Sterilization Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.74 Billion |

| Market Size (2031) | USD 7.42 Billion |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Sterilization Services Market Analysis by ���ϲ�����

The Sterilization Services Market size is expected to grow from USD 5.45 billion in 2025 to USD 5.74 billion in 2026 and is forecast to reach USD 7.42 billion by 2031 at 5.29% CAGR over 2026-2031.

Consistent adoption of stringent infection-control protocols, regulatory convergence toward ISO 13485, and rapid uptake of outsourced processing underpin steady expansion. Accelerating transition away from high-emission ethylene oxide (EtO) toward X-ray, electron-beam, and hydrogen-peroxide technologies adds both capital pressure and innovation headroom. Demand also rises as single-use bioprocess components and minimally invasive devices flood global supply chains. Market leaders leverage acquisitions to broaden geographic reach and validation expertise, while emerging specialists focus on niche materials and digitalized monitoring. Collectively, these forces sustain pricing power even as competitive intensity grows.

Key Report Takeaways

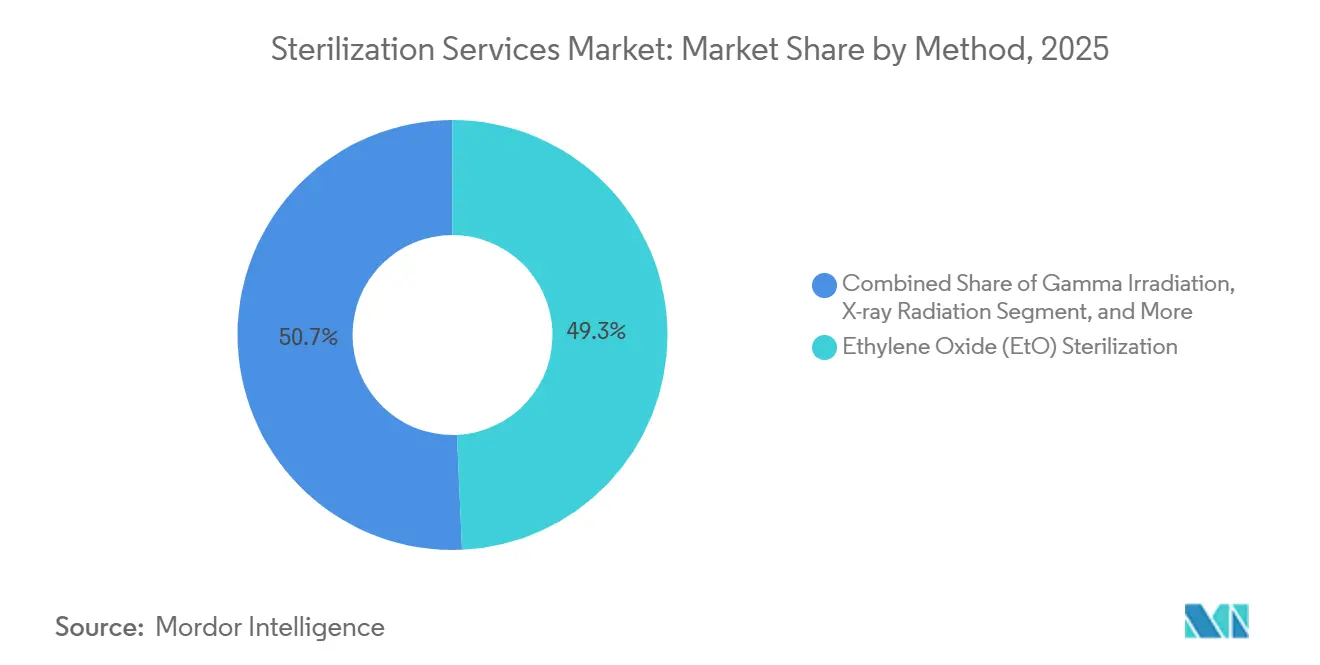

- By method, ethylene oxide retained a 49.30% share of the sterilization services market in 2025; X-ray is forecast to expand at a 12.15% CAGR through 2031.

- By mode of delivery, off-site centers commanded a 67.05% share of the sterilization services market in 2025, while on-site services are set to grow at a 10.98% CAGR through 2031.

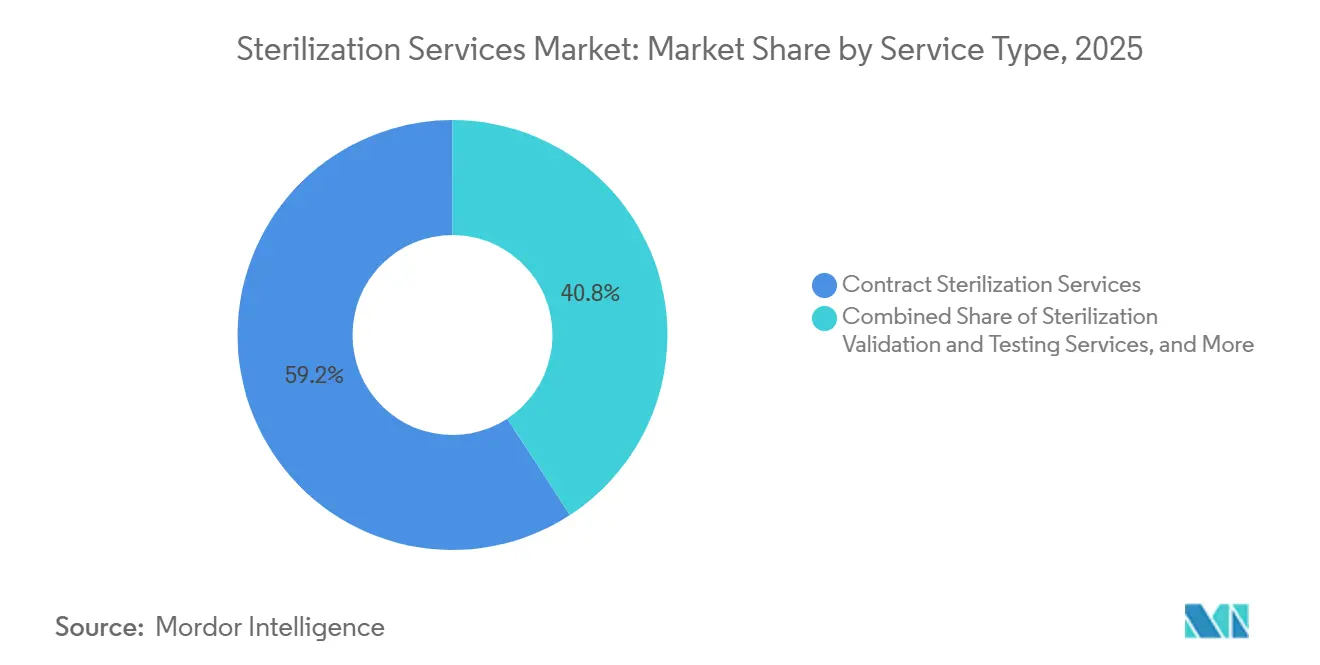

- By service type, contract sterilization accounted for 59.20% of the sterilization services market in 2025; validation and testing are projected to grow at a 9.37% CAGR through 2031.

- By end user, medical device manufacturers held 45.10% of the sterilization services market share in 2025, whereas pharmaceutical and biotech manufacturers are projected to have the highest CAGR of 10.55% to 2031.

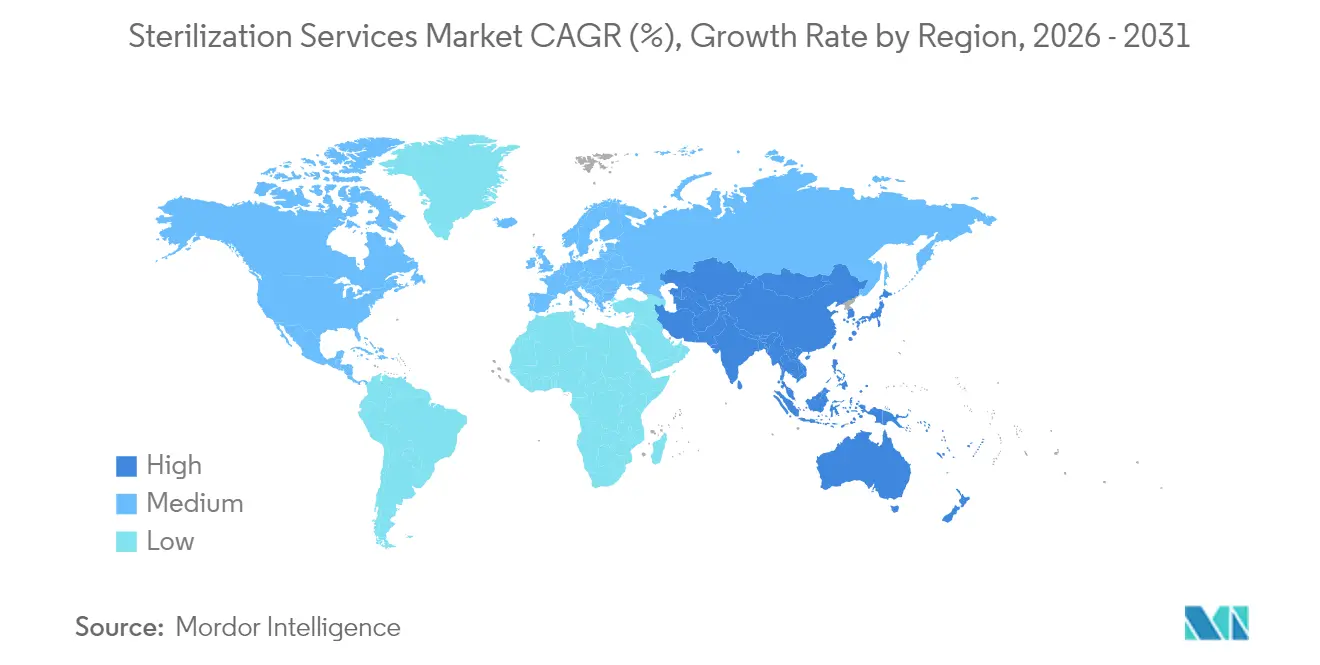

- By geography, North America led with a 39.10% revenue share in 2025; Asia-Pacific is advancing at a 10.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sterilization Services Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Escalating prevalence of hospital-acquired infections | +0.8% | Global, with acute pressure in North America & Europe | Medium term (2–4 years) |

| Outsourcing surge among device and pharma manufacturers | +1.2% | Global, concentrated in North America, Europe, Asia-Pacific | Long term (≥4 years) |

| Global alignment to iso 13485 and FDA QMSR final rule | +0.6% | North America & Europe, spillover to Asia-Pacific | Short term (≤2 years) |

| Rapid uptake of single-use & minimally-invasive devices | +0.9% | Global, led by North America & Asia-Pacific | Medium term (2–4 years) |

| Decentralised, AI-enabled cycle-tracking platforms | +0.4% | North America & Europe, early adoption in select APAC hubs | Medium term (2–4 years) |

| X-ray capacity build-outs mitigating cobalt-60 supply risk | +0.7% | Global, with priority investments in North America & Europe | Long term (≥4 years) |

| Source: ���ϲ����� | |||

Escalating Prevalence of Hospital-Acquired Infections

Hospital-acquired infections continue to impose substantial clinical and economic burdens, with the Centers for Disease Control and Prevention estimating that 1 in 31 hospital patients in the United States contracts at least one HAI on any given day, translating to approximately 687,000 infections and 72,000 deaths annually The 2024 indicates significant reductions in most (HAIs) compared to 2023 in US hospitals, with 2%–11% decreases for infections like CLABSI, CAUTI, and MRSA. However, surgical site infections (SSIs) following abdominal hysterectomy rose by 8%.[1]Centers for Disease Control and Prevention, “Cleaning & Disinfection for Infection Prevention,” cdc.gov

Healthcare facilities worldwide are intensifying decontamination protocols to curb infections that prolong hospital stays and inflate costs. Guidance from the Centers for Disease Control and Prevention positions thorough environmental cleaning as a frontline defense, pushing providers to adopt validated, high-capacity sterilization services. Low-resource regions, which report infection rates several times higher than those in advanced economies, increasingly outsource processing to achieve reliable sterility assurance without heavy capital investment. Insurance payers reinforce the shift by linking reimbursement to infection metrics. Contract processors benefit as device manufacturers bundle sterile packaging with production runs to streamline regulatory submissions. Collectively, these behaviors lift annual procedure volumes flowing into the sterilization services market.

Outsourcing Surge Among Device and Pharma Manufacturers

Manufacturers are divesting fixed sterilization assets to free capital for research pipelines and speed product launches. Johnson & Johnson’s Ethicon unit, for example, shuttered its San Lorenzo EtO plant in October 2024, transferring throughput to an external network and cutting USD 18 million in annual costs. Contract providers offer multi-modal choices, EtO, gamma, E-beam, and X-ray, allowing firms to balance material compatibility, dose uniformity, and cycle time without multimillion-dollar infrastructure commitments. The strategy particularly benefits startups and mid-tier firms that cannot justify USD 30–50 million to build and validate an in-house facility, supporting the expansion of the sterilization services market.

Global Alignment to ISO 13485 and FDA QMSR Final Rule

Regulators are consolidating rules to remove jurisdictional ambiguities. The U.S. Food and Drug Administration’s Quality Management System Regulation final rule, coming into force in February 2026, aligns domestic requirements with ISO 13485:2016.[2]U.S. Food and Drug Administration, “Quality Management System Regulation Final Rule,” fda.gov Europe’s revised GMP Annex 1 embeds robust contamination-control strategies for sterile medicines. As guidance coalesces, manufacturers can operate a single global quality system, yet must demonstrate tighter dose uniformity and cycle reproducibility. Service providers deploy parametric release and real-time sensor suites to document performance, deepening switching costs for customers and raising the technical bar for new entrants.

Rapid Uptake of Single-Use & Minimally-Invasive Devices

Ambu, Boston Scientific, and Olympus collectively supplied more than a million single-use devices. Single-use formats eliminate reprocessing risks but shift full sterilization responsibility upstream to manufacturers. Complex geometries and heat-sensitive polymers found in laparoscopic trocars and catheter-based tools limit the applicability of steam, favoring low-temperature EtO, hydrogen-peroxide plasma, or vapor-phase hydrogen peroxide.

Restraint Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent EtO emission & radio-isotope security regulations | -0.9% | North America & Europe, with regulatory spillover to Asia-Pacific | Short term (≤2 years) |

| High capex for multi-modal compliant facilities | -0.6% | Global, acute in emerging markets with limited access to project finance | Long term (≥4 years) |

| Shortage of certified sterility-assurance professionals | -0.5% | North America & Europe, emerging in Asia-Pacific | Medium term (2–4 years) |

| Polymer-compatibility failures with next-gen bio-composites | -0.3% | Global, concentrated in advanced medical device segments | Medium term (2–4 years) |

| Source: ���ϲ����� | |||

Stringent EtO Emission & Radio-Isotope Security Regulations

The U.S. Environmental Protection Agency’s April 2024 rule slashed acceptable EtO emissions to 0.2 ppm over eight hours and mandated 99.9% capture efficiency.[3]U.S. Environmental Protection Agency, “National Emission Standards for EtO,” epa.gov Retrofitting a facility costs USD 5–15 million; several small United States plants closed rather than invest, curbing roughly 12% of national EtO capacity. Operators are redirecting capital toward X-ray and E-beam assets, yet the pace of replacement lags near-term demand, tightening supply in the sterilization services market.

High Capex for Multi-Modal Compliant Facilities

Building a site that houses EtO, gamma, E-beam, and X-ray systems demands more than USD 50 million and carries payback periods exceeding eight years. Financing hurdles are the steepest in Southeast Asia and Latin America, where banks perceive radiation facilities as higher risk. Consequently, most new builds cluster in North America and Western Europe, reinforcing regional capacity concentration.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Method: X-Ray Gains as EtO Faces Emission Caps

Ethylene oxide retained a dominant 49.30% share of the sterilization services market in 2025, reflecting its unmatched compatibility with heat-sensitive, lumen-rich devices. Yet, cumulative regulatory pressure and public health concerns accelerate diversification. X-ray cycles, already validated for a widening catalog, are forecast to record a 12.15% CAGR through 2031, the fastest within the segment. Dose-uniformity studies show its efficacy is equivalent to gamma irradiation while avoiding cobalt-60 logistics. Gamma retains entrenched infrastructure and reliable deep-penetration performance, although isotope supply constraints spur contingency planning. Electron-beam offers rapid throughput but faces limitations with dense pallets. Hydrogen-peroxide plasma and vapor-phase systems capture temperature-sensitive items like electronic endoscopes, building a loyal customer base in high-value surgical kits. As material science evolves, method selection increasingly hinges on polymer behavior under oxidative stress, pushing processors to offer multi-modal capabilities.

The sterilization services market continues reallocating capex toward radiation vaults equipped for dual-energy switching, enabling seamless migration from isotope to machine sources. Providers collaborate with device engineers to embed dose mapping at the design stage, reducing post-production inconsistencies. Regulatory acceptance of vaporized hydrogen peroxide as an Established Category A method simplifies 510(k) submissions, further fragmenting modal shares. Consequently, method diversification reshapes revenue streams and safeguards supply continuity.

By Mode of Delivery: Economic Imperatives Reshape Service Models

Off-site service centers captured 67.05% of the sterilization services market in 2025, leveraging scale to amortize capital outlays and environmental controls. Centralized hubs process mixed loads 24/7, offering validated truck routes and digital chain-of-custody reporting. Hospitals, pressured by staffing shortages and surgical-instrument backlogs, increasingly divert trays to regional off-site reprocessing centers, citing improved compliance and predictable turnaround times. Conversely, on-site service models, projected to advance at a 10.98% CAGR, appeal to high-volume pharma campuses where real-time release trims inventory days. Hybrid models emerge, blending mobile EtO pods for overflow with routine off-site irradiation, permitting clients to fine-tune cost versus cycle time.

Evolving geopolitical risks underscore redundancy. Multinational manufacturers allocate dual validation across geographically separated providers to ensure pandemic or natural-disaster resilience. In response, contract processors develop mirrored digital documentation systems that enable the instant transfer of cycle data between facilities and clients’ quality portals.

By Service Type: Validation Services Surge on Audit Intensity

Contract terminal processing delivered 59.20% of 2025 revenue, but validation and testing lines, necessitated by new polymers, 3-D-printed geometries, and detailed bioburden mapping, are expanding by 9.37% CAGR. Regulations require dose audits at installation, operational, and performance qualification stages, each documented via electronic batch records. Laboratories offering accelerated aging, cytotoxicity, and residual-gas analytics attract bundled contracts. Advisory teams help clients transition from cobalt-60 to X-ray, modelling dose-rate effects on tensile strength. Process optimization frameworks integrating in-line dosimetry and AI trend analysis reduce rework and bolster traceability, cementing client loyalty.

By End-User: Pharma and Biotech Outpace Device Makers

Medical-device firms generated 45.10% of 2025 revenue, relying on validated protocols to secure global market authorizations. Device miniaturization and intricate assemblies intensify sterility-assurance specifications, locking in steady order flow. The pharmaceutical & biotech cohort, registering a projected 10.55% CAGR, drives specialized demand for syringe tubs, nested vials, and single-use bioreactor components. Radiation-tolerant packaging solutions become pivotal, and processors collaborate closely with packaging scientists to prevent delamination or barrier loss. Hospitals and clinics, sensitive to infection penalties, run autoclave cycles for metal instruments but increasingly outsource complex, flexible endoscopes. Food producers form a nascent but strategic niche, favoring low-dose e-beam to extend shelf life without preservatives.

Geography Analysis

North America led the sterilization services market with a 39.10% share in 2025, underpinned by robust reimbursement models, dense medical-device clusters, and proactive environmental oversight. The Environmental Protection Agency’s 2025 final rule demanding 99.99% EtO capture forces providers to retrofit abatement technology and accelerates migration toward machine-source radiation. Investment in alternative modalities safeguards supply continuity and sustains regional leadership despite higher compliance costs.

Asia-Pacific represents the fastest-growing region, with a 10.82% CAGR through 2031. Expanding device contract-manufacturing organizations in China, India, and Malaysia require proximity sterilization capacity that meets United States and EU audit requirements. STERIS’s 2025 commissioning of an X-ray facility in Suzhou exemplifies market-entry strategies oriented toward multi-energy resilience. Governments encourage domestic irradiation to minimize export bottlenecks, and local regulators are aligning with ISO 11137 and ISO 13408, streamlining cross-border trade.

Europe maintains a roughly 30.20% share in 2025, characterized by the Medical Device Regulation’s stringent device and packaging validation clauses. Providers diversify into supercritical carbon dioxide and vaporized hydrogen peroxide cycles to meet sustainability objectives. SGS’s expanded MDR sterilization certification scope underscores its competitive advantage by providing broader process coverage. Sustainability metrics embedded in corporate tenders now influence vendor selection, prompting investment in energy-efficient accelerators and heat-recovery ventilation.

Competitive Landscape

The sterilization services market shows moderate concentration: the top five players account for significant revenue, while regional specialists thrive in specialized niches. STERIS plc and Sotera Health dominate via expansive irradiation networks, EtO chambers, and microbiological laboratories. Acquisition pipelines remain active; incumbents absorb smaller labs to secure talent and bolster validation throughput.

Differentiation pivots on multimodal capability, regulatory fluency, and digital transparency. Providers deploy RFID-enabled load tracking and cloud-based certificate portals to enhance client audits. Emerging entrants emphasize X-ray, e-beam, and plasma as eco-conscious alternatives, pre-empting EtO capacity constraints. BGS Beta-Gamma-Service’s planned United States expansion illustrates trans-Atlantic growth pursuits amid cobalt-60 supply anxiety.

White-space opportunities center on advanced composites, 3-D-printed porous lattices, and drug-device combination products requiring tailored cycles. Players investing in AI-guided dose mapping and real-time gas-residual analytics are well-positioned to capture these premium segments. Strategic alliances with packaging innovators ensure that advances in material science accompany improvements in sterilization performance.

Sterilization Services Industry Leaders

STERIS PLC

Sotera Health (Sterigenics, Nordion, Nelson Labs)

Getinge AB

Solventum Corporation

Johnson & Johnson Services, Inc (Ethicon)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: India’s Department of Atomic Energy extended electron-beam sterilization capacity, processing millions of medical devices and positioning the country among a handful with advanced radiation infrastructure.

- May 2025: STERIS expanded X-ray capability in Suzhou, China, adding regional throughput for device exporters.

- April 2025: SGS secured MDR approval to include dry-heat, vaporized hydrogen-peroxide, and super-critical carbon-dioxide processes in its European portfolio.

- March 2025: STERIS launched Verafit sterilization bags with a viewing window that aligns with EU GMP Annex 1 dryness confirmation requirements.

Global Sterilization Services Market Report Scope

As per the scope of the report, sterilization is a process that destroys or eliminates all forms of microbial life and is carried out in healthcare facilities by physical or chemical methods. Sterilization services are essential for ensuring that medical and surgical instruments do not transmit infectious pathogens to patients.

The sterilization services market is segmented by method, mode of delivery, service type, end user, and geography. By method, the market is segmented into ethylene oxide (EtO) sterilization, gamma sterilization, steam sterilization, electron beam radiation sterilization, and other sterilization. By service type, the market is segmented into contract sterilization services and sterilization validation services, and Process Advisory & Optimisation Services. By end-user, the market is segmented into medical device companies, hospitals and clinics, the pharmaceutical and biotechnology industry, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers market size and forecasts in value (USD) for the above segments.

| Ethylene Oxide (EtO) Sterilization |

| Gamma Irradiation |

| Electron-Beam (E-beam) Radiation |

| X-ray Radiation |

| Steam (Moist-Heat) Sterilization |

| Dry-Heat Sterilization |

| Hydrogen Peroxide & Plasma Sterilization |

| Off-site (Service-Centre) Sterilization |

| On-site (In-house as a Service) Sterilization |

| Contract Sterilization Services |

| Sterilization Validation & Testing Services |

| Process Advisory & Optimisation Services |

| Medical Device Manufacturers |

| Pharmaceutical & Biotech Manufacturers |

| Hospitals & Clinics |

| Food & Beverage Industry |

| Laboratory & Research Organisations |

| Other Industrial Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Method | Ethylene Oxide (EtO) Sterilization | |

| Gamma Irradiation | ||

| Electron-Beam (E-beam) Radiation | ||

| X-ray Radiation | ||

| Steam (Moist-Heat) Sterilization | ||

| Dry-Heat Sterilization | ||

| Hydrogen Peroxide & Plasma Sterilization | ||

| By Mode of Delivery | Off-site (Service-Centre) Sterilization | |

| On-site (In-house as a Service) Sterilization | ||

| By Service Type | Contract Sterilization Services | |

| Sterilization Validation & Testing Services | ||

| Process Advisory & Optimisation Services | ||

| By End-User | Medical Device Manufacturers | |

| Pharmaceutical & Biotech Manufacturers | ||

| Hospitals & Clinics | ||

| Food & Beverage Industry | ||

| Laboratory & Research Organisations | ||

| Other Industrial Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the sterilization services market expected to grow through 2031?

Revenue is projected to advance from USD 5.74 billion in 2026 to USD 7.42 billion by 2031, reflecting a 5.29% CAGR over the period.

Which sterilization method is gaining traction the quickest?

X-ray processing is forecast to record the fastest 12.15% CAGR as manufacturers shift volume away from gamma and EtO modalities.

Why are pharmaceutical companies adopting on-site sterilization?

On-site models eliminate transport risks for high-value biologics, synchronize cycles with fill-finish lines, and are expanding at a 10.98% CAGR.

What is driving demand for validation and testing services?

Stricter ISO 13485 and FDA QMSR documentation demands are lifting validation revenue at a 9.37% CAGR as manufacturers seek third-party evidence.

Which region offers the highest growth opportunity?

Asia-Pacific is progressing at a 10.82% CAGR, propelled by device-manufacturing hubs in China, India, and Southeast Asia that require outsourced capacity.

How are providers addressing EtO emission regulations?

Leading operators are investing in catalytic oxidizers, shifting volume to X-ray or E-beam lines, and constructing multi-modal plants to diversify risk.

Page last updated on: