Talc Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

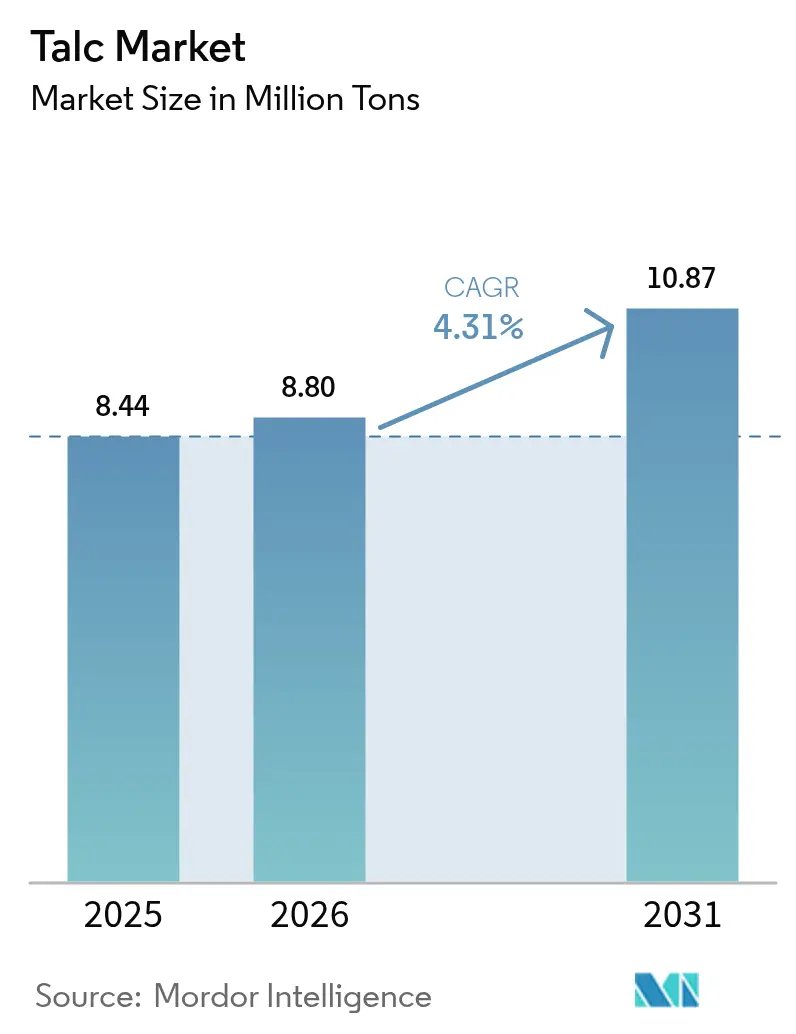

| Market Volume (2026) | 8.80 Million tons |

| Market Volume (2031) | 10.87 Million tons |

| Growth Rate (2026 - 2031) | 4.31% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Talc Market Analysis by ���ϲ�����

The Talc Market size is expected to grow from 8.44 Million tons in 2025 to 8.80 Million tons in 2026 and is forecast to reach 10.87 Million tons by 2031 at 4.31% CAGR over 2026-2031. Rising demand in Asia-Pacific, coupled with application-specific grade optimization, is reshaping trade flows and tightening quality specifications. Ceramics producers in India and Vietnam are adding multi-million-square-meter tile lines, lifting regional offtake, while Chinese automakers mandate lightweight polypropylene (PP) and thermoplastic olefin (TPO) components that embed 15%–25% talc by weight to meet fuel-economy targets. At the same time, China’s GB30981.1-2025 standard for water-based architectural paints, effective June 2026, raises talc loading levels by 30%–40% to maintain opacity and scrub resistance. Persistent North American litigation, the exit of Minerals Technologies, and labor disruptions at Nordic mines temper supply resilience but accelerate investment in AI-enabled ore-sorting to boost recovery rates and lower unit costs.

Key Report Takeaways

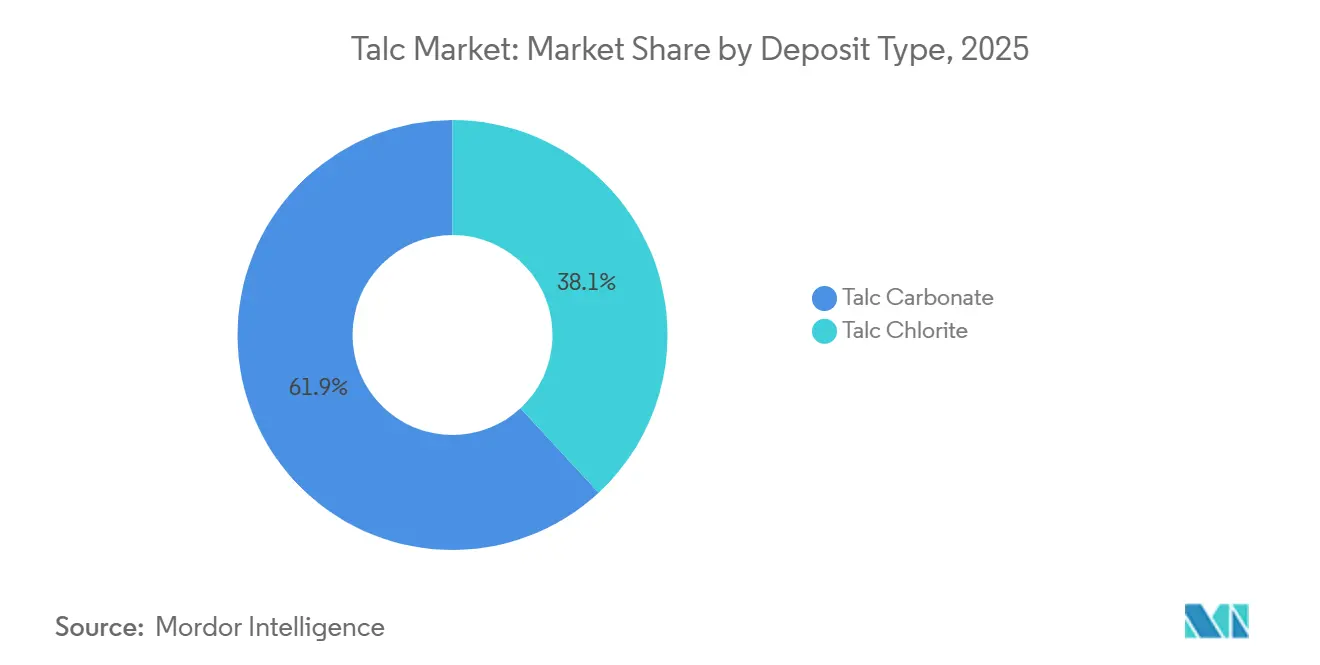

- By deposit type, talc carbonate led with 61.90% of 2025 volume; talc chlorite is forecast to grow at a 4.76% CAGR through 2031.

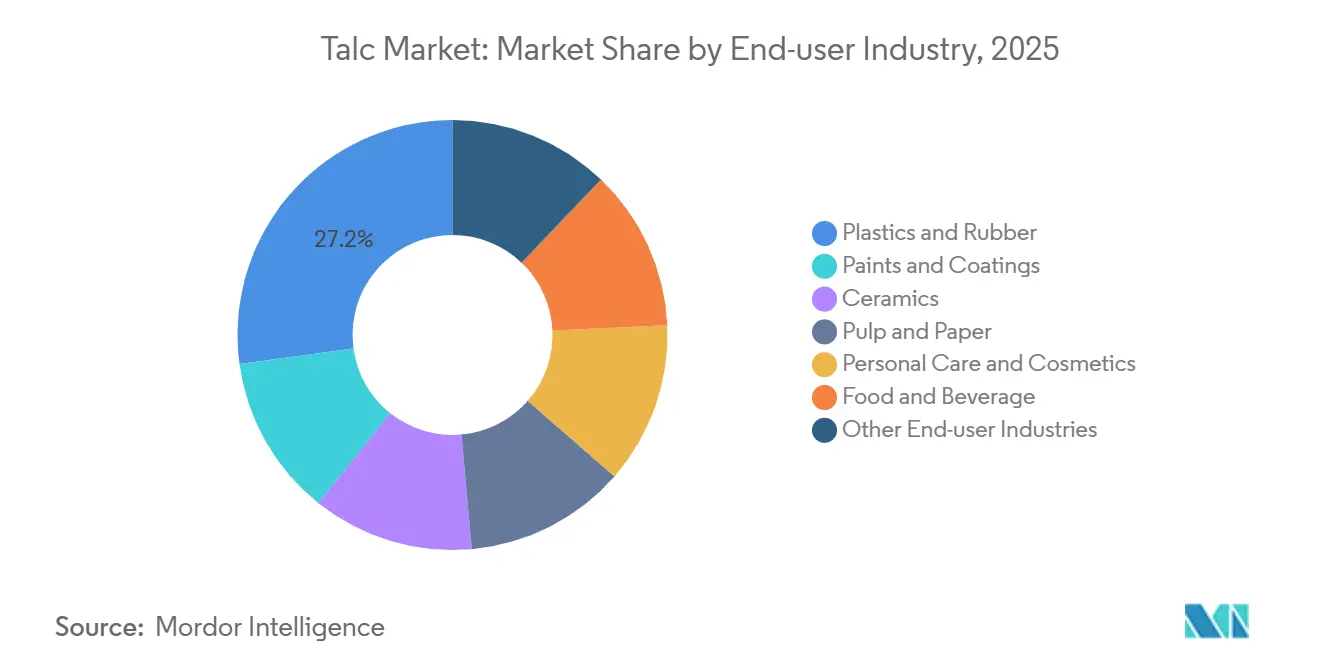

- By end-user industry, plastics and rubber captured 27.15% of 2025 demand and is projected to expand at a 4.98% CAGR over 2026–2031.

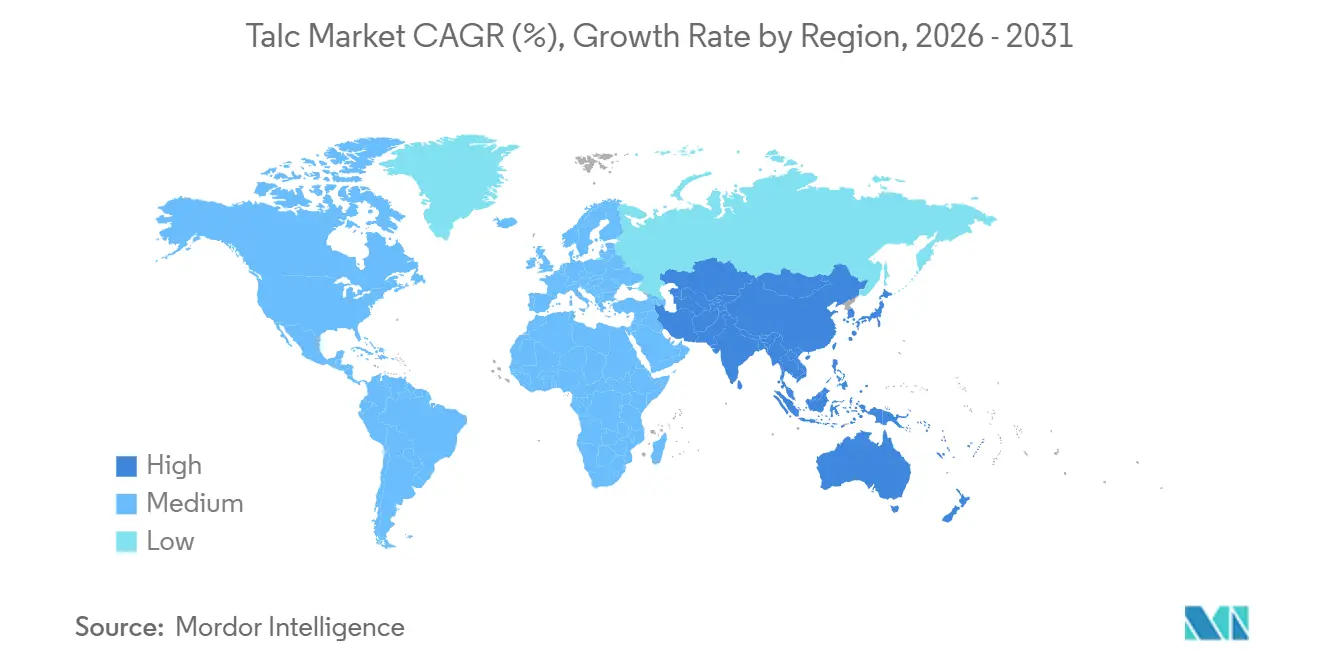

- By geography, Asia-Pacific commanded 53.22% of 2025 consumption and is set to grow at a 5.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Talc Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust PP and TPO Adoption in Automotive Lightweighting | +1.2% | Global, with concentration in China, ASEAN, North America | Medium term (2-4 years) |

| Growing Shift to Water-Based Architectural Paints in Asia | +0.9% | Asia-Pacific core, particularly China, India, Vietnam | Short term (≤ 2 years) |

| Strong Demand for Talc-Filled Polymer Masterbatch in Packaging | +1.1% | Global, with early gains in ASEAN, South Asia, Europe | Medium term (2-4 years) |

| Expansion of Ceramics Production in South and Southeast Asia | +0.8% | India, Vietnam, Thailand, Indonesia | Long term (≥ 4 years) |

| AI-Enabled Ore-Sorting Boosting Ore Recovery and Unit Economics | +0.3% | Global mining regions, early adoption in Australia, Canada, China | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Robust PP and TPO Adoption in Automotive Lightweighting

Automakers embed 15%–25% talc in PP and TPO compounds to achieve stiffness-to-weight ratios that meet fuel-economy and EV-range mandates without retooling injection lines. Imerys opened a EUR 43 million facility in Wuhu in 2025 to supply 30,000 tons of ultra-fine grades targeted at battery housings and interior panels. The OECD projects plastics use in Southeast and East Asia to rise from 60 million tons in 2019 to 150 million tons by 2060, with automotive and electronics driving the steepest slopes. Malaysia’s circular-economy initiative recovered 12,000 tons of PP and ABS from end-of-life vehicles in 2024, a figure expected to triple by 2030. Talc’s nucleating effect shortens molding cycles by 8%–12%, raising throughput for tier-one suppliers operating at 85%–90% capacity utilization.

Growing Shift to Water-Based Architectural Paints in Asia

China’s GB30981.1-2025 caps VOCs at 80 g/L for interior coatings, forcing formulators to adopt aqueous binders that require higher talc loadings. India’s Bureau of Indian Standards is drafting similar limits for notification in late 2026. Water-based systems typically contain 12%–18% talc, up from 8%–12% in solvent-borne paints, because the mineral’s lamellar platelets compensate for lower hiding power. Thailand’s Office of Industrial Economics recorded a 17.27% rise in domestic talc output in 2024, with exports up 14.73% on demand from Vietnam, Indonesia, and the Philippines. Compared with titanium dioxide, talc is priced at USD 150–250 per ton, enabling paint makers to hold shelf prices steady despite inflation in other additives.

Strong Demand for Talc-Filled Polymer Masterbatch in Packaging

Flexible-packaging converters dose 3%–5% talc masterbatch into polyethylene and polypropylene films to improve slip and anti-block properties at high line speeds. The OECD estimates packaging will account for 40% of incremental plastics volume in ASEAN through 2060, translating into 15,000–20,000 additional tons of talc demand per year. Talc’s platelet morphology reduces coefficient of friction from 0.5 to 0.3, cutting web breaks by half and justifying a USD 0.02–0.03 per kg premium for pre-compounded masterbatch. EU Ecolabel criteria now award points for mineral fillers that displace virgin polymer, indirectly favoring talc in retail and e-commerce packaging[1]European Commission, “EU Ecolabel Criteria for Plastic Carriers,” ec.europa.eu . Masterbatch suppliers are co-locating plants within 50 km of major film extruders to tighten logistics and raise switching costs.

Expansion of Ceramics Production in South and Southeast Asia

India’s ceramic-tile revenue reached INR 51,000–53,000 crore (USD 6.1–6.4 billion) in FY 2025 on 6%–7% domestic volume growth. Kajaria, Somany, and Asian Granito announced 25.4 million m² of new capacity, requiring 45,000–50,000 tons of talc annually. Vietnam’s tile exports to the United States and EU climbed 22% in 2024, prompting investment in roller kilns that shorten firing times from 50 minutes to 35 minutes, demanding tighter talc particle distributions. Thailand and Indonesia are each adding 8–10 million m² of glazed porcelain lines to exploit anti-dumping gaps in Middle Eastern and African markets. Talc lowers firing temperature by 30–50 °C, delivering natural-gas savings of 10%–12% when energy exceeds USD 8 per MMBtu.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Asbestos-Related Litigation Costs | -0.6% | North America, Europe, with spillover to Australia | Long term (≥ 4 years) |

| Bio-Based Fillers Replacing Talc in Premium Papers | -0.4% | Europe, North America | Medium term (2-4 years) |

| High-Purity Ore Shortages in Europe After Finnish Labor Strike | -0.3% | Europe, with secondary impact on North America and Asia pharmaceutical/food-grade buyers | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Persistent Asbestos-Related Litigation Costs

Johnson & Johnson offered USD 10 billion in May 2024 to settle 62,000 ovarian-cancer claims tied to cosmetic talc. The proposal remains in limbo after successive Chapter 11 filings by LTL Management were dismissed, prolonging uncertainty for upstream miners. Minerals Technologies booked a USD 215 million provision in Q1 2025 to fund a trust for 684 open cases, after divesting Barretts Minerals for USD 32 million. Imerys obtained 90% creditor approval in January 2025 for its North American restructuring, ring-fencing legacy liabilities but constraining balance-sheet flexibility. Insurance premiums on talc producers’ primary layers rose 40%–60% in 2025, while aggregate limits tightened to USD 50–100 million, compelling mid-tier players to self-insure or exit cosmetic grades.

Bio-Based Fillers Replacing Talc in Premium Papers

European and North American mills are shifting to precipitated calcium carbonate, kaolin, and cellulose nanofibers to satisfy brand-owner sustainability mandates. Talc’s share in European paper applications fell from 12% in 2020 to below 9% in 2025. Alternatives cost 5%–10% more yet qualify for carbon-capture credits under the EU Emissions Trading System, closing the economic gap. Micro-fibrillated cellulose trials at 2%–4% loadings deliver 15%–20% tensile-strength gains, enabling basis-weight down-gauging that offsets higher raw-material costs. The European Commission’s proposed Ecodesign for Sustainable Products Regulation, slated for 2028, will require material passports—a transparency obligation that disadvantages feedstocks with opaque mining footprints. U.S. specialty paper producers echo the shift as luxury-goods brands commit to plastic-free packaging.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deposit Type: Chlorite Grades Gain in Specialty Applications

Talc carbonate accounted for 61.90% of 2025 tonnage, thanks to abundant metamorphic belts in China, India, and Brazil that yield cost-effective ore for plastics, paints, and ceramics. Talc Chlorite, holding the balance, will expand at a 4.76% CAGR as automotive and electronics customers impose sub-50 ppm iron limits impossible for many carbonate ores. Chlorite talc delivers less than 0.05% iron versus 0.15%–0.30% for carbonate, eliminating color shift in white automotive trim and cutting bleaching costs in cosmetic formulations. Chlorite grades fetch a USD 50–100 premium but reduce kiln CO₂ evolution by 8%–12%, aiding EU carbon-pricing compliance. Finnish labor strikes in 2024 sidelined 40,000–50,000 t/y, forcing buyers to pre-book 60%–70% of annual needs under fixed-price contracts, a structural move that reshapes the talc market share at the value-added end of the spectrum.

Stockpiling by Japanese and South Korean electronics firms illustrates tightness: importers doubled safety inventories to 45 days in 2025, up from 22 days pre-strike, insulating supply chains yet locking in working capital. Indian processors eye Western Australia’s chlorite veins to diversify sourcing and hedge currency exposure. Carbonate ore remains indispensable for construction fillers and rubber, where price outweighs purity.

By End-user Industry: Plastics and Rubber Lead Growth Amid Lightweighting Push

Plastics and rubber consumed 27.15% of global tonnage in 2025, and this slice will widen as the segment logs a 4.98% CAGR through 2031. PP compounds with 20%–30% talc achieve flexural modulus above 2,500 MPa, letting automakers thin wall sections by 15%–20% and cut vehicle weight by 4–5 kg per car. Imerys’s Wuhu plant targets ultra-fine talc for electric-vehicle battery housings, priced at USD 400–500 per ton, underpinning a high-margin niche.

Paints and coatings are benefiting from Asia’s pivot to low-VOC water-borne systems. Ceramics demand is driven by India’s affordable-housing boom and Vietnam’s export surge. Pulp and paper, personal care and cosmetics, and food and beverage face substitution from bio-based fillers and heightened safety oversight. The FDA’s 2024 guidance that each cosmetic-talc batch undergoes microscopy testing inflates per-batch costs by USD 5,000–10,000. Ancillary segments such as roofing membranes and sealants mirror construction cycles in emerging economies, offering mid-single-digit growth.

Geography Analysis

Asia-Pacific’s 53.22% slice in 2025 and a 5.18% forecast CAGR rely on synchronized forces. India’s ceramic sector generated INR 51,000–53,000 crore (USD 6.1–6.4 billion) in FY 2025, underpinned by 6%–7% domestic tile demand and 25.4 million m² of announced capacity. Vietnam’s tile exports jumped 22% in 2024 after anti-dumping rulings against Chinese products, spurring investment in roller-kiln retrofits that demand finer talc to avert warping. China’s GB30981.1-2025 VOC cap forces formulators to raise talc in water-based paints by 30%–40%. Thailand’s 17.27% rise in 2024 output reflects its role as an ASEAN processing hub. OECD long-range models see regional plastics demand tripling to 150 million tons by 2060, locking talc into the lightweighting narrative. Japan and South Korea specialize in chlorite-grade imports for electronics and pharma, where sub-ppm heavy-metal limits create high barriers to entry.

North America’s growth is restricted owing to litigation and producer exits. Minerals Technologies’ April 2024 sale of Barretts Minerals for USD 32 million underscores the squeeze between liability risk and operating returns. Johnson & Johnson’s unresolved USD 10 billion proposal magnifies insurance costs, adding 40%–60% to premiums. U.S. mines in Montana and Vermont still supply automotive and paints customers, but new permits evolve slowly amid public scrutiny. In Canada and Mexico, primarily in auto plastics, covered by USMCA rules favouring local content. The FDA’s 2024 microscopy mandate raises batch-testing costs, nudging niche cosmetics brands toward starch alternatives[2]U.S. FDA, “Testing of Talc-Containing Cosmetic Products,” fda.gov .

Europe is curbed by bio-based substitution in premium paper and the March 2025 bankruptcy of Imerys Talc Italy. Nordic chlorite operations feed pharmaceutical and food-contact markets, strike, tighten spot supply, and drive buyers to commit 60%–70% of annual needs under take-or-pay terms. Germany, France, the UK, and Italy’s consumption spans automotive, architectural paints, and ceramics. The EU’s forthcoming Ecodesign Regulation, which will require material passports from 2028, favors fillers with transparent provenance and lower life-cycle carbon, putting cost pressure on energy-intensive talc producers. South America and the Middle-East and Africa together take a smaller share, led by Brazil’s auto plastics and Saudi Arabia’s nascent ceramics clusters, though currency swings and logistics bottlenecks limit velocity.

Competitive Landscape

The talc market is moderately concentrated. The five largest players—Imerys, Golcha Group, Sibelco, Magris Performance Materials, Minerals Technologies Inc. and IMI Fabi SpA controlled 40%–45% of global capacity, while hundreds of regional miners in China, India, and Brazil fragment the rest. Golcha Group leverages 24 million tons of reserves in Rajasthan, extracting 300,000 tons of crude and processing 200,000 tons of finished talc annually, capturing USD 20–30 per ton in freight savings inside a 500 km radius. Imerys pivoted toward specialty automotive and electronics grades, commissioning its Wuhu plant in 2025, expected to deliver EUR 30 million in annual sales when fully ramped. Sibelco and Nippon Talc employ in-line particle-size analyzers that cut batch variation below 2%, meeting tier-one automotive tolerances beyond the reach of smaller Asian competitors.

Riverspan Partners, a private-equity entrant, bought Barretts Minerals for USD 32 million with plans to pivot away from cosmetic grades to industrial fillers, sidestepping litigation drag. Technology adoption is uneven: Australian and Canadian mines integrate AI-enabled ore sorting, shaving energy use by 10%–12%, whereas many Chinese pits still hand-pick ore, widening cost spreads. The FDA’s 2024 microscopy rule raises the bar for ISO 17025 labs, indirectly consolidating supply among vertically integrated processors. Meanwhile, insurers have narrowed aggregate coverage, prompting self-insurance or cosmetic-grade withdrawal among mid-tier firms. Against this backdrop, specialty chlorite suppliers enjoy pricing power, while carbonate producers fight commoditization through logistics optimization and service bundling.

Talc Industry Leaders

Imerys

Magris Performance Materials

Golcha Group

Minerals Technologies Inc.

IMI Fabi SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Cuticura introduced a new talc product promising 8-hour freshness, supported by a branding campaign on Kochi Metro trains. The campaign aims to target Onam festival-goers, utilizing Kochi Metro's extensive reach to highlight the product's features and enhance visibility.

- June 2024: Dabur India introduced Cool King Icy Perfume Talc, incorporating a distinctive double-burst cooling formula and offering 12 hours of icy freshness. The launch was intended to deliver a refreshing and fragrant talc experience to users.

Global Talc Market Report Scope

Talc is a naturally occurring mineral mined from the earth and made up of magnesium, silicon, oxygen, and hydrogen. It is a hydrous magnesium silicate used in many industries, including plastics, rubber, paints, paper, and pharmaceuticals.

The Talc Market is segmented by deposit type, end-user industry, and geography. By deposit type, the market is segmented into talc carbonate and talc chlorite. By end-user industry, the market is segmented into plastics and rubber, paints and coatings, ceramics, pulp and paper, personal care and cosmetics, food and beverage, and other end-user industries. The report also covers the market size and forecasts for talc in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

| Talc Carbonate |

| Talc Chlorite |

| Plastics and Rubber |

| Paints and Coatings |

| Ceramics |

| Pulp and Paper |

| Personal Care and Cosmetics |

| Food and Beverage |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Deposit Type | Talc Carbonate | |

| Talc Chlorite | ||

| By End-user Industry | Plastics and Rubber | |

| Paints and Coatings | ||

| Ceramics | ||

| Pulp and Paper | ||

| Personal Care and Cosmetics | ||

| Food and Beverage | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will the talc market be by 2031?

It is forecast to reach 10.87 million tons by 2031, advancing at a 4.31% CAGR from 2026 to 2031.

Which end-use segment will add the most incremental talc demand?

Plastics and rubber are projected to post the fastest 4.98% CAGR as automakers and packaging converters intensify lightweighting and performance requirements.

Why is Asia-Pacific the dominant consumption region?

Ceramics capacity additions, automotive lightweighting mandates, and new water-based paint regulations lift Asia-Pacific to 53.22% of global volume with a 5.18% CAGR through 2031.

How is litigation influencing North American supply?

Ongoing asbestos-related lawsuits have prompted producer exits, raised insurance premiums by 40%–60%, and capped regional growth at roughly 3% through 2031.

What advantages do chlorite-grade deposits offer?

Chlorite talc contains less than 0.05% iron, meets premium purity standards, lowers kiln CO₂ emissions by up to 12%, and therefore secures higher pricing in automotive, electronic, and cosmetic applications.

Page last updated on: