Squalene Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

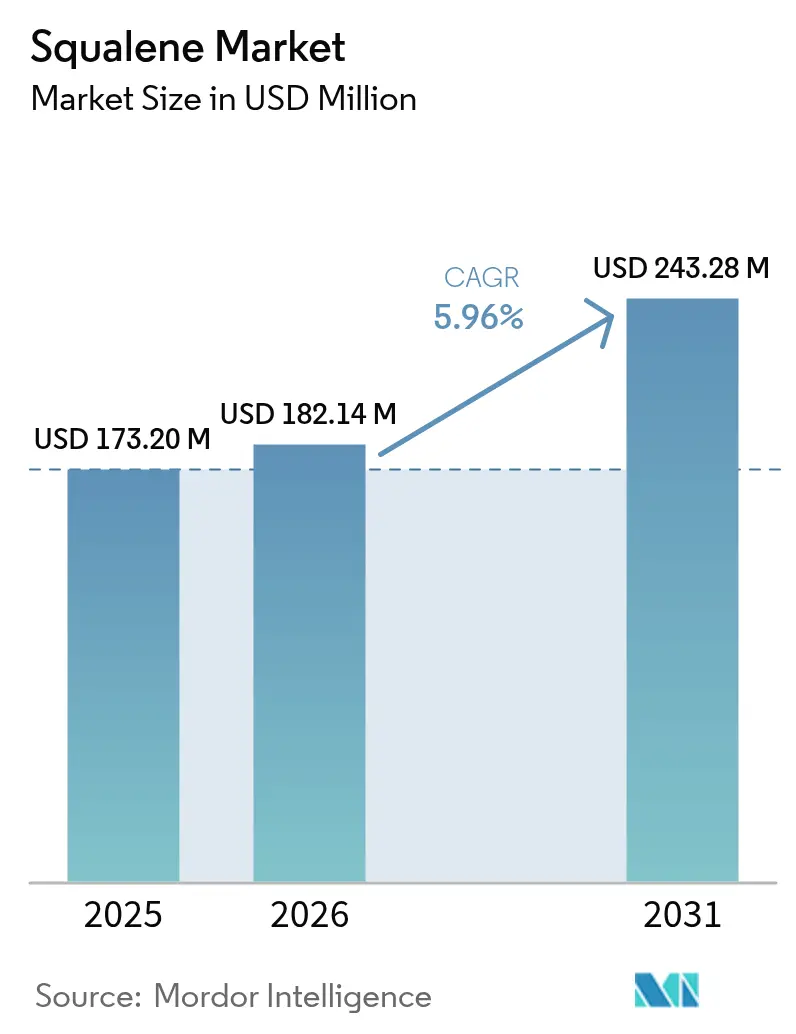

| Market Size (2026) | USD 182.14 Million |

| Market Size (2031) | USD 243.28 Million |

| Growth Rate (2026 - 2031) | 5.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Squalene Market Analysis by ���ϲ�����

The Squalene Market size is expected to grow from USD 173.20 million in 2025 to USD 182.14 million in 2026 and is forecast to reach USD 243.28 million by 2031 at 5.96% CAGR over 2026-2031. Rising preference for plant-derived and biosynthetic grades is realigning supply chains that had long depended on shark-liver extraction. Accelerated adoption in cosmetics reflects persistent clean-beauty demand, while vaccine adjuvants and oncology nano-delivery platforms are opening pharmaceutical-grade opportunities that capture premium margins. Regulatory bans on shark-sourced inputs and falling fermentation costs have narrowed the historic price gap between marine and sustainable feedstocks, spurring a bifurcated landscape in which cosmetic grade drives volume but pharmaceutical grade anchors profitability. Even so, drought-driven olive-oil volatility and elevated sugar prices for fermentation can trigger episodic cost spikes that challenge margin stability.

Key Report Takeaways

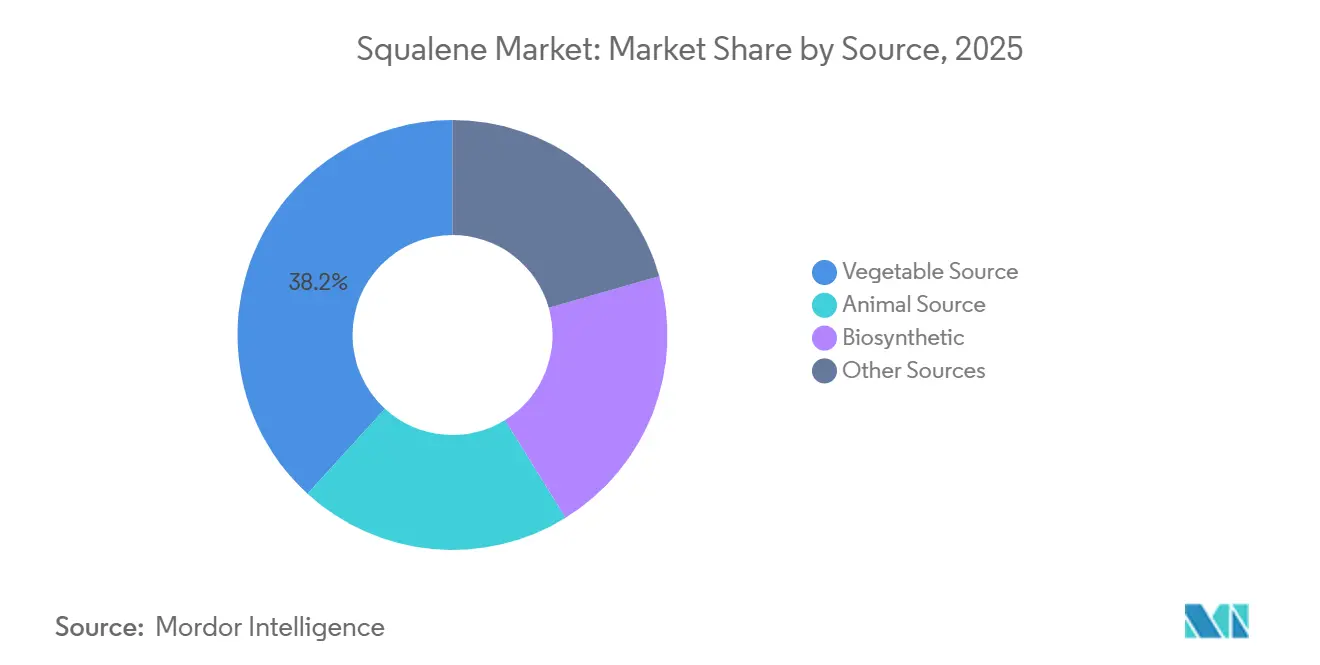

- By source, vegetable source commanded 38.22% of squalene market share in 2025 and is forecast to advance at a 6.96% CAGR through 2031.

- By purity grade, cosmetic grade held 68.85% of the squalene market size in 2025 and is projected to expand at a 6.58% CAGR to 2031.

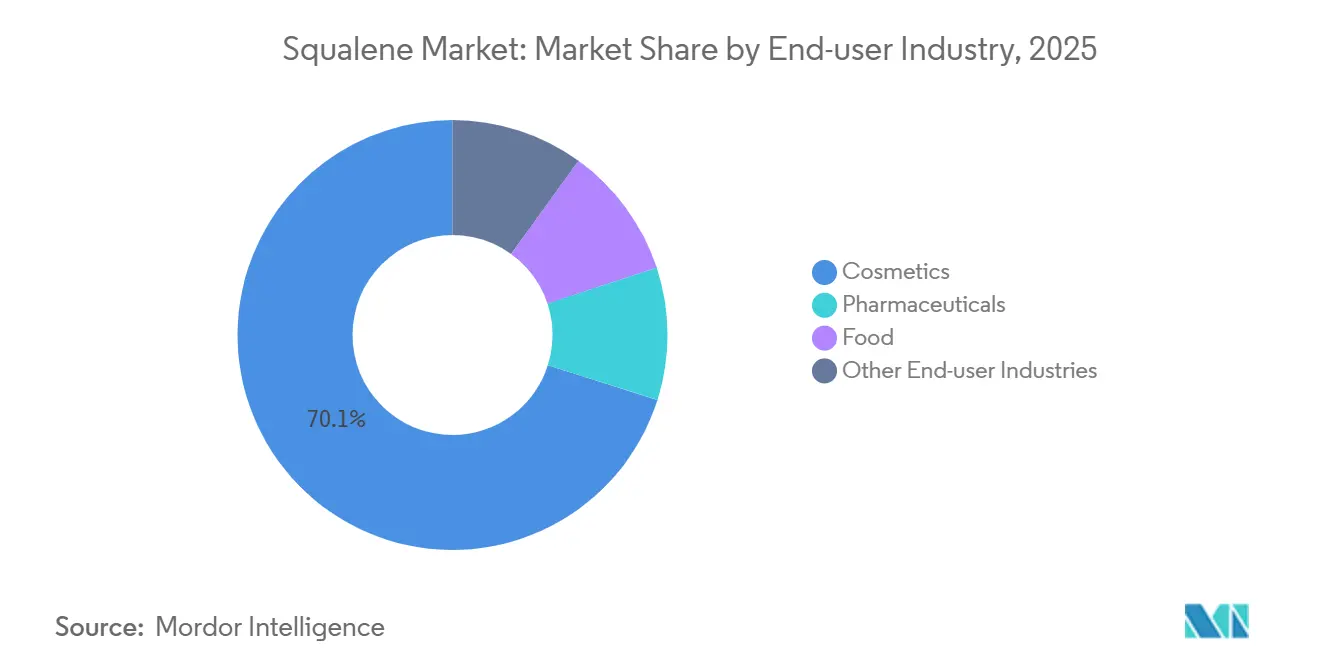

- By end-user industry, cosmetics accounted for 70.12% share of the squalene market size in 2025 and is growing at a 6.64% CAGR through 2031.

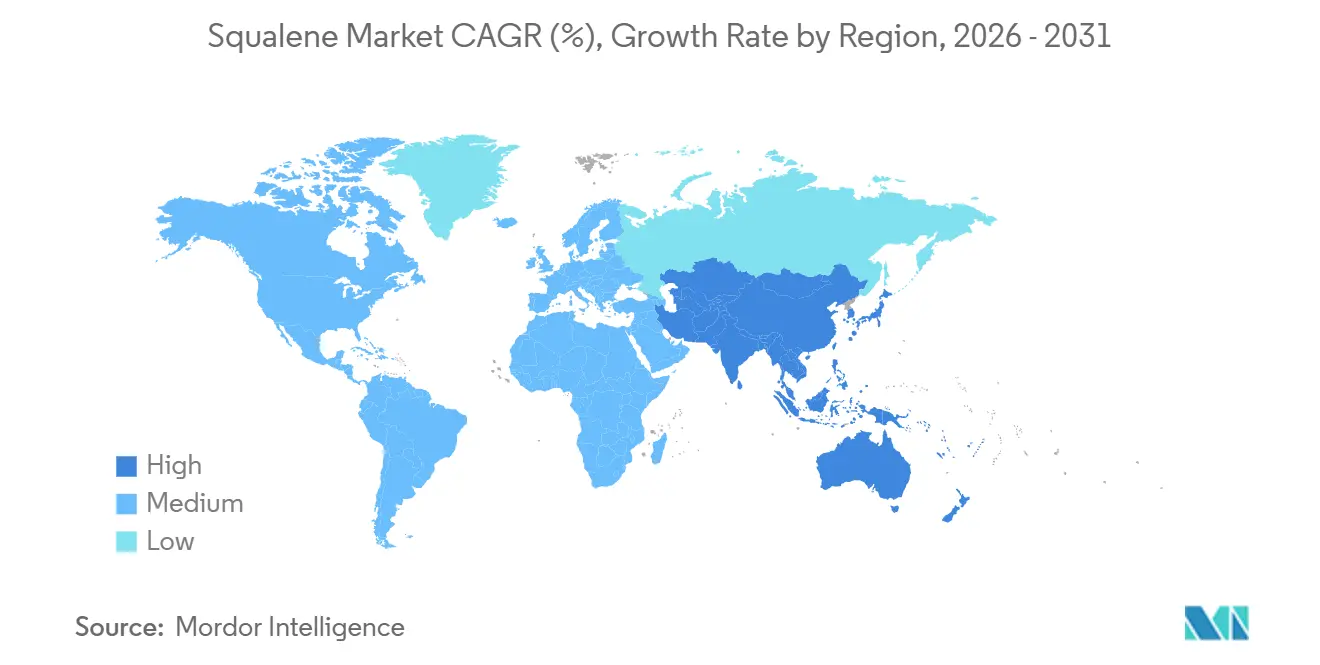

- By geography, Europe captured 42.08% of squalene market share in 2025; Asia-Pacific is the fastest-growing region at a 6.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Squalene Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clean-beauty boom boosting plant and bio-fermented supply | +1.8% | Global, with concentration in North America, Western Europe, and urban Asia-Pacific markets | Medium term (2-4 years) |

| Accelerating use in next-gen vaccine adjuvants | +1.5% | Global, with early adoption in North America and Europe for pandemic-preparedness stockpiles | Long term (≥ 4 years) |

| Synthetic-biology cost curve crossing shark-oil pricing | +1.2% | Global, with production hubs in Brazil, United States, and emerging fermentation clusters in China | Medium term (2-4 years) |

| Regulatory tailwinds banning shark-sourced ingredients | +1.0% | North America, European Union, and select Asia-Pacific jurisdictions (Taiwan, Australia) | Short term (≤ 2 years) |

| Emerging oncology nano-delivery trials adopting high-purity squalene | +0.8% | North America and Europe, with spillover to leading cancer-research centers in Asia-Pacific | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Clean-Beauty Boom Boosting Plant and Bio-Fermented Supply

Growing consumer insistence on transparent, cruelty-free labels is forcing cosmetic majors to abandon shark-derived squalene, a shift that has catalyzed capital allocation into olive, amaranth, and fermentation routes. Enzymatic extraction now recovers 0.5-1.0% of squalene from vegetable feedstock, roughly double solvent yields, tightening the squalene market supply chain and improving sustainability credentials. Evonik’s PhytoSquene, launched in 2023 and compliant with European Pharmacopoeia, illustrates how clean-beauty preferences dovetail with pharmaceutical-grade requirements. French refiner Sophim raised USD 21.5 million in 2023 to double olive-based capacity, responding to cosmetics and food players willing to pay 20-30% premiums for verified plant origin. Major beauty retailers now oblige suppliers to state squalene provenance on labels, effectively excluding shark sources even where law does not yet impose an outright ban. Industry observers expect shark-oil’s contribution to global supply to fall below 10% by 2028 as brands preempt reputational risk.

Accelerating Use in Next-Gen Vaccine Adjuvants

Squalene-containing adjuvants such as MF59 and Sepivac SWE have validated safety at scale, encouraging government stockpiles for pandemic-preparedness. Seqirus’s MF59 appears in more than 100 million administered flu vaccine doses, providing a regulatory benchmark that late-stage COVID-19 and universal influenza candidates are following. Microfluidic manufacturing, demonstrated in 2024, shortens batch time to seven hours and delivers 200-liter GMP emulsions, producing material for 5 million doses while lowering capital intensity for contract manufacturers by 40%. These efficiencies position decentralized facilities in emerging markets to meet surging demand without heavy investment. Early-phase oncology immunotherapies are also trialing squalene adjuvant systems that stimulate T-cell responses, hinting at broader pharmaceutical uptake. If regulatory approvals accelerate, pharmaceutical-grade offtake could exceed current forecasts and stretch capacity in the squalene market.

Synthetic-Biology Cost Curve Crossing Shark-Oil Pricing

Fermentation processes now deliver cosmetic-grade material at USD 50-70 per kg, matching or undercutting marine supply when compliance and ethical costs are considered. Amyris’s Barra Bonita plant in Brazil, retaining 1.8 million liter capacity after a 2026 line expansion, showcases economic viability despite Chapter 11 restructuring. Croda’s 2023 licensing of Amyris technology secures pharmaceutical-grade batches that avoid peroxide and heavy-metal purification steps required for shark-oil, trimming USD 20-30 per kg relative downstream expenses. Academic metabolic-engineering studies reach lab yields of 2-4 g/L in engineered cyanobacteria, and scale-up could drive cost to USD 30-40 per kg by 2028. Continuous drops in biosynthetic cost therefore tighten price dispersion among all sustainable grades in the squalene market.

Regulatory Tailwinds Banning Shark-Sourced Ingredients

CITES restricted liver-oil trade for deep-sea sharks in 2025, adding paperwork hurdles that disincentivize exporters. Taiwan and Australia mandate origin declarations that de facto eliminate shark-based imports, while the European Union’s cosmetics rules require ingredient transparency, letting consumer pressure do the rest. In the United States, policy think-tanks such as the National Security Commission on Emerging Biotechnology cast 2.7 million-shark annual harvests as a supply-chain risk, foreshadowing possible federal constraints[1]National Security Commission on Emerging Biotechnology, “Bio-Manufacturing Supply-Chain Report,” nsceb.gov . This regulatory momentum favors vegetable and biosynthetic capacity, further driving the squalene market toward sustainable sources.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-linked volatility in olive and amaranth feedstock pricing | -0.9% | Mediterranean Europe (Spain, Italy, Greece), South America (Argentina, Peru) | Short term (≤ 2 years) |

| Global fermentation-grade sugar price spikes (biofuel competition) | -0.7% | Brazil, India, Thailand, and other sugarcane-producing regions with ethanol mandates | Medium term (2-4 years) |

| Pharmaceutical-grade capacity bottlenecks for lipid adjuvants | -0.5% | Global, with acute constraints in North America and Europe where GMP certification timelines are longest | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Climate-Linked Volatility in Olive and Amaranth Feedstock Pricing

Mediterranean droughts cut Spanish and Italian olive yields during 2023-2024, lifting feedstock costs and squeezing refiners without long-term contracts[2]OECD-FAO, “Agricultural Outlook 2024-2033,” oecd-fao.org . Amaranth harvests in the Andes fluctuate 20-30% year on year, compelling processors to carry costly inventory buffers. Meanwhile, 16% of global vegetable oil now flows into biodiesel, diverting raw materials that could otherwise become squalene. The dual shocks of climate and biofuel demand can compress cosmetic-grade margins by 15-25% within a quarter. Unless drought-resistant cultivars scale quickly, price volatility will remain a near-term headwind for the squalene market.

Global Fermentation-Grade Sugar Price Spikes (Biofuel Competition)

Brazil’s RenovaBio and India’s E20 mandate channel sugarcane toward ethanol, tightening sucrose availability for biochemical fermentation. Elevated sugar costs have already forced Amyris to test molasses and bagasse hydrolysates, but added pretreatment lifts unit cost USD 5-10 per kg. Because GMP revalidation takes at least a year, producers cannot easily switch feedstocks without delaying pharmaceutical deliveries. Elevated sugar prices are thus a structural restraint on biosynthetic expansion and can temper the upside potential of the squalene market over the medium term.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Vegetable and Biosynthetic Grades Ascendant

Vegetable-source squalene represented 38.22% of squalene market share in 2025 and is projected to advance at a 6.96% CAGR, outperforming animal-derived supply. Expansion by olive refiners in Spain and France and amaranth processors in Argentina and Peru is supported by capital aimed at meeting GMP requirements for both cosmetic and pharmaceutical channels. The squalene market size for vegetable source is therefore set to climb steadily as retail mandates solidify plant-only positioning in prestige beauty.

Biosynthetic is growing already indispensable for vaccine adjuvants. Amyris’s 1.8 million-liter Barra Bonita footprint anchors global supply agreements with Croda, which uses the feedstock for pharmaceutical-grade emulsions. Ongoing metabolic-engineering breakthroughs promise even greater yields that can trim cost curves further. Conversely, animal-source share is shrinking under CITES trade limits and consumer backlash. As more jurisdictions legislate origin labeling, shark-oil segments will continue to decline, reinforcing a structural pivot toward sustainable feedstocks in the squalene market.

By Purity Grade: Cosmetic Volume vs. Pharmaceutical Margin

Cosmetic grade comprised 68.85% of 2025 volume and is on course for a 6.58% CAGR. Reformulation away from shark oil has pushed legacy and indie brands alike to specify olive, amaranth, or biosynthetic grades, turning supply transparency into a selling point on retail shelves. Sustainable positioning supports price resilience even when raw-material costs rise.

The squalene market size for pharmaceutical grade is also projected to widen as adjuvant stockpiles increase and oncology nano-delivery trials progress. Croda’s and Evonik’s GMP lines meet European Pharmacopoeia standards, giving them pricing leverage especially during vaccine surges. Food grade is expanding into nutraceutical softgels and fortification, but total uptake remains modest relative to topical cosmetics.

By End-user Industry: Cosmetics Lead, Pharma Gains Momentum

Cosmetics captured 70.12% share of the overall squalene market size in 2025, expanding at a 6.64% CAGR through 2031. Anti-aging serums, moisturizers, and hair-care treatments value squalene’s emollient and oxidative-stability properties, and ingredient-disclosure requirements are nudging even mass brands into sustainable sources.

Pharmaceutical usage is smaller but rising swiftly. MF59, Sepivac SWE, and new TLR-agonist systems underline growth potential in both pandemic preparedness and immuno-oncology. If even a few pipeline candidates win approval, the squalene market share for pharmaceutical end users could climb significantly, absorbing much of the forthcoming biosynthetic capacity. Food, lubricant, and specialty-chemical applications remain niche but deliver diversification upside, especially where squalene’s thermal stability outperforms petro-based analogs.

Geography Analysis

Europe held 42.08% squalene market share in 2025, anchored by legacy olive supply chains in Spain, Italy, and France and by GMP plants serving vaccine hubs. The EU cosmetics rulebook obliges INCI transparency, favoring plant or biosynthetic inputs over shark derivatives, and regional refiners such as Sophim have expanded to capture both cosmetic and food verticals. Evonik’s PhytoSquene award underscores Europe’s commitment to pharmaceutical-grade innovation.

North America benefits from clean-beauty enthusiasm and government assessments framing biosynthetic squalene as a strategic asset. Nearshoring of vegetable refining into Mexico adds logistical resilience, while U.S. firms monitor potential regulatory shifts that could mirror Europe’s stricter stance on animal sourcing.

Asia-Pacific is the fastest-growing region, advancing at 6.79% CAGR through 2031. Chinese, Indian, and Korean brands are incorporating plant-based and biosynthetic squalene into affordable SKUs, widening addressable volume. India’s vaccine-manufacturing expansion seeks cost-effective GMP squalene, and local fermentation clusters can meet both domestic and export demand. Japanese and South-Korean premium brands employ squalene to cement skin-compatible reputations, while Southeast Asian nations explore palm and coconut-based extraction despite lower yields.

South America merges Brazil’s fermentation leadership with Argentina’s and Peru’s amaranth agriculture. Amyris’s plant signals export potential if feedstock costs stabilize. Middle-East and Africa currently import most requirements, yet vaccine facility build-outs in Saudi Arabia and Egypt imply future pharmaceutical-grade demand.

Competitive Landscape

The squalene market remains moderately fragmented. Croda, Evonik, and Sophim anchor established plant-based and pharmaceutical channels, while Amyris leads biosynthetic output despite its restructuring. Croda’s 2023 agreement secures exclusive access to Amyris fermentation batches for vaccine adjuvants, illustrating how incumbents hedge supply-chain risk. Evonik’s PhytoSquene expands vegetable grades into GMP territory and garners premium pricing.

Emerging players pursue microalgae and engineered-microbe routes. Laboratory yields show promise, yet capital intensity and scale-up risks continue to deter immediate commercialization. Technology differentiation focuses on microfluidic adjuvant production that cuts batch time and capex, a feature attractive to contract manufacturers under pandemic-preparedness mandates. Patent filings around squalene-drug conjugates indicate intensifying R&D race for oncology applications.

Regulatory certification differentiates winners. USP compliance allows 30-50% price premiums, especially when vaccine programs surge. Cosmetic-grade sellers, by contrast, confront commoditization unless vertically integrated into the raw olive or sugar supply. Collective moves imply sharpening competition over sustainable feedstock control and pharmaceutical-grade throughput, shaping the next growth phase of the squalene market.

Squalene Industry Leaders

Croda International Plc

Sophim

Amyris

efpbiotek

KISHIMOTO SPECIAL LIVER OIL CO., LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Amyris expanded its Barra Bonita facility in Brazil by adding a fourth independent precision fermentation line. This expansion enhanced the production capacity for specialty ingredients, including components such as squalene used in vaccine adjuvants.

- October 2023: Evonik Industries AG launched PhytoSquene, a GMP-grade, plant-based squalene sourced from amaranth oil. It provided a sustainable, non-animal-derived alternative to shark liver oil for pharmaceutical, vaccine adjuvant, and cosmetic applications while ensuring consistent quality and supporting biodiversity.

Global Squalene Market Report Scope

Squalene, a colorless and odorless organic compound, is commercially extracted from shark liver oil and is non-toxic. Due to its non-toxic nature, squalene has extensive applications in personal care. In the cosmetics industry, squalene oil combats free radicals, which are known to damage the skin and accelerate aging.

The squalene market is segmented by source, purity grade, end-user industry, and geography. By source, the market is segmented into animal source, vegetable source, biosynthetic, and other sources. By purity grade, the market is segmented into cosmetic grade, pharmaceutical (GMP) grade, and food grade. By end-user industry, the market is segmented into cosmetics, pharmaceuticals, food, and other end-user industries. The report also covers the market size and forecasts for squalene in 27 countries across major regions. For each segment, the market size and forecasts have been done on the basis of value (USD).

| Vegetable Source |

| Animal Source |

| Biosynthetic |

| Other Sources |

| Cosmetic Grade |

| Pharmaceutical (GMP) Grade |

| Food Grade |

| Cosmetics |

| Pharmaceuticals |

| Food |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Turkey | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| Nigeria | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Source | Vegetable Source | |

| Animal Source | ||

| Biosynthetic | ||

| Other Sources | ||

| By Purity Grade | Cosmetic Grade | |

| Pharmaceutical (GMP) Grade | ||

| Food Grade | ||

| By End-user Industry | Cosmetics | |

| Pharmaceuticals | ||

| Food | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Turkey | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the squalene market?

The squalene market size reached USD 182.14 million in 2026 and is projected to hit USD 243.28 million by 2031, reflecting a 5.96% CAGR over 2026-2031.

Which source segment is expanding quickest?

Vegetable-source squalene is advancing at a 6.96% CAGR through 2031 as clean-beauty reformulations accelerate.

What drives pharmaceutical demand for squalene?

Vaccine adjuvants such as MF59 and emerging oncology nano-delivery platforms require high-purity GMP squalene that offers batch consistency and proven safety profiles.

Why is shark-liver squalene declining?

Conservation rules, mandatory ingredient disclosure, and the falling cost of biosynthetic and plant-derived alternatives are steadily eroding marine sourcing.

Page last updated on: