Seaweed Protein Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

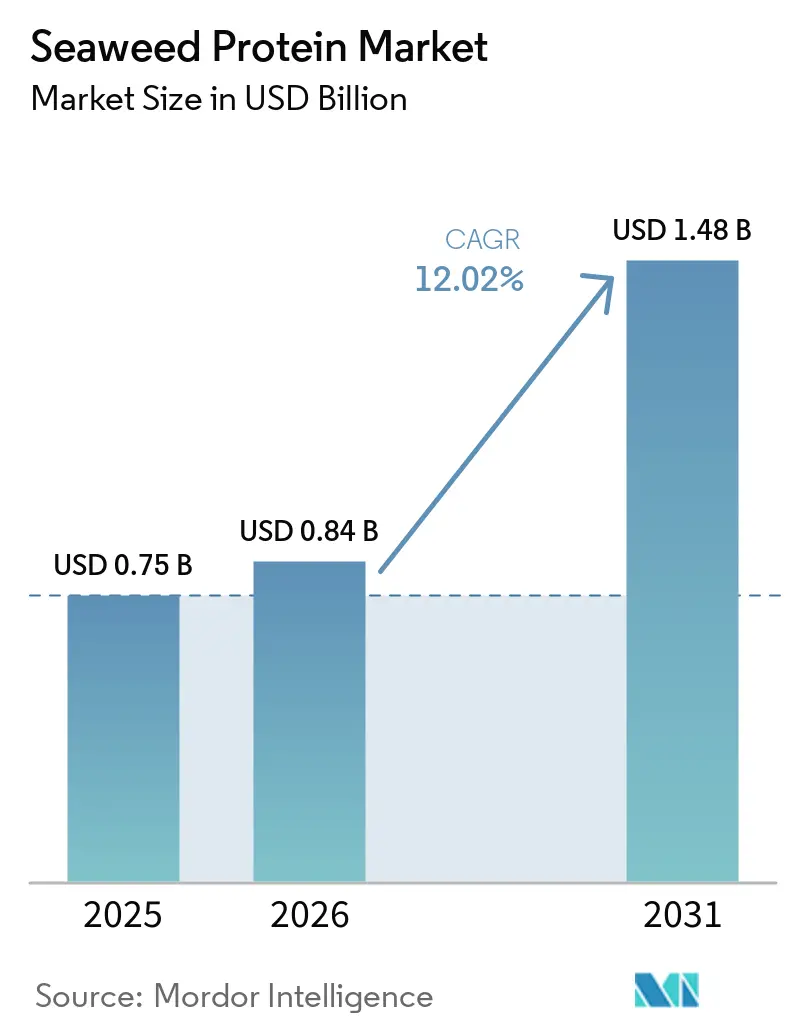

| Market Size (2026) | USD 0.84 Billion |

| Market Size (2031) | USD 1.48 Billion |

| Growth Rate (2026 - 2031) | 12.02% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Seaweed Protein Market Analysis by ���ϲ�����

The Seaweed Protein Market size was valued at USD 0.75 billion in 2025 and is estimated to grow from USD 0.84 billion in 2026 to reach USD 1.48 billion by 2031, at a CAGR of 12.02% during the forecast period (2026-2031). Seaweed proteins contain up to 32% protein content by dry weight and require minimal environmental resources for production, including no freshwater, fertilizers, or arable land. The market growth is driven by advances in cultivation and extraction technologies, such as improved bioreactor systems and enzymatic processes, that improve protein yields by 40-50% compared to conventional extraction methods. These technological developments have enabled manufacturers to produce high-quality seaweed protein concentrates and isolates suitable for various food and beverage applications.

Key Report Takeaways

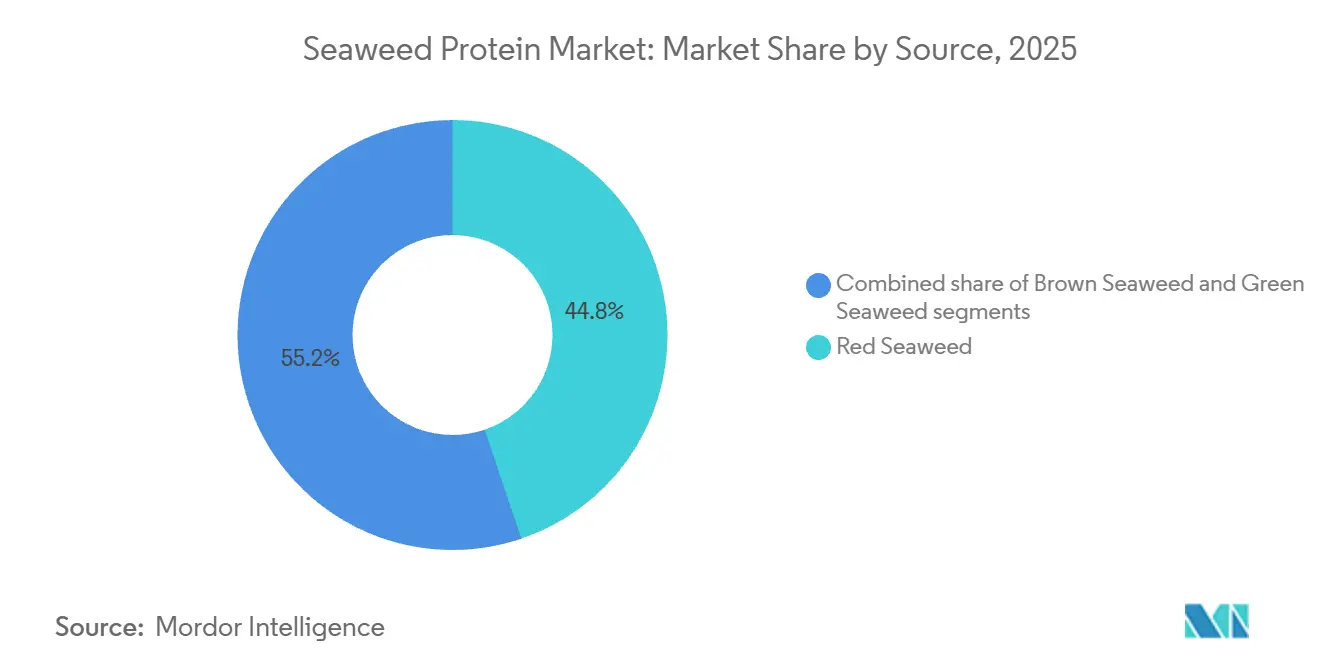

- By source, red seaweed holds the largest share in the seaweed protein market at 44.81% in 2025, while green seaweed is expected to grow at a CAGR of 12.67% during the forecast period through 2031.

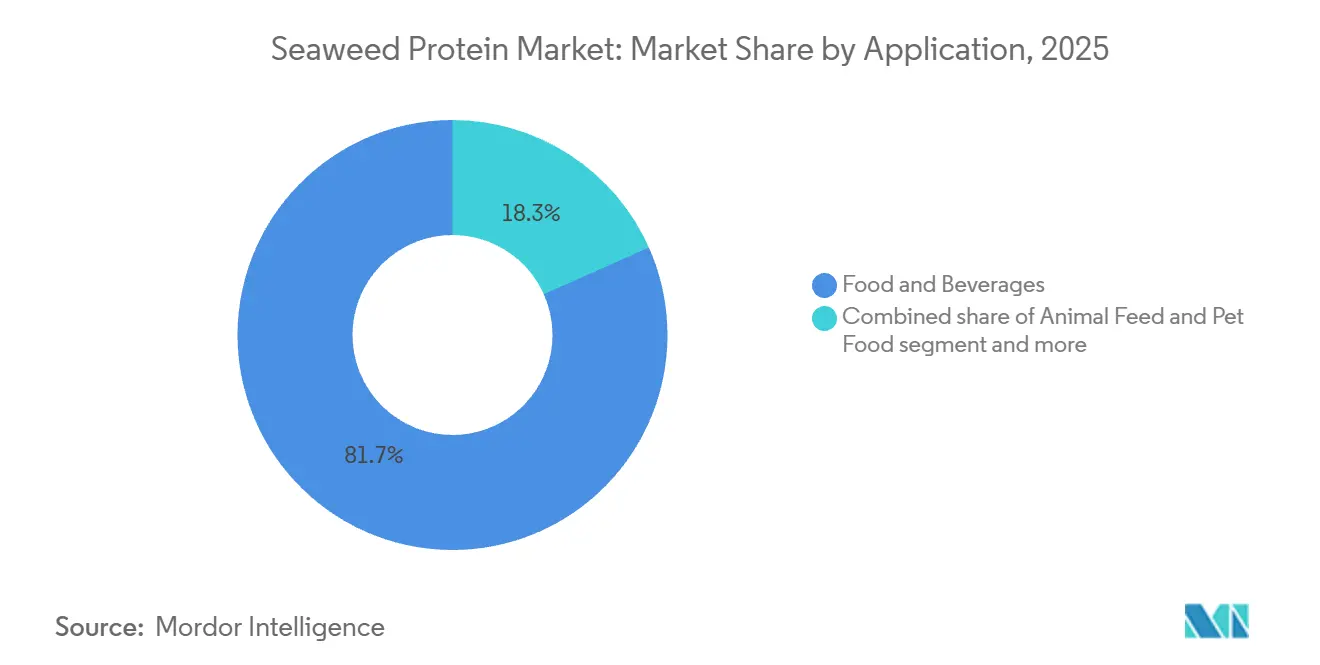

- By application, food and beverages held 81.67% share of the seaweed protein market size in 2025, while personal care and cosmetics are projected to register a 12.98% CAGR between 2026 and 2031.

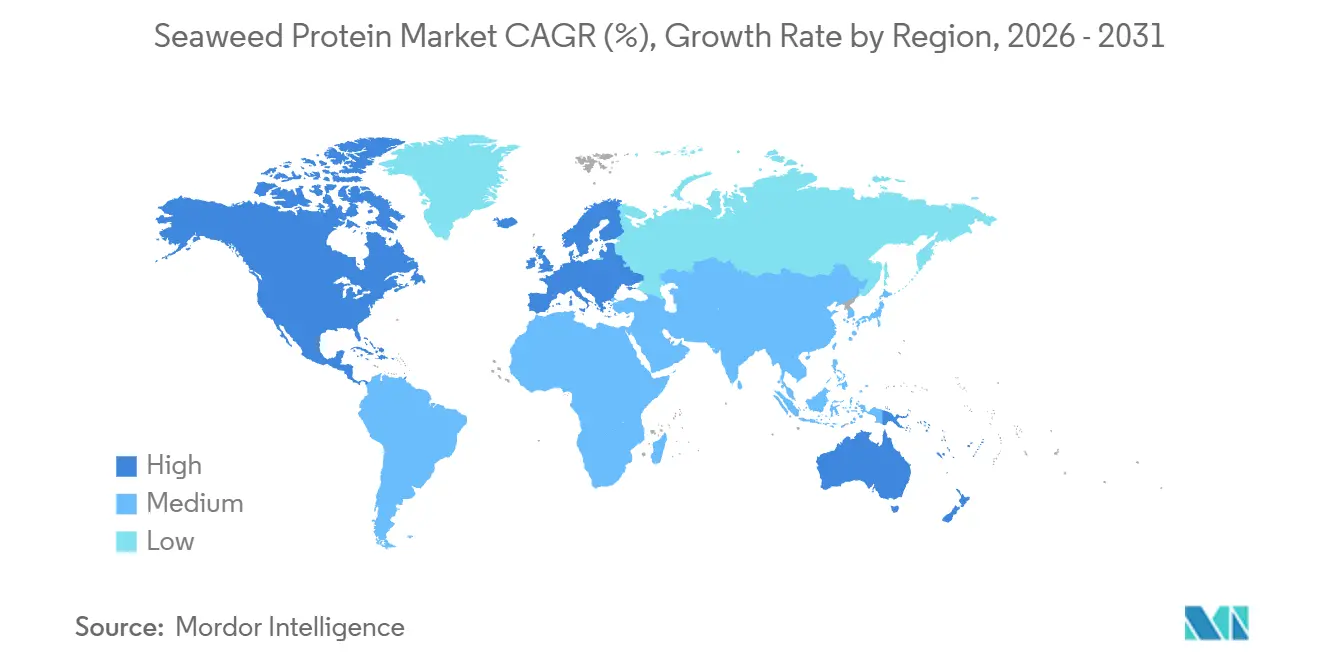

- By geography, Asia-Pacific led with 61.55% share in 2025, and North America is forecast to deliver a 13.88% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Seaweed Protein Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancements in extraction technologies improve seaweed's yield and functionality | +2.1% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Rising applications in convenience foods, health drinks, and processed products | +2.8% | Global, strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Shift to natural ingredients in cosmetics for bioactive and moisturizing properties | +1.9% | North America, Europe, and premium segments in Asia-Pacific | Medium term (2-4 years) |

| Increased use of seaweed in functional foods and nutraceuticals for nutrition | +1.7% | Global, with concentration in North America and Japan | Medium term (2-4 years) |

| Growing awareness of seaweed's health benefits, including immune support, blood sugar regulation, and antioxidants | +1.5% | Asia-Pacific core, expanding to North America and Europe | Long term (≥ 4 years) |

| Rising demand for plant-based proteins due to vegan, vegetarian, and flexitarian diets | +2.3% | North America and Europe, spillover to urban Asia-Pacific | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Advancements in Extraction Technologies Improve Seaweed's Yield and Functionality

Ultrasound-assisted and enzyme-assisted extractions are replacing traditional solvent methods, reducing processing times from 4 hours to 90 minutes and increasing polysaccharide recovery by 25% to 40%. Combined ultrasound-enzyme protocols (20-50 kHz, 100-500 W/cm², 15-60 minutes) break down cell walls more effectively than thermal hydrolysis, preserving heat-sensitive bioactives like fucoxanthin and phlorotannins, which degrade above 60°C. In March 2026, Marine Biologics introduced SeaTex, an AI-designed brown seaweed powder with FDA GRAS status. It replaces carrageenan, xanthan gum, and methylcellulose, simplifying plant-based meat formulations. Smaller processors in Indonesia and Vietnam are adopting modular ultrasound units under USD 50,000, enabling premium-grade carrageenan production for European dairy-alternative brands without the USD 2 million cost of spray-drying towers. This trend is fragmenting supply chains and reducing the pricing power of traditional hydrocolloid suppliers who cannot match the bioactive profiles of enzyme-assisted methods.

Rising Applications in Convenience Foods, Health Drinks, and Processed Products

Seaweed extracts are moving from niche health-food aisles to mainstream products as formulators seek clean-label hydrocolloids with familiar ingredient names. Carrageenan from red seaweed stabilizes protein in oat and almond milks without the chalky texture of guar or locust bean gums, supporting the growing dairy-alternative market, which surpassed USD 3 billion in North America in 2025. Aqua Theon launched OoMee functional beverages in May 2025, using seaweed extracts for sustained energy. The product sold over 100,000 units in six months across 700 stores, including Sprouts, Raley's, and Bristol Farms. Alginate from brown seaweed is replacing modified starches in bakery and confectionery products due to its better freeze-thaw tolerance, benefiting frozen dessert makers facing grain supply issues. Clean-label trends and demand for functional benefits are driving seaweed extracts into products that previously used synthetic stabilizers.

Shift to Natural Ingredients in Cosmetics for Bioactive and Moisturizing Properties

Cosmetic brands are increasingly using seaweed-derived actives for hydration and barrier repair, avoiding parabens and silicones. Macro Oceans' Big Kelp Hydration, validated by an MS Clinical Research study, showed an 80% immediate hydration boost and a 26% improvement in skin-barrier function after 28 days, outperforming hyaluronic acid in water-loss tests. Fucoidan and fucoxanthin from brown seaweed slow collagen breakdown and reduce wrinkle depth by 12% to 18%, as confirmed by 8-week trials in independent dermatology labs. In April 2026, Pure Ocean Algae launched a Palmaria palmata-based nutraceutical line for hair, nails, cognition, and hormone balance in Ireland and the UK, with plans to expand to the EU and Asia later in 2026. The demand for bioactive seaweed extracts is rising as consumers value their sustainability and effectiveness, enabling brands to charge 20% to 30% more than petroleum-based alternatives.

Increased Use of Seaweed in Functional Foods and Nutraceuticals for Nutrition

Seaweed, packed with micronutrients and prebiotic polysaccharides, is becoming a key ingredient in functional foods for metabolic health and gut microbiome support. Fucoxanthin from brown seaweed improves insulin sensitivity and reduces post-meal glucose spikes by activating uncoupling protein 1 in fat tissue. Human trials have shown an 8% to 12% reduction in fasting blood glucose over 12 weeks. Fucoidan enhances immunity by boosting natural killer cell activity and interferon-gamma production, making it popular in immune-support supplements launching in 2024 and 2025. Pure Ocean Algae's Palmaria palmata supplements provide bioavailable iodine, iron, and B vitamins, addressing deficiencies in vegans and vegetarians without causing common side effects of synthetic supplements. Formulators are combining seaweed extracts with adaptogens and nootropics to create multi-benefit blends for flexitarian consumers seeking plant-based alternatives to fish oil and collagen. The functional-food sector is growing faster than traditional supplements as it allows structure-function claims without strict pharmaceutical regulations.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain volatility from climate-driven crop failures | -1.8% | Asia-Pacific core, particularly Philippines, Indonesia, and Japan | Short term (≤ 2 years) |

| Regulatory and standards barriers | -0.9% | Global, with concentration in Europe and North America | Medium term (2-4 years) |

| High production and processing costs | -1.2% | Global, most acute in small-scale operations in developing markets | Medium term (2-4 years) |

| High iodine and heavy-metal content compliance costs | -1.0% | Europe and North America, spillover to export-oriented Asia-Pacific | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Supply-Chain Volatility from Climate-Driven Crop Failures

Extreme weather and rising ocean temperatures are disrupting seaweed farming in tropical and temperate regions, leading buyers to source from multiple locations and face higher costs. In 2024 and 2025, the Philippines faced severe ice-ice disease outbreaks in areas like Northern Samar and Central Visayas, causing up to 90% crop losses in Kappaphycus and Eucheuma due to bacterial infections triggered by warmer seas[1]Source: Food and Agriculture Organization, “The State of World Fisheries and Aquaculture 2024,” FAO.ORG. Japan's Fisheries Research and Education Agency predicts that by 2030, Undaria pinnatifida grown south of 39°N could see a 50% reduction in blade length under RCP8.5 warming scenarios. Farmers may need to move north or use heat-tolerant strains, which yield 20% less alginate per tonne. Typhoons Phanfone and Odette destroyed 15,000 hectares of seaweed farms in the Visayas, causing 6 to 9 months of revenue loss for small farmers and disrupting carrageenan supply chains for up to 18 months. Processors are now stockpiling raw materials for 60 to 90 days and contracting with farms across different regions, but these measures increase costs by 5% to 8% and squeeze margins for mid-tier converters.

High Production and Processing Costs

Seaweed extraction is expensive and energy-intensive, especially when aiming for pharmaceutical-grade purity. Installing equipment such as ultrasound extractors, enzyme reactors, and spray-drying towers costs USD 1.5 million to USD 3 million, posing challenges for smallholder cooperatives in Indonesia, the Philippines, and Tanzania, which produce 60% to 70% of global Kappaphycus and Eucheuma. Drying seaweed from 80% to 12% moisture accounts for 20% to 30% of processing costs, with fluctuating diesel and electricity prices in off-grid areas adding USD 0.40 to USD 0.60 per kilogram. The European Food Safety Authority's 2024 cadmium limit of 0.3 mg/kg for food-grade seaweed extracts requires processors to add ion-exchange purification lines, increasing costs by USD 0.15 to USD 0.25 per kilogram and limiting smaller operators' access to premium export markets[2]Source: European Food Safety Authority, “Cadmium Limits for Seaweed Ingredients,” EFSA.EUROPA.EU. Labor for harvesting and cleaning makes up 15% to 25% of costs in Asia-Pacific farms, while aging populations in Japan and South Korea are driving wages up 8% to 12% annually. These rising costs are consolidating the industry around vertically integrated players who can spread investments across multiple products and regions.

Segment Analysis

By Source: Red Seaweed Dominates Through Processing Infrastructure

In 2025, red seaweed captured 44.81% of the market, driven by carrageenan's essential role in stabilizing dairy alternatives and meat substitutes. Kappaphycus and Eucheuma species dominate cultivation in the Philippines, Indonesia, and Tanzania, producing kappa, iota, and lambda carrageenan with unique gelling and stabilizing properties for food. In April 2026, Pure Ocean Algae launched a nutraceutical line from Palmaria palmata, targeting hair, nail, cognitive, and hormone health in Ireland and the UK, with plans to expand into the EU and Asia later in 2026. Red seaweed's rich iodine, iron, and B vitamin content make it crucial for vegan supplements, though iodine variability requires strict testing to ensure safe levels. Brown seaweed, including Undaria, Saccharina, and Ascophyllum nodosum, provides alginate, fucoidan, and fucoxanthin for pharmaceuticals, cosmetics, and agriculture. In October 2024, Acadian Seaplants partnered with BASF to distribute Ascophyllum-based biostimulants.

Green seaweed is expected to grow at a 12.67% CAGR from 2026 to 2031, driven by Ulva and Chlorella's 20%-30% protein content and suitability for closed-system cultivation, which reduces contamination risks. Ulva doubles its biomass every 7 to 10 days under optimal conditions, enabling year-round production in systems that recycle aquaculture nutrients, appealing to eco-conscious brands. Chlorella, with its complete amino-acid profile and high chlorophyll content, is popular in functional beverages and beauty supplements, with its green color symbolizing plant-based authenticity. Green seaweed's lower iodine levels simplify regulatory compliance in strict markets like the EU and Japan. Growth depends on scaling closed-system cultivation to match open-ocean farming costs, with modular photobioreactors nearing cost parity as capital costs drop 15%-20% annually.

By Application: Food Dominates, Personal Care Surges on Bioactive Innovation

In 2025, food and beverages accounted for 81.67% of market demand, driven by carrageenan and alginate's roles in dairy alternatives, meat analogs, and confectionery. Marine Biologics introduced SeaTex in March 2026, a brown seaweed powder replacing synthetic hydrocolloids in plant-based meats, with FDA GRAS approval. Carrageenan ensures smooth textures in oat and almond milks, avoiding the chalky feel of guar gum, as North American dairy-alternative sales surpassed USD 3 billion in 2025. Alginate's freeze-thaw stability is crucial for frozen desserts and bakery fillings, preventing syneresis and maintaining texture during cold chain distribution. Aqua Theon's OoMee functional beverage, launched in May 2025 with seaweed extracts, sold over 100,000 units in six months across 700 stores, reflecting growing consumer interest in seaweed-based products. In animal feed and pet food, seaweed's prebiotic polysaccharides and minerals improve gut health and coat quality.

From 2026 to 2031, personal care and cosmetics are projected to grow at a 12.98% CAGR, driven by seaweed bioactives' benefits for hydration, barrier repair, and anti-aging. Macro Oceans' Big Kelp Hydration product increased hydration by 80% and improved skin-barrier function by 26% in an MS Clinical Research study, outperforming hyaluronic acid in water-loss tests. Fucoidan and fucoxanthin from brown seaweed slow collagen breakdown and reduce wrinkle depth by 12% to 18% in eight weeks. The shift to bioactive ingredients with measurable benefits, free from synthetic additives, supports 20% to 30% price premiums over petroleum-based alternatives. Seaweed extracts' link to marine sustainability appeals to clean-beauty consumers, helping brands secure premium placements in retailers like Sephora and Ulta. However, supply-chain fragmentation and inconsistent bioactive concentrations remain challenges, which vertically integrated producers address through controlled cultivation and standardized extraction methods.

Geography Analysis

In 2021, Asia-Pacific contributed 61.55% of global seaweed revenues, driven by China's 23.1 million tonnes of production, which made up 90% of East Asia's output. Of this, 12 million tonnes were used for alginate and mannitol extraction. Japan produced 50,000 tonnes of Undaria pinnatifida and 201,000 tonnes of Pyropia species but imports 80% of its seaweed due to aging farmers and shrinking coastal farms. South Korea harvested 596,000 tonnes of Saccharina, 533,000 tonnes of Pyropia, and 567,000 tonnes of Undaria, with 60%-70% used as feed for a USD 500 million abalone aquaculture industry. In January 2026, Qingdao Bright Moon launched a mannitol extraction project to improve efficiency and purity for pharmaceutical and food-grade products. The region's dominance is due to its expertise, favorable ocean conditions, and strong value chains. However, climate issues like the Philippines' ice-ice disease and Japan's warming seas are disrupting supply and raising costs.

North America is expected to grow at a 13.88% CAGR from 2026 to 2031, driven by clean-label trends, FDA GRAS approvals, and rising demand for plant-based products. Marine Biologics launched SeaTex in March 2026, featuring FDA GRAS status and AI-designed ingredients. Acadian Seaplants expanded its Cornwallis Park facility by 100,000 square feet, doubling capacity within 12 months with a CAD 1.99 million investment and a CAD 498,000 rebate. Macro Oceans raised USD 7.5 million and acquired Everything Seaweed in October 2024 to scale its Big Kelp Hydration cosmetics and enter functional foods. Limited domestic cultivation forces North America to import seaweed from Canada, Iceland, and Chile, but investments in land-based systems that recycle aquaculture and wastewater nutrients are addressing this. In Europe, strict EFSA regulations, including a 2024 cadmium limit of 0.3 mg/kg dry weight, are consolidating the market among processors with purification capabilities. South America, the Middle East, and Africa are emerging markets, with Chile supplying alginate producers and Tanzania exporting Kappaphycus to Asia.

Europe's protein market benefits from the Novel Food Status Catalogue, which authorized over 20 algae species for protein-based food applications in February 2024, reducing industry regulatory costs by EUR 10 million. The European Food Safety Authority's updated guidance, effective February 2025, streamlines protein product approvals while maintaining safety standards. OCEANIUM secured USD 2.6 million for innovative protein extraction processes in Scotland. Norwegian research demonstrates seaweed protein production's environmental advantages over Brazilian soy protein under optimal conditions.

Competitive Landscape

With a concentration score of 4 out of 10, the seaweed protein market showcases fragmented competition, hinting at potential consolidation opportunities and diverse strategic maneuvers throughout the value chain. Established players, like AlgaeCore Technologies, exemplify this trend, employing vertical integration strategies that span from cultivation and processing to distribution, notably in their production of spirulina-based salmon alternatives.

Technology differentiation stands out as a pivotal competitive edge. Companies harness AI and predictive modeling to navigate seaweed's inherent chemical variability, while Provectus Algae champions modular biomanufacturing platforms, ensuring consistent quality. Moreover, forging strategic alliances with research institutions and government bodies further bolsters their competitive stance.

Beyond conventional food applications, there's a burgeoning interest in seaweed proteins for bioplastics, pharmaceuticals, and advanced materials, sectors where their distinct properties fetch premium prices. As a testament to the market's dynamism, emerging disruptors are carving out niche segments, leveraging innovative processing technologies. Meanwhile, heightened patent activity in extraction and cultivation methods underscores a race for technological supremacy, with firms vying for proprietary edges in processing efficiency and product excellence.

Seaweed Protein Industry Leaders

Sushil Corporation

Central Pharma

MYCSA Ag, Inc.

Swaroop Agrochemical Industries

Qingdao Hiwoss Seaweed Biotechnology Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Marine Biologics commercialized SeaTex, a brown seaweed powder developed through AI-driven ingredient design that replaces carrageenan, xanthan gum, and methylcellulose in plant-based meat formulations. The product carries FDA GRAS status and simplifies ingredient decks while maintaining texture and mouthfeel in extruded and formed applications.

- January 2026: SeaForester Group completed a merger of SeaForester and Seaweed Solutions, launching a capital raise to scale offshore kelp cultivation and carbon-sequestration projects. The combined entity raised USD 1.9 million in October 2025 from WWF and Schmidt Marine and partnered with KSAT and Kongsberg Discovery in December 2025 to deploy satellite monitoring for farm managemen.

- July 2025: Provectus Algae secured USD 10.1 million in Series A funding and a USD 2.5 million Australian government grant to scale its indoor Asparagopsis cultivation system. The investment supports the company's modular biomanufacturing platform that produces 'Surf 'n' Turf' feed additive for methane reduction in livestock, targeting significant production increases for the Australian market and beyond.

- April 2025: Marine Biologics processes seaweed into functional food ingredients using predictive modeling and artificial intelligence to ensure consistent product quality.

Global Seaweed Protein Market Report Scope

| Red Seaweed |

| Brown Seaweed |

| Green Seaweed |

| Food and Beverages | Bakery and Confectionery |

| Meat Alternatives | |

| Dairy Alternatives | |

| Others | |

| Animal Feed and Pet Food | |

| Personal Care and Cosmetics | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Source | Red Seaweed | |

| Brown Seaweed | ||

| Green Seaweed | ||

| By Application | Food and Beverages | Bakery and Confectionery |

| Meat Alternatives | ||

| Dairy Alternatives | ||

| Others | ||

| Animal Feed and Pet Food | ||

| Personal Care and Cosmetics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the seaweed extract market be by 2031?

The seaweed extract market size is projected to reach USD 1.48 billion by 2031, expanding at a 12.02% CAGR from 2026 to 2031.

Which source segment is growing fastest?

Green seaweed, led by Ulva and Chlorella, is forecast to post a 12.67% CAGR through 2031, driven by demand for plant-based protein concentrates.

What is the biggest application for seaweed extracts today?

Food and beverages accounted for 81.67% of 2025 demand, supported by carrageenan and alginate adoption in dairy alternatives and meat analogs.

Which region is set to record the highest growth rate?

North America is forecast to grow at a 13.88% CAGR through 2031 as FDA GRAS approvals and clean-label trends accelerate mainstream grocery penetration.

Page last updated on: