Saudi Arabia Waste Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

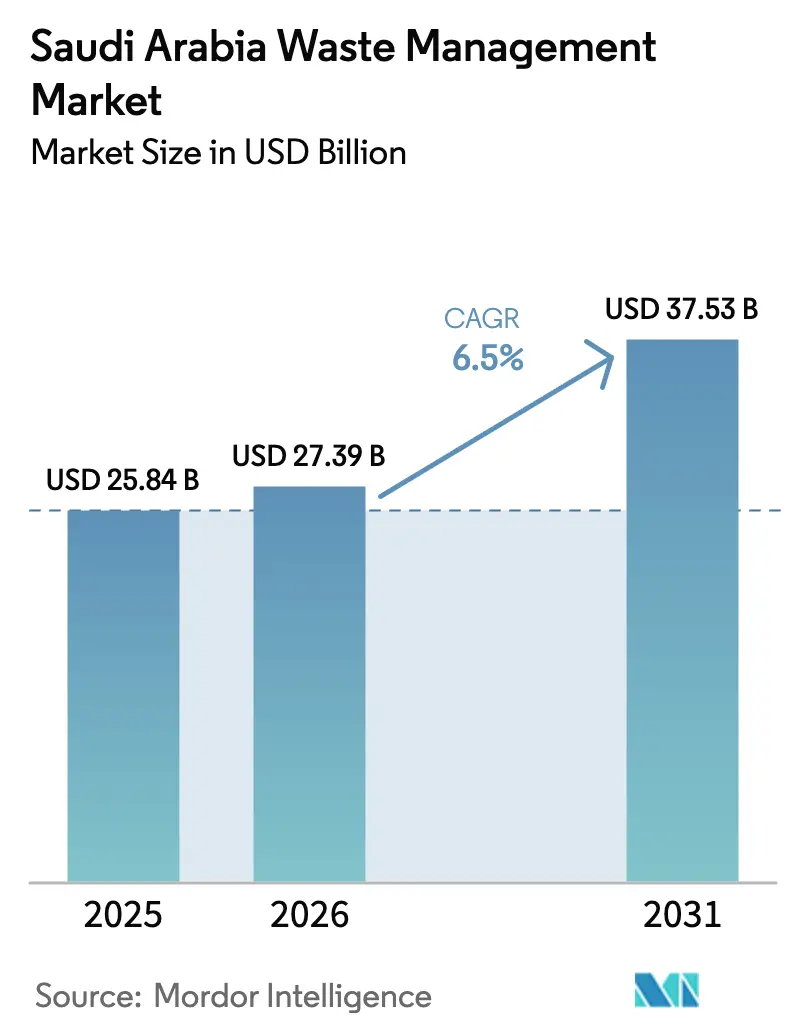

| Base Year Market Size (2025) | USD 25.84 Billion |

| Market Size (2026) | USD 27.39 Billion |

| Market Size (2031) | USD 37.53 Billion |

| Growth Rate (2026 - 2031) | 6.50% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Waste Management Market Analysis by ���ϲ�����

The Saudi Arabia waste management market size was valued at USD 25.84 billion in 2025 and is estimated to grow from USD 27.39 billion in 2026 to reach USD 37.53 billion by 2031, at a CAGR of 6.5% during the forecast period (2026-2031). Policy pressure from Vision 2030, stricter penalties under Royal Decree M/3, and an expanding public-private-partnership (PPP) pipeline are steering the transition away from uncontrolled landfilling toward integrated resource recovery. Population growth above 36 million by 2030, combined with urban migration toward Riyadh, Jeddah, and Dammam, is raising per-capita municipal solid-waste (MSW) generation from 1.4 kilograms per day in 2024 to 1.6 kilograms by 2030. At the same time, large construction programs such as NEOM and the Red Sea Project are accelerating construction-and-demolition (C&D) waste output, creating demand for mobile crushers, material recovery facilities (MRFs), and refuse-derived-fuel (RDF) plants. The Saudi Arabia waste management market is also benefiting from technology adoption: blockchain-enabled traceability for extended producer responsibility (EPR) credits, and solar-powered electric collection fleets are already in operation.[1]Vision 2030 Secretariat, “Zero-Landfill Road Map,” vision2030.gov.sa

Key Report Takeaways

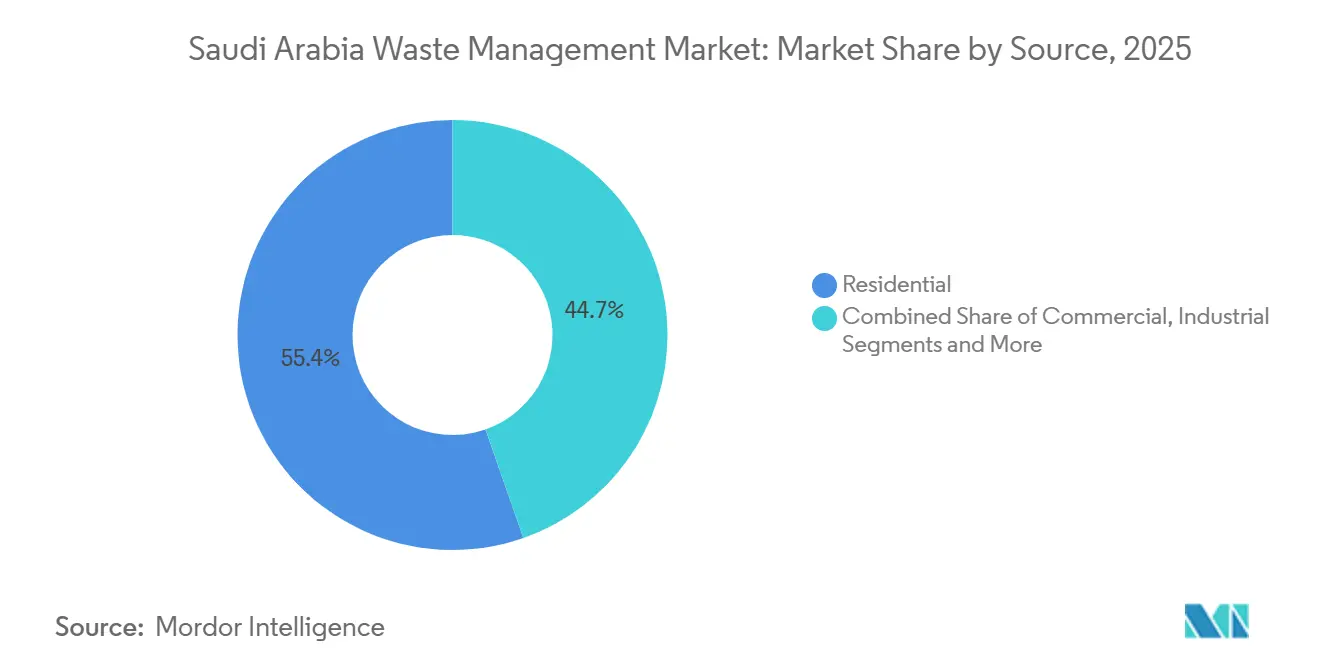

- By source, residential waste held 55.35% of the Saudi Arabia waste management market share in 2025, while commercial waste is forecast to post the fastest growth at a 9.6% CAGR through 2031.

- By service type, disposal and treatment services accounted for 53.45% of the Saudi Arabia waste management market in 2025, and recycling is projected to grow at a 9.7% CAGR through 2031.

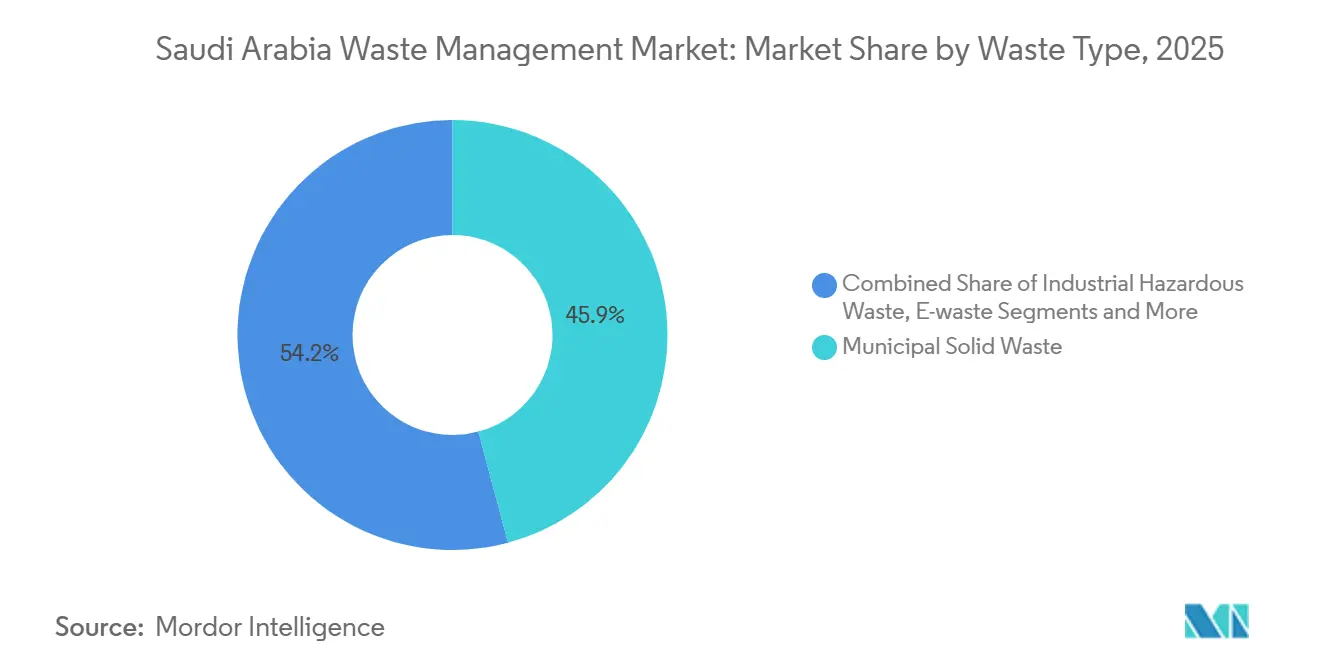

- By waste type, MSW accounted for 45.85% of the Saudi Arabia waste management market share in 2025, and e-waste is expected to grow at an 8.49% CAGR over 2026-2031.

- Riyadh accounted for 38.5% of the Saudi Arabia waste management market size in 2025, whereas the Rest of the Saudi Arabia cluster is set to expand at an 8.19% CAGR to 2031.

- Saudi Investment Recycling Company (SIRC), Veolia, SUEZ, Averda, and BEEAH collectively managed more than 50% of treated volumes in 2025, and SIRC alone recycled 16 million tons of C&D waste that year.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Waste Management Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 zero-landfill target milestones | +1.5% | National, 25 geographic clusters | Long term (≥ 4 years) |

| Economic growth and urban migration | +1.2% | Riyadh, Jeddah, Dammam metropolitan areas | Medium term (2-4 years) |

| Private-sector PPP pipeline for infrastructure | +1.0% | Riyadh, Makkah, Eastern Province | Medium term (2-4 years) |

| Construction giga-projects | +0.8% | NEOM, Red Sea, Qiddiya, Diriyah Gate | Short term (≤ 2 years) |

| Green-hydrogen cluster raising RDF demand | +0.5% | NEOM, later Jazan and Ras Al-Khair | Medium term (2-4 years) |

| Blockchain-enabled EPR credits | +0.4% | National, first in Riyadh | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Vision 2030 Zero-Landfill Target Milestones

The 90% diversion goal for 2040 embeds recycling, composting, and waste-to-energy (WtE) thresholds into building permits and producer obligations. Royal Decree M/3 introduced fines up to USD 8 million and prison terms for non-compliance, transforming environmental rules into board-level risks. Technical guidelines released in 2024 require on-site segregation for projects larger than 10,000 square meters and insist on third-party waste audits. Municipalities are therefore phasing out unlined dumps, shifting budgets toward sanitary cells with gas capture and leachate treatment. The direction is clear: landfilling is turning into the disposal option of last resort.[2]Saudi Gazette, “Royal Decree M/3 Enforces Environmental Penalties,” saudigazette.com.sa

Economic Growth and Urban Migration

Saudi Arabia’s non-oil economy grew 4.2% in 2024, spurring retail, hospitality, and logistics activity that widens commercial and industrial waste streams. Urbanization above 85% funnels new residents into Riyadh, Jeddah, and Dammam, lifting daily household refuse to an expected 1.6 kilograms by 2030. Municipal collection systems in secondary cities lag behind, creating a two-tier service landscape that the National Waste Management Center (NWMC) plans to harmonize through its 25-cluster strategy. Private haulers are deploying GPS-routed fleets to cut fuel use and raise pickup frequency. The sheer scale of urban growth positions the Saudi Arabia waste management market for steady volume gains.

Private-Sector PPP Pipeline for Waste Infrastructure

Since 2024, SWPC and the NWMC have closed more than USD 2 billion in build-operate-transfer contracts covering sewage, MRFs, and WtE assets. The Al Haer independent sewage treatment plant (ISTP) in Riyadh reached financial close at USD 480 million and will start commercial operations in 2026, trimming freshwater demand by recycling 200,000 cubic meters per day. PPP structuring transfers the design, construction, and performance risks to private operators while allowing municipalities to accelerate delivery timelines. Veolia’s USD 500 million industrial wastewater reuse scheme in Jubail follows the same template, proving that long-tenor concessions now attract both local and international lenders. A visible deal flow keeps the Saudi Arabia waste management market attractive to global majors.[3]Saudi Water Partnership Company, “PPP Project Pipeline 2025-2027,” swpc.sa

Construction Giga-Projects Generating High C&D Waste

NEOM, the Red Sea Project, Qiddiya, and Diriyah Gate together inject more than USD 1 trillion of capital spending into the economy and generate up to 70 million tons of rubble, steel, and timber each year during peak building phases. NEOM’s tender documents mandate verified recycled content in concrete, asphalt, and rebar, creating captive demand for secondary aggregates. SIRC’s Riyadh C&D plant already runs at 600 tons per hour and achieves 90% material recovery, offering a template rapidly copied at Qiddiya and the Red Sea Project. On-site mobile crushers reduce trucking distances and curb carbon emissions linked to haulage. This wave of construction secures a multiyear pipeline of feedstock for recyclers inside the Saudi Arabia waste management market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile demand for reclaimed polymers | -0.6% | Jubail and Yanbu petrochemical hubs | Short term (≤ 2 years) |

| High upfront CapEx for integrated sites | -0.5% | National, greenfield WtE and MRF facilities | Medium term (2-4 years) |

| Fragmented collection in secondary cities | -0.4% | Outside Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Low household participation in recycling | -0.3% | National, especially low-income districts | Long term (≥ 4 years) |

| Thin domestic market for secondary materials | -0.2% | Export-oriented plastics, metals, and paper | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Volatile Demand for Reclaimed Polymers Amid New Petrochemical Capacity

SABIC’s Amiral complex added 11 million tons of virgin polyolefins in 2024, pushing resin prices below USD 1,000 per ton and eliminating the historical premium that recycled grades enjoyed. Local recyclers face collection and sorting costs upward of USD 150 per ton, squeezing margins unless subsidies or strict recycled-content rules intervene. Although TotalEnergies and Aramco produced certified circular polymers in 2023, volumes remain pilot scale and cannot absorb national plastic waste flows. Export channels to Europe offer better economics thanks to carbon-border levies on virgin resin, yet logistics expenses eat into profits. The result is choppy demand that deters fresh investment in mechanical recycling capacity.

High Upfront CapEx for Integrated Sites

New WtE and hazardous-waste facilities require USD 400-600 per ton of annual capacity, translating into project sizes of USD 200-800 million. Imported grate furnaces, optical sorters, and rotary kilns carry 18-month lead times and expose sponsors to currency swings. Permitting may take another 12-18 months and involves environmental impact studies, NWMC licensing, and municipal zoning reviews. Debt costs are 150-200 basis points above other infrastructure because lenders still perceive technology risk. If regulators later tighten diversion targets, some assets could become stranded, raising fears among equity investors.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Residential Waste Holds the Lead while Commercial Volume Accelerates

Residential waste accounted for 55.35% of the Saudi Arabia waste management market share in 2025, reflecting household consumption patterns in cities where per-capita refuse already exceeds 1.4 kilograms per day. Commercial streams covering malls, offices, and hotels are forecast to outpace all other categories at a 9.6% CAGR to 2031 as Vision 2030 tourism targets draw 30 million visitors annually. Industrial sources around Jubail and Yanbu add specialty sludges and catalysts that flow into Veolia’s 120,000-ton hazardous-waste plant, while medical facilities in Jeddah now send infectious waste to SIRC’s new 50,000-ton autoclave line. Residential generators remain the primary focus for curbside pilot programs that aim to lift segregation rates above the current 5%.

The commercial segment offers higher contract values and predictable volumes per site, enabling operators to introduce on-premise sorting cages and real-time weighing systems. Retail franchises in Riyadh have already locked in five-year take-back agreements that guarantee cardboard, plastic, and food scraps are delivered to dedicated recovery lines. Industrial producers are expected to account for more than 600,000 tons of hazardous material per year by 2028, keeping incineration and stabilization services tight. Household organics, which form 40% of the residual bin, are starting to feed SIRC and Edama’s composting partnership that targets landscaping markets. As commercial volume grows, the Saudi Arabia waste management market size for collection and sorting services tied to shopping malls and hotels will climb steadily through the forecast horizon.

By Service Type: Disposal Leads yet Recycling Takes Off

Disposal and treatment accounted for 53.45% of the Saudi Arabia waste management market size in 2025, but recycling is projected to grow fastest at 9.7% a year through 2031. The landfill share is shrinking as unlined cells close and sanitary sites with gas capture raise tipping fees to USD 70 per ton, narrowing the cost gap with WtE plants. Incineration capacity will triple to more than 700 megawatts by 2030 once the 3,500-ton-per-day Jeddah unit and the 1.3-million-ton Riyadh facility come online. MRFs and C&D crushers are meanwhile expanding; SIRC’s Riyadh plant runs at 600 tons per hour and posts a 90% recovery rate, supplying recycled aggregate to Qiddiya road building.

Collection and transport remain labor-intensive, but automation is creeping in. Averda’s solar-powered electric fleet at the Red Sea Project trims diesel use by 30%, and Envac Gulf’s pneumatic tubes in Riyadh towers cut pickup frequency in dense districts. Consulting and audit services are a small but growing slice, as NWMC rules require annual waste plans to be verified by accredited firms. Composting and chemical treatment address food and hazardous sludges, respectively, adding diversity to revenue streams inside the Saudi Arabia waste management market. As recycling tonnage ramps up, operators expect to capture higher gate fees and sell more secondary commodities, underpinning long-run profitability.

By Waste Type: MSW Dominates but E-Waste Climbs Rapidly

Municipal solid waste supplied 45.85% of the Saudi Arabia waste management market share in 2025 and remains the baseline flow into most collection networks. E-waste, however, is rising at an 8.49% CAGR due to 90% smartphone penetration, shorter appliance lifecycles, and the opening of new NCEC drop-off centers across the three largest cities. Industrial hazardous waste keeps two licensed incinerators running near nameplate, with Veolia and SIRC forming a tight duopoly. Plastic waste is subject to the Saudi Plastic Pact’s 30% recycled-content goal, but domestic mechanical capacity remains below 100,000 tons per year, forcing exporters to ship bales to Europe and Southeast Asia.

C&D waste peaks during 2026-2028, when NEOM and other giga-projects reach maximum excavation and concrete pouring, after which tonnage moderates as sites move into finishing stages. Agricultural streams, such as date-palm fronds, are slowly being turned into compost and biochar through SIRC-Nadec pilots, reducing open-field burning. Biomedical waste volumes are rising alongside hospital expansions in the Makkah and Al Madinah regions; the Jeddah autoclave hub treated 10,000 tons during its first two months of trial operation. Radioactive and other specialized materials remain negligible but fall under strict KACARE oversight. Altogether, evolving waste mix dynamics ensure continuous capital rotation across multiple subsectors in the Saudi Arabia waste management market.

Geography Analysis

Riyadh accounted for 38.5% of Saudi Arabia's waste management market in 2025, supported by an 8 million population and the Integrated Waste Management Program, which targets 81% MSW diversion. The capital’s 600-ton-per-hour C&D recycling line hits a 90% recovery rate and supplies road aggregate to Diriyah Gate, while tender documents for two additional MRFs totaling 2,000 tons per day are already in the market. A forthcoming 1.3-million-ton WtE plant, budgeted at USD 800 million, will feed 200 megawatts of baseload power to the grid by 2029. Seamless coordination between SIRC headquarters and the NWMC accelerates permitting for innovative pilots such as blockchain EPR credits, making Riyadh a bellwether for nationwide rollouts.

Makkah Province ranks second in revenue, bolstered by seasonal pilgrim surges that push collection volumes to record peaks. The 3,500-ton-per-day Jeddah WtE facility demonstrates best-in-class flue-gas cleaning and ash vitrification, while Veolia’s and Averda’s concession incorporates smart bins that message fill-level data to dispatchers every 30 minutes. Hazardous medical capacity increased in 2025 when SIRC opened a 50,000-ton autoclave hub near King Abdulaziz University Hospital, in compliance with the 24-hour treatment rule. Along the Tabuk-Makkah coastline, the Red Sea Project enforces 70% on-site C&D recycling, driving demand for mobile crushers, optical sorters, and composting units immediately after resort handover.

The Eastern Province combines heavy industry with rising residential density, producing the Kingdom’s highest ratio of hazardous to municipal waste. Veolia’s 120,000-ton incinerator in Jubail processes refinery sludge and petrochemical catalysts under an exclusive Aramco contract, while a USD 500 million joint-venture plant will recycle 8.8 million cubic meters of industrial wastewater each year starting in 2028. A municipal study pinned the lack of segregated bins as a major hurdle, and the NWMC is packaging a regional concession to cover Dammam, Khobar, and 14 rural districts. Elsewhere, the Rest of Saudi Arabia cluster, including NEOM’s Tabuk site, is forecast to grow at 8.19% a year as giga-project build-outs drive C&D tonnage and push operators to install modular processing lines. AlUla’s organic waste composting initiative shows that smaller cities can leapfrog to circular models when capital and regulatory clarity align.[4]Diriyah Gate Development Authority, “Waste Handling Protocol 2025,” dgda.gov.sa

Competitive Landscape

SIRC leads the Saudi Arabia waste management market with 16 million tons of C&D recycling, 600,000 tons of industrial waste treatment, and a flagship RDF line that embeds blockchain for batch-level traceability. Its December 2024 frameworks with SUEZ and Veolia seek to pool European technology with domestic site portfolios and aim to create a national champion by 2027. Veolia generated USD 304 million (EUR 280 million) in local revenue during 2023 and holds an exclusive Aramco contract that guarantees 200,000 tons of hazardous throughput each year, cementing its position in the high-margin industrial niche.

Strategic focus has shifted toward vertical integration. SIRC couples collection fleets, MRFs, WtE, and recycled-commodity trading within the same concession, locking in gate fees and offtake. Averda won a February 2026 mandate at the Red Sea Project that fuses an automated MRF, solar-charged e-trucks, composting drums, and an on-site incinerator to meet a 70% recycling target. Veolia’s USD 500 million wastewater reuse plant in Jubail widens its environmental services scope to water, mirroring global trends in which waste and water merge into a single utility platform. Smaller operators such as NESMA Recycling and Sama Environmental Services specialize in event clean-up and niche hazardous streams, avoiding direct competition with market leaders while still capturing profitable segments.

M&A prospects remain active. International suppliers of mobile equipment, such as Kiverco, rely on UK Export Finance for credit insurance, indicating a steady pipeline of imported machinery. Blockchain EPR platforms may spur joint ventures between software firms and waste operators, while mounting CapEx burdens could drive mid-tier consolidations as new NWMC licensing rules raise financial thresholds. Overall, the top five companies controlled just above 50% of treated tonnage in 2025, supporting a market concentration score of 6.

Saudi Arabia Waste Management Industry Leaders

Saudi Investment Recycling Co. (SIRC)

BEEAH Group

Veolia Middle East

Averda

SUEZ Middle East

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Averda secured a contract with SEPCO III to build and operate an integrated waste facility for the Red Sea Project that includes an automated MRF, incinerator, composting line, and solar-powered electric trucks.

- January 2026: The Saudi Investment Recycling Company (SIRC) signed a strategic agreement with Hydrogen Utopia International (HUI) on the sidelines of the IFAT Saudi Arabia 2026 exhibition in Riyadh. The collaboration aims to deploy advanced Plasma Enhanced Melter technology to process non-recyclable plastic waste into high-purity syngas. This syngas will be combined with hydrogen to manufacture Sustainable Aviation Fuel (SAF) and other low-carbon hydrocarbon products, heavily supporting the Kingdom's net-zero and circular economy objectives.

- May 2025: SIRC signed a major MoU with U.S.-based institutional investor EIG Management Company to co-finance and develop critical waste management infrastructure in Saudi Arabia. The partnership centers on two massive projects: a $375 million facility in Riyadh to produce Refuse-Derived Fuel (RDF) from municipal waste to power heavy industry kilns, and a $250 million facility dedicated to processing end-of-life tires into green energy products like pyrolysis oil and recycled carbon black.

- February 2025: A Miahona-BESIX-Marafiq consortium won the USD 480 million Al Haer ISTP in Riyadh under a 25-year build-own-operate-transfer model.

Saudi Arabia Waste Management Market Report Scope

Waste management is the complete process of collecting, hauling, treating, and disposing of waste materials in a method that minimizes their impact on the environment and human health. It encloses various activities and practices to reduce waste generation and manage waste materials efficiently and sustainably.

The report provides a comprehensive background analysis of the market, covering the current market trends, restraints, technological updates, and detailed information on various segments and the competitive landscape of the industry.

The Saudi Arabian waste management market is segmented by waste type (industrial waste, municipal solid waste, e-waste, plastic waste, and biomedical and other waste types [including construction waste]), disposal method (landfill, incineration, recycling, and other disposal methods), and region (Riyadh, Jeddah, Dammam, Yanbu, and Other Regions). The report offers market sizes and forecasts for all the above segments in terms of value (USD).

| Residential |

| Commercial (retail, office, etc.) |

| Industrial |

| Medical (Health and Pharmaceutical) |

| Construction & Demolition |

| Others (institutional, agricultural, etc) |

| Collection, Transportation, Sorting & Segregation | |

| Disposal / Treatment | Landfill |

| Recycling & Resource Recovery | |

| Incineration & Waste-to-Energy | |

| Others (Chemical Treatment, Composting, etc.) | |

| Others (Consulting, Audit & Training, etc.) |

| Municipal Solid Waste |

| Industrial Hazardous Waste |

| E-waste |

| Plastic Waste |

| Biomedical Waste |

| Construction & Demolition Waste |

| Agricultural Waste |

| Other Specialized Waste (radio active, etc) |

| Riyadh |

| Makkah Province (incl. Jeddah) |

| Eastern Province (Dammam, Khobar) |

| Rest of Saudi Arabia |

| By Source | Residential | |

| Commercial (retail, office, etc.) | ||

| Industrial | ||

| Medical (Health and Pharmaceutical) | ||

| Construction & Demolition | ||

| Others (institutional, agricultural, etc) | ||

| By Service Type | Collection, Transportation, Sorting & Segregation | |

| Disposal / Treatment | Landfill | |

| Recycling & Resource Recovery | ||

| Incineration & Waste-to-Energy | ||

| Others (Chemical Treatment, Composting, etc.) | ||

| Others (Consulting, Audit & Training, etc.) | ||

| By Waste Type | Municipal Solid Waste | |

| Industrial Hazardous Waste | ||

| E-waste | ||

| Plastic Waste | ||

| Biomedical Waste | ||

| Construction & Demolition Waste | ||

| Agricultural Waste | ||

| Other Specialized Waste (radio active, etc) | ||

| By Region | Riyadh | |

| Makkah Province (incl. Jeddah) | ||

| Eastern Province (Dammam, Khobar) | ||

| Rest of Saudi Arabia | ||

Key Questions Answered in the Report

What is the current value of the Saudi Arabia waste management market?

The sector stands at USD 27.39 billion in 2026 and is on track to reach USD 37.53 billion by 2031.

How fast is the market expected to grow?

It is projected to advance at a 6.5% CAGR between 2026 and 2031, driven by Vision 2030 mandates and rising urban population.

Which waste source generates the largest share of volumes?

Residential streams led with 55.35% of total value in 2025, reflecting high per-capita refuse in major cities.

Where is recycling seeing the strongest momentum?

Recycling and resource recovery is the fastest-growing service type, expanding at a 9.7% CAGR as new MRFs and WtE plants come online.

Which region offers the quickest growth prospects?

The Rest of Saudi Arabia cluster, anchored by NEOM and secondary cities, is forecast to rise at an 8.19% CAGR through 2031.

Who are the leading companies in the field?

SIRC, Veolia, SUEZ, Averda, and BEEAH hold the largest footprints, with SIRC alone recycling 16 million tons of C&D waste in 2025.

Page last updated on: