Portable Magnetic Resonance Imaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.64 Billion |

| Market Size (2031) | USD 6.23 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Portable Magnetic Resonance Imaging Market Analysis by ���ϲ�����

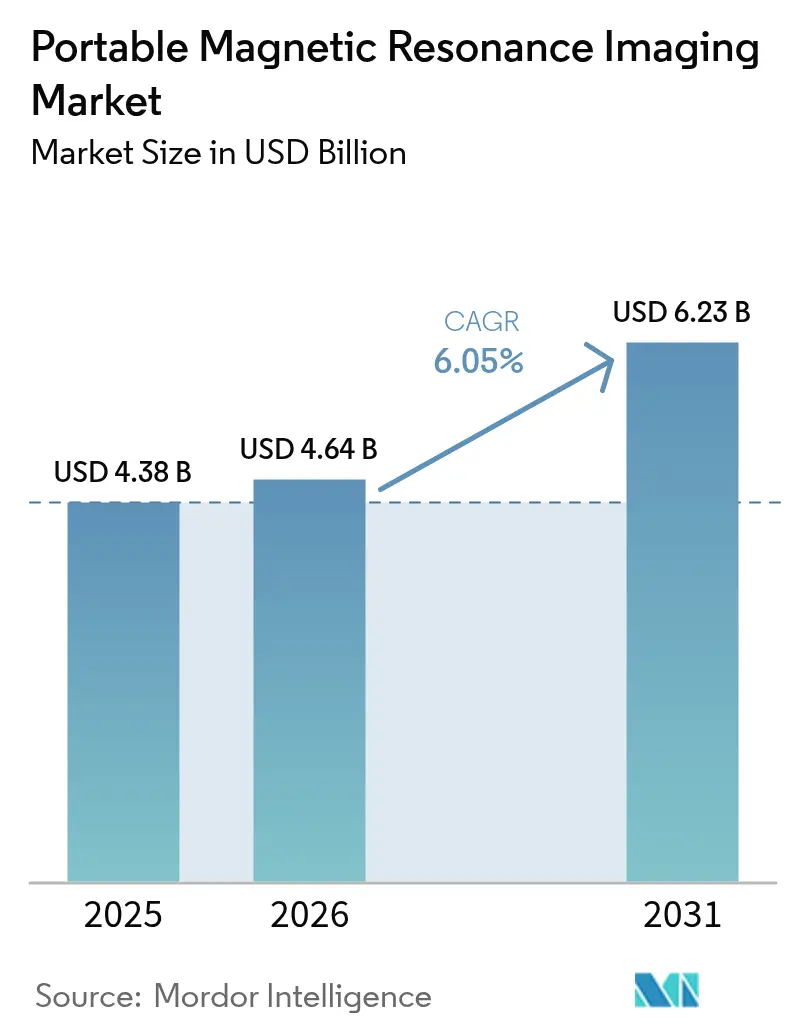

The Portable Magnetic Resonance Imaging Market size is projected to be USD 4.38 billion in 2025, USD 4.64 billion in 2026, and reach USD 6.23 billion by 2031, growing at a CAGR of 6.05% from 2026 to 2031.

Falling prices of ultra-low-field hardware, now priced between USD 50,000 and 150,000, are expanding diagnostic capabilities from traditional shielded radiology suites to emergency departments, intensive care units, neonatal bays, and ambulatory clinics. In November 2024, the Intersocietal Accreditation Commission (IAC) updated its accreditation standards to formally approve portable systems for neurology offices. This regulatory development has opened reimbursement opportunities through the Centers for Medicare & Medicaid Services (CMS) and driven significant investments in outpatient care facilities. While the neurology segment accounted for 45.12% of application revenue in 2025, pediatrics and neonatal imaging are experiencing faster growth, as bedside scanning minimizes transport and sedation risks for fragile infants. Hardware innovations are also driving market transformation: Halbach permanent-magnet arrays eliminate the need for helium and complex cooling systems, reducing system weight to under 635 kg and enabling standard-floor installations without structural reinforcements.

Key Report Takeaways

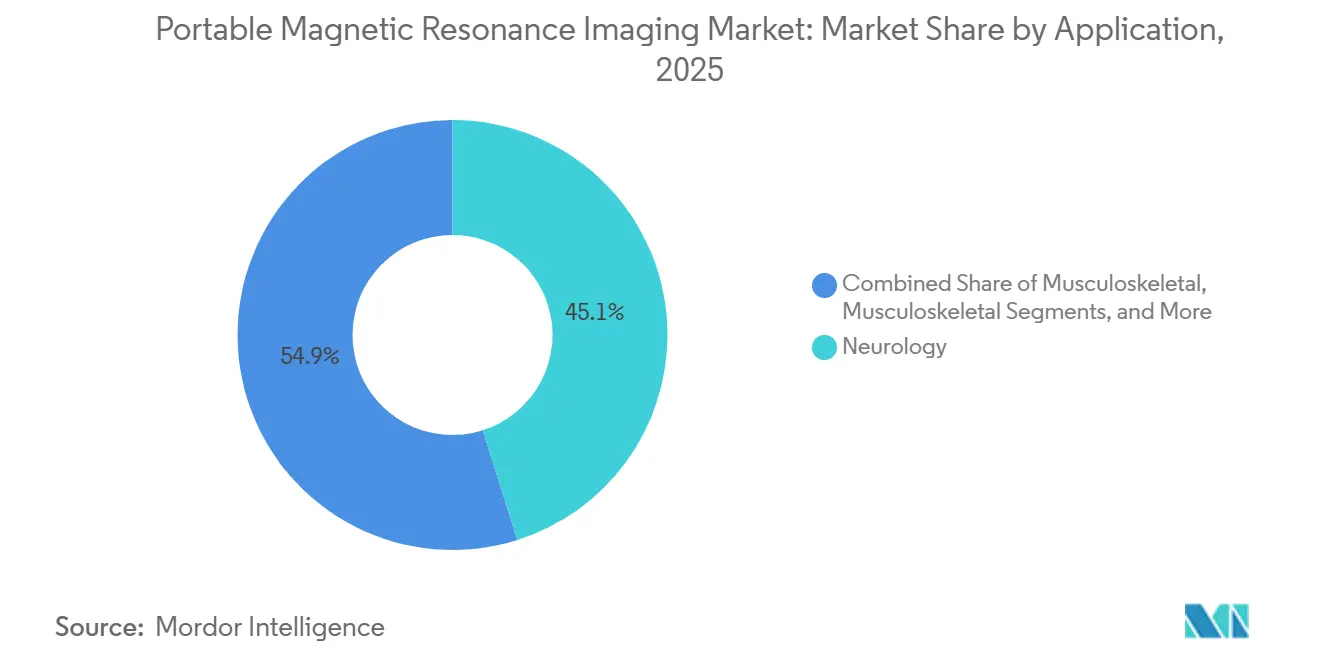

- By application, neurology held 45.12% of the portable magnetic resonance imaging market share in 2025, while pediatrics and neonatal imaging is expanding at an 8.53% CAGR through 2031.

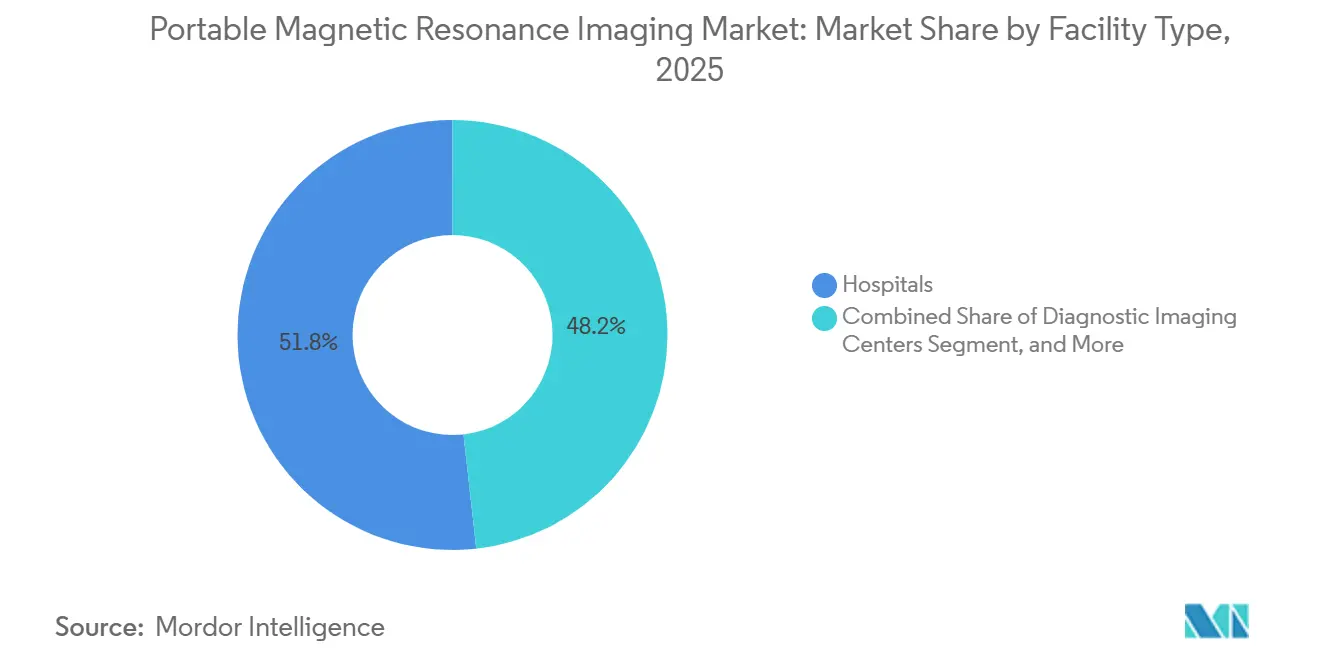

- By facility type, hospitals commanded 51.76% of 2025 revenue, whereas ambulatory surgery centers are forecast to grow at 8.91% CAGR between 2026 and 2031.

- By magnet strength, ultra-low-field systems captured 58.65% of 2025 sales and are projected to advance at 9.75% CAGR through 2031.

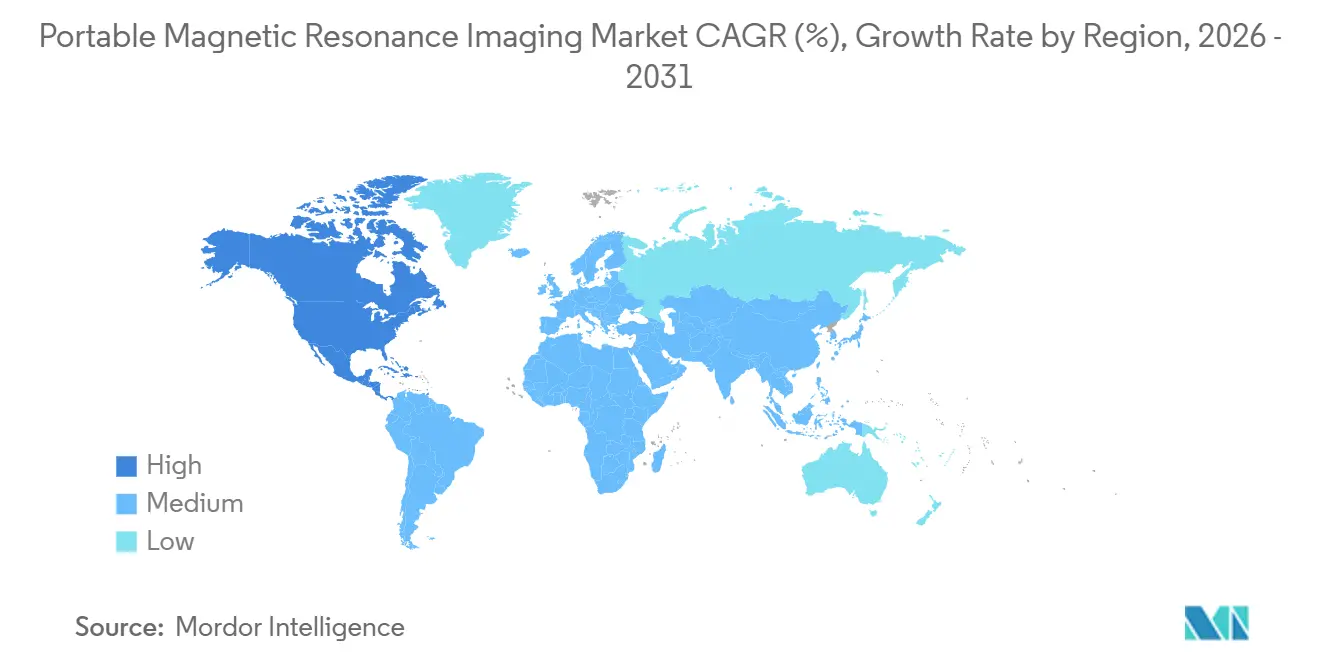

- By geography, North America accounted for 42.65% of the portable MRI market in 2025; Asia-Pacific is projected to expand at an 7.64% CAGR, the quickest regional trajectory through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Portable Magnetic Resonance Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Advantage Over Conventional MRI | +1.8% | Global, strongest in North America & Asia-Pacific | Short term (≤ 2 years) |

| Technological Miniaturization Advancements | +1.5% | Global, led by North America & Europe | Medium term (2–4 years) |

| Growing Point-of-Care Diagnostics Demand | +1.3% | North America & Europe, spill-over to Asia-Pacific | Medium term (2–4 years) |

| Favorable Regulatory & Accreditation Reforms | +0.7% | North America, gradual uptake in Europe & Asia-Pacific | Short term (≤ 2 years) |

| Rural and Remote Healthcare Access Initiatives | +0.9% | Asia-Pacific core, spill-over to Middle East & Africa | Long term (≥ 4 years) |

| Expanding Venture and Strategic Investment Landscape | +0.4% | North America, selective activity in Asia-Pacific | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Cost Advantage Over Conventional MRI

Over a seven-year lifespan, the total ownership cost of a 0.064 T portable unit averages approximately USD 300,000, compared to around USD 5 million for a 1.5 T suite when accounting for cryogens, RF shielding, and HVAC upgrades[1]Yale School of Medicine, “Economic Analysis of Bedside MRI,” yale.edu. Community hospitals and ambulatory surgery centers can recover this investment in fewer than 1,000 scans, with many achieving it within 24 months, given reimbursement rates of nearly USD 400 per neurological study. Additionally, the ability to install scanners in spaces previously used for observation beds has significantly reduced installation timelines from the standard 18–24 months to less than 30 days. Rural hospitals in the United States, which previously referred MRI volumes to regional centers, are now retaining revenue locally. This shift enhances the availability of same-day stroke care while reducing patient transfer costs. Similar economic considerations are influencing middle-income markets in the Asia-Pacific region, where public budget limitations and floor-loading restrictions challenge traditional installations.

Technological Miniaturization Advancements

Since 2023, Halbach arrays utilizing neodymium-iron-boron segments have effectively optimized magnetic flux, achieving a nearly 40% reduction in system weight. This advancement has also eliminated reliance on helium, addressing challenges posed by the global helium shortage of 2024[2]Science, “Halbach Magnet Arrays for Portable MRI,” science.org. Researchers at the University of Hong Kong demonstrated a 2 mm in-plane resolution on a 0.05 T prototype by integrating advanced gradient coils with iterative reconstruction algorithms, highlighting untapped potential for hardware performance improvements. In 2024, Siemens Healthineers introduced the FreeStar 0.55 T air-cooled system, specifically designed for emerging markets lacking chilled-water infrastructure. Additionally, deep-learning networks trained on paired low-field and high-field datasets now generate synthetic T1, T2, and FLAIR contrasts from a single 10-minute acquisition, reducing traditional protocol times by up to 80%. These advancements—lighter magnet systems and AI-driven reconstruction—enable critical-care teams to conduct on-site scans for ventilated patients, minimizing risks associated with patient transport through elevators, hallways, and magnetically shielded areas.

Growing Point-of-Care Diagnostics Demand

In 2024, approximately 145 million emergency department visits were recorded in the United States, with neurological complaints accounting for 8% of these cases. Portable MRI technology has revolutionized the traditional CT-first diagnostic workflow by enabling bedside examinations[3]CDC, “National Hospital Ambulatory Medical Care Survey,” cdc.gov. This innovation reduces diagnostic delays from nearly 4 hours to under 1 hour, ensuring thrombolytic therapy can be administered within the critical 4.5-hour therapeutic window. A JAMA Neurology trial reported an 80.4% sensitivity and 96.6% specificity for detecting intracranial hemorrhage at 0.064 T, providing sufficient accuracy to guide real-time anticoagulant reversal decisions. In neonatal intensive care units, over 1,200 unsedated scans conducted at Cincinnati Children’s Hospital demonstrated zero transport-related adverse events, validating the technology’s potential to reduce risk. Additionally, ambulatory surgery centers are increasingly adopting portable extremity scanners to confirm implant positions following same-day knee and shoulder repairs. This practice has effectively reduced 30-day readmissions, protecting bundled-payment margins and enhancing operational efficiency.

Favorable Regulatory & Accreditation Reforms

In November 2024, the IAC introduced new standards requiring quality-control phantoms, technologist certification, and radiologist over-reads, aligning regulatory requirements for portable devices with those of fixed systems. In response, CMS clarified that accredited neurology offices are eligible to bill existing MRI CPT codes, resolving prior reimbursement uncertainties that had slowed adoption in community practices. In June 2025, the U.S. Food and Drug Administration approved Hyperfine’s Optive AI 510(k) submission within 90 days, reflecting increased institutional familiarity with ultra-low-field physics and AI-driven reconstruction technologies. In contrast, Europe’s regulatory environment remains more cautious. The Medical Device Regulation (MDR) necessitates post-market surveillance, delaying product launches by up to 18 months and prompting vendors to pursue pilot contracts while gathering follow-up data required by Germany’s Federal Joint Committee and France’s Haute Autorité de Santé. However, the UK’s national health services have initiated pilot funding for portable stroke networks, signaling potential reimbursement opportunities if outcome benefits are demonstrated.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Image Quality and Resolution Limitations | -0.9% | Global, most acute in North America & Europe | Medium term (2–4 years) |

| Uncertain and Fragmented Reimbursement Policies | -1.2% | Europe & Asia-Pacific, limited North America impact | Short term (≤ 2 years) |

| Operational Expertise and Training Gaps | -0.5% | Asia-Pacific & Middle East, lower North America exposure | Medium term (2–4 years) |

| Rare-Earth Magnet and Supply-Chain Vulnerabilities | -0.3% | Global, peak exposure in Asia-Pacific hubs | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Image Quality and Resolution Limitations

Signal-to-noise ratios in 0.064 T systems are approximately 20 times lower than those in 1.5 T platforms, limiting spatial resolution to around 2–3 mm and resulting in up to 18% of acute lacunar infarcts being undetected compared to 3 T imaging. This diagnostic limitation restricts the use of these systems for complex oncology staging, pituitary microadenoma detection, and subtle demyelinating-plaque monitoring. Radiologists trained on high-field scanners experience longer reading times and reduced confidence when interpreting images from these systems, negatively impacting workflow efficiency in academic centers. While AI advancements have improved T2-FLAIR contrast-to-noise ratios to approach 0.35 T standards, global regulators have yet to define equivalence thresholds. As a result, hospitals remain responsible for confirmatory imaging on conventional systems, which diminishes the cost-saving potential that often justifies investment in these technologies.

Uncertain Reimbursement Pathways

In the U.S., CMS has informally allowed billing for traditional brain MRI CPT codes in IAC-accredited portable studies, but the absence of formal parity guidance has led to inconsistent payer approvals and delays in prior authorizations. Private insurers, such as UnitedHealthcare, require additional documentation to establish clinical necessity, further contributing to scheduling delays and reducing the efficiency of point-of-care services. In Europe, reimbursement frameworks are even less defined. Germany’s Diagnosis-Related Group catalog has yet to include ultra-low-field procedures, and the UK’s NICE has not issued technology-appraisal guidance, forcing vendors to rely on ad hoc pilot funding. Without clear reimbursement policies, community hospitals operating on tight budgets are hesitant to adopt these systems, extending return-on-investment timelines from the standard 3 years to over 5 years.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Neurology Commands, Pediatrics Accelerates

In 2025, neurology contributed 45.12% of the revenue, driven by the adoption of portable scanners in emergency departments. These devices enabled efficient triaging of strokes and traumatic brain injuries, reducing time-to-thrombolysis to under 60 minutes. The portable magnetic resonance imaging market for neurology is projected to grow at a 5.6% CAGR through 2031, supported by IAC accreditation and CMS reimbursement, which are expanding outpatient applications in movement-disorder clinics. Pediatrics and neonatal imaging are advancing at the fastest pace, with an 8.53% CAGR. Over 1,200 scans conducted at Cincinnati Children’s Hospital demonstrated that bedside MRI eliminates transport-related desaturation events, a critical factor for infants weighing less than 2 kg. While musculoskeletal postoperative checks are limited by a 2–3 mm ceiling, ambulatory surgery centers continue to adopt these scans for same-day implant confirmations, helping reduce readmission penalties. In cardiology, applications remain exploratory, focusing on pericardial effusion screenings due to challenges with temporal resolution for perfusion analysis. However, research consortia are testing prototype sequences synchronized with ECG gating to expand the technology’s utility.

The portable magnetic resonance imaging market is diversifying beyond neuro-critical care, driven by advancements in AI algorithms that address image-quality gaps. Hospital networks integrating portable units with tele-neurology services report a 28-minute reduction in door-to-needle stroke workflows, delivering measurable outcome improvements under Medicare’s value-based purchasing guidelines. Pediatric hospitals highlight cost savings by eliminating the need for anesthesiology staffing during routine follow-up scans, with resource reallocation valued at approximately USD 1,200 per avoided sedation episode. As vendors refine musculoskeletal extremity coils, early adopters anticipate shifting 20% of postoperative orthopedic imaging from fixed suites, freeing capacity for high-margin reimbursable contrast studies. Across applications, AI-driven noise-reduction pipelines are enhancing operational efficiency by reducing radiologist fatigue and cutting interpretation time by an average of 15%, ultimately improving throughput and physician satisfaction.

By Facility Type: Hospitals Lead, ASCs Surge

In 2025, hospitals accounted for 51.76% of the revenue from neurodiagnostic facilities, reflecting the high demand for bedside neurodiagnostics in emergency and intensive care units. However, the hospital segment's dominance in the portable magnetic resonance imaging market is expected to decline slightly as ambulatory surgery centers (ASCs) expand at a robust rate of 8.91% through 2031. This growth is driven by increasing fee-for-service orthopedic volumes and bundled-payment mandates that penalize readmissions. Diagnostic imaging centers remain cautious, citing challenges such as reimbursement parity and the costs of radiologist adaptation. In contrast, rural stand-alone centers are leveraging portable units as cost-effective solutions to serve community clinics lacking comprehensive MR capabilities. Neurology offices, supported by IAC accreditation, are emerging as a promising market segment. This accreditation has enabled clear billing for office-based studies, reduced patient travel, and facilitated longitudinal disease monitoring.

Tertiary hospitals are increasingly adopting a dual-fleet model to optimize operations. High-field suites are allocated for oncology and cardiac contrast protocols, while portable devices are utilized for hyper-acute neurological screenings and ICU follow-ups. This approach enhances suite utilization and increases overall throughput by up to 12%. In the United States, ASCs, performing 23 million procedures annually, are integrating portable extremity MRI systems to ensure implant clearance before discharge. This practice not only replaces postoperative CT scans but also delivers cost savings of approximately USD 34 per patient by reducing radiation exposure and improving workflow efficiency. Corporate neurology chains are positioning portable systems as competitive differentiators, offering same-visit diagnoses to enhance patient satisfaction scores, which directly influence payer ratings. Additionally, across all facility types, the adoption of cloud-based AI is driving operational efficiency. Unified reporting dashboards are reducing IT overhead and enabling enterprise-wide standardization of protocols.

By Magnet Strength: Ultra-Low-Field Dominates, Mid-Field Evolves

Ultra-low-field devices, operating at less than 0.2 T, accounted for 58.65% of 2025 revenue and are projected to grow at a 9.75% CAGR. This growth is attributed to their cost-effectiveness, ease of installation, and ability to function on standard floors without requiring shielding renovations. The ultra-low-field portable magnetic resonance imaging market is expected to exceed USD 4 billion by 2031, reinforcing its importance in point-of-care neurotriage and pediatric monitoring. Low-field platforms, ranging from 0.2 to 0.5 T, such as Siemens’ Free.Star 0.55 T, are gaining traction among clinics seeking a balance between portability and enhanced image quality. However, air-cooling limitations restrict their adoption in power-grid-constrained regions. Compact mid-field scanners, like Aspect Imaging’s 1.0 T neonatal model, deliver near-diagnostic resolution but, due to their weight exceeding one ton, are categorized as semi-mobile rather than fully portable. On the research front, superconducting mid-field prototypes aim to achieve helium-free 1.5 T performance. However, their commercial viability depends on advancements in zero-boil-off magnet technology and the identification of clinical applications beyond those already addressed by fixed suites.

Diagnostic capabilities have traditionally been tied to field strength, but advancements in AI are redefining these boundaries. Hyperfine’s Optive AI is enhancing 0.064 T T2-FLAIR contrast to levels comparable to 0.35 T, challenging the conventional perception of ultra-low-field systems as limited to triage applications. Academic consortia are benchmarking 0.05 T whole-body prototypes against 0.2 T clinical scanners, indicating a future where sub-0.1 T imaging could be sufficient for musculoskeletal postoperative evaluations, prostate biopsy guidance, and limited abdominal assessments. As these algorithmic innovations secure FDA approvals, the combination of cost reductions and performance parity is expected to drive a shift in capital allocation. This shift could move investments away from traditional mid-field upgrades toward fleets of AI-enhanced ultra-low-field devices, accelerating the decentralization of the portable magnetic resonance imaging market.

Geography Analysis

In 2025, North America captured 42.65% of global revenue, driven by rapid FDA approvals, well-established reimbursement frameworks, and strong adoption in academic hospitals. The United States hosts over 150 operational systems, primarily concentrated in comprehensive stroke centers and pediatric hospitals. However, the adoption is expanding into mid-tier community facilities, supported by IAC accreditation that resolves billing uncertainties. In 2024, Canada secured Health Canada approval and initiated provincial pilots aimed at reducing inter-facility transfers for critical-care patients. Meanwhile, private hospital chains in Mexico are deploying portable scanners in emergency departments to reduce costly cross-border referrals, a strategy gaining traction due to rising stroke incidence and limited neurointerventional capacity.

The Asia-Pacific region is projected to lead growth with a 7.64% CAGR through 2031, supported by China's RMB 100 billion county-hospital modernization initiative and India's Ayushman Bharat universal health program. Hyperfine's clearance in December 2025 positions the company to supply over 150,000 rural Indian facilities lacking high-field suites, though success depends on achieving per-scan costs below the USD 50 reimbursement threshold. Japan's aging population and high stroke incidence highlight significant clinical demand, but reimbursement challenges and conservative radiologist practices are slowing adoption. In Australia, the Royal Flying Doctor Service is piloting airborne units, focusing on ruggedization and power autonomy for challenging environments, with findings expected to inform humanitarian deployments in Pacific Island states. South Korea's innovation-friendly regulatory environment is enabling tertiary centers to explore AI-driven low-field cardiac sequences, which could unlock a new market vertical if upcoming studies confirm diagnostic equivalence for pericardial assessments.

Europe accounted for approximately 22% of 2025 revenue, constrained by MDR compliance costs and fragmented reimbursement systems. In Germany, the Federal Joint Committee's delay in assigning a DRG code has hindered national rollouts despite CE-mark approvals. The United Kingdom is funding NHS stroke-network pilots, but a shortage of radiologists and technologists is limiting expansion beyond the initial 15 sites. France and Italy are prioritizing the utilization of their existing high-field fleets, citing sufficient geographic coverage and established referral patterns. However, peripheral regions with aging infrastructure are expressing interest in portable solutions as interim measures until suite refurbishments are completed. In the Middle East, private hospitals catering to medical tourists are adopting portable MRI systems as a premium differentiator. Sub-Saharan Africa faces capital constraints but benefits from non-profit partnerships that integrate tele-radiology support. In Latin America, the market remains nascent, with Brazil testing portable systems on Amazon riverboats to deliver remote care, while Argentina's currency volatility continues to challenge import financing.

Competitive Landscape

Fewer than ten companies have obtained regulatory approvals for sub-0.5 T portable brain-imaging platforms. Among these, the top three players—Hyperfine, Siemens Healthineers, and Aspect Imaging—account for approximately 70% of the market share. Hyperfine has leveraged its first-mover FDA clearance in 2020 and SPAC funding to deploy over 175 units globally, capturing nearly half of the ultra-low-field segment. Siemens launched the Free.Star 0.55 T in 2024, positioning it as a cost-effective, helium-free solution for emerging markets while safeguarding its high-field product portfolio. Aspect Imaging has established a strong foothold in neonatal intensive care with its 1.0 T Embrace scanner, securing a defensible niche in high-resolution imaging despite its larger physical footprint.

Market strategies are increasingly centered on subscription-based pricing models that bundle hardware, cloud-hosted AI, and continuous software updates. This approach aligns vendor revenues with utilization rates and reduces capital expenditure barriers for smaller healthcare facilities. Hyperfine’s Optive AI, cleared in June 2025, offers deep-learning reconstruction capabilities that radiologists equate to a nearly half-tesla performance boost. This creates significant switching costs and strengthens Hyperfine’s competitive position with a defensible algorithmic advantage. Patent analysis highlights Hyperfine’s focus on Halbach geometry and AI pipelines, while Siemens is investing in zero-boil-off superconducting magnets, which are expected to feature in future mid-field portable devices. Chinese companies, such as United Imaging Healthcare, are adopting aggressive domestic pricing strategies supported by government localization programs.

However, their limited FDA and CE mark approvals restrict their operations to regional markets. Meanwhile, niche players like Promaxo are targeting specialized applications, such as prostate biopsy guidance, with portable 0.064 T systems integrated with trans-perineal navigation. This demonstrates how clinical specialization can offset the disadvantages of late market entry. Although competition in the portable magnetic resonance imaging market is intensifying, regulatory barriers, supply chain complexities, and lengthy hospital procurement cycles continue to moderate competitive pressures.

Portable Magnetic Resonance Imaging Industry Leaders

-

Siemens Healthineers

-

Hyperfine Inc.

-

Canon Medical Systems

-

Voxelgrids Innovations Pvt. Ltd.

-

PrizMed Imaging Solution

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: New Zealand-based medical technology company Wellumio raised USD 7.3 million to continue development of its portable MRI device, Axana.

- October 2025: Hyperfine, Inc., the groundbreaking health technology company that has redefined brain imaging with the first FDA-cleared AI-powered portable MRI system for the brain—the Swoop system launched the Portable Ultra-Low-Field Scientific Exchange (PULSE), a subscription-based platform designed to empower a global community of clinical researchers and developers advancing access and innovation in portable MRI.

- July 2025: Jefferson Washington Township Hospital is the first in the U.S. to use an FDA-cleared AI-powered portable MRI system, enhancing bedside brain imaging. This innovation improves accessibility, efficiency, and image quality in patient care.

Global Portable Magnetic Resonance Imaging Market Report Scope

As per the scope of this report, portable magnetic resonance imaging refers to a compact, mobile MRI device that allows imaging at various locations outside traditional hospital settings. It provides quick, high-resolution scans for medical diagnosis with enhanced convenience and flexibility.

The Portable Magnetic Resonance Imaging Market is Segmented by Application (Neurology, Musculoskeletal, Cardiology, Pediatrics/Neonatal, Emergency & Trauma Care, and Other Applications), Facility Type (Hospitals, Diagnostic Imaging Centers, Ambulatory Surgery Centers, Neurology Offices & Clinics, and Other Facility Types), Magnet Strength (Ultra-Low-Field <0.2T, Low-Field 0.2–0.5T, Mid-Field 0.5–1.5T Compact, and Compact Super-Conducting >1.5T), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (USD million) for the above segments.

| Neurology |

| Musculoskeletal |

| Cardiology |

| Pediatrics / Neonatal |

| Emergency & Trauma Care |

| Other Applications |

| Hospitals |

| Diagnostic Imaging Centers |

| Ambulatory Surgery Centers |

| Neurology Offices & Clinics |

| Other Facility Types |

| Ultra-Low-Field (<0.2 T) |

| Low-Field (0.2–0.5 T) |

| Mid-Field (0.5–1.5 T) Compact |

| Compact Super-Conducting (>1.5 T) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Neurology | |

| Musculoskeletal | ||

| Cardiology | ||

| Pediatrics / Neonatal | ||

| Emergency & Trauma Care | ||

| Other Applications | ||

| By Facility Type | Hospitals | |

| Diagnostic Imaging Centers | ||

| Ambulatory Surgery Centers | ||

| Neurology Offices & Clinics | ||

| Other Facility Types | ||

| By Magnet Strength | Ultra-Low-Field (<0.2 T) | |

| Low-Field (0.2–0.5 T) | ||

| Mid-Field (0.5–1.5 T) Compact | ||

| Compact Super-Conducting (>1.5 T) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What CAGR is expected for portable MRI through 2031?

The market is projected to post a 6.05% CAGR from 2026 to 2031 based on current revenue trajectories.

Which clinical segment contributes the most revenue?

Neurology leads with 45.12% of 2025 revenue because portable MRI shortens stroke and head-trauma workflows.

Why do ambulatory surgery centers invest in portable MRI?

ASCs adopt portable scanners to confirm implant positioning before discharge, reducing readmissions and boosting bundled-payment margins.

How does ultra-low-field technology maintain image quality?

Vendors pair Halbach permanent magnets with deep-learning reconstruction that elevates 0.064 T images toward 0.35 T contrast-to-noise ratios.

Which region is forecast to grow fastest?

Asia-Pacific, supported by large rural-health initiatives in China and India, is expected to expand at 7.64% CAGR through 2031.

What are the principal barriers to adoption in Europe?

Fragmented reimbursement, MDR post-market studies, and radiologist staffing gaps slow widespread European deployment.

Page last updated on: