Refrigeration Coolers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.71 Billion |

| Market Size (2031) | USD 6.52 Billion |

| Growth Rate (2026 - 2031) | 6.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Refrigeration Coolers Market Analysis by ���ϲ�����

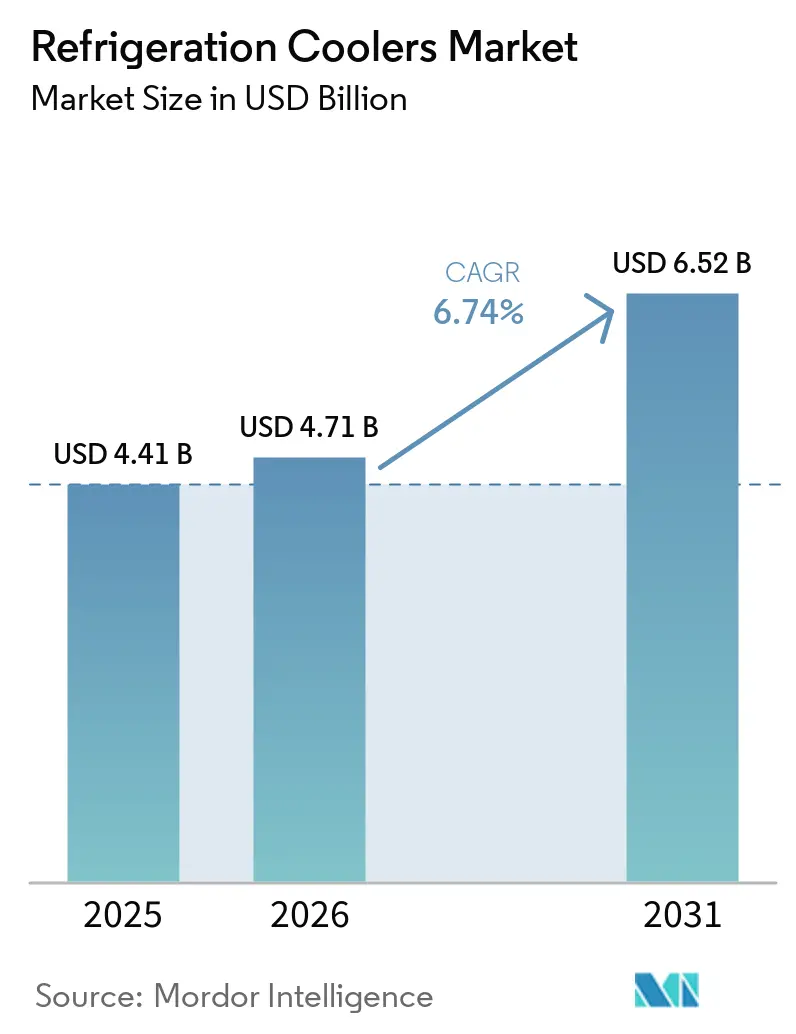

The refrigeration coolers market size is projected to expand from USD 4.41 billion in 2025 and USD 4.71 billion in 2026 to USD 6.52 billion by 2031, registering a CAGR of 6.74% between 2026 and 2031. The refrigeration coolers market is being boosted by parallel investments in cold-chain warehousing, food retail remodeling, pharmaceutical logistics, and industrial upgrades as operators replace older, high-GWP systems and build new capacity. Upgrade cycles that once moved slowly are now tightening because HFC phase-down rules, greenfield cold-storage construction, and connected monitoring tools are all pushing equipment decisions forward simultaneously. The refrigeration coolers market is also seeing capital shift away from HFC-dependent centralized racks and toward natural-refrigerant platforms, controls, and application-specific systems for demanding environments. Competitive intensity in the refrigeration coolers market remains moderate to high, as established European, American, and Japanese specialists compete directly with broader HVAC and refrigeration OEMs. Regional momentum is not uniform, since technician shortages and uneven policy timelines are creating faster adoption in Europe and Japan and a more mixed path in the United States and parts of the Middle East.

Key Report Takeaways

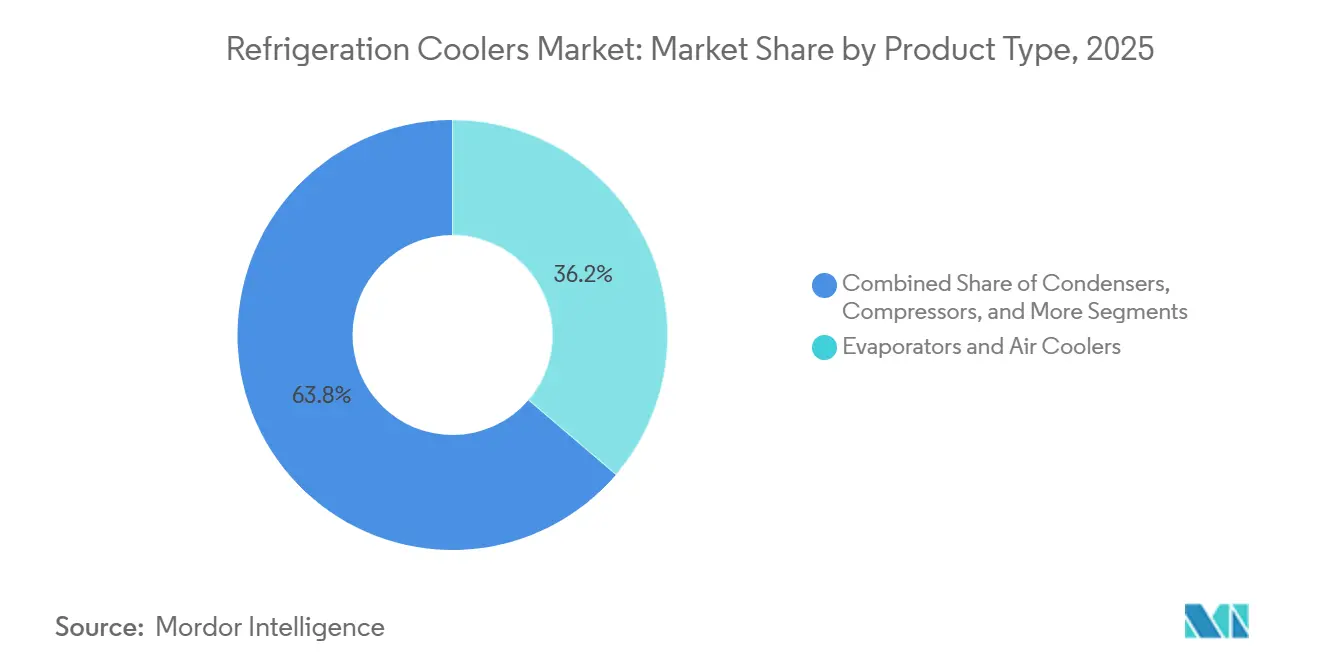

- By product type, evaporators and air coolers held 36.24% share of the refrigeration coolers market in 2025, while magnetic cooling modules are forecast to grow at a 6.81% CAGR through 2031.

- By refrigerant type, ammonia held 29.11% share of the refrigeration coolers market in 2025, while Carbon Dioxide (CO₂) is projected to expand at a 6.95% CAGR through 2031.

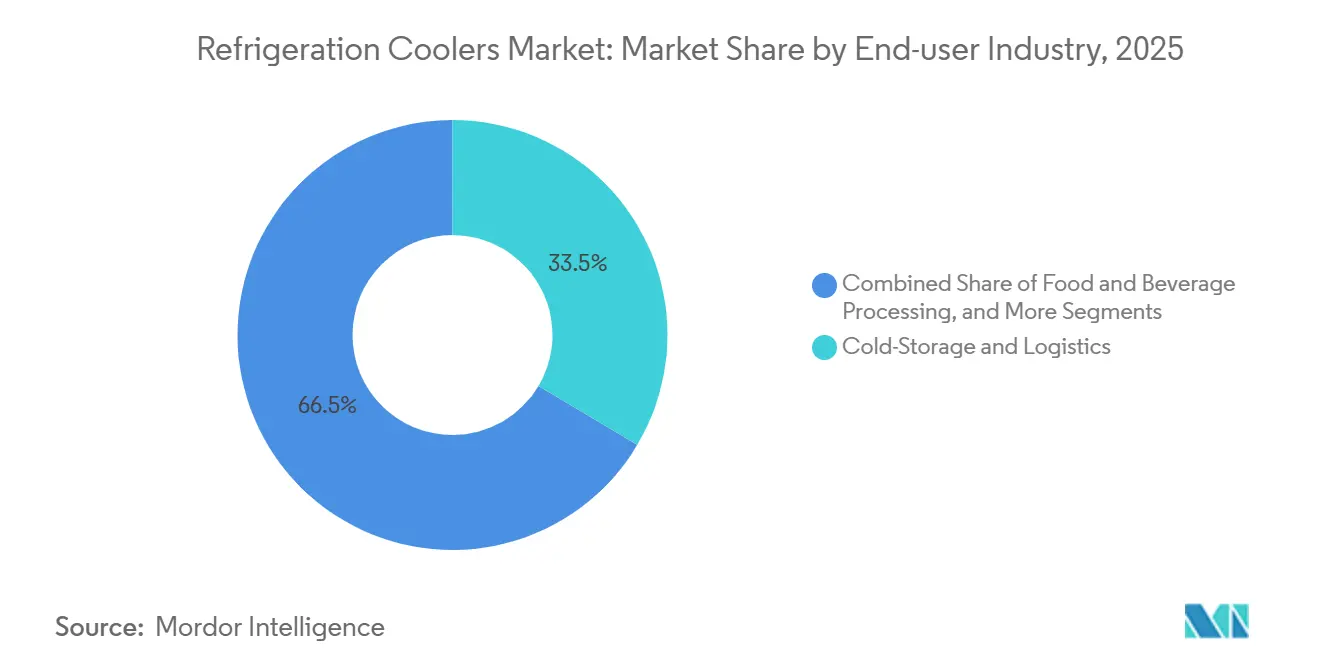

- By end-user industry, cold-storage and logistics led represented 33.53% share of the refrigeration coolers market in 2025, while data centers and electronics cooling is forecast to grow at a 7.05% CAGR through 2031.

- By system type, centralized rack systems held 41.12% share of the refrigeration coolers market in 2025, while hybrid and transcritical CO₂ systems are projected to grow at a 6.79% CAGR through 2031.

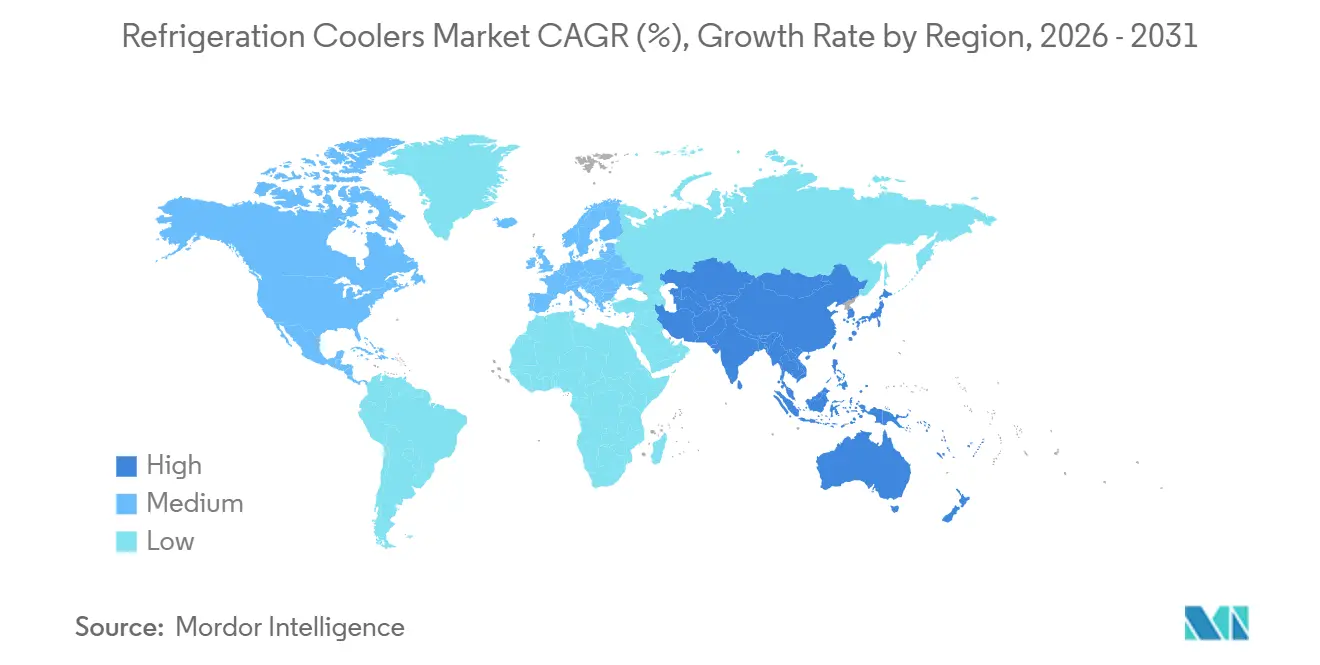

- By geography, Asia-Pacific held 43.33% share of the refrigeration coolers market in 2025, and it is also the fastest-growing regional segment with a 6.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Refrigeration Coolers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion Of Cold-Chain Warehousing And Last-Mile Cold Logistics | +2.0% | Global, with particularly strong pull in South Asia, Southeast Asia, and North America | Short term (≤ 2 years) |

| Tightening HFC Phase-Down And Low-GWP Refrigerant Migration | +1.8% | Global, most acute in EU, UK, and Japan, accelerating in North America and South America | Medium term (2-4 years) |

| Growth In Retail Food Merchandising And Convenience Formats | +1.2% | Global, highest intensity in Asia-Pacific and North America | Short term (≤ 2 years) |

| AI-Enabled Monitoring And Predictive Maintenance Adoption | +0.8% | North America, Europe, and Australia, with rapid adoption in APAC core | Medium term (2-4 years) |

| Higher R290 Charge Limits Enabling Larger Plug-In Cabinets | +0.5% | North America and EU core, spillover to Middle East and APAC | Short term (≤ 2 years) |

| Public Funding And Retail Rollouts Accelerating CO₂ Refrigeration Adoption | +0.4% | Japan, Germany, South Korea, Canada, emerging in South America | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Expansion Of Cold-Chain Warehousing And Last-Mile Cold Logistics

The refrigeration coolers market is benefiting from a clear capital-spending cycle in temperature-controlled infrastructure, following years of underinvestment across parts of Asia, Africa, and South America. Lineage reported 83 automated warehouses and a development pipeline with an estimated total cost of USD 1.095 billion on December 31, 2025, covering both greenfield and automated projects in the United States and Europe. Americold and EQT then announced a USD 1.3 billion North American cold-storage joint venture in May 2026, which showed that institutional capital was still backing multi-year capacity growth. Automated sites also require tighter temperature consistency than conventional warehouses, which lifts demand for higher-specification evaporators, controls, and monitoring layers rather than just more equipment. This makes cold-chain build-out a durable demand source for the refrigeration coolers market through the rest of the decade.

Tightening HFC Phase-Down And Low-GWP Refrigerant Migration

Tighter low-GWP compliance deadlines in major regions are also pulling forward the refrigeration coolers market. The revised EU F-Gas framework has accelerated phase-down timelines and is pushing new centralized refrigeration systems above 40 kW toward an average GWP below 150 by 2032. That shift affects full system architecture because compressors, heat exchangers, controls, and piping often need replacement when operators move from HFC centralized racks to CO₂ transcritical or ammonia-based systems.[1]Danfoss A/S, “F-Gas Regulation, HFC Phase-Down Timeline,” Danfoss, danfoss.com Germany’s food retail sector directed 60% of its energy efficiency investment to refrigeration technology in early 2026, demonstrating how compliance pressure is shaping capex priorities. In the United States, the EPA revised certain AIM Act timelines in May 2026 and extended some grocery equipment deadlines to 2032, but large retailers were already moving ahead with CO₂-based new-build decisions, indicating that market demand in the refrigeration cooler market is now running ahead of minimum policy requirements.

Growth In Retail Food Merchandising And Convenience Formats

The refrigeration coolers market continues to draw steady volume from convenience expansion and organized food retail upgrades across Asia-Pacific and the Americas. In Japan, transcritical CO₂ penetration in convenience stores rose to 18% in 2025 from 16% in 2024, suggesting ongoing replacement demand in a very large installed base. Retail conversion programs at scale create recurring orders for condensing units, display evaporators, and related accessories because store fleets are upgraded in stages rather than all at once. Germany again showed the investment pattern clearly, with refrigeration taking more than 60% of total food retail energy efficiency spending in 2026. The refrigeration coolers market is therefore getting more of its volume from convenience footprints, remodel cycles, and smaller store formats where plug-in and remote systems compete on installation ease and total ownership cost.

AI-Enabled Monitoring And Predictive Maintenance Adoption

The refrigeration cooler market is getting an additional boost from digital tools, as refrigeration still accounts for a large share of store electricity and maintenance costs. EHI data showed that refrigeration accounts for 52% of total electricity use in food retail, which keeps optimization projects high on the spending list. Danfoss stated that its Alsense platform and Microsoft AI integration can help supermarkets cut food waste by up to 30% and reduce refrigeration energy use by up to 15%. Bueno Analytics reported a 22% reduction in refrigeration ice-up callouts across Woolworths’ connected fleet, with 95% detection accuracy and 5-7 days of advance notice for servicing. A 2026 peer-reviewed study also found that AI-assisted model predictive control in meat processing refrigeration could deliver energy savings of up to 36%, which supports faster adoption of connected hardware and controls across the refrigeration coolers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Retrofit And First-Cost Burden For Compliant Systems | -1.8% | Global, most pronounced in price-sensitive emerging markets and SME food retail | Medium term (2-4 years) |

| Shortage Of Technicians Certified For CO₂, Ammonia, And Hydrocarbons | -1.2% | Global, most acute in North America, India, and Southeast Asia | Long term (≥ 4 years) |

| Patchy Building Code Adoption For Larger Hydrocarbon Charges | -0.8% | United States with state-level variance, Southeast Asia, Middle East | Medium term (2-4 years) |

| Grid Instability In Emerging Cold Chains | -0.5% | Sub-Saharan Africa, South and Southeast Asia, parts of South America | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

High Retrofit And First-Cost Burden For Compliant Systems

The refrigeration coolers market still faces a clear first-cost barrier when operators move from HFC centralized systems to CO₂ transcritical or ammonia-based architectures. Danfoss noted that a transcritical CO₂ booster system typically costs 15-25% more upfront than a comparable HFC rack, and the gap widens further in warm climates that require extra efficiency-support hardware. That burden is especially hard on smaller food retail operators, where Germany’s EHI Retail Institute recorded investment rates of EUR 961 (USD 1,040) per square meter in 2025, which the supplied draft converted to USD 1,057 per square meter using 2025 exchange rates. Japan’s Ministry of Environment offers grants of up to JPY 500 million (USD 3.46 million), which the supplied draft converted to USD 3.3 million using the IRS 2024 yearly average rate of JPY 151.98 (USD 1.06) per USD, but subsidy coverage is still not universal.[2]Japan Ministry of Environment, “Cold Chain De-fluorination and Decarbonization Promotion Subsidy, FY2025,” Ministry of the Environment Japan, env.go.jp This leaves the refrigeration cooler market on a two-speed path, with large chains and logistics owners moving earlier, while smaller operators continue to delay replacement decisions.

Shortage Of Technicians Certified For CO₂, Ammonia, And Hydrocarbons

The refrigeration coolers market is also being slowed by a labor constraint that equipment makers cannot solve through product supply alone. NASRC’s March 2026 Food Retailer Survey identified the shortage of trained technicians as the most important barrier to faster refrigerant transition across US food retail chains. CO₂ transcritical systems run at much higher pressures than typical HFC rack systems, which means contractors need different tools, safety practices, and diagnostic skills before new systems can be supported at scale. Copeland’s renovated Vilter facility in Cudahy, Wisconsin, added 16,000 square feet of training space in May 2026, which showed that suppliers now treat workforce development as a capital need. The gap is most visible among small and mid-size contractors, which limits how quickly replacement work can be mobilized even when owner demand is already there, and it remains a meaningful drag on the refrigeration coolers market. EPA Section 608 rules and EU F-Gas training requirements provide a baseline, but local enforcement still does not consistently push legacy technicians to recertify for natural refrigerants.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Evaporators Lead As Solid-State Cooling Builds A Commercial Foothold

Evaporators and air coolers accounted for 36.24% of the refrigeration cooler market in 2025, the largest share among product types. Their lead reflects their widespread use across every system architecture, from self-contained display cases to centralized industrial cold rooms. In the refrigeration coolers industry, that position is reinforced every time a warehouse, supermarket, or pharmaceutical cold room adds or replaces cooling equipment. Compressors, condensers, and accessories still account for much of the remaining demand because refrigerant transitions often require component-level upgrades, even when full-system replacement is delayed.

Magnetic cooling modules are projected to grow at a 6.81% CAGR through 2031, making them the fastest-growing product type in the refrigeration coolers market. MAGNOTHERM Solutions launched a pilot deployment of its ECLIPSE refrigerant-free cabinet in REWE stores in 2026.[3]MAGNOTHERM Solutions and REWE Group, “MAGNOTHERM and REWE Group Launch Magnetic Cooling Pilot in German Supermarkets,” Station Frankfurt, station-frankfurt.de REWE planned 10-20 installations, and earlier in-store testing showed that the unit used 15% less energy than a comparable R290 cabinet while maintaining product temperature within the target range. The segment remains small in absolute terms, but the refrigeration coolers market is beginning to treat solid-state cooling as a credible long-range option for high-efficiency commercial use cases.

By Refrigerant Type: Ammonia Holds The Industrial Base While CO₂ Gains Speed In Commercial Use

Ammonia retained the largest share at 29.11% of the refrigeration coolers market in 2025, reflecting its entrenched role in industrial cold storage, food processing, and district cooling. That installed base remains stable because many NH₃ systems are designed to operate for 20-40 years under heavy-duty conditions. LU-VE reported new low-charge ammonia unit coolers with recirculation ratios as low as 1.8, demonstrating that suppliers are extending the operating range of ammonia systems rather than forcing full replacement. HFC and HFO blends still hold a place among budget-constrained operators, but the phase-down path continues to erode that position in the refrigeration coolers market.

Carbon Dioxide (CO₂) is the fastest-growing refrigerant type with a 6.95% CAGR through 2031. European transcritical CO₂ installations reached 111,650 sites in 2025, and penetration in European food retail rose to 34% of stores. North America reached 6,360 food retail and industrial sites in 2025 with 28% year-over-year growth, and major chains, including ALDI US, Costco, Kroger, Loblaws, and Target, had already committed to CO₂ for new builds. Copeland’s December 2025 launch of a transcritical CO₂ scroll compressor with dynamic vapor injection showed that the refrigeration coolers market is no longer treating this shift as a narrow compliance response, but as a broader platform change across components and service models.

By End-User Industry: Cold Storage Leads While Data Centers Add A New Demand Layer

Cold storage and logistics held 33.53% of the refrigeration cooler market share in 2025, making it the largest end-user segment. NewCold’s third expansion phase in Lebanon, Indiana, included a USD 500 million investment in a new automated facility, underscoring the scale of greenfield demand still entering the refrigeration cooler market. Food and beverage processing remains another major demand center, as operators pursue both compliance and direct energy savings through industrial CO₂ and low-charge ammonia systems. Cencosud’s rollout of 22 transcritical CO₂ stores across 5 South American countries by 2025, including 7 additions in 2025, delivered 16-17% lower absolute energy use and showed what that conversion logic can look like in practice.

Data centers and electronic cooling are the fastest-growing end-user segment, with a 7.05% CAGR through 2031. In the refrigeration coolers industry, that growth reflects the rising heat density of AI-oriented computing loads that are pushing beyond the practical range of conventional air cooling. LU-VE supplied 102 CO₂ evaporators for a 1.5 MW transcritical CO₂ cooling system at a data center in Paterna, Spain, in March 2026, which marked one of the first large-scale cases of CO₂ as a primary refrigerant in this setting. Pharmaceuticals and life sciences are also supporting steady demand in the refrigeration coolers market because biologics and cell and gene therapies require dependable cold-chain performance and tighter procurement standards.

By System Type: Centralized Racks Remain Large While CO₂ Architectures Gain Ground

Centralized rack systems accounted for 41.12% of the refrigeration cooler market in 2025, making them the leading system type. Their long-standing strength comes from centralized maintenance, scale efficiencies, and the way large grocery stores were historically designed around rack-room layouts. That same installed base is now more exposed to regulation, as large, centralized HFC systems are among the earliest categories to face tighter restrictions under EU Regulation 2024/573. Metro completed 49 F-Gas Exit projects in fiscal 2025, planned 40 more in 2026, and had already shifted 73% of its EU stores to natural refrigerants, demonstrating how major retailers are responding in the refrigeration market.

Hybrid and transcritical CO₂ systems are projected to grow at a 6.79% CAGR from 2026 to 2031, which makes them the fastest-growing system type. NASRC reported that 1,470 of more than 2,000 new US grocery stores planned through 2029 had already selected transcritical CO₂ refrigeration systems. Self-contained systems are also gaining support following the EPA SNAP Rule 26, which raised the maximum R290 charge limit to 500 grams for open self-contained cases and 300 grams for closed cases. Hillphoenix’s Next Generation Flex Mini, launched in March 2026, reflects how the refrigeration coolers market is moving toward lower installation complexity, simpler service, and closer performance parity with legacy systems.

Geography Analysis

Asia-Pacific accounted for 43.33% of the refrigeration coolers market in 2025 and is projected to grow at a 6.88% CAGR through 2031. The region’s position in the refrigeration coolers market is being shaped by cold-storage build-out, organized retail expansion, and policy-backed refrigerant transitions, all occurring simultaneously. Japan had 14,350 food retail stores using transcritical CO₂ systems in 2025, and penetration in convenience stores and supermarkets rose to 18% from 16% in 2024.[4]ATMOsphere, “New Data Natural Refrigerants in Commercial and Industrial in Asia,” Natural Refrigerants, naturalrefrigerants.com In July 2025, AEON said it aims to shift all domestic store refrigeration equipment to natural refrigerants by 2040. Japan’s cold-chain de-fluorination subsidy and Lotte Global Logistics’ May 2026 completion of its Dong Nai Cold Chain Center in Vietnam show that both public support and private logistics investment are still expanding regional demand.

Europe is a mature but still very active part of the refrigeration coolers market, with 106,000 food retail outlets already using CO₂ rack or condensing-unit systems and EU-wide penetration at 34%, while rack installations rose from 76,200 sites in 2024 to 88,000 in 2025. METRO’s global natural refrigerant penetration reached 59%, and 73% of its EU stores were already on natural refrigerants, with 40 more projects planned in 2026. Germany stands out because food retail directed 60% of energy-efficiency investment to refrigeration, keeping this equipment category at the center of store modernization. Electricity use per square meter fell from 317 kWh in 2018 to 289 kWh in 2025, yet refrigeration still accounted for 52% of total food retail electricity use, underscoring why modernization remains active in the refrigeration market.

North America is moving at a differentiated pace, and the refrigeration coolers market there is being shaped more by retailer strategy than by the extended federal timelines in some categories. The EPA’s May 2026 AIM Act revision extended certain grocery equipment deadlines to 2032, but voluntary commitments from large retailers continued to support CO₂ transcritical as the preferred platform for new stores. Americold’s Port Saint John project and the Americold-EQT joint venture point to continued strength in cold-storage infrastructure spending across the region. South America remains smaller but is still advancing, while Cencosud’s rollout across 5 countries shows the natural-refrigerant model is spreading, and the Middle East and Africa continue to offer food security-led potential even as grid reliability remains a real constraint in several underdeveloped markets.

Competitive Landscape

The refrigeration coolers market is moderately consolidated. Daikin Industries, Danfoss A/S, Emerson’s Copeland brand, GEA Group, and Johnson Controls International continue to anchor global supply across components and systems in the refrigeration coolers market. Competitive separation is now coming more from technology stacks than from manufacturing scale alone. Danfoss has built a broad CO₂ offering across ejectors, condensing units, controls, and cloud monitoring, making it harder for single-product rivals to match the full-system value for food retail customers. Haier Smart Home’s October 2024 acquisition of Carrier’s commercial refrigeration business for USD 775 million reshaped the competitive map by bringing CO₂ licenses and a global installed base into Haier’s portfolio.

White-space opportunity in the refrigeration coolers market is clearest in data center cooling and AI-enabled service platforms. LU-VE signed a multi-year framework agreement worth more than EUR 100 million (USD 113 million), which the supplied draft converted to USD 110 million, with a global hyperscaler in April 2026 and then expanded its Texas production hub in May 2026.[5]LU-VE S.p.A., “LUVE Has Signed a Multi-Year Supply Agreement for Data Centre Cooling Solutions Worldwide,” LU-VE, lu-ve.com Hillphoenix’s Flex Mini platform added low-pressure ejector technology, a filter-less oil separator, and dual-brand compressor compatibility, demonstrating that standards compliance and service simplification are now product design priorities. Certification demands and leak-detection requirements are also raising the technical threshold for entry, which supports continued demand for specialized controls and accessories inside the refrigeration coolers market.

Emerging disruptors in the refrigeration coolers market include MAGNOTHERM Solutions and other solid-state cooling developers, although they remain some distance from broad cost parity with vapor-compression systems. EVAPCO’s May 2026 launch of PuRe-JET showed that innovation is also continuing in industrial and commercial heat rejection and adiabatic cooling. Güntner’s Aicore Cloud push and Danfoss’s Active Cooling expansion show that monitoring, efficiency, and oil-free performance are becoming more important competitive tools across adjacent applications. The refrigeration coolers market, therefore, continues to favor suppliers that can combine refrigerant compliance, service simplicity, digital visibility, and application breadth across retail, industrial, and mission-critical sites.

Refrigeration Coolers Industry Leaders

Daikin Industries, Ltd.

Rivacold S.r.l.

Danfoss A/S

Johnson Controls International plc

Modine Manufacturing Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: LU-VE S.p.A. inaugurated a 20,000 square-meter expansion of its Jacksonville, Texas, manufacturing facility, bringing the total surface area to over 30,000 square meters. In the same period, LU-VE signed a multi-year framework agreement worth over EUR 100 million (USD 113 million), approximately USD 110 million, with a global hyperscaler for the supply of advanced cooling solutions for data center facilities. The expansion positions LU-VE as a major supplier for the rapidly growing North American data center cooling segment.

- May 2026: EVAPCO introduced PuRe-JET™, a pumpless adiabatic cooling system that eliminates mechanical pumps through a proprietary ejector device, targeting lower water use, reduced maintenance complexity, and improved thermal performance in industrial and commercial refrigeration applications.

- April 2026: Danfoss launched the Optyma™ iCO₂ 37 kW MT and 20 kW LT condensing units, the largest-capacity model in its CO₂ condensing unit portfolio, designed for medium- and low-temperature commercial refrigeration applications and featuring brushless two-stage compressors for an expanded operating range.

- March 2026: Hillphoenix, a Dover Food Retail brand, launched the Next Generation Flex Mini CO₂ transcritical system for the food retail and industrial markets. The unit features advanced low-pressure ejector technology, a filter-less oil separator, dual-brand compressor compatibility, and multiple voltage options, reducing installation complexity for smaller-format stores and industrial applications.

Global Refrigeration Coolers Market Report Scope

The Refrigeration Coolers Market Report is Segmented by Product Type (Evaporators and Air Coolers, Condensers, Compressors, Magnetic Cooling Modules, Controls and Accessories, and Other Product Types), Refrigerant Type (Ammonia (NH₃), Carbon Dioxide (CO₂), HFC/HFO Blends, Hydrocarbons (R-290, R-600a), and Other Refrigerant types), End-user Industry (Food and Beverage Processing, Cold-Storage and Logistics, Supermarkets and Hypermarkets, Pharmaceuticals and Life-Sciences, Data Centres and Electronics Cooling, and Other End-user Industries), System Type (Self-Contained (Plug-in), Remote Condensing Units, Centralised Rack Systems, Hybrid / Transcritical CO₂ Systems, and Other System Types), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Evaporators and Air Coolers |

| Condensers |

| Compressors |

| Magnetic Cooling Modules |

| Controls and Accessories |

| Other Product Types |

| Ammonia (NH₃) |

| Carbon Dioxide (CO₂) |

| HFC/HFO Blends |

| Hydrocarbons (R-290, R-600a) |

| Other Refrigerant Types |

| Food and Beverage Processing |

| Cold-Storage and Logistics |

| Supermarkets and Hypermarkets |

| Pharmaceuticals and Life-Sciences |

| Data Centres and Electronics Cooling |

| Other End-user Industries |

| Self-Contained (Plug-in) |

| Remote Condensing Units |

| Centralised Rack Systems |

| Hybrid / Transcritical CO₂ Systems |

| Other System Types |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Evaporators and Air Coolers | |

| Condensers | ||

| Compressors | ||

| Magnetic Cooling Modules | ||

| Controls and Accessories | ||

| Other Product Types | ||

| By Refrigerant Type | Ammonia (NH₃) | |

| Carbon Dioxide (CO₂) | ||

| HFC/HFO Blends | ||

| Hydrocarbons (R-290, R-600a) | ||

| Other Refrigerant Types | ||

| By End-user Industry | Food and Beverage Processing | |

| Cold-Storage and Logistics | ||

| Supermarkets and Hypermarkets | ||

| Pharmaceuticals and Life-Sciences | ||

| Data Centres and Electronics Cooling | ||

| Other End-user Industries | ||

| By System Type | Self-Contained (Plug-in) | |

| Remote Condensing Units | ||

| Centralised Rack Systems | ||

| Hybrid / Transcritical CO₂ Systems | ||

| Other System Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current and forecast value of refrigeration coolers?

The refrigeration coolers market was valued at USD 4.41 billion in 2025, rises to USD 4.71 billion in 2026, and is forecast to reach USD 6.52 billion by 2031 at a 6.74% CAGR.

Which region leads global demand for refrigeration coolers?

Asia-Pacific led with a 43.33% share in 2025 and is also the fastest-growing region through 2031, supported by cold-chain expansion, organized retail growth, and refrigerant transition programs.

Which product category holds the largest share in this space?

Evaporators and air coolers led product demand with a 36.24% share in 2025 because they are required across nearly every refrigeration architecture.

What is driving faster adoption of CO2-based systems?

Tighter F-Gas and AIM Act rules, strong retailer commitments, and validated energy performance are pushing more new-build and retrofit decisions toward CO2 platforms.

Why are data centers becoming important for cooling suppliers?

Data centers and electronics cooling is the fastest-growing end-user area at a 7.05% CAGR through 2031, as AI workloads raise thermal density and require more specialized cooling systems.

What are the main barriers slowing adoption of compliant systems?

Higher retrofit costs and the shortage of trained technicians for CO2, ammonia, and hydrocarbon systems remain the two most visible constraints on broader conversion activity.

Page last updated on: