Market Overview

| Study Period | 2021 - 2031 |

|---|---|

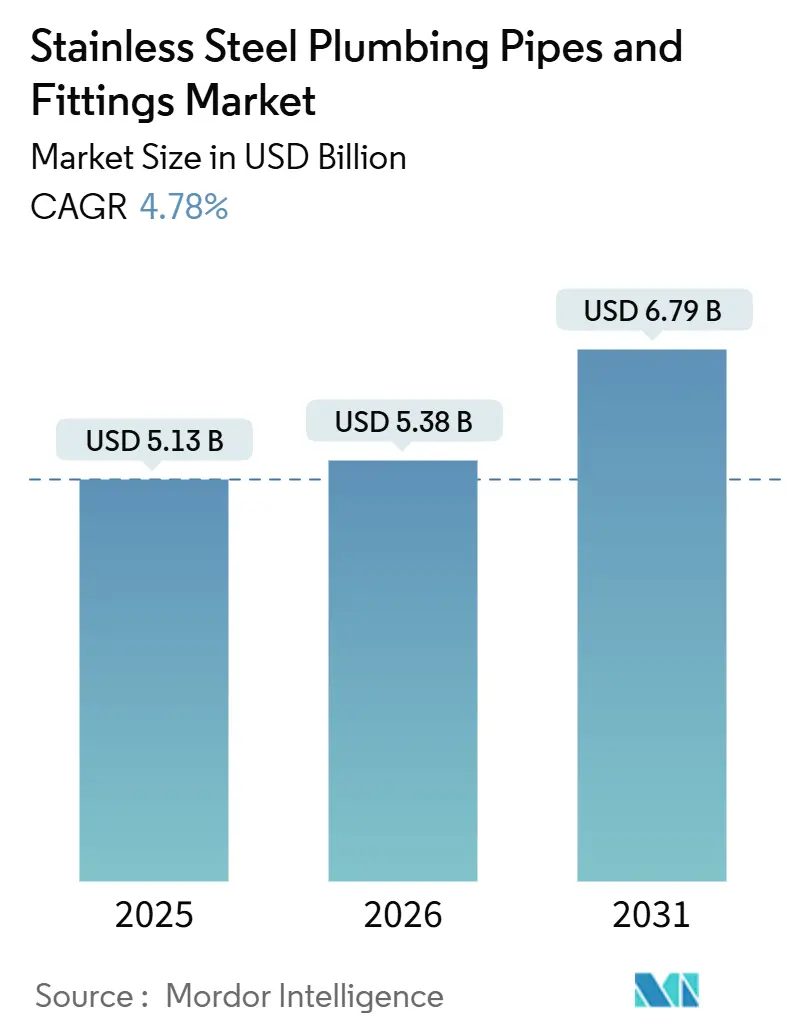

| Market Size (2026) | USD 5.38 Billion |

| Market Size (2031) | USD 6.79 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

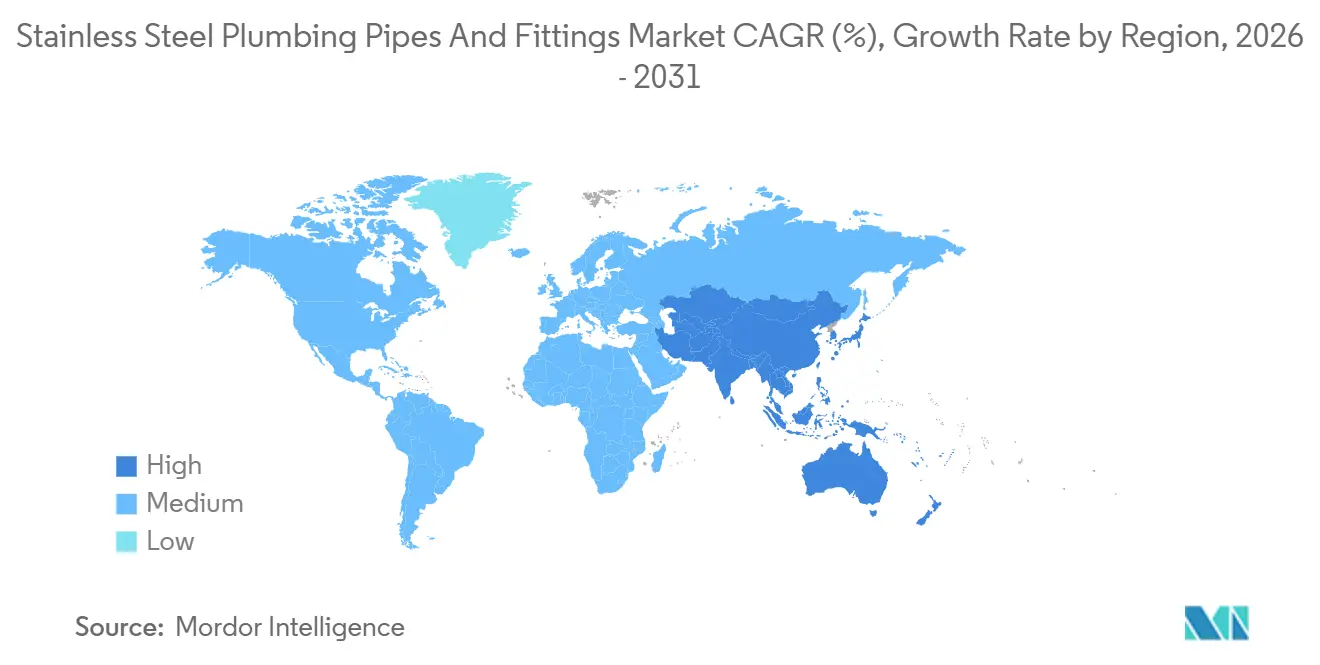

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Stainless Steel Plumbing Pipes And Fittings Market Analysis by ���ϲ�����

The Stainless Steel Plumbing Pipes And Fittings Market size was valued at USD 5.13 billion in 2025 and is estimated to grow from USD 5.38 billion in 2026 to reach USD 6.79 billion by 2031, at a CAGR of 4.78% during the forecast period (2026-2031). Organized manufacturers are enlarging their footprint at a 6.12% annual pace, while e-commerce channels are scaling even faster at 6.42%, signaling that distribution efficiency is becoming as decisive as shipment volume. Stainless steel commands a 32.46% slice of 2025 revenues, yet polyethylene rivals are growing at a 6.24% CAGR as home retrofits chase lower upfront costs. Welded pipes continue to dominate large-diameter potable-water lines with 44.38% 2025 value share, but seamless variants are taking high-pressure niches at 6.18% CAGR. North America and Europe are replacing legacy lines to meet stricter lead-free mandates, whereas Asia-Pacific, already holding 49.52% of 2025 revenues, is set for 5.94% growth powered by urban water-access programs.

Key Report Takeaways

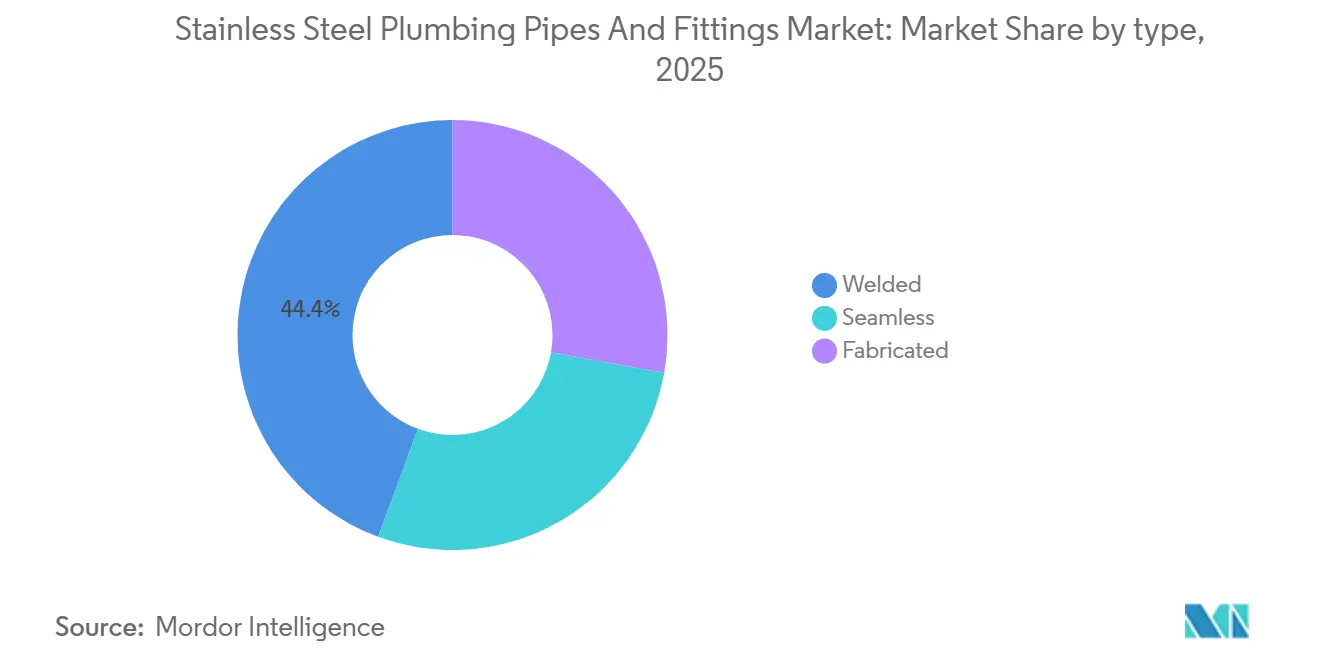

- By type, welded pipes held 44.38% of the stainless steel plumbing pipes market share in 2025, and seamless pipes are forecast to expand at a 6.18% CAGR through 2031.

- By market structure, organized accounted for 61.27% share of the stainless steel plumbing pipes market size in 2025 and is projected to grow at a 6.12% CAGR to 2031.

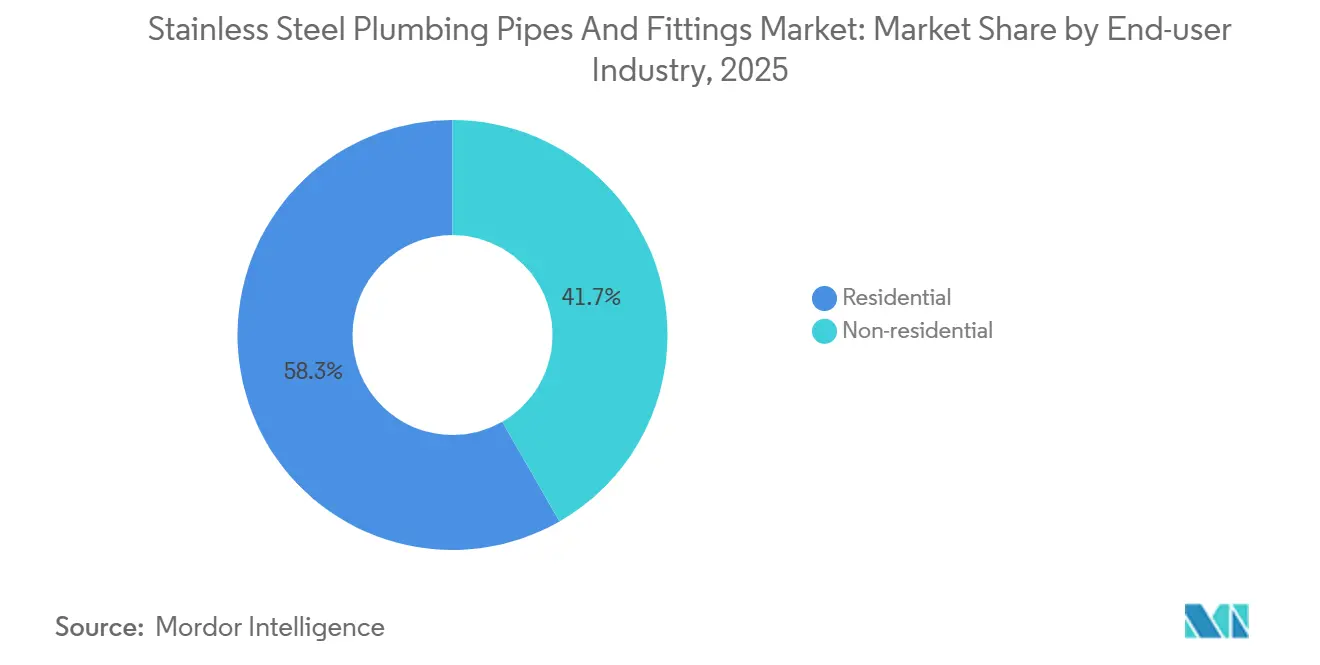

- By end-user industry, residential accounted for 58.34% share of the stainless steel plumbing pipes market size in 2025. The non-residential segment is advancing at a 6.31% CAGR through 2031.

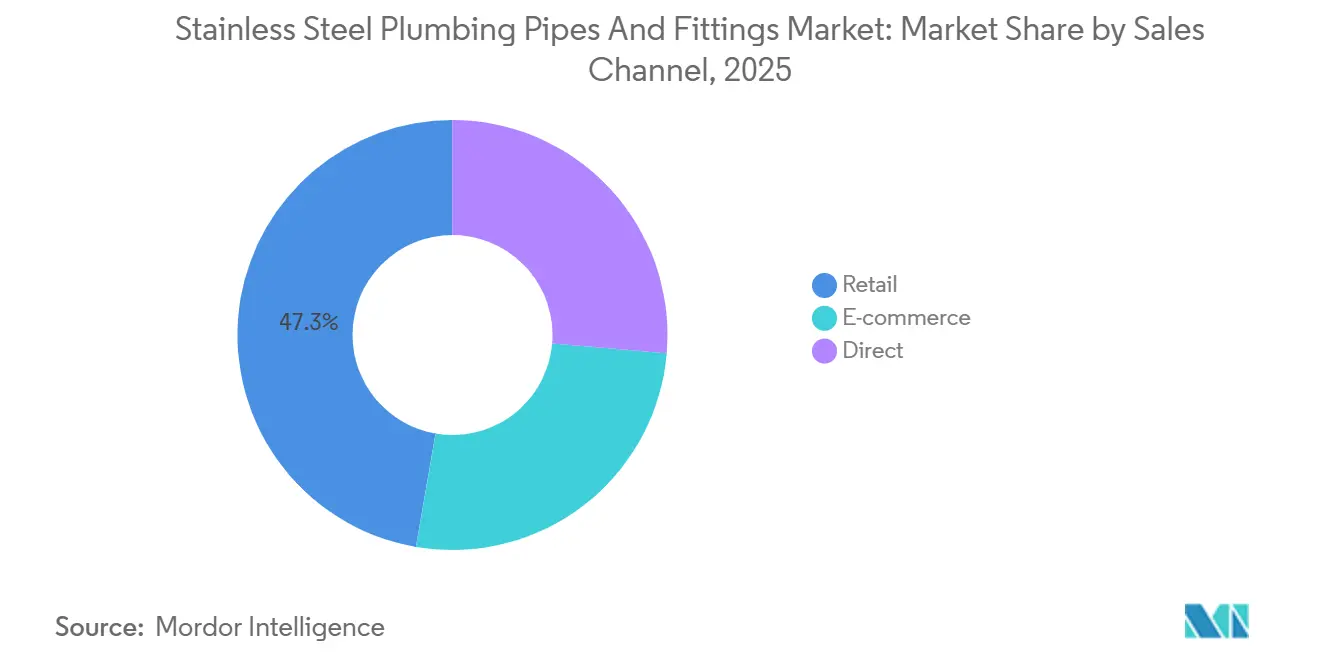

- By sales channel, retail held 47.29% of the stainless steel plumbing pipes market share in 2025, and e-commerce is forecast to expand at a 6.42% CAGR through 2031.

- By geography, Asia-Pacific controlled 49.52% of the 2025 value and is climbing at a 5.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Stainless Steel Plumbing Pipes And Fittings Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing residential and non-residential construction | +1.8% | Global, with concentration in Asia-Pacific (China, India, Indonesia), Middle East (Saudi Arabia, UAE), and North America | Medium term (2-4 years) |

| Stricter potable-water quality regulations | +1.2% | North America, Europe, with spillover to Asia-Pacific urban centers | Long term (≥ 4 years) |

| Emerging-economy infrastructure boom | +1.5% | Asia-Pacific (India, Indonesia, Vietnam, Thailand), Middle East (Saudi Arabia, UAE, Qatar), South America (Brazil) | Long term (≥ 4 years) |

| Advances in welding and forming technologies | +0.7% | Global, with early adoption in North America, Europe, and Japan | Medium term (2-4 years) |

| Green-building certification push | +0.6% | North America, Europe, with emerging traction in Asia-Pacific (Singapore, India) | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Growing Residential and Non-Residential Construction

Data centers, pharmaceutical clean rooms, and food-processing plants are now prioritizing corrosion-free piping, overshadowing the once-dominant housing sector. In 2024, U.S. non-residential construction spending experienced significant growth. In contrast, residential outlays saw a more modest rise. China's water-conservancy spending, after a meteoric rise in the first ten months of 2024, stabilized by July 2025. India's Jal Jeevan Mission, achieving substantial progress in rural tap installations by mid-2025, bolstered the demand for stainless lines in areas with chlorinated groundwater. Germany, riding the EU Renovation Wave, reported notable construction turnover in 2024. Meanwhile, Indonesia's ambitious Nusantara project is set to further expand the market for stainless steel plumbing pipes.

Stricter Potable-Water Quality Regulations

Under the U.S. EPA’s 2024 Lead and Copper Rule Improvements, municipalities must replace all lead service lines[1]U.S. Environmental Protection Agency, “Lead and Copper Rule Improvements, 2024,” epa.gov. The EPA defines "lead-free" as having a weighted-average content inherently met by the 304 and 316L grades of stainless steel. Meanwhile, Europe's revised Drinking Water Directive, set to be enforced by 2027, mandates municipalities to replace corroding iron mains with more corrosion-resistant alternatives[2]European Commission, “Revised Drinking Water Directive,” ec.europa.eu. These regulatory shifts are propelling the stainless steel plumbing pipes market, as public utilities increasingly prioritize materials known for their durability and long service lives. Additionally, BREEAM’s 2024 update incentivizes leak-free distribution systems, further promoting stainless steel installations in buildings seeking green certification.

Emerging-Economy Infrastructure Boom

In the Asia-Pacific and Middle-East, megaprojects are driving growth. Vietnam has allocated significant resources for infrastructure initiatives, with a keen focus on enhancing pipe durability in cities vulnerable to flooding. Meanwhile, Thailand is investing in water management within its Eastern Economic Corridor. In Saudi Arabia, the NEOM project, slated to be partially complete by 2025, is integrating stainless lines into its green-hydrogen complex. Over in Brazil, a sanitation law mandates substantial investment, simultaneously opening doors for municipal tenders specifically for stainless steel providers.

Advances in Welding and Forming Technologies

Orbital TIG systems, adhering to ASTM A814 standards, reduce installation time and guarantee consistent welds. Meanwhile, hybrid laser-arc techniques enable single-pass welds on 10 mm walls, a crucial advancement for seamless options in ultra-pure loops. In 2024, the AWS D10.4M revision tightened ferrite-number limits, steering contractors closer to automation. Such advancements not only address the shortage of certified welders but also enhance lifecycle integrity, thereby expanding the market for stainless steel plumbing pipes.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nickel and chromium price volatility | -1.1% | Global, with acute sensitivity in Asia-Pacific and Europe due to import dependence | Short term (≤ 2 years) |

| Competition from PVC/PEX piping | -0.9% | North America, Europe, with emerging pressure in Asia-Pacific residential segments | Medium term (2-4 years) |

| Shortage of certified stainless welders | -0.6% | North America, Europe, with localized constraints in Middle-East mega-projects | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Nickel and Chromium Price Volatility

In 2024-2025, South African supply issues caused chromium prices to oscillate. Meanwhile, London nickel prices, influenced by surging battery demand, experienced fluctuations. Furthermore, an increase in alloy costs could reduce pipe margins, prompting price-sensitive buyers to consider alternatives like PVC or copper.

Competition from PVC/PEX Piping

Builders typically opt for Schedule 40 PVC over the more expensive 304 stainless steel. This price gap narrows only when building codes require metal or when water chemistry is particularly aggressive. PEX-A, already holding a significant share of U.S. repiping jobs, operates under ASTM F876 and NSF 61 approvals. While stainless steel remains the preferred choice for kitchens, clean rooms, and high-rise risers facing 200 °C service limits, the rising adoption of higher-temperature PEX variants presents a medium-term challenge.

Segment Analysis

By Type: Welded Controls Scale, Seamless Captures High-Pressure Niches

Welded products generated 44.38% of 2025 revenues by excelling in greater than 6-inch mains operating below 150 psi. Seamless tubes, free of longitudinal welds, are growing 6.18% CAGR by serving 3,000 psi steam, hydrogen, and ultrapure loops that reject weld-crevice contamination. ASTM A312 draws a clear hydrostatic test gap between the two, justifying seamless’s price premium. Municipal projects such as India’s Jal Jeevan Mission prioritize welded lines for lateral runs, while pharmaceutical clean rooms default to seamless electropolished tubing to pass FDA 21 CFR Part 211 audits.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Market Structure: Formalization Rewards Organized Players

Organized players captured 61.27% of 2025 revenues and are growing at a 6.12% CAGR through 2031 as BIS and ISO certifications become gatekeepers. Indian majors—Jindal Stainless, APL Apollo, Ratnamani—expand capacity, while distributors such as Ferguson leverage scale to bundle stainless alongside PVC. Unorganized workshops cling to rural builds, yet rising insurance and code scrutiny erode their base.

By End-User Industry: Non-Residential Leads Growth

Non-residential demand is climbing 6.31% CAGR, outstripping residential’s 4.78%, propelled by data-center cooling loops and GMP-compliant pharmaceutical plumbing. Food plants adopting 3-A sanitary standards also champion 316L tubing. Residential accounted for a 58.34% share of the stainless steel plumbing pipes market size in 2025. High-rise apartments still use stainless risers for fire and pressure codes, yet single-family homes lean toward PEX unless water chemistry corrodes polymers.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Sales Channel: E-Commerce Outpaces Legacy Retail

Retail still holds 47.29% of 2025 revenues, but e-commerce is expanding 6.42% CAGR as procurement managers value embedded datasheets and ERP integrations. The American Supply Association reported an increase in digital penetration by 2025. Grainger conducted a significant portion of its 2024 sales online, with a particular emphasis on standardized stainless fittings. While physical counters are shifting their focus to same-day fulfillment and custom cutting, digital marketplaces are increasingly securing routine replenishment orders.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Asia-Pacific dominated 49.52% of the 2025 global value and is set for a 5.94% CAGR to 2031. While China's infrastructure growth has moderated, it remains substantial in absolute terms. India's Jal Jeevan Mission, which emphasizes stainless steel, and Indonesia's Nusantara development, grappling with salinity issues, highlight the region's allure. Additionally, Vietnam's commitment to infrastructure and Thailand's water initiative further bolster this momentum.

In North America, a boost comes from investments allocated under the Infrastructure Act for water projects, coupled with the EPA's decade-long lead-line deadline. Meanwhile, Europe channels funds through its Renovation Wave and Drinking Water Directive, targeting building enhancements and corrosion-resistant mains. Both continents show a preference for stainless steel, valuing its long-term compliance and insurance benefits.

In the Middle-East and Africa, despite a smaller value share, growth is notable, exemplified by NEOM's hydrogen facilities, heavily investing in stainless steel. South America's trajectory hinges on Brazil's commitments to sanitation laws, with provinces experimenting with stainless steel to mitigate revenue losses from leaks. Japan and South Korea, both established markets, prioritize seismic-resilient stainless systems to protect their potable water lines.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The stainless steel plumbing pipes market is fragmented. Jindal Stainless is investing in a complex alongside an expansion at its Jajpur brownfield site. Automation is a rising moat. Mills deploying AWS-certified robotic cells achieve repeatable ferrite-number control, matching tougher ASTM A814 limits. ISO 9001 and ISO 14001 compliance now appears on municipal tenders, sidelining informal fabricators unable to finance labs and audits.

Stainless Steel Plumbing Pipes And Fittings Industry Leaders

APL Apollo

Jindal Stainless Ltd

Nippon Steel Corporation

Ratnamani Metals & Tubes Limited

Geberit Plumbing Technology India Private Limited

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: In Odisha (India), Ratnamani Metals & Tubes launched a Helically Submerged Arc Welded (HSAW) pipe manufacturing facility. This plant boosts its ability to cater to the demands of the infrastructure, water, and energy sectors.

- October 2024: Jindal Stainless pledged an investment of INR 5,400 crore (~USD 648 million) to boost its melt capacity to 4.2 million tonnes by 2027, allocating a significant portion of the funds for its downstream plumbing tube mills.

Global Stainless Steel Plumbing Pipes And Fittings Market Report Scope

Stainless-steel plumbing pipes are made of stainless steel, a metal alloy with at least 10.5% chromium that is exceptionally corrosion-resistant. For various reasons, stainless-steel plumbing pipes are extensively used in home and commercial systems. They are long-lasting, corrosion-resistant, and reasonably simple to install. Furthermore, stainless-steel plumbing pipes come in a wide range of diameters and styles, making them suited for various applications. Pipe elbows, tees, stub ends, pipe bends, end caps, reducers, pipe crosses, saddles, and many other fittings are available.

The stainless-steel plumbing pipes and fittings market is segmented by type, market structure, end-user industry, sales channel, and geography. By type, the market is segmented into seamless, welded, and fabricated. By market structure, the market is segmented into organized and unorganized. By end-user industry, the market is segmented into residential and non-residential. By sales channel, the market is segmented into retail, e-commerce, and direct. The report also covers the market size and forecasts for 28 countries. For each segment, the market sizing and forecasts are provided on the basis of value (USD).

By Type

| Seamless |

| Welded |

| Fabricated |

By Market Structure

| Organized |

| Unorganized |

By End-user Industry

| Residential |

| Non-residential |

By Sales Channel

| Retail |

| E-commerce |

| Direct |

By Geography

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Malaysia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Turkey | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Seamless | |

| Welded | ||

| Fabricated | ||

| By Market Structure | Organized | |

| Unorganized | ||

| By End-user Industry | Residential | |

| Non-residential | ||

| By Sales Channel | Retail | |

| E-commerce | ||

| Direct | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Malaysia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Turkey | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the value of the stainless steel plumbing pipes market?

The stainless steel plumbing pipes market size reached USD 5.38 billion in 2026 and is expected to reach USD 6.79 billion by 2031, registering a 4.78% CAGR in the period.

How fast is non-residential demand growing for stainless plumbing lines?

Non-residential applications are expanding at a 6.31% CAGR through 2031, outpacing housing projects.

Which region leads the global consumption of stainless steel plumbing pipes?

Asia-Pacific held 49.52% of 2025 global revenue and is projected to grow at a 5.94% CAGR.

Why are seamless stainless pipes gaining share?

Seamless versions eliminate weld seams, enabling up to 3,000 psi ratings, and are growing at a 6.18% CAGR.

How will e-commerce affect the procurement of stainless fittings?

Digital channels are growing 6.42% CAGR, embedding specifications and real-time inventory into contractor workflows.