Sweden Data Center Power Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

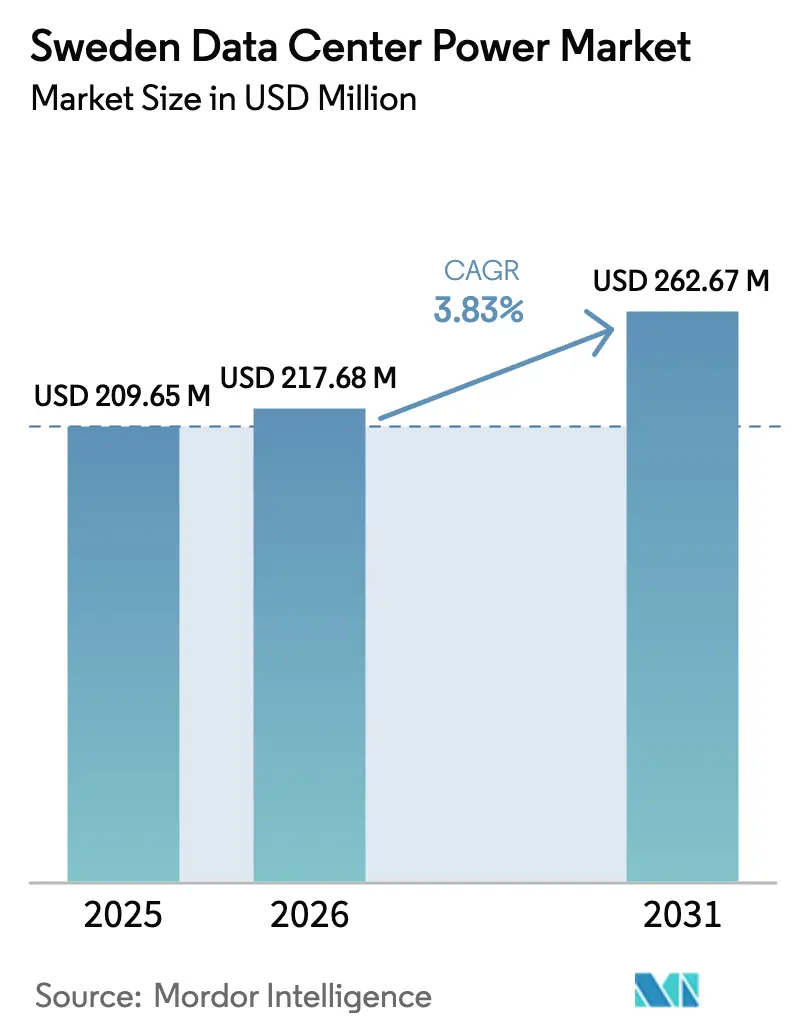

| Base Year Market Size (2025) | USD 209.65 Million |

| Market Size (2026) | USD 217.68 Million |

| Market Size (2031) | USD 262.67 Million |

| Growth Rate (2026 - 2031) | 3.83% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Sweden Data Center Power Market Analysis by ���ϲ�����

Sweden data center power market size in 2026 is estimated at USD 217.68 million, growing from 2025 value of USD 209.65 million with 2031 projections showing USD 262.67 million, growing at 3.83% CAGR over 2026-2031. Moderate headline growth conceals a structural shift toward higher power density as hyperscale AI projects move rack loads from 5–10 kW to 50–100 kW. Operators are responding with medium-voltage switchgear, grid-interactive UPS, and battery energy storage that unlock new ancillary-service revenues while complying with stringent uptime needs. The 97% electricity tax rebate keeps delivered energy costs among Europe’s lowest, reinforcing Sweden’s appeal for carbon-aware investors. Development is pivoting northward where renewable headroom is abundant, yet Stockholm still commands premium colocation demand despite longer grid-connection queues, sustaining healthy competition across the Sweden data center power market.

Key Report Takeaways

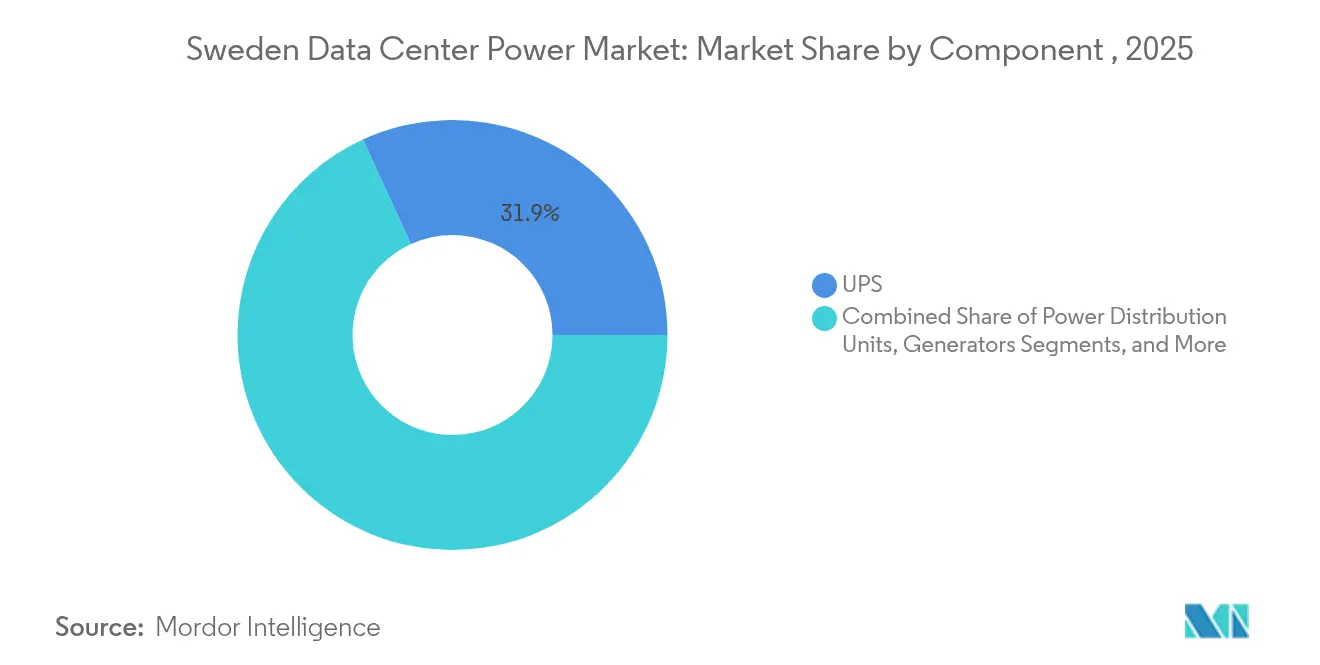

- By component, UPS Systems led with 31.85% of Sweden's data center power market share in 2025, while PDUs are forecast to grow at a 5.69% CAGR through 2031.

- By data center type, colocation providers held 46.90% revenue share in 2025, and the segment is expected to expand at a 5.19% CAGR to 2031.

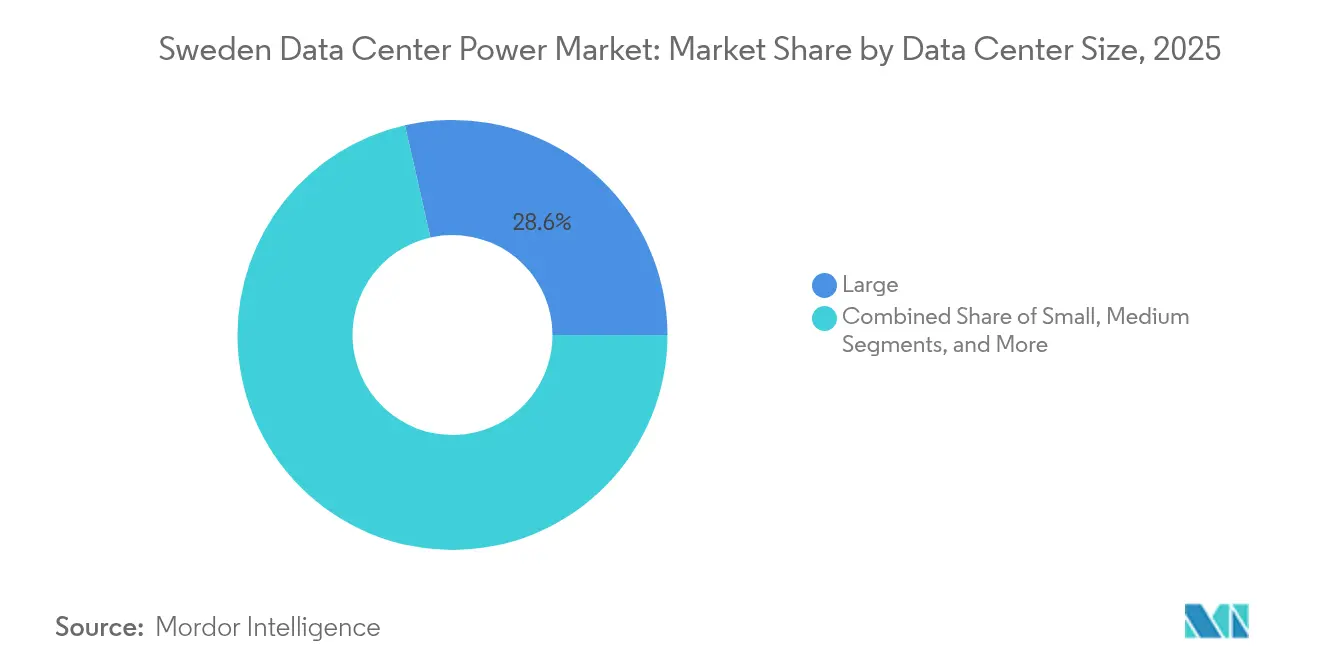

- By data center size, large facilities accounted for 28.55% of the Sweden data center power market size in 2025; massive facilities are projected to advance at a 4.58% % CAGR between 2026 and 2031.

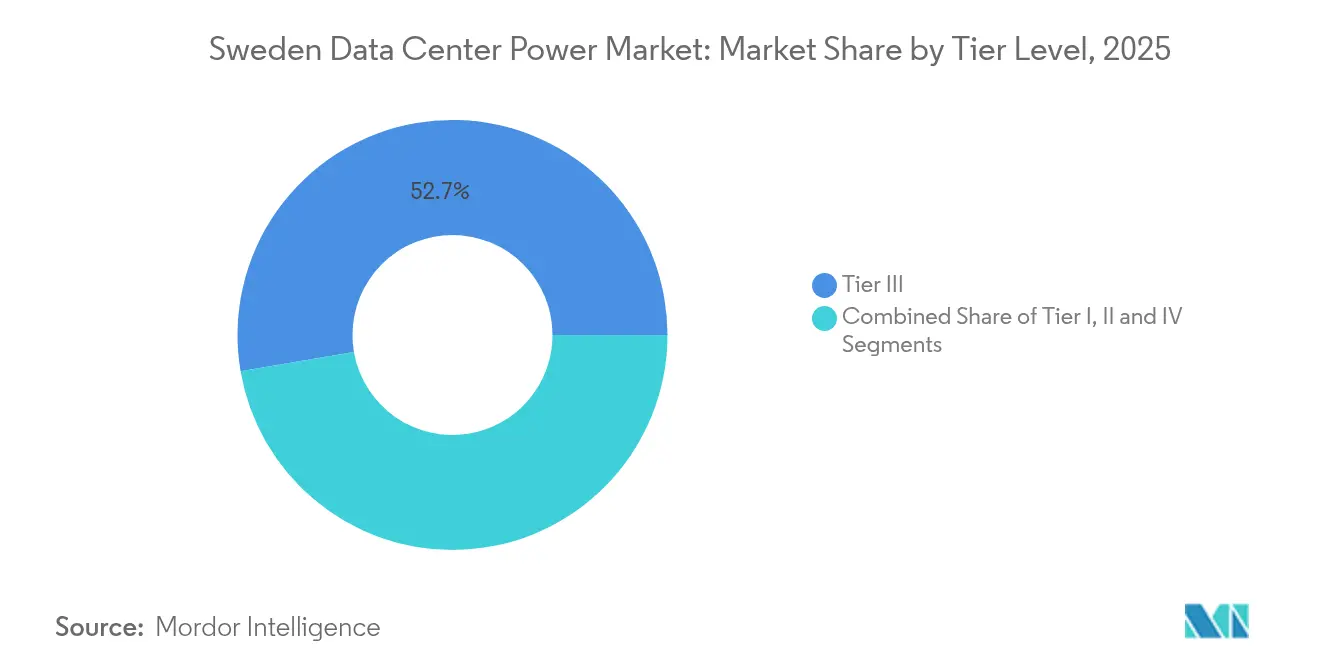

- By tier level, Tier III sites controlled 52.70% of the Sweden data center power market size in 2025, whereas Tier IV facilities are set to register the highest 6.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sweden Data Center Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated hyperscale-AI build-outs | +0.80% | National, with concentration in Stockholm, Luleå, and emerging sites in northern regions | Medium term (2-4 years) |

| Government's 97% electricity-tax rebate | +1.30% | National | Long term (≥ 4 years) |

| Rising grid-interactive UPS deployments | +0.90% | National, with early adoption in Stockholm and Gothenburg | Medium term (2-4 years) |

| Demand-charge avoidance via BESS microgrids | +1.10% | National, with concentration in high-density urban areas | Medium term (2-4 years) |

| On-site H₂ backup pilots by hyperscalers | +0.60% | Limited to hyperscale facilities in northern regions | Long term (≥ 4 years) |

| EU CSRD-driven Scope-2 disclosure pressure | +0.50% | National, with greater impact on international operators | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Accelerated Hyperscale-AI Build-outs

AI compute growth is lifting power densities toward 100 kW per rack, forcing a redesign of distribution topologies. CoreWeave’s USD 2.2 billion campus plan validates Sweden’s suitability for GPU clusters that will quadruple electricity use relative to conventional workloads. Medium-voltage switchboards and 24 kV static UPS protect these megawatt blocks while preserving 98% efficiency. The International Energy Agency notes that AI data centers could contribute more than 20% of future demand growth in advanced economies, heightening the urgency for capacity upgrades.[1]International Energy Agency, “AI Is Set to Drive Surging Electricity Demand from Data Centres,” iea.org Hyperscalers are demanding campus capacities above 200 MW, spurring joint planning with utilities for dedicated substations. Innovation in power protection, notably 24 kV static UPS, is emerging to secure these enormous loads while sustaining 98% efficiency.

Government 97% Electricity-Tax Rebate

Introduced in 2016 and extended in 2023, Sweden’s electricity tax reduction slashes operating costs for any data center drawing at least 100 kW. The measure keeps delivered energy prices among Europe’s lowest, allowing operators to reinvest savings in high-efficiency transformers and liquid-cooling power shelves. Strong policy continuity underpins long-horizon capex commitments by global cloud platforms. Financial headroom created by the rebate accelerates early adoption of grid-interactive UPS that earn ancillary-service revenues, improving total project returns. The incentive also amplifies Sweden’s green appeal because the rebate applies uniformly to hydropower, wind, and solar electricity procured on long-term PPA contracts.

Demand-charge Avoidance via BESS Microgrids

Peak-demand fees can exceed 90% of monthly bills, prompting campuses to use battery energy storage during tariff spikes. Swedish projects such as the Simris microgrid validate BESS in both grid-connected and islanded operation, proving resilience for critical IT loads rwth-aachen.de. ABB’s data-center-specific microgrid controller shapes load to shave peaks and arbitrage time-of-use pricing. Paired with on-site solar arrays, BESS cuts net emissions while shortening payback to close to five years on sites with high capacity charges. Uniper’s hydropower-plus-battery scheme further illustrates how storage upgrades grid stability, indirectly supporting colocation uptime during winter demand surges.[2]Saft, “Batteries and Battery Systems make a Difference in Every Market Sector they Serve,” saft.com

On-site H₂ Backup Pilots by Hyperscalers

Caterpillar and Microsoft achieved 99.999% uptime with a 1.5 MW hydrogen fuel cell string, proving parity with diesel gensets. Swedish hyperscale campuses in the north are piloting similar stacks that produce only water vapor at the point of use. Hitachi Energy’s HyFlex generator, sized for multi-megawatt blocks, is being optimized for cold-start performance in Nordic climates.[3]Hitachi Energy, “Backup Power for Data Centers of the Future,” hitachienergy.com Obstacles remain around green hydrogen supply and storage permits, but corporate decarbonization targets and CSRD reporting pressure sustain R&D budgets. Over time, hydrogen backup could eliminate roughly 2,000 tCO₂e annually per 10 MW of replacement capacity.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long grid-connection lead times in Stockholm | -0.50% | Stockholm region | Medium term (2-4 years) |

| Scarcity of qualified high-voltage technicians | -0.30% | National, with acute impact in rapidly developing areas | Short term (≤ 2 years) |

| Uncertain SMR nuclear licensing pathway | -0.90% | National | Long term (≥ 4 years) |

| Local community opposition to new corridors | -0.50% | Primarily in densely populated regions | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Long Grid-connection Lead Times in Stockholm

Svenska kraftnät’s 10-year plan highlights 1,500 km of new lines and 30 substations still required to relieve Stockholm bottlenecks. Queue times exceeding five years force operators either to pre-book capacity long before the design freeze or migrate builds northward. Researchers describe “air bookings” by cloud giants that lock capacity yet delay build decisions, squeezing local developers. Short-term workarounds involve behind-the-meter generation and demand-response schemes, but those add cost and complexity. The persistence of the bottleneck curbs near-term uptake of new megawatt-scale sites in the capital region, shaving growth from the Sweden data center power market.

Uncertain SMR Nuclear Licensing Pathway

Small modular reactors attract interest as baseload complements to intermittent wind, but Sweden is still formalizing site criteria and finance models. Samsung C&T’s partnership with Kärnfull Next aims for first SMR commissioning by 2032; licensing milestones remain undefined. Data center investors hesitate to book speculative SMR power, limiting private funding streams that could accelerate deployment. Policy ambiguity, therefore, postpones a potential low-carbon capacity boost that would otherwise unlock new hyperscale corridors.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: PDUs Surge with AI Power Demands

The segment generated the largest revenue in 2025 when UPS Systems secured 31.85% of the Sweden data center power market share, underscoring how power protection remains foundational. PDUs, however, will grow fastest at 5.69% CAGR through 2031 as operators tailor branch-circuit metering and outlet-level switching for racks drawing 80 kW. The Sweden data center power market size for PDUs is projected to surpass USD 52.41 million by 2031, reflecting hyperscale customization budgets tied directly to GPU cluster deployment. ABB’s HiPerGuard MV UPS demonstrates how copper savings and high efficiency temper rising load currents, while Vertiv’s modular PDUs embed hot-swappable breakers to sustain uptime at extreme densities.

Generators are evolving from diesel toward dual-fuel and hydrogen-ready variants to reduce on-site CO₂; Cummins’ Centum Force container can operate on hydrotreated vegetable oil and integrate with BESS for low-noise testing cycles. Energy-storage systems, including Saft’s MW-scale lithium-ion arrays, are replacing spinning reserve and offsetting demand charges. Service revenues grow as complexity rises, and OEMs bundle predictive analytics with maintenance contracts to guarantee availability SLAs. Collectively, these component shifts reinforce Sweden’s reputation for resilient yet sustainable power infrastructure, bolstering competitiveness within the Sweden data center power market.

By Data Center Type: Colocation Retains Lead Through Green Credentials

Colocation captured 46.90% revenue in 2025 and is expanding at 5.19% CAGR as enterprises favor shared infrastructure that meets CSRD transparency rules without a capital burden. Providers such as Conapto embed waste-heat reuse and 100% renewable PPAs, attracting international clients needing low-carbon footprints. EcoDataCenter’s sale of smaller sites to fund hyperscale capacity shows providers scaling vertically to house AI superclusters.Hyperscalers and cloud platforms continue to build green-field campuses, yet many still lease phase-one halls from colocation landlords for speed-to-market. Enterprise and edge footprints remain relevant for latency-critical workflows, but will form a shrinking proportion of power spend. Sweden’s national green grid ensures all facility types can advertise near-zero Scope-2, but colocation operators monetize this fact most effectively by pooling load profiles and procuring hydro certificates wholesale. The resulting economies of scale sustain their leadership within the Sweden data center power market.

By Data Center Size: Massive Facilities Expand for AI Workloads

Large halls held 28.55% of spending in 2025 as incumbents extended modular wings, yet massive complexes above 150 MW will grow 4.58% annually through 2031. EcoDataCenter’s planned Borlänge mega-campus alone accounts for 240 MW and signals a structural pivot to fewer but larger power feeds. Medium and small facilities remain essential for edge caches and sovereign control, but their growth lags at single-digit rates. CoreWeave’s multi-site plan demonstrates how GPU cloud firms treat Sweden as an Arctic capital corridor, clustering compute near abundant hydro reservoirs. Larger footprints drive innovation in bus bar trunking, fault-tolerant MV switchgear, and robotic battery swap systems. In turn, suppliers refine designs around mega-campus norms, reinforcing the shift in the Sweden data center power market toward high-power densities.

By Tier Level: Tier IV Facilities Rise with Reliability Demands

Tier III still dominates at 52.70% revenue owing to cost-balanced redundancy, yet Tier IV is posting a 6.12% CAGR as outage tolerance shrinks for AI pipelines that train round-the-clock. Operators deploy 2N+1 power trains, discreet dual utility feeds, and mirrored energy-storage banks to hit the 99.995% uptime cut-off. Vertiv’s collaboration with Conapto illustrates how next-generation switchboards and busways deliver a concurrently maintainable architecture without a footprint penalty. Tier I and II footprints persist for backup offices and DR nodes, yet their share is eroding. Over time, Sweden’s stable grid and renewable surplus may permit relaxed redundancy, but for now, AI workloads push designers upward in tier hierarchy, channeling capex into high-efficiency duplication across the Sweden data center power market.

Geography Analysis

Northern clusters benefit from hydro abundance and cooler ambient temperatures that drive average PUE down to 1.37, compared with global norms above 1.55. Boden Type DC One recorded a 1.0148 PUE, showcasing world-class efficiency and reinforcing the Sweden data center power market as a benchmark for sustainability.

Stockholm still commands premium colocation pricing, yet grid-connection delays redirect new megawatt projects to Norrbotten and Västernorrland. Government incentives favor waste-heat reuse in district heating loops, and EcoDataCenter’s Falun site already channels heat to pellet production, illustrating circular-economy synergies. Northbound migration dovetails with national agendas to balance load across transmission zones, and Uniper’s hybrid hydro-battery plants stabilize frequency for these rural campuses.

Competitive Landscape

The equipment tier shows moderate concentration with players like ABB, Schneider Electric, and Vertiv. Their portfolios span MV static UPS, modular PDUs, and digital-twin monitoring, creating high switching costs for operators. Local champions such as Hitachi Energy leverage domestic grid expertise to win high-voltage packages, while Saab drives microgrid control logic. Competition intensifies on sustainability features; ABB’s HiPerGuard MV UPS achieves 98% efficiency and 90% copper saving, setting a high bar.

Operationally, EcoDataCenter, atNorth, and Conapto lead colocation footprints, while Meta and Microsoft anchor hyperscale segments with self-owned campuses. Operators differentiate on renewable sourcing, heat-extraction integration, and CSRD-aligned carbon reporting dashboards. Service providers bundle power equipment with energy-as-a-service contracts, aligning fees to avoided emissions and peak-charge reductions.

White-space innovation focuses on hydrogen backup, SMR co-location, and AI-driven predictive repairs. Kärnfull Next’s SMR program with Samsung C&T may disrupt conventional power sourcing by 2032. In the meantime, integrated BESS-plus-PPA offers immediate resilience gains. The ongoing convergence of power equipment, software analytics, and sustainability services continues to reshape the Sweden data center power market competitive chessboard.

Sweden Data Center Power Industry Leaders

ABB Ltd

Schneider Electric SE

Vertiv Group Corp.

Eaton Corp. plc

Cummins Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Cummins launched the Centum Force containerized generator, able to run on hydrotreated vegetable oil for greener backup power.

- April 2025: CoreWeave committed USD 2.2 billion to Swedish, Norwegian, and Spanish AI data centers, all powered by renewables.

- March 2025: EcoDataCenter announced a 240 MW mega campus conversion of a former Borlänge paper mill, adding 200 long-term jobs.

- December 2024: atNorth secured a 30-hectare plot in Sollefteå for its first Swedish mega facility with up to 100 MW

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Sweden's data center power market as all on-site electrical delivery and back-up systems, chiefly uninterruptible power supplies, power-distribution units, switchgear, generators, remote power panels, and related monitoring software, installed at colocation, cloud and enterprise server halls across the country. The valuation covers new equipment sales plus associated design-build services in USD at factory gate prices.

Scope exclusion: Renewable PPAs, district-heating reuse hardware, and cooling infrastructure are outside the present power scope.

Segmentation Overview

- By Component

- Electrical Solutions

- UPS Systems

- Generators

- Diesel Generators

- Gas Generators

- Hydrogen Fuel-cell Generators

- Power Distribution Units

- Switchgear

- Transfer Switches

- Remote Power Panels

- Energy-storage Systems

- Service

- Installation and Commissioning

- Maintenance and Support

- Training and Consulting

- Electrical Solutions

- By Data Center Type

- Hyperscaler/Cloud Service Providers

- Colocation Providers

- Enterprise and Edge Data Center

- By Data Center Size

- Small Size Data Centers

- Medium Size Data Centers

- Large Size Data Centers

- Massive Size Data Centers

- Mega Size Data Centers

- By Tier Level

- Tier I and II

- Tier III

- Tier IV

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts next interviewed Nordic electrical-contracting firms, facility engineers at hyperscale operators in Stockholm, and regional government officers who approve grid connections. Conversations clarified average rack densities, current lead-time bottlenecks, and likely spending cadence, which sharpened assumptions drawn from secondary data.

Desk Research

We began by screening Swedish-language releases from Statistics Sweden, Swedish Energy Agency datasets on electricity generation, and Eurostat trade codes that capture imports of UPSs and switchgear. Trade-association briefs from the Energy Markets Inspectorate, patents pulled through Questel, and listed-company 10-Ks provided baseline shipment volumes and typical margins. News flows within Dow Jones Factiva, as well as project announcements in Tenders Info, helped map build pipelines. The sources cited are illustrative; many others were explored to cross-check figures and usage factors.

Market-Sizing & Forecasting

A top-down build started with Sweden's installed IT power capacity (MW) and its five-year expansion pipeline. We overlaid average electrical-infrastructure cost per megawatt, segmented by facility tier and redundancy level, then validated the totals with selective bottom-up checks of supplier revenue disclosures. Key inputs include annual MWh delivered to data centers, typical UPS refresh cycles, grid-connection queue length, lithium-ion adoption rates, and prevailing SEK-USD exchange movements. A multivariate regression anchored forecast growth to hyperscale CAPEX trends, renewable-energy tax rebates, and Stockholm grid build-outs, while ARIMA smoothing handled shorter-term swings. Gaps in vendor roll-ups were bridged using median ASPs from invoices shared confidentially by installation partners.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance flags, peer assessment by a senior analyst, and a final sign-off before publication. We refresh the model annually, with interim revisions when utility-rate changes or mega-campus announcements move the market.

Why Mordor's Sweden Data Center Power Baseline Rings True

Published estimates often diverge because firms mix investment spending with replacement sales or apply Europe-wide ASPs to Swedish volumes. Mordor tests scope and variables repeatedly, which helps us stay aligned to what buyers actually purchase in Sweden.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 209.65 M | ���ϲ����� | - |

| USD 201.80 M | Research Publisher A | excludes remote power panels and uses 2022 shipment ASPs |

| USD 201.80 M | Industry Consultancy B | rolls Nordic averages into Sweden and omits SEK-USD currency adjustments |

The comparison shows that small definition shifts and currency timing explain most gaps. By grounding every assumption in local capacity data and verified ASPs, Mordor delivers a transparent, repeatable baseline trusted by procurement and strategy teams.

Key Questions Answered in the Report

What is the projected value of the Sweden data center power market in 2031?

The market is forecast to reach USD 262.67 million in 2031, expanding from USD 209.65 million in 2025 at a 3.83% CAGR.

Why are PDUs growing faster than other power components?

AI workloads need outlet-level metering and custom power mapping, pushing PDUs to a 5.69% CAGR, the fastest among all components.

How does Sweden’s electricity-tax rebate affect data center costs?

The 97% tax reduction lowers delivered energy prices, freeing capital to invest in efficiency upgrades and making Sweden one of Europe’s most cost-effective data center locations.

What role will hydrogen fuel cells play in Swedish data centers?

Hydrogen stacks demonstrated 99.999% uptime and zero emissions, and pilots in northern campuses indicate they could replace diesel gensets for reliable, carbon-free backup.

How is the EU CSRD influencing Swedish operators?

The directive requires detailed Scope-2 reporting, so operators leverage Sweden’s low-carbon grid and renewable PPAs to keep disclosures minimal and gain a competitive edge.

Page last updated on: