Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

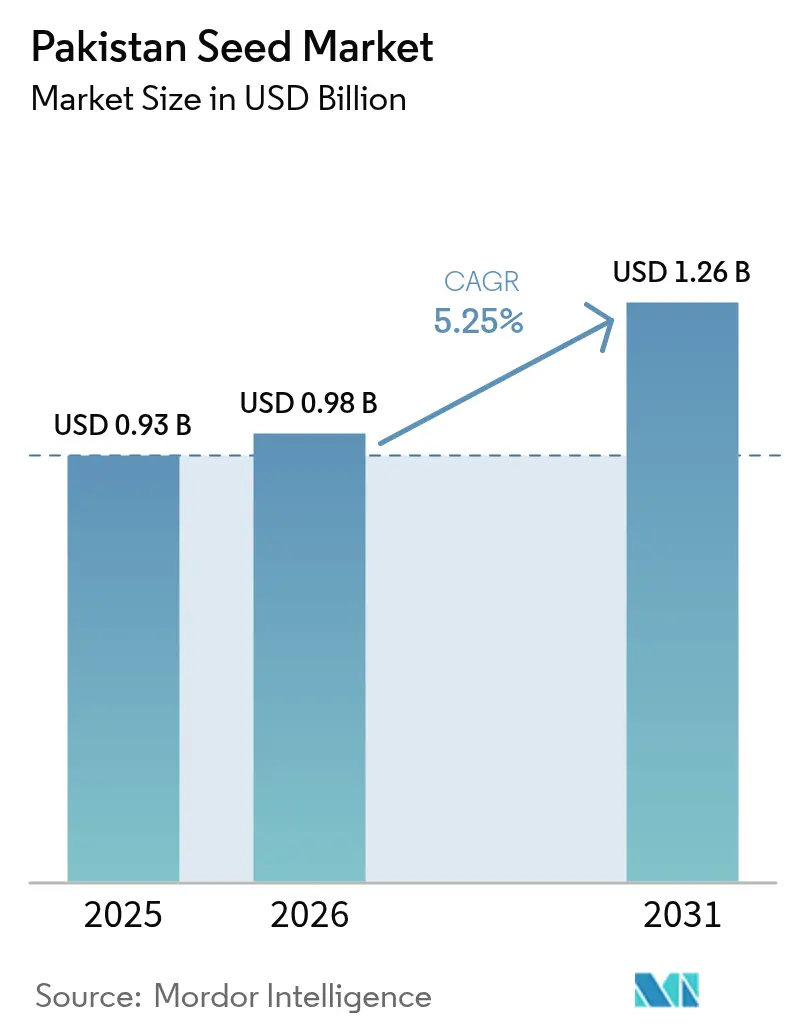

| Base Year Market Size (2025) | USD 0.93 Billion |

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 1.26 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Pakistan Seed Market Analysis by ���ϲ�����

The Pakistan seed market size is projected to expand from USD 0.93 billion in 2025 and USD 0.98 billion in 2026 to USD 1.26 billion by 2031, registering a 5.25% CAGR over 2026-2031. Rapid adoption of hybrid rice, stricter enforcement of seed quality standards, and the spread of drip irrigation underpin this growth. Branded demand concentrates in Punjab, yet Khyber Pakhtunkhwa posts the quickest gains as ag-fintech credit unlocks smallholder purchasing power. Currency swings and biotech IP gaps continue to weigh on multinational margins, although localized breeding and tissue-culture investments temper import exposure. The Pakistan seed market now pivots on traceability tools and corporate-farming contracts that bypass fragmented retail networks.

Key Report Takeaways

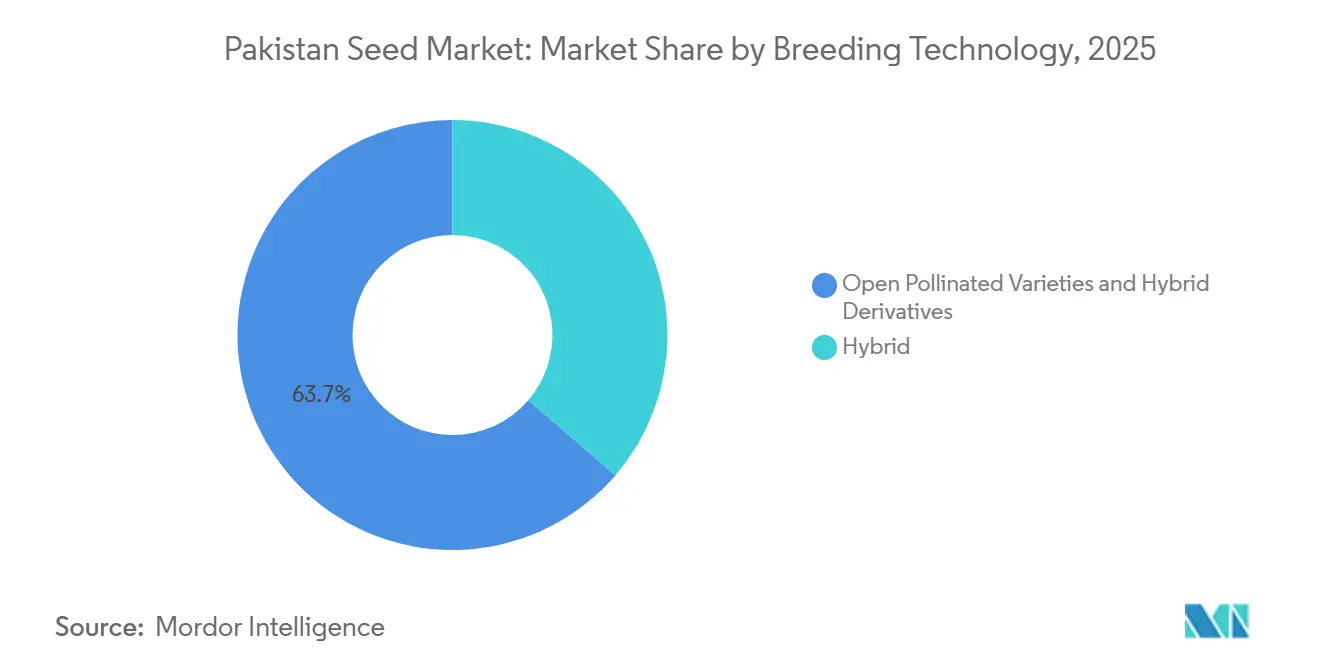

- By breeding technology, open-pollinated varieties and hybrid derivatives held 63.7% of Pakistan seed market share in 2025 and also posted the quickest 5.7% CAGR through 2031.

- By cultivation mechanism, open-field farming accounted for 99.9% of Pakistan seed market size in 2025, whereas protected cultivation is projected to expand at an 8.6% CAGR.

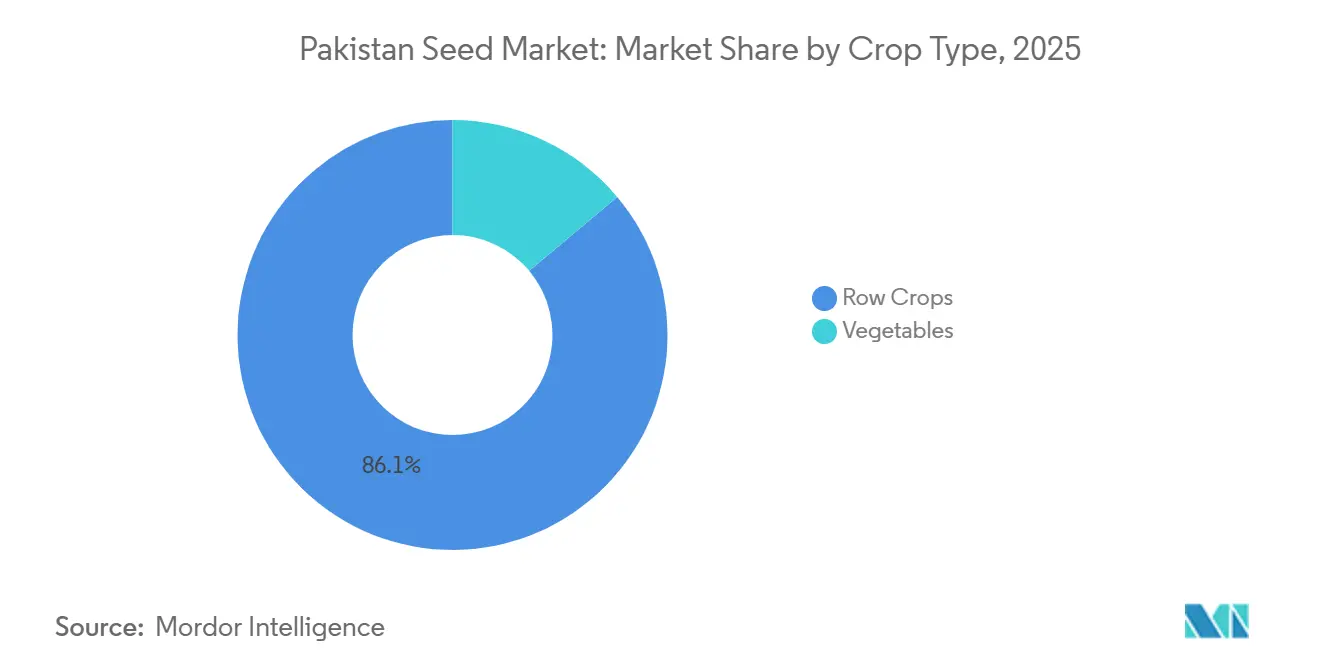

- By crop type, row crops accounted for 86.10% of Pakistan seed market share in 2025 sales and remain the fastest-growing at a 5.5% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Pakistan Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of hybrid rice varieties | +1.2% | Punjab, Sindh, and southern Khyber Pakhtunkhwa | Medium term (2–4 years) |

| Government seed-certification reforms | +0.9% | National | Short term (≤ 2 years) |

| Expansion of high-efficiency drip-irrigation acreage | +0.7% | Sindh and southern Punjab | Medium term (2–4 years) |

| Corporate-farming projects in Sindh and Punjab | +0.8% | Sindh and Punjab | Long term (≥ 4 years) |

| Climate-resilient-seed Research and Development funding spike post-2023 floods | +0.6% | Flood‑prone Sindh and southern Punjab | Long term (≥ 4 years) |

| Rise of ag-fintech seed-bundle financing | +0.5% | Punjab and Khyber Pakhtunkhwa | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Rapid Adoption of Hybrid Rice Varieties

In 2024, 12 new hybrids were approved by the National Seed Council, formulated to deliver 30 to 40% yield gains over older International Rice Research Institute (IRRI) and Basmati lines, resulting in a significant rise in seed replacement in 2025[1]Source: Pakistan Agricultural Research Council, “Hybrid Rice Trials 2024,” parc.gov.pk. Growers in Sindh switched acreage from aromatic Basmati to short-duration hybrids that preserve groundwater and meet European residue limits. Bayer and Corteva bundled seed with precision-planting guides, reducing waste by 12% on saline soils. The Pakistan seed market, therefore, sees a clear volume uplift as mid-sized farms under 25 acres transition. Counterfeiting still clips 15% of sales, yet regulatory audits in key districts are gradually closing those gaps.

Government Seed-Certification Reforms

The 2024 Seed Amendment Act unified federal and provincial oversight under the National Seed Development and Regulatory Authority (NSDRA), halving varietal-approval times to 18 months. Blockchain-based traceability now tracks lots from breeder plots to retail counters, enabling March 2025 raids that eliminated 4,200 metric tons of fake seed. Faster import permit clearance opened the door to new climate-ready maize and sunflower hybrids. Certified sales jumped significantly during the 2025 kharif window, cementing trust among growers who had previously been wary of mislabeled bags. The uplift is strongest in the first two years while the enforcement staffings ramp up.

Expansion of High-Efficiency Drip-Irrigation Acreage

In 2025, the drip systems covered around 0.68 million acres, up from 0.45 million in 2023, mostly in Sindh’s peri-urban belts and southern Punjab[2]Source: Pakistan Council of Research in Water Resources, “Drip Irrigation Status 2025,” pcrwr.gov.pk . Vegetable growers report water savings of nearly 45% and yield increases of more than 30%, driving demand for hybrids selected for low-pressure fertigation. Syngenta and East-West launched early-maturing tomato hybrids in 2025, doubling the frequency of annual seed orders. An Asian Development Bank-backed subsidy covers 50% of hardware costs, accelerating uptake among plots of 50 acres or less. Momentum should persist until 2028 as the pipeline widens to include chilies and cucumbers.

Corporate-Farming Projects in Sindh and Punjab

Contiguous holdings beyond 1,000 acres grew from 180,000 to 265,000 acres by 2025 after Gulf-funded leases in Tharparkar and Cholistan[3]Source: Pakistan Council of Research in Water Resources, “Drip Irrigation Status 2025,” pcrwr.gov.pk . Firms pre-specify purity and germination thresholds in bulk contracts, shifting 18% of national seed flows from shops to direct B2B channels. Seed-replacement cycles shrink to a single season because corporate agronomists prize uniformity over thrift. Big orders already locked in alfalfa and sunflower hybrids from Guard and Advanta. As land consolidation extends into Balochistan, the Pakistan seed market adds another durable growth lane.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High post-harvest losses reducing effective seed demand | −0.8% | Sindh and Balochistan | Medium term (2–4 years) |

| Counterfeit seed trade via informal channels | −1.0% | Rural Punjab, Sindh, and Khyber Pakhtunkhwa | Short term (≤ 2 years) |

| Limited domestic biotech IP protection | −0.6% | National | Long term (≥ 4 years) |

| Currency volatility inflating imported germplasm costs | −0.7% | National | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

High Post-Harvest Losses Reducing Effective Seed Demand

Grain and oilseed losses hover near 30% because storage remains rudimentary for most smallholders. Wheat alone lost 3.2 million metric tons in 2025, shrinking cash for Rabi seed purchases by almost one-fifth. Only 1.8 million metric tons of modern silo capacity covers 7% of national output, keeping farmers reliant on mud bins that attract rodents and fungus. Similar spoilage in Sindh rice mills cuts growers’ net returns PKR 8,000-12,000 (USD 28-43) per acre, dampening hybrid uptake. Until cold-chain and silo builds catch up, disposable seed budgets remain stressed.

Counterfeit Seed Trade via Informal Channels

Roughly one-third of seed volume still moves through unlicensed dealers who dilute hybrids with grain, slashing yields 25-35%. The March 2025 National Seed Development and Regulatory Authority (NSDRA) crackdown purged many outfits, yet later audits found that 18% of lots in Swat and Dir still failed to meet germination norms. Informal vendors lure growers with doorstep credit where bank coverage is thin. Bayer and Corteva printed QR codes on every bag and trained 1,500 retailers, but user scanning rates stay patchy. Counterfeiting, therefore, cuts the Pakistan seed market growth baseline by a full 1%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology – Certified Seed Gains Ground

Open-pollinated varieties and hybrid derivatives accounted for 63.7% of Pakistan seed market size in 2025 and are simultaneously projected to post the highest 5.7% CAGR through 2031, reflecting the pull of tighter certification and subsidy programs that steer growers away from farm-saved grain. Farmers now equate the certification stamp with predictable germination and stronger market prices, so replacement cycles shorten and volume compounds quickly. Extension agents continue to showcase side-by-side yield gains, deepening confidence in this category. This unusual pairing of scale and speed makes it the focal point for supplier investment and government oversight.

The remaining share falls under the broader hybrids segment, which, although smaller, sustains steady uptake where heterosis delivers clear yield benefits. Hybrid penetration advances most in maize and rice belts, where profitability hinges on input efficiency, yet the category’s overall growth pace trails that of the certified open-pollinated leader. Suppliers keep hybrids in their pipeline to hedge demand across varying farm sizes and capital constraints. Even at slower expansion, hybrids ensure portfolio balance and continuous technology transfer to the market.

By Cultivation Mechanism – Protected Systems Gain Momentum

Open-field systems retained near-total dominance, accounting for 99.9% of Pakistan seed market share in 2025 sales, because Pakistan’s fragmented small-farm structure still relies on traditional irrigation and broad-acre staples. Millions of farms spread across Punjab and Sindh guarantee consistent throughput for thousands of seed dealers, keeping per-acre costs modest while maintaining high aggregate volumes. This entrenched base locks in supplier revenue and underpins national food security. Consequently, open-field cultivation remains the cornerstone that stabilizes industry cash flow year after year.

Protected cultivation, while tiny today, is on track for an 8.6% CAGR from 2026 to 2031 as greenhouse vegetables multiply around urban centers where water scarcity and land prices justify intensive production. Growers pay several times more per acre for greenhouse-grade hybrid seed, lifting vendor margins and encouraging product specialization. Provincial tunnel subsidies and drip irrigation financing accelerate adoption in Sindh and Punjab's peri-urban belts. Continued policy support and localized breeding could elevate this niche into a meaningful revenue stream over the next decade.

By Crop Type – Row Crops Anchor Demand

Row crops accounted for 86.1% of 2025 seed revenue and are also projected to expand at the fastest 5.5% CAGR from 2026 to 2031, confirming their dominant place in Pakistan’s food and feed system. Large wheat, rice, cotton, and maize acreages keep dealer networks active year-round and ensure high seed-replacement volumes. Government procurement floors for staples and corporate contracting in hybrid maize smooth demand cycles, making row crops both a scale anchor and a growth engine. Ongoing varietal refresh aimed at drought and heat resilience further secures this segment’s momentum through the forecast window.

Vegetables held the remaining market share in 2025 and are set to grow at a decent CAGR through 2031, as protected-cultivation clusters spread around major cities. Greenhouse operators pay premium prices for hybrid tomato and chili seed, which helps vendors offset the segment’s smaller land base. Urban diet shifts and wholesale quality standards drive steady uptake of uniform, disease-resistant varieties. While vegetables cannot match the acreage of row crops, they provide profitable diversification that reduces the industry’s dependence on broad-acre staples.

Geography Analysis

Punjab remains the anchor of national seed demand, accounting for a major share of Pakistan seed market in 2025, as its 6.5 million hectares of wheat, rice, and maize ensure deep dealer networks and strong certified seed uptake. Corporate farms in the Cholistan and Bahawalpur belts keep bulk contracts flowing, while the Punjab Seed Council’s ongoing enforcement actions continue to boost farmer trust in branded labels. Khyber Pakhtunkhwa is the fastest-expanding province, advancing at a rapid CAGR through 2031 on the back of rising hybrid-maize acreage and the rapid adoption of smartphone-based credit, which lowers entry barriers for smallholders. Together, these two provinces shape near-term volume trends while setting benchmarks for regulatory compliance and fintech integration.

Sindh follows as the second-largest contributor, driven by 1.2 million hectares of cotton, 1.1 million hectares of rice, and a greenhouse cluster that supplies Karachi’s wholesale markets. Hybrid rice approvals and drip-irrigated vegetables keep the province’s growth above the national average, even though illicit Bt cotton seed tempers gains for branded suppliers. Balochistan contributes a smaller base but registers steady improvement as orchard regeneration and solar-heated greenhouses in the Quetta valley lift demand for virus-free potato and protected-vegetable seed. These regions collectively diversify geographic risk and expand the addressable customer base beyond the core Punjab heartland.

Looking ahead, provincial investment in traceability systems, cold-chain upgrades, and high-efficiency irrigation is set to unlock fresh pockets of seed demand across all territories. Punjab will likely retain leadership due to scale advantages, yet its incremental growth hinges on continued corporate-farming expansion and stricter counterfeit enforcement. Khyber Pakhtunkhwa’s sustained rise depends on extending ag-fintech platforms into hilly districts and rolling out flood-tolerant wheat lines tailored for river valleys. Sindh and Balochistan can accelerate further by pairing greenhouse subsidies with localized breeding, ensuring that regional opportunities converge to uphold the national market’s mid-single-digit trajectory.

Competitive Landscape

The combined top five suppliers control the majority of Pakistan seed market share, underscoring a moderate yet defensible level of concentration. The competitive field is led by Bayer AG and Corteva Agriscience, both of which anchor the hybrid-seed segment through strong maize and rice portfolios and nationwide dealer footprints. Bayer AG leverages its FarmRise mobile platform to deliver precision-planting advice that boosts germination rates and drives repeat purchases. Corteva Agriscience matches that reach with 240 field agronomists who stage on-farm demonstrations and bundle credit through the Kissan Card program to lower adoption hurdles for smallholders.

Syngenta Group, Advanta Enterprises Limited (UPL Group), and Guard Agricultural Research & Services (Pvt.) Limited rounds out the leading cohort with differentiated strengths that keep competitive pressure high. Syngenta Group widens its vegetable catalog after acquiring a local tomato-and-chili breeder, giving greenhouse growers virus-resistant choices. Advanta Enterprises Limited (UPL Group) localizes maize parent lines through a new Faisalabad breeding station, shortening product-release cycles while hedging foreign-exchange risk. Guard Agricultural Research & Services (Pvt.) Limited builds on its rice-export pedigree to branch into forage and oilseeds, using deep provincial relationships to secure corporate-farm contracts.

Future gains hinge on how quickly these companies embed digital traceability, climate-resilient traits, and tailored financing in their go-to-market playbooks. Bayer AG and Corteva Agriscience plan to expand research and development spending on nutrient-efficient hybrids that address rising fertilizer costs, while scaling QR-code authentication to curb counterfeit flows in outlying districts. Syngenta Group is anticipated to leverage global gene-editing pipelines once plant-variety protection laws mature, positioning itself for higher-value trait launches. Domestic leaders such as Guard Agricultural Research & Services (Pvt.) Limited and Four Brothers Group can lift share by pairing localized genetics with fintech partnerships, ensuring that competitive intensity remains healthy even as overall market growth steadies in the mid-single digits.

Pakistan Seed Industry Leaders

Bayer AG

Advanta Enterprises Limited (UPL Group)

Guard Agricultural Research & Services (Pvt.) Limited

Syngenta Group

Corteva Agriscience

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: The Punjab government began distributing 400,000 free packets of vegetable seed to farmers in flood-hit districts to accelerate re-cultivation and strengthen provincial food security.

- June 2025: HBL Zarai Services Limited and Bayer Pakistan signed a strategic memorandum of understanding to widen smallholder access to certified seed, crop-protection products, and field advisory through the Zarai Deras and Zarai Dost retail networks.

- February 2025: The Punjab Seed Council approved 16 new crop varieties, including five wheat, five cotton, and six rice, during its 60th meeting in Lahore, indicating a quicker genetic update for key staple crops.

Pakistan Seed Market Report Scope

A Seed is the small, hard part of a plant from which a new plant of the same kind can grow. The study includes commercial seeds for sowing for various crop categories, including grains and cereals, vegetables, and oilseeds.

The report on the Pakistan Seed Market presents a comprehensive analysis based on product type, covering transgenic, non-transgenic, and open-pollinated seeds, as well as crop type, including grains and cereals, oilseeds, vegetables, and other seeds. It delivers market-size estimates and future projections for each segment, expressed in value USD and volume in metric tons.

By Breeding Technology

| Hybrids | Transgenic Hybrids |

| Non-Transgenic Hybrids | |

| Open Pollinated Varieties and Hybrid Derivatives |

By Cultivation Mechanism

| Open Field |

| Protected Cultivation |

By Crop Type

| By Vegetables | Solanaceae | Tomato |

| Chilli | ||

| Eggplant | ||

| Other Solanaceae | ||

| Cucurbits | Cucumber and Gherkin | |

| Pumpkin and Squash | ||

| Other Cucurbits | ||

| Brassicas | Carrot | |

| Cabbage | ||

| Cauliflower and Broccoli | ||

| Other Brassicas | ||

| Roots and Bulbs | Onion | |

| Garlic | ||

| Potato | ||

| Other Roots and Bulbs | ||

| Unclassified Vegetables | Okra | |

| Lettuce | ||

| Peas | ||

| Spinach | ||

| Other Unclassified Vegetables | ||

| By Row Crops | Grains and Cereals | Rice |

| Corn | ||

| Wheat | ||

| Sorghum | ||

| Other Grains and Cereals | ||

| Pulses | ||

| Oilseeds | Sunflower | |

| Canola, Rapeseed and Mustard | ||

| Other Oilseeds | ||

| Fiber Crops | Cotton | |

| Other Fiber Crops | ||

| Forage Crops | Alfalfa | |

| Forage Corn | ||

| Forage Sorghum | ||

| Other Forage Crops | ||

| By Breeding Technology | Hybrids | Transgenic Hybrids | |

| Non-Transgenic Hybrids | |||

| Open Pollinated Varieties and Hybrid Derivatives | |||

| By Cultivation Mechanism | Open Field | ||

| Protected Cultivation | |||

| By Crop Type | By Vegetables | Solanaceae | Tomato |

| Chilli | |||

| Eggplant | |||

| Other Solanaceae | |||

| Cucurbits | Cucumber and Gherkin | ||

| Pumpkin and Squash | |||

| Other Cucurbits | |||

| Brassicas | Carrot | ||

| Cabbage | |||

| Cauliflower and Broccoli | |||

| Other Brassicas | |||

| Roots and Bulbs | Onion | ||

| Garlic | |||

| Potato | |||

| Other Roots and Bulbs | |||

| Unclassified Vegetables | Okra | ||

| Lettuce | |||

| Peas | |||

| Spinach | |||

| Other Unclassified Vegetables | |||

| By Row Crops | Grains and Cereals | Rice | |

| Corn | |||

| Wheat | |||

| Sorghum | |||

| Other Grains and Cereals | |||

| Pulses | |||

| Oilseeds | Sunflower | ||

| Canola, Rapeseed and Mustard | |||

| Other Oilseeds | |||

| Fiber Crops | Cotton | ||

| Other Fiber Crops | |||

| Forage Crops | Alfalfa | ||

| Forage Corn | |||

| Forage Sorghum | |||

| Other Forage Crops | |||

Key Questions Answered in the Report

What is the projected size of the Pakistan seed market from 2026 to 2031?

The Pakistan seed market is anticipated to reach USD 0.98 billion in 2026 and is forecast to grow to USD 1.26 billion by 2031.

What crop segment is growing the fastest?

Row Crops are projected to grow at a CAGR of 5.5% through 2031.

Why are hybrid rice varieties being adopted so quickly?

The 30% to 40% higher yield and shorter maturity periods help farmers address water scarcity and reduce labor costs, leading to increased adoption among farmers.

How is counterfeit seed being reduced?

The National Seed Development and Regulatory Authority (NSDRA) has shut down 392 unlicensed firms and, with the rising adoption of QR code authentication, has removed up to 40% of fake products from formal channels.

Page last updated on: