Toilet Paper Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 56.90 Billion |

| Market Size (2031) | USD 66.43 Billion |

| Growth Rate (2026 - 2031) | 3.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Toilet Paper Market Analysis by ���ϲ�����

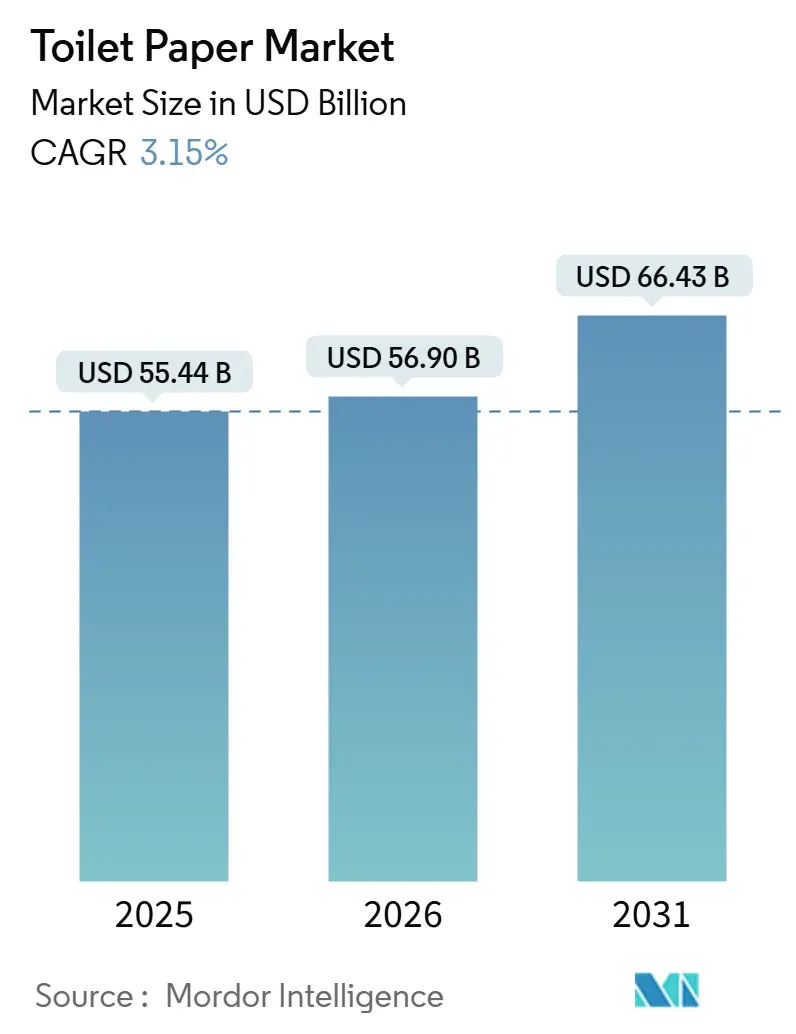

The toilet paper market size is expected to increase from USD 55.44 billion in 2025 to USD 56.90 billion in 2026 and reach USD 66.43 billion by 2031, growing at a CAGR of 3.15% over 2026-2031. Stable household demand in mature economies, rapid sanitation build-out in Asia-Pacific, and accelerating e-commerce adoption jointly anchor this outlook. Rolled formats remain the dominant product, recycled fiber leads on cost and sustainability, and premium multi-ply SKUs support value growth in regions with flat volumes. Structural cost pressure from pulp price swings, expanding chain-of-custody rules, and growing bidet adoption in parts of Europe and East Asia temper the headline trajectory. Competition is moderate: the top five suppliers accounted for 45% of revenue in 2025, leaving scope for regional specialists, private-label converters, and digitally native brands to take share.

Key Report Takeaways

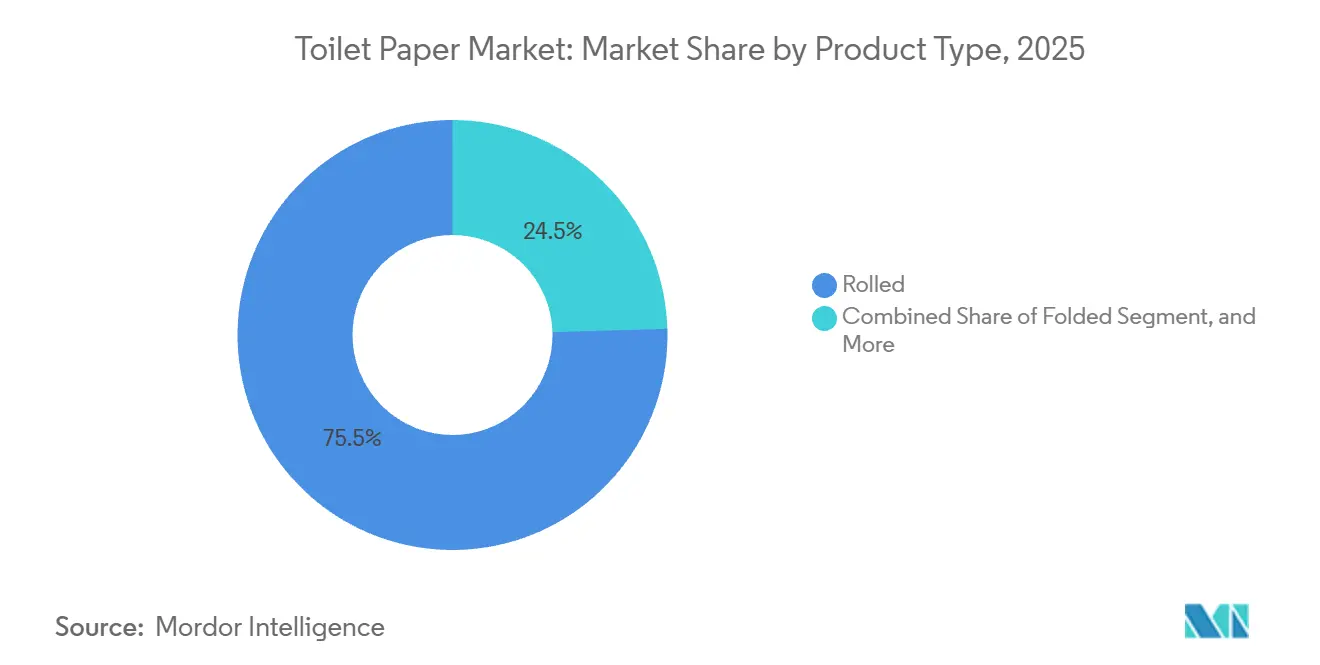

- By product type, rolled formats led with 75.46% revenue share in 2025, while folded tissue is projected to expand at a 4.31% CAGR through 2031.

- By material source, recycled fiber commanded 53.26% of the toilet paper market share in 2025, and bamboo plus other alternative fibers are forecast to register a 4.98% CAGR to 2031.

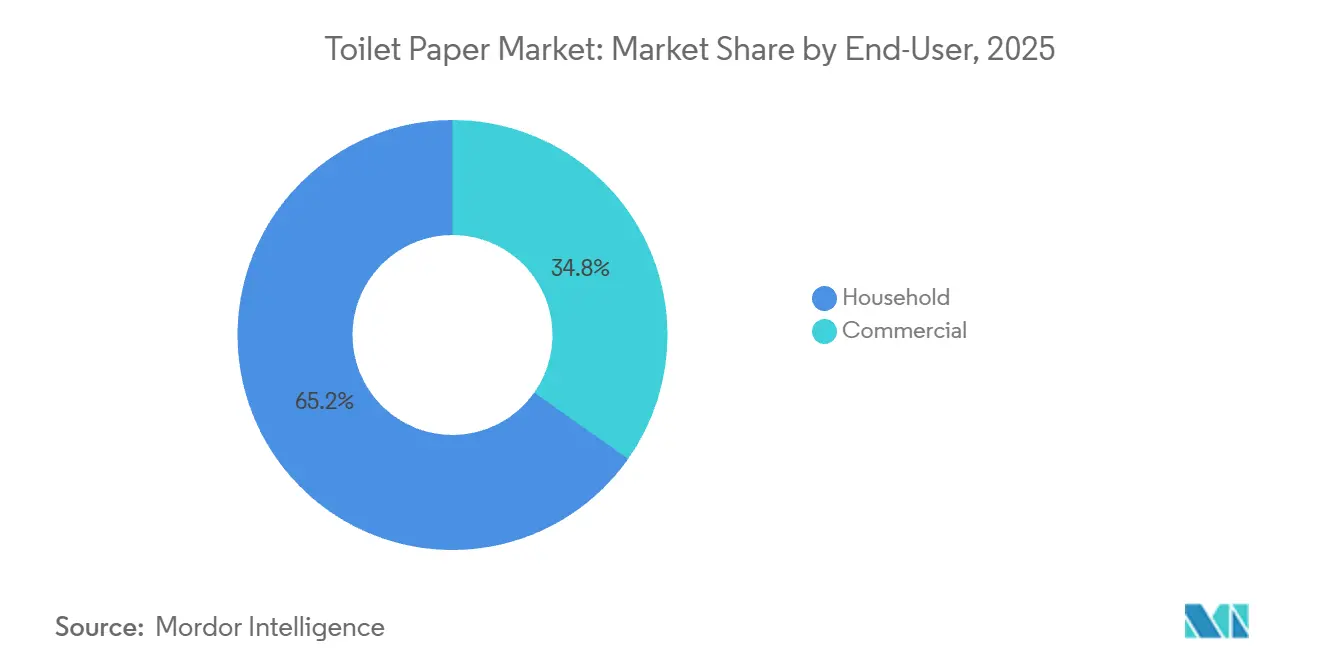

- By end-user, household consumption accounted for 65.23% of the toilet paper market size in 2025, and commercial procurement is advancing at a 4.57% CAGR over the forecast period.

- By distribution channel, offline outlets retained 54.78% share of the toilet paper market in 2025, whereas online sales are set to rise at a 4.72% CAGR to 2031.

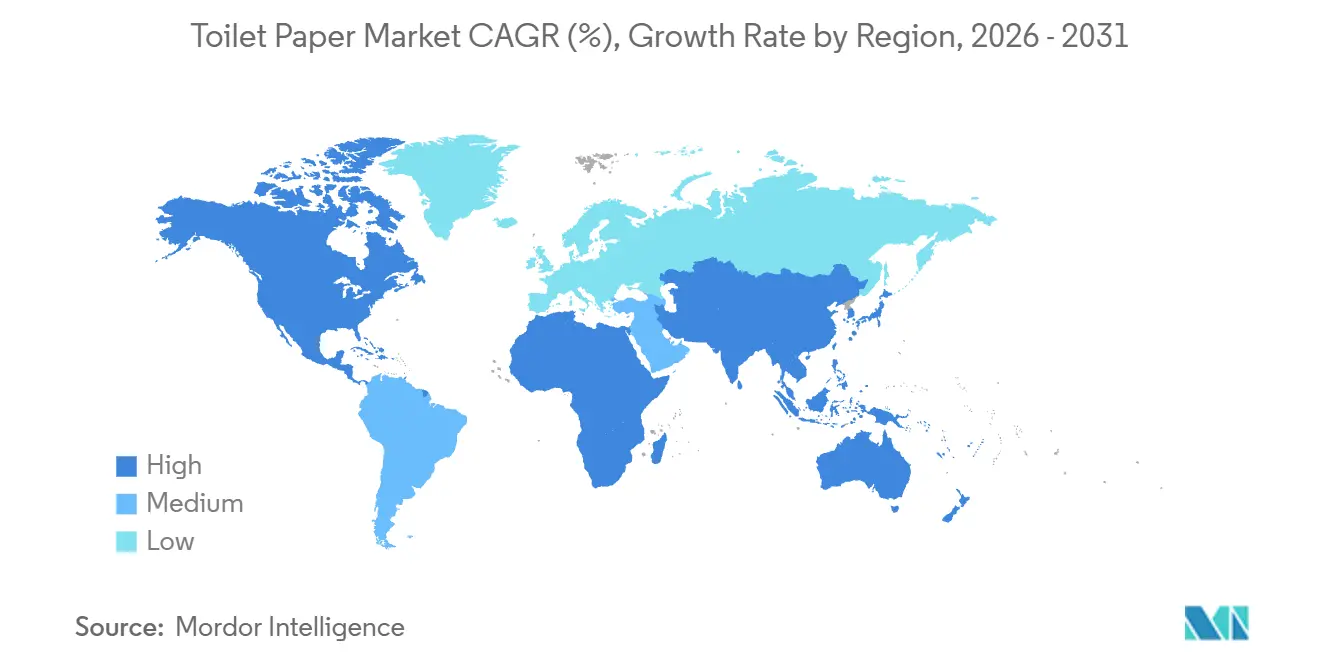

- By geography, North America contributed 39.88% of market share in 2025, while Asia-Pacific is on track for the fastest regional expansion at a 5.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Toilet Paper Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hygiene and Urbanization Surge | +0.8% | Global, core in India, China, Indonesia | Long term (≥ 4 years) |

| Post-Pandemic Hospitality Rebound | +0.5% | Europe, North America, Middle East | Medium term (2-4 years) |

| E-Commerce Penetration in Tissue Sales | +0.6% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Premiumization via Multi-Ply and Scented SKUs | +0.4% | North America, Western Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Patent Expiry Enabling Coreless Rolls | +0.3% | North America and Europe first, global later | Short term (≤ 2 years) |

| AI-Driven Predictive Maintenance | +0.2% | Global, concentrated in large mills | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Hygiene and Urbanization Surge

National toilet-construction programs in India and China have shifted millions of households from open defecation to private facilities, creating new baseline demand for entry-level tissue. Rural water connections lower the switching cost by making flush systems practical, and urban migration raises disposable income as well as aspirational consumption. Across large parts of sub-Saharan Africa and South America, city growth above 3% per year echoes this pattern, lifting per-capita tissue use from a low base. Brands that pair lightweight, single-ply rolls with e-commerce bulk packs are positioned to capture early-stage consumers. Over the long term, the combination of infrastructure, income, and changing hygiene norms remains the largest positive input to the toilet paper market.

Post-Pandemic Hospitality Rebound

Global tourist arrivals recovered to nearly pre-pandemic levels by 2024, filling hotels, restaurants, and entertainment venues that source high-traffic tissue formats.[1]United Nations World Tourism Organization, “International Tourist Arrivals 2024,” unwto.org Average revenue per available room rebounded in North America and Europe, encouraging operators to upgrade bathroom amenities, including scented multi-ply rolls that support premium nightly rates. Healthcare facilities likewise restarted deferred refurbishment cycles, specifying interfold or touch-free dispensing systems to meet infection-control protocols. Although hybrid work caps office occupancy, baseline restroom traffic has stabilized close to 70% of 2019 levels, ensuring steady institutional demand. The hospitality driver is strongest over the next three years as capacity utilization normalizes.

E-Commerce Penetration in Tissue Sales

Direct-to-consumer channels compressed logistics costs for bulky tissue packs and unlocked subscription bundles that guarantee repeat orders.[2]Procter and Gamble, “Fiscal 2024 Annual Report,” pginvestor.com Restraints Large incumbents disclosed double-digit gains in online sales in 2024, while marketplaces reported sustained category share after pandemic peaks. Urban zones with dense last-mile networks convert fastest, but mobile platforms now deliver to rural households in India and China. Online share lifts manufacturers’ forecasting accuracy, reduces trade promotion expense, and supports micro-segmented SKUs such as bamboo blends that rarely secure shelf slots offline. The medium-term uplift is material, given that online penetration in tissue still lags that of most household staples.

Premiumization via Multi-Ply and Scented SKUs

Affluent buyers in the United States, the United Kingdom, Germany, Japan, and major Chinese cities continue to trade up from standard two-ply products to thicker, softer, or fragranced varieties that retail up to 30% above mainstream price points. Format innovations, such as mega-rolls and coreless rolls, amplify perceived value by extending change intervals and reducing packaging waste. Advertising reframes toilet paper as a personal care product, moving the category away from pure commodity positioning. Premiumization is less visible in price-sensitive markets but gains traction as middle-class cohorts expand, making this a durable, long-horizon driver.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Pulp Price Volatility | -0.4% | Global, acute for pulp importers | Short term (≤ 2 years) |

| Deforestation-Linked Regulations Tightening | -0.3% | Europe and North America, extending to Asia-Pacific | Medium term (2-4 years) |

| Rising Bidet Penetration | -0.2% | Japan, South Korea, parts of Western Europe | Long term (≥ 4 years) |

| Fiber Shortages from Beetle Infestations | -0.2% | North America with global ripple effects | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Raw-Pulp Price Volatility

Northern bleached softwood kraft touched EUR 1,380 per ton (USD 1,518 per ton) in April 2024, the highest on record, following mill closures, energy shocks, and freight spikes.[3]Fastmarkets RISI, “Global Pulp Price Index April 2024,” risi.com Spot pulp inflation shaved 200-300 basis points from tissue gross margins at mills that buy on the open market rather than source internally. China’s tighter import rules on contaminated recovered paper pushed converters toward virgin fiber, shrinking cost differentials between recycled and virgin inputs. While new South American capacity may cool prices after 2026, short-term volatility pressures procurement budgets and limits aggressive price promotions.

Deforestation-Linked Regulations Tightening

European Union rules require geolocated proof that wood pulp and bamboo were harvested outside deforested zones, adding audit costs of 5-8% per imported tissue shipment. Several high-profile mislabeling cases in 2024 led retailers to delist non-compliant brands, triggering abrupt revenue losses. North American state procurement policies echo the European stance, elevating the importance of FSC and PEFC certification. Small and mid-size converters often lack the capital for satellite-tracking or blockchain chain-of-custody systems, accelerating market consolidation into players that can prove origin at scale.

Segment Analysis

By Product Type: Coreless Innovation Challenges Rolled Dominance

Rolled tissue accounted for 75.46% of the toilet paper market in 2025, driven by household habits and shelf-efficient packaging. Coreless technology, now off patent, lets challengers offer waste-free rolls that reduce packaging material by roughly 40%. Mainstream brands answer by bundling larger sheet counts per roll, extending change intervals, and adding fragrance options. Folded tissue is projected to expand at a 4.31% CAGR through 2031, as hotels, hospitals, and airports prefer single-sheet dispensing to curb over-pull and cross-contact. Moist toilet tissue, positioned between dry rolls and fully plumbed bidet solutions, is gaining ground in the United States and Germany but faces scrutiny from wastewater systems. Innovation in this segment is less about absolute volume and more about added value that shields margin against pulp swings.

Consumer preference inertia anchors rolled SKUs, yet technology shifts accelerate format mixing. Private-label chains across Europe introduced store-brand coreless rolls in 2025 at 5-10% below branded price points, eroding legacy share. Commercial buyers are retesting jumbo interfold packs to cut maintenance labor, especially in hotels where staffing gaps persist. Category leaders keep a design pipeline focused on embossing, ink-free branding, and rapid-dissolve cores to align with tightening flush-ability norms. The product landscape is diversifying, but rolled tissue will remain the category backbone through 2031.

Note: Segment shares of all individual segments available upon report purchase

By Material Source: Recycled Fiber Dominates, Bamboo Gains Cautiously

Recycled fiber captured 53.26% of the toilet paper market share in 2025, propelled by waste-collection schemes in Western Europe and North America that feed cost-effective pulp streams. Virgin pulp retains a central role in ultra-soft, multi-ply lines where brightness and fiber length drive tactile performance. Bamboo plus other alternative fibers are forecast to register a 4.98% CAGR to 2031. Bamboo acreage expands in southern China and parts of Southeast Asia, yet retailer disquiet after mislabeling audits moderates ordering volumes until chain-of-custody tools mature. Agricultural residues such as wheat straw and bagasse attract pilot investment in India, where government incentives reward the valorization of farm waste. Over the forecast window, blended fabrics that mix recycled, bamboo, and certified virgin fibers emerge as the preferred hedge against raw-material shock and regulatory scrutiny.

Fiber procurement strategies now incorporate pulp price insurance, multi-year offtake deals with South American plantations, and life-cycle assessments that quantify carbon and water intensity. Brands differentiate with clearer on-pack sourcing claims supported by QR-code traceability. Rapid-test spectroscopy on mill floors verifies furnish ratios in real time, reducing off-spec output and protecting certification. The overall shift is toward diversified, transparent fiber baskets that can flex with climate events, trade disruptions, and evolving audit protocols.

By End-User: Commercial Recovery Outpaces Household Stability

Households accounted for 65.23% of the market share in 2025, but growth is subdued in high-income countries, where per-capita tissue use plateaus. The commercial segment is forecast to grow at a CAGR of 4.57% over the forecast period, as hotels, restaurants, and healthcare facilities return to full capacity, lifting demand for jumbo-roll, interfold, and touch-free products. Hospitality chains now include premium scented tissue as part of guest-experience upgrades aimed at capturing leisure travelers. Hospitals expand tender specifications to mandate touchless dispensers paired with interfold sheets that minimize cross-contact. Large employers lock in national restroom supply contracts to streamline hybrid office operations. By 2031, commercial accounts will contribute a larger slice of incremental value, especially in regions where tourism and medical infrastructure growth coincide.

Household channels split along income lines. Premium shoppers migrate toward FSC-certified, lotion-infused lines, often via e-commerce subscriptions that guarantee stock during peak demand. Value shoppers bulk-buy private-label packs online to offset price creep from pulp cost pass-through. Marketing campaigns that frame tissue as self-care rather than pure utility continue to coax volume to trade up the price ladder, partially balancing the cannibalization risk from bidet adoption in dense urban centers.

By Distribution Channel: Online Gains Erode Offline Shelf Space

Brick-and-mortar remains the primary shopping venue, yet digital share continues to rise each quarter. In 2025, offline outlets held a 54.78% share of the toilet paper market, while online sales are projected to grow at a CAGR of 4.72% through 2031. Supermarkets shrink facings for slow-turning SKUs, opting for narrower assortments to keep footfall-critical categories efficient. Pure-play e-commerce operators exploit low incremental shipping costs once bulk routes are optimized, offering pallet-sized bundles that would overwhelm household vehicles. Subscription enrolment deepens, with leading platforms giving 10-15% discounts and flexible cadence. Omnichannel grocers respond with click-and-collect lockers and same-day delivery promises, but margin dilution looms as freight subsidies must match those of online-only rivals. The channel battle influences pack design choices: lightweight, high-count packs suit courier networks, whereas eye-catching shelf art becomes less relevant.

Emerging markets compress the e-commerce adoption curve. Mobile wallets combined with social-commerce threads push toilet paper to rural households that previous distribution grids underserve. Cross-border platforms ship Chinese bamboo brands directly to Europe, sidestepping middlemen and igniting price competition. The pivot online is persistent, and by 2031, the toilet paper market is expected to see digital routes approach or surpass half of urban sales in several developed economies.

Geography Analysis

North America, with 39.88% of market share in 2025, shows modest unit expansion but steady premium-mix uplift. Bark beetle infestations that damaged 6.3 million forest acres reduced local pulpwood output 15.7% from 2019-2023, heightening import reliance and inflating freight exposure. Suppliers passed a portion of the cost to retail, spurring private-label growth at warehouse clubs. Bidet fixture marketing is gaining traction in coastal metros, chipping away at incremental roll growth but not yet displacing core demand categories such as travel-size packs in consumer staples pantries. Policy discourse around recycled-content mandates remains active, meaning compliance spending continues to rise.

Asia-Pacific is the fastest-growing contributor, expanding at a projected 5.11% CAGR. India’s nationwide toilet drive and rural water grid upgrades unlock vast new demand for tissue. Chinese rural sanitation efforts gather pace, though willingness to pay for premium formats remains muted, steering volume toward value brands sold via e-commerce flash sales. Developed sub-regions such as Japan, South Korea, Australia, and New Zealand maintain high saturation but differ in substitution risk: compact urban units adopt integrated bidet fixtures at rising rates, a longer-run headwind for traditional rolls. Southeast Asian growth accelerates as tourism corridors reactivate and urban wages firm.

Europe’s approximately one-quarter global share is shaped by rule-tight supply chains, widespread recycling, and fragmented mill ownership. EU deforestation regulations heighten audit intensity and compress small-mill margins, triggering consolidation. Germany leads on recovered-fiber penetration, the United Kingdom on brand-led premium traded up, and Southern Europe trails on disposable income but offers growth headroom. Eastern Europe posts solid mid-single-digit growth as organized retail scales. Middle East and Africa, taken together, account for under one-tenth of world revenue but grow ahead of average on hospitality mega-projects in the Gulf states and urbanization across Nigeria, Egypt, and Kenya. South America, from Brazil to Colombia, enjoys moderate demand growth and supplies significant eucalyptus pulp exports that stabilize regional trade balances.

Competitive Landscape

The market is fragmented in nature, with players like Procter and Gamble, Kimberly-Clark, Essity, Georgia-Pacific, and others. These leaders defend their position with integrated pulp assets, marketing heft, and global distribution contracts. Patent expiry on coreless rolls levels the playing field in the innovation space, letting private-label chains and regional converters deliver similar waste-saving functionality. Large mills deploy AI-driven predictive maintenance to raise uptime by up to 30%, narrowing unit-cost gaps and freeing capex for sustainability retrofits.

Digitally native challengers rely on direct-to-consumer engagement, carbon-neutral fulfillment, and transparent ingredient lists. Scaling hurts profitability because shipping bulky products erodes gross margins, yet social media allegiance fosters repeat business. Regional Asian firms ramp capacity to meet explosive urban demand, sometimes through joint ventures that marry international know-how with local price sensitivities. Compliance cost escalation in Europe and North America nudges smaller unintegrated players toward strategic exits or niche specialization, such as agricultural-residue tissue that bypasses forest-origin audits. Over the forecast window, the field will likely compress into a barbell of global majors and agile niche innovators, with middle-tier converters squeezed hardest.

Private-label penetration keeps rising as grocery and discount chains exploit shopper price sensitivity, sourcing from contract converters that leverage open patents and recycled fiber to hit aggressive cost targets. European retailers already attribute 45% of in-aisle toilet paper volume to store brands. Partnerships between retailers and pulp-integrated producers have emerged, giving stores access to chain-of-custody documentation without bearing certification costs directly. Simultaneously, equipment vendors promote turnkey micro-mills that allow regional distributors to backward-integrate and intensify price pressure on established manufacturers.

Toilet Paper Industry Leaders

Procter and Gamble

Kimberly Clarke Corporation

Georgia Pacific LLC

Suzano S.A

Essity AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Kimberly-Clark announced a USD 180 million investment to construct a bamboo-fiber tissue mill in Vietnam, targeting Southeast Asian demand for certified sustainable products.

- January 2026: Procter and Gamble unveiled a blockchain-based pulp traceability program for the Charmin supply chain, committing to full global coverage by 2027.

- December 2025: Georgia-Pacific expanded its United States subscription pilot to Canada, adding bilingual customer support and carbon-neutral logistics.

- October 2025: Procter and Gamble completed a USD 110 million retrofit of its Ohio mill, installing closed-loop water systems projected to lower freshwater draw by 30%.

Global Toilet Paper Market Report Scope

Tissue paper products contribute significantly to maintaining cleanliness, especially concerning personal hygiene. Toilet paper are lightweight and easily disposable which cater to an individual's daily needs. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The Toilet Paper Market Report is Segmented by Product Type (Rolled, Folded, Moist Toilet Tissue, and Biodegradable/Bamboo-Based Rolls), Material Source (Virgin Pulp, Recycled Fiber, and Bamboo and Alternative Fibers), End-User (Household, and Commercial), Distribution Channel (Offline, and Online), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Rolled | Standard Roll |

| Mega/Jumbo Roll | |

| Coreless Roll | |

| Folded | Multifold |

| Interfold | |

| Moist Toilet Tissue | |

| Biodegradable/Bamboo-Based Rolls |

| Virgin Pulp |

| Recycled Fiber |

| Bamboo and Alternative Fibers |

| Household | |

| Commercial | Hospitality and Travel |

| Offices and Institutions | |

| Healthcare Facilities |

| Offline | Supermarket/Hypermarket |

| Convenience and Drug Stores | |

| Other Offline Distribution Channels | |

| Online |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Rolled | Standard Roll | |

| Mega/Jumbo Roll | |||

| Coreless Roll | |||

| Folded | Multifold | ||

| Interfold | |||

| Moist Toilet Tissue | |||

| Biodegradable/Bamboo-Based Rolls | |||

| By Material Source | Virgin Pulp | ||

| Recycled Fiber | |||

| Bamboo and Alternative Fibers | |||

| By End-User | Household | ||

| Commercial | Hospitality and Travel | ||

| Offices and Institutions | |||

| Healthcare Facilities | |||

| By Distribution Channel | Offline | Supermarket/Hypermarket | |

| Convenience and Drug Stores | |||

| Other Offline Distribution Channels | |||

| Online | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the global toilet paper market today and how fast will it grow?

The market stands at USD 56.90 billion in 2026 and is expected to reach USD 66.43 billion by 2031, reflecting a 3.15% CAGR.

Which product type leads worldwide sales?

Rolled formats hold 75.46% revenue share because of entrenched household preference and shelf efficiency.

Where is demand expanding fastest by region?

Asia-Pacific is projected to grow at a 5.11% CAGR, supported by sanitation infrastructure and rising disposable income.

What role does recycled fiber play in current supply?

Recycled fiber accounts for 53.26% of global volume, underpinned by circular-economy policies in Europe and North America.

How is online retail reshaping category dynamics?

Online channels, helped by subscription discounts and doorstep delivery, are forecast to grow at a 4.72% CAGR and steadily erode offline share.

Which strategic moves are market leaders making to stay ahead?

Incumbents invest in certified fiber sourcing, AI-driven efficiency, and premium SKUs while experimenting with direct-to-consumer models.