Special Effect Pigments Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 1.02 Billion |

| Growth Rate (2026 - 2031) | 4.11% CAGR |

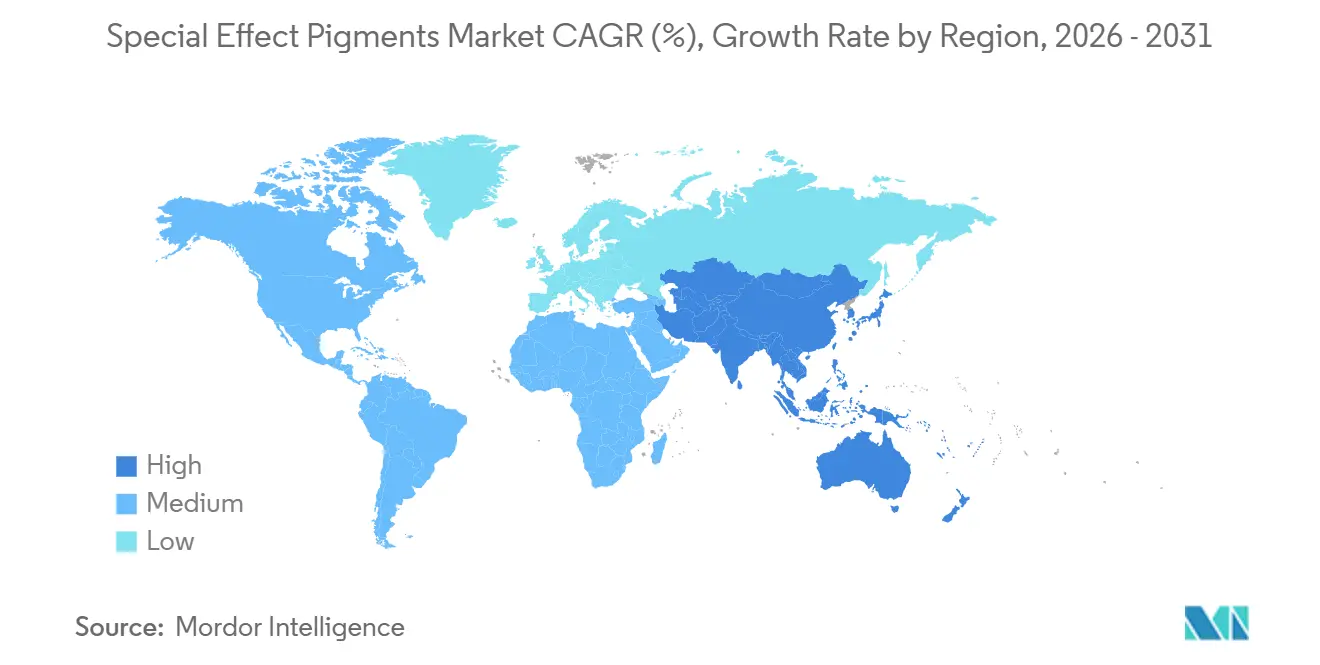

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

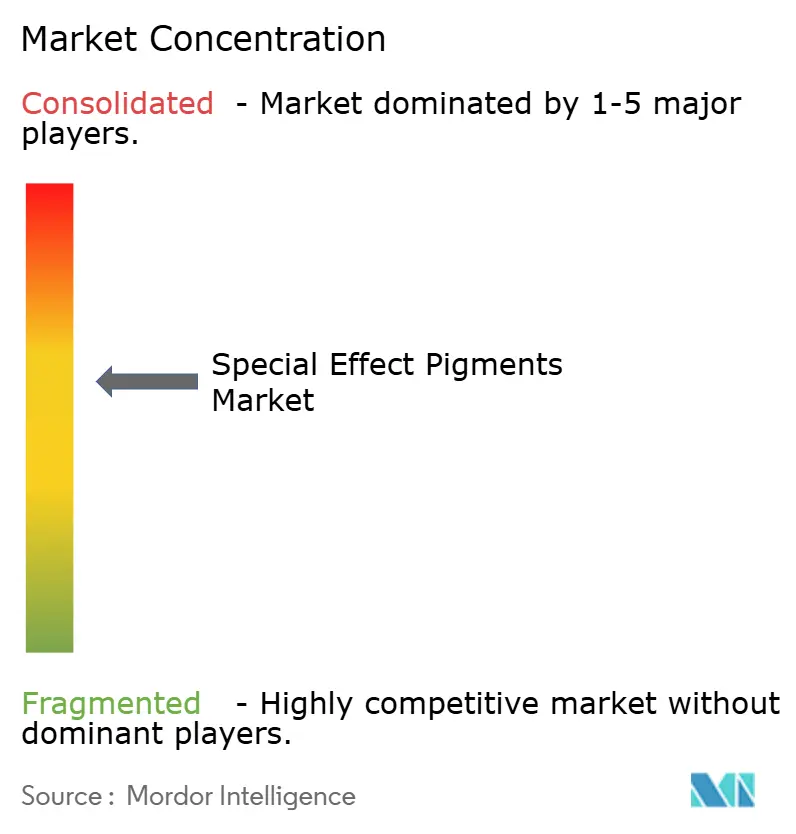

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Special Effect Pigments Market Analysis by ���ϲ�����

The Special Effect Pigments Market size was valued at USD 0.8 billion in 2025 and is estimated to grow from USD 0.83 billion in 2026 to reach USD 1.02 billion by 2031, at a CAGR of 4.11% during the forecast period (2026-2031). Increasing demand for multi-dimensional finishes in beauty products, the reformulation of automotive coatings to meet radar-compatibility requirements, and the expanded use of optically variable pigments (OVPs) in anti-counterfeit packaging are influencing competitive dynamics. In the cosmetics industry, formulators are transitioning to lab-grown synthetic mica to mitigate supply chain risks. Automotive original equipment manufacturers (OEMs) are optimizing metallic-flake geometries to prevent 77 GHz radar scattering in advanced driver-assistance systems. In North America and the European Union, coatings manufacturers are shifting from solvent-borne to waterborne and powder systems. While this transition increases dispersion-technology costs, it provides regulatory advantages by addressing volatile organic compound (VOC) limits. Additionally, packaging converters are adopting OVPs as the growth of cross-border e-commerce heightens the risk of counterfeit losses, driving investments in high-security visual features.

Key Report Takeaways

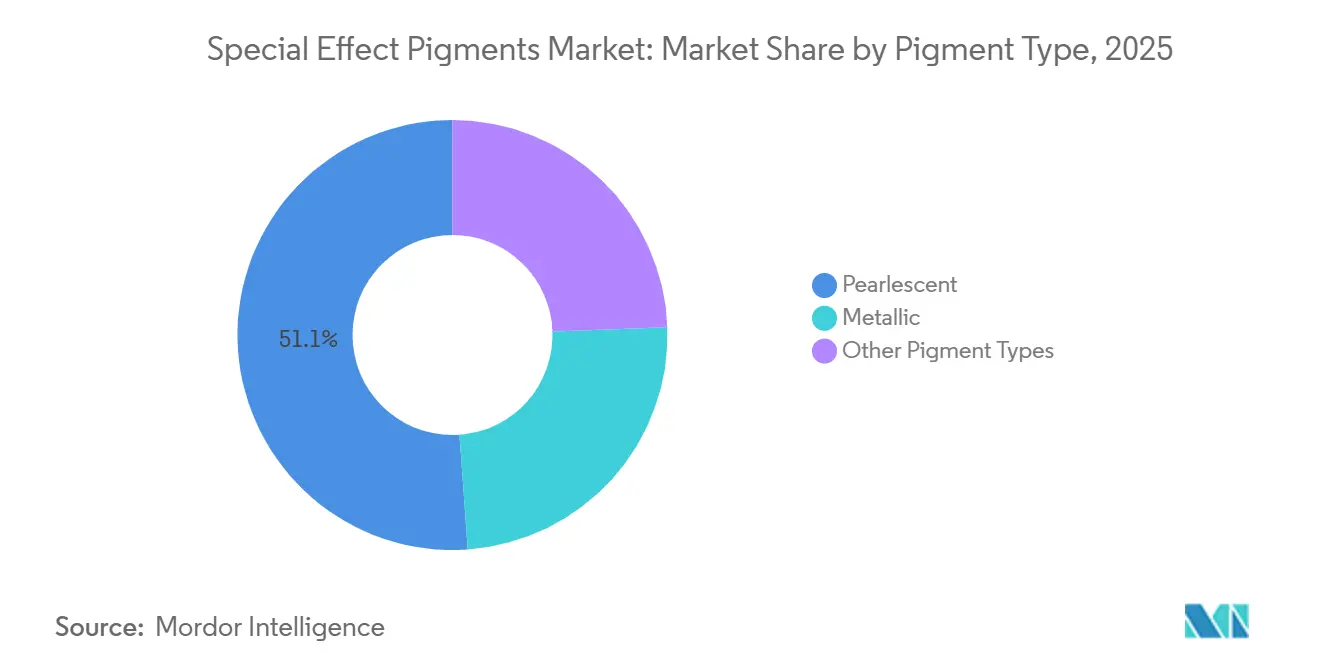

- By pigment type, pearlescent held 51.13% of the special effect pigments market share in 2025 and is projected to expand at a 4.16% CAGR to 2031.

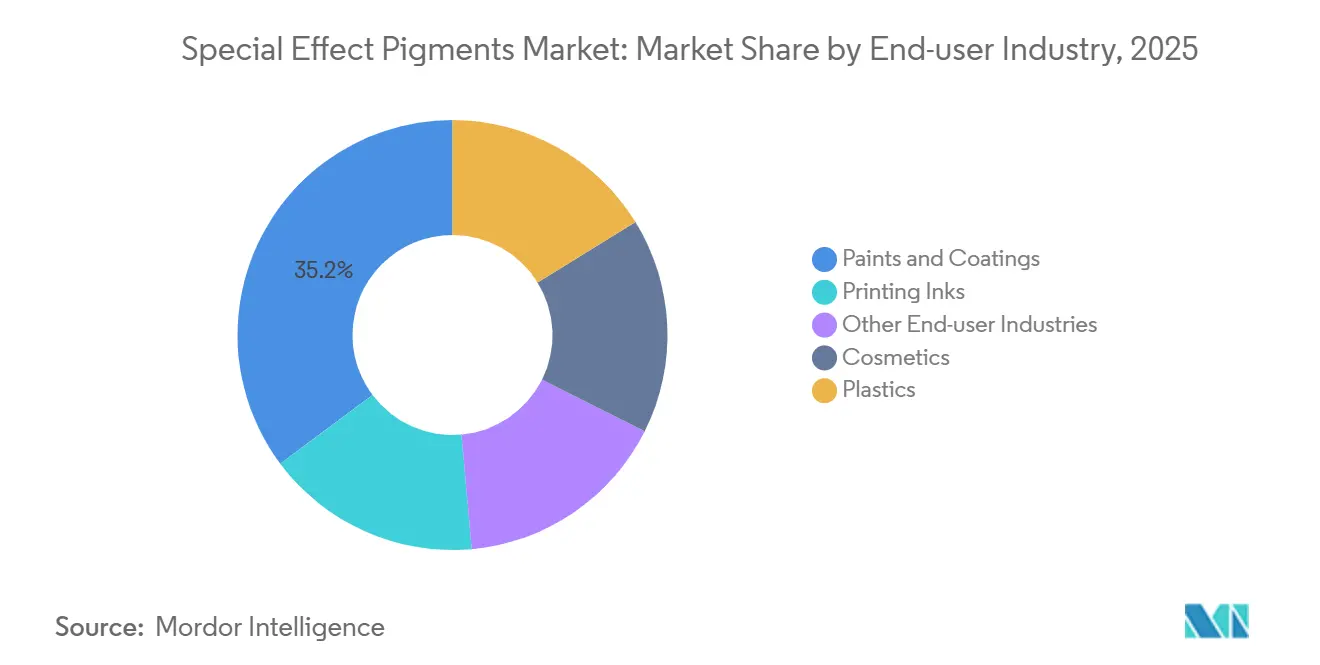

- By end-user industry, paints and coatings retained the largest 35.22% of the special effect pigments market share in 2025, while cosmetics is forecast to advance at a 5.24% CAGR to 2031.

- By geography, Asia-Pacific accounted for 45.18% of the special effect pigments market share in 2025 and is poised to grow at a 4.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Special Effect Pigments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid uptake of visual-effect cosmetics and personal-care products | +1.2% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Sustainability shift to waterborne and powder coatings | +0.9% | North America and EU, spillover to APAC | Long term (≥4 years) |

| Growth of additive-manufacturing powders needing effect pigments | +0.5% | North America and EU, early adoption in China | Long term (≥4 years) |

| Anti-counterfeit packaging adoption of optically-variable pigments | +0.7% | Global, concentrated in North America and EU | Short term (≤2 years) |

| Bio-based synthetic-mica enabling clean-beauty compliance | +0.6% | Global, strongest in EU and North America | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rapid Uptake of Visual-Effect Cosmetics and Personal-Care Products

The premiumization of color cosmetics is driving demand for products such as holographic highlighters, duo-chrome eyeshadows, and pearl-infused foundations that create the "glass-skin" aesthetic popular among Gen Z consumers. In 2024, South Korea exported USD 7.6 billion in cosmetics, with interference and pearlescent pigments accounting for a significant portion of formulation costs in high-margin SKUs aimed at Southeast Asian and North American e-commerce markets. Clean-beauty initiatives are accelerating the adoption of synthetic fluorphlogopite, addressing traceability concerns associated with mica sourced from informal mining operations in India. The European Union's stricter heavy-metal limits for colorants under Cosmetics Regulation (EC) No 1223/2009 further support this transition to purer substrates[1]European Commission, “Cosmetics Regulation (EC) 1223/2009 Update,” ec.europa.eu. Multi-layer interference stacks based on synthetic mica allow formulators to achieve color-travel effects while maintaining natural-origin claims, enabling price premiums of 20-30%. Additionally, social-media-driven product launch cycles have shortened to weeks, requiring suppliers to ensure just-in-time deliveries of micronized grades with consistent sparkle intensity across batches.

Sustainability Shift to Waterborne and Powder Coatings

Regulations in North America and the European Union limiting VOCs to 65 g/L and 420 g/L, respectively, are driving coatings manufacturers to transition to waterborne and powder systems. In 2024, PPG allocated USD 150 million to re-engineer basecoat production lines for aluminum and pearlescent pigments, incorporating modified rheology packages to prevent flocculation. AkzoNobel's Autowave Optima, introduced in 2024, uses encapsulated metallic flakes that remain stable in aqueous media, addressing long-standing issues with brightness loss. Evonik's polyester flow additives, set to launch in 2025, enable pearlescent dispersion at temperatures below 180 °C, reducing energy consumption by 12% compared to conventional hybrid systems. China's 14th Five-Year Plan, which aims for a 30% reduction in VOC emissions by 2025, is expected to accelerate the adoption of low-solvent chemistries in the country's automotive coatings industry.

Growth of Additive-Manufacturing Powders Needing Effect Pigments

3D-printed interior trims for electric vehicles are increasingly using nylon-12 blended with 2-5% pearlescent or metallic pigments, eliminating the need for downstream painting and reducing cycle times by 30%. BASF's Ultrasint PA11 ESD, launched in 2024, combines conductive carbon and metallic flakes to provide electrostatic discharge safety along with a brushed-metal appearance. Binder-jetting of stainless steel now incorporates bronze pigments in the binder to create vintage patina effects, a technique scaled by GE Additive for aerospace tooling applications. Suppliers are miniaturizing flakes to a D50 of less than 50 µm to ensure compatibility with laser-sintering nozzles while maintaining interference color. Early adopters in consumer electronics are leveraging multicolor gradient builds to personalize device housings without requiring additional tooling.

Anti-Counterfeit Packaging Adoption of Optically-Variable Pigments

The OECD estimates the global counterfeit trade at USD 464 billion annually, prompting brands to integrate optically-variable pigment (OVP) stripes into cartons and labels. VIAVI Solutions provides green-to-purple flakes printable via gravure, offering a quick visual authenticity check that cannot be replicated by scanners. The European Union's Falsified Medicines Directive has driven the inclusion of OVPs on pharmaceutical packaging since 2024, while spirits producers like Diageo are piloting OVP neck labels for premium whiskies sold in duty-free markets. Saudi Arabia's regulatory proposal for mandatory track-and-trace systems for cosmetics by 2025 is expected to drive OVP adoption across the GCC region by 2027. The rise of direct-to-consumer e-commerce further highlights the need for overt security features that also serve as marketing tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile aluminum and TiO₂ cost base | -0.8% | Global, acute in North America and EU | Short term (≤2 years) |

| Ethical-mica supply disruptions | -0.4% | Global, concentrated in Asia-Pacific supply | Medium term (2-4 years) |

| ADAS sensor interference from high-flake pigments | -0.3% | North America and EU automotive markets | Short term (≤2 years) |

| Source: ���ϲ����� | |||

Volatile Aluminum and TiO₂ Cost Base

London Metal Exchange aluminum prices rose from USD 2,182.5 per ton in March 2024 to USD 2,789.5 per ton by October 2025, as European smelters reduced capacity. Metallic pigment producers implemented list-price increases of 8-12%, yet still faced a decline of 200-300 basis points in gross margins. Titanium dioxide (TiO₂) price fluctuations added to the challenges. Chemours halted operations at its Altamira facility, while Tronox closed its Kwinana smelter, removing 90,000 tons of chloride-grade feedstock from the market. In China, spot prices for chloride-process TiO₂ were at CNY 19,200 per ton in Q4 2024 before dropping to CNY 17,800 per ton in Q2 2025, complicating inventory valuation for pigment blenders. Mid-tier coatings manufacturers postponed purchases or reformulated products with lower metallic-flake content when price increases were not feasible.

Ethical-Mica Supply Disruptions

In 2024, only 38% of mica from Jharkhand and Bihar was traceable to certified mines, according to the Responsible Mica Initiative. Monsoon floods in Q2 2025 caused shipment delays of up to six weeks, leading to a 15-20% rise in spot mica prices. Merck invested EUR 1 million in community programs to stabilize supply; however, synthetic alternatives continue to gain market share. The European Union’s upcoming Corporate Sustainability Due Diligence Directive, expected in 2027, will require large enterprises to audit human rights risks, potentially increasing compliance costs for companies that continue to use natural mica.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pigment Type: Pearlescent Dominance Anchors Premium Positioning

Pearlescent pigments represented 51.13% of 2025 revenue, emphasizing their importance in premium color cosmetics and high-chroma automotive finishes. This segment is anticipated to grow at a 4.16% CAGR through 2031, maintaining its leadership in the special effect pigments market even as metallic and OVP (optically variable pigment) niches expand. Multi-layer stacks of synthetic fluorphlogopite coated with titanium dioxide and iron oxides continue to be in high demand due to their ability to achieve ultra-low impurity levels, meeting the EU's stricter heavy-metal regulations. Products like Merck’s Ronastar and Eckart’s Syncrystal lines support clean-beauty claims and are widely used by brands such as L’Oréal, Estée Lauder, and indie companies targeting Gen Z consumers.

Aluminum-based metallic pigments remain significant in industrial powder and automotive OEM coatings, though their growth is limited by radar-interference challenges. ECKART’s Radar Transparent technology helps address this issue, allowing OEMs to retain sparkle effects without compromising 77 GHz radar performance, which is critical for ADAS-equipped vehicles. Smaller niches, such as OVPs primarily supplied by VIAVI Solutions, are expected to grow faster than core categories, albeit from a smaller base, driven by their use in anti-counterfeit packaging for pharmaceuticals and high-end spirits. These trends collectively support diversified demand, ensuring the special effect pigments market remains resilient against downturns in specific applications.

By End-user Industry: Cosmetics Velocity Outpaces Coatings Scale

Paints and coatings accounted for the largest share of 2025 revenue at 35.22%, driven by volumes in automotive OEM and industrial maintenance finishes. However, the cosmetics segment is projected to grow at a 5.24% CAGR through 2031, making it the fastest-growing end-user industry. This positions beauty brands to achieve significant gains in the special effect pigments market over the next five years. South Korea’s USD 7.6 billion cosmetics export market strongly favors pearlescent-rich products aimed at Gen Z consumers on social commerce platforms.

The coatings segment is expected to grow more slowly due to the higher costs of dispersion technologies for waterborne and powder systems, which are less accessible to mid-tier formulators dominating regional markets. For instance, PPG’s USD 150 million investment in converting U.S. and Italian plants highlights the capital-intensive requirements for maintaining brightness and flop in low-VOC platforms. Meanwhile, plastics and 3D-printing applications offer additional growth opportunities. Automotive interior trims made from pearlescent polypropylene or laser-sintered nylon now provide the same visual depth as painted metal while reducing vehicle weight. Printing inks, though a smaller revenue contributor, are expanding as OVPs are increasingly used in serialized labels mandated by the EU Falsified Medicines Directive.

Geography Analysis

Asia-Pacific generated 45.18% of 2025 revenue and is forecast to grow at a CAGR of 4.67% through 2031, maintaining its position as the largest regional contributor to the special effect pigments market. In China, coatings production reached 30.93 million tons in the first half of 2024, supported by the launch of electric vehicles that favor color-shifting basecoats. Government targets for VOC reduction are accelerating the adoption of waterborne formulations, driving demand for modified pearlescent dispersions. In South Korea, the export of K-beauty products, particularly multi-chromatic eye and lip cosmetics, is fueling pigment imports. Meanwhile, India’s Sudarshan Chemical increased its production capacity by 15% in 2024 to strengthen regional supply.

In North America and Europe, California’s 65 g/L VOC limit and the EU Industrial Emissions Directive are encouraging coatings manufacturers to adopt encapsulated flake systems that resist oxidation in waterborne formulations. The EU Cosmetics Regulation 1223/2009, which restricts heavy-metal content, is prompting beauty brands to shift toward synthetic mica with sub-ppm impurity levels, boosting demand for lab-grown substrates. Additionally, upcoming due-diligence legislation will require multinational companies to audit mica sourcing, likely increasing demand for certified synthetic alternatives.

South America and Middle-East and Africa collectively account for the remaining market share. In South America, Brazil’s automotive sector recovery is driving metallic-flake consumption in OEM and refinish applications, while Argentina’s adoption of K-beauty formulations is increasing pearlescent pigment imports. In the Middle-East, luxury cosmetics are expanding, with Saudi Arabia’s proposed track-and-trace regulations encouraging the use of optically variable pigments (OVPs) in packaging[2]Saudi Food and Drug Authority, “Draft Cosmetics Track and Trace Regulation 2025,” sfda.gov.sa . In South Africa, the appliance powder coatings sector is driving demand for pearlescent pigments that remain stable at cure cycles of ≤180°C, supported by Evonik’s flow-additive solutions.

Competitive Landscape

The special effect pigments market is moderately concentrated, with the five largest suppliers, inclduing Merck KGaA, ALTANA’s ECKART, DIC Corporation, The Chemours Company, and Sudarshan Chemical, accounting for approximately 60% of global revenue in 2025. Vertical integration offers cost and traceability advantages; for instance, Merck manufactures synthetic mica substrates in Germany and the United States, ensuring supply chain stability and reducing reliance on artisanal mines in India. ECKART utilizes alloy engineering to produce radar-transparent metallic flakes, which are in demand for OEMs developing Level-2 and higher ADAS vehicles.

Strategic investments in sustainability are shaping the market. DIC Corporation aims to achieve carbon-neutral pigment production by 2030, supported by renewable energy agreements for its Japanese facilities. Sudarshan Chemical expanded its pearlescent pigment capacity by 3,000 tons per year in 2024, targeting cost-sensitive regional brands while adhering to ISO 16128 natural-origin standards. BASF and Shepherd Color are focusing on high-value functional additives, such as electrostatic-discharge powders and infrared-reflective pigments for cool roofs, which command premiums of 30-50% over standard grades.

Patent activity highlights a competitive race to develop ultra-thin glass or nano-aluminum flakes that meet ADAS requirements without compromising sparkle. VIAVI Solutions continues to protect its intellectual property portfolio for optically variable pigments used in anti-counterfeit packaging, a high-margin segment with limited substitutes. Regional competitors in Southeast Asia and Latin America are exploring bio-based substrates derived from rice husk silica and Brazilian muscovite, indicating ongoing market fragmentation despite consolidation among leading players.

Special Effect Pigments Industry Leaders

Merck KGaA

ALTANA (ECKART)

DIC Corporation

The Chemours Company

Sudarshan Chemical Industries Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: UK-based startup Sparxell secured USD 5 million in pre-Series A funding to expand its plant-based structural color technology. The University of Cambridge spin-out utilized cellulose derived from wood pulp to produce biodegradable and non-toxic pigments for applications in fashion, packaging, and beauty.

- August 2025: Sun Chemical unveiled Paliocrom Premium Orange L 2900, which was designed for vibrant metallic effects. The company also introduced Lumina HD Exterior Sienna S3903V, new bronze-to-copper shades in the Lumina HD high-definition mica effects line.

Global Special Effect Pigments Market Report Scope

Special effect pigments are high-performance colorants designed to produce visual effects such as pearlescence, metallic luster, color-shifting, and holography. These effects are achieved by manipulating light through reflection, refraction, and interference. The pigments are composed of multi-layered, thin-film flakes, typically made from materials like mica, aluminum, or silica, and are widely used in automotive coatings, cosmetics, plastics, and inks to enhance visual appeal.

The Special Effect Pigments Market is segmented by pigment type, end-user industry, and geography. By pigment type, the market is segmented into pearlescent, metallic, and other pigment types. By end-user industry, the market is segmented into paints and coatings, cosmetics, plastics, printing inks, and other end-user industries. The report also covers the market size and forecasts for special effect pigments in 27 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Pearlescent |

| Metallic |

| Other Pigment Types |

| Paints and Coatings |

| Cosmetics |

| Plastics |

| Printing Inks |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| NORDIC Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Pigment Type | Pearlescent | |

| Metallic | ||

| Other Pigment Types | ||

| By End-user Industry | Paints and Coatings | |

| Cosmetics | ||

| Plastics | ||

| Printing Inks | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| NORDIC Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the special effect pigments market?

The special effect pigments market stands at USD 0.83 billion in 2026 and is projected to reach USD 1.02 billion by 2031.

Which end-user industry is expected to grow fastest through 2031?

Cosmetics is slated to post a 5.24% CAGR through 2031.

Why are synthetic mica pigments gaining traction?

They remove the ethical-sourcing risks tied to natural mica and meet stricter heavy-metal limits in EU and U.S. cosmetics rules.

How are VOC regulations influencing pigment demand?

VOC caps in North America and the EU accelerate the switch to waterborne and powder coatings that use specialized pearlescent and metallic dispersions.

Page last updated on: