United Kingdom Chocolate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

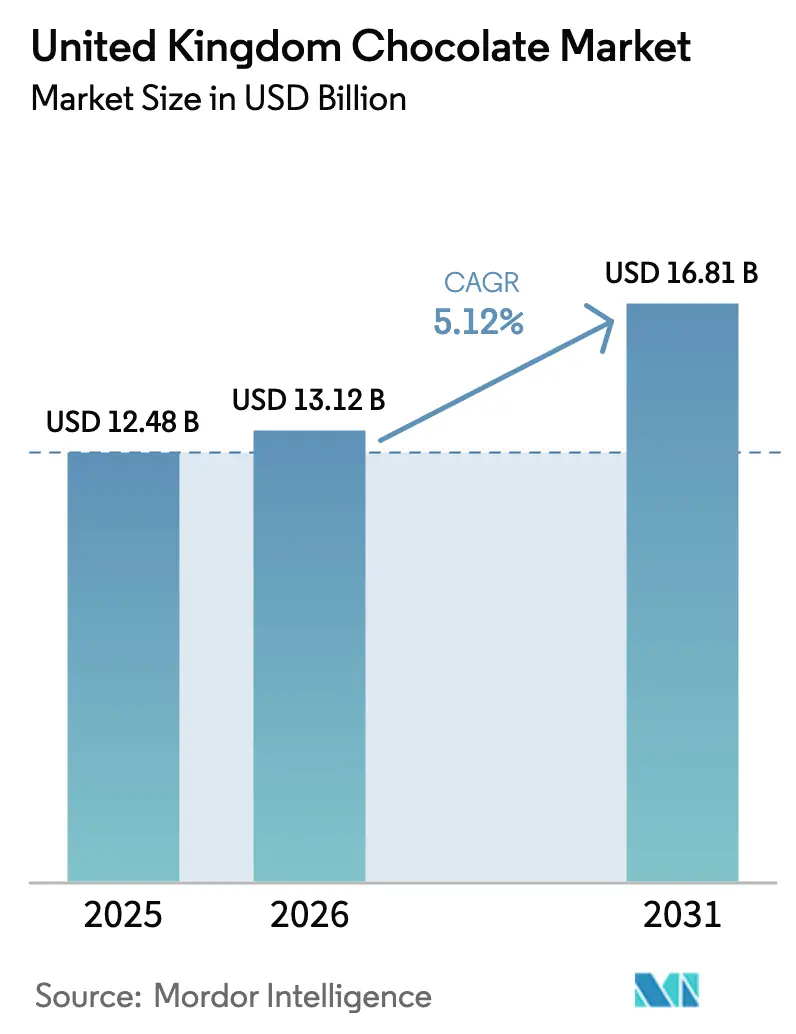

| Base Year Market Size (2025) | USD 12.48 Billion |

| Market Size (2026) | USD 13.12 Billion |

| Market Size (2031) | USD 16.81 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Chocolate Market Analysis by ���ϲ�����

The United Kingdom chocolate market size was valued at USD 12.48 billion in 2025, increased to USD 13.12 billion in 2026, and is projected to reach USD 16.81 billion by 2031, registering a compound annual growth rate (CAGR) of 5.12% during the forecast period. The market's growth is primarily driven by premiumisation trends, changing consumer taste preferences, and ongoing product innovation in flavors, ingredients, and formats. Rising demand for high-cocoa content chocolate, artisanal products, single-origin offerings, and ethically sourced options is enhancing average value realization within the category. Additionally, plant-based and allergen-free alternatives are expanding the consumer base, catering to vegan, lactose-intolerant, and health-conscious consumers. The growing adoption of digital retail channels, subscription gifting models, and direct-to-consumer strategies is further improving accessibility and consumer engagement.

Key Report Takeaways

- By product type, milk and white chocolate led with 53.63% of the United Kingdom chocolate market share in 2025, while dark chocolate is projected to expand at a 6.03% CAGR to 2031.

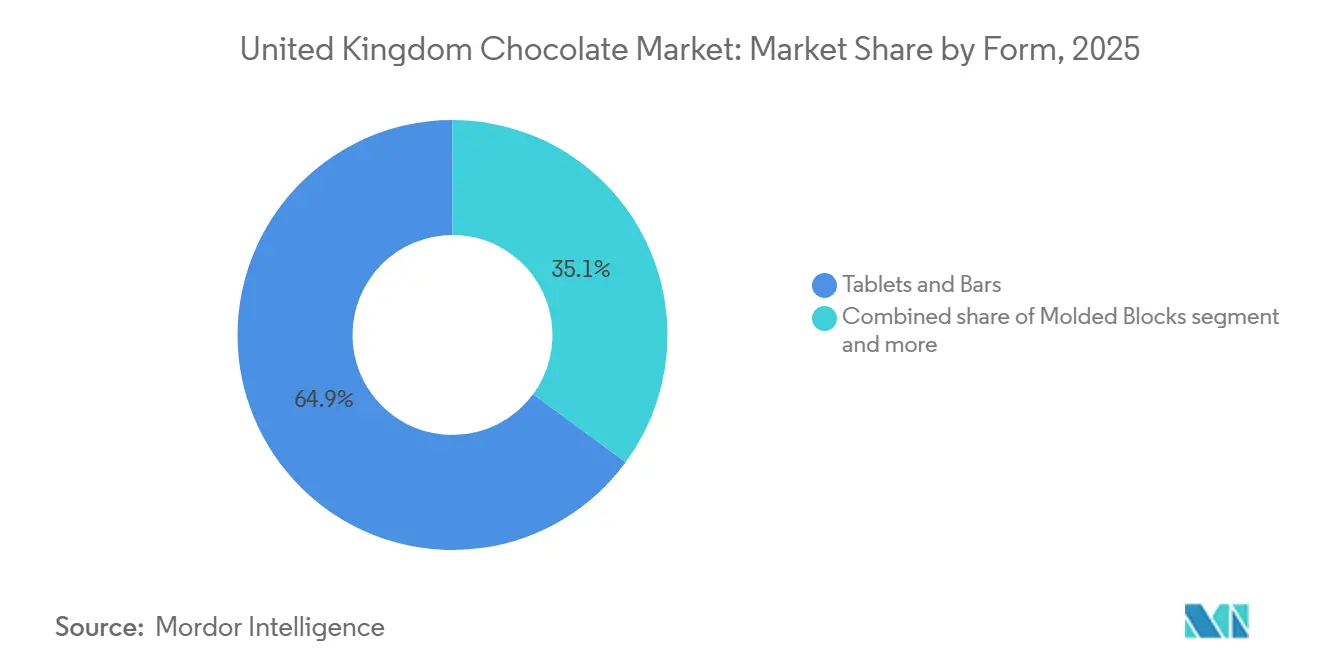

- By form, tablets and bars held 64.91% share of the United Kingdom chocolate market size in 2025, whereas pralines and truffles are forecast to grow at 5.82% CAGR through 2031.

- By price range, mass-market lines accounted for 68.09% of 2025 revenue, yet premium products are expected to post the fastest growth at a 6.45% CAGR between 2026 and 2031.

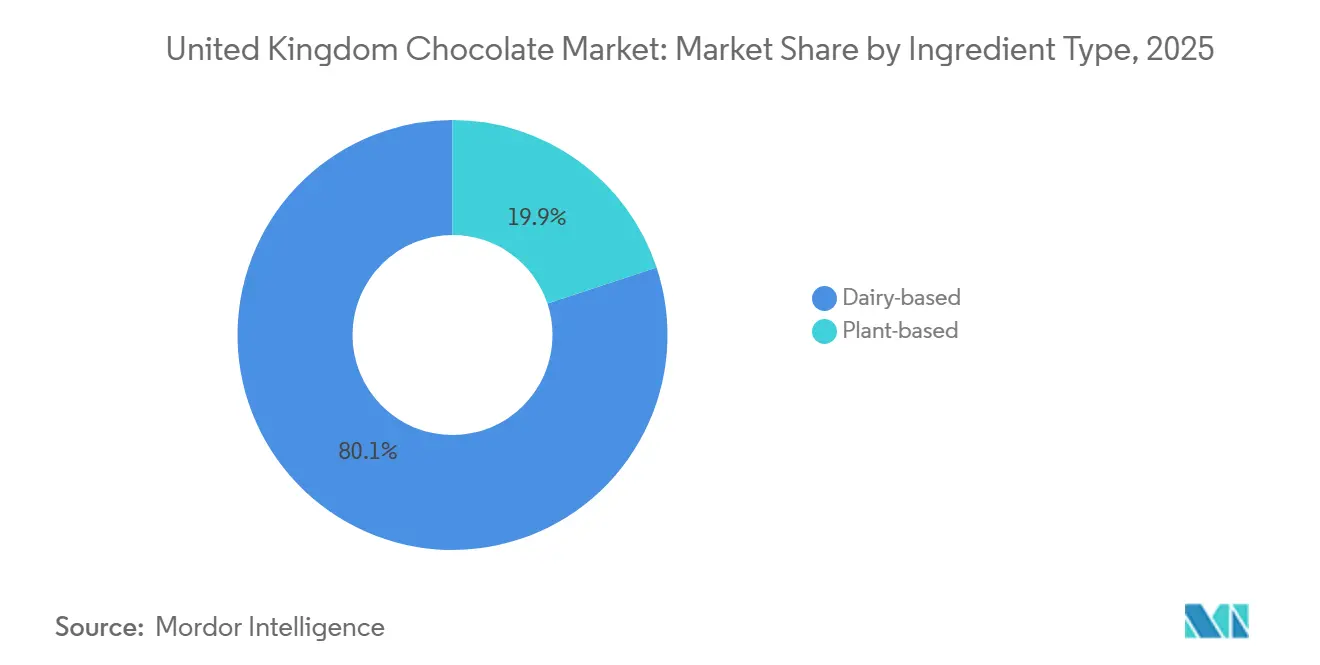

- By ingredient type, dairy-based recipes represented 80.09% of the 2025 value, but plant-based alternatives should climb at a 6.11% CAGR to 2031.

- By category, conventional chocolate delivered 65.45% of 2025 sales, while single-origin craft variants are set to expand at 6.76% CAGR over the forecast window.

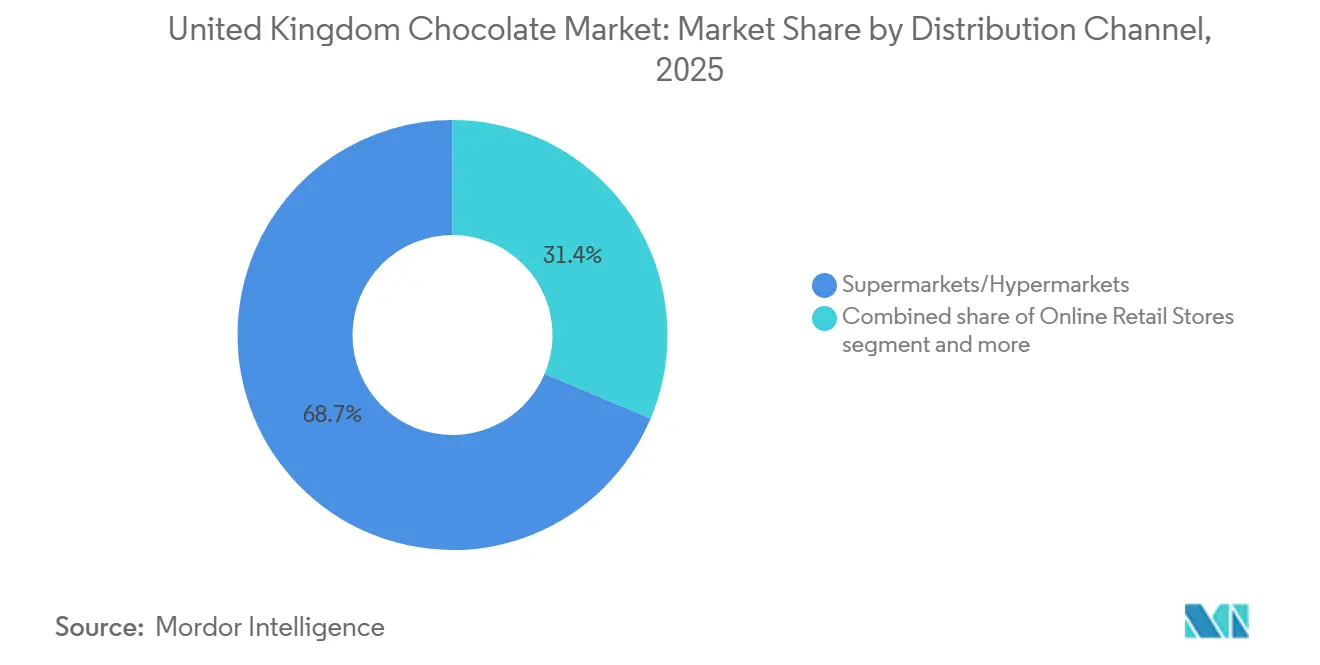

- By distribution channel, supermarkets and hypermarkets captured 68.65% of 2025 turnover, yet online retail is expected to register the highest growth at a 7.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of premium and artisanal chocolates | +1.2% | National, concentrated in London, South East England, Edinburgh | Medium term (2-4 years) |

| Growth in plant-based and vegan chocolate alternatives | +0.9% | National, with early gains in urban centres (London, Manchester, Bristol) | Medium term (2-4 years) |

| Innovation in flavours and formats | +0.7% | National | Short term (≤ 2 years) |

| Seasonal demand spikes during holidays | +0.6% | National | Short term (≤ 2 years) |

| Demand for allergen-free options | +0.5% | National | Medium term (2-4 years) |

| Advancements in chocolate processing | +0.4% | National, manufacturing hubs in Bournville, York, Halifax | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising popularity of premium and artisanal chocolates

The increasing demand for premium and artisanal chocolates is a key growth driver for the United Kingdom chocolate market. Consumers are prioritizing high-quality ingredients, unique flavor profiles, handcrafted appeal, and transparent sourcing practices, leading to a shift toward gourmet and small-batch chocolate products. The trend of premiumisation is further bolstered by interest in single-origin cocoa, ethical production methods, sophisticated packaging, and indulgent gifting options. Artisanal brands are responding to this demand by focusing on craftsmanship, limited-edition flavors, and enhanced sensory experiences compared to mass-market products. For example, in November 2024, Maldon Chocolates, renowned for its handcrafted artisan chocolates, launched a new website to offer its premium locally crafted chocolates directly to consumers. This digital platform improves direct-to-consumer access, enhances brand storytelling, and supports personalized gifting options, illustrating how artisanal chocolatiers are utilizing e-commerce to broaden their reach.

Growth in plant-based and vegan chocolate alternatives

The increasing demand for plant-based and vegan chocolate alternatives is driving growth in the United Kingdom chocolate market. The rising adoption of flexitarian and vegan lifestyles, coupled with growing awareness of lactose intolerance and sustainability issues, is prompting consumers to opt for dairy-free chocolate options. In response, manufacturers are reformulating products with plant-based milk substitutes such as oat, almond, and coconut, which mimic the creamy texture of traditional milk chocolate. Advances in ingredient technology have improved taste and mouthfeel, narrowing the sensory gap between dairy and non-dairy chocolate and fostering broader consumer acceptance. For example, in May 2025, NOMO introduced two new chocolate bar varieties in United Kingdom supermarkets. One of these, the Salted Popcorn bar in a 32g format, features smooth dairy-free chocolate combined with roasted corn pieces, offering indulgence alongside allergen-free benefits.

Innovation in flavors and formats

Continuous innovation in flavors and formats remains a significant growth driver in the United Kingdom chocolate market, as brands strive to meet evolving consumer preferences for novelty, indulgence, and premium taste experiences. Manufacturers are increasingly incorporating fruit infusions, botanical extracts, layered textures, and seasonal limited editions to differentiate their products in a highly competitive retail environment. Format innovations, such as filled cremes, fondants, bite-sized assortments, and sharing packs, further support impulse purchases and gifting occasions while expanding consumption opportunities beyond traditional tablets and bars. For example, in February 2026, Hames Chocolates, a Lincolnshire-based British chocolatier, introduced a new Dark Chocolate Fondant Cremes Range. This range features four fruit variants: Dark Chocolate Raspberry Cremes, Dark Chocolate Lemon Cremes, Dark Chocolate Orange Cremes, and Dark Chocolate Mango Cremes. Additionally, the range includes Dark Chocolate Mint Cremes, made with English peppermint oil distilled from English Black Mitcham.

Seasonal demand spikes during holidays

Seasonal demand spikes during key holidays are a significant growth driver in the United Kingdom chocolate market. Events such as Easter, Christmas, Valentine’s Day, and Mother’s Day lead to increased chocolate sales through themed packaging, novelty formats, and limited-edition product launches. Retailers dedicate additional shelf space and promotional displays during these periods, encouraging impulse purchases and gifting-related consumption. Seasonal product ranges also allow brands to introduce innovative flavors, premium assortments, and specialty dietary options, generating consumer interest and short-term volume growth. For example, in February 2024, Moo Free expanded its free-from chocolate portfolio with its latest Easter collection, which included two new products. A notable addition was the Strawberry Sundae Egg, a strawberry-flavored chocolate innovation in the free-from category. This launch highlights how seasonal events provide a strategic platform for product innovation, particularly in allergen-free and vegan segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating cocoa prices due to climate change | -1.1% | National, United Kingdom entirely reliant on West African imports | Short term (≤ 2 years) |

| Rising health concerns over sugar content and obesity | -0.8% | National, intensified by HFSS and LHF regulations | Medium term (2-4 years) |

| Intense competition from multinational brands | -0.6% | National, concentrated in supermarket and online channels | Medium term (2-4 years) |

| Regulatory pressures on food safety | -0.4% | National, manufacturing compliance costs highest in South East England | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Fluctuating cocoa prices due to climate change

Fluctuating cocoa prices, driven by climate change, pose a significant challenge to the United Kingdom's chocolate market. Cocoa production is predominantly concentrated in West African countries, where rising temperatures, irregular rainfall, prolonged droughts, and increased crop diseases are disrupting yields and undermining supply stability. Climate-related issues, including soil degradation and pest infestations, have further exacerbated price volatility in global cocoa markets, directly affecting manufacturers' raw material procurement costs. For chocolate producers in the United Kingdom, unpredictable cocoa pricing pressures profit margins, complicates long-term sourcing agreements, and increases the likelihood of reformulation or price adjustments. Smaller and artisanal manufacturers are particularly at risk due to their limited sourcing networks and lack of hedging capabilities.

Rising health concerns over sugar content and obesity

Health concerns related to sugar consumption and obesity are constraining the growth of the United Kingdom chocolate market. Increasing public awareness of the connection between excessive sugar intake, weight gain, and chronic diseases is influencing consumer purchasing behavior, particularly among health-conscious individuals. Chocolate, particularly milk and white varieties, is often viewed as high in sugar and calories, leading to reduced purchase frequency or a shift toward lower-sugar snacks and functional alternatives. According to the Government of the United Kingdom, the prevalence of type 2 diabetes among adults aged 17 and over in England rose to 7.0% in March 2024, up from 6.8% in March 2023 [1]Source: Government of the United Kingdom, "Diabetes profile", gov.uk. The growing incidence of diet-related conditions has heightened regulatory scrutiny, public health campaigns, and reformulation efforts within the confectionery market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dark Chocolate Gains as Health Pivot Accelerates

Milk and white chocolate accounted for 53.63% of the total market share in 2025, establishing this category as the leading product segment. This dominance is primarily attributed to widespread consumer preference for smooth, creamy, and sweeter taste profiles that appeal to various age groups. Milk chocolate remains a core everyday indulgence, supported by its extensive availability in supermarkets, convenience stores, and discount retailers, along with strong brand loyalty developed over decades. White chocolate, while smaller in market size compared to milk chocolate, benefits from flavor innovations, premium inclusions, and seasonal limited editions, which enhance its appeal.

Dark chocolate is expected to grow at a CAGR of 6.03% through 2031 in the United Kingdom chocolate market, making it the fastest-growing product type during the forecast period. This growth is driven by increasing consumer preference for higher cocoa content, reduced sugar formulations, and the perceived health benefits of dark chocolate, such as antioxidant properties and lower sweetness levels. Trends in premiumisation and demand for ethically sourced ingredients are further supporting the segment's expansion. For instance, in January 2024, KitKat reintroduced its 70% Dark variant in the UK for a limited time. The four-finger bar is made using cocoa mass sourced from families participating in Nestlé’s Cocoa Income Accelerator Programme, underscoring the brand’s commitment to responsible sourcing and improving farmer livelihoods.

By Form: Tablets Dominate, but Gifting Fuels Pralines

Tablets and bars accounted for 64.91% of total form-based sales in 2025 in the United Kingdom chocolate market, establishing them as the leading format category. This dominance is attributed to strong consumer familiarity, convenient portioning, and widespread availability across supermarkets, convenience stores, and discounters. These formats cater to both everyday individual consumption and sharing occasions, supported by a variety of pack sizes ranging from single-serve countlines to large family-sharing blocks. Additionally, tablets and bars facilitate extensive product innovation, including filled centers, high-cocoa dark variants, and limited-edition seasonal launches. Bars also serve as the primary format for premium, organic, and ethically sourced chocolate ranges, enhancing their shelf presence and visibility.

Pralines and truffles are projected to grow at a CAGR of 5.82% through 2031 in the United Kingdom chocolate market, making them one of the fastest-growing premium formats. This growth is driven by increasing demand for indulgent, artisanal, and gift-oriented chocolate products. Consumers are showing a preference for premium boxed assortments, luxury fillings, and sophisticated flavor combinations such as salted caramel, hazelnut praline, champagne ganache, and exotic infusions. Furthermore, the rising interest in handcrafted and ethically sourced chocolates has bolstered the appeal of boutique chocolatiers and high-end retail brands.

Note: Segment shares of all individual segments available upon report purchase

By Price Range: Premium Outpaces Mass Despite Economic Headwinds

Mass-market offerings accounted for 68.09% of the total market share in 2025, maintaining a dominant position within the category. This segment's strength is attributed to high household penetration, affordability, and widespread distribution across supermarkets, convenience stores, discounters, and impulse retail channels. Typical products in this category include standard tablets, countlines, sharing pouches, and seasonal novelties, catering to routine consumption rather than premium gifting. The segment benefits from strong brand recognition, promotional visibility, and frequent product rotations, such as flavor extensions and limited-edition launches. Additionally, impulse purchases at checkout counters and multipack formats for family consumption contribute to volume stability within this price tier.

Premium chocolate is projected to grow at a CAGR of 6.45% through 2031 in the United Kingdom chocolate market, making it the fastest-growing price segment during the forecast period. This growth is driven by increasing consumer demand for high-quality ingredients, artisanal craftsmanship, single-origin cocoa, and enhanced taste experiences. Premium chocolate is increasingly associated with indulgence and experiential consumption, supported by refined packaging and strong sustainability narratives. In October 2025, Valrhona introduced its latest premium chocolate range in the United Kingdom market. Each piece of the French-made luxury collection features a balance of crisp texture, intense pistachio praline, and silky milk chocolate, reinforcing the brand’s reputation for sophisticated flavors and culinary excellence.

By Ingredient Type: Plant-Based Gains Traction as Dairy Dominates

Dairy-based chocolate accounted for 80.09% of the total market share in 2025 in the United Kingdom chocolate market, establishing itself as the leading ingredient category. This dominance is attributed to the widespread popularity of milk chocolate products, which heavily utilize dairy components such as milk powder, condensed milk, and butterfat to achieve a creamy texture and smooth mouthfeel. The segment benefits from long-standing consumer preference for traditional flavor profiles, strong brand loyalty, and extensive availability across retail channels. Additionally, dairy-based chocolate is a key component in premium products like pralines, truffles, and gifting assortments, where texture and richness are essential attributes.

Plant-based chocolate alternatives are projected to grow at a CAGR of 6.11% through 2031 in the United Kingdom chocolate market, making them the fastest-growing ingredient segment during the forecast period. This growth is primarily driven by the increasing adoption of vegan, lactose-free, and dairy-free diets, coupled with heightened awareness of environmental sustainability and animal welfare concerns. Manufacturers are reformulating products with plant-based milk substitutes such as oat, almond, coconut, and rice to replicate the creamy texture traditionally associated with dairy chocolate. The segment is also benefiting from advancements in taste and texture enhancement, improved ingredient functionality, and greater retail visibility.

By Category: Single-Origin Craft Challenges Conventional Scale

Conventional chocolate accounted for 65.45% of the total market share in 2025 in the United Kingdom chocolate market, maintaining its position as the leading category. Its dominance is attributed to wide product availability, established brand presence, and strong penetration across supermarkets, convenience stores, and discounters. This category encompasses mainstream milk, dark, and white chocolate products produced using standard cocoa sourcing practices and positioned for everyday consumption. Conventional chocolate benefits from strong promotional activities, multipack formats, impulse placements, and seasonal launches, which drive high sales volumes. Additionally, it offers diverse flavor extensions and format innovations while maintaining competitive pricing across mass-market channels.

Single-origin chocolate is projected to grow at a CAGR of 6.76% through 2031 in the United Kingdom chocolate market, making it one of the fastest-growing niche categories. This growth is driven by increasing consumer interest in cocoa provenance, traceability, and distinctive flavor profiles associated with specific growing regions. Single-origin products appeal strongly to premium and ethically conscious consumers who prioritize transparency, sustainability credentials, and terroir-driven taste differentiation. In June 2024, Love Cocoa introduced two new products to its portfolio: a buttery 35% Blonde Chocolate Bar and a rich 85% Dark Chocolate Bar. Both bars are crafted using sustainably sourced single-origin Colombian cocoa, emphasizing the brand’s commitment to ethical sourcing and flavor authenticity. Such product innovations demonstrate how brands are leveraging origin storytelling and high cocoa content differentiation to meet premium consumer demand.

By Distribution Channel: Supermarkets Hold, but Online Surges

Supermarkets and hypermarkets accounted for 68.65% of the total distribution share in the United Kingdom chocolate market in 2025, maintaining their position as the leading retail channel. This segment's strong performance is attributed to extensive shelf space allocation, diverse product assortments across various price tiers, and high foot traffic. These large-format retailers offer consumers access to mass-market, premium, private-label, seasonal, and specialty chocolate products in a single location, catering to both planned purchases and impulse buying. Promotional strategies, including price discounts, multipack offers, end-of-aisle displays, and seasonal merchandising, further strengthen the channel's dominance. Additionally, supermarkets and hypermarkets play a significant role in introducing new product innovations and limited-edition variants, providing brands with high visibility and nationwide reach.

Online retail is projected to grow at a CAGR of 7.05% through 2031, making it the fastest-growing distribution channel in the United Kingdom chocolate market during the forecast period. This growth is driven by increasing adoption of digital shopping, convenience-focused purchasing behavior, subscription gifting models, and direct-to-consumer strategies employed by both premium chocolatiers and mainstream brands. According to the International Telecommunication Union (ITU), 95.5% of individuals in the United Kingdom were using the internet in 2024, reflecting the country's high level of digital penetration [2]Source: International Telecommunication Union (ITU), "United Kingdom", datahub.itu.int. This widespread internet access supports the growth of e-commerce grocery platforms, brand-owned websites, and online marketplaces, thereby accelerating online chocolate sales.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

The United Kingdom chocolate market exhibits distinct regional dynamics, with Wales, Scotland, and South East England significantly influencing premiumisation trends. Wales has emerged as a key player in the premium chocolate segment, driven by increasing consumer demand for high-quality and artisanal products. According to the Government of Wales, the region had an estimated population of approximately 3,187,000 in 2024, providing a stable consumer base for premium and specialty chocolate offerings [3]Source: Government of Wales, "Mid year estimates of the population", gov.wales. Additionally, there is a growing preference for ethically sourced, organic, and locally inspired chocolate products in Wales, aligning with broader sustainability and provenance trends across the United Kingdom.

Scotland also represents a robust regional market, particularly for premium boxed chocolates and gifting assortments. This growth is supported by tourism, specialty confectionery stores, and heritage-driven brands. Urban centers such as Edinburgh and Glasgow contribute significantly to retail chocolate sales through department stores, supermarkets, and boutique chocolatiers. In contrast, South East England, including London, serves as a central hub for premiumisation due to its higher exposure to global brands, luxury retail presence, and innovation-driven product launches. The region's concentration of high-end retail chains and specialty chocolate boutiques underpins the sustained growth of single-origin and artisanal chocolate categories.

Beyond these regions, other major cities in the United Kingdom, such as Manchester, Birmingham, Leeds, and Bristol, play critical roles in driving both mass-market and premium chocolate consumption. Northern England and the Midlands continue to exhibit strong demand for mainstream tablets, bars, and seasonal assortments, primarily through supermarket-led distribution channels. Meanwhile, urban regeneration and evolving retail landscapes are gradually increasing the penetration of premium and specialty chocolate products in these areas.

Competitive Landscape

The United Kingdom chocolate market is moderately concentrated, featuring a mix of multinational confectionery leaders and emerging premium players competing across various price tiers and product formats. Key companies, including Mars, Incorporated, Ferrero International SpA, Nestlé S.A., Chocoladefabriken Lindt & Sprüngli AG, and Mondelēz International Inc., hold a significant market share. These companies leverage extensive brand portfolios, robust retail distribution networks, and ongoing product innovation to maintain their market position. They compete in mass-market, premium, seasonal, and gifting categories, utilizing strong brand equity and promotional strategies to secure shelf space in supermarkets and hypermarkets.

Packaging innovation is a critical factor in competitive differentiation, especially as sustainability and premium visual appeal gain prominence. For example, in July 2025, Cadbury Bournville launched new chocolate bars accompanied by a bold packaging redesign, reinforcing its premium dark chocolate positioning and enhancing shelf visibility. Leading brands are increasingly adopting recyclable materials, reduced-plastic formats, and modernized visual designs to meet evolving consumer expectations. Packaging also serves as a medium for storytelling, emphasizing cocoa origin, ethical sourcing commitments, and flavor differentiation.

Despite strong competition from established multinational brands, niche segments present growth opportunities. Allergen-free, dairy-free, and functional chocolate products enriched with protein, fiber, or reduced sugar formulations show significant potential. Smaller artisanal brands and challenger companies are addressing these gaps by targeting health-conscious, vegan, and ethically driven consumers. As consumer preferences continue to shift toward sustainability, wellness, and premium indulgence, competitive intensity is expected to rise. This trend is likely to drive further innovation in product formulation, packaging, and brand positioning within the United Kingdom chocolate market.

United Kingdom Chocolate Industry Leaders

-

Mars, Incorporated

-

Ferrero International SpA

-

Nestlé S.A.

-

Chocoladefabriken Lindt & Sprüngli AG

-

Mondelēz International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Milkybar, a brand owned by Nestlé, has debuted a new white chocolate product in the United Kingdom. The new offering is crafted from whole milk, features cocoa certified by the Rainforest Alliance, and is free from artificial flavors.

- January 2026: Ferrero reintroduced Kinder Bueno Dark in the United Kingdom. This beloved treat features Kinder Bueno's iconic crispy wafer and creamy hazelnut filling, all enveloped in rich dark chocolate.

- April 2025: Reese's has launched its Peanut Butter White Bar, melding its iconic peanut butter filling with a white chocolate-flavored coating. This 90-gram bar showcases the familiar ridges of Reese's Peanut Butter Cups.

- March 2025: Lindt & Sprüngli has unveiled its latest flagship store in London, right under the famed Piccadilly Lights. The store features offerings from Lindt Master Chocolatiers, a Lindt Choco Barista, along with a selection of gifts, souvenirs, and more.

United Kingdom Chocolate Market Report Scope

The chocolate market encompasses the industry involved in the production, distribution, and sale of chocolate products derived from cocoa beans. The United Kingdom chocolate market is segmented by product type, form, price range, ingredient type, category, and distribution channel. Based on product type, dark chocolate, milk, and white chocolate. Based on form, the market is segmented into tablets and bars, molded blocks, pralines and truffles, and other forms. Based on price range, the market is segmented into mass and premium. Based on ingredient type, the market is segmented into dairy-based and plant-based. Based on category, the market is segmented into single-origin chocolate and conventional chocolate. Based on distribution channel, the market is segmented into supermarkets/hypermarkets, online retail stores, convenience stores, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (Units) for all segments mentioned.

| Dark Chocolate |

| Milk and White Chocolate |

| Tablets and Bars |

| Molded Blocks |

| Pralines and Truffles |

| Other Forms |

| Mass |

| Premium |

| Dairy-based |

| Plant-based |

| Single Origin Chocolate |

| Conventional Chocolate |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Convenience Store |

| Other Distribution Channels |

| By Product Type | Dark Chocolate |

| Milk and White Chocolate | |

| By Form | Tablets and Bars |

| Molded Blocks | |

| Pralines and Truffles | |

| Other Forms | |

| By Price Range | Mass |

| Premium | |

| By Ingredient Type | Dairy-based |

| Plant-based | |

| By Category | Single Origin Chocolate |

| Conventional Chocolate | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Online Retail Stores | |

| Convenience Store | |

| Other Distribution Channels |

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

���ϲ����� follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms