Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

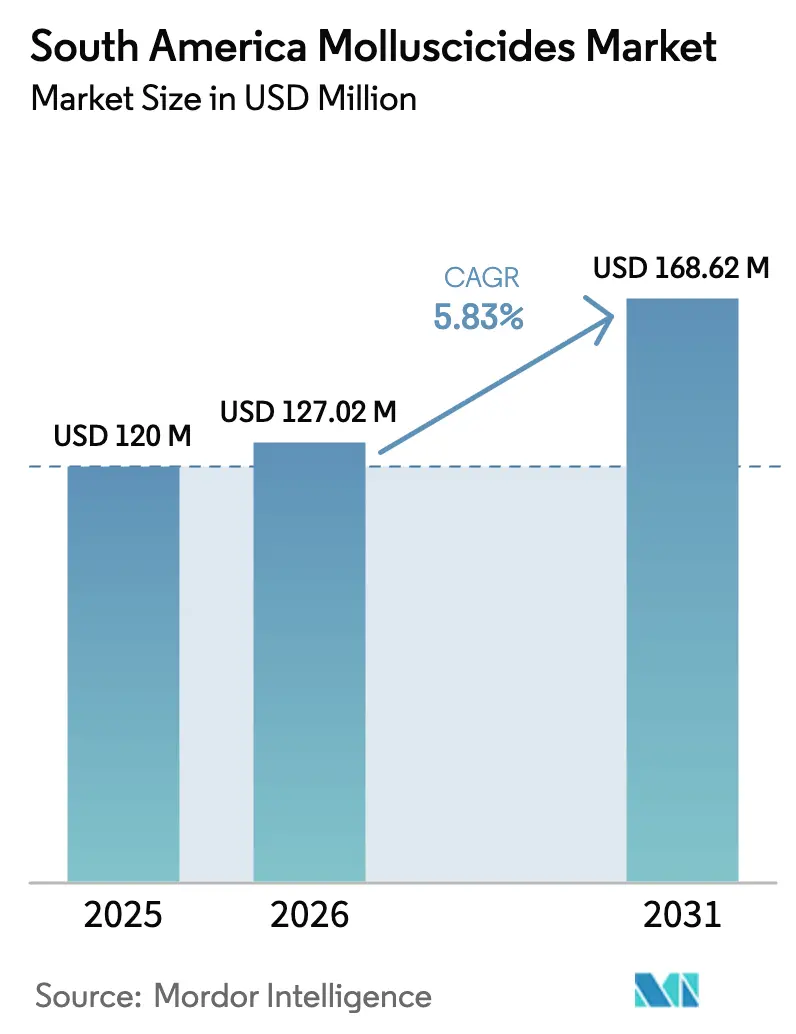

| Base Year Market Size (2025) | USD 419.10 Million |

| Market Size (2026) | USD 443.70 Million |

| Market Size (2031) | USD 598.5 Million |

| Growth Rate (2026 - 2031) | 6.17% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

South America Molluscicides Market Analysis by ���ϲ�����

The South America molluscicides market size is projected to expand from USD 419.10 million in 2025 and USD 443.70 million in 2026 to USD 598.50 million by 2031, registering a 6.17% CAGR between 2026 and 2031. Sustained humidity spikes during El Niño cycles, the spread of protected cultivation, and tightening export-market residue rules elevate baseline slug and snail pressure across soybean, coffee, sugarcane, and high-value horticulture. Regulatory scrutiny of metaldehyde accelerates the shift toward iron-phosphate, while counterfeit flows and price gaps temper smallholder adoption. Manufacturers are reformulating into moisture-stable granules and exploring repellent modes of action that protect non-target species. Competition is moderate with the top five suppliers holding significant revenue, yet they face margin pressure as regional formulators undercut prices with parallel imports.

Key Report Takeaways

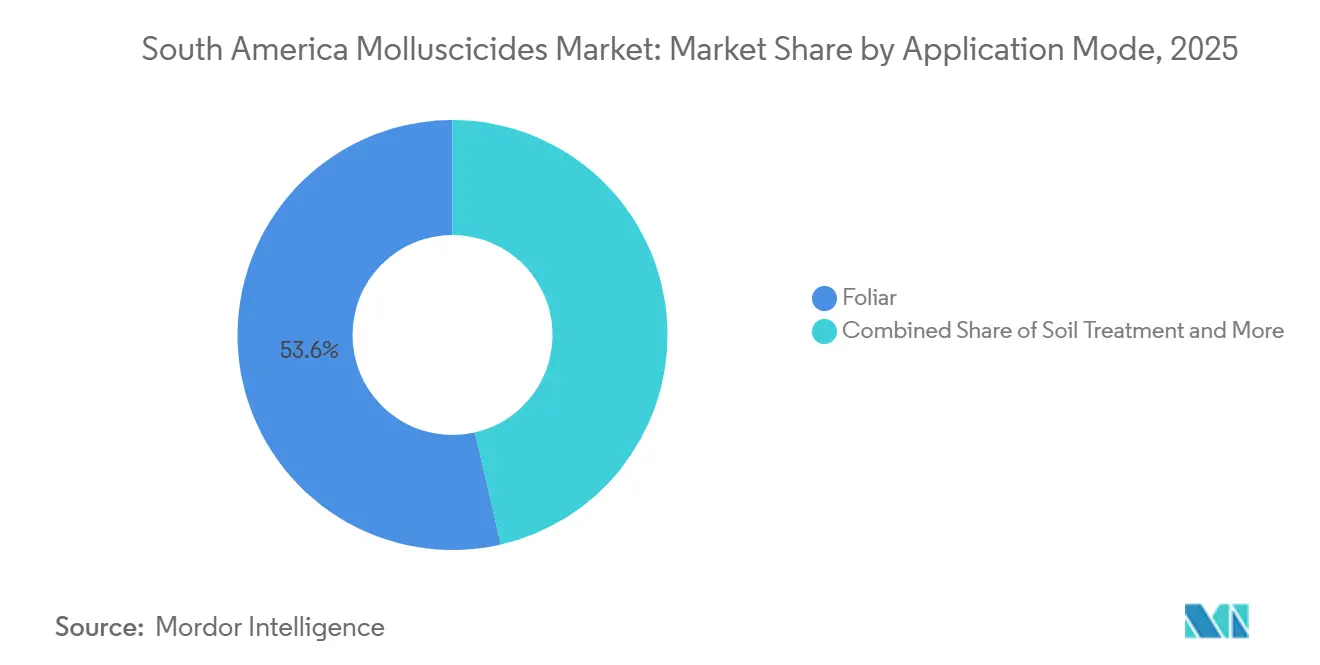

- By application mode, foliar commanded 53.6% of the South America molluscicides market size in 2025 and is growing fastest at a 6.3% CAGR from 2026 to 2031.

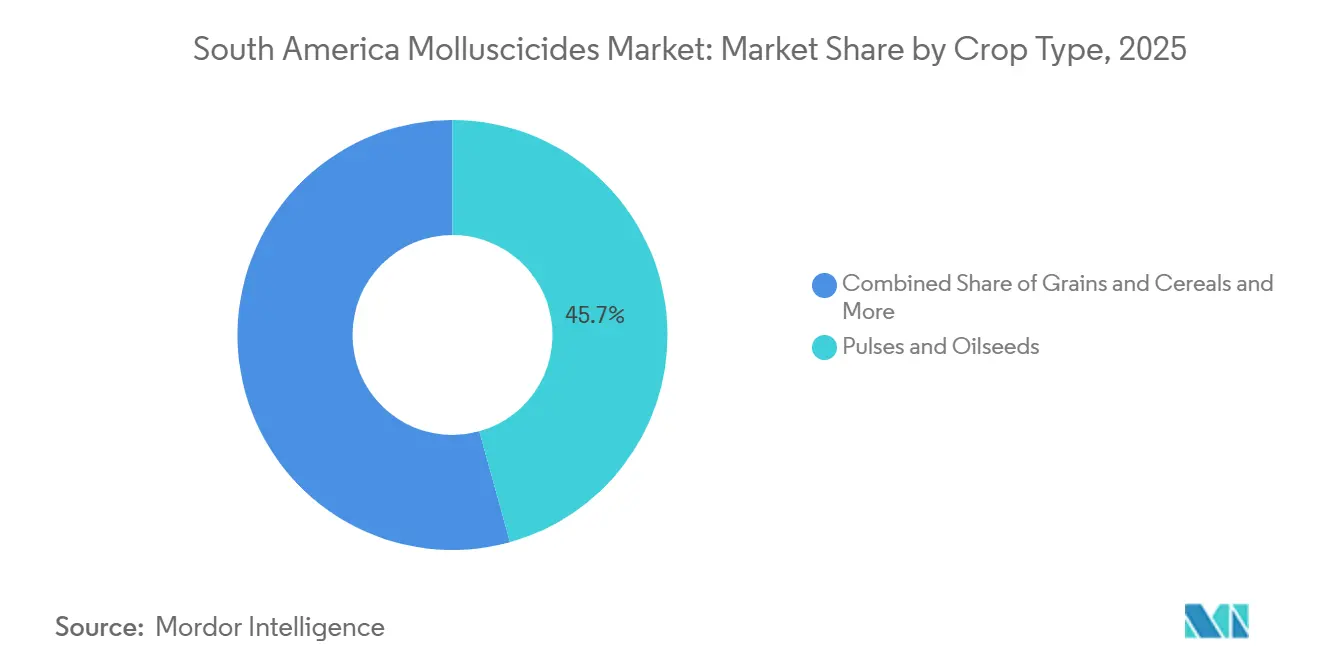

- By crop type, pulses and oilseeds held the largest share of 45.7% of 2025 market revenue, whereas commercial crops are projected to expand at a 6.9% CAGR from 2026 to 2031.

- By geography, Brazil contributed 48.2% of the South America molluscicides market share in 2025 and is the fastest-growing country, projected to grow at a CAGR of 8.6% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Molluscicides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating slug and snail outbreaks during humid El Niño cycles | +1.2% | Brazil, Argentina, Colombia, Peru (high), Chile, and Rest of South America | Short term (≤ 2 years) |

| Government incentives for sustainable coffee, sugarcane, and horticulture | +0.9% | Brazil, Colombia (high), Peru, and Rest of South America | Medium term (2-4 years) |

| European metaldehyde ban freeing iron-phosphate capacity for Brazil | +0.7% | Brazil (high), Argentina, and Chile | Short term (≤ 2 years) |

| Shift to protected cultivation escalating mollusk pressure | +1.1% | Brazil, Argentina, Colombia, Peru, Chile, and Rest of South America | Medium term (2-4 years) |

| Biotech seed coatings increasing survivability of juvenile snails | +0.5% | Brazil, Argentina (high), and Paraguay border | Long term (≥ 4 years) |

| Blockchain-enabled produce traceability penalizing blemished exports | +0.8% | Brazil, Chile, Peru (high), Argentina, and Colombia | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Escalating Slug and Snail Outbreaks During Humid El Niño Cycles

El Niño Southern Oscillation events raise soil moisture, extend feeding periods, and push gastropod populations beyond historic thresholds. Field trials by Empresa Brasileira de Pesquisa Agropecuária documented higher mollusk incidence in Paraná, Santa Catarina, and Rio Grande do Sul. No-till residue amplifies the effect by adding shelter and organic matter, so growers deploy preemptive bait applications that lift baseline demand for molluscicides. Brazilian Cerrado farms now schedule two additional pellet applications per season to protect early-maturing horticulture crops. Similar trends surface in Colombia’s Andean valleys, where persistent dew films allow slugs to feed overnight even during traditionally dry months. Continued climate volatility keeps this driver top of mind for agronomists and distributors.

Government Incentives for Sustainable Coffee, Sugarcane, and Horticulture

Brazil’s Plano Safra and ABC Plus programs subsidize molluscicide costs when growers switch to lower-toxicity baits that satisfy organic and export residue codes. Colombia’s National Federation of Coffee Growers offers parallel rebates that have already moved one-third of registered hectares to iron-phosphate. It grants reimbursement up to 30% of molluscicide costs if GPS-guided spreaders are used, spurring adoption of variable-rate pellets. Argentina widened its sustainable-farming tax code in 2025 to credit molluscicide resistance-management plans, indirectly lifting demand for dual-mode baits. These financial carrots shift purchasing decisions away from lowest-cost options toward safer formulations that pass residue audits. Peru channels similar support through cooperatives targeting European buyers that demand pesticide transparency. The initiatives also favor integrated pest management packages that bundle molluscicides with biostimulants, raising cross-selling potential for suppliers.

Shift to Protected Cultivation Escalating Mollusk Pressure

Greenhouse and high-tunnel acreage in Colombia exceeded 10,000-15,000 hectares by 2025 and continues to expand in Chile and Peru. These enclosed systems retain humidity and warmth, enabling slugs to reproduce two to three times faster compared to open fields. In response, crop managers have increased bait application frequency and adopted premium formulations designed to withstand irrigation splash. Government co-financing programs supporting the construction of plastic houses are anticipated to drive further expansion through 2029, boosting molluscicide usage. Formulators are also developing rain-fast granules tailored to these microclimates, contributing to technological advancements in the market.

Biotech Seed Coatings Increasing Survivability of Juvenile Snails

Seed coatings designed to retain moisture and improve seed vigor have unintentionally created favorable microhabitats for juvenile gastropods. Laboratory tests on soybean plots showed an increase in juvenile snail populations when coated seeds were used, compared to uncoated controls. This higher early-season survival rate necessitates earlier and, in some cases, multiple baiting applications within the same growing cycle. As the adoption of next-generation coatings progresses gradually, the long-term impact is anticipated to influence growth rates. Currently, formulators have not integrated repellent chemistries with seed coatings, highlighting an existing innovation gap in the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening residue limits on metaldehyde in South America | −0.8% | Brazil, Argentina, Chile, Colombia, and Peru | Short term (≤ 2 years) |

| High premium price of iron-phosphate active ingredient | −1.1% | Brazil, Argentina, Colombia, and Peru | Medium term (2-4 years) |

| Rising mollusk resistance to single-mode chemistries | −0.6% | Brazil, Argentina, Chile, and Colombia | Long term (≥ 4 years) |

| Informal cross-border trade in counterfeit inputs | −0.9% | Brazil, Paraguay, Argentina, Peru, and Colombia | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Tightening Residue Limits on Metaldehyde in South America

In 2025, Brazil’s National Health Surveillance Agency (ANVISA) aligned maximum-residue limits (MRLs) with European standards, requiring growers to reduce field application rates or shift to ferric phosphate for export-oriented produce. ANVISA introduced significant updates to pesticide and disinfectant residue regulations, including revised MRLs, pre-harvest intervals, and authorized uses, through Normative Instruction No. 371, published on June 5, 2025. In Argentina, the National Service of Agri-Food Health and Quality (SENASA) implemented buffer zones and timing restrictions, complicating the use of metaldehyde during rainy seasons. Compliance audits often coincide with peak harvest periods, increasing economic risks as residue violations can lead to shipment suspensions. Immediate compliance necessitates the withdrawal of non-conforming stock by distributors, leaving growers to choose between higher crop damage risks or increased costs associated with switching to ferric phosphate. Distributors have reported a 15% decline in metaldehyde volumes in regions where coffee and berries are predominant. Consequently, regulatory changes are slowing the adoption of legacy chemistries despite their cost advantages.

High Premium Price of Iron-Phosphate Active Ingredient

Iron-phosphate pellets are two to three times more expensive per kilogram of active ingredient compared to metaldehyde, largely because ferric production is less scalable and fewer suppliers compete. Price sensitivity is particularly significant in maize and wheat production, where molluscicide expenses compete with fungicide and fertilizer budgets. Currency fluctuations further exacerbate the cost difference; ferric-phosphate imports priced in euros become more expensive when local currencies weaken, leading farmers to delay adopting these products. In regions such as Brazil’s Northeast and Argentina’s Northwest, where profit margins are narrow, farmers continue to opt for the less expensive metaldehyde despite concerns over residue. Local manufacturing capacity remains limited, even with recent investments, resulting in slow realization of scale economies. Consequently, price ceilings restrict widespread adoption of iron-phosphate pellets outside of high-value horticultural markets.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Mode: Foliar Dominates Large-Scale Systems

Foliar treatments accounted for 53.6% of the South America molluscicides market size in 2025 because tractor spreaders can cover wide soybean and corn fields quickly. The segment is further projected to register the fastest growth, with a CAGR of 6.3% from 2026 to 2031. Growers favor banded rows when iron-phosphate prices bite, cutting active use by up to half while retaining efficacy. Aquatic snail control in irrigation canals remains limited yet strategic for regions fighting schistosomiasis, coordinated by health ministries rather than farm co-ops. Industrial premises and residential gardens combine for a low-volume retail sub-market served by 500-gram consumer packs.

South American agronomic advisers recommend two to three broadcast passes during peak slug hatch, synchronized with rain forecasts. Precision application technologies, including variable-rate satellite maps, are emerging but still expensive for most row-crop operators. The South America molluscicides market share for broadcast methods is unlikely to fall soon because equipment fleets are already optimized for pellet and granule distribution. Nevertheless, greenhouse users apply liquids via drip lines to reduce floor residue and keep worker re-entry intervals short.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Crop Type: Commercial Crops Accelerate on Subsidy Support

Pulses and oilseeds accounted for 45.7% of the South America molluscicides market size in 2025, driven by Brazil and Argentina’s position as the world’s second and third largest soybean exporters. However, subsidized integrated pest management budgets enable coffee, sugarcane, and horticulture gains, increasing market volume. Horticultural tunnels in Chile and Colombia generate premium-grade berries and vegetables that must arrive blemish-free in North America and Europe, reinforcing prophylactic use. Grains and cereals gain moderate traction as no-till expands but remain second-tier in value.

Subsidy coverage lowers net iron-phosphate cost by up to one-quarter, nudging growers to adopt it despite premium list prices. Export penalties on visible damage create a clear economic argument: one rejected berry pallet costs more than a season’s molluscicide outlay. The South America molluscicides market size for commercial crops is forecast to be the fastest mover at a 6.9% CAGR from 2026 to 2031, if subsidy envelopes are renewed. Ornamentals, largely Colombia’s cut flowers, form a small but price-elastic segment that chooses higher specification baits for visual consistency.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Brazil held a 48.2% revenue share in 2025 and is anticipated to achieve the fastest growth, with an 8.6% CAGR from 2026-2031, driven by extensive soybean cultivation in key regions. Yield improvements have been observed with the use of iron-phosphate bait instead of metaldehyde in no-till soybean farming[1]Source: Servicio Agrícola y Ganadero, “Resolution 243 Exenta,” SAG Chile, sag.gob.cl. Regulatory measures to reduce residues have encouraged distributors to stock higher-quality products, expanding the two-tier price structure. The launch of new products tailored to these conditions has further strengthened Brazil’s market position.

Argentina ranks second in market expenditure, with growth supported by regulatory streamlining that reduces product launch timelines. This has attracted more foreign brands, increasing competition and potentially lowering prices. Wetter planting windows linked to climate variability are expected to increase the frequency of bait applications in soybean-wheat rotations, although usage remains lower than in Brazil.

Chile and Colombia represent the next tier of the market, driven by export-focused horticulture under protected cultivation. In Chile, new regulations mandating bee-safety measures and certified applicator standards are encouraging the adoption of iron-phosphate-based solutions. In Colombia, greenhouse cultivation at high altitudes, where cool nighttime temperatures promote condensation and slug activity, is driving demand for bait applications. Smaller markets like Bolivia emphasize low-toxicity formulations to comply with community water-quality regulations, increasing demand for ferric-phosphate products. While distribution networks remain fragmented, digital-commerce platforms improve product accessibility in rural areas.

Competitive Landscape

The South America molluscicides market is moderately concentrated, with the top five suppliers dominating a significant portion of the market. Bayer AG leads the market with its Ferramol portfolio, followed by BASF SE, which has expanded its reach by integrating biological solutions with its chemical bait lines[2]Source: Valor International, “BASF Acquires Biological Insecticide Firm With an Eye to Brazil,” valorinternational.globo.com. Syngenta Group, De Sangosse, and Lonza complete the top players, focusing on portfolio diversification to address tightening regional residue regulations.

Distribution channels in the region remain fragmented. Numerous rural resellers repackage bulk active ingredients and sell unregistered brands at lower prices. To address challenges posed by this parallel economy, branded players are adopting track-and-trace labeling and farmer education initiatives[3]Source: INTERPOL, “Operation Crete II,” interpol.int. Suppliers are also promoting stewardship campaigns to prevent misuse and counterfeiting, which could accelerate resistance and compromise the long-term efficacy of active ingredient classes.

Innovation efforts in the market are centered on formulation science. De Sangosse has developed technology to enhance field longevity during tropical downpours, while Bayer is testing coatings that remain intact under heavy rainfall. Research institutions are exploring plant-derived repellents for integration with seed coatings. Success in these projects could shift the competitive landscape toward companies capable of quickly registering novel modes of action.

South America Molluscicides Industry Leaders

Bayer AG

BASF SE

De Sangosse Ltd.

Lonza Group AG

Adama Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: French multinational De Sangosse has launched IRONMAX PRO molluscicide in Brazil. The product contains Ferric Phosphate IP Max and incorporates the company's proprietary Colzactive technology.

- May 2025: UPL’s exclusive partnership with Elemental Enzymes in Brazil, starting in 2026, boosts its bioprotection portfolio for corn and soybean. This expansion strengthens UPL’s nationwide distribution network, potentially driving wider market access for all agri-inputs, including molluscicides.

- February 2025: UPL Ltd. invested USD 53.85 million to raise its stake in Brazil’s Sinova to nearly 50%. The move strengthens its distribution reach in South America’s largest crop-protection market, improving last-mile access for molluscicides. Expanded channel control supports faster in-season supply, aligning with demand surges in slug and snail management.

South America Molluscicides Market Report Scope

Molluscicides are pesticides that control mollusks, primarily snails and slugs. These species cause significant agricultural losses and pose a major threat to crops. They damage crops both above and below ground by feeding on seeds, seedlings, shoots, roots, leaves, and flowers, which reduces plant density and crop yields.

The South America molluscicides market is categorized by crop type into grains and cereals, pulses and oilseeds, fruits and vegetables, commercial crops, and turf and ornamental crops. Based on application mode, the market is divided into foliar, soil treatment, chemigation, and fumigation. Geographically, the analysis covers Brazil, Argentina, Chile, and the Rest of South America, with market forecasts presented in value terms (USD).

By Application Mode

| Foliar |

| Soil Treatment |

| Chemigation |

| Fumigation |

By Crop Type

| Grains and Cereals |

| Pulses and Oilseeds |

| Fruits and Vegetables |

| Commercial Crops |

| Turf and Ornamental |

By Geography

| Brazil |

| Argentina |

| Chile |

| Rest of South America |

| By Application Mode | Foliar |

| Soil Treatment | |

| Chemigation | |

| Fumigation | |

| By Crop Type | Grains and Cereals |

| Pulses and Oilseeds | |

| Fruits and Vegetables | |

| Commercial Crops | |

| Turf and Ornamental | |

| By Geography | Brazil |

| Argentina | |

| Chile | |

| Rest of South America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected market size of the South America chemical molluscicides market in 2026, and how is it expected to grow by 2031?

The South America chemical molluscicides market is projected to reach USD 443.70 million in 2026 and is expected to grow to USD 598.50 million by 2031, registering a CAGR of 6.17% during the forecast period (2026–2031).

Why is Brazil the dominant consumer of molluscicides?

Large no-till soybean acreage, stricter residue enforcement by Agência Nacional de Vigilância Sanitária, and subsidized integrated pest programs combine to lift Brazilian demand above all neighbors.

What formulations perform best in high-rainfall regions?

Hydrophobic granules outperform traditional pellets because they remain intact after heavy showers, reducing reapplication frequency.

Which mode of action helps manage rising resistance?

Repellent chemistries that deter feeding without lethality grow fastest and serve as rotation partners for contact and ingestive baits, extending overall product efficacy.