Polymer Binder Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

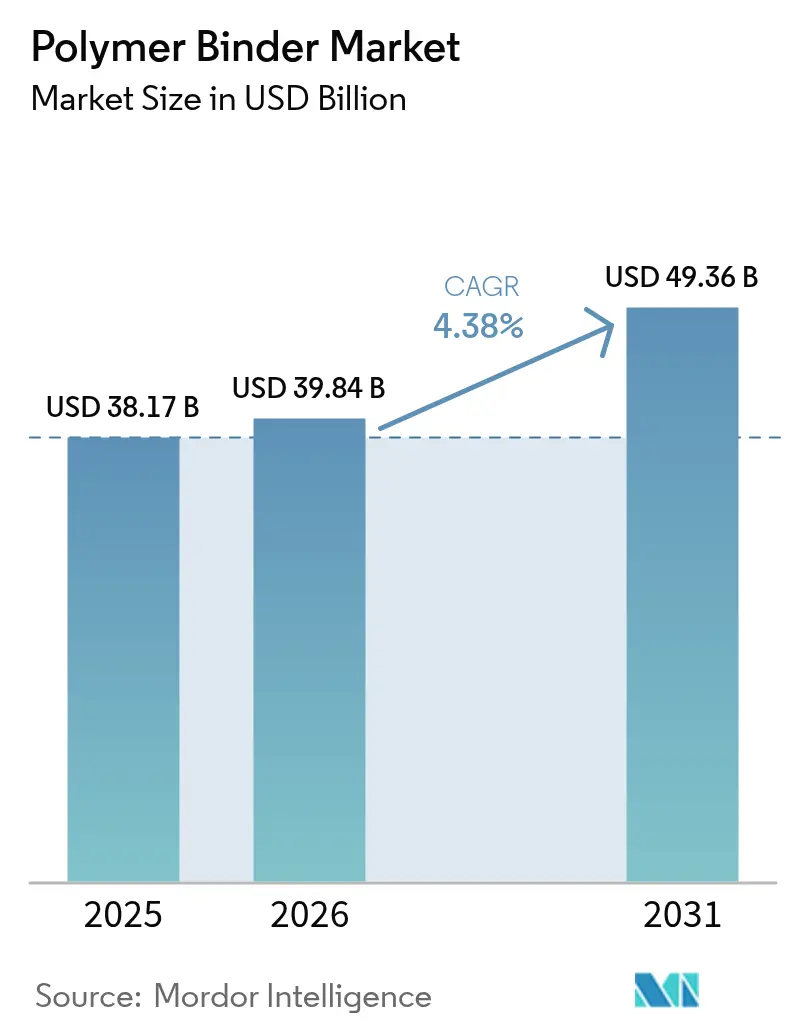

| Market Size (2026) | USD 39.84 Billion |

| Market Size (2031) | USD 49.36 Billion |

| Growth Rate (2026 - 2031) | 4.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Polymer Binder Market Analysis by ���ϲ�����

Polymer Binder Market size in 2026 is estimated at USD 39.84 billion, growing from 2025 value of USD 38.17 billion with 2031 projections showing USD 49.36 billion, growing at 4.38% CAGR over 2026-2031. Architectural and industrial coatings continue to anchor consumption, yet battery electrodes, powder-bed additive manufacturing, and circular-economy packaging are carving measurable new volumes that compensate for declines in legacy paper and carpet uses. Liquid, water-borne formulations have moved into the mainstream as regulations in North America, Europe, and parts of Asia restrict solvent emissions, prompting chemistry innovations that preserve adhesion while cutting VOCs. Vinyl acetate continues to outperform competing chemistries thanks to its wide formulation window, price competitiveness, and compatibility with low-VOC systems, while bio-attributed grades now in pilot scale promise lower carbon footprints. Competitive pressure is increasingly expressed through sustainability pledges, regional capacity additions, and technical alliances that safeguard intellectual property in emerging battery and 3D printing applications.

Key Report Takeaways

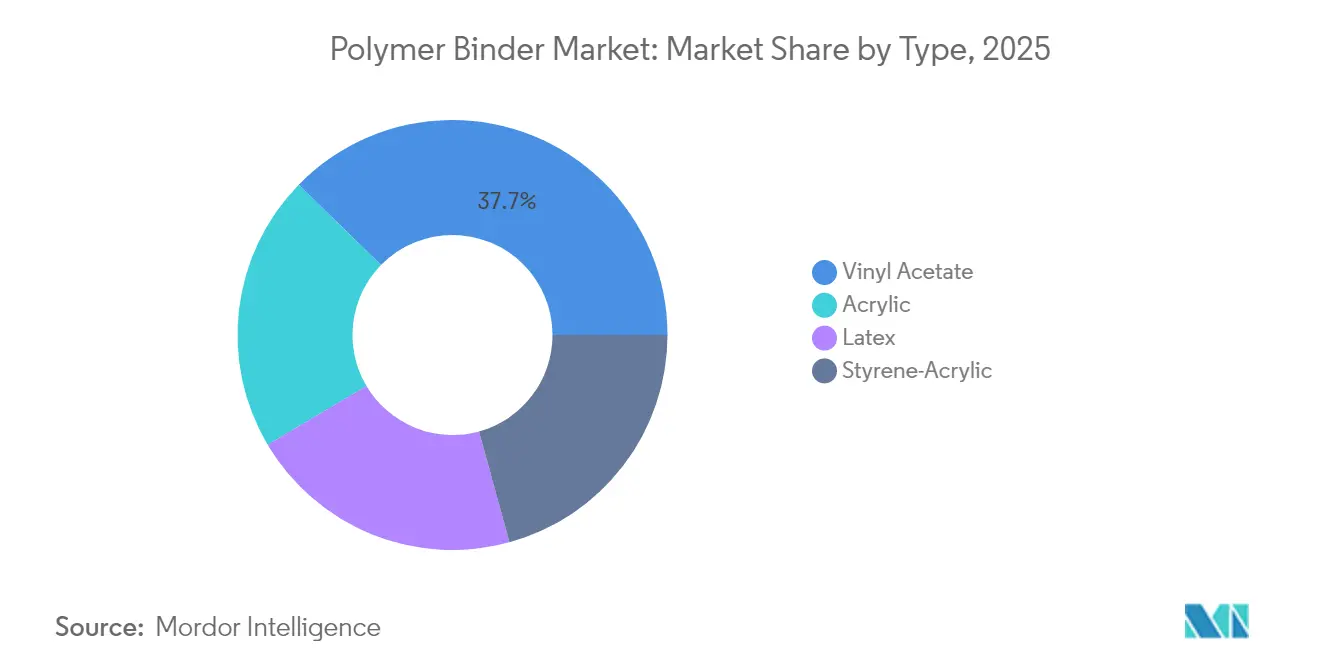

- By type, vinyl acetate led with 37.68% share of the polymer binder market in 2025 and is expected to expand at 5.83% CAGR to 2031.

- By form, liquid grades held 64.10% of 2025 revenue and are advancing at a 5.14% CAGR as producers shift further toward waterborne systems.

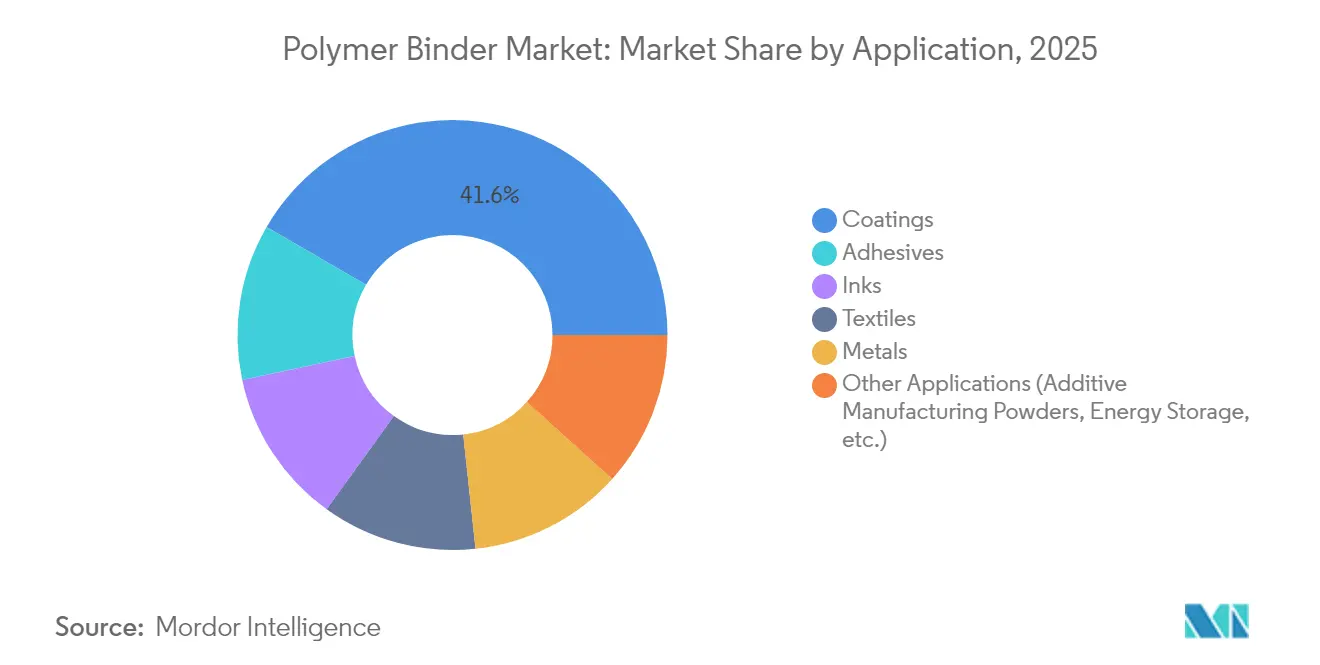

- By application, coatings commanded 41.62% revenue share of the polymer binder market in 2025, whereas the “Other Applications” cluster is projected to accelerate at 5.98% CAGR through 2031.

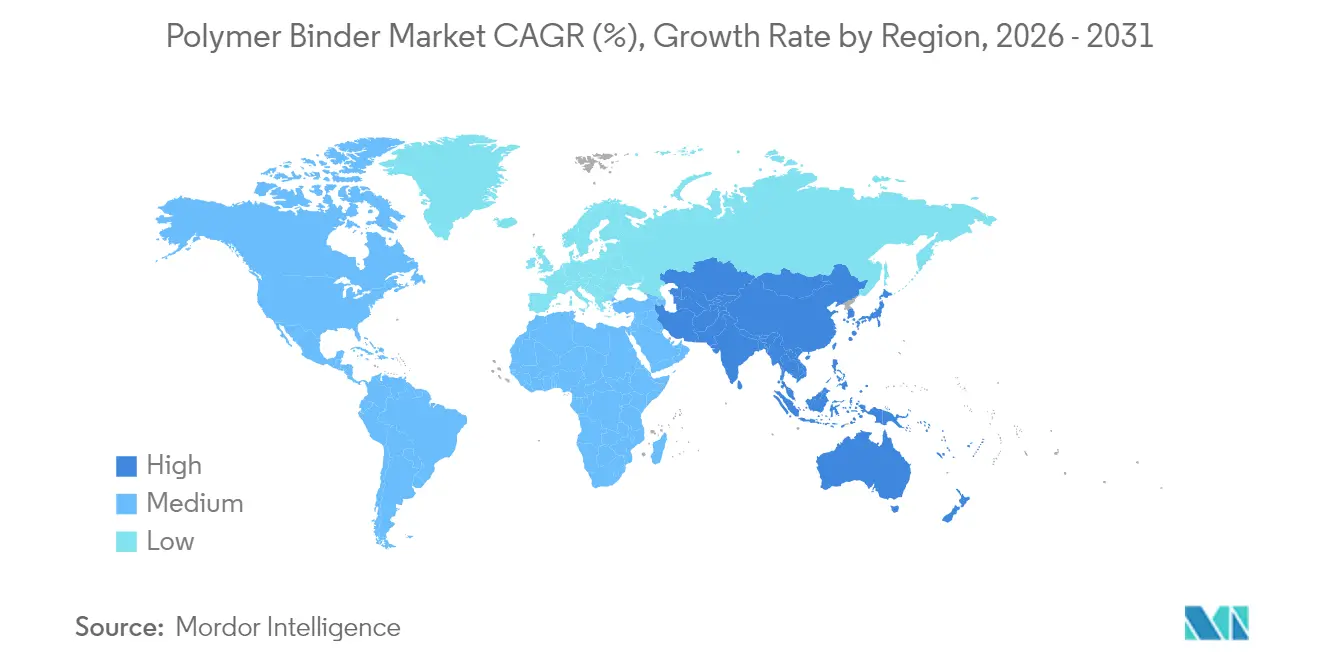

- By geography, Asia-Pacific accounted for 54.20% of 2025 demand and is forecast to grow fastest at 5.19% CAGR, reflecting simultaneous construction and battery manufacturing upswings.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polymer Binder Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand from architectural and industrial coatings | +1.2% | Global with APAC leading | Medium term (2-4 years) |

| Rapid shift toward waterborne low-VOC formulations | +0.8% | North America and EU first adopters, APAC following | Short term (≤ 2 years) |

| Rising adoption of polymer binders in Li-ion battery electrodes | +0.6% | APAC core with spillover to North America | Long term (≥ 4 years) |

| Expanding use in powder-bed additive manufacturing | +0.4% | North America and EU innovation hubs | Long term (≥ 4 years) |

| Bio-based binder Research and Development for circular-economy compliance | +0.3% | EU leading, North America following | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Surging Demand from Architectural and Industrial Coatings

Urbanization, infrastructure renewal, and higher performance expectations in harsh climates push coating formulators to specify advanced polymer binders that deliver durability, stain resistance, and color retention under tropical humidity or severe winter freeze–thaw cycles. Waterborne emulsions claimed almost two-thirds of new architectural coating formulations 2025, a milestone reflecting stricter emissions rules and end-user preferences for low-odor products. Industrial facilities are adopting high-solids epoxy-acrylic hybrids to extend maintenance intervals on bridges, pipelines, and rolling stock, drawing on binder chemistries that withstand chemical immersion and thermal shock. Premium exterior paints integrate self-crosslinking vinyl acetate systems that reduce coalescent demand, trimming VOC emissions without compromising film integrity. The upgrading trend is particularly visible in China, India, and Indonesia, where mass housing programs combine with rising disposable income to lift expectations for façade longevity. Multinational coatings groups localize supply chains, anchoring regional demand for reliable binder raw materials.

Rapid Shift Toward Waterborne Low-VOC Formulations

Regulators now push VOC limits well below 50 g/L in building coatings, turning legacy solvent-borne systems into niche products within two years in California and several EU states. Binder producers responded with acrylic and vinyl acrylic emulsions capable of forming hard, chemical-resistant films at room temperature while keeping VOC well under 5 g/L. For instance, Dow’s ML-520 acrylic binder achieves exterior durability ratings comparable with long-standing solvent-borne alkyds[1]Dow, “MULTILOBE ML-520 Acrylic Binder,” dow.com. Architects and health-conscious homeowners accelerated adoption by specifying zero-odor paints for schools and hospitals, creating a pull effect that spreads beyond regulated regions. Equipment suppliers also adapted; spray-gun manufacturers launched tips optimized for low-viscosity water-borne paints, reducing overspray and easing the switch for contractors. Asian construction markets are following quickly as export-oriented coating companies align formulations to meet EU eco-labels. The resulting demand surge for water-compatible binders has shortened order cycles, forcing some suppliers to run plants near capacity.

Rising Adoption of Polymer Binders in Li-Ion Battery Electrodes

Electrification of mobility reshaped the customer base for binder producers by introducing gigafactories that consume specialty grades at volumes unseen five years ago. Cathode and anode coatings require binders that tolerate high voltages, withstand hundreds of charge cycles, and maintain adhesion on aluminum and copper foils after exposure to electrolyte solvents. Chinese and South Korean cell makers have issued multi-year procurement contracts to secure reliable quality, rewarding suppliers that can document metal-ion purity below 50 ppm and particle size under 500 nm. Celanese broadened its portfolio with flexible polyamide binders tailored to thermal management layers inside battery packs.

Expanding Use in Powder-Bed Additive Manufacturing Processes

Powder-bed fusion printers for aerospace, dental, and high-performance automotive parts need polymer binders that flow smoothly at room temperature yet fuse rapidly when hit by laser or electron beams. Rheology, thermal decomposition curve, and off-gas profile must align with machine parameters to avoid warping or voids. Research teams at North American universities published studies using multifunctional acrylic-urethane binders to reach tensile strengths above 75 MPa in carbon-fiber reinforced prints[2]MDPI, “Performance of Multifunctional Acrylic-Urethane Binders in Additive Manufacturing,” mdpi.com . Chemical companies responded by introducing narrowly distributed powder binders with antistatic coatings that minimize agglomeration during storage in humid climates. Early adopters report 15% faster build rates after binder optimization, validating the value proposition despite higher raw-material cost. Government-funded aerospace projects in the United States and Germany further stimulate demand by specifying additive manufacturing for satellite components, cementing a technological beachhead that feedstocks suppliers will scale over the decade.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural decline in paper and carpet manufacturing | -0.7% | North America and EU | Medium term (2-4 years) |

| Volatility in key monomer feedstock prices | -0.5% | Global with APAC exposure | Short term (≤ 2 years) |

| Tightening PFAS-related regulations on fluoropolymer binders | -0.3% | North America and EU leading | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Structural Decline in Paper and Carpet Manufacturing

Digitalization keeps shrinking demand for graphic printing papers, eliminating once-steady volumes for starch-vinyl acetate copolymer binders used in surface sizing. Carpet demand in residential remodeling is also waning in favor of luxury vinyl tile and laminate flooring that use different adhesive chemistries, undercutting latex binder sales in North America and Western Europe. Packaging paper and tissue segments still grow, yet they require higher wet-strength additives and bio-based binders that command different formulation balances, forcing producers to redesign lines. International Paper announced its merger with DS Smith, positions fiber-based packaging to serve e-commerce, creating pockets of opportunity for new aqueous binders. The net effect on total polymer binder volume is modestly negative because emerging grades have higher unit value but lower wet pickup rates, resulting in smaller tonnage. Regional mills idled since 2023 are unlikely to restart, cementing the structural shift.

Volatility in Key Monomer Feedstock Prices

Acetic acid, butyl acrylate, and styrene prices have swung 30% in six-month intervals since 2024 as refinery outages, shipping congestion, and geopolitical tensions disrupted supply. Smaller binder producers lacking backward integration absorb cost spikes that erode margins and restrict capital for innovation. Asian formulators face added currency risks when spot cargoes are priced in USD, compelling them to hedge or shorten quotation validity. Some multinationals diversified via long-term bio-route contracts, locking in feedstock derived from sugarcane ethanol or tall-oil fractions, thereby smoothing cost curves. The approach requires certification under ISCC PLUS or comparable mass-balance schemes to satisfy eco-label auditors, adding administrative overhead. Despite these efforts, sustained price turbulence still delays customer price lists and complicates budgeting for paint and adhesive manufacturers.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Vinyl Acetate Sustains Leadership Through Versatility and Regulatory Fit

Vinyl acetate held 37.68% of the polymer binder market in 2025 and is forecast to record a 5.83% CAGR through 2031, underscoring its adaptability to water-borne, low-VOC paints and to emerging battery slurries that demand stable colloidal dispersions. Complementary chemistries such as pure acrylics dominate premium topcoat formulations requiring chalking resistance, while styrene-acrylics serve economical interior paints and select paper saturations. Recent bio-attributed pilot batches demonstrate that vinyl acetate can incorporate fermentative acetic acid without altering polymer performance, aligning the matrix with Scope 3 decarbonization targets.

Continued research into self-crosslinking technology is sharpening vinyl acetate’s competitive edge by boosting block resistance and early water resistance in exterior paints, features once reserved for pure acrylics. The incorporation of reactive surfactants improves scrub durability while lowering free surfactant migration, an attribute that enhances stain resistance on interior walls.

By Form: Liquid Grades Preserve Dominance as Water-Borne Shift Accelerates

Liquid dispersions accounted for 64.10% of polymer binder market size in 2025 and are projected to post a 5.14% CAGR to 2031 as formulators worldwide replace solvent-borne systems with water-thin alternatives. Their ease of pumping, blending, and filtration on existing paint lines removes costly process changes, enabling small and midsize coaters to comply with VOC caps within tight budgets. High-solids liquids are penetrating industrial maintenance coatings, offering low flash points and expedited cure times compared with traditional two-component epoxies. Powder binders retain relevance in additive manufacturing and select textile finishes that demand extended shelf life without refrigeration, yet supply remains constrained to specialized plants with stringent particle morphology controls.

By Application: Coatings Anchor Revenue while Emerging uses Propel Incremental Growth

Coatings maintained 41.62% of the 2025 demand in the polymer binder market as households, infrastructure managers, and OEM finishers prioritized aesthetics and protection. The segment’s volume scale underwrites feeder plant economics, yet its growth rate trails the 5.98% CAGR predicted for “Other Applications,” a bucket encompassing batteries, 3D printing, and specialty filtration. Adhesives remain a steady mid-growth niche, leveraging vinyl acetate–ethylene copolymers that offer high green-bond strength in carton sealing and parquet installation. Textile finishing uses continue migrating toward Asia, combining with functional apparel exports to maintain respectable tonnage despite competition from mechanically bonded nonwovens.

Geography Analysis

Asia-Pacific delivered 54.20% of 2025 revenue and is forecast to outpace all regions with a 5.19% CAGR, cementing its dual role as volume leader and growth engine. China’s megacity expansions and refurbishment of older apartment blocks sustain a massive need for exterior wall coatings that rely on versatile vinyl acetate binders. At the same time, the country’s battery manufacturers are commissioning cathode-active material lines at a record pace, each requiring dedicated binder supply streams with rigorous impurity thresholds.

North America exhibits mature, replacement-driven demand dynamics tempered by regulation-led formulation shifts. State agencies in the United States push VOC thresholds lower than federal baselines, while Canadian building codes now reference embodied-carbon targets. Europe upholds its role as a regulatory bellwether, compelling early adoption of fluorine-free, waterborne acrylic and silicone-hybrid binders. PFAS proposals add urgency, prompting formulators to clear inventories and secure alternative chemistries.

Competitive Landscape

The market is highly fragmented. Competition in the polymer binder market centers on a mix of scale, regional depth, and technology breadth. Strategic capacity expansions align with regional and end-use hotspots. Sustainability now drives differentiation as much as technical performance. Companies quantify cradle-to-gate greenhouse-gas intensity and broadcast reductions achieved through renewable electricity, carbon capture, and bio-feedstock adoption. Customers align purchasing policies accordingly, introducing internal scoring matrices that favor suppliers with third-party verified life-cycle assessments.

Polymer Binder Industry Leaders

Dow

Celanese Corporation

Arkema

Wacker Chemie AG

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Arkema earned ISCC PLUS certification for bio-attributed water-borne acrylic resin production at its Saint Charles, Louisiana plant, expanding its mass-balance polymer-binder offering for coatings and adhesives.

- April 2025: BASF introduced Acrodur ecotechnology solutions at CHINAPLAS 2025, delivering tailor-made, more-sustainable polymer binders for diverse industrial uses.

Global Polymer Binder Market Report Scope

The polymer binder market report includes:

| Vinyl Acetate |

| Acrylic |

| Styrene-Acrylic |

| Latex |

| Powder |

| Liquids |

| High-Solids |

| Coatings |

| Adhesives |

| Textiles |

| Inks |

| Metals |

| Other Applications (Additive Manufacturing Powders, Energy Storage, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Vinyl Acetate | |

| Acrylic | ||

| Styrene-Acrylic | ||

| Latex | ||

| By Form | Powder | |

| Liquids | ||

| High-Solids | ||

| By Application | Coatings | |

| Adhesives | ||

| Textiles | ||

| Inks | ||

| Metals | ||

| Other Applications (Additive Manufacturing Powders, Energy Storage, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current polymer binder market size and its projected growth?

The market is valued at USD 39.84 billion in 2026 and is set to reach USD 49.36 billion by 2031, advancing at a 4.38% CAGR

Which application leads demand in the polymer binder market?

Architectural and industrial coatings together secured 41.62% of 2025 revenue, maintaining the largest share owing to ongoing construction and maintenance activity

Why is vinyl acetate important to the polymer binder industry?

Vinyl acetate combines strong adhesion, low-VOC compatibility, and cost efficiency, enabling it to cover conventional coatings while penetrating new battery electrode formulations, and it achieves a 5.83% CAGR outlook

Which region is expanding fastest in the polymer binder market?

Asia-Pacific leads both in volume and growth, posting a 5.19% CAGR to 2031 as China, India, and Southeast Asia invest in construction, battery plants, and manufacturing hubs

Page last updated on: