Sports Sunglasses Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

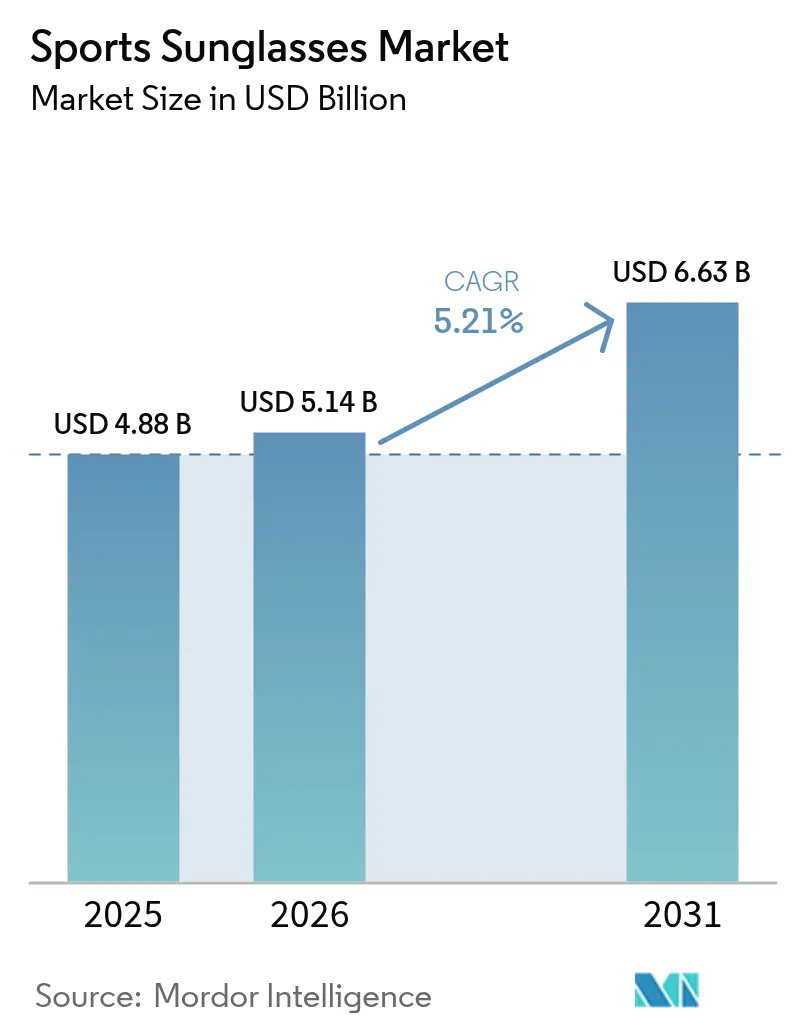

| Market Size (2026) | USD 5.14 Billion |

| Market Size (2031) | USD 6.63 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Sports Sunglasses Market Analysis by ���ϲ�����

The sports sunglasses market size is expected to grow from USD 4.88 billion in 2025 to USD 5.14 billion in 2026 and is forecasted to reach USD 6.63 billion by 2031 at 5.21% CAGR over 2026-2031. Driving factors behind this growth include a surge in women's participation in sports, the melding of eyewear with fashion trends, and government investments in new sports facilities. North America leads in market volume, but the Asia-Pacific region is poised for the fastest growth, spurred by government policies and a boost in local manufacturing. While athletes remain the primary users of sports sunglasses, there's a notable uptick in demand from lifestyle consumers using them for daily activities. The premium segment of the product category is witnessing rapid growth, although the mass-market segment retains a dominant share. E-commerce is reshaping the sales landscape, positioning online platforms as vital channels for companies. The market is concentrated, with a handful of key players at the helm. For example, Essilor Luxottica is broadening its global manufacturing reach, setting up a lens production hub in Thailand and expanding its high-index lens facility in Mexico.

Key Report Takeaways

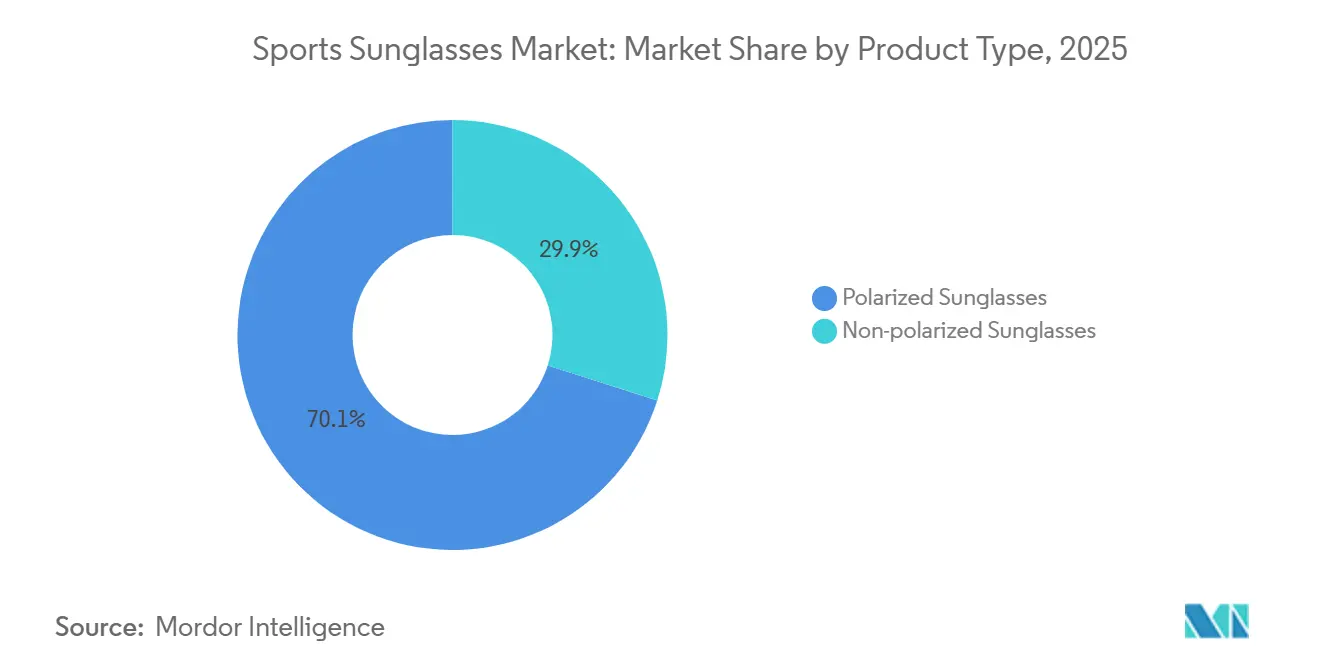

- By product type, polarized lenses captured 70.04% of the sports sunglasses market share in 2025; non-polarized lenses are forecast to expand at a 7.63% CAGR to 2031.

- By sports type, cycling and motorsports accounted for 32.74% of 2025 demand, while running and outdoor adventure sports posted the strongest outlook, with a 6.83% CAGR.

- By end user, adults accounted for 78.13% of the sports sunglasses market in 2025, whereas the kids/children’s segment is projected to grow at a 6.21% CAGR through 2031.

- By consumer group, amateur and professional athletes accounted for 63.45% of 2025 demand, while outdoor lifestyle users recorded the strongest outlook at 7.78% CAGR.

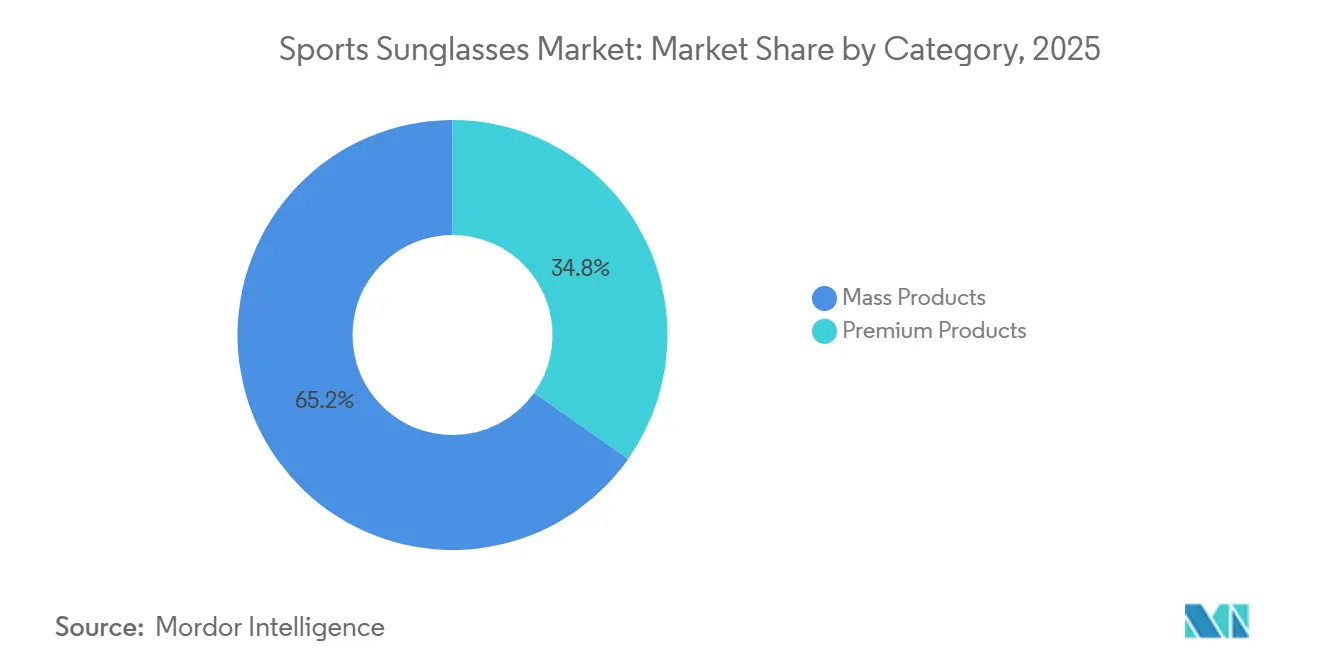

- By category, mass products led with 65.22% revenue share in 2025; the premium tier is set to advance at a 6.35% CAGR to 2031.

- By distribution channel, offline stores retained 65.76% share of the sports sunglasses market size in 2025, yet online sales are poised for a 7.57% CAGR.

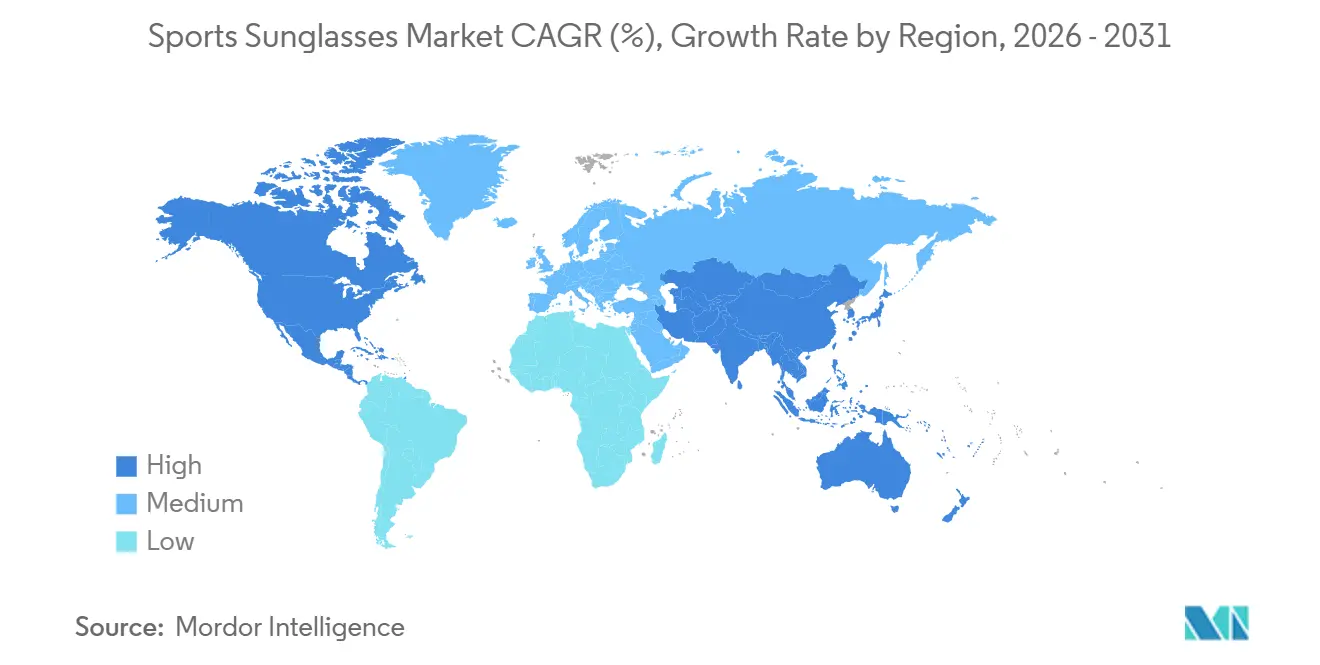

- By geography, North America held 33.04% of 2025 revenue, and Asia-Pacific is projected to deliver a 6.55% CAGR, the quickest regional climb.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sports Sunglasses Market Trends and Insights

Drivers Impact Table*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Significant growth in women sports participation rate | +1.2% | Global, with early gains in United Kingdom, North America | Medium term (2-4 years) |

| Aggressive marketing by reputed brands | +0.9% | Global | Short term (≤ 2 years) |

| Influence of social media platforms and celebrity endorsements | +0.8% | Global, stronger in North America and Europe | Short term (≤ 2 years) |

| Favourable government initiatives to boost sports culture | +1.0% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Increasing participation in outdoor and sports activities | +1.1% | Global | Medium term (2-4 years) |

| Fashion and lifestyle integration | +0.7% | North America and Europe | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Increasing participation in outdoor and sports activities

More people around the world are taking part in sports and outdoor activities, which is increasing the demand for performance gear like sports sunglasses. In 2024, around 247.1 million Americans, or about 80% of the population, participated in at least one sport, fitness, or outdoor activity [1]Source: Sports and Fitness Industry Association, "SFIA’s Topline Participation Report Shows 247.1 Million Americans Were Active in 2024," sfia.org. Popular activities such as hiking, running, cycling, and water sports have seen significant growth. For example, over 37 million people are cycling, 40 million are camping, and activities like paddleboarding, climbing, and mountain biking are steadily growing each year. Similarly, visits to U.S. national parks reached nearly 331.9 million in 2024, the highest ever recorded, showing a clear rise in outdoor recreation [2]Source: National Park Service Government, "Annual Visitation Statistics Release," nps.gov. Globally, more young people are also getting involved in sports, especially outdoor activities. With this increased participation in outdoor environments where sun exposure is high, there is a growing awareness of the need for protective and functional eyewear. Brands like Sunski launched its Spring 2025 Collection featuring ultralight models such as Foxtrot, targeting casual users who prioritize comfort and aesthetics over technical specifications.

Favorable government initiatives to boost sports culture

Governments worldwide are increasingly prioritizing safety and performance gear, such as sports sunglasses, as part of their strategies to enhance sports ecosystems. For instance, India’s National Sports Policy 2024 emphasizes the use of protective equipment across all levels of sports training, from grassroots programs to elite competitions, ensuring high-performance eyewear becomes a standard part of sports gear [3]Source: Department of Sports, Ministry of Youth Affairs and Sports, "The Department of Sports, Ministry of Youth Affairs and Sports, New Delhi, is in the process of framing National Sports Policy (NSP), 2024 for the development of sports and providing a roadmap to achieve excellence in sports in the country," yas.gov.in. State-backed programs are expanding sports participation in emerging markets, creating new consumer cohorts. China's State Council set a target of 5 trillion yuan for the sports industry by 2025, with policies promoting outdoor recreation and fitness infrastructure, according to the State Council of China. India's Khelo India initiative funds grassroots sports development, increasing access to organized athletics and protective equipment, according to the Ministry of Youth Affairs and Sports, India. These interventions lower entry barriers for first-time participants, many of whom require affordable, durable eyewear. These efforts establish the consistent use and regular replacement of performance-grade sunglasses, driving sustained demand across both amateur and professional sports sectors.

Influence of social media platforms and celebrity endorsements

Social media amplifies product visibility and drives impulse purchases, particularly among Gen Z and Millennials. Oakley capitalized on this by launching Tour de France-specific models, Sutro Lite Sweep and Velo Kato, in 2025, paired with influencer content during the race. EssilorLuxottica extended its Ray-Ban Meta partnership, integrating smart eyewear with social sharing features, blurring the line between performance optics and connected devices. However, authenticity matters; consumers penalize brands perceived as inauthentic or misaligned with athlete values. The shift toward micro-influencers and sport-specific communities suggests that broad celebrity endorsements may yield diminishing returns compared to targeted partnerships with credible athletes in niche disciplines like trail running, gravel cycling, or open-water swimming.

Significant growth in women sports participation rate

Women’s participation in sports has grown significantly worldwide in recent years, creating a larger market for performance eyewear like sports sunglasses. Government initiatives, such as the U.K.’s Women’s Sport Investment Accelerator, aim to boost the women’s sports economy beyond GBP 1 billion in 2024, further driving this trend [4]Source: Government UK, "Government pledges to make UK ‘top destination for women’s sport investment’ following record-breaking summit," gov.uk. As more women engage in structured training and competitive sports, the demand for specialized gear, including protective eyewear designed for various outdoor conditions, has increased. Brands investing in women-specific frame geometries, narrower nose bridges, and smaller lens profiles stand to capture loyalty in a segment historically underserved. The trend extends beyond elite athletes; recreational runners, cyclists, and outdoor enthusiasts now expect eyewear that accommodates physiological differences without sacrificing style or protection.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Prevalence of counterfeit and low-quality products | -0.8% | Global, concentrated in Asia-Pacific | Short term (≤ 2 years) |

| Lack of standardized regulations restricts growth | -0.6% | Global | Long term (≥ 4 years) |

| High cost of premium sports sunglasses | -0.5% | Global | Medium term (2-4 years) |

| Seasonality and weather dependence | -0.4% | North America and Europe | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Prevalence of counterfeit and low-quality products

The global market for sports sunglasses faces a significant challenge due to the rise of counterfeit and low-quality products, which undermine consumer trust and damage the reputation of premium brands. For instance, in Southeast Asia, authorities are actively combating this issue. In the Philippines, the National Bureau of Investigation seized over 1,000 fake Oakley sunglasses valued at PHP 1.6 million in May 2025. Low-quality lenses lacking UV protection pose health risks, yet price-conscious consumers often cannot distinguish fakes from genuine products. Brands are responding with authentication technologies, serialized holographic labels, blockchain-based provenance tracking, and direct-to-consumer models that bypass gray-market intermediaries. This growing prevalence of fake products not only raises safety concerns but also discourages consumers from investing in authentic, high-quality performance eyewear, ultimately hindering the growth of the market.

High cost of premium sports sunglasses

Premium sports sunglasses often come with hefty price tags, posing a significant barrier to wider consumer adoption. Oakley, for instance, their high-performance sunglasses, equipped with advanced features like Prizm lenses, prescription options, and lightweight carbon fiber frames, range from USD 230 to a staggering USD 930, contingent on customization. Even mid-tier brands like Revo and Tifosi have models priced between USD 80 and USD 200, which can be a stretch for many. Moreover, industry behemoth Luxottica, the parent of renowned brands such as Ray-Ban, Oakley, and Sunglass Hut, faces accusations of monopolistic pricing. This consolidation not only keeps prices elevated but also curtails the availability of budget-friendly alternatives. Consequently, many price-sensitive consumers either shy away from premium sunglasses or resort to cheaper, lower-quality, or even counterfeit options.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Polarized Technology Drives Premium Positioning

Polarized sunglasses led the sports sunglasses market in 2025, capturing 70.04% of the market share. Their dominance is attributed to their ability to effectively reduce glare, making them highly suitable for activities like water and snow sports. This trend is expected to continue through 2031, although non-polarized lenses are anticipated to grow at a faster CAGR of 7.63%. Costa Del Mar launched new polarized models in December 2024, emphasizing water-activity performance and expedition durability, while Oakley's Watersports Collection in April 2025 targeted anglers and boaters with Prizm lens technology optimized for aquatic environments. These technological developments not only support premium pricing but also help sustain the market's position in the high-value category.

Meanwhile, non-polarized growth reflects two dynamics: budget-conscious first-time buyers entering the market through mass-market channels, and athletes in sports like cycling or running, where polarization can obscure road hazards or trail features. UVEX and 100% Speedlab offer non-polarized models with UV400 protection at accessible price points, capturing share among recreational users who value basic eye protection without advanced optics. The segment also benefits from fashion-forward consumers who prioritize aesthetics over technical performance, particularly in athleisure contexts where sunglasses function as style accessories. Compliance with ISO 12312-1 ensures that even non-polarized products meet minimum UV protection and optical quality standards, reducing the performance gap and making them viable for casual use, according to ISO.

By Sports Type: Cycling and Motorsports Lead While Running and Outdoor Adventure Accelerate Growth

The cycling and motorsports segment is projected to lead the global sports sunglasses market, accounting for 32.74% of total demand in 2025. This dominance is attributed to the extensive use of performance eyewear by professional and recreational cyclists and motorsport enthusiasts. The segment benefits from innovations such as lightweight frames, aerodynamic designs, and advanced lens technologies like polarization and UV protection. Additionally, consistent participation in cycling across regions such as Europe and North America, coupled with frequent use, continues to drive demand in this category.

Running and outdoor adventure sports are expected to grow the fastest, with a CAGR of 6.83% during the forecast period. This growth is fueled by the growing global emphasis on health and fitness, alongside rising participation in activities such as running, trekking, and hiking. Expanding adventure tourism and heightened awareness of protective eyewear in outdoor settings further support this trend. The segment is also gaining momentum in emerging markets where fitness trends are on the rise. Furthermore, product versatility and growing affordability are encouraging adoption among both casual and professional users.

By End User: Adult Dominance Masks Children’s Growth Potential

In 2025, adults accounted for 78.13% of the sports sunglasses market revenue, driven by their consistent demand for high-performance lenses and regular replacement cycles. While adults remain the primary consumers of sports sunglasses due to their purchasing power and preference for premium products, the rising adoption among school-age athletes is creating new growth opportunities. The increasing focus on youth-oriented designs and safety features is diversifying the market, ensuring it caters to a broader age group. This shift not only reflects the evolving consumer base but also underscores the importance of addressing the unique requirements of younger users. As a result, the sports sunglasses market is poised for sustained growth across both adult and children’s segments.

However, the children’s segment is projected to grow at a faster CAGR of 6.21%, propelled by rising youth sports enrollment and heightened parental awareness of eye-injury risks. England reported that 47.8% of children aged 5-16 met activity guidelines, while the US records approximately 600,000 sports-related eye injuries annually among youth, with 90% preventable through proper eyewear, according to Sport England and the American Academy of Ophthalmology. ASTM F803 sets impact-resistance standards for youth sports eyewear, and compliance is increasingly mandated by schools and youth leagues, creating a regulatory tailwind for certified products. EssilorLuxottica expanded its Essilor Stellest sun lens range in May 2024, offering prescription sunglasses for children and adolescents with myopia-correcting optics and UV protection, addressing both vision correction and outdoor safety.

By Consumer Group: Athletes Lead While Lifestyle Consumers Accelerate

In 2025, amateur and professional athletes accounted for 63.45% of the customer base, highlighting the critical role of precision optics in enhancing sports performance. However, the outdoor lifestyle segment is growing at a notable CAGR of 7.78%, driven by the increasing adoption of sunglasses as both functional sports gear and everyday accessories. Amateur and professional athletes remain critical for product validation and technical feedback, yet their slower growth reflects market saturation in established sports like road cycling and marathon running. For instance, Oakley’s collaboration with Tudor Pro Cycling to develop integrated helmet-eyewear systems demonstrates how innovations designed for elite athletes are gradually becoming accessible to the broader market, catering to both performance and style needs.

The rise of the athleisure trend has further expanded the appeal of sports sunglasses. The athleisure segment skews younger and more fashion-conscious, with Gen Z and Millennials valuing influencer endorsements and social media visibility over traditional athlete sponsorships. Products like Nike’s Athena and Zeus, which are crafted using recycled materials and equipped with Max Extreme lenses, seamlessly blend functionality with fashion. These sunglasses are versatile enough to be used in gyms, as part of streetwear, or in competitive sports settings. This dual-purpose approach has strengthened the sports sunglasses market, allowing it to attract both performance-driven athletes and style-conscious casual consumers, ensuring sustained growth across diverse customer segments.

By Category: Premium Segment Accelerates Despite Mass Market Dominance

In 2025, mass-priced sports sunglasses dominated the market, contributing 65.22% of the total revenue due to their affordability and accessibility to a broad consumer base. Mass-market players like Decathlon and UVEX benefit from vertical integration and economies of scale, offering competent optics at accessible price points that capture the majority of volume. Sustainability is emerging as a premium differentiator; Bollé's REACT FOR GOOD program aims for 90% eco-designed products by 2027, using bio-sourced and recycled materials in helmets and goggles, with the Eco V-Atmos visor helmet priced at EUR 195.41. Rudy Project launched the Astral model with its RideToZero sustainability initiative, appealing to environmentally conscious consumers willing to pay a premium for circular-economy practices.

Despite this, the premium segment is experiencing notable growth, with a projected CAGR of 6.35%. This growth is fueled by innovations in materials and lens technology, offering enhanced performance and durability. For example, TAG Heuer’s titanium frames with a proprietary 27° hinge showcase how luxury-level engineering is being integrated into sports eyewear, appealing to consumers seeking high-quality, performance-driven products. The premium segment's trajectory depends on articulating clear performance or sustainability benefits that justify price premiums, particularly in price-sensitive regions where mass products dominate.

By Distribution Channel: Digital Transformation Accelerates Online Growth

In 2025, offline retail stores dominated the market, contributing 65.76% of the total revenue, as many consumers preferred the ability to try on sports sunglasses in person before making a purchase. Despite this, online sales are projected to grow at a robust annual rate of 7.57%, fueled by advancements in virtual try-on technologies and the convenience of direct-to-consumer delivery models. For instance, leading eyewear brands like Oakley and Decathlon have reported significant growth in their e-commerce divisions, with Oakley noting a sharp increase in online engagement following the integration of 3D try-on features across its product lines.

Brands are increasingly focusing on enhancing their digital presence to attract online shoppers. Evil Eye, for example, has introduced interactive lens simulators that allow customers to experience real-world glare reduction virtually, bridging the gap between online and in-store shopping experiences. On the other hand, physical retailers are adopting digital tools within their stores, such as offering personalized, data-driven consultations. This hybrid approach combines the tactile experience of trying on products in-store with the convenience and customization of digital solutions, creating a seamless and engaging shopping journey for consumers.

Geography Analysis

North America accounted for 33.04% of global revenue in 2025. The region benefits from high disposable incomes, widespread adoption of premium eyewear, and robust retail infrastructure spanning specialty outdoor stores, optical chains, and direct-to-consumer channels. Oakley's Foothill Ranch R&D facility and 372 global stores reflect the brand's North American roots and continued investment in product innovation. Additionally, strict FDA and ANSI regulations create high entry barriers for low-quality products, enabling premium brands to maintain strong profit margins. EssilorLuxottica reported record sales in its North American segment in FY 2024, reflecting favorable market conditions.

Asia-Pacific is the fastest-growing region at 6.55% CAGR through 2031, driven by China's 400 million outdoor enthusiasts and government policies targeting a 5 trillion yuan sports industry by 2025, according to the China Outdoor Industry Association. India's Khelo India program expands grassroots sports access, creating new consumer cohorts in tier-2 and tier-3 cities where organized athletics were previously limited, according to the Ministry of Youth Affairs and Sports, India. Japan's aging population sustains demand for outdoor recreation, with hiking and cycling popular among retirees seeking active lifestyles. The region's growth is tempered by price sensitivity; mass-market products dominate, and counterfeit proliferation erodes brand equity.

Europe, South America, and Middle East and Africa collectively account for the remaining market share, each exhibiting distinct dynamics. Europe continues to show steady growth, supported by the EN ISO 12312-1 solar protection standard, which influences global product requirements. South America's growth is constrained by economic volatility and currency fluctuations, yet outdoor recreation is gaining traction in Brazil, Argentina, and Chile, supported by natural landscapes conducive to hiking and trail running. Middle East and Africa represents a nascent opportunity, with Saudi Arabia and UAE investing in sports infrastructure as part of economic diversification strategies.

Competitive Landscape

The sports sunglasses market is moderately consolidated. EssilorLuxottica SA has been expanding its global manufacturing capabilities, including its lens hub in Thailand and a high-index lens facility in Mexico. These expansions aim to reduce lead times and shipping costs, enhancing operational efficiency. Additionally, the company’s acquisitions of Supreme and Heidelberg Engineering highlight its dual focus on lifestyle and medical technology, ensuring a diversified revenue stream and long-term growth potential.

Collaborations with elite athletes and sports organizations continue to strengthen brand visibility and product innovation. For instance, Oakley collaborates with professional athletes across sports such as basketball, cycling, and esports to co-develop advanced lens technologies. This collaboration creates a feedback loop that drives continuous product improvement. Furthermore, evolving sports-specific eyewear guidelines from the ISO/TC 94/SC 6 committee are shaping the design and functionality of products across the industry, ensuring compliance and performance standards are met.

Manufacturing hubs are becoming more sophisticated, with China’s Fengjie facilities now producing eyewear for global brands like Adidas and Under Armour. These advancements have streamlined production timelines and opened opportunities for private-label manufacturing. At the same time, private equity-backed startups are entering niche segments such as gaming optics, children’s eyewear, and adaptive lenses. These new players are intensifying competition, pushing established brands to accelerate innovation and introduce frequent product upgrades and limited-edition releases to maintain their market position.

Sports Sunglasses Industry Leaders

-

Adidas AG

-

Decathlon SA

-

Under Armour Inc.

-

EssilorLuxottica SA

-

Kering SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Hobie Eyewear debuted new polarized sunglasses products at Surf Expo in January 2026, including the Hatch Float floating polarized frame and the Mojo Float 2.0 with enhanced performance features.

- April 2025: EssilorLuxottica recently completed the acquisition of Visard and made strategic investments in Mistral. These moves aim to enhance the company’s production capacity and diversify its product portfolio. This expansion also aligns with the company’s strategy to strengthen its global footprint and maintain a competitive edge in the sports sunglasses market.

- February 2025: Jaylen Brown has entered into a multi-year partnership with Oakley to collaborate on the creation of products, including both eyewear and apparel. This collaboration aims to combine Brown's influence as a professional athlete with Oakley's expertise in innovative design.

Global Sports Sunglasses Market Report Scope

Sports sunglasses are protective eyewear worn by athletes to shield their eyes from UV rays, dirt, and dust during play. The Sports Sunglasses Market Report is Segmented by Product Type (Polarized Sunglasses and Non-Polarized Sunglasses), End User (Adult and Kids/Children), Consumer Group (Amateur and Professional Athletes and More), Category (Mass and More), Distribution Channel (Offline and Online), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Polarized |

| Non-Polarized |

| Cycling and Motorsports |

| Running and Outdoor Adventure Sports |

| Winters Sports |

| Water Sports |

| Ball Sports |

| Others (Shooting, Hunting, Tactical Sports) |

| Adults |

| Kids/Children |

| Amateur and Professional Athletes |

| Outdoor Lifestyle/Athleisure Consumer |

| Mass |

| Premium |

| Online Stores |

| Offline Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Polarized | |

| Non-Polarized | ||

| By Sports Type | Cycling and Motorsports | |

| Running and Outdoor Adventure Sports | ||

| Winters Sports | ||

| Water Sports | ||

| Ball Sports | ||

| Others (Shooting, Hunting, Tactical Sports) | ||

| By End User | Adults | |

| Kids/Children | ||

| By Consumer Group | Amateur and Professional Athletes | |

| Outdoor Lifestyle/Athleisure Consumer | ||

| By Category | Mass | |

| Premium | ||

| Distribution Channel | Online Stores | |

| Offline Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the sports sunglasses market in 2026?

The sports sunglasses market size reached USD 5.14 billion in 2026 and is on course to hit USD 6.63 billion by 2031.

Which product type leads sales?

Polarized models dominate with 70.04% of 2025 revenue, though non-polarized variants are growing faster at 7.63% CAGR.

Why is Asia-Pacific the fastest-growing region?

Government-funded sports programs in China and India, coupled with a surge in outdoor recreation, push Asia-Pacific to a 6.55% CAGR.

What restrains broader adoption of premium models?

High retail prices, especially after import duties in Latin America and Asia, limit premium penetration despite rising interest.

Page last updated on: