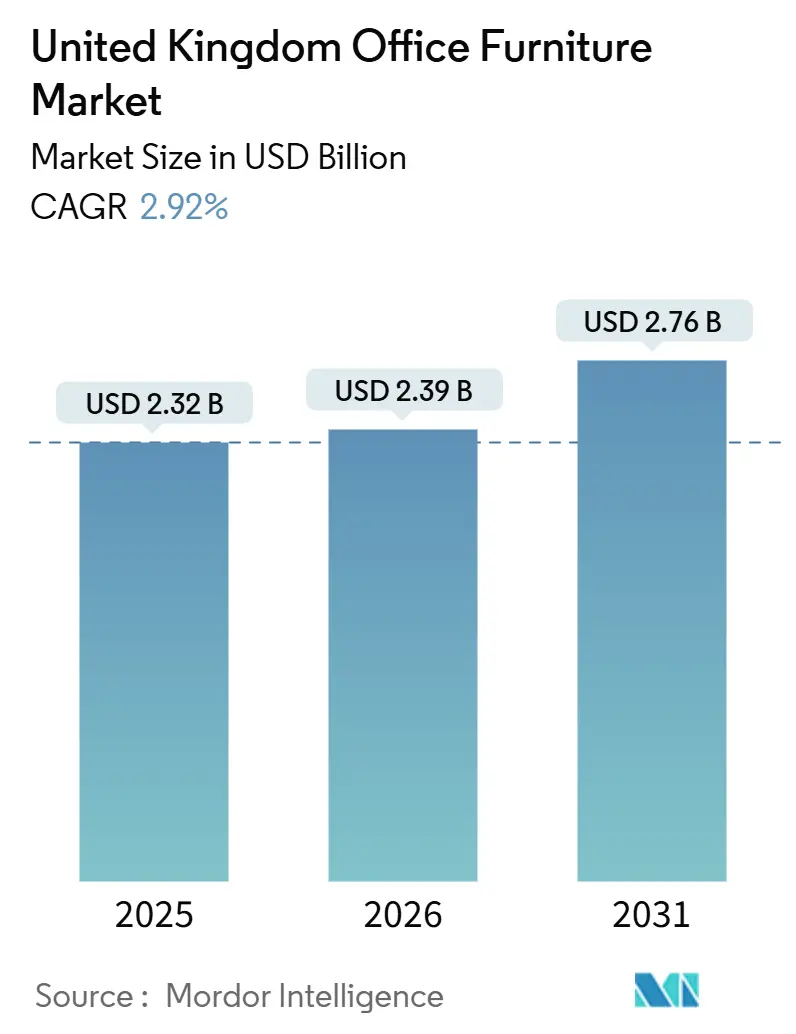

| Base Year Market Size (2025) | USD 2.32 Billion |

| Market Size (2026) | USD 2.39 Billion |

| Market Size (2031) | USD 2.76 Billion |

| Growth Rate (2026 - 2031) | 2.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Office Furniture Market Analysis by ���ϲ�����

The United Kingdom office furniture size stood at USD 2.39 billion in 2026, up from USD 2.32 billion in 2025, and is projected to reach USD 2.76 billion by 2031 at a 2.92% CAGR. The United Kingdom office furniture market is positioned for steady growth as regulatory compliance, hybrid-era workspace redesign, and sustainability requirements shape procurement priorities, with buyers standardizing ergonomic task chairs and adjustable desks. Heightened focus on public-sector frameworks and lifecycle documentation, along with demand for suppliers that can evidence Environmental Product Declarations and verified take-back schemes, is changing how specifications are written and evaluated. Domestic manufacturing remains a differentiator for projects that value assured lead times and shorter logistics chains, with vertically integrated suppliers benefiting from tighter control over finishes and components. Employers’ legal duty to assess display screen setups for onsite and home-based users sustains ongoing ergonomic upgrades, even as headcount or footprints shift, anchoring resilient category demand. Public-sector procurement through the Crown Commercial Service’s Furniture and Associated Services 2 framework embeds carbon-reduction plans, packaging rules, and social-value scoring into supplier selection, favoring manufacturers with traceable materials and documented take-back programs[1]Crown Commercial Service, “Furniture and Associated Services 2 (RM6308),” Crown Commercial Service, crowncommercial.gov.uk .

Key Report Takeaways

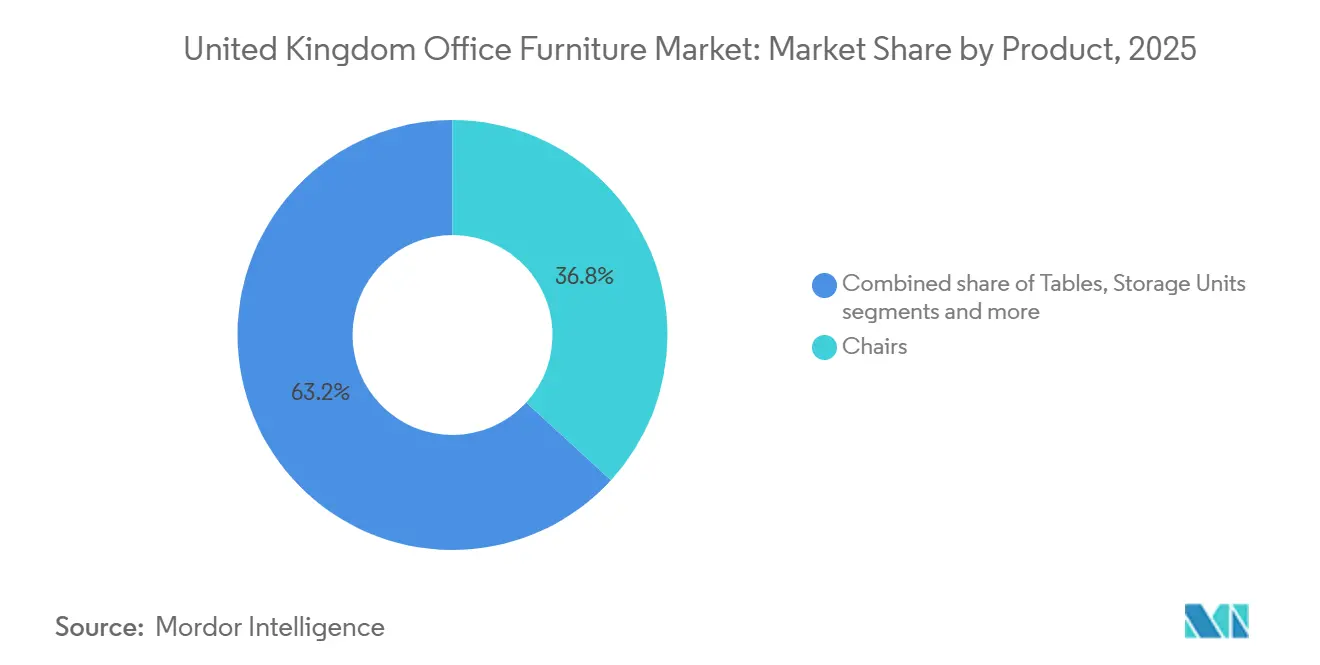

- By product category, chairs led with 36.80% of the United Kingdom office furniture market share in 2025, while booths and office dividers are projected to expand at a 3.62% CAGR through 2031.

- By material, wood accounted for 39.25% of the United Kingdom office furniture market share in 2025, while plastic and polymer registered the highest projected CAGR at 3.23% to 2031.

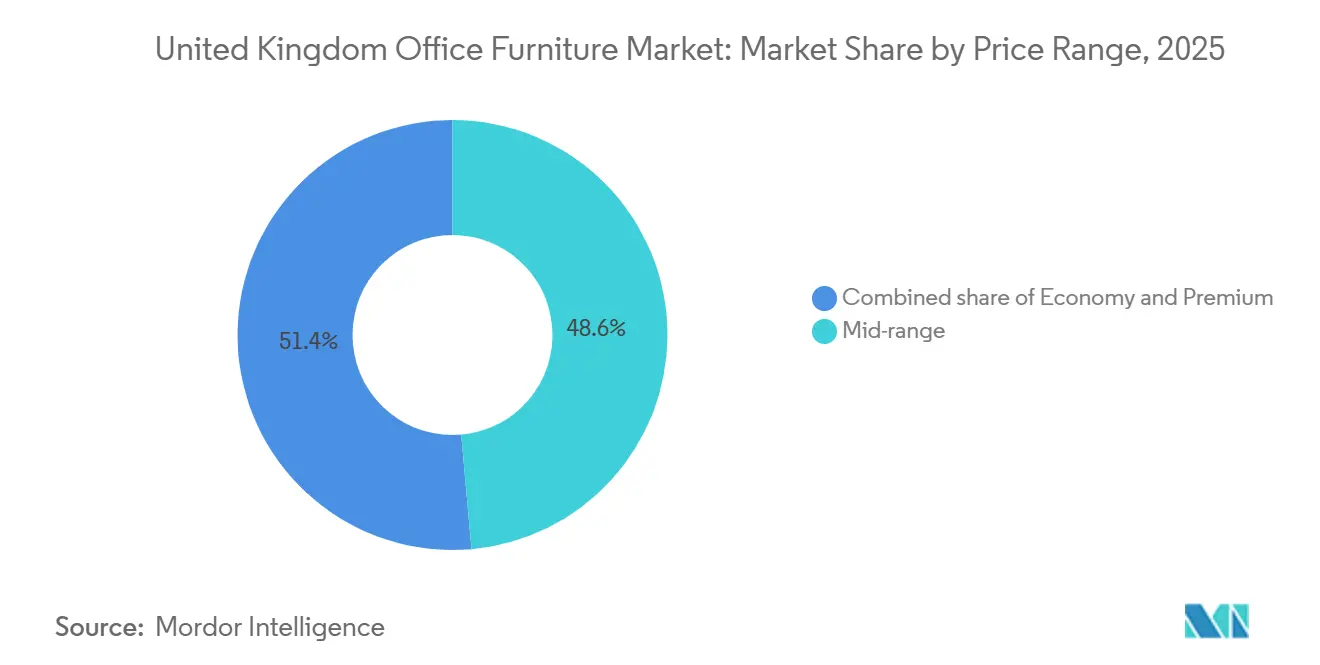

- By price range, mid-range commanded 48.60% of the United Kingdom office furniture market share in 2025, while premium is forecast to grow at a 2.98% CAGR through 2031.

- By end-user, corporate offices held 61.35% of the United Kingdom office furniture market share in 2025, while healthcare offices are advancing at a 2.54% CAGR to 2031.

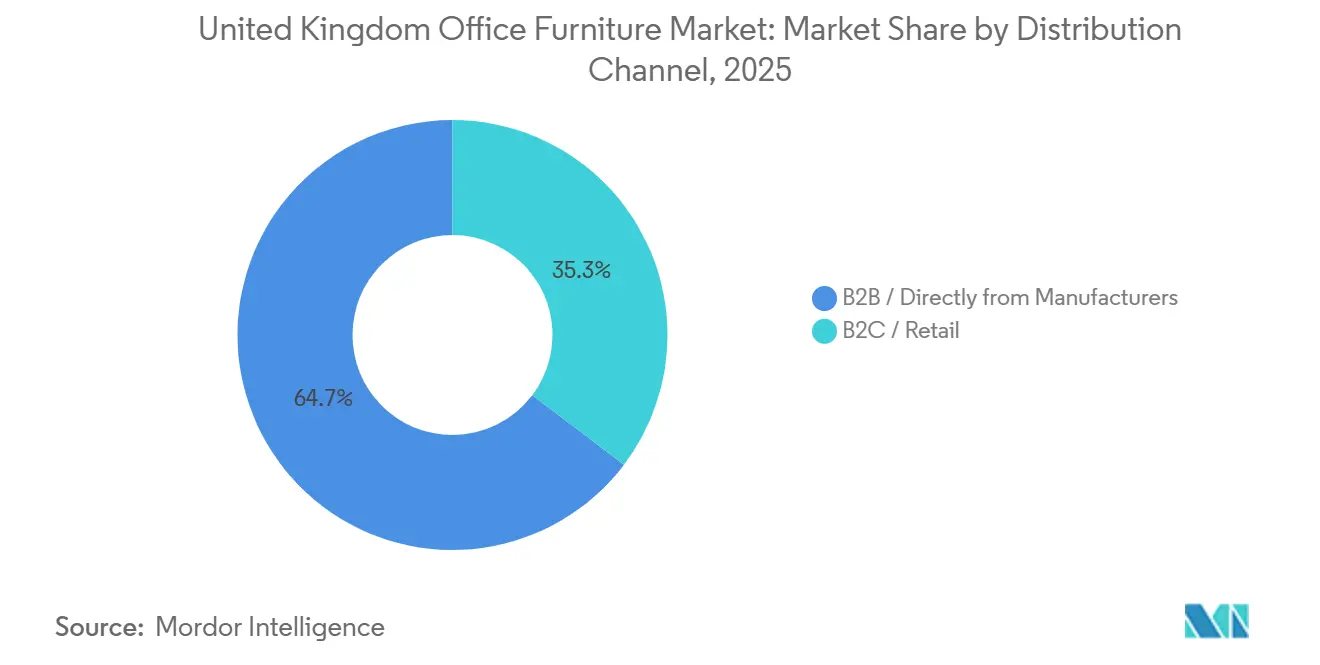

- By distribution channel, B2B direct from manufacturers is estimated at 64.67% of the United Kingdom office furniture market share in 2025, while B2B / Directly from Manufacturers recorded the fastest projected CAGR at 3.41% through 2031.

- By geography, England accounted for 82.40% of the United Kingdom office furniture market share in 2025, while Scotland recorded the fastest projected CAGR at 1.95% through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Office Furniture Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compliance-Driven Ergonomics and DSE Readiness | +0.8% | National, with enforcement escalating in Scotland and Wales | Medium term (2-4 years) |

| Flight-To-Quality Workplaces and Post-2024 Redesign Programs | +0.7% | London, Manchester, Birmingham, Edinburgh, Bristol CBDs | Short term (≤ 2 years) |

| Public-Sector Procurement Via CCS Frameworks and Hubs | +0.5% | National, with NHS estates and education sectors leading | Medium term (2-4 years) |

| Sustainability Certifications and Circular Procurement (BREEAM, SKA, WELL, WRAP) | +0.4% | National, concentrated in FTSE 100 HQs and public frameworks | Long term (≥ 4 years) |

| Acoustic Privacy and Video-First Collaboration (Pods and Dividers) | +0.6% | Dense urban cores in London and Manchester, and among co-working operators | Short term (≤ 2 years) |

| Embodied-Carbon Thresholds and Take-Back or Remanufacture Requirements in Tenders | +0.3% | National, with early adoption in government-managed estates | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Compliance-Driven Ergonomics and DSE Readiness

Employers’ statutory duty to conduct Display Screen Equipment risk assessments creates a consistent baseline for ergonomic purchases across desk setups for office and home-based workers. The Health and Safety Executive clarifies that DSE obligations apply to home-based users when work at a display screen reaches daily thresholds, extending compliance to hybrid staff and keeping the category core for multi-site employers. This sustained requirement supports ongoing investment in adjustable desks and supportive task chairs, as employers seek to avoid risk exposure while improving comfort during longer screen sessions. Ergonomic upgrades remain a priority even in firms that rationalize footprints, since duty-of-care rules persist regardless of seat count or space configuration. The United Kingdom office furniture market, therefore, captures steady per-capita spending on compliant seating and workstations, with procurement programs refreshing high-use items on multi-year cycles to maintain standards and warranties. This compliance anchor also supports dealer activity in assessments and aftercare services aligned with HSE guidance, which helps maintain throughput for ergonomic SKUs in the United Kingdom office furniture market.

Flight-To-Quality Workplaces and Post-2024 Redesign Programs

Flight-to-quality is driving demand toward prime buildings, where occupiers seek modern, efficient workspaces with documented sustainability credentials. In Central London during 2024, Grade A space dominated leasing as tenants prioritized new or comprehensively refurbished buildings, a pattern that shapes furniture specifications that favor certified materials and verified lifecycle data[2]. These projects prefer new installations with Environmental Product Declarations and supplier take-back capabilities, which narrows options for legacy inventory without provenance. Landlords increasingly kit spec suites with plug-and-play furniture packages to shorten letting times, which pushes curated assortments from selected OEMs and reduces post-occupancy substitution risk. This reshapes the United Kingdom office furniture market by deepening premium demand in prime zones while forcing suppliers aligned to secondary stock to adapt product positioning and documentation. The result is a sharper divide in both pricing and specifications that rewards brands with early engagement among architects and tenant advisors active in Grade A relocations in the United Kingdom office furniture market.

Public-Sector Procurement VIA CCS Frameworks and Hubs

The Crown Commercial Service’s RM6308 framework makes sustainability and social value core elements of tender evaluation, shifting selection toward suppliers that can demonstrate carbon-reduction plans, repairability, and responsible packaging. Requirements in this framework include carbon-reduction documentation under Procurement Policy Note 06/21 and rules for reusable or recyclable packaging, with suppliers required to provide annual sustainability reporting as part of ongoing participation. Similar sustainability and reuse provisions are reflected in government workplace design guidance, which emphasizes lifecycle documentation and prioritization of reuse where feasible. These rules impact how specifications are written across the central government and broader public sectors, including health and education, thereby strengthening the addressable base for vendors with proven take-back and remanufacturing processes. Suppliers that demonstrate FSC-controlled timber sourcing, low-VOC finishes, and EPD coverage for core ranges position well for frameworks and mini-competitions, while broker-only models find it harder to meet evidentiary thresholds. This procurement posture influences the United Kingdom office furniture market by giving manufacturers with traceable, circular operations a clear path into recurring public demand pools.

Acoustic Privacy and Video-First Collaboration (Pods/Booths, Dividers)

Hybrid schedules have increased the frequency of video calls in open-plan environments, raising privacy and noise concerns and driving the adoption of pods and acoustic dividers. Modern pods deliver certified levels of speech privacy and include integrated ventilation and lighting, creating small-format meeting spaces without permanent construction and offering specifiers predictable performance characteristics. Pod installations have accelerated in landlord-spec suites and flexible-space portfolios, where shared banks of booths help differentiate listings and reduce meeting-room bottlenecks. For smaller budgets and SME layouts, mobile acoustic partitions and desk-mounted panels provide lower-cost solutions to zone collaboration and focus areas with measurable absorption performance. Subscription and rental models have emerged to extend pod access while spreading capital outlays over time, an approach that appeals to occupiers with shorter lease horizons and changing team sizes. This subcategory’s momentum supports the United Kingdom office furniture market by addressing practical workflow friction while giving buyers new choices in terms of ownership, performance, and sustainability credentials.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Office Footprint Rationalization and Capex Caution in Secondary Stock | -0.9% | Suburban business parks and secondary London submarkets | Medium term (2-4 years) |

| Input Cost Volatility for Steel, Timber, Foam, And Textiles | -0.6% | National, affecting manufacturers without hedging or pass-through clauses | Short term (≤ 2 years) |

| Second-Life or Refurbished Supply Cannibalizing New Purchases | -0.7% | London, Manchester, Bristol, where dealer networks and circular platforms are concentrated | Medium term (2-4 years) |

| Class MA Office-To-Residential Conversions Are Reducing Office Stock | -0.4% | City centers with lower-grade Class E stock | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Office Footprint Rationalization and Capex Caution in Secondary Stock

Net reductions in office floor space by some occupiers have weighed on aggregate furniture volumes, but many expansions within prime buildings have continued as part of a quality shift into higher-performing space. That contrast leaves secondary stock exposed to deferred refresh cycles and surplus disposals, while Grade A projects move forward with curated furniture packages that support new workplace strategies and higher utilization. Excess inventory from relocations flows into refurbishment channels and auctions, which tightens pricing power for new products in budget-sensitive categories. In parallel, tenants rushing to populate new high-spec floors often pay a premium for immediate delivery of standardized kits from established brands, compressing lead times for priority lines. The United Kingdom office furniture market, therefore, shows a split between premium projects that demand fully documented new products and price-sensitive refurbishments that absorb secondary stock. That split increases variability in order timing and average selling prices for manufacturers and dealers that operate across both Grade A relocations and secondary building churn in the United Kingdom office furniture market.

Input Cost Volatility for Steel, Timber, Foam, Textiles

A scaled ecosystem of refurbishers and asset-reuse platforms has matured to offer verified, warranty alternatives to new products, diverting a portion of spend away from first-sale channels. Large refurbishment operations have demonstrated significant landfill diversion and item throughput, alongside quality assurance and warranties, which institutional buyers can verify when qualifying reuse options through[3]. The United Kingdom office furniture market has seen growing acceptance of refurbished premium chairs at sizable discounts relative to new equivalents, which puts pressure on the price-to-performance calculus in mid-tier categories. Subscription-based models add another route by providing premium seating and desking as a monthly service with refresh rights and redeployment, reducing disposal risk and smoothing costs over shorter lease horizons. Documented carbon savings from reuse strengthen the business case for organizations with Scope 3 reduction targets, and procurement teams can incorporate these benefits into tender scoring frameworks. Together, these channels increase competitive pressure on commodity lines and reward OEMs that differentiate through verifiable sustainability features, faster service, and technology integration in the United Kingdom office furniture market.

Segment Analysis

By Product: Chairs Propel Compliance Spending, Booths Address Hybrid-Era Workflow Friction

Chairs accounted for 36.80% of revenue in 2025 within the United Kingdom office furniture market, supported by employers prioritizing DSE-compliant seating with lumbar support and adjustability to satisfy legal duties across office and home use. This compliance anchor underwrites steady replacement of high-wear chair fleets on predictable cycles, while meeting chairs gain share to support collaboration spaces that encourage office attendance for team tasks. Demand for acoustic booths and office dividers is expanding at a projected 3.62% CAGR through 2031 as organizations retrofit for video-first work and speech privacy without major construction, thereby changing layout strategies on open-plan floors. Desking systems continue to evolve toward modular frames that support quick reconfiguration and integrated power, while storage remains relevant through repurposed lockers and tech equipment enclosures that align with hot-desking. Sofas and soft seating contribute to hospitality-like zones that balance comfort and productivity, which helps signal brand values in reception and client areas of the United Kingdom office furniture market. Category leaders with certified materials, easy serviceability, and measured acoustic performance gain an edge in Grade A refurbishments and framework bids.

Across categories, component standardization and disassembly-first design are becoming more important in frameworks that score circularity and reuse potential. Pods and dividers help reduce meeting-room conflicts while improving noise control for hybrid calls, reshaping budgets by shifting a portion of the build cost into furniture line items. The United Kingdom office furniture market for acoustics continues to grow as buyers balance unit cost with time-to-value versus built rooms, with rentals offering an additional path for dynamic portfolios. Chairs and desks remain core due to compliance and everyday use, making them candidates for standardized specifications across multi-site rollouts. Vendors with robust aftercare and repair programs extend product life and support circular objectives, which are now factored into tender scoring, helping secure repeat business across both public and private channels. This dynamic favors OEMs that can supply compliant seating and acoustics with traceable materials, clear documentation, and predictable lead times in the United Kingdom office furniture market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Material: Wood’s Prestige Anchors Share, Polymers Rise with Circular Narratives and Agile Modularity

Wood held a 39.25% revenue share in 2025, reflecting its alignment with biophilic design, executive finishes, and corporate sustainability narratives that value FSC-controlled sources and durable aesthetics. Metal frames are essential for stability and sit-stand functionality, but cost movements in steel and aluminum have encouraged dual-sourcing and staggered pricing to manage variability in the United Kingdom office furniture market[4]Gordian, “What the Data Says: Steel Price Updates,” Gordian, gordian.com . Plastic and polymer formulations are projected to grow fastest at 3.23% CAGR, often incorporating verified recycled content that meets scoring in public tenders and helps buyers document progress against sustainability criteria. Industry analysis of the wood panel sector points to structural growth in engineered materials used for modular systems, supporting consistent supply for desks, storage, and partitions over the medium term. Timber pricing trends in late 2024 showed softening in hardwood categories, though vendors continue to manage category-level volatility and maintain labeling integrity through chain-of-custody practices. These material shifts support specifications that balance aesthetics, durability, and embodied-carbon considerations in the United Kingdom office furniture market.

As lifecycle assessment gains visibility, manufacturers are emphasizing EPD coverage, verified recycled content, and low-emission finishes, which are now routine requests in public and private projects. Shorter logistics chains and domestic finishes can aid tenders that emphasize transport emissions, provided documentation and verification meet auditor expectations. Buyers use material mix to reconcile brand expression with maintenance, reconfiguration, and cleaning requirements in high-traffic areas. The United Kingdom office furniture market for engineered panels and recycled polymers is supported by procurement that prioritizes circularity and documentation in frameworks and mini competitions. Suppliers that can show verified recycled content, robust repair programs, and local service strengthen their bids and create differentiation beyond price points in the United Kingdom office furniture market.

By Price Range: Mid-Range Dominates SME Budgets, Premium Grows as Sustainability and Experience Justify Upgrades

Mid-range packages captured 48.60% of spend in 2025, reflecting SME priorities that balance compliance, functionality, and credible finishes at a manageable price point in the United Kingdom office furniture market. This band favors modular systems with proven ergonomics, integrated cable management, and warranty support, thereby reducing risk and speeding installation. Economy-tier solutions continue to serve price-driven settings and temporary layouts where durability outweighs branded design. Premium packages are projected to grow at a 2.98% CAGR as blue-chip tenants emphasize brand signaling and guest experience in prime locations, often aligning with architect-specified assortments for Grade A buildings. Subscription models that offer premium seating and desking-as-a-service enable access to higher-end brands while helping younger firms manage cash flow, introducing a complementary channel in the United Kingdom office furniture market.

Price segmentation is also reshaped by circular options that compress the gap between economy and premium outcomes. Refurbished premium chairs offer a low-embodied-carbon alternative to new mid-tier seats, complicating direct price comparisons and underscoring the importance of documentation, data, and aftercare in vendor selection. Premium vendors respond with embedded technology and workplace analytics that extend value beyond materials and finishes. Mid-range leaders emphasize reliable service levels, configurable kits that integrate with building systems, and certifications. These shifts help sustain a balanced price mix in the United Kingdom office furniture market, with differentiated value propositions tied to sustainability, technology, and service in each tier.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User: Corporate Offices Anchor Volume, Healthcare Expands on Infection-Control Requirements

Corporate offices accounted for 61.35% of end-user demand in 2025, reflecting the concentration of financial, professional, and technology tenants that require standardized, compliant work points and collaboration spaces in the United Kingdom office furniture market. Large enterprises drive specification control and multi-site rollouts through OEM and dealer networks, while SMEs prioritize speed and configurable packages that fit phased growth. Public-sector demand continues to align with CCS frameworks, in which social value, carbon-reduction planning, and documentation of circular practices influence tender scoring and supplier choice. Healthcare offices are projected to grow at a 2.54% CAGR as estates programs incorporate furniture with infection-control properties, cleanable surfaces, and appropriate ergonomics for clinical-adjacent work. Education and government continue to procure through framework routes that emphasize durability and repairability, and maintain consistent standards across the United Kingdom office furniture market.

End-user requirements also reflect hybrid schedules and growing collaboration intensity, which influence the balance of desks, pods, meeting tables, and soft seating. Corporate tenants in Grade A towers prioritize hospitality-grade finishes in front-of-house and client areas, while back-of-house layouts emphasize flexible zones to support team sprints and project work. Public buyers request clear lifecycle documentation and service-level commitments to de-risk installation, maintenance, and end-of-life processing. The United Kingdom office furniture market size tied to enterprise rollouts remains meaningful, but subscription and circular channels continue to build relevance in smaller offices and transitional environments. Suppliers that blend compliance, service, and sustainability signaling improve win rates across corporate, healthcare, and education segments in the United Kingdom office furniture market.

By Distribution Channel: B2B Direct Sales Leverage Specification Control, Retail Fragmentation Persists with Online Aggregation

In the United Kingdom office furniture market, B2B routes, whether direct from manufacturers or dealer-led, are projected to capture around 64.67% of the market value by 2025. These routes are set to grow at a CAGR of 3.41% from 2026 to 2031, driven by enterprises increasingly adopting account-managed rollouts, framework pricing, and a focus on documented compliance. These channels coordinate BIM, certifications, and phasing requirements for complex projects, often supported by showrooms and pilot installations. B2C and retail pathways serve microbusinesses and remote workers with curated assortments and rapid delivery, while online aggregators extend reach and discovery. Subscription models introduce recurring revenue and refresh flexibility that aligns with shorter lease terms and uncertain headcounts, offering additional choice in acquisition paths for pods and seating. This distribution mix rewards vertically integrated OEMs that control factory-to-site execution, while leaving room for specialized refurbishers and installers to address circular and niche categories in the United Kingdom office furniture market.

Showroom networks and demo spaces support critical evaluation for ergonomic and acoustic products where trial experience is central to selection. Dealers strengthen their roles through space planning, installation, and aftercare that ensure compliant setups and fewer service calls. Public-sector procurement directs transactions through frameworks that streamline competition while elevating sustainability thresholds, which consolidate volumes with pre-approved vendors. Online tools now support visualization and configuration, but heavy items, delivery, and assembly continue to sustain showroom relevance for higher-value transactions. The United Kingdom office furniture market distribution will remain multi-channel as procurement teams balance control, speed, and lifecycle outcomes across project types and budgets.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

England’s dominant 82.40% share in 2025 mirrors the capital’s status as a leading European office location, where Grade A buildings attract tenants seeking energy-efficient spaces and curated fitouts that meet certification targets in the United Kingdom office furniture market. West End and City core districts continue to command premium attention, and prime buildings with landlord-furnished suites can move faster to lease completion because furniture and technology are integrated from the outset. Regional English markets such as Manchester, Birmingham, and Bristol show sustained activity, with demand concentrated in high-spec assets, creating consistent demand for compliant seating, modular desking, and acoustic solutions. The link between prime take-up and curated fit-outs remains strong, and projects in premium buildings typically require new products with documented lifecycle data that meet building-level sustainability goals. This drives higher per-station investments for front-of-house and meeting areas that showcase client-facing experiences in the United Kingdom office furniture market.

Scotland outpaces the national average on growth to 2031 as building upgrades accelerate furniture refresh cycles in office estates aligned to stricter efficiency trajectories. Edinburgh’s financial services and technology clusters continue to support premium specifications in client rooms, collaboration zones, and executive suites. Glasgow’s public and engineering anchors reinforce demand for durable, repairable sets, with supporting documentation that eases tender evaluation in the United Kingdom office furniture market. Regional service capability, repair programs, and refurbishment partnerships add weight in Scottish tenders where reuse and circular outcomes are rewarded. Suppliers with clear EPDs and buy-back options are well placed to meet expectations for lifecycle transparency and support predictable installation and aftercare.

Wales and Northern Ireland contribute steady volumes through government hubs and professional offices, with dealer networks that can coordinate delivery and assembly. Rules that enable commercial-to-residential conversion continue to tilt demand away from some secondary offices and toward prime buildings with curated suites, increasing the share of furniture budgets tied to Grade A stock. As this structural change progresses, the United Kingdom office furniture market is concentrating a larger share of value in premium projects, while circular and refurbished channels absorb items from downsizing or relocations. Redeployment and reuse programs remain relevant across regions because they deliver measurable environmental benefits that align with organizational goals. Vendors that deliver consistent service levels and clear documentation across regional hubs will continue to capture share in multi-site rollouts in the United Kingdom office furniture market.

Competitive Landscape

The United Kingdom office furniture market remains moderately fragmented, with established British manufacturers, American multinationals, and European importers competing across enterprise, public-sector, and SME channels. Domestic leaders leverage UK production and regional logistics to offer shorter lead times and service responsiveness, which strengthens bids that value supply chain resilience and lower transport distances. Global brands invest in research, showrooms, and architect relationships to embed products early in fitout planning, which supports specification consistency across international portfolios. Public-sector frameworks channel a share of volumes into pre-qualified pools where sustainability documentation and repair programs are evaluated alongside price and delivery. Circular specialists provide refurbish-and-redeploy services at scale, offering a structural price and carbon alternative to new items and increasingly appearing in large tenders. This mix keeps dealer margins viable and supports differentiated plays from premium showrooms to circular hubs in the United Kingdom office furniture market.

Technology is an emerging battleground where embedded sensors, analytics, and booking integrations add value to seating, pods, and collaboration areas. Global OEMs highlight software-linked experiences in showrooms and WorkLife centers that demonstrate how space can support community and hybrid collaboration, which influences enterprise decisions beyond individual desks. Manufacturers also publish sustainability updates and progress on emissions reductions to meet scrutiny in tenders and shareholder reporting, which aligns with client expectations for material transparency and lifecycle control. Circular platforms extend OEM lifecycles through repair and remanufacture that align with public procurement values. These strategic moves support a market where no single player dominates and where differentiated propositions on documentation, technology, and service are decisive in the United Kingdom office furniture market.

Recent moves illustrate how brands expand capability and positioning across the value chain. Haworth added Heller to strengthen its design breadth, which can translate into high-end corporate lounges, hospitality-grade zones, and premium collaboration areas for financial and legal tenants. Boss Design showcased integrated storage and mobile screens for agile layouts at a major London event in early 2026, signaling product roadmaps built for flexible zoning and modularity. Steelcase opened a new WorkLife Center focused on community-centric workplace design, a theme with direct relevance to UK occupiers rebalancing individual and shared spaces in post-pandemic layouts. These actions mirror a broader shift toward visible sustainability credentials, ready-to-spec documentation, and experiences that help occupiers translate real estate strategy into workplace outcomes across the United Kingdom office furniture market.

United Kingdom Office Furniture Industry Leaders

The Senator Group

Steelcase Inc.

MillerKnoll Inc.

Bisley Office Furniture

Haworth

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2026: Boss Design unveiled its refined workplace design approach at Workspace Design Show 2026 (Business Design Centre, London, February 25-26), showcasing BeSmart™ smart-storage technology integrated with Deco and LockerWall systems, alongside new steel planters and Arches mobile screens for agile layouts.

- February 2026: Heller Furniture joined Haworth, expanding the group's design leadership and product portfolio in the premium residential and hospitality segments, with potential crossover to high-end corporate lounges in finance and legal sectors.

- January 2026: Steelcase earned recognition for the 20th consecutive year as one of Fortune's World's Most Admired Companies, reinforcing brand equity in the United Kingdom corporate procurement, where reputation and post-installation service influence dealer preferences.

- October 2025: Crown Workspace's Renew Centre diverted 2,800 tonnes of furniture from landfill since program inception, refurbishing 125,000+ desks, chairs, and storage units with 6-month warranties, demonstrating scaled circular-economy operations that compete with new-furniture offerings.

United Kingdom Office Furniture Market Report Scope

Office furniture is defined as furniture pieces and accessories designed for use in office spaces. The UK office furniture market is segmented by type and distribution channel. By type, the market is segmented into seating, tables, storage, desks, and other office furniture (file cabinets). By distribution channel, the market is segmented into home centers, flagship stores, specialty stores, online stores, and other distribution channels (local dealers). The report offers market sizes and forecasts in value (USD) for all the above segments.

By Product

| Chairs | Employee Chairs |

| Meeting Chairs | |

| Guest Chairs | |

| Tables | Conference Tables |

| Desks | |

| Other Tables | |

| Storage Units | Filing Cabinets |

| Bookcases & Shelving | |

| Sofas/Soft Seating | |

| Booths and Office Dividers | |

| Other Office Furniture (Stools, Reception, Accessories) |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Other Materials |

By Price Range

| Economy |

| Mid-range |

| Premium |

By End-user

| Corporate Offices |

| Healthcare Offices |

| Educational Institutions |

| Government & Public Offices |

| Hospitality & Retail Back-office |

| Others |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Directly from Manufacturers |

By Geography (United Kingdom)

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Product | Chairs | Employee Chairs |

| Meeting Chairs | ||

| Guest Chairs | ||

| Tables | Conference Tables | |

| Desks | ||

| Other Tables | ||

| Storage Units | Filing Cabinets | |

| Bookcases & Shelving | ||

| Sofas/Soft Seating | ||

| Booths and Office Dividers | ||

| Other Office Furniture (Stools, Reception, Accessories) | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymer | ||

| Other Materials | ||

| By Price Range | Economy | |

| Mid-range | ||

| Premium | ||

| By End-user | Corporate Offices | |

| Healthcare Offices | ||

| Educational Institutions | ||

| Government & Public Offices | ||

| Hospitality & Retail Back-office | ||

| Others | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Directly from Manufacturers | ||

| By Geography (United Kingdom) | England | |

| Scotland | ||

| Wales | ||

| Northern Ireland | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the 2031 outlook for the United Kingdom office furniture market?

The United Kingdom office furniture market size is projected to reach USD 2.76 billion by 2031 at a 2.92% CAGR from its 2025 base of USD 2.32 billion, supported by compliance-led ergonomics, premium Grade A fitouts, and circular procurement standards.

Which product categories lead demand and growth in the United Kingdom office furniture market?

Chairs led revenue at 36.80% in 2025, and booths and office dividers are the fastest-growing, with a projected 3.62% CAGR through 2031 as offices adapt to video-first collaboration and privacy needs.

Which materials are most important in the United Kingdom office furniture market?

Wood held the highest 2025 share at 39.25% due to durability and brand alignment, while plastic and polymer are growing fastest at a projected 3.23% CAGR, with recycled-content advantages in tenders.

Which end-users drive the most spending in the United Kingdom office furniture market?

Corporate offices accounted for 61.35% of 2025 spending, and healthcare offices are projected to expand at the fastest rate, with a 2.54% CAGR, as estates programs specify cleanable, infection-control furniture.

How United Kingdom public procurement rules affect vendor selection in the United Kingdom office furniture market?

Public-sector tenders now score bids on carbon footprint and circular-economy credentials, favouring manufacturers with verified sustainability programs.