Single-Use Bioprocessing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

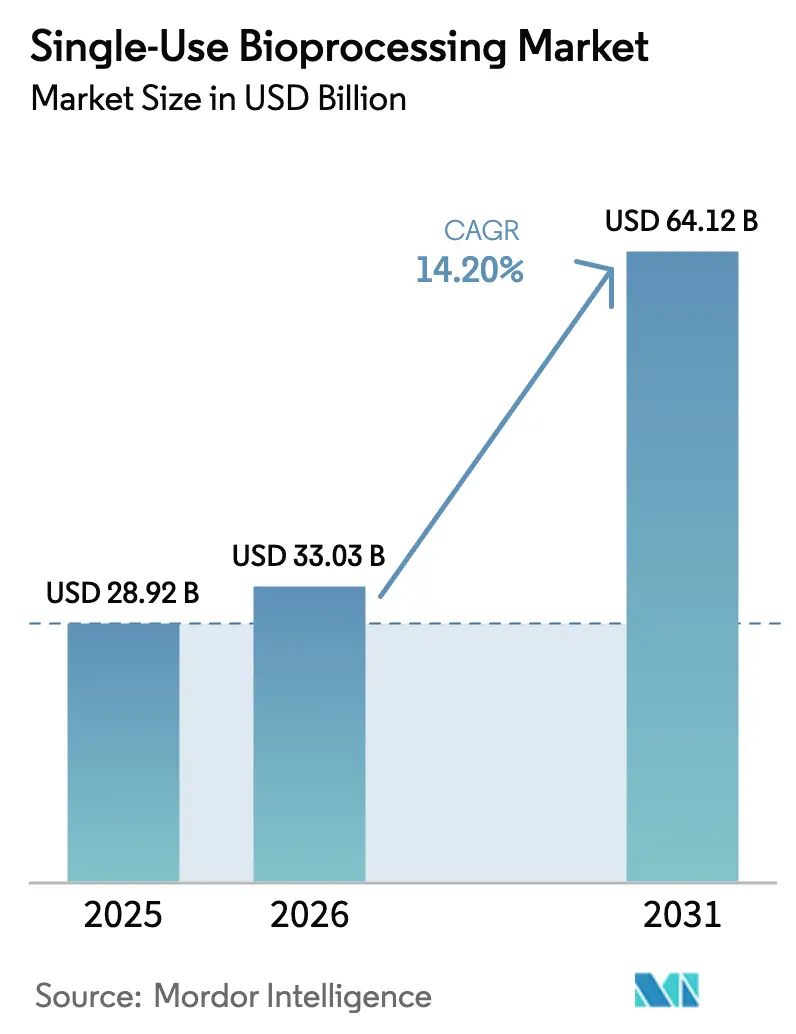

| Market Size (2026) | USD 33.03 Billion |

| Market Size (2031) | USD 64.12 Billion |

| Growth Rate (2026 - 2031) | 14.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Single-Use Bioprocessing Market Analysis by ���ϲ�����

The single-use bioprocessing market size was valued at USD 28.92 billion in 2025 and estimated to grow from USD 33.03 billion in 2026 to reach USD 64.12 billion by 2031, at a CAGR of 14.2% during the forecast period (2026-2031). Single-use bioprocessing market adoption accelerated as manufacturers sought faster facility build-outs, lower capital outlays, and the flexibility to run multiple biologics without cross-contamination risk. Regulatory bodies in the United States and Europe published technology-friendly guidance in 2025, effectively removing a lingering compliance barrier. Downstream operations are now pivoting toward membrane-based purification formats that match high-titer antibody processes, while AI-enabled control loops elevate demand for disposable inline sensors. Medical-grade polymer supply shocks in late 2025 revealed upstream vulnerabilities and triggered vertical-integration moves by leading suppliers. Sustainability pressure, especially in the European Union, is catalyzing take-back pilots and design tweaks that enable polymer recovery rather than incineration.

Key Report Takeaways

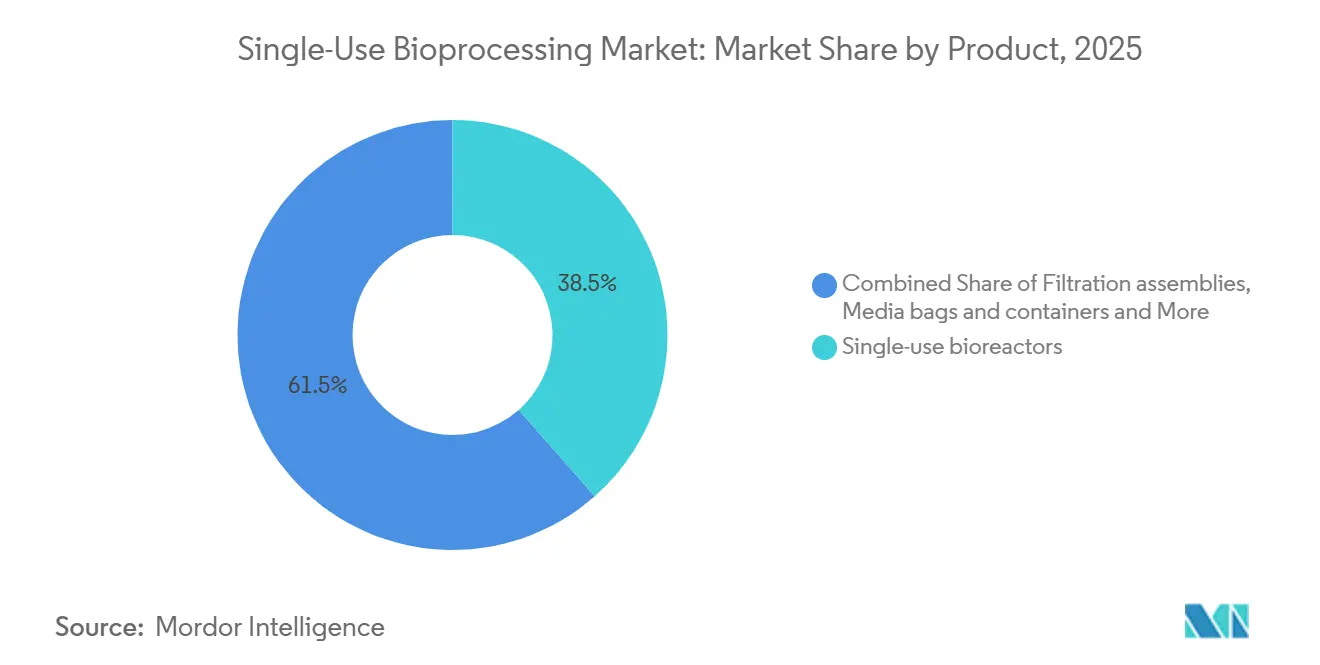

- By product category, single-use bioreactors led with 38.55% of the single-use bioprocessing market share in 2025. Sensors and analytics are forecast to expand at a 16.25% CAGR through 2031 as the fastest-growing product line.

- By workflow stage, upstream processing accounted for 52.53% of 2025 revenue, while downstream operations are projected to grow at a 15.75% CAGR to 2031.

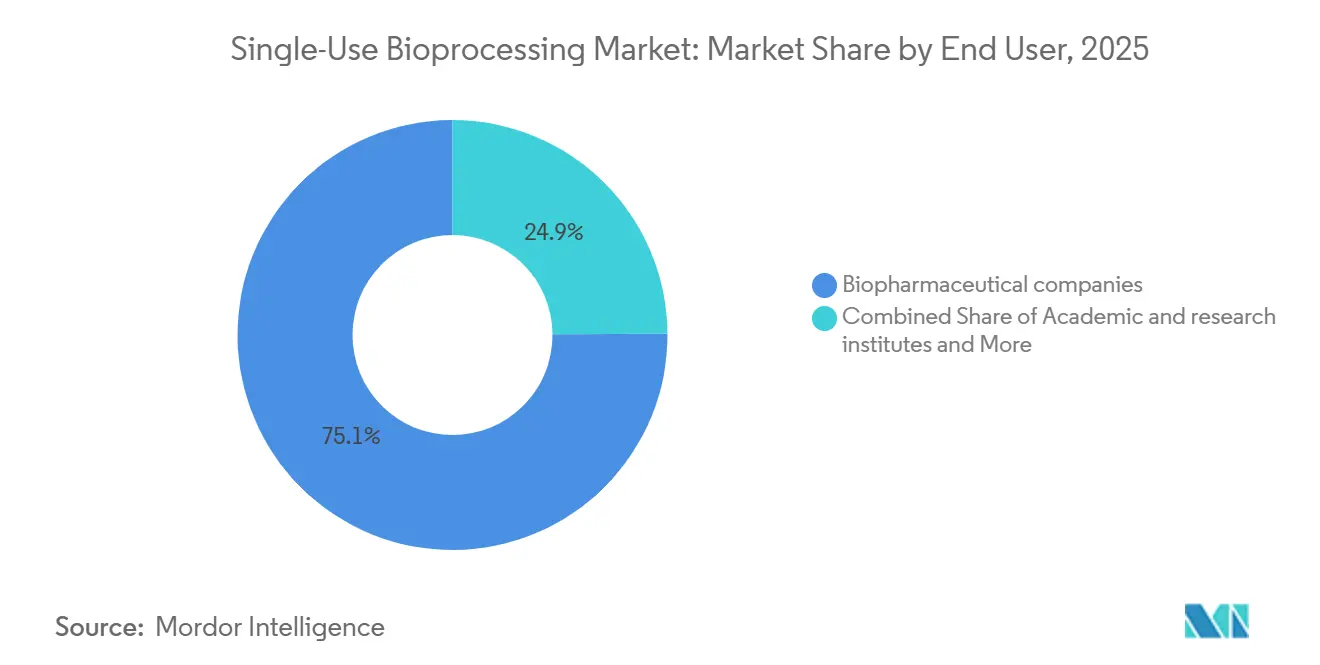

- By end user, biopharmaceutical companies held 75.15% revenue share in 2025; contract development and manufacturing organizations are advancing at a 14.82% CAGR through 2031.

- By scale, the commercial scale held 66.65% revenue share in 2025, rising at 15.32% CAGR to 2031.

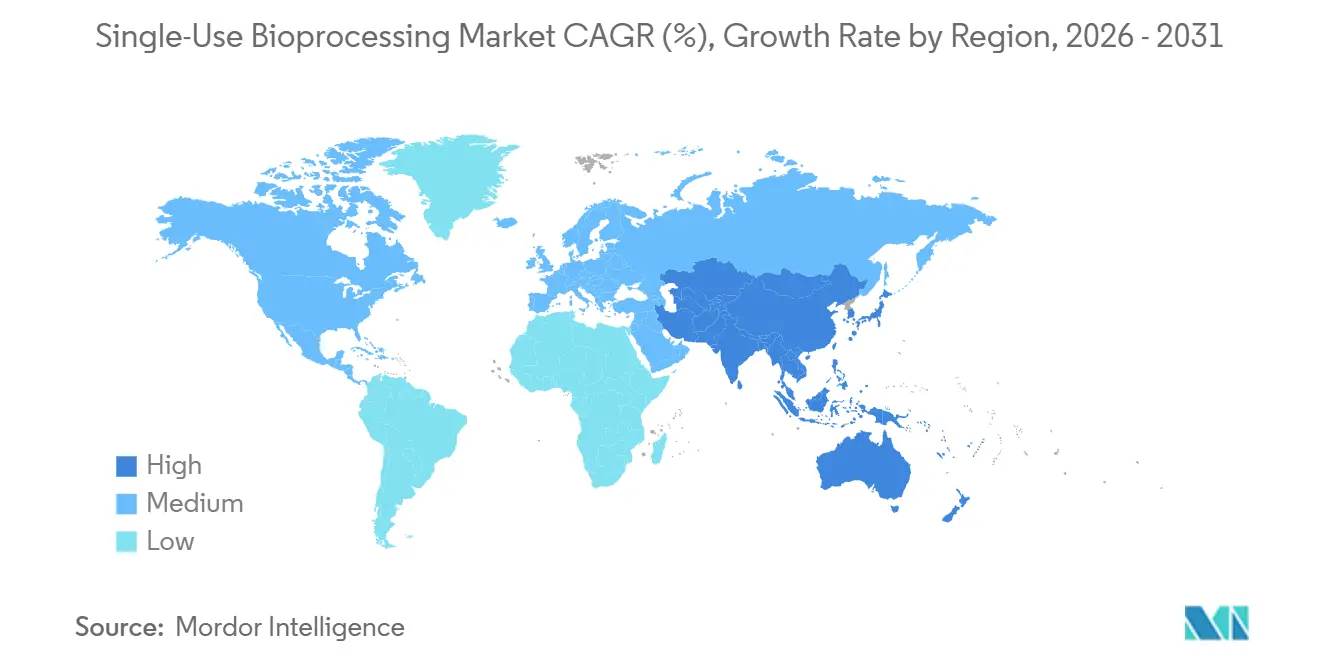

- By geography, North America captured 35.23% of 2025 revenue, whereas Asia-Pacific is poised for the highest regional growth at a 15.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Single-Use Bioprocessing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost & CAPEX avoidance vs. stainless-steel plants | +3.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Rising demand for biologics & biosimilars | +2.8% | Global; APAC biosimilar wave accelerating | Long term (≥ 4 years) |

| Rapid scale-up needs for mRNA vaccines & personalized therapies | +2.1% | North America and Europe core, spillover to APAC | Short term (≤ 2 years) |

| Circular-economy mandates favoring polymer recovery | +1.5% | Europe regulatory, voluntary in North America | Long term (≥ 4 years) |

| Plug-and-play microbial single-use fermentors ≥3,000 L | +1.3% | Global, strongest in U.S. and China | Medium term (2-4 years) |

| AI-enabled hybrid-continuous control loops | +1.1% | North America and Europe early adopters | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Cost & CAPEX Avoidance vs. Stainless-Steel Plants

Replacing clean-in-place and steam-in-place hardware with disposable assemblies compresses green-field project timelines by up to two years and cuts capital budgets nearly in half. Peer-reviewed modeling of a 2,000 L monoclonal antibody campaign showed breakeven at only 12 batches a year, a level typical for multi-product CDMO facilities. Lonza reported that 70% of mammalian capacity added since 2023 employs single-use lines, citing quicker client onboarding[1]Lonza Group, “Annual Report 2024,” Lonza.com. Updated FDA guidance allows stainless vessels to be swapped with validated disposables without triggering new comparability studies, further tilting the economic balance. These factors collectively underpin the structural shift captured in the single-use bioprocessing market.

Rising Demand for Biologics & Biosimilars

Global approvals surpassed 80 monoclonal antibodies in 2025, and EU biosimilar filings hit a record 34 products, each requiring flexible capacity. China cleared 47 biosimilars the same year, spurring Jiangsu and Shanghai CDMOs to install modular disposable suites. India’s 22% biosimilar export growth leaned on lower-capex single-use lines that still meet EU GMP requirements. Antibody-drug conjugate containment challenges amplify the appeal of closed, disposable systems. These converging trends feed a robust long-term pull on the single-use bioprocessing market.

Rapid Scale-up Needs for mRNA Vaccines & Personalized Therapies

BARDA’s USD 1.2 billion program contracted modular suites capable of pivoting from pandemic vaccines to commercial products within six weeks. BioNTech is retrofitting its Marburg site with single-use fermentors for individualized cancer vaccines, a conversion financially unrealistic for stainless assets. Every FDA-approved autologous cell therapy facility now operates closed disposable paths to avoid patient cross-contamination. A recent CAR-T case study documented batch-turnaround cuts of one-third after eliminating cleaning validation steps. These speed demands reinforce growth in the single-use bioprocessing market.

Circular-Economy Mandates Favoring Polymer Recovery

The EU’s revised Single-Use Plastics Directive requires take-back schemes for polyethylene and polypropylene films over 10 kg per unit, directly impacting bioreactor bags. Sartorius and Veolia launched a Lyon pilot diverting 120 tons of film waste annually from incineration through mechanical recycling. Enzymatic depolymerization research shows promise but must contend with gamma-irradiation chain scission. ISPE quantified 0.8 tons of plastic per 2,000 L batch, a metric now embedded in many European tenders. Procurement teams increasingly weigh circularity alongside performance, shaping supplier roadmaps in the single-use bioprocessing market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Leachables & extractables compliance risk | -1.8% | Global; heightened scrutiny in North America and EU | Short term (≤ 2 years) |

| Plastic-waste disposal & ESG regulations | -1.3% | Europe regulatory; voluntary in North America and APAC | Medium term (2-4 years) |

| Viscosity/shear limits in high-volume downstream steps | -0.9% | Global; acute in high-titer mAb production | Medium term (2-4 years) |

| Medical-grade polymer supply-chain tightness | -1.1% | Global; exacerbated by regional resin shortages | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Leachables & Extractables Compliance Risk

FDA’s ANDA guidance now mandates extractables and leachables studies for every disposable component contacting drug substance, adding six to nine months and roughly USD 200,000 per product. ICH Q3E sets a 1.5 µg/day genotoxic threshold that some plasticizers can surpass, forcing tighter gamma-irradiation controls. MilliporeSigma recalled 800 tubing sets after phthalate levels hit 4.2 ppm. USP chapters <665> and <1665> now require mass-spectrometry characterization above 0.1 ppm, a hurdle for small suppliers. Compliance costs temper near-term momentum in the single-use bioprocessing market.

Plastic-Waste Disposal & ESG Regulations

The EU directive imposes 30% recycling targets by 2028, compelling suppliers to finance take-back logistics. A sustainability review pegged plastic intensity at 0.8 t per 2,000 L antibody batch, with incineration still dominant in North America and APAC. Sartorius diverted 18% of returned disposables via French and German pilots but cited gamma-irradiation degradation as a technical hurdle. Investor coalitions managing USD 4 trillion demanded plastic-waste disclosures from the top 10 suppliers in early 2025. These ESG headwinds shave growth from the single-use bioprocessing market.

Segment Analysis

By Product: Sensors Drive Margin Expansion

Single-use bioreactors dominated 2025 revenue, yet inline sensors are the fastest-growing product class. FlowVPE spectroscopy alone generated USD 42 million in its launch year, underscoring how analytics attach high margins to consumable sales[2]Repligen Corporation, “Investor Presentation 2025,” Repligen.com. Filtration cassettes and media bags underpin buffer prep, while proprietary tubing geometries lock in recurring demand. Mixers benefit from continuous-manufacturing trends, with magnetic designs shortening media-prep cycles from eight hours to 90 minutes. The single-use bioprocessing market size for sensors is projected to expand briskly as AI-centric control schemes spread.

The competitive battleground pivots on ecosystem lock-in. Sartorius and Cytiva secure share through connector and bag exclusivity, discouraging third-party component substitution. Chromatography formats trail because reusable columns still underpin high-volume antibody workflows, yet membrane adsorbers are gaining as titers rise. Supplier R&D now funnels toward integrating disposable sensors, ensuring that data-rich operation remains inseparable from the broader single-use bioprocessing market.

Note: Segment shares of all individual segments available upon report purchase

By Workflow Stage: Downstream Gains Momentum

Upstream assets, especially bioreactors, accounted for a 52.53% single-use bioprocessing market share in 2025, reflecting long-standing maturity. Downstream units, however, post the quickest gains as continuous filtration and single-use TFF systems displace steel Protein A columns at high titers. A 0.5 m² disposable TFF cassette introduced in 2025 processes 500 L in a single pass, removing a 12-hour cleaning step. The single-use bioprocessing market size for downstream modules is projected to climb alongside hybrid continuous lines.

Continuous chromatography pilot data show 95% step yields with membrane adsorbers, cutting validation times and water consumption. Regulatory clarity from ICH Q13 accelerates adoption by defining control-strategy expectations. Fill-finish operations also lean on disposable tubing and pump heads that reduce product changeovers from eight hours to two. Collectively these shifts rebalance value from upstream to downstream within the single-use bioprocessing market.

By End User: CDMOs Outpace Innovators

Biopharmaceutical innovators captured three-quarters of 2025 revenue, yet CDMOs exhibit the steeper trajectory. A BioProcess International survey reported 68% of CDMOs citing disposables as their principal multi-product enabler. Lonza deploys single-use formats in 85% of small-client suites, shortening cleaning turnarounds that would otherwise erode utilization. Government grants to universities and public labs also stipulate disposable platforms to maximize shared-facility uptime.

Academic demand is steady, anchored by flexibility needs in early trials. EMA guidance now lets Phase I and II batches run fully disposable without stainless comparability, unlocking early investment at smaller scales. As autologous therapies proliferate, end-user segmentation will continue to tilt toward organizations managing many products in parallel, a core advantage of the single-use bioprocessing market.

Note: Segment shares of all individual segments available upon report purchase

By Scale: Commercial Dominates, Clinical Accelerates

Commercial-scale programs held two-thirds of 2025 revenue, widening as biosimilar launches crest. Disposable bioreactors now span 50 L to 5,000 L, letting firms use one platform from Phase I to launch. Cytiva said 40% of 2024 XDR sales were to customers planning dual clinical-commercial use, compressing tech-transfer timelines. A 2,000 L campaign reaches cost parity versus stainless steel at roughly 12 batches a year, a threshold most commercial antibodies exceed.

Retrofit activity is meaningful: 30% of Sartorius STR units shipped in 2024 replaced legacy steel vessels at multiproduct plants. For clinical-stage autologous therapies, disposables are non-negotiable due to patient-specific batch segregation. Collectively, these dynamics keep the single-use bioprocessing market on a steep adoption curve across both scales.

Geography Analysis

North America’s 35.23% revenue share in 2025 stemmed from BARDA’s pandemic-preparedness build-out, which specified modular disposable suites[3]Biomedical Advanced Research and Development Authority, “mRNA Vaccine Manufacturing Investment Program,” Phe.gov. FDA’s advanced-manufacturing framework further validated the approach, prompting retrofit programs in legacy facilities. Canada directed CAD 2.2 billion (USD 1.6 billion) to bolster vaccine and biologic capacity, stipulating single-use platforms for multi-product flexibility. Mexican CDMOs expanded to capture nearshoring demand from U.S. biopharma, choosing disposables for rapid deployment.

Europe blends regulatory push and sustainability pull. The Single-Use Plastics Directive mandates producer take-back, nudging adoption of recyclable bag films. Germany earmarked EUR 800 million (USD 880 million) for continuous single-use hubs, while the UK MHRA updated validation guidance to cover hybrid workflows. France installed 18 new suites for biosimilar output, and Southern European facilities added roughly 10,000 L of disposable bioreactor capacity in 2025, primarily for fill-finish programs.

Asia-Pacific is set for the fastest growth at 15.42% CAGR. China’s 47 biosimilar approvals in 2025 sparked facility expansions that favor disposable trains over steel. India’s USD 500 million upgrade fund names single-use equipment an eligible expense. Japan’s PMDA guidance now permits disposables without comparability studies for biosimilars, accelerating local uptake. South Korean majors added 120,000 L of new capacity over 2024-2025, positioning the peninsula as a global CDMO hub. Emerging regions join the trend: the UAE committed USD 300 million to a disposable-based biosimilar JV, and South Africa’s Biovac installed a 2,000 L suite for vaccine surge capacity.

Competitive Landscape

Market concentration is moderate. Cytiva and Sartorius collectively dominate bioreactor volumes through proprietary bag geometries and sensor integration, discouraging cross-platform mixing. Suppliers compete on volume range, plug-and-play assemblies, and data connectivity. Repligen’s FlowVPE sensor illustrates how inline analytics add high-margin attachments to consumables. Patents filed with the USPTO in 2024-2025 show 40% focus on sensors or data platforms, underlining this pivot.

Smaller entrants exploit niches. PBS Biotech targets oxygen-intensive microbial fermentations, while Cellexus serves closed cell-therapy workflows unmet by stirred-tank incumbents. Downstream continuous processing remains white space; membrane adsorber and high-capacity TFF launches aim to displace resin-heavy columns. Sustainability differentiation is nascent but rising: the Sartorius-Veolia polymer-recovery pilot offers early-mover credibility ahead of expected EU take-back mandates.

Supply-chain resilience surfaced as a strategic priority after a 2025 European resin-plant fire doubled lead times for 200 L bags. Thermo Fisher’s January 2026 joint venture with a polyolefin producer exemplifies vertical integration to lock in film supply. Similar moves are anticipated from other top-tier vendors as raw-material risk management becomes integral to sustaining the single-use bioprocessing market.

Single-Use Bioprocessing Industry Leaders

Sartorius AG

Thermo Fisher Scientific

Eppendorf AG

Merck KGaA

Danaher Corporation (Cytiva)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sartorius Stedim Biotech almost doubled cleanroom space in France to 9,000 m² to meet ballooning demand for single-use solutions.

- April 2025: Thermo Fisher Scientific launched the 5 L DynaDrive single-use bioreactor, extending its platform to larger perfusion cultures.

Global Single-Use Bioprocessing Market Report Scope

As per the scope of the report, single-use bioprocessing is a fast-moving technology used to develop disposable bioprocessing equipment to manufacture biopharmaceutical products.

The single-use bioprocessing market is segmented by product into single-use bioreactors, filtration assemblies, media bags and containers, mixers and blenders, tubing and connectors, single-use sensors and analytics, chromatography and purification columns, sampling and aseptic transfer systems, and other niche components. By workflow stage, the market is categorized into upstream processing, downstream processing, and ancillary operations (formulation, fill-finish). By end user, the segmentation includes biopharmaceutical companies, academic and research institutes, and contract development and manufacturing organizations (CDMOs). By scale, the market is divided into clinical scale and commercial scale. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report offers the value (USD) for the above segments.

| Single-use bioreactors |

| Filtration assemblies |

| Media bags & containers |

| Mixers & blenders |

| Tubing & connectors |

| Single-use sensors & analytics |

| Chromatography & purification columns |

| Sampling & aseptic transfer systems |

| Other niche components |

| Upstream processing |

| Downstream processing |

| Ancillary operations (formulation, fill-finish) |

| Biopharmaceutical companies |

| Academic & research institutes |

| Contract development & manufacturing organisations (CDMOs) |

| Clinical scale |

| Commercial scale |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Single-use bioreactors | |

| Filtration assemblies | ||

| Media bags & containers | ||

| Mixers & blenders | ||

| Tubing & connectors | ||

| Single-use sensors & analytics | ||

| Chromatography & purification columns | ||

| Sampling & aseptic transfer systems | ||

| Other niche components | ||

| By Workflow Stage | Upstream processing | |

| Downstream processing | ||

| Ancillary operations (formulation, fill-finish) | ||

| By End User | Biopharmaceutical companies | |

| Academic & research institutes | ||

| Contract development & manufacturing organisations (CDMOs) | ||

| By Scale | Clinical scale | |

| Commercial scale | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the single-use bioprocessing market expected to grow between 2026 and 2031?

It is forecast to expand at a 14.2% CAGR, rising from USD 33.03 billion in 2026 to USD 64.12 billion by 2031.

Which region will register the highest growth?

Asia-Pacific is projected to post the fastest pace at 15.42% CAGR through 2031, driven by Chinese and Indian capacity additions.

What product line is growing quickest?

Disposable sensors and analytics are set to increase at a 16.25% CAGR, propelled by AI-enabled control requirements.

Why are CDMOs adopting single-use platforms rapidly?

Serving many clients demands fast changeovers, and single-use assemblies replace multi-day cleaning with quick bag swaps, enabling a 14.82% CAGR for CDMOs.

What is the main supply-chain risk?

Tight availability of medical-grade polymer film, highlighted by an eight-week shortage after a 2025 European plant fire, has led suppliers to seek vertical integration.

How are regulators influencing adoption?

FDA and EMA guidance in 2024-2025 explicitly support validated disposable replacements for stainless steel, removing prior comparability study hurdles.