Scopolamine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

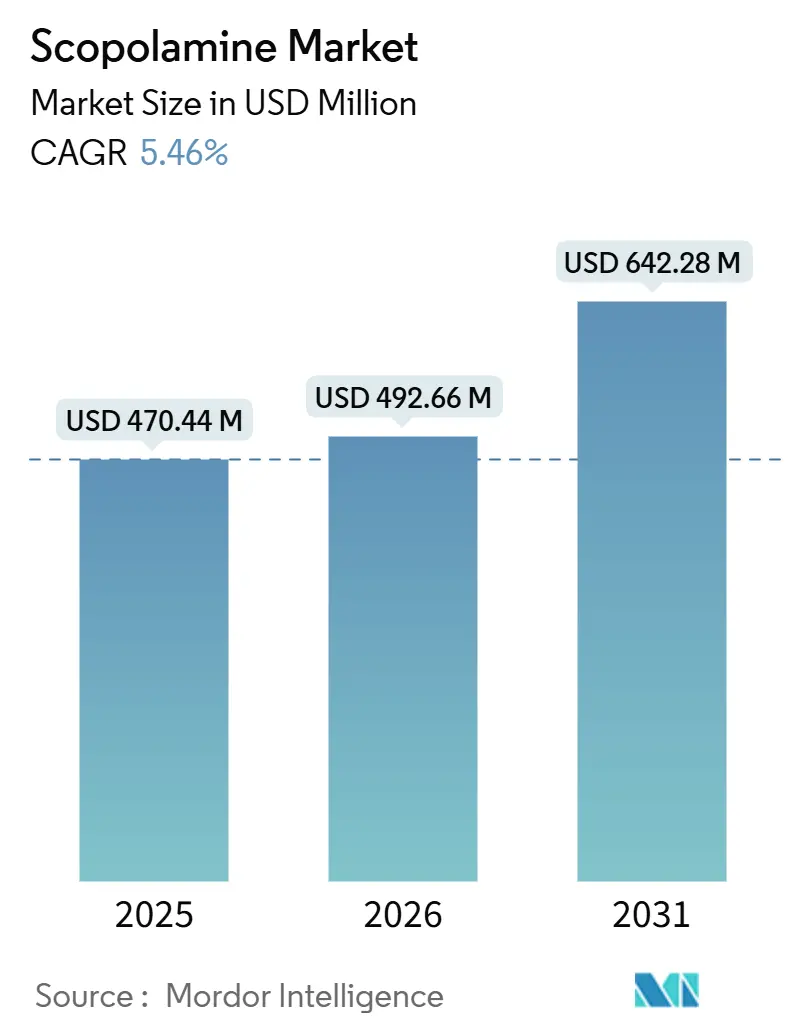

| Market Size (2026) | USD 492.66 Million |

| Market Size (2031) | USD 642.28 Million |

| Growth Rate (2026 - 2031) | 5.46% CAGR |

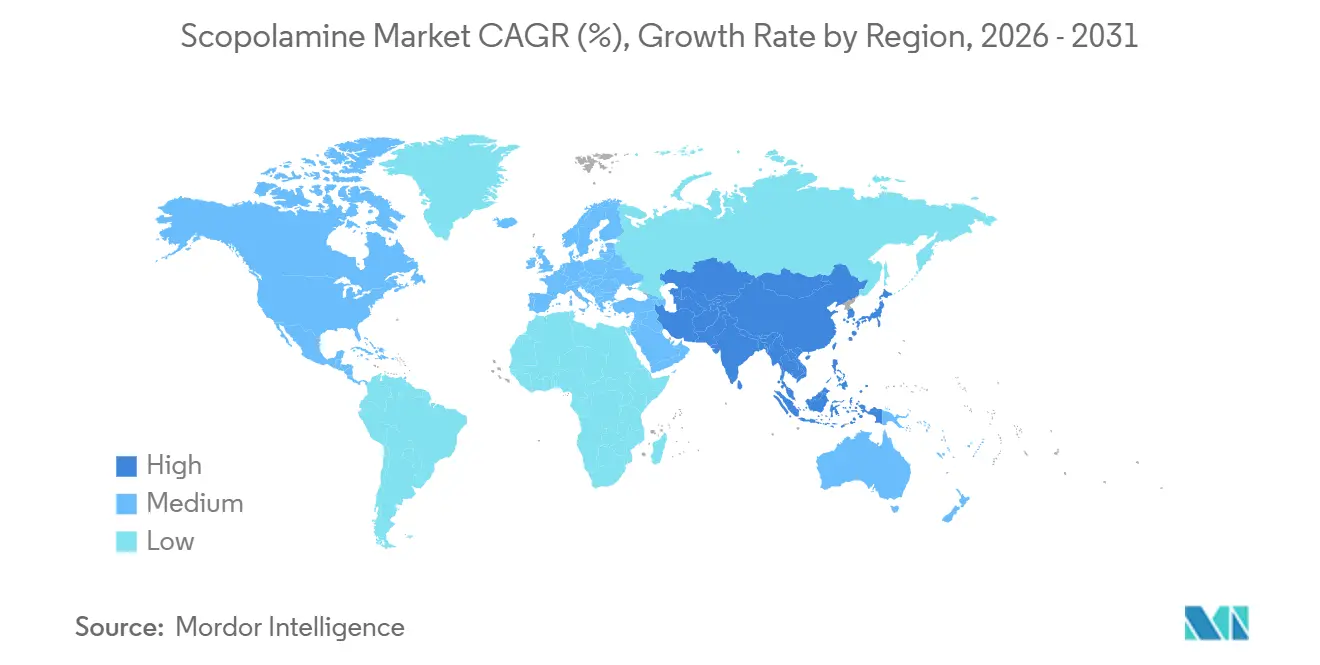

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Scopolamine Market Analysis by ���ϲ�����

The Scopolamine Market size is expected to increase from USD 470.44 million in 2025 to USD 492.66 million in 2026 and reach USD 642.28 million by 2031, growing at a CAGR of 5.46% over 2026-2031.

Steady procedure volumes, entrenched patch use in travel medicine, and fresh demand signals from space tourism offset tighter safety oversight, while API innovation cushions raw-material risk.[1]U.S. Food and Drug Administration, “FDA Adds Warning About Serious Risk of Heat-Related Complications With Antinausea Patch Transderm Scōp (Scopolamine Transdermal System),” fda.gov Manufacturers juggle hyperthermia labeling changes, accelerating generic competition, and new antiemetic rivals even as they court niche, high-value growth pockets such as virtual-reality cybersickness defense and intranasal formulations for suborbital flights. Cost-effective synthetic-biology supply lines strengthen bargaining power with formulary committees, whereas Duboisia crop volatility raises hedging costs and spurs vertical integration inside the scopolamine market. Competitive intensity rises fastest in North America where six AB-rated patches launched within nine months, compressing price corridors and forcing brand-loyal prescribers to pivot. Asia-Pacific posts the swiftest volume gains as surgical throughput climbs and tele-pharmacy channels flourish, lifting visibility for the scopolamine market across India, China, Thailand, and Singapore.

Key Report Takeaways

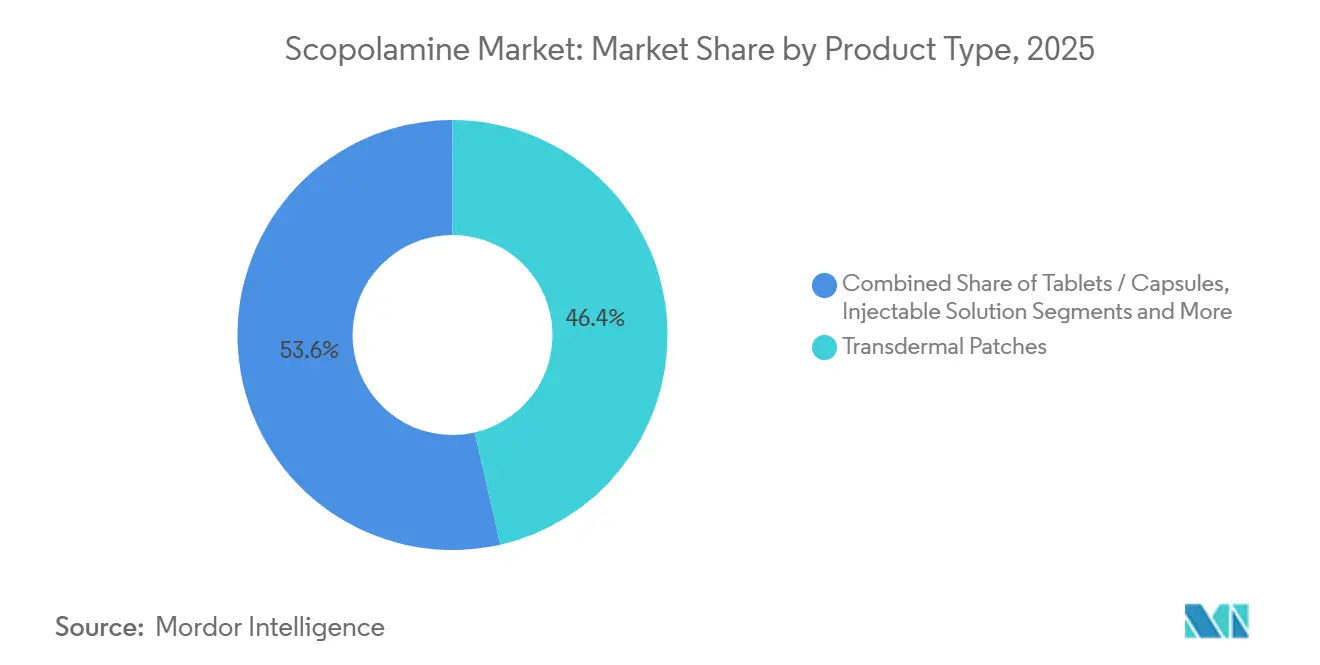

- By product type, transdermal patches led with 46.44% of scopolamine market share in 2025, whereas injectable solutions are projected to climb at a 9.37% CAGR through 2031.

- By application, motion sickness accounted for 43.83% of the scopolamine market size in 2025, while post-operative nausea and vomiting represents the fastest trajectory at an 8.22% CAGR to 2031.

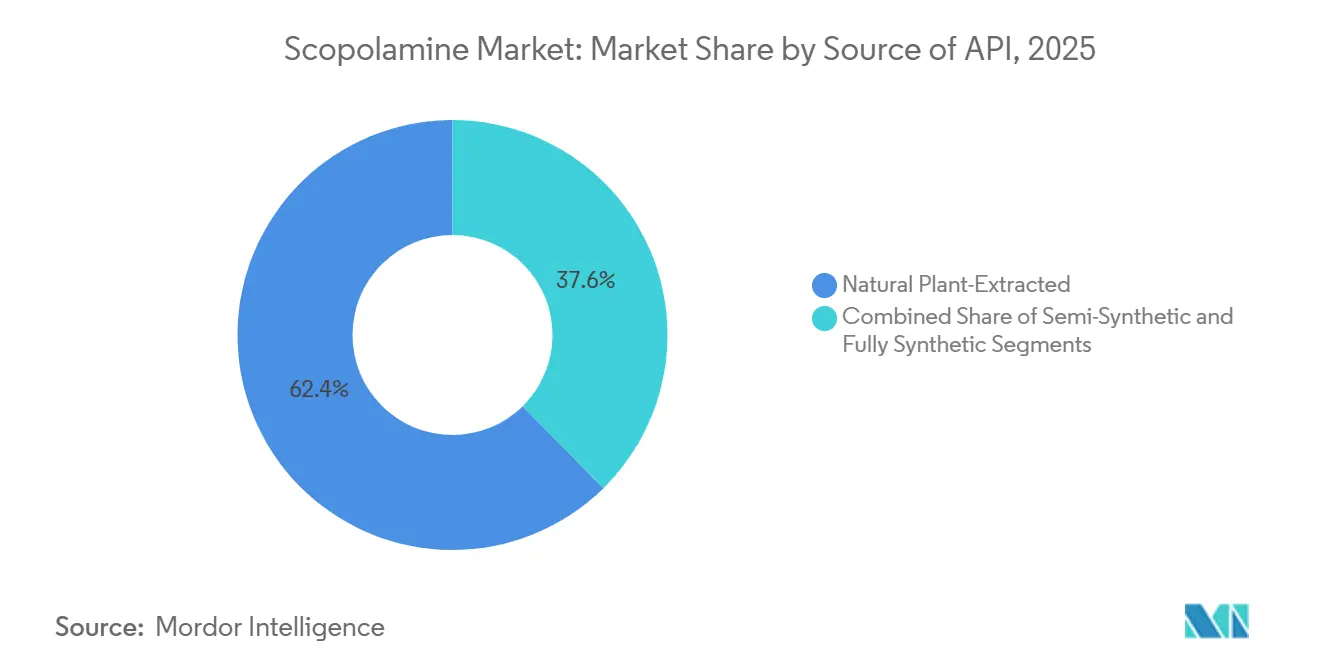

- By source of API, natural plant-extracted scopolamine retained a 62.38% share in 2025, and fully synthetic or fermentation-based routes are expanding at a 7.62% CAGR over the forecast window.

- By distribution channel, retail pharmacies captured 37.49% revenue share in 2025, whereas online pharmacies are advancing at a 9.49% CAGR through 2031.

- By geography, North America held the largest 34.11% share in 2025, and Asia-Pacific is the fastest-growing region with a 7.41% CAGR projected to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Scopolamine Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence of Motion Sickness & PONV | +1.2% | Global, with concentration in North America surgical centers and Asia-Pacific medical tourism hubs | Medium term (2-4 years) |

| Rising Adoption of Transdermal Patches | +0.8% | North America & Europe, spill-over to urban Asia-Pacific markets | Short term (≤ 2 years) |

| Expanding Geriatric Vestibular Disorder Base | +0.9% | Global, highest in aging societies (Japan, Germany, Italy, South Korea) | Long term (≥ 4 years) |

| Space Tourism–Induced Anti-Nausea Demand | +0.3% | National (US, UAE), early commercial launch sites (Florida, Texas, Abu Dhabi) | Long term (≥ 4 years) |

| Synthetic-Biology–Enabled Low-Cost API Supply | +0.7% | Global API production, early adoption in Canada and India | Medium term (2-4 years) |

| VR-Induced Cybersickness Prophylaxis | +0.2% | North America & Asia-Pacific tech hubs (Silicon Valley, Seoul, Shenzhen) | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Growing Prevalence of Motion Sickness & PONV

Post-operative nausea and vomiting remains the fastest-rising application, expanding at 8.22% CAGR on the back of enhanced-recovery surgery pathways that hard-wire multimodal prophylaxis. A 2024 BMC Anesthesiology retrospective covering more than 60,000 procedures linked perioperative scopolamine use to higher mortality and delirium among adults over 60, yet low unit cost and broad prescriber familiarity sustain formulary preference.[2]Yanting Zheng, “Scopolamine Use Is Associated With Increased Mortality, Delirium, and Pneumonia in Older Adults Undergoing General Anesthesia,” BMC Anesthesiology, bmcanesthesiol.biomedcentral.com Motion-sickness prophylaxis still anchors over 43% of revenues but faces mounting over-the-counter antihistamine substitution in developed cruising markets. Asia-Pacific day-surgery volumes, cruise itineraries from Singapore, and fast-growing Indian medical tourism collectively underpin incremental uptake inside the scopolamine market.

Rising Adoption of Transdermal Patches

Transdermal systems captured 46.44% of 2025 sales, driven by non-invasive 72-hour dosing that sidesteps hepatic first-pass metabolism. June 2025 FDA hyperthermia labeling, however, tempers momentum by flagging 13 severe heat-injury events, most in children and seniors. Meanwhile, six AB-rated generics entered the U.S. during 2024-2025, squeezing average patch wholesale acquisition cost by almost 35% and making the scopolamine market even more price-elastic.[3]Zydus Lifesciences, “Zydus Receives USFDA Approval for Scopolamine Transdermal System,” zyduslife.com Research pipelines explore microneedle and iontophoretic systems poised to personalize release kinetics and reduce dermal irritation.

Expanding Geriatric Vestibular Disorder Base

Populations aged ≥ 65 hit unprecedented levels, creating steady vestibular suppressant demand. Yet cumulative anticholinergic load, falls, and cognitive impact invite scrutiny. Four of the FDA’s 13 hyperthermia cases involved seniors; geriatric pharmacists are steering toward lower-burden alternatives, restricting growth primarily to acute travel episodes and short-stay outpatient procedures.

Space Tourism–Induced Anti-Nausea Demand

NASA’s intranasal scopolamine (INSCOP) Phase 2 trial posts a 22-minute mean onset, aligning with suborbital flight profiles that cannot accommodate two-hour patch kick-in windows. Commercial seats remain low today, but projections of several thousand passengers by the early 2030s inject a specialized boost into the scopolamine market as operators bake anti-nausea kits into passenger packages.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Controlled-Substance Regulations | -0.6% | Global, most restrictive in EU member states and select Asian markets | Short term (≤ 2 years) |

| Anticholinergic Side-Effects Limit Compliance | -0.9% | Global, acute impact in geriatric and pediatric populations | Medium term (2-4 years) |

| Climate-Risk to Duboisia Crop Supply | -0.4% | Australia (primary cultivation), global API supply chain | Long term (≥ 4 years) |

| Uptake of Alternative Antiemetics | -0.7% | North America & Europe oncology/surgical centers, Asia-Pacific urban hospitals | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Stringent Controlled-Substance Regulations

Scopolamine scheduling tightens inventory controls, especially across EU states that mandate hospital-only dispensing, curbing retail visibility. January 2025 Texas Medicaid realignment illustrates payer readiness to override brand loyalty when shortages bite.

Anticholinergic Side-Effects Limit Compliance

Dry mouth, blurred vision, and cognitive drag curtail adherence, while the FDA’s heat-injury advisory heightens litigation risk, nudging clinicians toward 5-HT3 and NK1 antagonist triplets despite higher per-dose costs.

Segment Analysis

By Product Type: Generics Erode Patch Pricing Power

Transdermal patches still control 46.44% of scopolamine market share, but the 2024-2025 generic influx compressed brand premiums and spotlighted fulfillment gaps. The scopolamine market size for injectables is forecast to expand at 9.37% CAGR as anesthesiologists lean on rapid titration during ambulatory surgeries. Tablets play minor roles in regions where controlled-substance dispensing in pharmacies remains lenient. Regulatory scrutiny post-hyperthermia notice places added educational load on pharmacists and digital channels.

Second-generation systems that embed microneedles and biosensors could command higher pricing tiers if they demonstrate reduced side-effect incidence and cleaner pharmacokinetics. Development, however, is capital-intensive and must traverse rigorous drug-device combination reviews, keeping time-to-market beyond 2029.

By Application: PONV Gains as Motion Sickness Plateaus

Motion sickness accounted for 43.83% of 2025 revenue, yet market saturation on popular cruise corridors and cheaper antihistamine substitutes cap growth. Conversely, the scopolamine market size linked to PONV is projected to expand at an 8.22% CAGR, underpinned by Asia-Pacific surgical uptrend and standardized enhanced-recovery protocols. Space-flight usage remains nascent but reinforces scopolamine’s relevance in cutting-edge environments where rapid-onset delivery routes are mission-critical.

By Source of API: Fermentation Challenges Plant Dominance

Plant-extracted Duboisia feedstock maintains 62.38% scopolamine market share, though fermentation-based supply is scaling at 7.62% CAGR. Synthetic pathways promise price stability and independence from climate oscillations. Semi-synthetic conversions of hyoscyamine add optionality but do not eliminate agricultural reliance.

By Distribution Channel: Online Pharmacies Accelerate

Retail pharmacies keep a 37.49% foothold, yet online channels register the fastest 9.49% CAGR. Digital refill reminders and tele-consults boost compliance with revised hyperthermia cautions, while centralized fulfillment eases controlled-substance reconciliation. Hospital and ASC inventories continue to prioritize injectable formats under bundled-payment pressure.

Geography Analysis

North America represented 34.11% of 2025 value, driven by historical patch usage and a sharp generic ramp-up that pulled unit prices down by one-third within a year. The FDA hyperthermia bulletin shapes prescribing sentiment, particularly in pediatrics and geriatrics, prompting many ambulatory clinics to introduce temperature-monitoring advisories alongside patch dispensing. Canada’s embrace of yeast-fermentation APIs offers a hedge against Australian raw-material shocks and signals a regulatory green light for synthetic pathways. Mexico’s growing medical-tourism pipeline increases injectable uptake, strengthening the scopolamine market footprint south of the border.

Asia-Pacific posts a 7.41% CAGR through 2031, steered by rising elective surgeries, expanding cruise deployments, and e-pharmacy maturity. India and China rapidly add fermentation capacity, while Japan’s and South Korea’s aging profiles ensure a continual vestibular-disorder base. Australia, both a producer and a consumer, hedges climatic risks by financing pilot fermentation plants.

Europe remains regulatory-dense; EMA pharmacovigilance and hospital-only rules in multiple member states stifle OTC momentum. Northern European surgical centers shift toward guideline-driven 5-HT3-NK1 combinations, squeezing scopolamine volumes. Southern Europe’s cruise traffic and cross-border auto tourism sustain patch turnover, yet expansion is incremental. Emerging regions in the Middle East, Africa, and South America show modest adoption, but GCC investments in medical hubs and Brazil’s procedure growth each add selective lift to the scopolamine market.

Competitive Landscape

The scopolamine market exhibits moderate concentration. GlaxoSmithKline’s Transderm Scōp lost exclusive lift as Zydus, Amneal, Perrigo, and Rhodes shipped six AB-rated generics between late 2024 and mid-2025, capturing a combined 58% share of U.S. patch dispenses. Zydus’s Ahmedabad SEZ plant underscores India’s ascent in complex transdermal device manufacturing, while Perrigo leverages the Aveva platform to sustain supply during brand outages. Hyasynth Bio leads synthetic-biology APIs; once their cost curve drops below extraction parity, vertically integrated formulators will likely migrate to fermentation to blunt crop shocks.

Injectable supply is scattered across Baxter, Fresenius Kabi, and regional CMOs, producing a price-competitive arena governed by GPO tender cycles. White-space innovators focus on intranasal and microneedle routes, with NASA’s INSCOP readout pivotal for broader industrial adoption.

Scopolamine Industry Leaders

Pfizer Inc.

Baxter International Inc.

Novartis AG

GlaxoSmithKline plc

Perrigo plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The FDA has issued a warning regarding the anti-nausea patch, Transderm Scōp (scopolamine transdermal system), highlighting its serious risk of heat-related complications. This patch has the potential to elevate body temperature, leading to complications that could necessitate hospitalization or, in severe instances, result in death.

- January 2025: Texas Health and Human Services moves generic patches to preferred status to offset branded supply delays.

Global Scopolamine Market Report Scope

As per the scope of the report, scopolamine is an anticholinergic agent that is used to reduce the secretions of certain organs. It is used in the treatment of motion sickness and postoperative nausea and vomiting. It is sometimes also used before the surgery to decrease secretions such as saliva.

The Scopolamine Market Report is segmented by Product Type, Application, Source of API, Distribution Channel, and Geography. By Product Type, the market is segmented into Transdermal Patches, Tablets/Capsules, Injectable Solution, and Oral Drops & Others. By Application, the market is segmented into Motion Sickness, PONV, Pupil Dilation/Ophthalmic Uses, and GI & Other Antispasmodic Uses. By Source of API, the market is segmented into Natural Plant‑Extracted, Semi‑Synthetic, and Fully Synthetic/Fermentation‑Based. By Distribution Channel, the market is segmented into Hospital & ASC, Retail Pharmacies, and Online Pharmacies. By Geography, the market is segmented into North America, Europe, Asia‑Pacific, Middle East & Africa, and South America.The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Transdermal Patches |

| Tablets / Capsules |

| Injectable Solution |

| Oral Drops & Others |

| Motion Sickness |

| Post-operative Nausea & Vomiting (PONV) |

| Pupil Dilation / Ophthalmic |

| GI & Other Antispasmodic Uses |

| Natural Plant-Extracted |

| Semi-Synthetic |

| Fully Synthetic / Fermentation-Based |

| Hospital & Ambulatory Surgical Centers |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Transdermal Patches | |

| Tablets / Capsules | ||

| Injectable Solution | ||

| Oral Drops & Others | ||

| By Application | Motion Sickness | |

| Post-operative Nausea & Vomiting (PONV) | ||

| Pupil Dilation / Ophthalmic | ||

| GI & Other Antispasmodic Uses | ||

| By Source of Active Pharmaceutical Ingredient (API) | Natural Plant-Extracted | |

| Semi-Synthetic | ||

| Fully Synthetic / Fermentation-Based | ||

| By Distribution Channel | Hospital & Ambulatory Surgical Centers | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the scopolamine market in 2026?

The scopolamine market is valued at USD 492.36 million in 2026 and is projected to reach USD 642.28 million by 2031.

Which product type is growing fastest?

Injectable solutions show the highest growth, advancing at a 9.37% CAGR through 2031, driven by acute PONV management needs.

What triggered the new FDA safety warning?

Thirteen global hyperthermia cases, including two deaths, led the FDA in June 2025 to require stronger heat-exposure warnings on scopolamine patches.

Why is synthetic-biology production important?

Fermentation methods reduce dependence on climate-sensitive Duboisia crops, lower cost, and ensure consistent API supply.

Which region offers the most rapid market growth?

Asia-Pacific exhibits the fastest expansion at 7.41% CAGR, bolstered by rising surgical volumes and maturing online pharmacy ecosystems.

Page last updated on: