Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

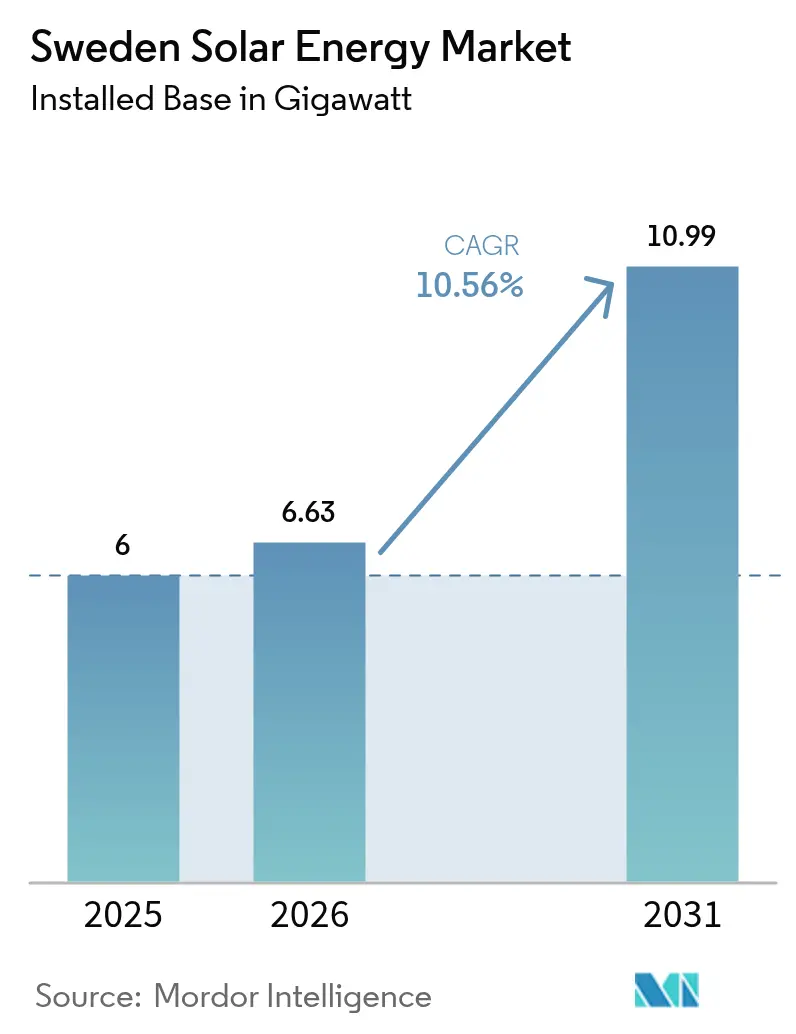

| Base Year Market Size (2025) | 6 gigawatt |

| Market Volume (2026) | 6.63 gigawatt |

| Market Volume (2031) | 10.99 gigawatt |

| Growth Rate (2026 - 2031) | 10.56% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Sweden Solar Energy Market Analysis by ���ϲ�����

The Sweden Solar Energy Market size in terms of installed base is expected to grow from 6 gigawatt in 2025 to 6.63 gigawatt in 2026 and is forecast to reach 10.99 gigawatt by 2031 at 10.56% CAGR over 2026-2031.

Demand momentum is currently strongest in the residential segment because the 20% Grön Teknik tax deduction continues through June 2025, yet the looming cut to 15% and the abolition of the SEK 0.60 per kWh micro-production credit in early 2026 are reshaping project timing.[1]Swedish Tax Agency, “Grön Teknik Deduction,” skatteverket.se Corporate power-purchase agreements tied to data-center and battery manufacturing loads are accelerating utility-scale pipelines, while module prices that fell below EUR 0.10 per Wp in 2024 have compressed equipment costs and intensified installer competition.[2]Bloomberg, “European Solar Module Pricing Trends,” bloomberg.com Grid queues that average 501 days, a certified-installer shortfall, and Sweden’s low winter irradiation temper growth, but battery coupling, vertical bifacial agrivoltaics, and land-lease partnerships with state forestry firm Sveaskog are opening new niches.[3]Svenska Kraftnät, “Grid Connection Timelines,” svk.se Competitive strategies, therefore, hinge on securing grid capacity, bundling storage, and tailoring technology to Nordic light conditions rather than chasing headline wattage alone.

Key Report Takeaways

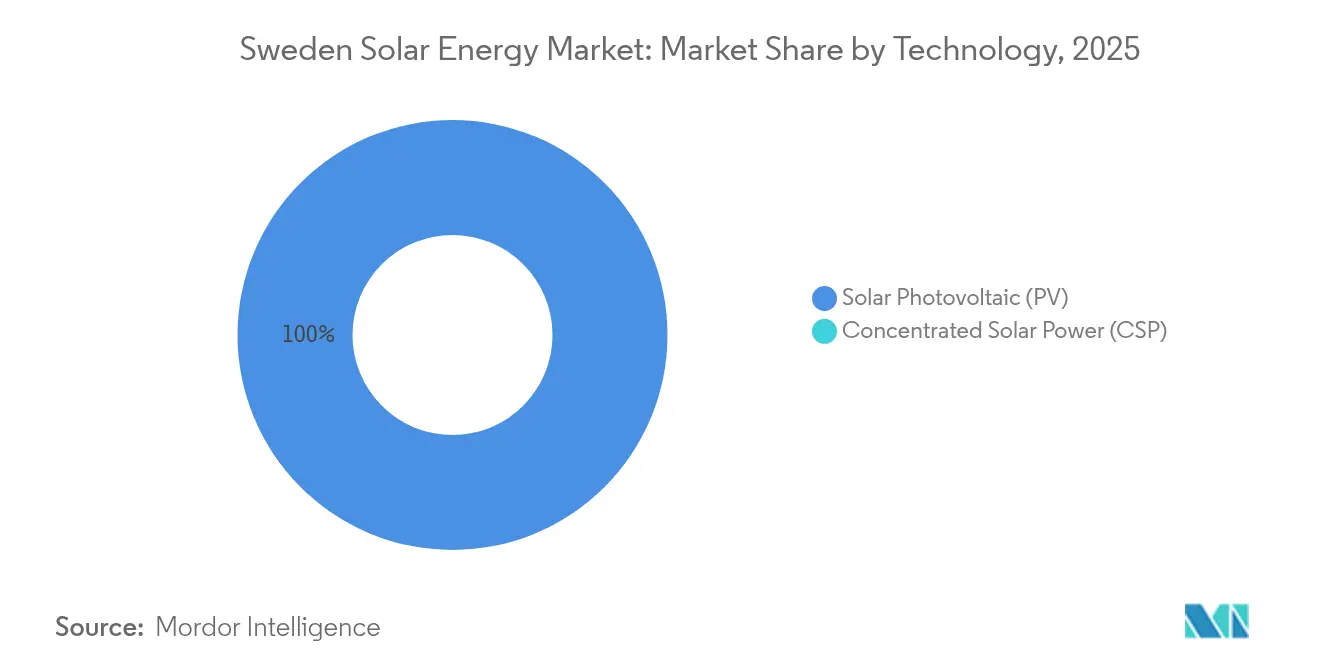

- By technology, photovoltaic systems held 100% of capacity in 2025, and crystalline silicon will continue to dominate while thin-film CIGS captures weight-restricted rooftops.

- By grid type, on-grid systems accounted for 87.20% of 2025 installations, yet off-grid systems are advancing at a 16.62% CAGR through 2031 as remote industries bypass connection delays.

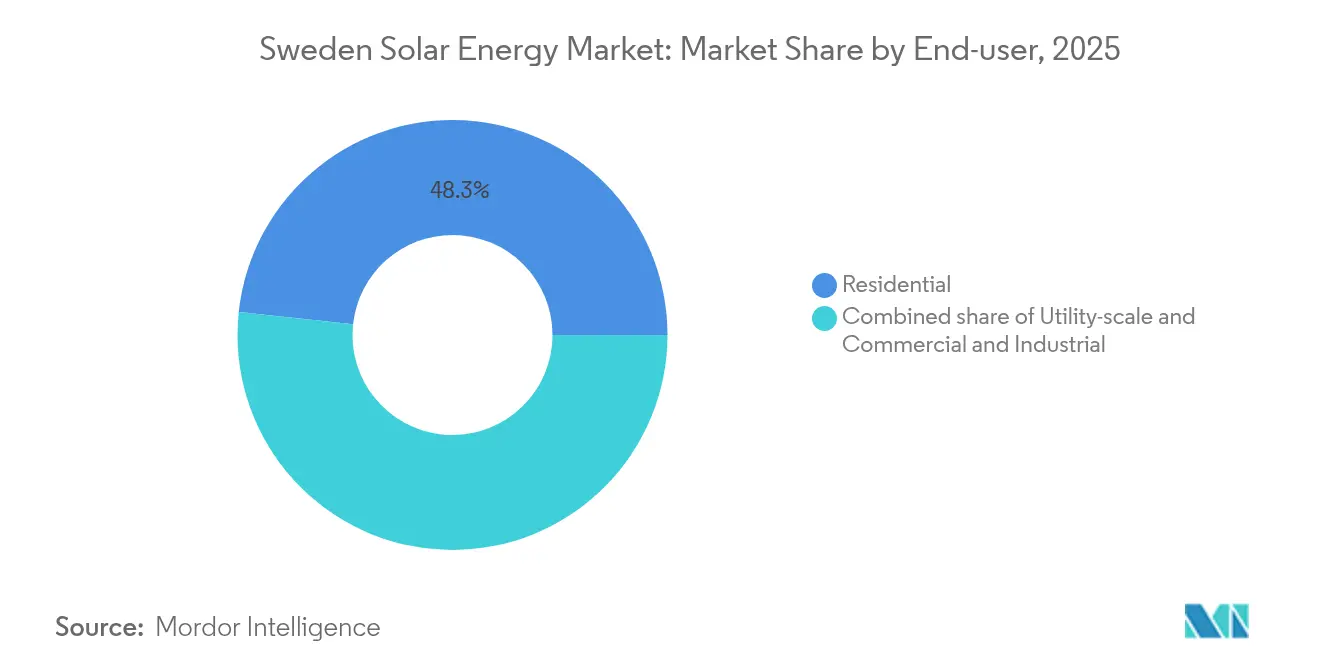

- By end-user, residential rooftops led with 48.30% of the Sweden solar energy market share in 2025, whereas utility-scale plants are the fastest-growing segment at 27.36% CAGR to 2031.

- By geography, southern regions delivered roughly 59.30% of 2025 additions and are set to retain volume leadership, but central Sweden offers the highest pipeline growth, where land leases with Sveaskog de-risk permitting.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sweden Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grön Teknik rebate remains until mid-2025 | +1.8% | Nationwide, strongest in southern Sweden | Short term (≤ 2 years) |

| EU Fit-for-55 and RED-III acceleration areas | +2.3% | Nationwide under EU mandates | Medium term (2–4 years) |

| Module prices below EUR 0.10 per Wp | +2.1% | Nationwide with Nordic spillover | Short term (≤ 2 years) |

| Corporate PPAs from data-center and battery plants | +2.5% | Southern and central industrial hubs | Medium term (2–4 years) |

| Grid-flexible rooftop-battery subsidy (proposed) | +1.4% | Stockholm, Gothenburg, Malmö | Medium term (2–4 years) |

| Agrivoltaic vertical bifacial adoption | +0.7% | Rural south and central | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Sweden’s Grön Teknik Rebate Until Mid-2025

The Grön Teknik deduction sustains a 20% tax credit through June 2025, encouraging residential owners to advance purchase decisions before the rate falls to 15%. The looming change elongates payback periods from 8–10 years to 10–12 years for a typical 6 kW system, even after factoring module prices near EUR 0.09 per Wp.[4]Swedish Tax Agency, “Grön Teknik Deduction,” skatteverket.se Installers, therefore, report a surge in first-half 2025 bookings that risks a post-July demand cliff. Larger rooftops above 25 kW remain excluded from the deduction cap, which channels more growth toward smaller homes. As a result, residential contractors are accelerating hiring and inventory purchases to capture the transient peak.

EU Fit-for-55 and RED-III Acceleration Areas

Sweden’s revised National Energy and Climate Plan doubles its 2030 solar target in line with RED-III and requires renewable acceleration zones by May 2025.[5]European Commission, “RED-III Guidelines,” ec.europa.eu Designating brownfield sites and industrial roofs could trim permitting from 501 days to under 180 days, but municipal veto powers persist. Divergent local policies already led Skåne to reject a 50 MW park despite grid approval, confirming that southern pro-renewable councils will attract most near-term capital. Developers, therefore, map municipality attitudes as carefully as irradiation maps when screening sites.

Module Prices Below EUR 0.10 per Wp

Chinese oversupply drove European spot prices down 40% in 2024 to EUR 0.08–0.10 per Wp. The collapse squeezed residential installer margins to 8–12% and triggered a wave of consolidation, including three regional acquisitions by Svea Solar. Utility-scale developers responded by locking in multiyear supply contracts at fixed EUR 0.09 per Wp ahead of possible trade tariffs in 2026. With polysilicon producers operating near cash-cost at EUR 0.08 per Wp, further declines look limited, shifting buyer focus from price to warranty terms and logistics certainty.

Corporate PPAs From Data-Center and Battery Plants

Data-center demand is forecast to reach up to 5 TWh by 2030, and Microsoft extended its 24/7 carbon-free pledge to its Swedish campuses in 2024. Vattenfall therefore signed a 10-year 150 GWh PPA that bundles 50 MW of solar with 20 MWh of batteries, creating the first hourly matched solar contract in Sweden. Battery maker Northvolt, consuming 1.5 TWh annually, has signaled interest in similar structures. These contracts underpin revenue certainty for new utility-scale arrays, accelerating ground-mount finance decisions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low winter irradiation and seasonal mismatch | −1.5% | National, strongest in the north | Long term (≥ 4 years) |

| Distribution-grid congestion and lengthy permits | −2.2% | Nationwide, acute in the south | Medium term (2–4 years) |

| Certified installer shortage | −1.1% | Urban labor markets | Short term (≤ 2 years) |

| Rooftop competition from green roofs and EV chargers | −0.6% | Stockholm, Malmö, Gothenburg | Medium term (2–4 years) |

| Source: ���ϲ����� | |||

Low Winter Irradiation and Seasonal Mismatch

Solar capacity factors range from 10% in Norrbotten to 12% in Skåne, with December and January delivering less than 2% of annual output. Swedish demand peaks during winter heating, forcing rooftop owners to export summer surplus at negative prices while buying expensive winter power. Hydro reservoirs currently absorb 10–15 TWh of balancing duties, but that flexibility caps Sweden’s export revenues under Nord Pool. Utility developers respond by co-locating batteries sized for four to six hours of discharge, yet storage adds SEK 2–3 per watt to capital costs, slowing adoption outside corporate PPA structures.

Distribution-Grid Congestion and Lengthy Permits

Connection approval still takes a median of 501 days, and southern zones can exceed 600 days. The legacy 10 kV network was designed for central hydro rather than two-way rooftop flows. Upgrading a single substation costs SEK 5–10 million, and distribution operators are hesitant to socialize that expense. Svenska Kraftnät’s maturity-based queue favors projects with financing and land permits, disadvantaging small developers. The result is a secondary market in grid-ready projects that inflates development premiums and concentrates ownership among capital-rich entities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Photovoltaic Dominance Under Nordic Light Conditions

Solar PV held 100% of the Sweden solar energy market in 2025 because low direct normal irradiance renders CSP unviable. Crystalline silicon commands the bulk of installations at 20–22% module efficiency. The Sweden solar energy market size for PV technology is projected to grow from 6 GW in 2025 to about 10.99 GW by 2031 at a 10.56% CAGR. Thin-film CIGS panels address rooftops that cannot tolerate the 15–25 kg per m² weight of crystalline modules, and Midsummer’s 200 MW factory in Flen will supply that niche with deliveries from 2026.

Bifacial modules are advancing in utility arrays because vertical east-west layouts raise yield by 10–15% through diffuse and snow-albedo gains. R&D also centers on perovskite-silicon tandem cells, with a EUR 2.8 million EU grant issued in April 2025 to push efficiencies past 30%. Although pilot production is unlikely before 2027, sustained funding suggests technology competition will emphasize application specificity over headline watt cost.

By Grid Type: Off-Grid Uptick as Developers Evade Queues

On-grid arrays represented 87.20% of 2025 capacity, yet off-grid systems are expanding at 16.62% CAGR because remote mines, telecom towers, and farms are unwilling to wait 501 days for interconnection. The Sweden solar energy market size for off-grid installations stood near 0.77 GW in 2025 and could exceed 1.93 GW by 2031. Cabin owners typically deploy 3–5 kW solar with 10–15 kWh of lithium-ion storage, whereas industrial microgrids combine 100 kW solar with 250–300 kWh batteries to replace diesel. Regulatory proposals to compensate residential batteries for frequency reserve could blur the on-grid and off-grid boundary, since homeowners would stay connected for ancillary revenue yet avoid summer exports.

Larger grid-tied farms face curtailed returns once the micro-production credit ends in 2026, steering developers toward “zero-export” inverter settings and on-site storage. The resulting self-consumption model raises internal rates of return if discharged during evening peaks when spot prices average SEK 1.20 per kWh, far higher than midday lows.

By End-User: Utility-Scale Surge Rebalances the Mix

Residential rooftops delivered 48.30% of 2025 additions because high electricity prices and the 20% deduction favored homeowners. Utility-scale projects, however, will grow fastest at 27.36% CAGR, lifting their share from 31.20% in 2025 to more than 46.30% by 2031. The Sweden solar energy market share for utility-scale plants is therefore on track to overtake the residential segment soon after the subsidy cut. Ground-mount economics benefit from capital costs of SEK 6–7 per watt and 10–15 year PPAs with creditworthy buyers such as Microsoft.

C&I rooftops bridge the two extremes. Average systems of 50–150 kW shave demand charges and qualify for emerging grid-flexible battery incentives. Yet green-roof mandates and competing EV charger conduits constrain usable roof area in Stockholm and Malmö. The trajectory of this middle segment hinges on whether a proposed 30% battery-cost subsidy survives parliamentary review in 2025.

Geography Analysis

Southern counties (Skåne, Västra Götaland, Stockholm) delivered roughly 59.30% of Sweden’s 2025 solar additions because irradiation reaches 1,100 kWh per m², about 20% higher than northern averages. They also host the densest transformer capacity, reducing grid reinforcement charges. Competition for agricultural land remains intense, so developers increasingly lease parcels from institutional owners such as Sveaskog, which offered 70 hectares in Skåne at SEK 8,000–12,000 per hectare annually.

Central Sweden (Östergötland, Södermanland) is emerging as an agrivoltaics testbed. A 1 MW vertical bifacial pilot in Östergötland generated 1.2 GWh per year while cutting wheat yield by only 3–5%. However, grid connection lines can cost SEK 1.5–2.0 million per km, so most pilots remain below 5 MW. Expected acceleration-area zoning under RED-III could compress permitting to 180 days in pro-renewable municipalities, yet local veto power still introduces asymmetry, making site scouting a municipality-by-municipality exercise.

Northern regions (Norrbotten, Västerbotten) attract projects that serve industrial loads such as Northvolt’s 1.5 TWh gigafactory. Land leases cost less than SEK 5,000 per hectare annually, but low irradiation holds capacity factors near 10%. Battery co-location, therefore, becomes essential to arbitrage intraday price spreads that widen when hydro dams throttle exports. Svea Solar’s 12 MW battery park for Luleå Energi illustrates this logic, capturing SEK 1.5–2.0 million per year in price differences between midday lows and evening peaks.

Competitive Landscape

The top five players, Vattenfall, Svea Solar, Soltech Energy, E.ON, and Fortum, controlled roughly 40–45% of installed capacity in 2024, indicating moderate concentration. Utilities regard solar as a diversification hedge: Vattenfall allocated SEK 19 billion of its SEK 170 billion 2025–2029 plan to “other renewables,” compared with SEK 77 billion for wind. Pure-play operators fill the gap. Svea Solar is vertically integrating by locking in 2 GW of land through Sveaskog, while also adding storage EPC capacity to bid on utility PV plus battery packages.

On the manufacturing side, Midsummer is scaling domestic thin-film output, reducing exposure to Chinese module tariffs. Exeger pursues consumer electronics with dye-sensitized cells, yet its SEK 13.3 million revenue in 2023 underscores the pre-commercial status of that segment. ABB holds about 25–30% of the Swedish inverter supply, giving it pricing power but leaving project-development margins untouched. Installer consolidation is ongoing: three acquisitions by Svea Solar in 2024 and Soltech Energy’s sale of its Ramsjöholm solar park to fund battery assets reveal a shift toward storage and service bundling as pure EPC returns tighten.

Sweden Solar Energy Industry Leaders

Exeger Sweden AB

Vattenfall AB

Svea Solar AB

Eneo Solutions AB

Soltech Energy Sweden AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Midsummer secured a EUR 2.8 million EU Innovation Fund grant to develop perovskite-silicon tandem cells targeting >30% efficiency, with pilot output slated for 2027.

- April 2025: Soltech Energy’s 28 MWh battery park in Lerum entered commissioning for frequency regulation services.

- August 2024: Svea Solar, Sveaskog, and Alight agreed to co-develop 2 GW of ground-mounted solar over five years, including 150 hectares in central Sweden.

- August 2024: Vattenfall signed an Industrikraft pact with Swedish heavy industry to co-invest in solar-plus-storage as part of its SEK 80 billion national allocation.

- July 2024: Midsummer received EUR 8 million from Invitalia to expand CIGS output in Italy, diversifying European manufacturing.

- April 2024: Midsummer confirmed a 200 MW CIGS factory in Flen backed by EUR 32.3 million from the EU Innovation Fund, with production commencing in 2026.

Sweden Solar Energy Market Report Scope

Solar energy is a type of renewable energy in which solar panels are used to generate electricity. Solar panels deployed on rooftops or mounted on the grounds are utilized effectively by end users, including residential, commercial & industrial (C&I), and utilities. Solar energy has become the fastest-growing renewable energy source owing to the country's supporting government initiatives and surging investments in renewable energy projects.

The Sweden Solar Energy Market Report is Segmented by Technology (Solar Photovoltaic (PV), Concentrated Solar Power (CSP)), Grid Type (On-Grid, Off-Grid), End-User (Utility-Scale, Commercial and Industrial (C&I), Residential), and Component (Qualitative Analysis only). The report offers the market size and forecasts in terms of installed capacity in MW for all the above segments.

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

How large is the Sweden solar energy market in 2026?

Installed capacity stands at about 6.63 GW in 2026, on track toward 10.99 GW by 2031.

What is driving new utility-scale solar in Sweden?

Corporate PPAs from data-center and battery factories, plus land-lease deals with Sveaskog, are underpinning most large projects.

How will the Grön Teknik change affect residential solar?

Cutting the deduction from 20% to 15% in July 2025 and ending the micro-production credit in 2026 will lengthen rooftop payback periods by roughly two years.

Why are off-grid systems growing quickly?

Remote industrial sites prefer to avoid 501-day grid queues and use solar plus battery microgrids for energy autonomy.

Which technology is gaining momentum on Swedish farms?

Vertical bifacial arrays enable agrivoltaics that preserve crop yield while boosting energy output by 1015%.

What hurdle most limits near-term solar deployment?

Distribution-grid congestion in southern zones currently imposes the longest delays and highest upgrade costs.

Page last updated on: