Polyethylene Furanoate (PEF) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

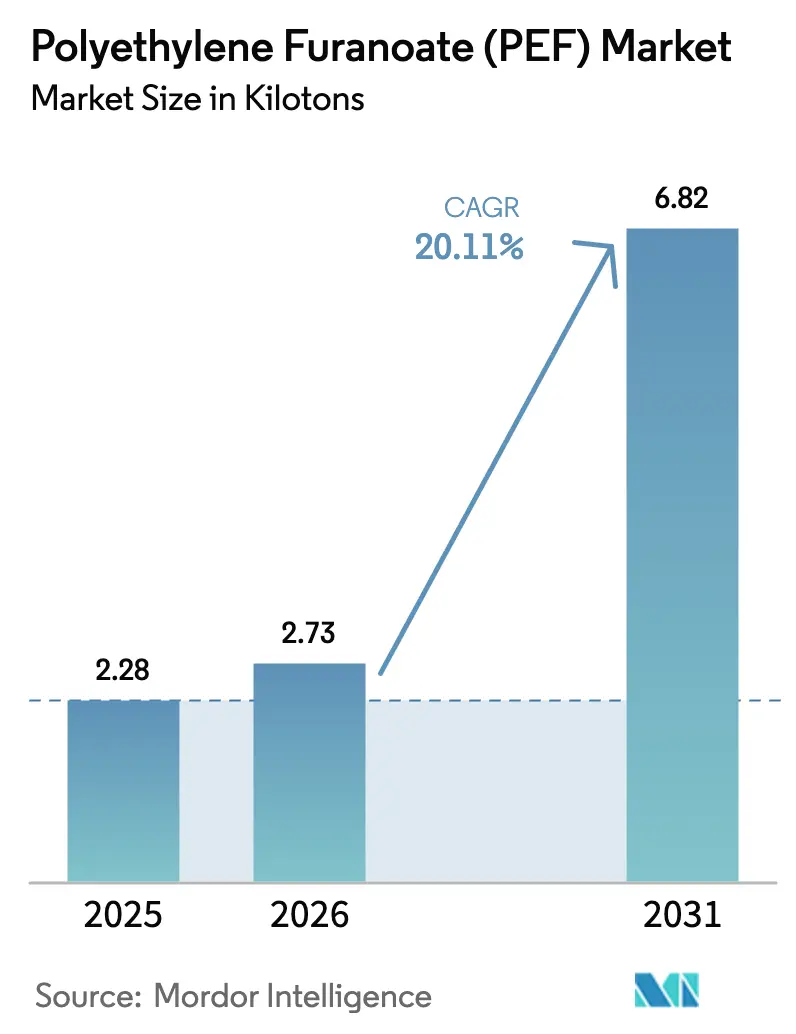

| Market Volume (2026) | 2.73 kilotons |

| Market Volume (2031) | 6.82 kilotons |

| Growth Rate (2026 - 2031) | 20.11% CAGR |

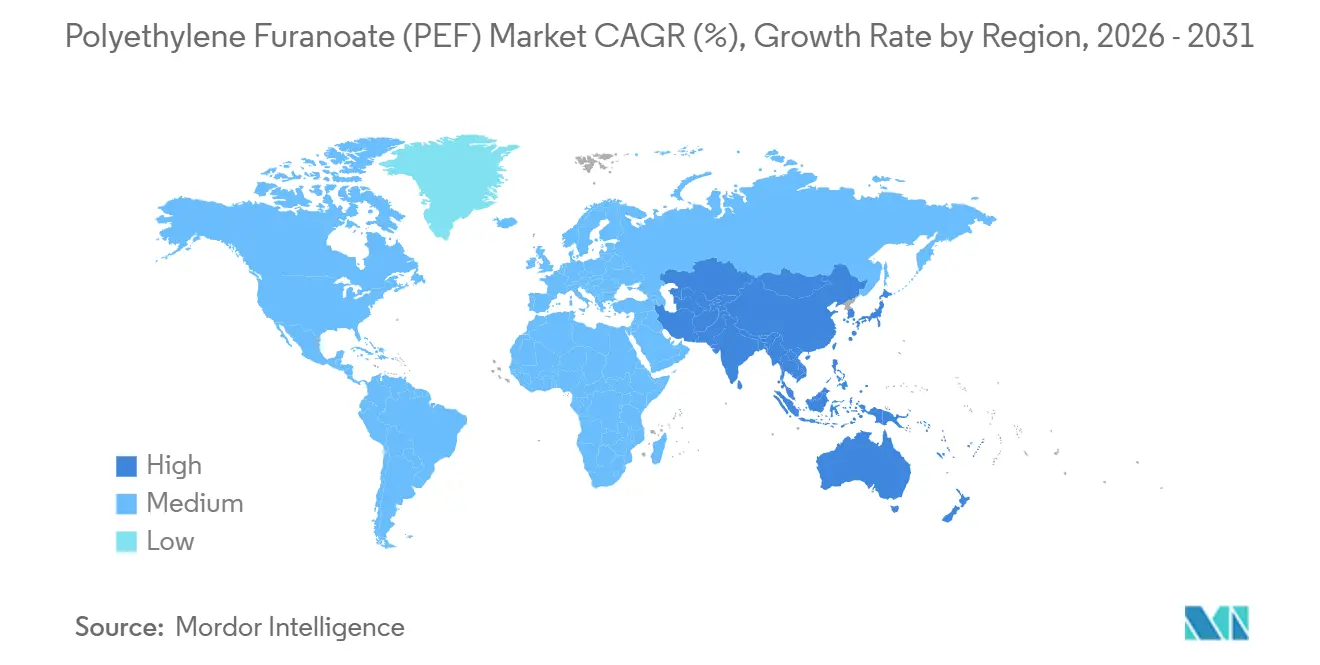

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Polyethylene Furanoate (PEF) Market Analysis by ���ϲ�����

The Polyethylene Furanoate Market size is expected to increase from 2.28 kilotons in 2025 to 2.73 kilotons in 2026 and reach 6.82 kilotons by 2031, growing at a CAGR of 20.11% over 2026-2031. Brand owners are now turning their voluntary pledges into binding resin offtake contracts. This shift not only de-risks capital for early adopters but also speeds up investments at the plant scale. Europe is at the forefront, driven by a significant FDCA unit in Delfzijl. Meanwhile, strong policy signals from China and India are spurring announcements of regional capacities. Early commercialization sees bottles taking the lead, thanks to PEF's enhanced gas-barrier performance. This advantage extends the shelf life of carbonated soft drinks and premium juices. Looking ahead, multilayer e-commerce films are emerging as the next significant opportunity. Producers are now eyeing megascale plants, targeting capacities above 100 kilo tons. This strategy aims to bridge the cost gap with purified terephthalic acid, setting the stage for a deeper penetration into the Polyethylene Furanoate market.

Key Report Takeaways

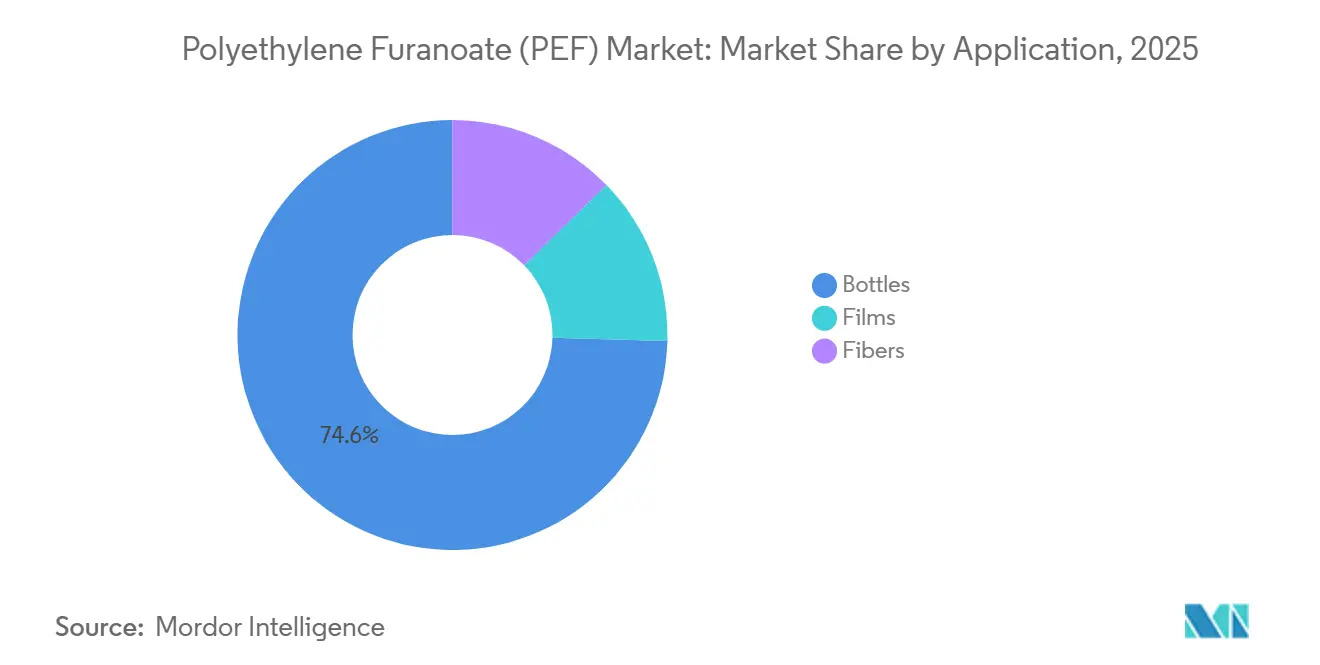

- By application, bottles held 74.57%of the polyethylene furanoate market share in 2025 while registering the fastest 20.56% CAGR through 2031.

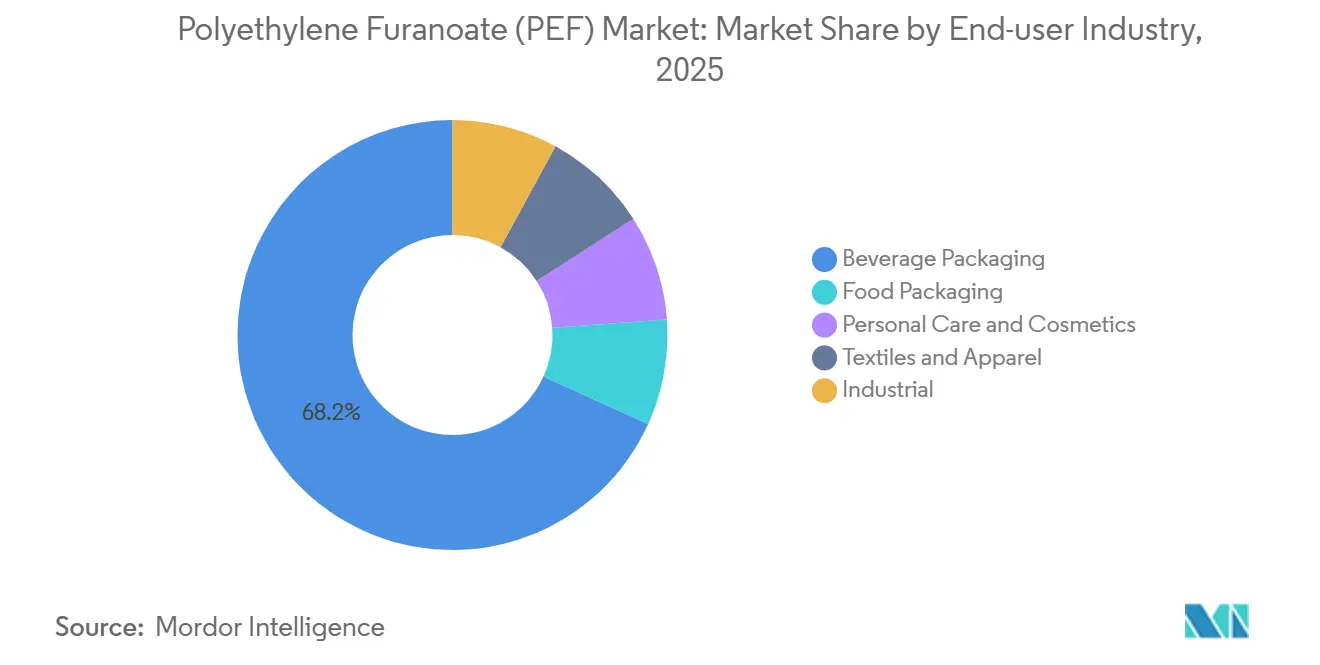

- By end-user industry, beverage packaging commanded 68.20% share of the polyethylene furanoate market size in 2025, whereas personal care and cosmetics are expanding at 20.81% CAGR to 2031.

- By geography, Europe led with 46.89% revenue in 2025; Asia-Pacific is forecast to grow at a 20.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyethylene Furanoate (PEF) Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Sustainable Beverage Packaging | +6.2% | Europe, North America, APAC urban clusters | Medium term (2-4 years) |

| Rising Adoption in Textile and Fiber Applications | +4.8% | APAC core (China, India), Europe | Long term (≥ 4 years) |

| Regulatory Tailwinds for Bio-Based Polymers | +3.9% | Europe (EU Packaging Regulation), North America (BioPreferred), India (BioE3) | Short term (≤ 2 years) |

| Integration into Multilayer E-Commerce Packaging | +2.7% | Global, with early traction in North America and Western Europe | Medium term (2-4 years) |

| Niche Use in Heat-Resistant Electronics Housings | +1.1% | APAC (Japan, South Korea), North America | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Growing Demand for Sustainable Beverage Packaging

Brand owners have transformed their aspirational pledges into multi-year supply agreements, collectively surpassing an annual volume of bottles. This move instills confidence in producers, prompting them to commission commercial plants. PEF boasts a smaller greenhouse gas footprint compared to fossil PET. This advantage aids beverage companies in achieving Science-Based Targets, without relying solely on recycled streams[1]Avantium, “Avantium and Amcor Announce Partnership for PEF Packaging,” avantium.com. Carlsberg's Green Fibre Bottle, launched in July 2025, incorporates a thin PEF barrier layer within molded fiber. This innovation demonstrates PEF's potential to enable hybrid formats, a feat previously restricted by gas transmission challenges. Additionally, EU deposit-return schemes enhance this momentum by monetizing end-of-life performance. Collectively, these dynamics accelerate the adoption of Polyethylene Furanoate in the packaging sector.

Rising Adoption in Textile and Fiber Applications

Polyester holds a dominant share of the global fiber volume. However, biobased polyester remains negligible in comparison. This sets the stage for PEF's (Polyethylene Furanoate) entry as a significant material substitution opportunity. Members of the PEF Textile Community are conducting melt-spinning trials. Their findings indicate that PEF yarns boast a higher glass-transition temperature and modulus than conventional PET. This characteristic enhances fabric stability, especially during high-heat dyeing processes[2]Frontiers in Chemistry, “Polyethylene Furanoate (PEF): A Review of Properties, Synthesis, and Applications,” frontiersin.org . In Germany, a pilot line has successfully validated the production of multifilaments. However, for commercial volumes to materialize, there's a pressing need for consistent resin purity and multi-ton trial batches. As a result, the PEF market in textiles is eyeing a revenue surge, but only post-2028.

Regulatory Tailwinds for Bio-Based Polymers

Finalized in 2024, Europe's Packaging and Packaging Waste Regulation mandates recyclability and sets thresholds for biobased content. This effectively embeds a compliance premium into qualifying packaging. Meanwhile, India's BioE3 framework offers capital subsidies on biopolymer plants and reduces the goods-and-services tax. These incentives position local FDCA production as economically viable, contingent on the maturation of feedstock logistics. In the U.S., while state-level mandates are sparse, federal bids now recognize PEF due to BioPreferred procurement preferences. Together, these global policies bolster business cases, propelling the adoption of Polyethylene Furanoate beyond its initial enthusiasts.

Integration into Multilayer E-Commerce Packaging

In e-commerce, packaging formats that guard against moisture and mechanical damage are increasingly favored. PEF, with a water-vapor transmission rate lower than that of PET, allows for the creation of lighter multilayer mailers that still pass performance audits. Avantium teamed up with Amcor in 2025, focusing on co-extruded films and thermoformed produce trays. Meanwhile, ALPLA is testing PEF as a thin barrier within corrugated mailers. By limiting PEF to a portion of the film's weight, costs are kept in check. Early field trials show promise, indicating an extension in shelf life for leafy produce. This finding is particularly appealing to grocery e-tailers aiming to cut down on waste.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from rPET and PLA Substitutes | -3.4% | Global, especially North America and Europe with mature recycling infrastructure | Short term (≤ 2 years) |

| High Cost and Limited Scale of FDCA Feedstock | -2.8% | Global, acute in regions without fructose or biomass feedstock proximity | Medium term (2-4 years) |

| Collection-Stream Incompatibility for Recycling | -1.6% | North America, Europe (advanced sorting infrastructure), APAC emerging | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Competition from rPET and PLA Substitutes

Recycled PET now satisfies a portion of the demand for polyester fibers, bolstered by a century's worth of established infrastructure. This has led to a steady influx of capital into closed-loop PET, overshadowing investments in novel polymers. PLA, with a more accessible entry cost compared to PEF, boasts food-contact approvals in both the EU and the U.S. As chemical-recycling plants work to reduce rPET's carbon footprint, the life-cycle advantage of PEF diminishes. This is particularly evident in price-sensitive Asian markets, where recycling rates are high.

High Cost and Limited Scale of FDCA Feedstock

Avantium's Delfzijl facility churns out a small amount of FDCA annually. This output pales in comparison to the global PET capacity. As a result, the supply of PEF remains tight, commanding a premium price. When it comes to feedstock costs, fructose and glucose are outpacing paraxylene. Additionally, the use of oxidation reactors further intensifies capital requirements. Origin Materials is exploring a wood-residue approach, touting the potential for negative carbon footprints. However, this method has yet to prove consistent yields on a larger scale. The expansion of the Polyethylene Furanoate market is currently hindered by feedstock economics, and it won't see relief until after 2027, when large-scale plants are expected to achieve mechanical completion.

Segment Analysis

By Application: Bottles Command Scale, Films Await Barrier Validation

Bottles captured 74.57% of the Polyethylene Furanoate market share in 2025 and are projected to grow at a 20.56% CAGR through 2031 as converters leverage PEF’s 31-fold lower CO₂ permeability to safeguard carbonation in premium beverages. Carlsberg’s fiber-based bottle illustrates how PEF layers can enable novel hybrid formats, sparking new demand pockets within the Polyethylene Furanoate market.

Films remain a proof-of-concept niche because conventional blown-film lines require retooling to accommodate PEF’s lower melt temperature. Avantium and Amcor test co-extruded structures for fresh produce pouches where shelf-life extension offsets resin premiums, hinting at future Polyethylene Furanoate market size growth once adhesion challenges are solved. Fibers, though currently marginal, represent a long-tail opportunity. Early yarns listed by Swicofil and trials at DITF suggest PEF’s higher modulus can deliver better drape retention in technical apparel, positioning textiles as a medium-term diversification play for the Polyethylene Furanoate industry.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Personal Care Chases Premium Positioning

Beverage packaging led 2025 demand with 68.20% volume, thanks to high-profile offtake contracts from Carlsberg and AmBev, defining the early revenue core of the Polyethylene Furanoate market. Personal care and cosmetics, however, are forecast to record the fastest 20.81% CAGR, as brands like L’Oréal and Unilever pilot PEF-lined paper bottles that align with luxury sustainability narratives.

Food packaging users evaluate PEF trays for oxygen-sensitive dairy and meat but await EU migration clearances. Textiles and apparel look to PEF for performance footwear uppers where higher modulus improves shape retention, yet mills demand continuous resin supply before switching looms. Industrial uses in electronics housings remain exploratory because PEF’s impact strength lags polycarbonate, although Japanese OEM trials under METI’s Green Transformation banner keep the door open. These diverse trials collectively expand the Polyethylene Furanoate market footprint beyond its beverage stronghold.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Europe accounted for 46.89% of 2025 volume, underwritten by Avantium’s Delfzijl flagship and policy frameworks that penalize fossil polymers, reinforcing the region’s leadership in the Polyethylene Furanoate market. Deposit-return schemes in Germany and the Netherlands internalize end-of-life costs, accelerating brand adoption, while Denmark showcased the first retail launch through Carlsberg’s paper bottle. France and the United Kingdom progress more slowly due to fragmented municipal systems, but premium juice and dairy brands there still run pilot batches. Italy’s biopolymer push offers both competition and partnership opportunities as converters test PEF bottles for oxygen-sensitive mineral water. the

Asia-Pacific is projected to grow at 20.98% and will add the largest incremental Polyethylene Furanoate market size by 2031. China’s pilot FDCA facilities in Zhejiang and India’s BioE3 subsidies create dual hubs of activity, supported by abundant sugarcane residues that lower feedstock costs. Japanese firms such as TOYOBO target PEF fibers for automotive interiors, while South Korean processors explore PEF bottles aimed at EU exports. Regional momentum hinges on local approvals, yet multiple governments endorse bioeconomy roadmaps that explicitly mention furan‐based polyesters, laying regulatory tracks ahead of supply.

North America trails Europe and Asia-Pacific in volume but benefits from Origin Materials’ Sarnia plant and Avantium’s offtake deal with Plastipak for U.S. food-contact applications. FDA approval is the key gate, and stakeholders expect a decision by late 2026. Canada positions itself as a biomass feedstock hub, leveraging forestry residues, and Mexico offers low-cost bottle molding capacity for U.S. brand owners. Latin American adoption rides on AmBev’s rollout in Brazil and Argentina, whereas the Middle East and Africa remain marginal due to fossil-petroleum subsidies and limited waste-management infrastructure that weakens the value proposition of a higher-priced biopolymer.

Competitive Landscape

The polyethylene furanoate (PEF) market is moderately consolidated. Downstream, established PET converters hedge their asset bases by signing multiyear PEF offtake agreements, ensuring they can pivot if adoption accelerates. Textile incumbents and niche distributors explore PEF filaments, although volumes remain a fraction of the bottle segment. Collaborative consortia accelerate scale-up costs and qualification. Such initiatives intensify competition and expand future supply, shaping the trajectory of the Polyethylene Furanoate market over the coming decade.

Polyethylene Furanoate (PEF) Industry Leaders

Avantium

TOYOBO CO., LTD.

ALPLA

Sulzer Ltd

Origin Materials

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Avantium supplied PEF bottles to a Dutch juice producer for Albert Heijn stores, marking first retail commercialization in Europe.

- May 2025: Avantium enhanced Dry Molded Fiber bottles with PEF polymers, extending application reach into fiber-based rigid packaging.

Global Polyethylene Furanoate (PEF) Market Report Scope

Polyethylene furanoate, also named Polyethylene furan-2,5-dicarboxylate, is a polymer that offers a higher gas barrier for oxygen, carbon dioxide, and water vapor. It is, therefore, used as an alternative for packaging applications such as bottles, films, and food trays.

The market is segmented by application, end-user industry, and geography. By application, the market is segmented into bottles, films, and fibers. By end-user industry, the market is segmented into beverage packaging, food packaging, personal care and cosmetics, textiles and apparel, and industrial (electronics, automotive). The report also covers the market size and forecasts for the market in 15 countries across the major regions. For each segment, the market sizing and forecasts have been done based on volume (Tons).

| Bottles |

| Films |

| Fibers |

| Beverage Packaging |

| Food Packaging |

| Personal Care and Cosmetics |

| Textiles and Apparel |

| Industrial (Electronics, Automotive) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Bottles | |

| Films | ||

| Fibers | ||

| By End-user Industry | Beverage Packaging | |

| Food Packaging | ||

| Personal Care and Cosmetics | ||

| Textiles and Apparel | ||

| Industrial (Electronics, Automotive) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

Which application absorbs the largest share of polyethylene furanoate today?

Bottles captured 74.57% of the 2025 volume by leveraging PEF’s superior gas-barrier properties that extend beverage shelf life.

Why is Asia-Pacific the fastest-growing region for polyethylene furanoate?

Policy support in China and India, combined with plentiful biomass feedstock, drives a 20.98% regional CAGR through 2031.

Which end-user segment is poised for the highest growth rate?

Personal care and cosmetics is forecast to expand at a 20.81% CAGR because consumers pay a premium for credible sustainability narratives.

What is the current global demand for the polyethylene furanoate market and its expected growth by 2031?

Global consumption is 2.73 kilotons in 2026 and is projected to reach 6.82 kilotons by 2031, reflecting a 20.11% CAGR

Page last updated on: