Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

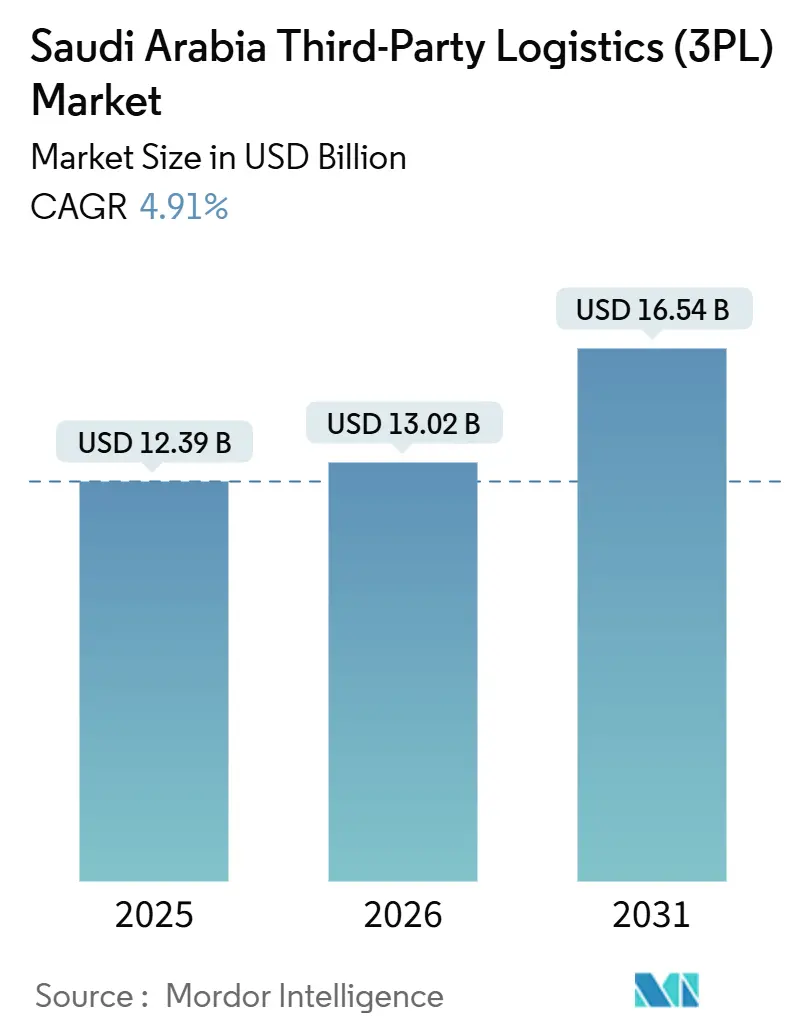

| Base Year Market Size (2025) | USD 12.39 Billion |

| Market Size (2026) | USD 13.02 Billion |

| Market Size (2031) | USD 16.54 Billion |

| Growth Rate (2026 - 2031) | 4.91% CAGR |

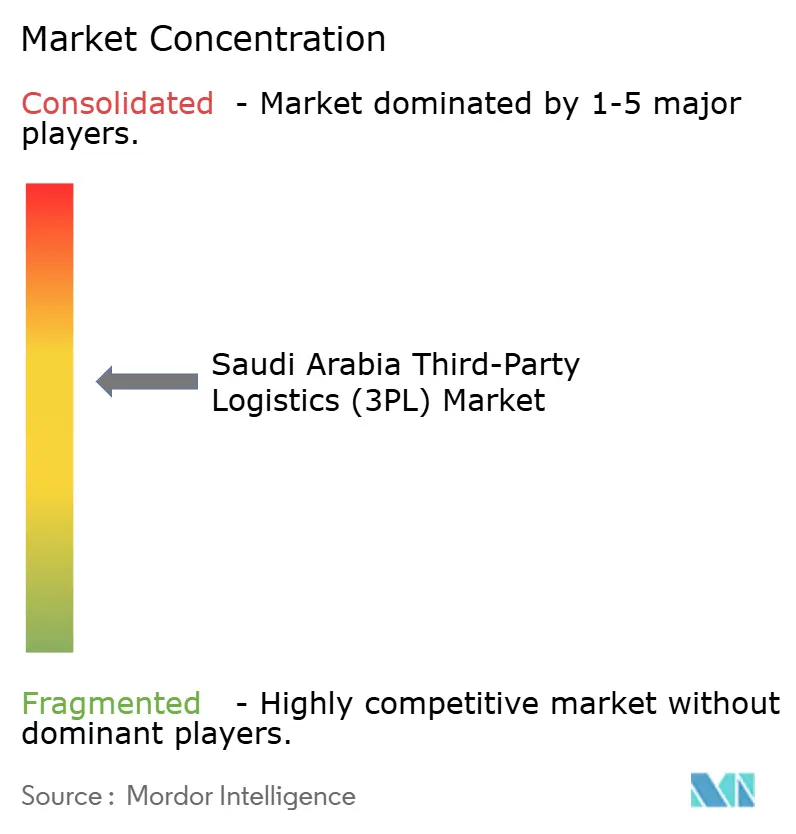

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Third-Party Logistics (3PL) Market Analysis by ���ϲ�����

The Saudi Arabia third-party logistics market size was valued at USD 12.39 billion in 2025 and is estimated to grow from USD 13.02 billion in 2026 to reach USD 16.54 billion by 2031, at a CAGR of 4.91% during the forecast period (2026-2031).

Saudi Arabia’s Vision 2030 reforms, mandatory carbon-disclosure rules, and 5G-enabled logistics corridors are pushing operators toward electric fleets, renewable-powered warehouses, and real-time data platforms. Private investment flows, including EUR 500 million (USD 588.47 million) from DHL and USD 860 million in venture funding, are accelerating warehouse automation and last-mile innovation. Rising free-trade talks with China and the United Kingdom strengthen the landbridge that links the Red Sea to the Gulf, giving Saudi Arabia 3PL market new east-west routes and premium-rate cargo. Pharmaceutical cold-chain demand, quick-commerce growth in tier-2 cities, and government stockpiling rules for strategic reserves broaden the contract base beyond energy logistics.

Key Report Takeaways

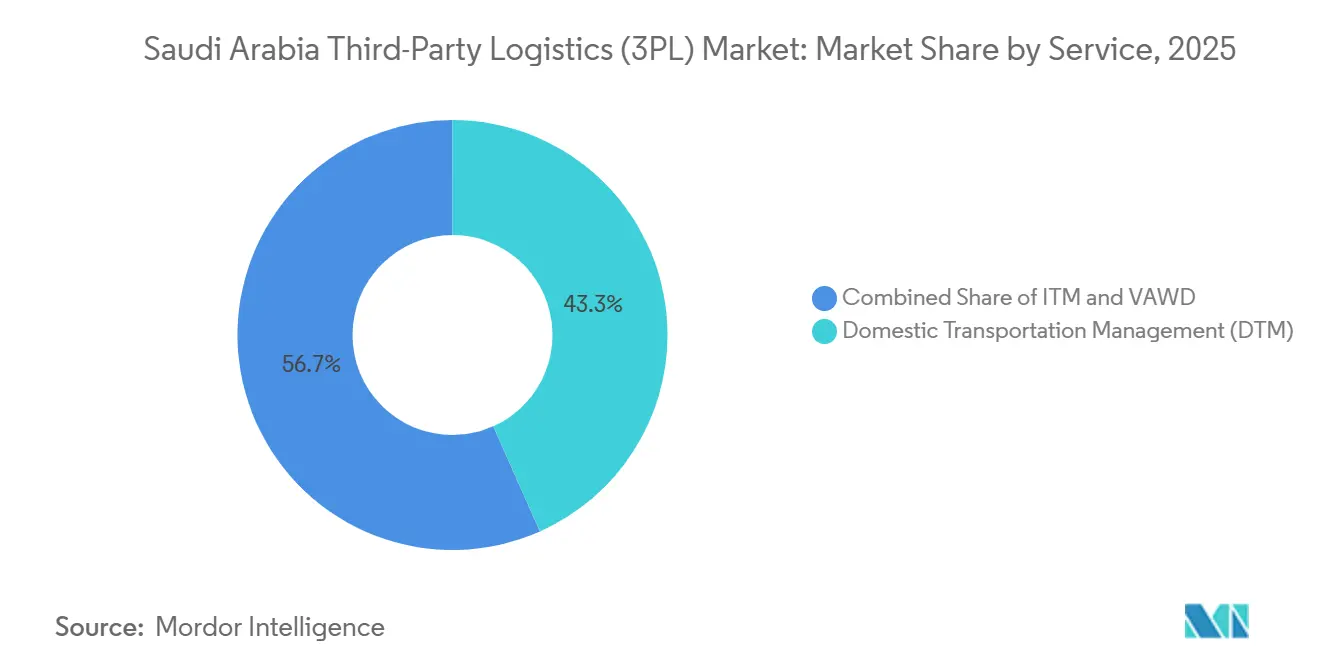

- By service, domestic transportation management led with 43.33% of the Saudi Arabia third-party logistics (3PL) market share in 2025, while international transportation management is forecast to record a 5.2% CAGR through 2031.

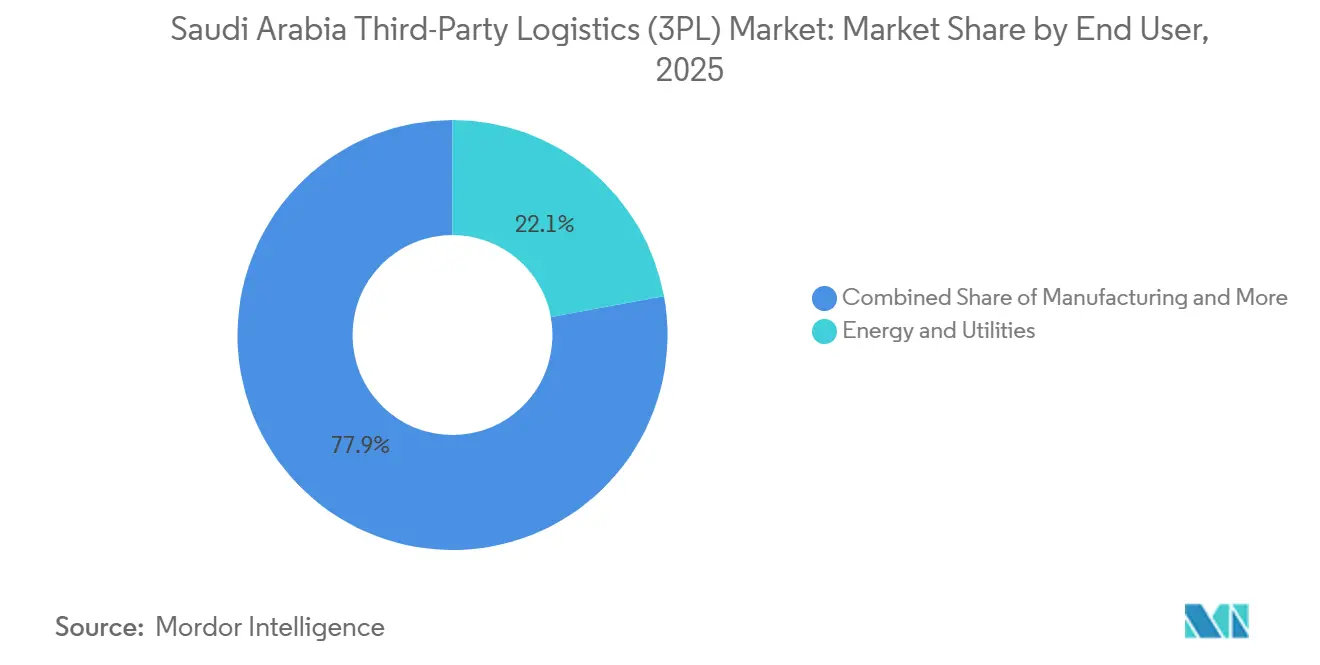

- By end user, energy & utilities held 22.12% of the Saudi Arabia third-party logistics (3PL) market size in 2025, yet life sciences & healthcare is projected to expand at a 5.39% CAGR to 2031.

- By logistics model, asset-heavy operators controlled 39.2% of the Saudi Arabia third-party logistics (3PL) market share in 2025, whereas asset-light models are advancing at a 5.26% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Third-Party Logistics (3PL) Market Trends and Insights

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory carbon-disclosure norms (SASO 2025) are catalyzing demand for green 3PL offerings | +0.9% | National, with early adoption in Riyadh, Jeddah, and Dammam industrial zones | Medium term (2-4 years) |

| 5G-enabled smart-port integrations at Jeddah & Dammam are sharply reducing port dwell times | +1.1% | Coastal regions, concentrated at major container terminals | Short term (≤ 2 years) |

| GCC–China and GCC–UK FTA negotiations unlocking new east–west trade corridors via the Saudi landbridge | +0.8% | National, with spillover to GCC partners and Red Sea economies | Long term (≥ 4 years) |

| Gulf Railway Phase-1 (Dammam–Riyadh–Jeddah) cutting cross-kingdom transit times by up to 50% | +0.7% | National, connecting Eastern Province, Central Region, and Western Coast | Medium term (2-4 years) |

| Local-content warehousing mandates for strategic reserves spurring multi-tenant bonded facilities | +0.5% | National, with concentration near industrial cities and SEZs | Short term (≤ 2 years) |

| The rapid rise of quick-commerce in tier-2 cities is driving micro-fulfilment networks build-out | +0.6% | Urban centers beyond Riyadh-Jeddah-Dammam, including Khobar, Tabuk, and Abha | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Mandatory Carbon-Disclosure Norms Catalyze Green 3PL Adoption

The 2025 SASO rule represents a structural shift in the Saudi 3PL market, embedding sustainability directly into procurement and tender qualification criteria. Emissions transparency is no longer a branding exercise but a measurable performance benchmark influencing contract awards and renewals. Providers investing in solar rooftops, electric fleets, and carbon-tracking platforms are able to command 8-12% pricing premiums, as clients increasingly value lower Scope 3 exposure and ESG alignment. Meanwhile, fleet-heavy laggards face margin pressure, weaker tender scores, and the risk of exclusion from government contracts. Access to capital is therefore emerging as a key divider, shaping competitive tiers and accelerating consolidation within the market.

5G Smart-Port Integrations Cut Dwell Time

Jeddah Islamic Port and King Abdulaziz Port are accelerating digital transformation through 5G-enabled devices, AI-driven yard planning, and automated gate systems, reducing container dwell time from four to two days. This materially cuts demurrage costs, improves truck turnaround, and increases asset utilization for logistics operators. 3PLs that integrate port APIs directly into their TMS platforms gain real-time visibility and faster clearance cycles, allowing them to convert time efficiency into pricing leverage and service differentiation across the Saudi Arabia 3PL market.

GCC–China and GCC–UK FTAs Unlock the Landbridge

Pending FTAs, tariff reductions, and harmonized e-documentation are enabling seamless rail–road container moves between Jeddah and Dammam, creating a corridor that can move cargo to Asia or Europe up to three days faster than the traditional all-water Suez routing. CMA CGM’s 2024 Red Sea terminal agreement underscores the carrier's confidence in this premium transit model[1]Ben Ames, “CMA CGM to Build Up Saudi Arabian Logistics Network,” DC Velocity, dcvelocity.com . As reliability and speed become strategic differentiators, intermodal specialists positioned along this corridor gain first-mover advantages within the Saudi Arabia 3PL market, capturing time-sensitive and higher-margin cargo flows.

Gulf Railway Phase-1 Halves Inland Transit

The 1,300 km Dammam-Riyadh-Jeddah freight rail corridor is set to reduce cross-Kingdom transit times by nearly 50% while lowering carbon emissions per ton-kilometer by an estimated 60-70% compared to long-haul trucking. 3PLs that integrate rail line-haul with first-and last-mile trucking can offer faster, lower-emission domestic solutions aligned with SASO compliance requirements and shipper ESG mandates. This multimodal bundling strengthens value propositions, particularly for industrial and FMCG clients seeking measurable decarbonization across their Saudi supply chains.

Restraint Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic chassis & container equipment imbalance caused by Red Sea security rerouting | -0.7% | Coastal regions, particularly Red Sea ports and connecting inland terminals | Short term (≤ 2 years) |

| Urban congestion from megaproject construction traffic (NEOM, Qiddiya) is hampering last-mile efficiency | -0.5% | Concentrated in the NEOM corridor, Riyadh (Qiddiya), and connecting highways | Medium term (2-4 years) |

| Delays in the nationwide customs single-window rollout are leading to repetitive documentation loops | -0.4% | National in scope, affecting all cross-border trade and bonded warehouse operations. | Short term (≤ 2 years) |

| Acute shortage of Grade-A cold-storage capacity outside Riyadh is inflating lease costs | -0.3% | Regional, concentrated in Jeddah, Dammam, and secondary cities | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Chronic Equipment Imbalance

Security-driven Cape detours are causing chassis and 40-ft containers to pile up at distant ports, leaving exporters in Jeddah waiting 15-20 days for equipment while facing rental costs up to three times higher than normal. These imbalances put significant pressure on international forwarding margins, shrinking profitability by as much as five points during peak congestion cycles and creating operational challenges for 3PLs across the Saudi Arabia market[2]TradeArabia News Service, “Naqel Express Launches Two Logistics Facilities in Jeddah,” tradearabia.com .

Megaproject Traffic Congestion

Heavy construction traffic around NEOM and Qiddiya is extending urban delivery times by 25-40%. 3PLs are incurring higher operating costs from night-shift premiums, micro-hub rentals, and expanded small-truck fleets, putting pressure on last-mile margins. These elevated costs are expected to persist until major construction activity slows after 2028, temporarily reshaping profitability dynamics in the Saudi Arabia last-mile delivery market.

Segment Analysis

By Service: Landbridge Economics Propel International Growth

Domestic transportation commanded 43.33% of the 2025 revenue of the Saudi Arabia third-party logistics (3PL) market share, while international transportation management is projected to expand at a 5.2% CAGR, reflecting gains in land bridge speed that justify premium pricing. Value-added warehousing grows on bonded stockpiling and e-commerce fulfillment needs. Road remains versatile but faces rail competition on long hauls. Rail carries bulk and containerized shipments with 60-70% less carbon than trucks, aligning with disclosure rules. Airfreight handles urgent pharma and electronics traffic, while smart ports boost water-sector resilience.

The Saudi Arabia third-party logistics (3PL) market benefits when smart-port APIs reduce vessel dwell time to 2 days, improving carrier reliability. Domestic road demand remains solid across 2.15 million km² of territory, yet carbon regulations are nudging fleet upgrades. Warehousing leverages solar roofs and automation to meet green contract bids. Together, these service shifts diversify revenue and support a more balanced Saudi Arabia 3PL market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Pharma Cold-Chain Outpaces Energy

Energy & utilities commanded 22.12% of 2025 revenue of Saudi Arabia third-party logistics (3PL) market share, but life sciences & healthcare will lead growth at a 5.39% CAGR. Acute cold-storage gaps outside Riyadh raise lease prices 60% higher in Jeddah, yet also lock in long-term contracts. Retail and e-commerce volumes surge on quick-commerce rollouts, while automotive logistics gains from Hyundai’s 50,000-unit plant scheduled for 2026. Manufacturing uses bonded hubs to hold higher inventory in accordance with strategic reserve rules.

The Saudi Arabia 3PL market attracts pharma multinationals that demand GDP-certified handling, serial number tracking, and sub-two-hour airport transfers. Energy cargo remains vital but less dominant as renewables and diversification policies advance. Mixed end-user demand smooths cyclicality and supports cross-selling of value-added services.

Note: Segment shares of all individual segments available upon report purchase

By Logistics Model: Joint Ventures Speed Asset-Light Adoption

Asset-heavy incumbents commanded a 39.2% of Saudi Arabia third-party logistics (3PL) market share in 2025, and are projected to grow at a 5.26% CAGR, supported by joint ventures such as CEVA Almajdouie Logistics, which manages 2,000 assets without heavy capital requirements[3].CEVA Logistics, “CEVA Logistics and Almajdouie Finalize Joint Venture,” cevalogistics.com Hybrid structures that mix owned depots with managed fleets optimize balance-sheet risk as the Saudi Arabia 3PL market wrestles with carbon-linked capex. Asset-heavy incumbents still hold a 39.2% share, thanks to deep fleets and Saudisation compliance, but face rising electric-vehicle outlays.

Private equity poured USD 860 million into software, robotics, and last-mile apps in 2025, enabling asset-light entrants to punch above their weight. Management-fee revenue grows faster than trucking haulage, and digital control towers boost visibility. The model spread widens service quality gaps and shapes consolidation patterns across the Saudi Arabia 3PL market.

Geography Analysis

Red Sea and Gulf gateways gain competitiveness from 5G-ready cranes, AI berth allocators, and Ports Community System links that shave 2 days off dwell time. NEOM’s remote-controlled cranes, live from 2025, foreshadow next-gen automation for ultra-large vessels. Riyadh’s Special Integrated Logistics Zone offers 0% tax for 50 years and VAT exemptions, attracting regional distribution centers amid colder storage shortages in coastal cities[4]NEOM Media Center, “Port of NEOM Strengthens Role in Global Supply Chain Connectivity,” neom.com .

The Gulf Railway links Dammam, Riyadh, and Jeddah, cutting inland freight time in half and reducing emissions by 60-70%. Intermodal hubs are emerging near railheads, pushing the Saudi Arabia 3PL market toward container block trains for electronics and FMCG. Tier-2 urban nodes, including Khobar and Tabuk, see micro-hub investment to avoid megaproject congestion and to meet 30-minute delivery pledges.

Secondary airports expand charter cargo as SAL partners with Hail Region Development Authority, improving export lanes for agrifood and light manufacturing. GFH-GWC’s 200,000 m² pipeline adds Grade-A space in all three major cities, easing strategic-reserve and cold-chain needs. Geography, therefore, defines a multi-hub Saudi Arabia 3PL market rather than a Riyadh-centric one.

Competitive Landscape

International logistics leaders such as DHL, DSV, Maersk, Kuehne + Nagel, and UPS are aggressively scaling their operations in Saudi Arabia, with combined investment commitments exceeding EUR 500 million (USD 588.47 million). Their strategies increasingly emphasize sustainability, from solar-powered hubs to sophisticated emissions-tracking dashboards, reflecting a broader push toward green logistics. These global players leverage advanced digital tools, data-driven route optimization, and integrated supply chain platforms to differentiate themselves in a market where environmental accountability is becoming a commercial imperative.

Local incumbents, including Almajdouie and SAL, defend their market share through strong governmental relationships, compliance with Saudization requirements, and deep regional knowledge. Joint ventures such as DHL-Aramco ASMO and CEVA-Almajdouie illustrate a strategic blend of global technological expertise with local operational assets, highlighting how relational capital and digital capabilities can reinforce competitive positioning. Sustainability-linked contracts further enhance this dynamic, offering 8-12% price premiums for operators who can reliably quantify per-shipment carbon footprints, thereby embedding environmental performance directly into commercial agreements.

Niche segments such as pharma cold-chain logistics demonstrate moat-like economics, as scarcity of compliant providers creates high barriers to entry and elevates the strategic value of GDP-ready operators. Meanwhile, tier-2 city networks for quick-commerce last-mile delivery represent untapped potential, allowing agile 3PLs to capture high-frequency flows in groceries and pharmaceuticals. Venture capital investment accelerates robotics deployment, platform integration, and operational scaling, setting the stage for a wave of consolidation as emerging startups mature, and positioning Saudi Arabia as a testbed for next-generation, tech-enabled logistics solutions.

Saudi Arabia Third-Party Logistics (3PL) Industry Leaders

Almajdouie Group

Wared Logistics

DHL Supply Chain

Aramex

Hala Supply Chain Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: DHL signed an MoU with Hyperview Saudi to pilot hydrogen-powered long-haul trucks in Jubail as a proof-of-concept for sustainable freight operations.

- February 2025: DHL eCommerce signed an agreement to acquire a minority equity stake in Saudi parcel logistics provider AJEX Logistics Services, marking its strategic entry into Saudi Arabia’s e-commerce parcel market.

- January 2025: Aramex inaugurated a state-of-the-art robotic sorting facility at Jeddah Islamic Port featuring advanced automation with 120 robotic guided vehicles (RGVs), processing up to 96,000 shipments per day.

- October 2024: CEVA Logistics and Almajdouie Group finalized the creation of a joint venture named CEVA Almajdouie Logistics, The JV combines both companies’ transport and logistics operations to offer end-to-end integrated logistics and supply chain services across Saudi Arabia.

Saudi Arabia Third-Party Logistics (3PL) Market Report Scope

By Service

| Domestic Transportation Management (DTM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| International Transportation Management (ITM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| Value-Added Warehousing & Distribution (VAWD) |

By End User

| Automotive |

| Energy & Utilities |

| Manufacturing |

| Life Sciences & Healthcare |

| Technology & Electronics |

| E-commerce |

| Consumer Goods & FMCG |

| Food & Beverages |

| Others |

By Logistics Model

| Asset-Light (Management-Based) |

| Asset-Heavy (Own Fleet & Warehouses) |

| Hybrid |

| By Service | Domestic Transportation Management (DTM) | Roadways |

| Railways | ||

| Airways | ||

| Waterways | ||

| International Transportation Management (ITM) | Roadways | |

| Railways | ||

| Airways | ||

| Waterways | ||

| Value-Added Warehousing & Distribution (VAWD) | ||

| By End User | Automotive | |

| Energy & Utilities | ||

| Manufacturing | ||

| Life Sciences & Healthcare | ||

| Technology & Electronics | ||

| E-commerce | ||

| Consumer Goods & FMCG | ||

| Food & Beverages | ||

| Others | ||

| By Logistics Model | Asset-Light (Management-Based) | |

| Asset-Heavy (Own Fleet & Warehouses) | ||

| Hybrid | ||

Key Questions Answered in the Report

What is the projected value of the Saudi Arabia 3PL market by 2031

The market is forecast to reach USD 16.54 billion by 2031.

Which service category is growing fastest within the sector

International Transportation Management is advancing at a 5.2% CAGR, supported by landbridge and FTA tailwinds.

Why are Life Sciences & Healthcare contracts expanding so quickly

Acute cold-storage shortages and regulatory track-and-trace rules drive specialized logistics demand at a 5.39% CAGR.

What infrastructure will cut inland freight times the most

The Gulf Railway will halve transit times between Dammam–Riyadh-Jeddah and reduce carbon per ton-kilometer by up to 70%.

How are carbon-disclosure mandates affecting 3PL strategies

SASO 2025 rules push providers toward electric trucks, solar warehouses, and emissions software, enabling 8-12% pricing premiums for compliant services.

How much private capital entered Saudi logistics technology in 2025

Venture funding reached USD 860 million, a 116% year-on-year jump, backing automation and last-mile platforms.

Page last updated on: