Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.45 Billion |

| Market Size (2031) | USD 4.69 Billion |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

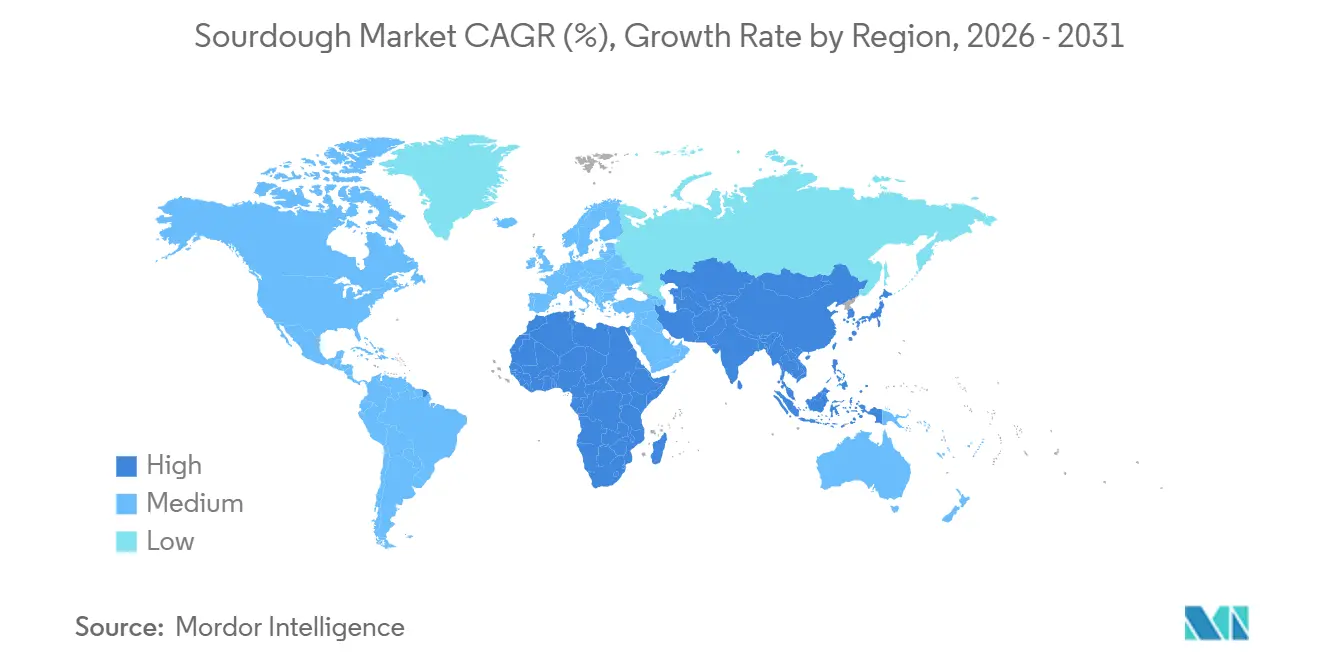

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

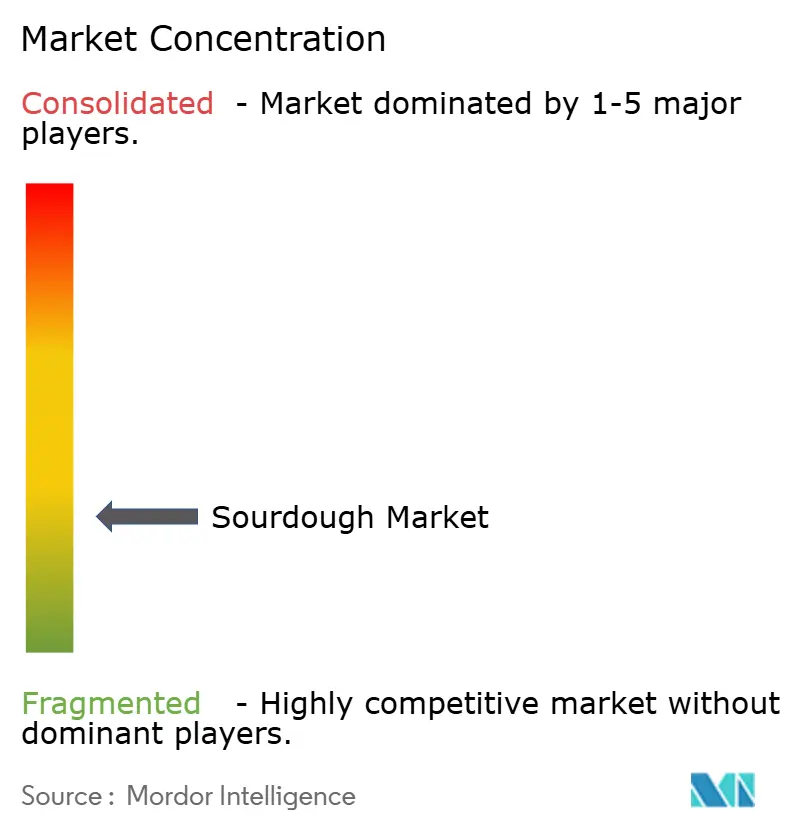

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Sourdough Market Analysis by ���ϲ�����

The sourdough market size is expected to increase from USD 3.24 billion in 2025 to USD 3.45 billion in 2026 and reach USD 4.69 billion by 2031, growing at a CAGR of 6.33% over 2026-2031. The growth is driven by the rising demand for naturally fermented bread, which is perceived as healthier and more flavorful. Supportive food-safety regulations in North America and the European Union further contribute to this trend. Industrial bakeries are expanding their offerings with ready-to-bake sourdough products, while artisan producers focus on traditional methods such as long fermentation and heritage grains to justify higher prices. Technological advancements in spray- and freeze-drying processes are improving the shelf life of sourdough starters, making it easier to distribute them across borders and reducing the risk of spoilage. Meanwhile, rapid urbanization in the Asia-Pacific region is driving the adoption of Western-style bakery products, making it the fastest-growing market for sourdough globally. The market remains highly fragmented.

Key Report Takeaways

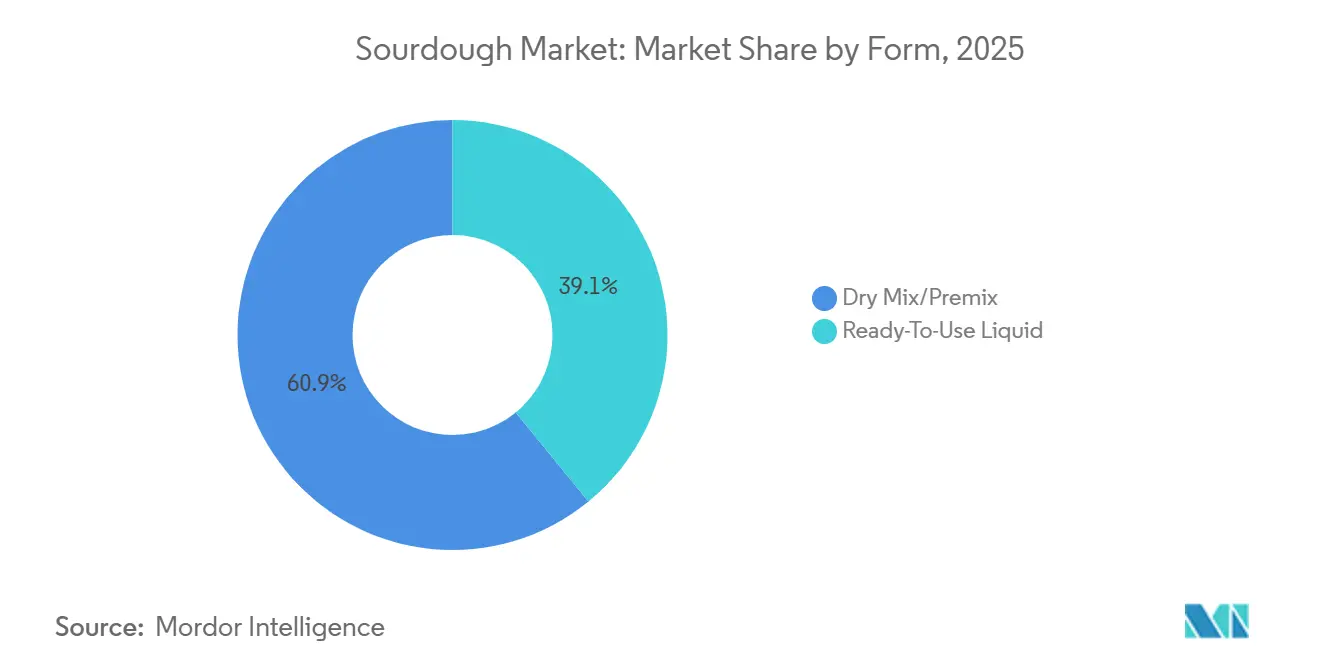

- By form, dry mix/premix captured 60.89% of the sourdough market share in 2025, whereas ready-to-use liquid formats are projected to grow at a 7.21% CAGR through 2031.

- By processing type, type III powder held the largest revenue share at 43.10% in 2025, while type II dried sourdough is forecast to expand at a 7.55% CAGR to 2031.

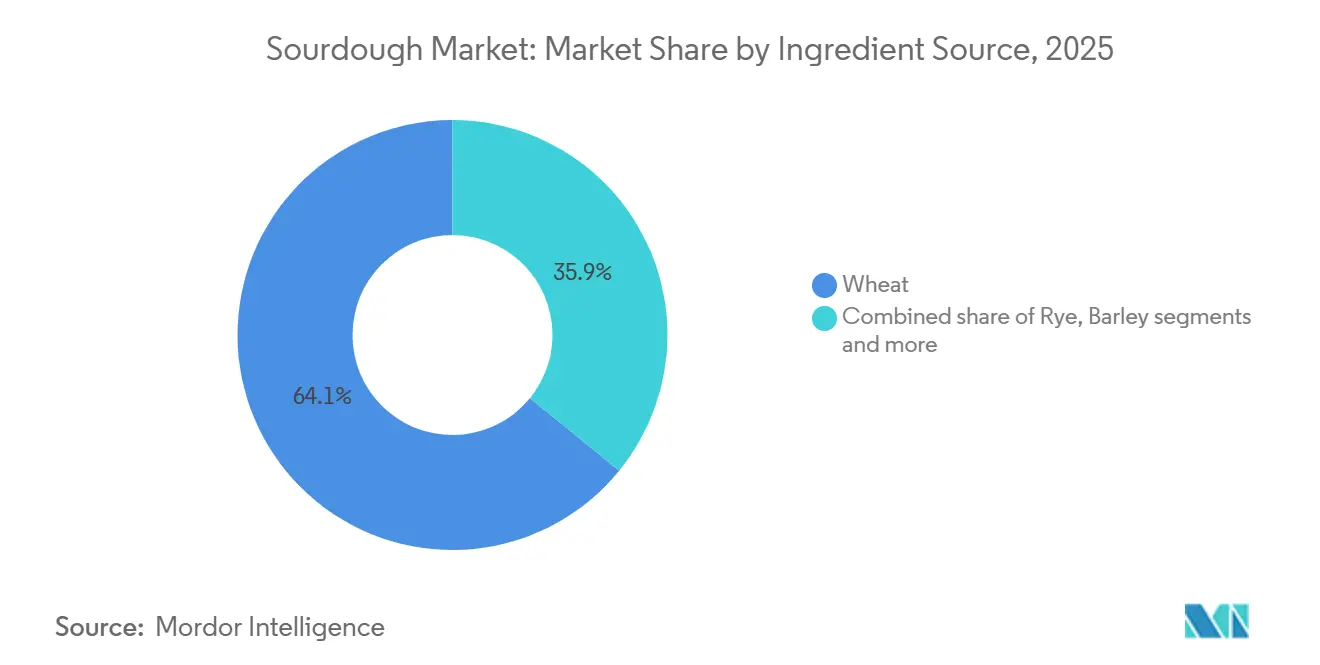

- By ingredient source, wheat-based variants accounted for 64.12% of the sourdough market size in 2025, and rye leads future growth with a 7.05% CAGR over 2026-2031.

- By application, breads and buns dominated with 59.85% revenue share in 2025; pizza crust is set to advance at an 8.05% CAGR through 2031.

- By distribution channel, retail outlets held 67.95% share of the sourdough market size in 2025, whereas foodservice is the fastest-rising channel at 7.70% CAGR.

- By geography, Europe led with 34.01% revenue share in 2025, and Asia-Pacific is positioned for the highest 8.60% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sourdough Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing awareness of perceived health benefits associated with sourdough, such as easier digestibility and lower glycemic response | +1.2% | Global, with strongest uptake in North America and Europe | Medium term (2-4 years) |

| Clean-label and minimal ingredient preference | +0.9% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Innovation in sourdough product formats, including packaged loaves, snacks, and ready-to-bake options | +0.8% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Rising participation in baking and home fermentation trends | +0.5% | North America and Europe, declining in United Kingdom but stable in United States/Canada | Short term (≤ 2 years) |

| Expansion of premium bakery offerings across retail and foodservice channels | +1.0% | Global, with Asia-Pacific and Middle East showing accelerated growth | Long term (≥ 4 years) |

| Growing consumer focus on gut health and digestive wellness driving demand for naturally fermented sourdough products | +1.1% | Global, particularly strong in North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Understand The Key Trends Shaping This Market

Download PDF

Growing awareness of perceived health benefits associated with sourdough, such as easier digestibility and lower glycemic response

Awareness of the health benefits of sourdough is driving the market's growth. Sourdough bread has a glycemic index of approximately 55, which is close to the low glycemic threshold of 50 or less. This makes it a preferred choice for individuals looking to manage their blood sugar levels effectively, as highlighted by the Cleveland Clinic in July 2024[1]Source: Cleveland Clinic, "Is Sourdough Bread Healthy for You?", health.clevelandclinic.org. The natural fermentation process used in sourdough production not only makes it easier to digest but also enhances nutrient absorption, making it appealing to health-conscious consumers. With the increasing prevalence of lifestyle-related health issues such as diabetes and obesity, there is a growing demand for bakery products that are functional and have a low glycemic index. In response, bakeries and ingredient manufacturers are introducing a wider range of sourdough products that focus on promoting digestive health and balanced nutrition.

Rising participation in baking and home fermentation trends

The growing interest in baking and home fermentation is driving the sourdough market. Consumers are increasingly drawn to artisanal and homemade foods, boosting the popularity of sourdough products. A survey conducted by the Agriculture and Horticulture Development Board in February 2025 revealed that 11% of people in the United Kingdom baked at least once a week, while 20% baked at least once a month[2]Source: Agriculture and Horticulture Development Board, "Baking Trends in 2024: To Bake Or To Buy, That Is The Question", ahdb.org.uk. This highlights consumers' consistent engagement in home baking. As a result, demand for sourdough starters, premixes, and fermentation ingredients has steadily risen, and these products are widely available at retail and specialty stores. Furthermore, more people are becoming aware of the benefits of natural fermentation, clean-label food options, and traditional baking techniques. This growing awareness has encouraged consumers to try sourdough baking at home, further expanding the market.

Growing consumer focus on gut health and digestive wellness is driving demand for naturally fermented sourdough products.

Consumers are increasingly focusing on gut health and digestive wellness, driving growth in the global sourdough market. Digestive diseases affect a significant portion of the population, with the National Institute of Diabetes and Digestive and Kidney Diseases reporting in October 2025 that around 60 to 70 million people in the United States suffer from such conditions[3]Source: National Institute of Diabetes and Digestive and Kidney Diseases, "Digestive Diseases Statistics for the United States", niddk.nih.gov. This has led to a rising demand for foods that promote better digestion. Sourdough, made through natural fermentation, produces compounds that make it easier to digest and help maintain a healthy balance of gut bacteria. As a result, bakeries and ingredient manufacturers are marketing sourdough as a healthier and gut-friendly option in the bakery segment. Growing awareness about the importance of digestive health and preventive nutrition is expected to further boost the demand for sourdough products worldwide, as consumers increasingly seek functional foods that support overall well-being.

Innovation in sourdough product formats, including packaged loaves, snacks, and ready-to-bake options

Innovation in sourdough product formats is significantly driving market growth by making sourdough products more accessible and versatile. Companies are expanding beyond traditional fresh bread to offer convenient options such as ready-to-bake kits, frozen dough, and packaged sourdough snacks. These innovations aim to meet the growing demand for easy-to-use, longer-lasting products. For example, in 2024, East Pizzas in the United Kingdom introduced 48-hour fermented retail pizza bases, providing consumers with a premium-quality product that is convenient for home use. Similarly, leading bakery companies like Bimbo Bakeries and Flowers Foods have launched sliced sourdough bread enriched with protein and fiber, targeting health-conscious consumers. These developments are helping manufacturers reach a broader audience while meeting the demand for both convenience and health-focused options.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sensitivity of sourdough cultures to temperature and humidity | -0.7% | Global, particularly challenging in tropical and subtropical regions (Southeast Asia, Latin America, Sub-Saharan Africa) | Medium term (2-4 years) |

| Competition from faster-rising yeast-based and packaged bread alternatives | -0.9% | Global, most acute in price-sensitive emerging markets (India, Indonesia, Nigeria) | Short term (≤ 2 years) |

| Longer fermentation cycles increase production complexity and constrain scalability | -0.8% | Global, affecting both artisan bakeries and industrial producers | Long term (≥ 4 years) |

| Higher retail prices compared to conventional bread | -0.6% | Global, with strongest impact in emerging markets and lower-income consumer segments | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Sensitivity of sourdough cultures to temperature and humidity

The sensitivity of sourdough cultures to temperature and humidity is a significant challenge for the sourdough market, as stable fermentation conditions are crucial for maintaining consistent product quality. The main bacteria in sourdough, Lactobacillus sanfranciscensis, thrive within a specific temperature range of 28 °C to 32 °C. Any deviation from this range or exposure to low humidity can slow down microbial activity, weaken the starter, and negatively impact the final product. This issue is particularly problematic in regions with extreme weather conditions, such as high heat or excessive humidity, where maintaining optimal fermentation conditions becomes difficult. To address this, bakeries often rely on specialized fermentation chambers and controlled production environments. However, these solutions come with high costs, making it especially challenging for smaller or artisanal bakeries to adopt them.

Competition from faster-rising yeast-based and packaged bread alternatives

Competition from faster-rising yeast-based alternatives poses a significant challenge to the growth of the global sourdough market. Yeast-based bread offers key advantages, such as quicker production times and lower costs. Unlike sourdough, which requires a long fermentation process that can take several hours or even days, yeast-based bread can be produced in just a few hours. This faster production process allows manufacturers to increase output and meet higher demand more efficiently. The cost difference between sourdough and yeast-based bread impacts consumer choices, especially in price-sensitive regions like India and Indonesia. In these markets, conventional white bread made with yeast is much more affordable, making it the preferred option for most consumers. This affordability ensures that yeast-based bread remains a staple in these regions.

Segment Analysis

By Form: Dry Formats Dominate, Liquid Variants Accelerate

Dry mix and premix products held the largest share of the sourdough market in 2025, accounting for 60.89% of the total market. These products are popular due to their longer shelf life, ease of storage, and convenience compared to traditional sourdough starters. They ensure consistent fermentation results, making them a preferred choice for commercial bakeries and large-scale food manufacturers. Premixes simplify the baking process by reducing preparation time and minimizing technical challenges. This convenience has driven their widespread use across both developed and emerging markets, furthering their dominance.

Ready-to-use liquid sourdough products are expected to grow at a CAGR of 7.21% between 2026 and 2031, driven by increasing demand for authentic flavors and artisanal-quality baked goods. These products save time by eliminating the need for fermentation preparation while delivering consistent taste and texture. They are particularly popular in premium bakery applications, such as specialty breads and clean-label products, which align with consumer preferences for natural and minimally processed ingredients. The growing availability of these products through commercial bakeries and foodservice channels is further boosting their adoption, contributing to their strong growth during the forecast period.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Processing Type: Powder Leads, Dried Formats Surge

Type III powder starters accounted for 43.10% of sourdough market revenue in 2025, primarily due to their suitability for high-speed industrial production. These starters can be directly added to automated mixing systems, helping save time and boost efficiency in large-scale operations. Their consistent composition ensures uniform flavor, texture, and fermentation quality across different production sites. This makes them a preferred choice for commercial bakeries and packaged food manufacturers that prioritize reliability and scalability. The growing need for standardized and efficient production processes continues to drive the dominance of this segment.

Type II dried starters are projected to grow the fastest, with a CAGR of 7.55% through 2031. Recent advancements in spray drying and freeze-drying technologies have enhanced the ability to preserve flavors and maintain the viability of microorganisms. These improvements ensure better fermentation performance while retaining the authentic sourdough taste. Additionally, the extended shelf life and ease of transportation make dried starters ideal for global distribution. The rising demand for stable and high-quality sourdough solutions, both in industrial-scale baking and artisanal production, is expected to fuel the growth of this segment significantly.

By Ingredient Source: Wheat Dominates, Rye Rises

Wheat-based sourdough accounted for 64.12% of total revenue in 2025. This dominance is primarily due to the widespread availability of wheat and its well-established global supply chains. Wheat sourdough is highly favored for its soft texture, versatile use in various bakery products, and familiar taste. The presence of advanced milling infrastructure ensures consistent flour quality, making it suitable for large-scale production. Commercial bakeries also prefer wheat sourdough for its reliable fermentation, further solidifying its leading position in the market.

Rye-based sourdough is expected to grow at a CAGR of 7.05% through 2031, driven by increasing consumer interest in health and nutrition. Rye is rich in fiber and has a lower glycemic index, which helps regulate blood sugar levels, making it a healthier option for many consumers. Its natural prebiotic properties also promote better digestive health, enhancing its appeal among health-conscious buyers. Furthermore, the rising demand for artisanal and specialty breads is boosting the adoption of rye-based sourdough. As awareness of its nutritional benefits grows, rye sourdough is anticipated to gain a stronger foothold in the market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Bread Anchors, Pizza Crust Outpaces

Breads and buns made up 59.85% of the sourdough market revenue in 2025, making them the most significant application of sourdough fermentation. These products are widely consumed across both retail and foodservice channels, ensuring steady demand. Sourdough improves the flavor, texture, and shelf life of breads and buns, making it a preferred choice for both artisan and packaged breads and bunsrising consumer interest in natural and fermented ingredients is encouraging manufacturers to incorporate sourdough into. Its tangy taste and unique crumb structure appeal to consumers, especially those seeking premium and clean-label bakery options. This strong consumer preference continues to drive the dominance of breads and buns in the sourdough market.

Pizza crust is projected to grow at a CAGR of 8.05% between 2026 and 2031, fueled by increasing demand for artisanal and high-quality pizza options. Sourdough-based crusts offer a better texture, richer flavor, and easier digestion than traditional dough. The growing popularity of specialty pizza chains and gourmet foodservice outlets is further boosting the adoption of sourdough crusts. Additionally, the rising interest in natural and fermented ingredients among consumers is encouraging manufacturers to use sourdough in pizza recipes. These factors are expected to drive significant growth in the pizza crust segment during the forecast period.

By Distribution Channel: Foodservice Ascends Amid Menu Premiumization

Retail channels, such as supermarkets, hypermarkets, and online stores, made up 67.95% of the sourdough market revenue in 2025. This dominance is due to the easy availability of sourdough products and their visibility to consumers. Many supermarkets now offer in-store bakery programs that produce fresh sourdough daily, attracting customers and allowing retailers to charge higher prices for artisan-quality products. The growing demand for both fresh and packaged sourdough items has boosted retail sales. The expansion of organized retail networks, especially in emerging markets like Latin America and Southeast Asia, is further driving growth in this segment.

The foodservice sector is expected to grow at the fastest rate, with a projected CAGR of 7.70% through 2031. Restaurants, cafes, and specialty bakeries are increasingly incorporating sourdough into their menus to stand out and offer premium options. Sourdough’s traditional fermentation process and artisanal appeal add value for consumers, making it a popular choice. The recovery of the foodservice industry after the pandemic has also contributed to this growth. As more consumers seek premium dining experiences and naturally fermented bakery products, the foodservice segment is likely to see sustained demand in the coming years.

Geography Analysis

Europe contributed 34.01% of the sourdough market revenue in 2025, driven by its strong baking traditions and recognition of natural fermentation processes by regulators. Countries like Germany, France, and the United Kingdom have a high demand for sourdough, as consumers prefer products made with heritage grains and artisanal techniques. Western Europe benefits from well-established bakery networks and premium product positioning, which maintain steady growth. Meanwhile, Eastern Europe is seeing new opportunities with the introduction of convenient options like ready-to-bake kits. These factors ensure Europe remains a key player in the global sourdough market while gradually expanding into emerging areas.

The Asia-Pacific region is the fastest-growing market, with a CAGR of 8.60% through 2031. Rapid urbanization and the expansion of the bakery industry are driving demand for sourdough, especially as consumers increasingly show interest in premium, fermented bakery products. Global and regional ingredient suppliers are investing in the region through acquisitions and training programs to strengthen their presence. Countries like China, India, and Australia are seeing a rise in organized bakeries, boosting sourdough adoption. Additionally, the growing popularity of artisanal bakery products in urban areas is further fueling market growth in this region.

North America continues to see steady growth in the sourdough market, supported by consumer interest in artisanal baking and fermented foods. Major commercial bakeries are driving innovation, while strong retail distribution networks ensure product availability. In Latin America, sourdough is gradually gaining traction, particularly in premium bakery segments and among urban consumers. The Middle East and Africa are also experiencing growth, supported by expatriate communities and the modernization of bakery operations. Investments in controlled production environments and the expansion of bakery infrastructure are helping producers meet the rising demand for artisanal products in these regions.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The sourdough market is highly fragmented, with both large multinational ingredient manufacturers and smaller regional or artisan producers playing key roles. Major companies such as Puratos Group, Lesaffre International, Lallemand Inc., IREKS GmbH, and Ernst Böcker GmbH dominate the global supply of starter cultures, premixes, and fermentation solutions. These companies leverage their strong research capabilities, extensive distribution networks, and established partnerships with commercial bakeries to maintain their market position. Meanwhile, smaller bakeries contribute to the market's diversity by offering regionally specialized products and catering to local tastes.

Large ingredient manufacturers are focusing on strategies like vertical integration, acquisitions, and product innovation to strengthen their market presence. By investing in advanced fermentation technologies, proprietary starter cultures, and scalable production methods, they ensure consistent product quality and operational efficiency. These companies are also responding to consumer demand for clean-label and health-focused products by offering natural fermentation solutions. Their ability to support large-scale production gives them a competitive edge in meeting the needs of industrial bakeries and commercial operations.

On the other hand, artisan bakeries differentiate themselves by focusing on traditional techniques, unique flavors, and premium-quality products. They often use heritage grains and locally sourced ingredients to appeal to consumers seeking authentic and high-quality sourdough. However, smaller producers face challenges in scaling their operations and maintaining consistent production conditions. Despite these limitations, the rise of online bakery platforms and specialty retail channels is creating new opportunities for artisan producers to reach niche markets and cater to the growing demand for premium sourdough products.

Sourdough Industry Leaders

-

Puratos Group

-

Lesaffre International

-

Lallemand Inc.

-

IREKS GmbH

-

Ernst Böcker GmbH

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Dave's Killer Bread launched Supreme Sourdough in time for National Homemade Bread Day. Consumer interest in sourdough had continued to grow, and Dave's Killer Bread addressed that demand with its organic Supreme Sourdough loaf, made with an authentic starter and a special double-fermentation process.

- June 2025: United Kingdom bread brand Jason’s Sourdough introduced two new product ranges, Jason’s Sourdough Creations and Jason’s Everyday Seeded Protein Rolls. The additions, which became available in 300 Tesco stores nationwide, expanded the brand’s core range to meet growing demand for premium bread products.

- December 2024: Manchester-based Robert Andrew Bakery introduced a new low-carb sourdough range. This product line was specifically developed for consumers actively seeking healthier bread alternatives.

- May 2024: Puratos Group launched Sapore Lavida, Belgium's inaugural fully traceable active sourdough, crafted solely from whole wheat flour. This groundbreaking ingredient championed regenerative agricultural practices, empowering bakers throughout mainland Europe to cater to the surging demand for locally produced and sustainably sourced sourdough products.

Global Sourdough Market Report Scope

Sourdough is made by the fermentation of dough using wild Lactobacillaceae and yeast. It is also known as a bread starter; sourdough gives baked products structure and taste. The sourdough market has been segmented by form, processing type, ingredient source, application, distribution channel, and geography. Based on form, the market is classified into ready-to-use liquid and dry mix/premix. Based on processing type, the market is classified into types I, II, and III. Based on ingredient source, the market is classified into wheat, rye, barley, and others. Based on application, the market is classified into breads and buns, cakes and pastries, pizza crust, cookies and crackers, and others. Based on the distribution channel, the market is classified into the food processing industry, foodservice, and retail. The report further analyzes the market scenario based on geography into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The market sizing has been done in USD for all the aforementioned segments.

By Form

| Ready-To-Use Liquid |

| Dry Mix/Premix |

By Processing Type

| Type I (Fresh) |

| Type II (Dried) |

| Type III (Powder) |

By Ingredient Source

| Wheat |

| Rye |

| Barley |

| Others (Oats, etc.) |

By Application

| Breads and Buns |

| Cakes and Pastries |

| Pizza Crust |

| Cookies and Crackers |

| Others |

By Distribution Channel

| Food Processing Industry | |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Online Stores | |

| Other Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Form | Ready-To-Use Liquid | |

| Dry Mix/Premix | ||

| By Processing Type | Type I (Fresh) | |

| Type II (Dried) | ||

| Type III (Powder) | ||

| By Ingredient Source | Wheat | |

| Rye | ||

| Barley | ||

| Others (Oats, etc.) | ||

| By Application | Breads and Buns | |

| Cakes and Pastries | ||

| Pizza Crust | ||

| Cookies and Crackers | ||

| Others | ||

| By Distribution Channel | Food Processing Industry | |

| Foodservice | ||

| Retail | Supermarkets/Hypermarkets | |

| Online Stores | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large will the global sourdough market be by 2031?

Forecasts show the global sourdough market size reaching USD 4.69 billion by 2031, up from USD 3.45 billion in 2026.

Which region offers the fastest growth for sourdough products?

Asia-Pacific is projected to post an 8.60% CAGR through 2031, driven by urbanization and Western bakery adoption.

What product form leads sales in sourdough?

Dry Mix/Premix formats dominate with 60.98% revenue share in 2025 due to their shelf stability and ease of use.

Why are rye-based sourdough breads gaining attention?

Rye offers higher prebiotic fiber and lower glycemic response than wheat, spurring a 7.05% CAGR for rye sourdough products.