Polyvinyl Butyral (PVB) Interlayers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.05 Billion |

| Market Size (2031) | USD 7.14 Billion |

| Growth Rate (2026 - 2031) | 7.17% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Polyvinyl Butyral (PVB) Interlayers Market Analysis by ���ϲ�����

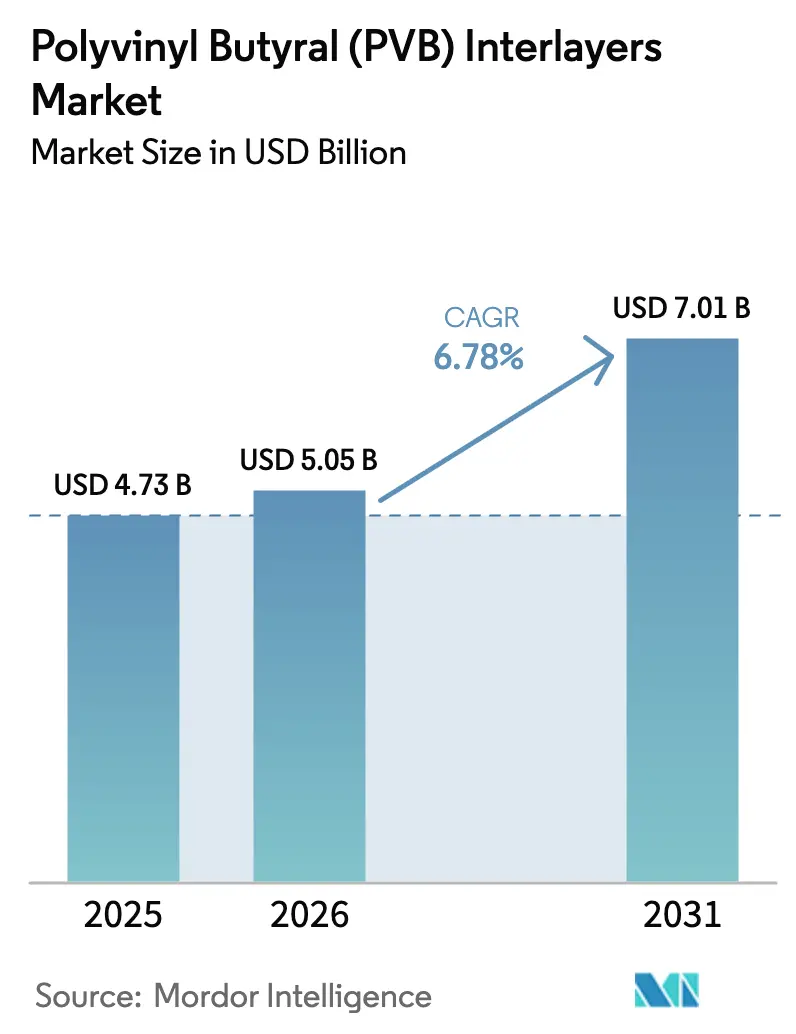

The Polyvinyl Butyral Interlayers Market size is projected to expand from USD 4.73 billion in 2025 and USD 5.05 billion in 2026 to USD 7.14 billion by 2031, registering a CAGR of 7.17% between 2026 to 2031. The acceleration comes from growing laminated-glass penetration in electric vehicles that favor thinner panoramic roofs, and from building-integrated photovoltaics mandated by net-zero construction goals. Acoustic PVB film uptake is widening as OEMs chase quieter cabins while keeping weight budgets in check, and architects are specifying UV-blocking grades that maintain daylighting yet limit glare. Asian resin producers have reached cost parity with global suppliers, encouraging local lamination investment and lifting regional demand. Vertical integration into polyvinyl-alcohol feedstocks is moderating price competition, and recycling breakthroughs hint at future circular-economy premiums.

Key Report Takeaways

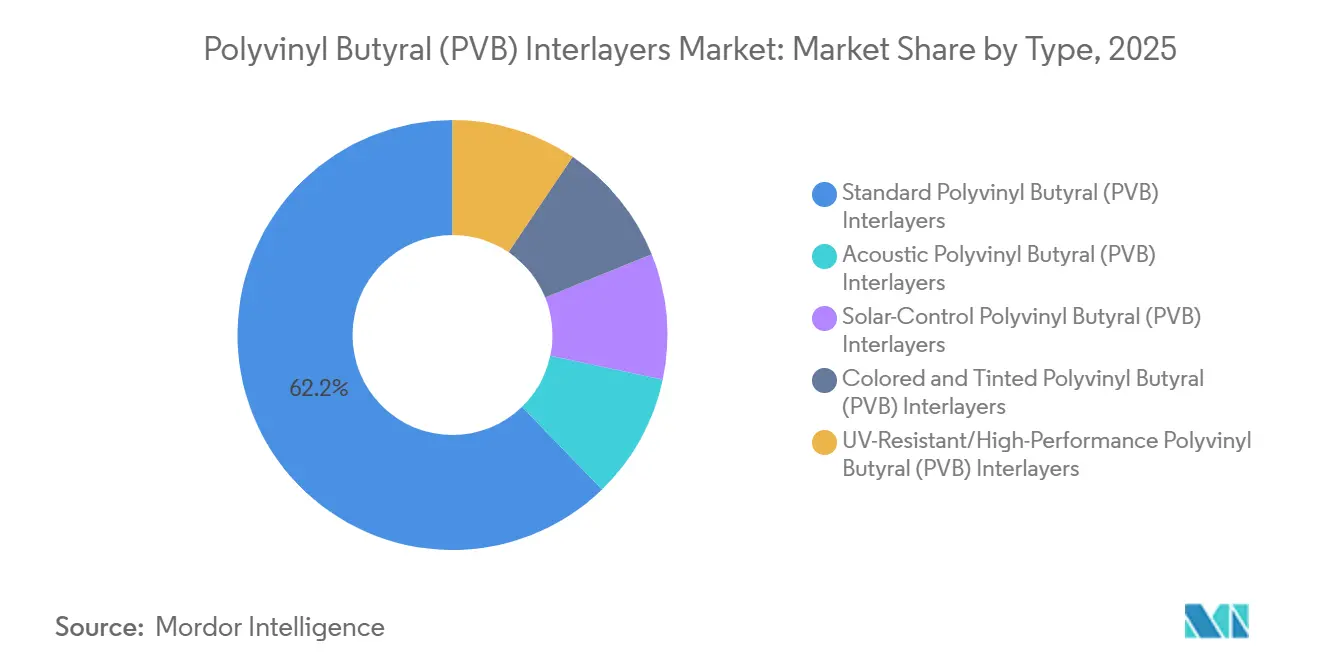

- By type, standard Polyvinyl Butyral (PVB) interlayers held 62.24% of the polyvinyl butyral (PVB) interlayers market share in 2025, while acoustic Polyvinyl Butyral (PVB) interlayers are on track for a 7.78% CAGR through 2031.

- By form, sheet/roll commanded 84.79% of the polyvinyl butyral (PVB) interlayers market share in 2025, but custom-cut/pre-laminated film is advancing at 7.91% CAGR through 2031.

- By application, automotive windshields led with 49.31% of the polyvinyl butyral (PVB) interlayers market share in 2025; interior decorative glass and partitions are forecast to expand at an 8.12% CAGR to 2031.

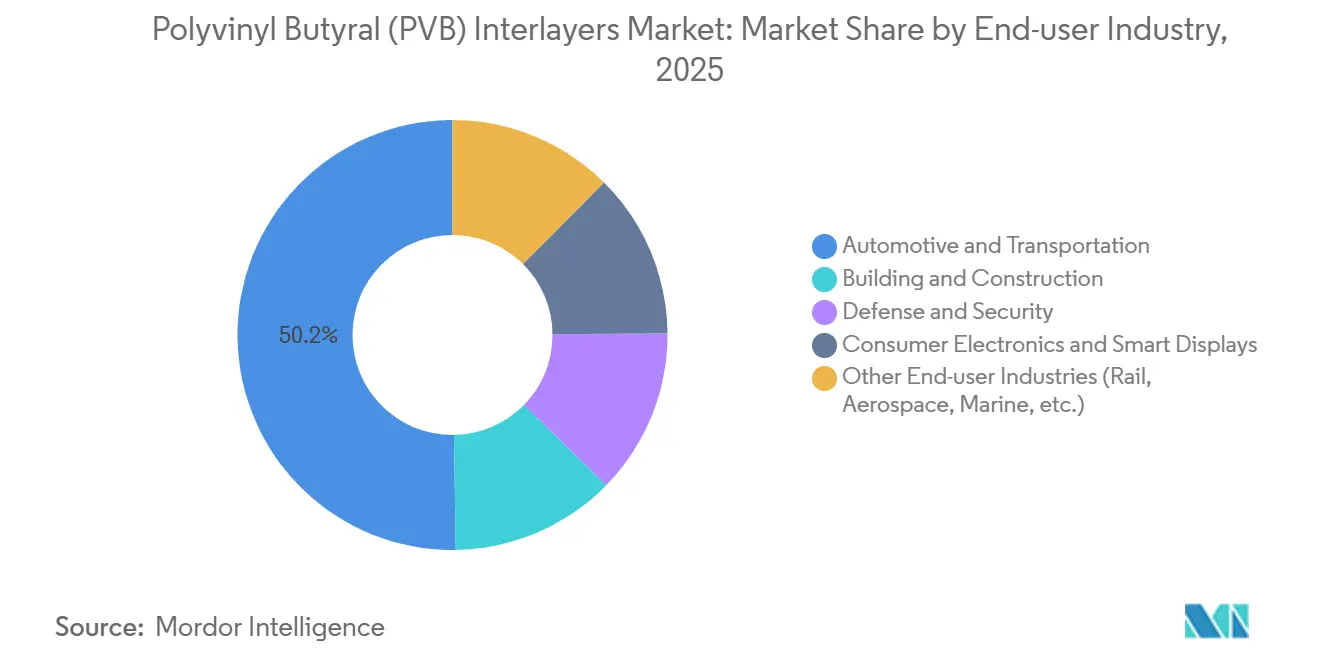

- By end-user industry, automotive and transportation captured 50.25% of the polyvinyl butyral (PVB) interlayers market share in 2025, whereas building and construction is projected to grow at an 8.23% CAGR through 2031.

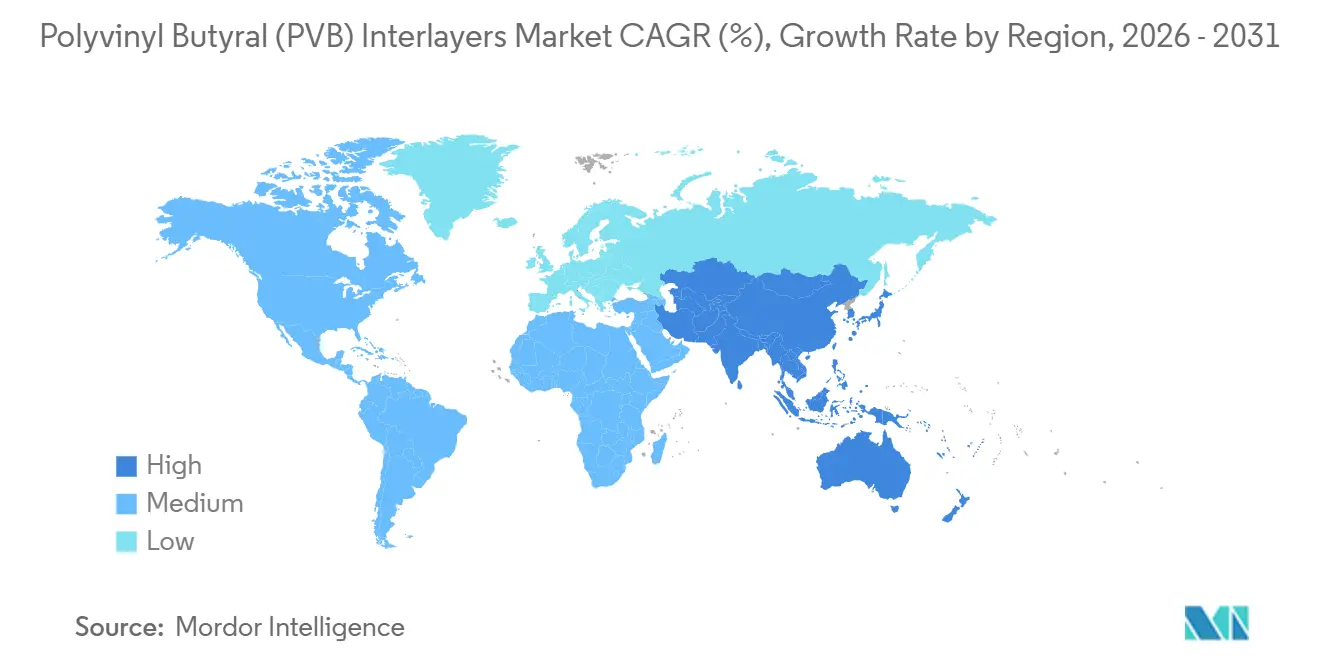

- By geography, Asia-Pacific accounted for 44.90% of the polyvinyl butyral (PVB) interlayers market share in 2025 and is poised for an 8.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyvinyl Butyral (PVB) Interlayers Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of laminated safety glass in automotive and construction | +1.8% | Global, with APAC and Europe leading automotive adoption; North America and Europe driving architectural glazing | Medium term (2-4 years) |

| Regulatory mandates for vehicle-occupant safety and glass strength | +1.5% | Global, strongest in Europe (ECE R43), North America (FMVSS 205), China (GB/T 5137) | Short term (≤ 2 years) |

| Rising demand for energy-efficient glazing and UV protection | +1.3% | Europe and North America for green building codes; APAC for commercial real estate | Medium term (2-4 years) |

| OEM shift to thinner panoramic EV sunroofs needing acoustic PVB | +1.4% | APAC core (China, India, South Korea), spill-over to North America and Europe | Short term (≤ 2 years) |

| Integration of PVB in building-integrated photovoltaics (BIPV) | +1.2% | Europe (Germany, France), China, emerging in Middle-East | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Growing Adoption of Laminated Safety Glass in Automotive and Construction

Automotive OEMs are extending laminated glass to side windows to meet updated crash protocols and to lower cabin noise, relying on PVB interlayers for viscoelastic damping. Architects specify laminated glass in façades, canopies, and balustrades that must pass ASTM E1996 and EN 12600 impact tests, particularly in typhoon-prone ASEAN markets. Thicker PVB constructions reaching 1.52 mm enable design pressures above 6 kPa, enhancing occupant safety. Insurance incentives and building codes further speed adoption, lifting PVB demand faster than underlying vehicle production or building starts. The driver’s influence radiates across both mobility and infrastructure supply chains.

Regulatory Mandates for Vehicle-Occupant Safety and Glass Strength

ECE R43 amendments effective 2024 require windshields to withstand higher-energy ball-drop tests, nudging PVB thickness to 0.89-1.14 mm in compact cars. China’s GB/T 5137 now aligns with ISO 3537 optical rules, steering domestic makers toward certified PVB brands. North America is consulting on extending laminated requirements to rear windows, widening the addressable volume. Certified suppliers with ISO 9001 and IATF 16949 status, therefore, capture a greater share as compliance costs discourage new entrants.

Rising Demand for Energy-Efficient Glazing and UV Protection

Energy codes in the EU, California Title 24, and China spur solar-control PVB that blocks infrared yet keeps visible transmittance above 70%, trimming HVAC loads by 15-25%. Saflex Solar interlayers with metal-oxide nanoparticles serve Middle-East façades where cooling can hit 60% of building energy demand. UV-blocking grades protect artifacts, retail goods, and cabin trims by screening 99-100% of sub-380 nm radiation, lowering warranty claims. BIPV modules gain extra durability because PVB encapsulation resists moisture ingress, underpinning 30-year service life requirements. The dual benefit of thermal savings and material longevity lifts willingness to pay for premium interlayers.

Integration of PVB in Building-Integrated Photovoltaics (BIPV)

IEA PVPS tests show PVB-encapsulated double-glass PV modules registering zero water penetration after 1,000 hours, versus 30 mm for EVA. China projects PV-grade PVB demand of 65,000 t in 2025 as Shenzhen and Shanghai mandate BIPV on new commercial roofs. Europe’s Energy Performance of Buildings Directive encourages BIPV in major renovations, with Germany and France leading uptake[1]European Commission, “Energy Performance of Buildings Directive,” europa.eu . PVB’s thermoplastic nature also eases module disassembly for end-of-life recovery. These factors anchor long-term growth in construction glazing that doubles as energy generation.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price fluctuations in PVB resins and additives | -0.9% | Global, most acute in regions dependent on imported polyvinyl alcohol (North America, Europe, Southeast Asia) | Short term (≤ 2 years) |

| Limited recycling infrastructure for end-of-life PVB laminates | -0.5% | Global, with infrastructure gaps most severe in Asia-Pacific and Middle-East and Africa | Long term (≥ 4 years) |

| Design-code compliance gaps on visco-elastic modulus (EU) | -0.4% | Europe, particularly Germany, France, Italy, and Nordic countries with stringent structural-glazing codes | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Price Fluctuations in PVB Resins and Additives

US export PVA hit USD 3,000 t in June 2025, 6% higher year-on-year, and force-majeure events on 2-ethylhexanol and TOTM spiked plasticizer prices in 2024. Anti-dumping duties on DOTP imports into the United States raised sourcing costs by 57-81%. Mid-tier film producers operating on single-digit margins struggle to pass through hikes locked in yearly contracts. Chinese players such as HuaiDe New Materials have responded with RMB 1.016 billion integrated film-plus-resin complexes that hedge feedstock risk.

Limited Recycling Infrastructure for End-of-Life PVB Laminates

The EU SUNRISE pilot processed 544 t per year with 90% sorting accuracy and a 70% CO₂ cut but remains confined to a handful of plants in Belgium, the Netherlands, and Germany. Asia and MEA largely landfill laminated glass, as collection networks are sparse and tipping fees remain low. Maltha Glass Recycling targets 40% re-PVB content yet needs virgin prices above USD 2,500 t to break even. Industrial solvent-dissolution techniques in Korea and Poland show promise at 8-10 t per day, but none yet match virgin resin cost at scale. Absent infrastructure curbs green-building credits that could widen PVB premiums.

Segment Analysis

By Type: Acoustic Variants Gain as EV Noise Floors Drop

Standard Polyvinyl Butyral (PVB) interlayers held 62.24% in 2025, anchored in windshields and budget façades where clarity and cost dominate. Acoustic Polyvinyl Butyral (PVB) interlayers targets a 7.78% CAGR through 2031 as battery-electric vehicles eliminate engine masking and side laminates become mainstream. Solar-control types remain below 10% share because of 15-20% premiums, yet heat-dominant climates in the Middle-East are tipping specifications. Colored, tinted, UV-resistant, and high-performance formulations chase niche façade aesthetics and artifact preservation needs.

Kuraray’s SkyViera fuses acoustic damping with solar reflection, reducing inventory complexity for glass fabricators[2]Kuraray, “Trosifol SkyViera Technical Sheet,” kuraray.com . Sekisui’s N-HPP wedge films integrate HUD optics without ghosting and will ship from Thailand in 2026. These multifunctional trends compress standard-grade volume share, yet replacement windshields and price-sensitive housing keep the latter dominant. Across all types, ISO 12543 and ASTM C1172 compliance costs deter small challengers, reinforcing incumbent positions.

Note: Segment shares of all individual segments available upon report purchase

By Form: Custom-Cut Films Reduce Laminator Waste

Sheet/roll captured 84.79% in 2025 as legacy autoclave lines rely on them for speed and simplicity. Custom-cut/pre-laminated films are tracking 7.91% CAGR through 2031 due to higher first-pass yields that trim scrap from 10-15% to under 5% in curved automotive lights. Digital cutting services now return net-shape interlayers within three days, a leap from multi-week lead times.

Roll stock retains an edge in high-volume windshields and oversized façade lites, letting fabricators integrate printed heaters and sensor arrays during extrusion. The polyvinyl butyral (PVB) interlayers market benefits as laminators balance throughput and customization, but custom-cut uptake is fastest where batch sizes stay small and product mixes shift quickly, notably in China, South Korea, and India.

By Application: Interior Decorative Glass and Partitions Outpace Automotive Windshields

Automotive windshields remained the single largest application at 49.31% in 2025. Interior decorative glass and partitions are expected to chart an 8.12% CAGR through 2031, driven by open-plan offices blending transparency with acoustic privacy. Premium partitions equipped with PVB achieve STC ratings of 32-38 dB that meet global office standards. Side and rear vehicle glazing is also pivoting to laminated constructions, extending UV and sound benefits to passengers.

Architectural use in façades grows on hurricane-resistant codes and blast-mitigation demands in the Middle-East, where PVB laminates tested to ASTM F3561 and EN 13541 offer balanced protection and clarity. Specialty ballistic and forced-entry glass for banks and embassies commands 20-30% price premiums. Consumer electronics are opening a new avenue with PDLC and SPD switchable films bonded through PVB, hinting at cross-industry growth.

By End-user Industry: Construction Overtakes Automotive Growth

Automotive and transportation maintained 50.25% in 2025 but faces slower vehicle build rates ahead. Building and construction is set for an 8.23% CAGR, buoyed by BIPV mandates and glass-rich interiors in post-pandemic refurbishments. Façade projects prize PVB for post-breakage retention and UV blocking while enabling lighter glass plies that reduce framing loads.

Defense and security yield outsized margins on multi-ply laminates certified to UL 752 and EN 1063. Consumer electronics are an emerging silver, embedding transparent OLEDs and electrochromic panes via PVB lamination. The polyvinyl butyral (PVB) interlayers market finds resilience through end-use industry diversification that cuts dependence on auto cycles.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific owned 44.90% of 2025 demand and also post an 8.15% CAGR to 2031. China, with HuaiDe and Anhui Wanwei is adding 20,000-t resin lines that integrate upstream and downstream capacity. India gains momentum as Mahindra Electric selects acoustic PVB for new EVs and the Bureau of Energy Efficiency bans single-pane glass in offices. Japan and South Korea preserve technical leads in HUD-compatible films, while Sekisui’s Thailand site will feed ASEAN OEMs with 7 million glass sets yearly starting H2 2026.

In North America, mature auto output tempers growth, but strict FMVSS and ASTM norms favor certified suppliers. Mexico is attracting laminated-glass investment under USMCA rules. Europe is led by BIPV adoption under the Energy Performance of Buildings Directive, though high energy costs squeeze fabricators. Germany, France, and the United Kingdom remain leaders in solar-control and acoustic interlayer demand for office and rail-station façades.

South America and the Middle-East and Africa combined for lower share. Saudi Arabia’s Vision 2030 pipeline and NEOM megaprojects specify PVB façades for energy-efficient envelopes while Brazil’s auto recovery lifts windshield volumes. South Africa functions as a regional hub for architectural lamination yet still imports most film, hinting at potential joint-venture openings.

Competitive Landscape

Kuraray, Eastman, Chang Chun Group, Saint-Gobain, and Sekisui command roughly 69% of global capacity, setting a moderate-concentration tone. They pursue regional expansions instead of price wars: Eastman’s Belgium site is online in 2026, Sekisui’s Thailand line arrives the same year, and Kuraray scales multifunctional acoustic grades. Chinese firms HuaiDe, Anhui Wanwei, and Zhejiang Decent climb the value ladder with acoustic and solar-control offerings, eroding technology gaps yet staying price-competitive.

Strategic themes include backward integration into PVA, co-location with lamination plants to cut freight, and R&D into wedge HUD, photochromic, and blast-resistant films that yield 15-25% gross-margin premiums. Disruptive prospects come from low-temperature liquid optical clear adhesives that bypass autoclaves, though durability testing is still underway. Circular-economy differentiation may arise as the SUNRISE recycling model scales and CEN CWA 18174 sets quality tiers for re-PVB. Certification hurdles under ISO 12543, ASTM C1172, and IATF 16949 remain high barriers for newcomers.

Polyvinyl Butyral (PVB) Interlayers Industry Leaders

Chang Chun Group

Eastman Chemical Company

Saint-Gobain

SEKISUI CHEMICAL CO., LTD.

KURARAY CO., LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: KURARAY CO., LTD. showcased its Trosifol PVB interlayers for high-performance architectural glass at the 5th edition of Zak World of Façades, Saudi Arabia. The presentation highlighted solutions tailored to endure the extreme heat of the Middle-East, focusing on structural strength, durability, and minimized delamination for complex facade, wind, and impact-resistant applications.

- November 2024: Eastman Chemical Company broke ground on a significant expansion at its Ghent, Belgium, facility to increase the production capacity of Saflex PVB interlayers. The project is expected to be completed in the second half of 2026.

Global Polyvinyl Butyral (PVB) Interlayers Market Report Scope

Polyvinyl Butyral (PVB) is a flexible, high-performance plastic resin film primarily utilized as an interlayer in laminated glass for automotive windshields and architectural safety glazing. Known for its strong adhesion, high optical clarity, tensile strength, and impact resistance, PVB helps hold glass together upon breakage, thereby improving safety and security.

The Polyvinyl Butyral (PVB) Interlayers Market is segmented by type, form, application, end-user industry, and geography, By type, the market is segmented into standard polyvinyl butyral (PVB) interlayers, acoustic polyvinyl butyral (PVB) interlayers, solar-control polyvinyl butyral (PVB) interlayers, colored and tinted polyvinyl butyral (PVB) interlayers, and UV-resistant/high-performance polyvinyl butyral (PVB) interlayers. By form, the market is segmented into sheet/roll and custom-cut/pre-laminated film. By application, the market is segmented into automotive windshields, side and rear automotive glazing, architectural glazing (windows, façades, roofs), interior decorative glass and partitions, and specialty (bullet, blast-resistant). By end-user industry, the market is segmented into automotive and transportation, building and construction, defense and security, consumer electronics and smart displays, and other end-user industries (rail, aerospace, marine, etc.). The report also covers market size and forecasts for polyvinyl butyral (PVB) interlayers in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Standard Polyvinyl Butyral (PVB) Interlayers |

| Acoustic Polyvinyl Butyral (PVB) Interlayers |

| Solar-Control Polyvinyl Butyral (PVB) Interlayers |

| Colored and Tinted Polyvinyl Butyral (PVB) Interlayers |

| UV-Resistant/High-Performance Polyvinyl Butyral (PVB) Interlayers |

| Sheet/Roll |

| Custom-Cut/Pre-laminated Film |

| Automotive Windshields |

| Side and Rear Automotive Glazing |

| Architectural Glazing (Windows, Façades, Roofs) |

| Interior Decorative Glass and Partitions |

| Specialty (Bullet, Blast-Resistant) |

| Automotive and Transportation |

| Building and Construction |

| Defense and Security |

| Consumer Electronics and Smart Displays |

| Other End-user Industries (Rail, Aerospace, Marine, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Standard Polyvinyl Butyral (PVB) Interlayers | |

| Acoustic Polyvinyl Butyral (PVB) Interlayers | ||

| Solar-Control Polyvinyl Butyral (PVB) Interlayers | ||

| Colored and Tinted Polyvinyl Butyral (PVB) Interlayers | ||

| UV-Resistant/High-Performance Polyvinyl Butyral (PVB) Interlayers | ||

| By Form | Sheet/Roll | |

| Custom-Cut/Pre-laminated Film | ||

| By Application | Automotive Windshields | |

| Side and Rear Automotive Glazing | ||

| Architectural Glazing (Windows, Façades, Roofs) | ||

| Interior Decorative Glass and Partitions | ||

| Specialty (Bullet, Blast-Resistant) | ||

| By End-user Industry | Automotive and Transportation | |

| Building and Construction | ||

| Defense and Security | ||

| Consumer Electronics and Smart Displays | ||

| Other End-user Industries (Rail, Aerospace, Marine, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the Polyvinyl Butyral (PVB) Interlayers market?

The polyvinyl butyral (PVB) interlayers market stands at USD 5.05 billion in 2026 and is forecast to reach USD 7.14 billion by 2031, with a CAGR of 7.17% through 2031.

Which type is growing fastest?

Acoustic Polyvinyl Butyral (PVB) interlayers are advancing at a 7.78% CAGR through 2031.

Why is Asia-Pacific expanding faster than other regions?

Cost-competitive Chinese resin, rising domestic auto glass demand, and new capacity in Thailand and India together support an 8.15% CAGR in the region.

How do regulatory changes influence automotive glazing choices?

Stricter ECE R43, FMVSS 205, and GB/T 5137 tests require thicker, higher-strength laminated glass, pushing OEMs toward certified PVB suppliers.