Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

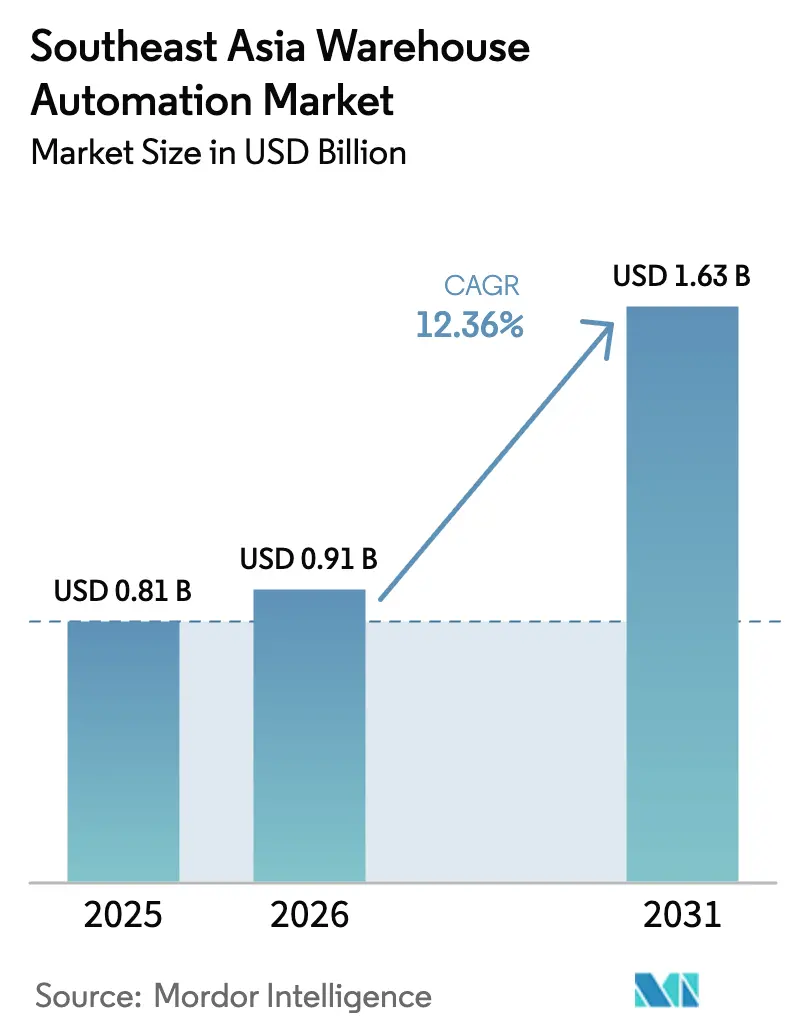

| Base Year Market Size (2025) | USD 0.81 Billion |

| Market Size (2026) | USD 0.91 Billion |

| Market Size (2031) | USD 1.63 Billion |

| Growth Rate (2026 - 2031) | 12.36% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Warehouse Automation Market Analysis by ���ϲ�����

The Southeast Asia Warehouse Automation Market size was valued at USD 0.81 billion in 2025 and is estimated to grow from USD 0.91 billion in 2026 to reach USD 1.63 billion by 2031, at a CAGR of 12.36% during the forecast period (2026-2031). Continuous shifts from labor-cost arbitrage toward platform-scale logistics have reshaped fulfillment economics as super-apps, quick-commerce networks, and RCEP-enabled cross-border trade compress delivery windows and lift throughput requirements beyond manual capacity. Indonesia led with 28.63% 2025 revenue, anchored by government-funded logistics parks along the Cikarang and Jakarta-Surabaya corridor, while Vietnam is forecast to post the fastest 13% CAGR through 2031 on the back of Shopee and SPX Express mega hubs. Singapore’s land scarcity and median warehouse-operative wages above SGD 3,000 (USD 2,250) per month have accelerated autonomous-mobile-robot (AMR) programs subsidized by the Infocomm Media Development Authority, tilting adopters toward space-efficient, energy-saving solutions.

Key Report Takeaways

- By country, Indonesia’s 28.63% 2025 share underscores how archipelagic realities demand island-specific distribution, of the ASEAN warehouse automation market share in 2025, while Vietnam is projected to expand at a 13% CAGR through 2031.

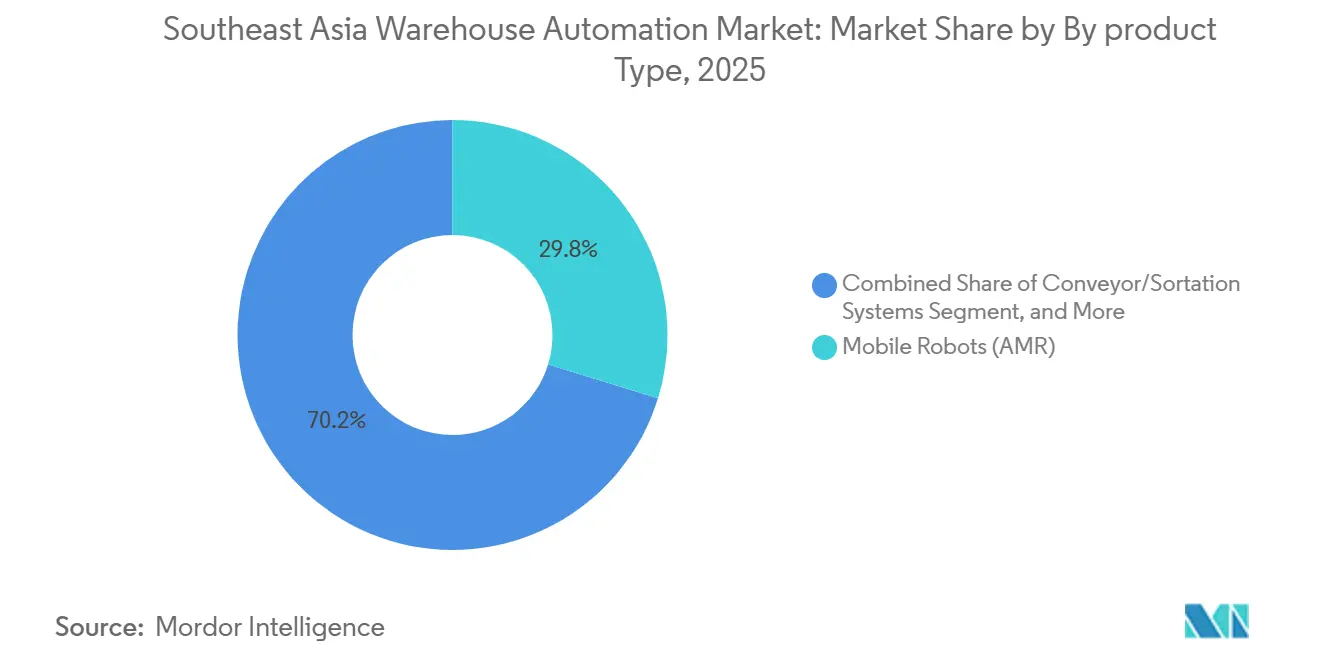

- By product type, mobile robots commanded 29.76% of Southeast Asia warehouse automation market share in 2025 and is on track to expand at a 13.92% CAGR through 2031.

- By end-user industry, retail and e-commerce led with 34.14% revenue share in 2025, while healthcare and pharmaceutical is projected to advance at a 13.81% CAGR through 2031.

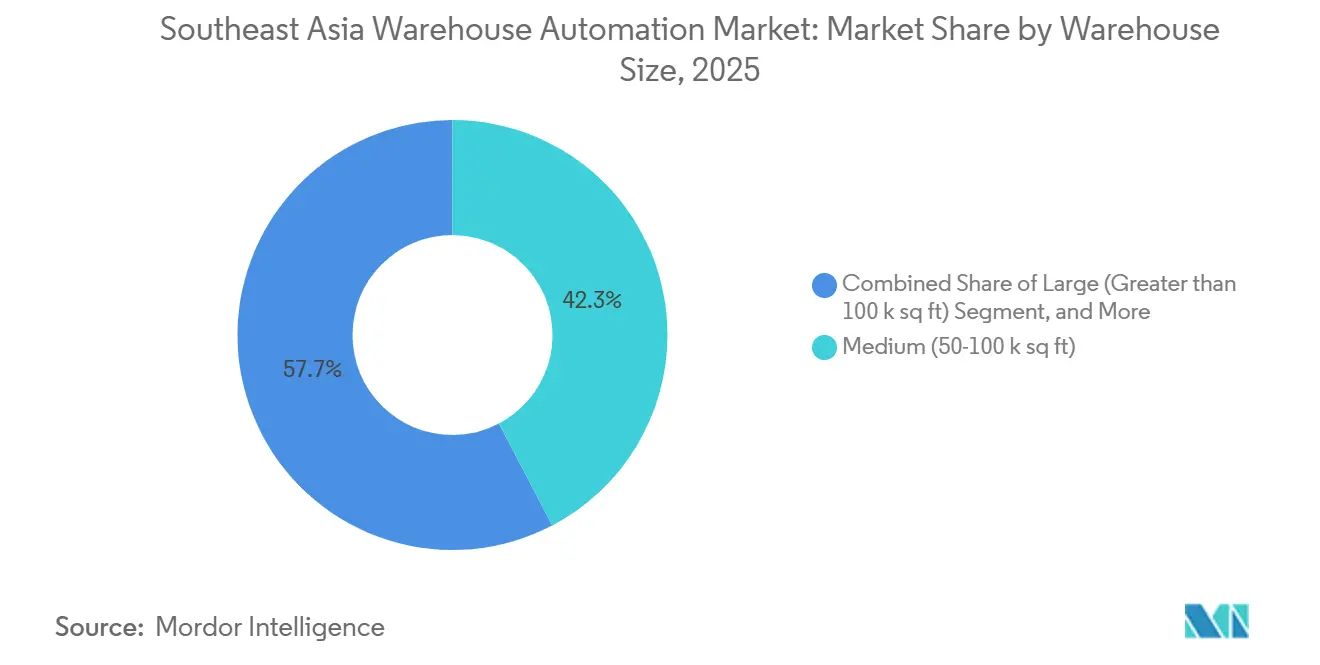

- By warehouse size, medium facilities of 50,000–100,000 ft² captured 42.32% share in 2025, whereas large hubs above 100,000 ft² is forecast to grow at a 12.96% CAGR to 2031.

- By automation level, semi-automated sites held 37.63% share in 2025, yet lights-out operation is expected to post a 12.92% CAGR through 2031.

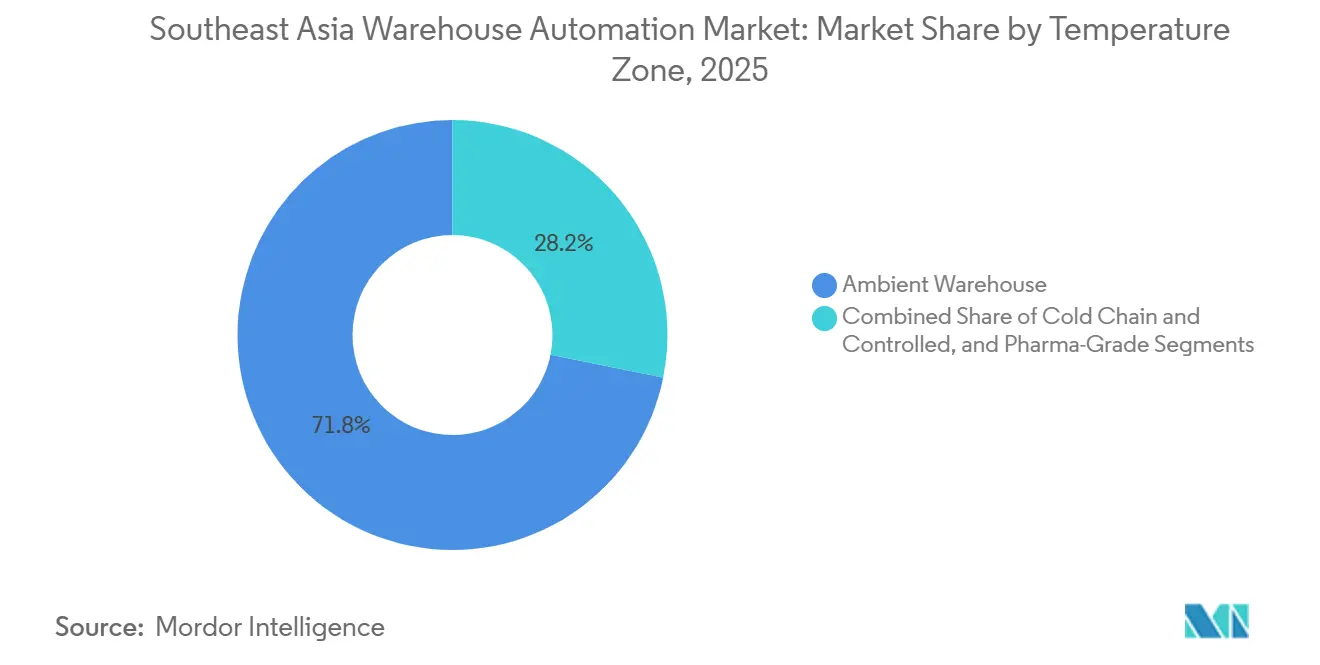

- By temperature zone, ambient warehouses controlled 71.84% share in 2025 and cold-chain facilitie is projected to accelerate at a 13.18% CAGR.

- By ownership type, third-party logistics providers led with 46.51% share in 2025, whereas e-commerce platform logistics arm is anticipated to register a 12.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia Warehouse Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-Funded Logistics Parks in Indonesia and Vietnam Compress Pay-Back for AS/RS | +2.1% | Indonesia (Cikarang, Jakarta-Surabaya corridor), Vietnam (Yen My, Ho Chi Minh City) | Medium term (2-4 years) |

| Land Scarcity and Rising Labor Costs in Singapore Fuel Mobile-Robot Adoption | +1.8% | Singapore, with spill-over to Johor Bahru (Malaysia) | Short term (≤ 2 years) |

| Surge of Dark-Store and Quick-Commerce Models Across Jakarta and Bangkok | +1.6% | Indonesia (Jakarta, Surabaya), Thailand (Bangkok, Chiang Mai) | Short term (≤ 2 years) |

| RCEP-Led Intra-ASEAN E-Commerce Volumes Elevating Throughput Needs | +2.3% | ASEAN-wide, with concentration in Indonesia, Thailand, Vietnam, Malaysia | Long term (≥ 4 years) |

| Temperature-Controlled Pharma Distribution, e.g., mRNA Vaccines, Driving AIDC Uptake | +1.4% | Singapore, Thailand, Vietnam, Philippines | Medium term (2-4 years) |

| Same-Day Delivery Expectation via Super-Apps Boosts High-Speed Sortation | +1.7% | Indonesia, Thailand, Singapore, Malaysia | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Government-Funded Logistics Parks Compress Payback for AS/RS

State-led projects such as Indonesia’s Cikarang Dry Port and Vietnam’s Yen My industrial zone bundle tax holidays, duty waivers, and pre-certified grid capacity that reduce retrofit engineering costs by 20–30%.[1]SPX Express, “Yen My Hub Factsheet,” spx.com Provincial mandates that earmark land parcels above 10 ha for distribution centers favor high-density automated storage over piecemeal mechanization. As subsidy windows close by 2028, operators fast-track investment decisions, compressing payback periods from five years to under three. Automotive parts distributors and 3PLs are first movers, citing reduced real-estate cost per pallet and lower handling error rates. The same model is being copied in Thailand’s Eastern Economic Corridor, suggesting spill-over adoption across ASEAN.

Land Scarcity and Rising Labor Costs Push Mobile-Robot Adoption

Singapore dedicates only 7.5% of its 728 km² land mass to logistics, which raised industrial rents above SGD 2.50 ft² per month in 2025.[2]JTC Corporation, “Industrial Land Supply,” jtc.gov.sg Wage inflation, now exceeding SGD 3,000 (USD 2,250) for floor staff, erodes manual-handling margins. IMDA co-funds up to 50% of AMR fleet-orchestration software, shrinking capex hurdles for small enterprises. Operators report 30–40% space savings by replacing fixed conveyors with dynamic robot paths. Green-building incentives award energy-efficient automation, further tipping the scale toward AMRs. The learning curve benefits Malaysia’s Johor Bahru cross-border warehousing cluster, which imports Singapore-developed best practices.

Dark-Store and Quick-Commerce Surge Lifts Micro-Fulfillment Demand

Foodpanda and TikTok Shop grew dark-store footprints across Jakarta and Bangkok, promising 15–30 minute delivery windows that require order-picking rates above 100 items-per-hour per picker.[3]Foodpanda, “Q-Commerce Expansion,” foodpanda.com AMR-based goods-to-person systems meet throughput in 2,000–5,000 ft² footprints located within 3–5 km of consumer clusters. Bangkok congestion, averaging 60 minutes travel per 10 km, makes hyperlocal inventory non-negotiable, pushing landlords to spec mezzanine levels for grid-based robotics. Island fragmentation in Indonesia drives separate dark-store rings per major island, lowering cross-dock reliance. Breakeven densities stay tight; store failures in Singapore during 2024 underline that sustained demand, not technology, determines ROI.

RCEP-Driven Intra-ASEAN Parcel Growth Boosts High-Speed Sortation

Tariff elimination on 90% of goods under RCEP has lifted cross-border parcel flows by 25% YoY during 2024-2025. Shopee and Lazada pools inventory in Thailand and Malaysia to reach Singapore and Indonesia next day. Manual sorting cannot keep error rates below 2% when multi-country labeling and customs forms converge, so operators migrate to crossbelt and tilt-tray technology. The Singapore-Chongqing land-sea corridor demonstrated 30% dwell-time reduction once digital visibility linked automated hubs. Forward-looking 3PLs now size hub footprints for five-year parcel-volume doubles to avoid mid-cycle reengineering.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Power and Building Codes Challenge Retro-Fit Automation | -1.2% | Indonesia, Philippines, Vietnam (tier-2 provinces) | Medium term (2-4 years) |

| Shortage of Certified Mechatronics Technicians Across Tier-2 Provinces | -0.9% | Indonesia (outside Java), Philippines (outside Metro Manila), Vietnam (Mekong Delta) | Long term (≥ 4 years) |

| Customs, Inter-Island Regulations Dilute ROI for Fully Automated DCs | -0.7% | Indonesia (inter-island), Philippines (inter-island) | Medium term (2-4 years) |

| Legacy Narrow-Aisle Facilities Limit AGV Deployment | -0.6% | Singapore, Malaysia (Klang Valley), Thailand (Bangkok) | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Fragmented Power and Building Codes Complicate Retrofits

Voltage variance from 220 V single phase in legacy Philippine warehouses to 415 V three phase in purpose-built Thai sites forces integrators to overspec uninterruptible power supplies by 30–50%, inflating project capex by up to USD 100,000 per 50,000 ft² facility. Floor-load ratings, fire codes, and seismic bracing differ across ASEAN jurisdictions, prolonging design cycles beyond 12 months for multi-country rollouts. Brownouts in Mindanao provinces average 4-6 hours weekly, compelling operators to add generators that raise carbon footprints and threaten Green Mark certifications. The extra cost skews ROI in favor of modular mobile solutions that tolerate power cuts and lower floor loads.

Shortage of Certified Mechatronics Technicians in Tier-2 Provinces

Only 15% of vocational graduates in Thailand possess automated handling skills, yet demand is rising 25% annually. Java-outside provinces in Indonesia and Mekong Delta sites in Vietnam import technicians from automotive OEMs, raising labor costs 20–30%. Commissioning timelines stretch to 8–12 months versus 4–6 months in capital regions. Integrators now bundle remote-monitoring service contracts, but latency hampers immediate error resolution. Talent shortages therefore bias operators toward semi-automated systems that need fewer PLC specialists, slowing lights-out penetration outside tier-1 metros.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mobile Robots Sustain Outperformance

The Southeast Asia warehouse automation market size for mobile robots accounted for USD 0.24 billion in 2025, translating into 29.76% Southeast Asia warehouse automation market share. Retrofitting narrow-aisle structures with conveyor loops can exceed USD 200 ft² due to floor reinforcement, whereas deploying AMRs costs USD 30,000–50,000 per unit, which explains the 13.92% forecast CAGR toward 2031. AutoStore grids demonstrated fourfold storage density gains without altering building envelopes at DHL’s APAC Innovation Center, lowering real estate costs per SKU. In contrast, AS/RS adoption concentrates in automotive and pharma cold chains, where payload weight or temperature control mandates rigid automation. Conveyor lines still dominate mega hubs, but energy consumption and land requirements curb use in retrofit mid-market facilities.

Software layers, particularly WMS and AIDC, act as technology force multipliers. CP AXTRA used Cainiao iWMS to increase order processing from 15,000 to 100,000 orders daily without new hardware, proving that orchestration can extend asset lifecycles. Crossbelt innovations like Dematic Silky cut power draw 30% and fit high-throughput demands within land-constrained sites. Consequently, AMR fleets, modular grids, and energy-efficient sorters will keep widening their collective share in the Southeast Asia warehouse automation market through 2031.

By End-User Industry: Healthcare Cold Chain Takes the Lead

Retail and e-commerce platforms generated USD 0.28 billion in 2025 revenue, the largest slice, reflecting Shopee, Lazada, and TikTok Shop fulfillment expansion. Yet the healthcare vertical is projected to expand its share of the Southeast Asia warehouse automation market at a 13.81% CAGR through 2031, driven by strict GDP compliance and biologics uptake. UPS Healthcare’s -80 °C freezer farms in Singapore deliver sub-0.1 °C temperature variance, and Zuellig Pharma’s multi-country cold-chain network drives RFID adoption, lifting inventory accuracy above 95%.

Logistics 3PLs leverage robot rental models from Locus Robotics to maintain utilization above 80% across client pools. Automotive OEMs are automating battery storage for 400-kg EV modules, focusing on reinforced AS/RS systems. Diverse use cases underscore why technology stacks differ across end users, but regulation and product-safety demands keep healthcare in pole position for growth.

By Warehouse Size: Mega Hubs Scale, Medium Sites Stay Core

Medium facilities (50,000–100,000 ft²) retained 42.32% share in 2025, confirming their role as the backbone of the Southeast Asia warehouse automation market. Their balanced scale enables seasonal flexibility, while payback on semi-automated pick-to-light systems remains under three years. Large hubs above 100,000 ft², such as Lazada’s 150,000 m² Lat Krabang sortation center, are expected to grow at a 12.96% CAGR to 2031 as e-commerce giants seek regional consolidation economies.

Capital outlays exceeding USD 50 million are justified once throughput exceeds 5 million parcels per day, in line with RCEP-driven cross-border flows. Small warehouses under 50,000 ft² adopt modular systems like Pingspace Matrix, securing ROI under two years by targeting micro-fulfillment near urban demand.

By Automation Level: Semi-Automated Today, Lights-Out Tomorrow

Semi-automated layouts commanded 37.63% share in 2025, marrying affordable capex with 30–50% productivity gains. Lights-out facilities are slated to grow at a 12.92% CAGR, driven by tier-2 labor shortages that push ROI below 2 years for fully automated grids in Penang and the Klang Valley.

Hybrid “highly automated” designs blend robotic storage with manual picking for exceptions, letting operators step-up automation without overexposing to talent gaps. Downgrades sometimes occur when exception volumes exceed system tolerances, suggesting that organizational process maturity, not technology, governs the feasible depth of automation.

By Temperature Zone: Cold Chain Outpaces Ambient

Ambient warehouses captured 71.84% of 2025 revenue, yet cold-chain segments are poised for 13.18% CAGR through 2031. UPS Healthcare’s Singapore freezer farms and Zuellig Pharma’s GDP-approved regional network exemplify the compliance-driven surge.

Cold-chain automation carries 20–30% pricing premia due to insulation and defrost engineering, but biologics penetration projected at 30% of ASEAN pharma sales by 2030 widens the addressable base. Food-and-beverage players prefer semi-automated solutions because of product variety, while pharmaceutical firms lean into full automation for strict chain-of-custody. Regulatory mandates therefore hard-wire growth momentum into cold-chain automation spending.

By Ownership Type: 3PLs Lead, Platforms Integrate

Third-party logistics firms held a 46.51% share in 2025, capitalizing on multi-client asset-sharing and robot-leasing models that improve return on invested capital. Shopee’s 100,000 m² Vietnam facility, Lazada’s Lat Krabang hub, and TikTok Shop nodes embody the 12.86% CAGR forecast for platform-owned infrastructure as marketplaces internalize logistics to circumvent 3PL margins. 3PLs respond by bundling technology integration, evidenced by YCH Group’s SSI Schaefer AS/RS in Singapore, blurring lines between space provider and integrator.

Platform logistics arms typically channel close to 70% of their own marketplace parcels through captive facilities, boosting slotting accuracy by 15% and reducing last-mile misroutes to below 1%, a benchmark that multi-client 3PLs rarely match. In response, leading 3PLs deploy subscription AMR fleets from Locus Robotics across several customer accounts, driving fleet utilization above 80% and expanding the segment’s Southeast Asia warehouse automation market size without tying capital to single-tenant buildings. Singapore’s IMDA open-protocol mandate accelerates this shift by allowing mixed-vendor robot fleets, enabling operators in Johor Bahru and Batam to integrate Hai Robotics units alongside legacy systems within months rather than years. As hardware prices fall and wage pressures intensify, both ownership models are converging on higher automation intensity, keeping their combined Southeast Asia warehouse automation market share near 90% through 2031 even as absolute spending expands at a double-digit pace.

Geography Analysis

Indonesia’s 28.63% 2025 share underscores how archipelagic realities demand island-specific distribution, supported by Cikarang Dry Port’s 50,000 TEU capacity and corridor upgrades that trimmed transit times 15–20%. The rapid densification of quick-commerce in Jakarta is generating micro-fulfillment demand, driving AMR adoption. Vietnam’s 13% CAGR projection arises from FDI-led infrastructure, such as Shopee’s 100,000 m² fulfillment center and SPX Express’s 170,000 m² Yen My hub, which bypasses incremental mechanization. Thailand rides on automotive-sector clustering and Eastern Economic Corridor tax holidays that underwrite AS/RS for EV battery storage.

Singapore’s land scarcity and high wages spur AMR fleets and vertical storage; Green-Mark energy credits reinforce the shift toward low-power robotics. Semiconductor supply-chain hubs in Penang adopt clean-room-compatible AS/RS, while Klang Valley e-commerce sites favor cost-efficient pick-to-light systems. S P Setia’s RM 4 billion (USD 900 million) smart-warehouse campus signals institutional capital inflows that could accelerate nationwide automation. The Philippines lags due to inter-island customs delays and brownouts, and automation is concentrated in Metro Manila, where grid reliability and technician pools are stronger.

Across the region, adoption speed correlates more with infrastructure readiness and labor dynamics than with e-commerce penetration or technology availability, ensuring heterogeneous growth trajectories within the Southeast Asia warehouse automation market.

Competitive Landscape

The market remains moderately fragmented as modular, software-defined solutions lower entry barriers. Global integrators Daifuku, Dematic (KION Group), SSI Schaefer, Swisslog, and Vanderlande secure mega-hub contracts like Dematic Silky at Lazada Thailand, while robotics natives such as Geek+, GreyOrange, Locus Robotics, and Hai Robotics court mid-market warehouses with subscription AMR fleets. Regional challengers, including Pingspace and Gen Surv Robotics, focus on micro-fulfillment niches and underprice multinationals by 30-40% with turnkey packages.

Platform logistics arms intensify rivalry. Shopee and Lazada build proprietary fulfillment to capture end-to-end economics, eroding 3PL wallet share and compelling incumbents to co-innovate. Singapore’s IMDA mandates open-protocol VDA 5050 compatibility, pressuring vendors to interoperate, which, in turn, reshapes switching costs. Patent portfolios in grid storage and navigation remain differentiators; AutoStore’s 400-plus patents shield premium pricing though litigation risk with Ocado remains a wild card. No ASEAN state enforces local-content quotas, yet energy-efficiency incentives tilt awards toward vendors with regenerative drives.

White-space persists in tier-2 provinces and cold-chain networks where standards such as HACCP and ISO 22000 tighten compliance. Integrators that offer rapid-deployment kits and remote monitoring can penetrate these underserved zones, but technician scarcity and power-grid fragility still hamper scale.

Southeast Asia Warehouse Automation Industry Leaders

Daifuku Co., Ltd.

Swisslog (KUKA)

SSI Schaefer

Vanderlande Industries

Dematic Corp. (KION Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Chin Hin Group Berhad and PTT Synergy unveiled a joint venture to build smart warehouses across Klang Valley and Penang, integrating automated storage and sortation aimed at e-commerce and 3PL clients.

- November 2025: CP AXTRA ramped order capacity from 15,000 to 100,000 daily via Cainiao iWMS, slashing mis-sorts below 0.5% and proving software-layer gains without heavy hardware outlay.

- August 2025: S P Setia partnered with ALP Taiwan to develop a 42-acre smart-warehouse campus in Klang with USD 900 million gross development value, embedding AS/RS and cold-chain zones.

- July 2025: NCS Group launched the SGD 130 million (USD 97 million) Sunshine.AI program with HTX, NVIDIA, and AWS to infuse predictive analytics into warehouse robotics.

Southeast Asia Warehouse Automation Market Report Scope

Warehouse automation is the automation of the movement of inventory into, within, and out of warehouses for delivery to customers. As part of an automation project, a business can eliminate labor-intensive tasks that require repetitive physical labor, manual data entry, and analysis. With warehouse automation, users' facilities can better meet customer demand. The initial step is automating manual processes, such as data collection and inventory control, using a warehouse management system (WMS). These systems integrate with other solutions to efficiently manage and automate tasks across various business and supply chain functions.

The Southeast Asia Warehouse Automation Market Report is Segmented by Product Type (Conveyor/Sortation Systems, AS/RS, Mobile Robots, WMS, AIDC), End-User Industry (Retail and E-Commerce, Logistics and Transportation, Automotive, General Manufacturing, Healthcare and Pharmaceutical, Food and Beverage/FMCG), Warehouse Size (Small, Medium, Large), Automation Level (Low, Semi-Automated, Highly Automated, Fully Automated), Temperature Zone (Ambient, Cold Chain, Controlled), Ownership Type (3PL, In-House Shippers, E-Commerce Platform Logistics), and Country (Malaysia, Thailand, Singapore, Indonesia, Vietnam, Philippines). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Conveyor/Sortation Systems |

| Automated Storage and Retrieval Systems (AS/RS) |

| Mobile Robots (AMR/AGV) |

| Warehouse Management Systems (WMS) |

| Automatic Identification and Data Capture (AIDC) |

By End-User Industry

| Retail and E-Commerce |

| Logistics and Transportation |

| Automotive |

| General Manufacturing |

| Healthcare and Pharmaceutical |

| Food and Beverage, FMCG |

By Warehouse Size

| Small (Less Than 50,000 sq ft) |

| Medium (50,000–100,000 sq ft) |

| Large (Greater Than 100,000 sq ft) |

By Automation Level

| Low, Basic Mechanization |

| Semi-Automated |

| Highly Automated |

| Fully Automated, Lights-Out |

By Temperature Zone

| Ambient |

| Cold Chain |

| Controlled, Pharma-Grade |

By Ownership Type

| Third-Party Logistics (3PL) |

| In-House Shippers |

| E-Commerce Platform Logistics |

By Country

| Malaysia |

| Thailand |

| Singapore |

| Indonesia |

| Vietnam |

| Philippines |

| By Product Type | Conveyor/Sortation Systems |

| Automated Storage and Retrieval Systems (AS/RS) | |

| Mobile Robots (AMR/AGV) | |

| Warehouse Management Systems (WMS) | |

| Automatic Identification and Data Capture (AIDC) | |

| By End-User Industry | Retail and E-Commerce |

| Logistics and Transportation | |

| Automotive | |

| General Manufacturing | |

| Healthcare and Pharmaceutical | |

| Food and Beverage, FMCG | |

| By Warehouse Size | Small (Less Than 50,000 sq ft) |

| Medium (50,000–100,000 sq ft) | |

| Large (Greater Than 100,000 sq ft) | |

| By Automation Level | Low, Basic Mechanization |

| Semi-Automated | |

| Highly Automated | |

| Fully Automated, Lights-Out | |

| By Temperature Zone | Ambient |

| Cold Chain | |

| Controlled, Pharma-Grade | |

| By Ownership Type | Third-Party Logistics (3PL) |

| In-House Shippers | |

| E-Commerce Platform Logistics | |

| By Country | Malaysia |

| Thailand | |

| Singapore | |

| Indonesia | |

| Vietnam | |

| Philippines |

Key Questions Answered in the Report

What CAGR is forecast for Southeast Asia warehouse automation through 2031?

The market is projected to grow at 12.36% between 2026 and 2031, reaching USD 1.63 billion by the end of the period.

Which product category is expanding the fastest?

Mobile robots are forecast to advance at a 13.92% CAGR, benefiting from retrofit flexibility and declining unit costs.

Why is the healthcare sector accelerating automation investment?

Strict GDP temperature-control mandates and biologics penetration push cold-chain automation, driving a 13.81% CAGR for healthcare facilities.

How do government logistics parks influence ROI?

Parks in Indonesia and Vietnam bundle tax breaks and ready infrastructure, trimming high-density AS/RS payback from five years to under three.

What is the biggest operational restraint in tier-2 provinces?

A shortage of certified mechatronics technicians extends commissioning lead times and inflates service costs, curbing full-automation uptake.

Which countries offer the strongest growth outlook?

Vietnam leads with a 13% CAGR through 2031, followed by Indonesia and Thailand that benefit from super-app logistics and automotive clustering.

Page last updated on: