Rolling Stock Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 35.25 Billion |

| Market Size (2031) | USD 42.44 Billion |

| Growth Rate (2026 - 2031) | 3.78% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

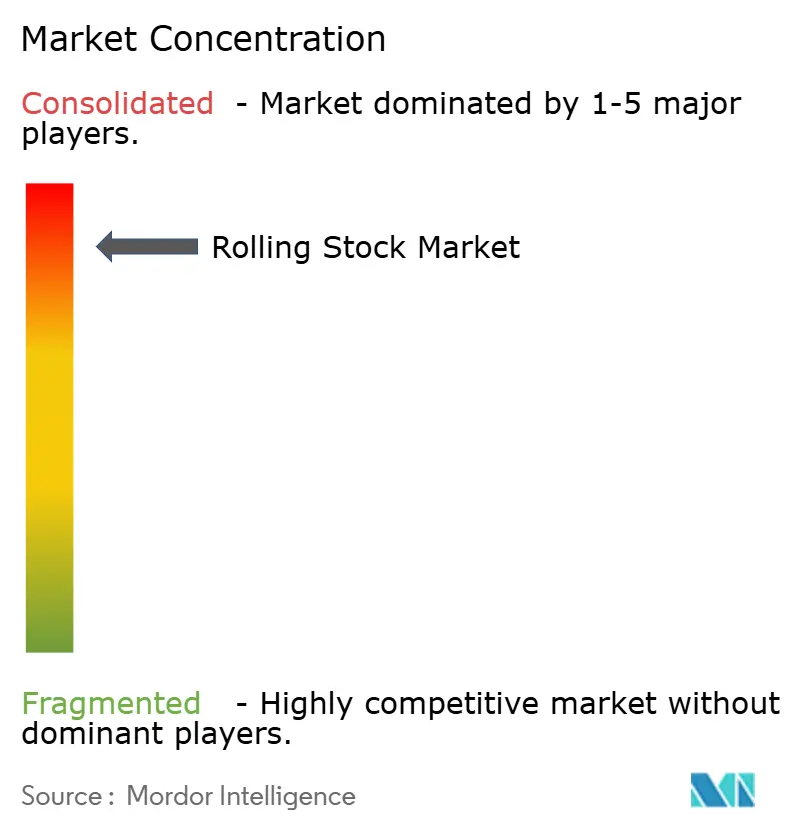

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Rolling Stock Market Analysis by ���ϲ�����

The rolling stock market size is projected to expand from USD 33.97 billion in 2025 and USD 35.25 billion in 2026 to USD 42.44 billion by 2031, registering a CAGR of 3.78% during the forecast period (2026-2031). Capital-intensive procurement cycles, sovereign budget allocations, and long delivery lead times shape purchasing behavior, so fleet renewal typically follows multi-year public investment plans rather than short consumer demand swings. Decarbonization mandates are encouraging operators to move away from diesel toward electric or hybrid propulsion, while urbanization has pushed metros and light rail to the front of municipal infrastructure agendas. Lifecycle service contracts, which bundle rolling stock, maintenance, spares, and digital analytics, are becoming a preferred financing model, locking in steady cash flows for suppliers and lowering operational risk for agencies. Moderate market concentration means global integrators must still localize carbody production, bogies, and after-sales services to comply with domestic-content rules and to compete with agile regional firms.

Key Report Takeaways

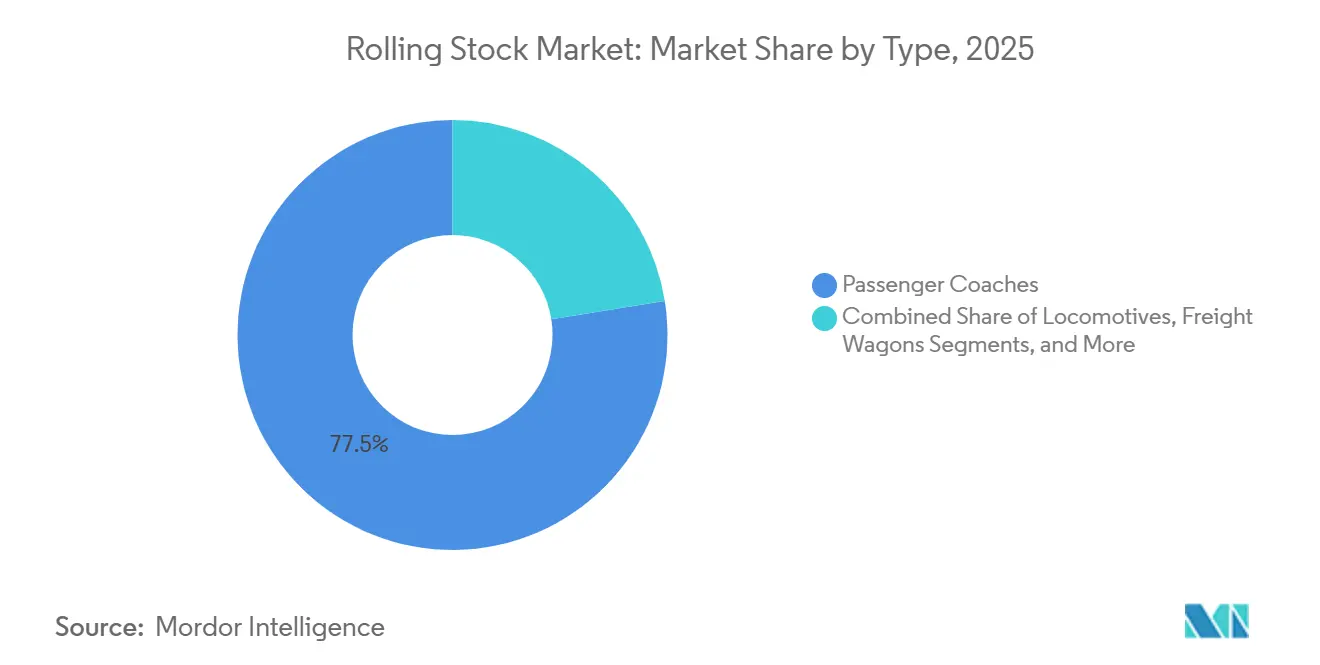

- By type, passenger coaches captured 77.53% of the rolling stock market share in 2025, while metros and light rail vehicles are projected to post the quickest expansion at a 13.11% CAGR through 2031.

- By propulsion, electric units accounted for 62.45% of the rolling stock market share in 2025, and this segment is advancing at a 5.74% CAGR over 2026-2031.

- By application, passenger rail accounted for 64.27% of the rolling stock market share in 2025 and is also the fastest-growing segment, rising at a 5.02% CAGR to 2031.

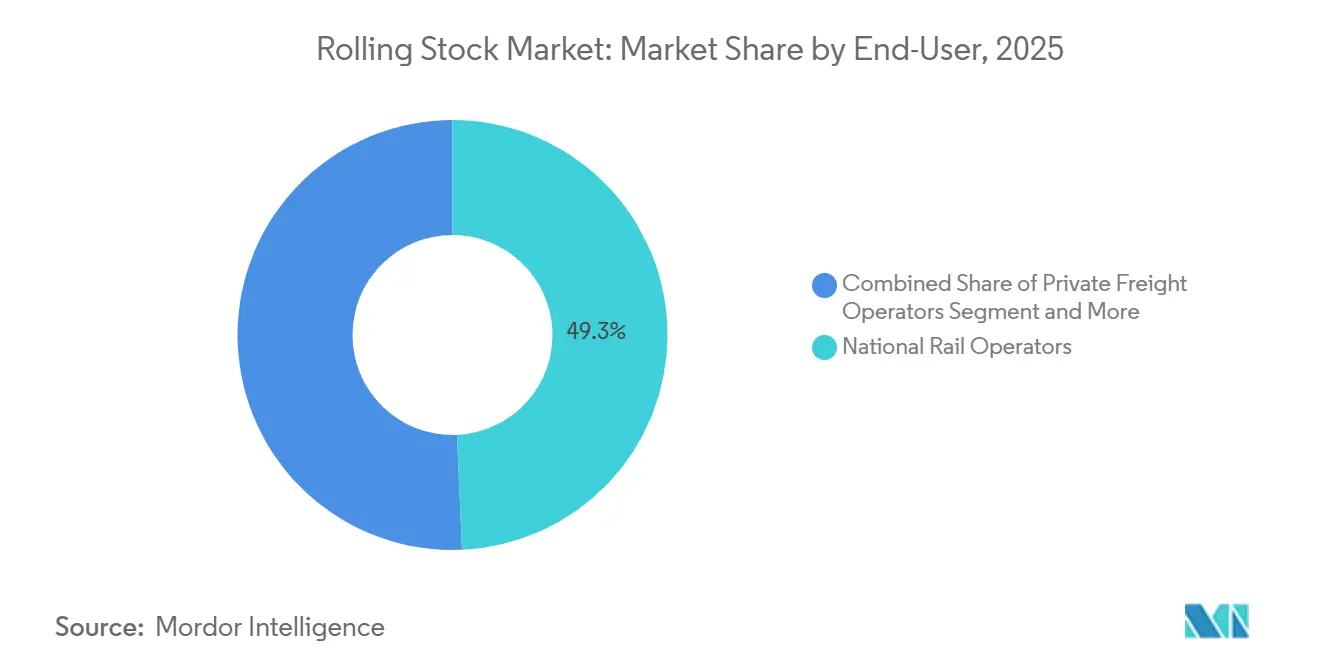

- By end user, national rail operators held 49.29% of the rolling stock market share in 2025; urban transit agencies are forecast to expand at a 7.27% CAGR through 2031.

- By technology, conventional fleets held a 94.53% of the rolling stock market share in 2025, but autonomous platforms are set to race ahead at an 11.78% CAGR over the same horizon.

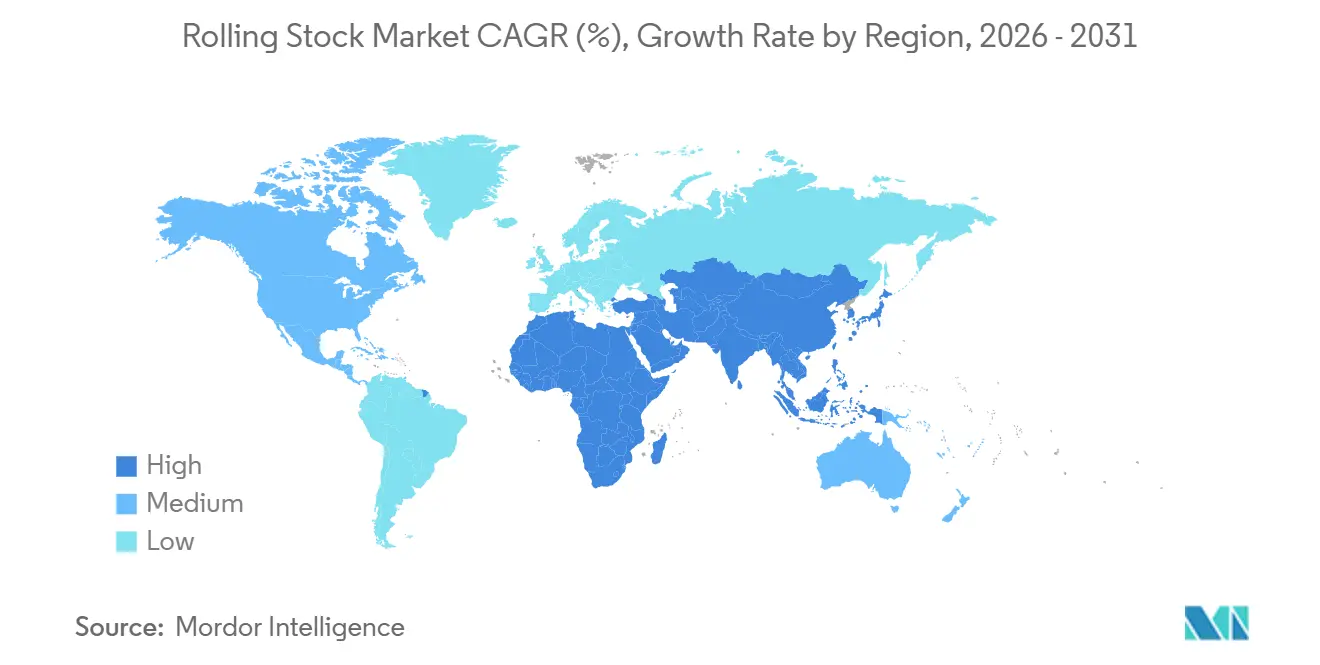

- By geography, Asia-Pacific accounts for 54.45% of the rolling stock market share in 2025, and the Middle East & Africa is growing at a 4.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rolling Stock Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Metro Expansion | +1.2% | APAC core, spill-over to MEA and South America | Medium term (2-4 years) |

| Decarbonization Policies | +0.9% | Global, with EU and China leading enforcement | Long term (≥ 4 years) |

| High-Speed Rail Corridors | +0.7% | Europe, APAC (China, India, Japan), North America | Long term (≥ 4 years) |

| Infrastructure Stimulus Packages | +0.6% | North America, EU, India | Medium term (2-4 years) |

| Lifecycle Service Contracts | +0.4% | Global, with mature markets (EU, North America) leading | Short term (≤ 2 years) |

| Zero-Emission Mandates | +0.3% | EU, Japan, select North American corridors | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Urbanization-Driven Metro Expansion

Rapid population growth in major Asian and Middle Eastern cities has made elevated or underground transit preferable to road widening, driving demand in the rolling stock market. China approved 15 new metro corridors in 2025, and India cleared several extensions under its 'Viksit Bharat 2047' vision, accelerating turnkey orders for vehicles coupled with signaling and depot technology[1]"Union Cabinet approves rail, metro, airport projects worth Rs 12,236 crore", The Economic Times, economictimes.indiatimes.com. Riyadh awarded Phase 2 contracts to expand its driverless network, illustrating how Grade-of-Automation-4 solutions reduce long-run labor costs. Municipal bond financing and multilateral loans now underwrite a large share of projects, bypassing slower sovereign budget processes. Consequently, suppliers that can deliver platform-level packages with tight delivery windows hold a competitive edge.

Decarbonization Policies Accelerating Electric Locomotives

Mandatory diesel phase-outs are shortening fleet lifecycles, especially in the European Union, where updated TEN-T rules require core freight corridors to be fully electrified by 2030[2]"Electrification of mobility Lessons learnt from the ECE region", UNECE, unece.org. India has committed to network-wide electrification by the same deadline, and China's incentives favor non-diesel traction on branch lines. These policies shift procurement toward three-phase AC electric or dual-mode units and penalize operators who delay conversion. Manufacturers with mature electric platforms and supply chains are therefore positioned for sustained order backlogs in the rolling stock market.

Government Investments in High-Speed Rail Corridors

Sovereign programs view high-speed rail as both climate infrastructure and a regional economic catalyst. The United States allocated new grants for California’s project, enabling contract awards for Siemens trainsets. Japan approved funding to extend the Hokkaido Shinkansen, requiring additional deliveries of rolling stock. India advanced its Mumbai–Ahmedabad line with a technology-transfer clause that embeds domestic manufacturing. These projects routinely include 15- or 20-year performance-based service contracts, moving revenue models from transactional sales to availability-based payments.

Infrastructure Stimulus Packages Boosting Rail CAPEX

Post-pandemic recovery bills merged with climate agendas to prioritize shovel-ready rail. The U.S. Infrastructure Investment and Jobs Act channeled funds into Amtrak’s new fleet orders, while the EU’s Connecting Europe Facility underwrites cross-border electrification. India’s updated National Infrastructure Pipeline sets aside dedicated funding for rolling stock aligned with freight-corridor buildouts. Compressed timelines are stretching supplier capacity, but forward order visibility encourages strategic investments in localized assembly hubs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost and Procurement Cycles | -0.5% | Global, acute in emerging markets with fiscal constraints | Medium term (2-4 years) |

| Supply-Chain Disruptions | -0.4% | Global, with North America and EU facing acute semiconductor shortages | Short term (≤ 2 years) |

| Regulatory Uncertainty | -0.2% | Europe, North America, cross-border corridors in ASEAN | Medium term (2-4 years) |

| Grid-Capacity Limits | -0.2% | India, Sub-Saharan Africa, Southeast Asia | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

High Capital Cost and Long Procurement Cycles

Electric multiple units can cost several million dollars per car, and high-speed trainsets often exceed USD 50 million each, in the rolling stock market. Competitive tenders typically span 2 to 3 years and require political and financial clearances, further delaying contract signing. Emerging-market buyers face currency and financing constraints, further delaying deals. Because the gap from order to entry into service can approach 6 years, manufacturers face significant working-capital exposure and margin risk if raw-material prices rise mid-production.

Raw-Material Inflation & Supply-Chain Disruptions

Since 2024, fluctuations in steel and copper prices, alongside chip shortages impacting traction inverters and signaling, have significantly extended lead times and necessitated frequent design revisions. While major OEMs, lacking vertical integration, employ partial hedging strategies, medium-sized suppliers frequently bear the full financial impact, squeezing their already tight margins. Operators are increasingly incorporating escalation clauses into contracts, but these additions can burden public budgets and, at times, delay tender approvals, causing frustration among stakeholders in the rolling stock market.

Segment Analysis

By Type: Metros Outpace Legacy Coaches

Passenger coaches retained 77.53% of the rolling stock market share in 2025, whereas metros and light rail vehicles, the fastest-growing sub-category, are forecast at a 13.11% CAGR through 2031. The popularity of driverless designs, compact station footprints, and higher passenger throughput underpin municipal preference for metros over traditional intercity coaches. Consortia that package vehicles with signaling and depot automation often clinch contracts because they shorten commissioning schedules and guarantee availability benchmarks.

Fleet planners in the rolling stock market still allocate significant budgets for coach overhauls, focusing on interior refurbishments, Wi-Fi upgrades, and energy-efficient HVAC systems that extend asset life. However, new-build coach demand is slowing as operators recalibrate services around flexible seating layouts and incremental digital enhancements. Suppliers differentiate by modularizing interiors and using recycled aluminum to meet sustainability targets without compromising structural rigidity.

Note: Segment shares of all individual segments available upon report purchase

By Propulsion: Electric Dominance, Hydrogen Emergence

Electric traction units accounted for a 62.45% share of the rolling stock market in 2025 and are growing at a 5.74% CAGR through 2031. Regulatory pressure, lower energy costs, and regenerative-braking savings keep electric propulsion firmly ahead of alternatives. Dual-mode configurations are bridging the gap where catenary coverage remains incomplete, giving operators route flexibility without full reliance on diesel.

Hydrogen and battery solutions are moving beyond demonstration into limited series production. While their combined share remains modest, dedicated rural routes and yard-switching operations provide use cases where zero-emission and off-grid functionality offer clear benefits. OEMs active in hydrogen platforms are forming alliances with energy providers to secure fuel infrastructure, an early-mover advantage that may pay off once volume uptake accelerates in the rolling stock market.

By Application: Passenger Rail Leads, Freight Seeks Efficiency

Passenger rail maintained 64.27% of the rolling stock market revenue in 2025 and is projected to post the quickest rise, advancing at a 5.02% CAGR through 2031. High urban population density, policy incentives, and congestion pricing all tilt in favor of public transit. Operators invest heavily in ride-quality, universal-access design, and on-board digital connectivity to rival short-haul air and road options.

Freight rail lags but remains strategically important as carbon-pricing schemes start to penalize long-haul trucking. Private operators focus on intermodal terminals and specialized wagons that handle temperature-sensitive or oversized cargo, reinforcing rail’s value proposition in high-value logistics chains. Predictive maintenance platforms reduce unplanned downtime, thereby improving asset turnover metrics critical to freight business models.

By End-User: Urban Transit Agencies Gain Autonomy

National rail operators accounted for 49.29% of the rolling stock market revenue in 2025, yet urban transit agencies are expanding fastest at a 7.27% CAGR to 2031. Devolved governance allows cities to approve projects quickly and to leverage municipal bonds, thereby speeding up rolling stock acquisition. Automated metros cut labor costs and enable 24-hour service, appealing to authorities under pressure to move more passengers without inflating operating budgets.

National incumbents are increasingly gravitating towards whole-life contracts, shifting the reliability risk to suppliers. This strategy aligns incentives and ensures smoother cash flows over extended periods, offering financial predictability. On the other hand, private freight operators are opting for lease models. These models free up capital from non-core assets, enabling them to scale capacity in response to shifting commodity cycles and market demand.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Autonomous Platforms Accelerate

Conventional trains still commanded 94.53% of the rolling stock market revenue in 2025, yet autonomous or driver-assist systems are advancing at an 11.78% CAGR. Urban networks lead adoption because grade-separated alignments mitigate safety risks, allowing agencies to capitalize on unattended operation to achieve higher service frequency. Suppliers bundle automatic train operation with platform screen doors and predictive analytics, pitching a holistic upgrade in safety and efficiency.

Mainline passenger and freight operators are leaning toward intermediate driver-assist features rather than full autonomy. This cautious approach stems from the challenges posed by mixed traffic and regulatory considerations. The modularity of these systems facilitates phased upgrades. Operators can first implement automatic speed regulation, followed by moving-block signaling, thereby distributing capital expenditures while simultaneously enhancing throughput and maintaining service reliability in the rolling stock market.

Geography Analysis

Asia-Pacific generated 54.45% of rolling stock revenue in 2025 and continues to anchor global demand. National planning commissions in China, India, and Japan approve large multi-line metro or high-speed schemes, ensuring steady order pipelines for both domestic and foreign suppliers. Southeast Asian projects often leverage development bank financing, paired with technology transfer clauses, to enable local assembly and skills development. Tier-1 cities adopt GoA4 automation, while smaller centers extend service life on diesel stock, illustrating a widening technological divide inside the region.

The Middle East and Africa post the swiftest growth, tracking a 4.92% CAGR. Gulf Cooperation Council members deploy driverless metros ahead of global events, signaling readiness to operate high-tech fleets in desert climates. North African capitals secure concessional European funding for line extensions and new vehicles. In contrast, Sub-Saharan states prioritize the rehabilitation of colonial-era corridors, hampered by limited grid capacity, and hence favor dual-mode or diesel-electric purchases until power infrastructure matures.

Europe maintains sizeable but maturing demand. Western operators extend fleet life through major overhauls, while Eastern members use EU Cohesion Funds to replace Soviet-era stock with modern electric or hybrid units. The United Kingdom’s HS2 orders and Scandinavian cross-border services keep high-speed assembly lines active. North America’s pipeline centers on Amtrak’s corridor upgrades and suburban fleet renewals, whereas South America depends mostly on Brazil’s metro expansions and Argentina’s commuter refurbishments, frequently involving Chinese financing that bundles rolling stock with infrastructure.

Competitive Landscape

The rolling stock market features moderate concentration, with the top five global integrators, CRRC, Alstom, Siemens, Stadler, and Hitachi Rail, able to execute turnkey metro or high-speed projects worldwide. Yet regional specialists such as Hyundai Rotem, CAF, and Titagarh Rail Systems win domestic tenders by leveraging cost advantages and government procurement preferences. Strategic consolidation is reshaping the ecosystem: Wabtec’s February 2026 acquisition of Dellner Couplers and Hitachi’s 2024 purchase of Thales Ground Transportation Systems highlight the push to integrate hardware, control, and digital services.

Technology is emerging as the chief battleground. Alstom’s commercial rollout of the Coradia iLint hydrogen unit, Siemens’ battery-electric Mireo Plus, and Stadler’s modular FLIRT platform underscore how alternative propulsion and lightweight composites help operators meet emission and energy-efficiency targets. Integrators embed predictive analytics, cloud-hosted condition monitoring, and cybersecurity into every new vehicle platform to secure multi-decade maintenance contracts.

Leasing and service-based models add competitive pressure. Entities such as GATX acquire locomotives for operating leases, allowing smaller freight lines to modernize without heavy capital outlay. Digital retrofit packages that raise existing fleets to GoA2 or GoA3 promise incremental revenue for suppliers and lower life-cycle costs for owners. Amid these shifts, OEMs are actively localizing assembly, with the United Kingdom, India, and the United States all hosting new plants opened since 2024 to satisfy domestic-content rules and reduce logistics risk.

Rolling Stock Industry Leaders

-

CRRC Corporation Limited

-

Alstom SA

-

Siemens AG

-

Stadler Rail AG

-

Hitachi Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Alstom rolled out the first refurbished train from CrossCountry’s renowned Voyager fleet. In the coming two years, Alstom is set to refurbish 136 Voyager Class 220 cars and 176 Super Voyager Class 221 cars at its Derby facility. The refurbishment program also encompasses 12 additional trains that were recently transitioned to CrossCountry after being released from Avanti West Coast.

- February 2026: SNCF Voyageurs, in collaboration with Île-de-France Mobilités (IDFM), initiated a tender to procure over 300 Z2N NG double-deck EMUs. This framework agreement, spanning 23 years, includes a confirmed order for 52 Z2N NG double-deck EMUs.

- October 2025: Sumitomo Corporation, in partnership with Nippon Sharyo, Ltd., clinched a contract from MRT Jakarta (MRTJ) – a company backed by Jakarta's Special Capital Region – to supply 48 subway cars for the North-South Line Phase 2A of the Jakarta Mass Rapid Transit (MRT).

- March 2025: Wabtec announced the USD 960 million acquisition of Dellner Couplers, adding an installed base of 100,000 couplers and 12,500 gangways and projecting USD 250 million in revenue in 2025.

Global Rolling Stock Market Report Scope

Rolling stock is generally employed for the transportation of goods, like heavy machinery, construction materials, conventional fuels, agricultural products, and so on, and passengers.

The Rolling Stock market is segmented by type, propulsion type, application, end-user, technology, and geography. By Type, the market is segmented into Locomotives (Diesel Locomotives, Electric Locomotives, and Hybrid/Hydro-Gen), Metros and Light Rail Vehicles, Passenger Coaches, and Freight Wagons. By Propulsion Type, the market is segmented into Diesel, Electric, Electro-diesel/Dual-mode, Hydrogen Fuel Cell, and Battery-electric. By Application, the market is segmented into Passenger Rail and Freight Rail. By End-user, the market is segmented into National Rail Operators, Private Freight Operators, and Urban Transit Agencies. By Technology, the market is segmented into Conventional and Autonomous / Driverless. By Geography, the market is segmented into North America (United States, Canada, and Rest of North America), South America (Brazil, Argentina, Chile, and Rest of South America), Europe (Germany, United Kingdom, France, Italy, Spain, Russia, and Rest of Europe), Asia-Pacific (China, India, Japan, South Korea, Australia, and Rest of Asia-Pacific), and Middle East and Africa (Saudi Arabia, United Arab Emirates, Turkey, South Africa, Egypt, and Rest of Middle East and Africa). Market forecasts are provided in terms of Value (USD) and Volume (Units).

| Locomotives | Diesel Locomotives |

| Electric Locomotives | |

| Hybrid / Hydrogen Locomotives | |

| Metros and Light Rail Vehicles | |

| Passenger Coaches | |

| Freight Wagons |

| Diesel |

| Electric |

| Electro-diesel / Dual-mode |

| Hydrogen Fuel Cell |

| Battery-electric |

| Passenger Rail |

| Freight Rail |

| National Rail Operators |

| Private Freight Operators |

| Urban Transit Agencies |

| Conventional |

| Autonomous / Driver-Assist |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Locomotives | Diesel Locomotives |

| Electric Locomotives | ||

| Hybrid / Hydrogen Locomotives | ||

| Metros and Light Rail Vehicles | ||

| Passenger Coaches | ||

| Freight Wagons | ||

| By Propulsion Type | Diesel | |

| Electric | ||

| Electro-diesel / Dual-mode | ||

| Hydrogen Fuel Cell | ||

| Battery-electric | ||

| By Application | Passenger Rail | |

| Freight Rail | ||

| By End-user | National Rail Operators | |

| Private Freight Operators | ||

| Urban Transit Agencies | ||

| By Technology | Conventional | |

| Autonomous / Driver-Assist | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is global demand for new rail vehicles expected to grow through 2031?

Installations are forecasted to rise at a 3.78% CAGR as public investment programs and urban transit expansion offset longer procurement cycles.

Which propulsion technology holds the largest fleet share today?

Electric traction dominates with about 62.45% of spending, owing to network electrification mandates and lower energy costs.

Why are metros attracting more investment than traditional coaches?

Urban congestion and automation benefits push cities to favor grade-separated metros, making them the quickest-growing type at a 13.11% CAGR.

What is driving interest in hydrogen and battery-electric locomotives?

Zero-emission regulations for non-electrified routes motivate operators to trial hydrogen and battery platforms where catenary is impractical.

How are lifecycle service contracts reshaping supplier–operator relationships?

Bundled maintenance and availability guarantees shift revenue from one-time sales to decades-long partnerships, aligning performance incentives.