Radar Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

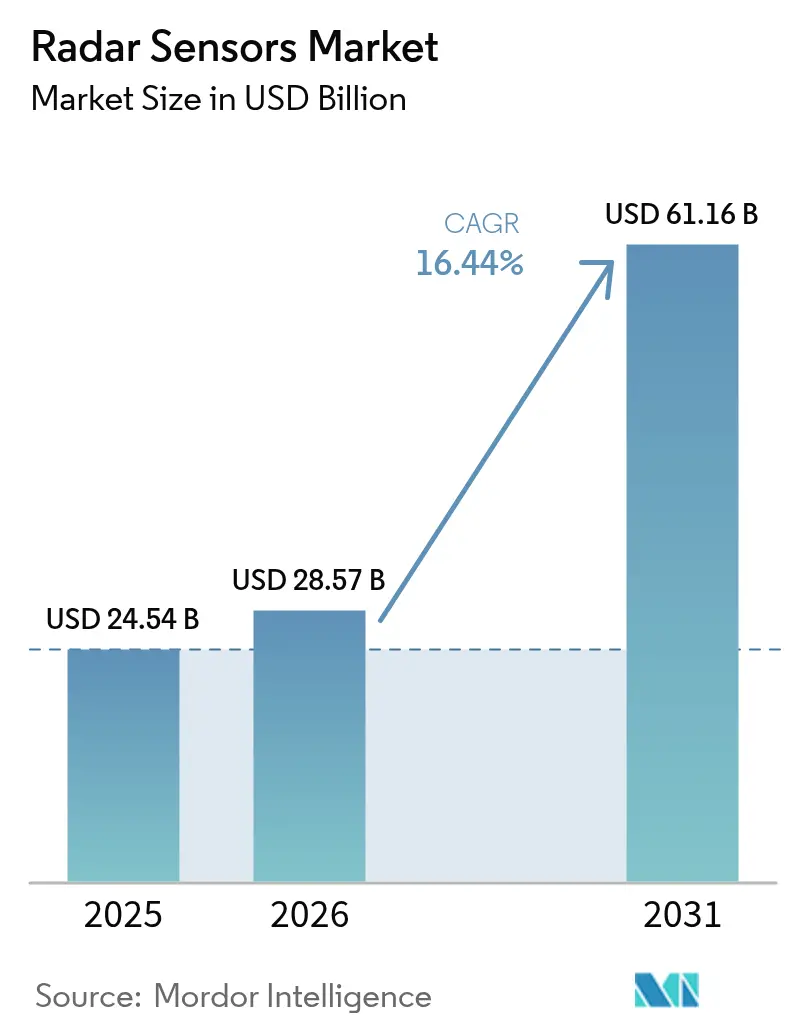

| Market Size (2026) | USD 28.57 Billion |

| Market Size (2031) | USD 61.16 Billion |

| Growth Rate (2026 - 2031) | 16.44% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Radar Sensors Market Analysis by ���ϲ�����

The radar sensors market size is expected to increase from USD 24.54 billion in 2025 to USD 28.57 billion in 2026 and reach USD 61.16 billion by 2031, growing at a CAGR of 16.44% over 2026-2031. Demand is accelerating because automotive safety regulations now require at least one forward-facing imaging sensor, defense ministries are funding upgrades to active electronically scanned array systems across Asia-Pacific fleets, and factories are embedding millimeter-wave collision-avoidance devices into collaborative robots. Platform makers are shifting from 24 GHz to 77-81 GHz architectures to gain 10 times finer range resolution while keeping antenna footprints small. Chip manufacturers have responded by integrating radio-frequency front ends, signal processing, and machine-learning inference on a single die, cutting the bill of materials for a short-range module to less than USD 20 in high volumes. Contract wins tied to Level 2+ advanced driver-assistance packages in China and Euro NCAP five-star ratings in Europe are locking in multiyear volume ramps, while drone-borne terrain-mapping and weather-radar modernization add further tailwinds.

Key Report Takeaways

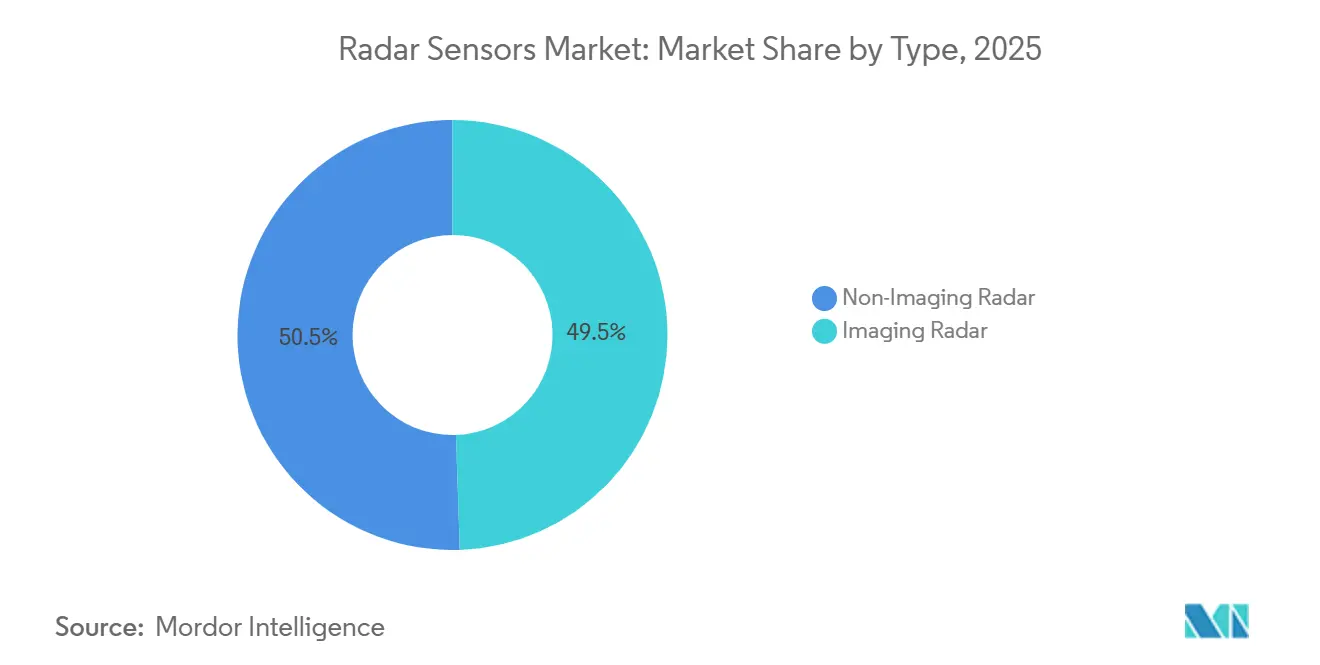

- By type, imaging radar led with 49.46% of the radar sensor market share in 2025, and is projected to advance at a 16.83% CAGR through 2031.

- By frequency band, the 77-81 GHz segment captured 43.89% of the radar sensors market share in 2025, whereas the 94 GHz and above band is forecast to grow at a 17.41% CAGR to 2031.

- By range, short-range modules accounted for 38.71% of the radar sensors market share in 2025, while medium-range units are expected to expand at a 17.07% CAGR over the same period.

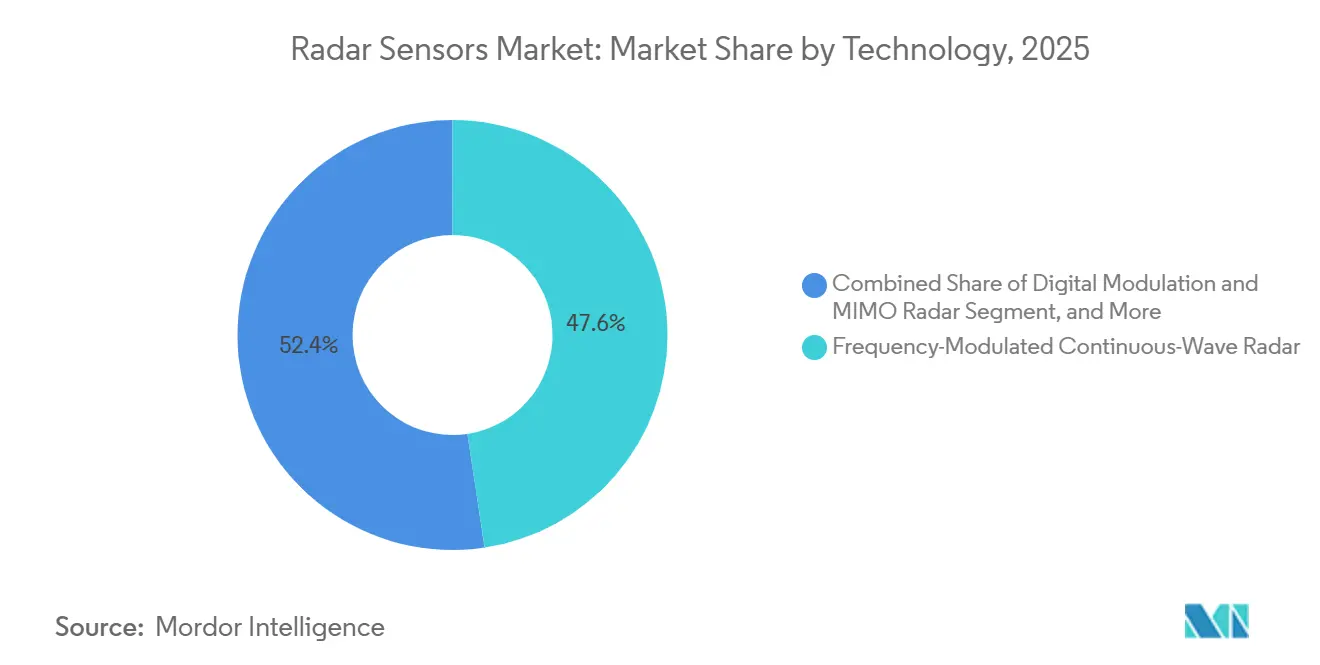

- By technology, frequency-modulated continuous-wave devices accounted for 47.62% of 2025 revenue, and digital MIMO radar is the fastest-growing category, with a 17.23% CAGR through 2031.

- By end-user, automotive commanded 59.83% of 2025 demand, whereas traffic-monitoring and smart-infrastructure applications are projected to post an 18.11% CAGR to 2031.

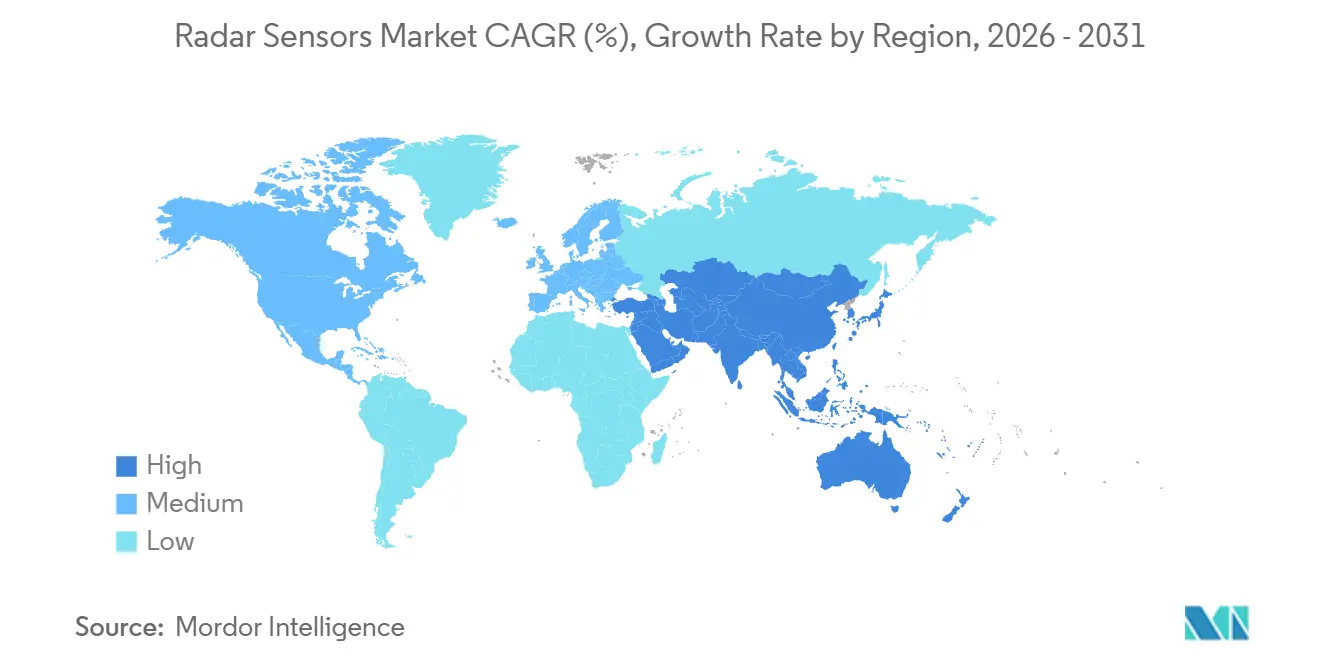

- By geography, Asia-Pacific accounted for 34.59% of global revenue in 2025, while the Middle East is the fastest-growing region, with a 17.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Radar Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption of 77-81 GHz Radars in Automotive Safety Systems | +4.2% | Europe, North America, China | Short term (≤ 2 years) |

| Surging Demand for Compact Imaging Radars in Drone-based Terrain Mapping | +2.8% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Rising Military Spend on AESA Radars in Asia-Pacific | +3.5% | India, Japan, South Korea, Australia | Medium term (2-4 years) |

| Growing Need for mm-Wave Sensors in Industrial Robot Collision Avoidance | +2.1% | Europe, North America, China, Japan | Medium term (2-4 years) |

| Infrastructure Push for Smart Highways and Traffic-Monitoring Radars in Europe | +2.3% | Germany, France, Netherlands, Middle East | Long term (≥ 4 years) |

| Climate-Change-Driven Uptake of Doppler Weather Radars in Coastal Regions | +1.5% | Global coastal zones | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Increasing Adoption of 77-81 GHz Radars in Automotive Safety Systems

Euro NCAP’s 2025 protocol rewards vehicles that detect vulnerable road users at night, a scenario that requires radar with sub-degree elevation resolution. Component makers have therefore standardized on 77-81 GHz frequency-modulated continuous-wave designs that offer ten-times finer range resolution than 24 GHz legacy sets.[1]Texas Instruments, “77-GHz to 81-GHz Automotive MIMO Radar Sensor,” ti.com China’s January 2026 mandate for automatic emergency braking pushes every new passenger car to include at least three corner radars and one forward-facing imaging unit, triggering immediate scale production. Consistent global allocation of the 76-81 GHz band by the International Telecommunication Union offers regulatory certainty, encouraging wafer-fab investments and lowering per-unit costs. Mobileye’s multi-model agreement with a leading European automaker further signals the consolidation of radar, lidar, and camera data into a single software platform. Collectively, these forces are projected to lift automotive penetration from 1.8 to 2.6 sensors per light vehicle between 2025-2027.

Surging Demand for Compact Imaging Radars in Drone-Based Terrain Mapping

Four-dimensional imaging radar mounted on small unmanned aircraft can pierce smoke, dense foliage, and heavy rain to create centimeter-level elevation models that lidar cannot deliver under the same conditions. HiRain’s LRR615 module outputs 2,000 detections per frame at 30 fps, providing real-time terrain classification for autonomous landing and wildfire assessment missions. U.S. Geological Survey contracts issued in 2025 have cut survey costs by more than 90% versus helicopter-based lidar, opening a recurring government services revenue stream.[2]U.S. Geological Survey, “Wildfire Burn-Scar Mapping with Radar-Equipped Drones,” usgs.gov Ambarella’s virtual-aperture technique reduces drone payload mass by 40%, extending flight times beyond 40 minutes with standard lithium-polymer packs. Europe’s Horizon projects fund additional agriculture-focused payloads that track soil moisture and crop stress, suggesting that commercial drone service providers will adopt imaging radar as a standard sensor alongside multispectral cameras.

Rising Military Spend on Active Electronically Scanned Array Radars in Asia-Pacific

India, Japan, South Korea, and Australia collectively budgeted more than USD 132 billion for modernization programs in 2025-2026, with a significant share devoted to domestic AESA production. The Uttam radar fitted on Tejas fighters and Mitsubishi Electric’s J/APG-2 upgrades both lift mean time between failures from 200 hours to above 10,000 hours, reducing through-life support costs by roughly 35%. Hanwha’s KRW 2.1 trillion contract for the Cheongung-II surface-to-air system includes 360-degree S-band radars that simultaneously track 100 threats. Australia’s deployment of Lockheed Martin’s AN/SPY-7 extends ballistic-missile detection from 1,000 km to 2,000 km, improving intercept confidence levels. These procurements also spur domestic semiconductor lines for gallium-nitride power amplifiers, which eventually diffuse into civil radar-sensor designs.

Growing Need for mm-Wave Sensors in Industrial Robot Collision Avoidance

ISO 13849-1 and IEC 61496 standards require collaborative robots to use safety-rated sensors that remain reliable in dusty, oily, or humid environments; millimeter-wave radar meets these requirements without being affected by optical occlusions.[3]Press Information Bureau India, “Defense Budget 2025-26,” pib.gov.in Source: ISO, “ISO 13849-1 Safety of Machinery,” iso.org Sick AG’s microScan3 Core detects limbs at 3 m with a false-alarm rate below 0.01%, allowing autonomous mobile robots to move at 2 m/s without cages. Texas Instruments’ IWRL6432 chip integrates the full radio and processor stack into a 10.4 mm square, bringing module cost to USD 8.50 at 100,000-unit volumes. ABB’s 2025 rollout across 14 vehicle plants eliminated 120 hours of annual downtime per line by removing laser-scanner maintenance cycles. As manufacturing shifts toward flexible, high-mix production, radar-based safety zones will replace floor-mounted light curtains in at least 12,000 European factories by 2028.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum Allocation Constraints in Sub-10 GHz Bands | -1.8% | Europe, North America | Short term (≤ 2 years) |

| High Calibration and Maintenance Cost of Imaging Radar Arrays | -1.5% | Global automotive and industrial | Medium term (2-4 years) |

| Thermal Management Challenges in High-Power mm-Wave Chipsets | -1.2% | Automotive and defense globally | Medium term (2-4 years) |

| Data-Privacy Concerns over 3-D People-Tracking Radars in Retail | -0.9% | Europe, select U.S. states | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Spectrum Allocation Constraints in Sub-10 GHz Bands

Mobile-network regulators have reassigned 3.3-3.8 GHz for 5G, forcing legacy S-band weather radars to accept potential interference or migrate to higher frequencies. The FCC’s 2025 proposal restricts automotive radar below 10 GHz to emergency vehicles, after maritime complaints that 9.3 GHz truck systems corrupt ship-borne X-band displays. ETSI caps 24 GHz short-range radar at 20 dBm, limiting effective range to 30 m and pushing suppliers toward costlier 77 GHz chips. India’s 2025 spectrum auction reduced bandwidth for airport surveillance, obliging upgrades worth INR 4,200 crore (USD 500 million). Divergent rules: Japan offers 4 GHz bandwidth at 79 GHz, while South Korea grants only 1 GHz, forcing automakers to maintain region-specific hardware versions.

High Calibration and Maintenance Cost of Imaging Radar Arrays

Four-dimensional radar requires phase alignment within 0.5° and amplitude matching within 0.2 dB across nearly 200 channels, a precision that drifts with temperature and mechanical stress. Aptiv’s self-calibrating Gen 8 platform adds 12 ms latency and 1.8 W consumption for reference-target comparisons. Continental reports EUR 47 per-unit warranty costs over five-year life cycles, nearly four times non-imaging modules, due to antenna delamination and radome moisture ingress. Independent repairers lack the RF test chambers needed for recalibration, leaving consumers to pay more than USD 800 per module at dealerships, a problem now cited in right-to-repair petitions. Meeting AEC-Q100 Grade 2 temperature performance adds USD 15-22 to the bill of materials, limiting near-term adoption in cost-sensitive vehicle classes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Imaging Radar Nears Majority Adoption

Imaging radar accounted for 49.46% of the radar sensors market share in 2025, expanding at a 16.83% CAGR through 2031 as automakers adopt point-cloud perception comparable to lidar at one-tenth the cost. Zadar Labs’ January 2026 acquisition of Fusionride underscores rising investment in software-defined stacks that allow over-the-air algorithm updates without hardware changes. Non-imaging systems retained 50.54% in 2025 because long-proven pulsed-Doppler systems remain the standard for weather monitoring and air traffic control, where elevation data are unnecessary. Yet hybrid vehicle architectures now pair one imaging unit with four non-imaging modules to satisfy Euro NCAP’s five-star protocol while capping sensor bills of materials below USD 180 per vehicle. Consequently, imaging radar’s revenue is projected to overtake legacy designs by 2028 as volume pricing falls under USD 45 per forward-facing module.

Growth momentum also stems from chipset innovation. Arbe Robotics’ virtual-aperture synthesis yields more than 2,000 detections per frame, compared with 64 in classic frequency-modulated continuous-wave systems, enabling reliable pedestrian classification at night. Automakers monetize this resolution through subscription features that unlock higher levels of autonomy post-sale, shifting radar from a one-time hardware cost to a recurring software platform. However, imaging radar’s advantage narrows beyond 250 m because atmospheric attenuation at 77-81 GHz degrades signal-to-noise ratio, so freight-truck OEMs still favor non-imaging long-range modules for adaptive cruise control duty cycles that exceed 5 hours daily. Overall, imaging solutions are set to capture the largest share of the radar sensors market by the end of the forecast window.

By Frequency Band: 77-81 GHz Remains Core While W-Band Accelerates

The 77-81 GHz band accounted for 43.89% of 2025 revenue, as the International Telecommunication Union designates it the global standard for automotive short-range radar, supporting economies of scale in silicon-germanium chip production. Texas Instruments’ AWR2944 family demonstrates a roadmap to 94 GHz operation with 10 GHz instantaneous bandwidth, catalyzing a 17.41% CAGR for the W-band segment through 2031. Sub-10 GHz radar, important for ground-penetrating and through-wall imaging, is growing at a 15.2% CAGR but faces interference from expanding 5G services, trimming its share despite demand in civil engineering surveys. Regulatory shifts have already forced suppliers to migrate 24 GHz automotive designs or accept detection ranges capped at 30 m, accelerating the transition to 77-81 GHz platforms.

Beyond automotive, 60-64 GHz unlicensed devices are surging in smart-building occupancy sensing. Infineon’s BGT60TR13C detects respiration through drywall up to 10 m, lowering HVAC energy use by 18% in pilot retrofits. Defense integrators are eyeing 94 GHz for compact seeker heads because wider sweep widths deliver the sub-centimeter resolution needed for counter-UAS missions. Against this backdrop, W-band silicon prices are forecast to fall 35% by 2029 as foundries ramp gallium-nitride processes, positioning 94 GHz to claim more than 12% of the radar sensors market size by 2031.

By Range: Medium-Range Modules Gain Pace on Parking Automation

Short-range sensors captured 38.71% of 2025 sales because blind-spot, cross-traffic, and rear-backup aids are now standard on most compact SUVs, with unit costs hovering near USD 18. Medium-range devices covering 50-100 m are projected to lead growth at 17.07% CAGR as automated parking and lane-change assistants proliferate in mid-segment vehicles. Valeo and Mobileye’s co-developed radar extends detection to 120 m while staying below USD 85 per module, fitting European urban Level 3 requirements. Long-range radar held 29.1% in 2025 but faces thermal constraints, as transmit power above 12 dBm raises junction temperatures to over 150 °C in compact housings.

Regulators further reinforce the mix. The U.S. FMVSS 111 rule mandates pedestrian detection within 3 m behind vehicles, a metric met by short-range radar at commodity prices, guaranteeing tens of millions of annual unit shipments through 2031. Meanwhile, Europe’s General Safety Regulation 2 compels reversing-detection systems on heavy trucks, channeling demand toward 77 GHz medium-range modules with 120-degree fields of view. As municipal parking fees rise, automakers promote hands-free parking subscriptions that rely on four-corner medium-range sensors, cementing this category’s leadership in incremental revenue per vehicle.

By Technology: Digital MIMO Steals Share from Classic FMCW

Frequency-modulated continuous-wave radar led with 47.62% of 2025 turnover because it measures range and velocity in a single chirp cycle at low computational cost. Infineon and NXP now ship single-chip solutions that embed MIMO beamforming and on-die machine-learning acceleration, propelling digital modulation to a 17.23% CAGR. Pulsed radar remains the standard for long-range air and weather surveillance, where peak power exceeds 1 MW and duty cycles remain below 1%, keeping average power consumption manageable. Phased-array and AESA architectures captured 12.1% in 2025 and could grow faster as Echodyne’s USD 120 metamaterial array shows cost parity with mechanical pans for automotive safety envelopes.

Digital MIMO’s rise is rooted in software flexibility. Arbe Robotics’ chipset synthesizes a virtual aperture exceeding 30 cm, delivering sub-degree angular accuracy without enlarging physical antenna size, an advantage that camera-only systems cannot replicate in fog or heavy rain. Over-the-air firmware updates further let automakers monetize new perception features post-sale, turning radar into an upgradable asset rather than a fixed-function device. As these capabilities filter down to mass-market models, digital MIMO is expected to eclipse 35% of the radar sensors market share by 2031, while classic FMCW falls below 40%.

By End-User: Infrastructure Projects Spawn New Growth Avenues

Automotive applications represented 59.83% of 2025 demand because Europe, China, and the United States all impose advanced driver-assistance mandates that typically require three to five sensors per vehicle. Traffic-monitoring and smart-infrastructure deployments are the fastest-growing, with an 18.11% CAGR, as the European Union and the U.S. Federal Highway Administration fund cooperative intelligent transport systems with roadside radars for wrong-way detection and variable-speed enforcement. Aerospace and defense held 14.2% as multibillion-dollar AESA upgrades lengthen platform life cycles and improve target-tracking fidelity. Industrial automation and robotics accounted for 5.4% but is closing in on double-digit share as factories replace laser scanners with radar that operates maintenance-free for 36 months.

Healthcare and assisted-living, although just 2.9% in 2025, are expanding rapidly after FDA-cleared fall-prevention radars cut hospitalization rates by 31% in pilot programs, encouraging insurer reimbursement. Environment and weather monitoring remains steady at 4.1% because national meteorological agencies' budgets are being upgraded to dual-polarization Doppler systems rather than expanded radar counts. Security and surveillance applications, particularly perimeter defense for energy facilities, add steady demand, while retail analytics faces headwinds from stringent biometric-privacy rules that restrict 3-D tracking without explicit consent. Overall, non-automotive verticals are projected to lift their combined portion of the radar sensors market size above 45% by 2031, reducing volatility tied to light-vehicle production cycles.

Geography Analysis

Asia-Pacific commanded 34.59% of the radar sensor market share in 2025 and is expanding at a 16.8% CAGR, as China’s Level 2+ mandate requires at least 4 sensors in every new passenger car and India earmarks USD 72.6 billion for defense radar upgrades. China generated more than half of regional demand in 2025 because domestic suppliers price imaging modules 25% below Western competitors, accelerating fitment across mass-market electric vehicles. India remains the fastest-growing country, with an 18.3% CAGR, driven by collision-warning rules for commercial trucks and large orders for indigenous Uttam AESA sets. A shrinking auto-production base tempers Japan’s 15.6% CAGR, yet Denso and Hitachi Astemo are scaling 94 GHz parking radars for premium hybrids. South Korea benefits from KRW 12 trillion in New Deal 2.0 subsidies that underwrite Level 3 systems on Hyundai and Kia models, lifting regional shipment forecasts through 2031.

Europe delivered 26.1% of global revenue in 2025 and is sustaining a 16.2% CAGR, underpinned by the General Safety Regulation 2, which requires intelligent speed assistance, lane-keeping, and emergency braking on all new platforms after July 2024. Germany accounted for 38% of the continent’s radar sensor market in 2025, as Volkswagen, BMW, and Mercedes-Benz standardized imaging units across electric-vehicle architectures. The United Kingdom is outpacing the region with a 17.1% CAGR because GBP 850 million in public trials of Level 4 shuttles require redundant sensor stacks, including two imaging radars per test vehicle. France and Italy post mid-teen growth but trail leaders due to slower electric-vehicle uptake and constrained incentive budgets. Revised EN 302 858 power limits, rising from 55 dBm to 58 dBm in September 2025, now allow a single 77 GHz unit to meet adaptive-cruise targets once handled by dual-sensor pairs.

North America accounted for 28.3% of 2025 revenue and is tracking a 15.9% CAGR, as the National Highway Traffic Safety Administration proposes an automatic emergency braking mandate covering 17 million light vehicles annually. Canada’s CAD 1.2 billion Strategic Innovation Fund brings Infineon’s first North American module line online in Ottawa by Q3 2026, enhancing continental supply resilience. Mexican plants in Guadalajara and Monterrey already assemble 18% of regional output, leveraging labor prices 40% below U.S. averages and proximity to Texas and Michigan assembly hubs. South America represents 4.2% of global revenue, with Brazil accounting for 68% of that total, yet radar penetration is below 12% because average transaction prices leave little budget for advanced driver-assistance systems. The Middle East and Africa together contribute 6.9%, though the Middle East clocks the fastest regional CAGR at 17.46%, as Saudi Arabia’s NEOM project and the UAE's critical infrastructure programs require traffic and perimeter radars on every new corridor.

Competitive Landscape

The radar sensors market exhibits moderate concentration: Bosch, Continental, Infineon Technologies, NXP Semiconductors, and Denso accounted for about 58% of 2025 revenue, yet their combined market share is slipping as imaging-radar disruptors win new platforms. Bosch leverages in-house GaAs and SiGe fabs to guarantee 12-week lead times, a strategic buffer against foundry bottlenecks that stretch delivery for fabless rivals to 20 weeks. Continental scales its fifth-generation corner radar to 14 million European units shipped in 2025, growing 22% year over year while embedding self-calibration firmware that cuts warranty claims 11%. Infineon’s February 2026 purchase of ams Osram’s non-optical sensors trims module footprint 30%, opening door-handle and mirror placements that legacy housings could not fit.

Start-ups are easing entry barriers through software-defined architectures. Arbe Robotics’ virtual-aperture chipset supports 2,000 detections per frame and secured six design wins with Chinese EV makers in 2025, generating its first USD 100 million order backlog. Uhnder shipped 500,000 digital-code modulation units that achieve sub-degree angular performance without expensive shielding, allowing Tier 1 supplier Valeo to quote a medium-range module at USD 75, down 15% from prior generations. Oculii’s signal-processing IP, now embedded in Ambarella SoCs, expanded into two North American truck fleets that needed 300-meter detection for highway platooning, demonstrating the value of software retrofits on modest RF hardware.

Regional champions add further fragmentation. HiRain holds a 12% share in China after bundling Arbe chips into its LRR615 unit, while Mando and HL Klemove supply 80% of Hyundai and Kia radar content in South Korea. Japan’s Denso and Hitachi Astemo collaborate on 94 GHz park-assist modules, aiming for a USD 60 billion bill of materials by 2028 to defend against lower-cost Chinese imports. Indie Semiconductor’s 22 nm fully depleted silicon-on-insulator process reduces power draw by 40% and is sampling with three European OEMs seeking sub-USD 50 forward radars for B-segment cars. Echodyne’s USD 120 metamaterial AESA array shows that electronically steered beams are approaching cost parity with mechanical pans, putting mid-decade margin pressure on legacy FMCW suppliers. Overall, price competition and over-the-air upgrade revenue models are expected to shrink the top-five revenue share to near 51% by 2031, resetting the balance between hardware incumbency and software agility.

Radar Sensors Industry Leaders

Robert Bosch GmbH

Continental AG

Infineon Technologies AG

NXP Semiconductors N.V.

Denso Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Infineon Technologies completed the EUR 570 million (USD 644 million) purchase of ams Osram’s non-optical sensor assets, adding antenna-in-package expertise and shrinking module footprints 30%.

- January 2026: Zadar Labs acquired Fusionride to integrate software-defined perception algorithms into its imaging-radar lineup.

- December 2025: Gapwaves won an Infineon order for waveguide antennas that deliver 20% higher gain for 77-81 GHz modules.

- October 2025: Infineon introduced the BGT60TR13C 60 GHz transceiver that senses human presence and vital signs through walls at 10 m range.

Global Radar Sensors Market Report Scope

The Radar Sensors Market Report is Segmented by Type (Imaging Radar, and Non-Imaging Radar), Frequency Band (Less than 10 GHz, 24 GHz, 60-64 GHz, 77-81 GHz, 94 GHz and Above), Range (Short-range Radar Sensor, Medium-range Radar Sensor, Long-range Radar Sensor), Technology (Pulsed Radar, Frequency-Modulated Continuous-Wave Radar, Phased-Array / AESA Radar, Digital Modulation and MIMO Radar), End-User (Automotive, Aerospace and Defense, Security and Surveillance, Industrial Automation and Robotics, Environment and Weather Monitoring, Traffic Monitoring and Smart Infrastructure, Healthcare and Assisted-Living, Other End-Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Imaging Radar |

| Non-Imaging Radar |

| Less than 10 GHz |

| 24 GHz |

| 60-64 GHz |

| 77-81 GHz |

| 94 GHz and Above |

| Short-range Radar Sensor |

| Medium-range Radar Sensor |

| Long-range Radar Sensor |

| Pulsed Radar |

| Frequency-Modulated Continuous-Wave Radar |

| Phased-Array / AESA Radar |

| Digital Modulation and MIMO Radar |

| Automotive |

| Aerospace and Defense |

| Security and Surveillance (Fixed and Mobile) |

| Industrial Automation and Robotics |

| Environment and Weather Monitoring |

| Traffic Monitoring and Smart Infrastructure |

| Healthcare and Assisted-Living |

| Other End-Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Type | Imaging Radar | ||

| Non-Imaging Radar | |||

| By Frequency Band | Less than 10 GHz | ||

| 24 GHz | |||

| 60-64 GHz | |||

| 77-81 GHz | |||

| 94 GHz and Above | |||

| By Range | Short-range Radar Sensor | ||

| Medium-range Radar Sensor | |||

| Long-range Radar Sensor | |||

| By Technology | Pulsed Radar | ||

| Frequency-Modulated Continuous-Wave Radar | |||

| Phased-Array / AESA Radar | |||

| Digital Modulation and MIMO Radar | |||

| By End-User | Automotive | ||

| Aerospace and Defense | |||

| Security and Surveillance (Fixed and Mobile) | |||

| Industrial Automation and Robotics | |||

| Environment and Weather Monitoring | |||

| Traffic Monitoring and Smart Infrastructure | |||

| Healthcare and Assisted-Living | |||

| Other End-Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the forecast value of the radar sensors market in 2031?

The radar sensors market is projected to reach USD 61.16 billion by 2031.

How quickly is the market expected to grow after 2026?

It is forecast to expand at a 16.44% CAGR from 2026 to 2031.

Which frequency band currently dominates commercial radar sensors?

The 77-81 GHz band held 43.89% of 2025 revenue due to its fine resolution and global regulatory approval.

Why are imaging radars gaining traction over non-imaging versions?

Imaging units deliver three-dimensional point clouds that classify vulnerable road users while matching lidar resolution at lower cost.

Which end-use sector is growing fastest?

Traffic-monitoring and smart-infrastructure projects are advancing at an 18.11% CAGR through 2031.

What is hindering rapid adoption of imaging radar arrays?

High calibration and maintenance costs, including dealership-only servicing priced above USD 800 per module, remain a barrier.

Page last updated on: