Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

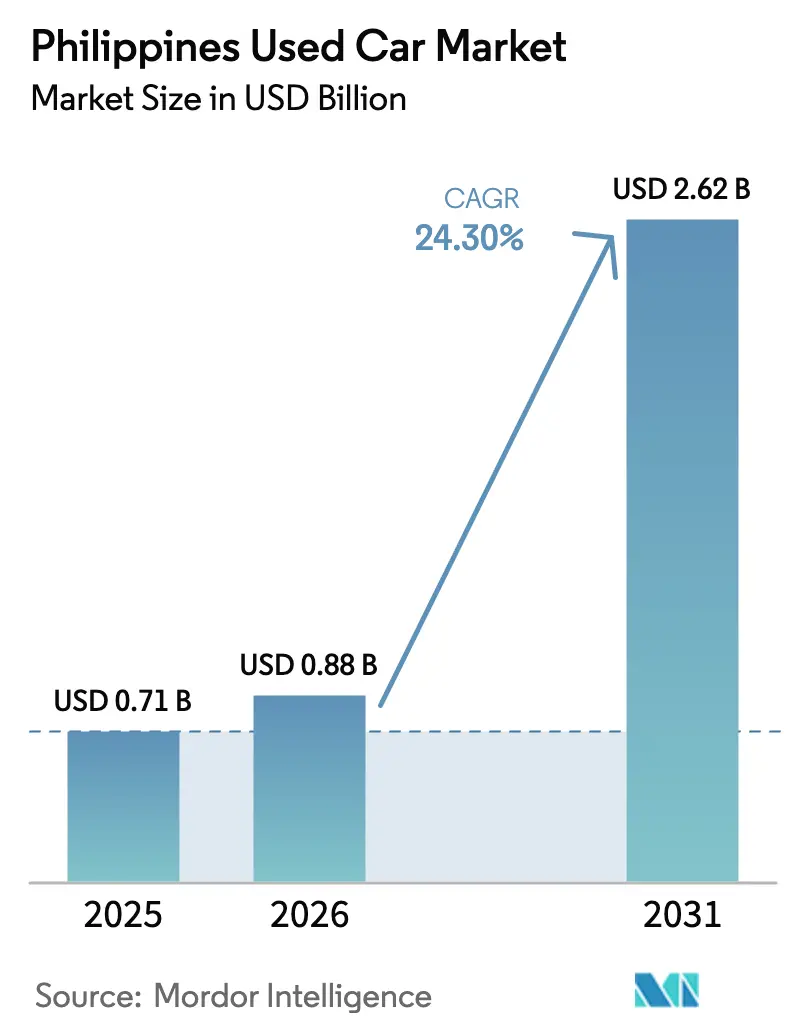

| Base Year Market Size (2025) | USD 5.90 Billion |

| Market Size (2026) | USD 6.25 Billion |

| Market Size (2031) | USD 8.39 Billion |

| Growth Rate (2026 - 2031) | 6.06% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Philippines Used Car Market Analysis by ���ϲ�����

The Philippines' used car market size is projected to expand from USD 5.90 billion in 2025 and USD 6.25 billion in 2026 to USD 8.39 billion by 2031, registering a 6.06% CAGR between 2026 and 2031. Organized dealership networks are widening their certified pre-owned footprints, using tighter inspection protocols and captive financing to convert trade-ins into higher-margin stock. Digital platforms are compressing search and documentation cycles, yet still funnel the majority of inquiries into physical showrooms because buyers insist on test drives and under-chassis inspections. SUVs and MPVs dominate demand as families prioritize flood resilience and versatility on provincial roads, while hybrid powertrains are gaining traction under the CREATE MORE excise tax exemptions. Remittance inflows from Overseas Filipino Workers (OFWs) continue to bankroll purchases in secondary cities where personal mobility remains aspirational.

Key Report Takeaways

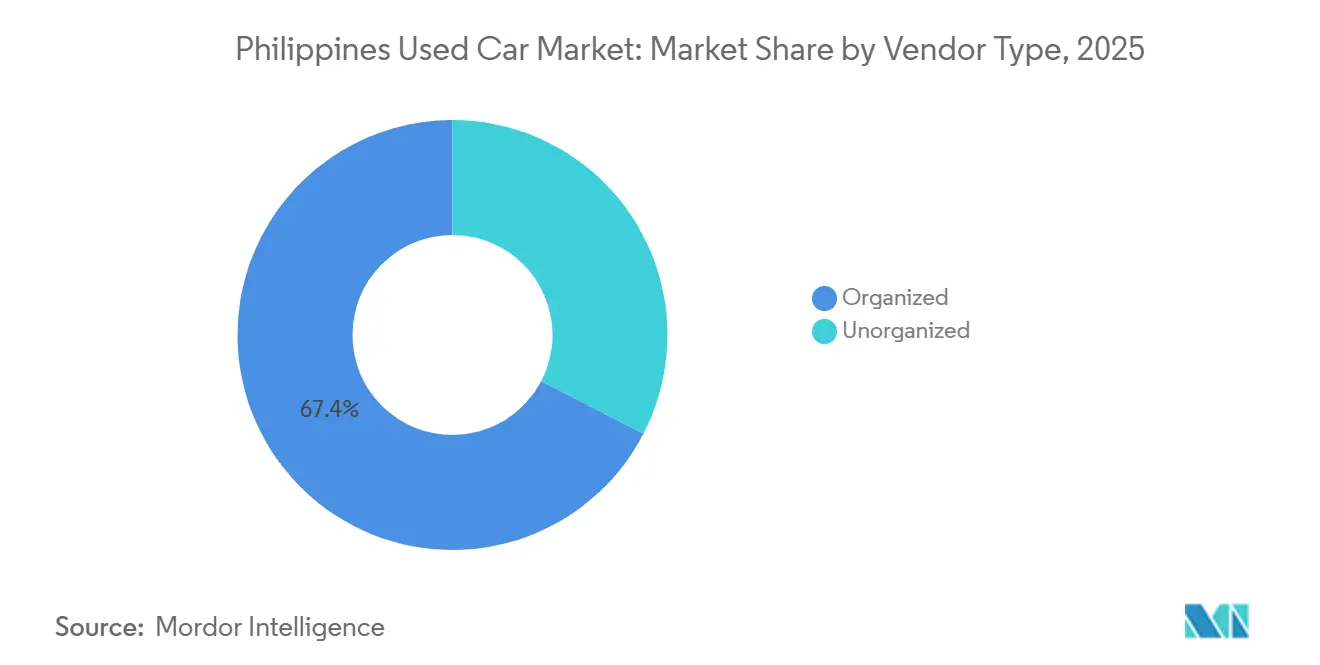

- By vendor type, organized dealerships secured 67.40% of 2025 revenue and are advancing at a 7.13% CAGR through 2031.

- By vehicle type, sport utility vehicles and multi-purpose vehicles led with 49.75% of 2025 volume and are growing at an 8.21% CAGR through 2031.

- By fuel type, petrol retained the largest 63.80% share in 2025, yet hybrid-electric variants are the fastest mover at an 11.32% CAGR through 2031.

- By sales channel, offline lots dominated with 81.60% of 2025 transactions, but online platforms scale at a 10.87% CAGR, the quickest among all channels.

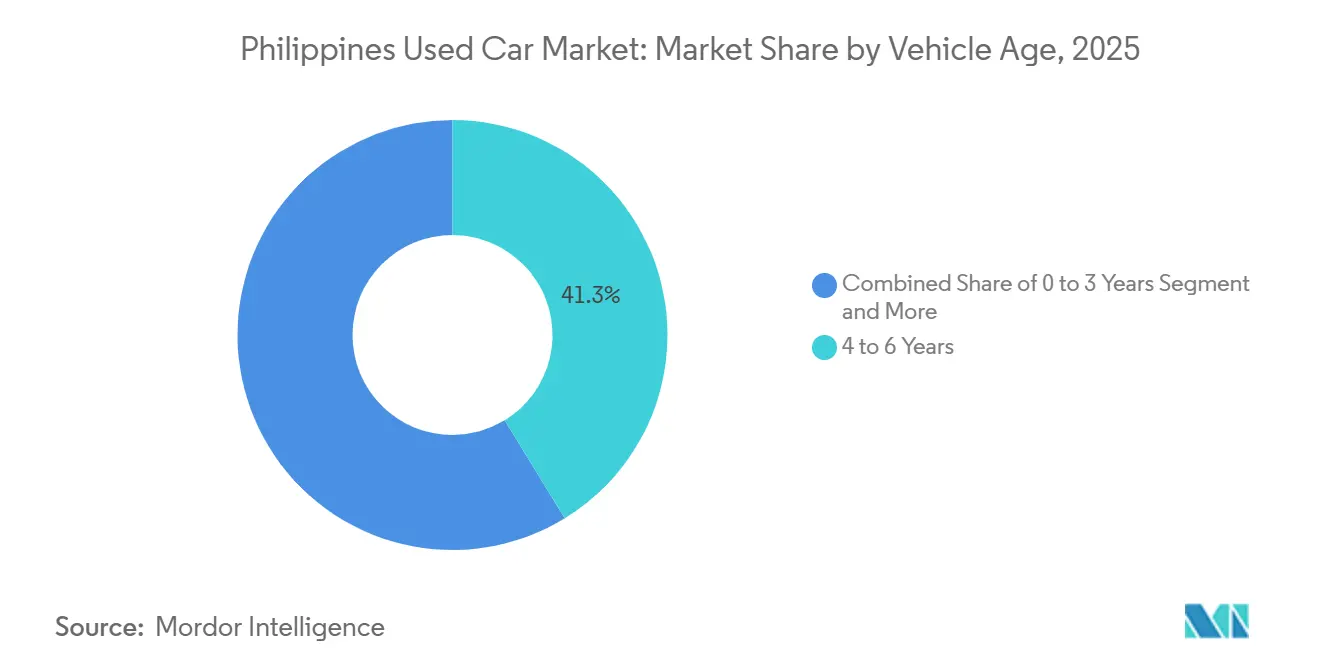

- By vehicle age, 4 to 6-year models controlled 41.25% of 2025 sales, while nearly-new 0 to 3-year units registered the highest 9.28% CAGR.

- By price band, the PHP 500 k to 1 million tier held a 46.20% share in 2025, whereas the above-PHP 1 million tier is the fastest-growing, with a 7.84% CAGR.

- By geography, Luzon accounted for 69.40% of the 2025 value, yet Visayas is the fastest-growing region, with a 7.14% CAGR through 2031, as Cebu and Iloilo attract remittance-funded purchases.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Philippines Used Car Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Online Classifieds and E-commerce Digitalize Used-Car Transactions | +2.8% | National, with Early Gains in Metro Manila, Cebu, Davao | Short term (≤ 2 years) |

| Metro Manila's Middle Class Fuels Affordable Mobility Demand | +2.5% | Metro Manila, Expanding to Surrounding Provinces | Medium term (2-4 years) |

| OEMs' Trade-in and Financing Programs Shorten Ownership Cycles | +2.0% | Urban Centers Across Luzon, Visayas, Mindanao | Medium term (2-4 years) |

| OFW Remittances Drive Purchases in Provincial Growth Centers | +1.7% | Provincial Cities and Rural Areas Nationwide | Long term (≥ 4 years) |

| Relaxed Import Quotas in Subic and Freeport Zones Boost Supply | +1.0% | Luzon, with Spillover to Visayas | Short term (≤ 2 years) |

| Rising Fuel Costs Shift Demand to Efficient Used Vehicles | +0.8% | National, Most Renounced in Urban Commuting Areas | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Understand The Key Trends Shaping This Market

Download PDF

Digitalization of Used-Car Transactions via Online Classifieds and E-commerce

In the Philippines, the used car market is undergoing a digital transformation, reshaping how transactions occur. A significant portion of leads now comes from online sources, with social media platforms, especially Facebook, leading the charge. This digital pivot has shortened the traditional buying cycle, enabling consumers to use digital tools to compare options, verify vehicle histories, and arrange financing, all before setting foot in a dealership. Moreover, digital platforms have evolved beyond just listing services; they now facilitate end-to-end transactions. This includes processing online payments, handling digital documentation, and even conducting virtual inspections. While this digital shift is most evident in Metro Manila, where internet penetration is high, it is swiftly spreading to provincial cities, driven by the rising adoption of smartphones.

Middle-Class Expansion in Metro Manila Boosting Affordable Mobility Demand

The expanding middle class in Metro Manila is creating unprecedented demand for affordable mobility solutions, with the used car market serving as the primary entry point for first-time vehicle owners. This demographic shift is characterized by young professionals aged 25-35 who prioritize value retention and practical features over new-car prestige. The economic pragmatism driving this trend is evident in the preference for vehicles in the PHP 500 k to 1 million range, which offers the optimal balance between quality and affordability for middle-income households earning PHP 50,000 to 100,000 monthly. The impact extends beyond simple ownership to influence vehicle selection criteria, with fuel efficiency and maintenance costs becoming primary considerations over brand prestige[1]"BTI 2024", Philippines Country Report, bti-project.org..

OEM Trade-in and Financing Programs Shortening Ownership Cycles

Original equipment manufacturers (OEMs) are strategically accelerating vehicle ownership cycles through innovative trade-in programs and flexible financing options, creating a steady stream of quality used inventory. Toyota Motor Philippines leads this transformation with its Certified Pre-Owned program, which has reduced average ownership periods from 7-8 years to 4-5 years by offering guaranteed buyback values and seamless upgrade paths to new models. This approach simultaneously addresses affordability barriers for new vehicle purchases while ensuring a controlled supply of certified pre-owned vehicles with documented maintenance histories[2]"Auto Loan", BDO Unibank, Inc., www.bdo.com.ph..

OFW Remittance-Driven Purchases in Provincial Growth Centers

In provincial growth centers, remittances from Overseas Filipino Workers (OFWs) are increasingly driving used car purchases, shaping unique market dynamics away from major urban hubs. In the first quarter of 2024, a survey revealed that 96.6% of OFW households primarily used their remittances for food. Meanwhile, 58.3% allocated funds for medical expenses. As these basic needs are addressed, acquiring vehicles is becoming a heightened priority. This surge in demand, fueled by remittances, is especially pronounced in secondary cities and rural locales. Here, with limited public transportation infrastructure, owning a private vehicle is not just a luxury—it's a practical necessity.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Vehicle History Transparency Erodes Trust | -1.8% | National, Most Acute in Provincial Areas | Medium term (2-4 years) |

| Flood-Damage Risks Post-Typhoon Lower Residual Values | -1.3% | Coastal Areas, Low-lying Regions Nationwide | Short term (≤ 2 years) |

| Ride-Hailing and Micro-Mobility Compete in Urban Hubs | -0.8% | Metro Manila, Cebu, Davao | Long term (≥ 4 years) |

| High Interest Rates Restrict Consumer Financing | -0.6% | National, Most Impact on Middle-income Segments | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Limited Vehicle-History Transparency Undermining Buyer Trust

The persistent challenge of limited vehicle history transparency continues to undermine consumer confidence in the Philippines used car market, particularly in the dominant unorganized segment, where documentation practices remain inconsistent. This information asymmetry creates significant friction in the purchasing process, with buyers forced to rely on superficial inspections or third-party mechanics rather than comprehensive vehicle history reports that are standard in more developed markets. The trust deficit is most acute in provincial areas where access to vehicle verification services is limited, creating geographic disparities in market efficiency and pricing.

Competition from Ride-hailing and Micro-mobility in Urban Hubs

The proliferation of ride-hailing services and micro-mobility options in major urban centers is creating structural competition for used car ownership, particularly among younger consumers in dense metropolitan areas. Additionally, parking fees above PHP 5,000 per month and severe traffic congestion persuade many city dwellers to rely on variable-cost ride-hailing or short-distance e-scooters. The restraint is most acute among younger consumers who value flexibility over ownership. Future urban transport policies will determine whether this headwind eases or widens.

Segment Analysis

By Vendor Type: Certified Programs Anchor Organized Growth

Organized dealers own 67.40% of the Philippines' used-car market share in 2025 and are growing at a 7.13% CAGR through 2031, as OEM inspection protocols and tiered warranties de-risk purchases for consumers. Banks favor certified inventory with lower interest spreads, and digital platforms route most high-intent leads to branded showrooms. Unorganized roadside sellers still dominate remote towns, but see margin pressure as younger buyers demand documentation and standardized pricing.

Certified stock also improves residuals; 0-to-3-year units maintain 80% of original value versus 65% for uncertified cars. The Philippines' used car market share for organized dealers is therefore poised to widen further as rural traders formalize operations or partner with aggregators to access captive-finance pools.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Vehicle Type: SUVs Dominate on Versatility and Flood Resilience

Sport utility vehicles and multi-purpose vehicles account for 49.75% of the 2025 volume and will expand at an 8.21% CAGR through 2031, outstripping hatchbacks and sedans. Ground clearance, seven-seat layouts, and diesel options make models such as the Toyota Fortuner and Mitsubishi Montero Sport perennial favorites during typhoon season. Cross-over SUVs with hybrid powertrains are entering the Philippines used-car market at competitive prices through 3-year lease returns, keeping demand elevated even as fuel costs rise.

Sedans and hatchbacks still serve budget urban commuters, but their combined share slides annually as families upsize. Vans and pickups maintain niche roles in logistics and agriculture, with steady demand in Mindanao’s farm corridors.

By Fuel Type: Petrol Leads, Hybrids Surge on Policy Tailwinds

Petrol retained a 63.80% share in 2025, yet hybrid and electric units are charting an 11.32% CAGR following CREATE MORE excise-tax exemptions. Charging stations exceeded 1,000 by mid-2025, concentrated in Metro Manila, Cebu, and Davao, easing range anxiety for early adopters. Diesel remains vital for pickups and commercial vans but faces Euro-5 restrictions in urban cores.

Hybrids filter into secondary listings two to four years after first sale, driving down acquisition costs enough to tempt middle-class buyers focused on operating expenses. Accordingly, the Philippines' used-car market for electrified drivetrains is set to expand steadily over the forecast period.

By Sales Channel: Offline Dominates, Online Scales Rapidly

Offline lots anchored 81.60% of 2025 deals because tactile validation remains non-negotiable, especially for big-ticket SUVs. Even so, online platforms post a 10.87% CAGR as mobile-first shoppers shortlist vehicles digitally before scheduling showroom visits. AutoDeal’s valuation engine can now issue loan pre-approvals within 48 hours, aligning the convenience gap with fast-fashion e-commerce expectations.

Platforms are layering on 360-degree tours, AI chat, and blockchain VIN checks to build trust, yet omnichannel models will remain dominant. The Philippines' used car industry is evolving toward “click-to-reserve, inspect-to-buy,” merging digital reach with physical reassurance.

By Vehicle Age: Nearly-New Units Gain on Warranty Appeal

Cars aged 0 to 3 years are growing at a 9.28% CAGR through 2031, lifted by corporate fleet turnovers and generous OEM warranty transfers. These nearly-new units command just a 20% depreciation penalty versus new prices, attracting value-conscious professionals. 4 to 6-year-old models still hold a 41.25% share in 2025, but face stiffer competition from fresher, better-equipped entries.

Older than 10-year vehicles exit Metro Manila under emission and ride-hailing fleet rules, migrating to provincial markets where upfront price trumps reliability. The Philippines' used car market share for nearly-new stock is thus set for sustained expansion.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Price Band: Premium Tier Expands on OFW and Expatriate Demand

The PHP 500 k to 1 million bracket captured 46.20% of 2025 transactions, but units costing above PHP 1 million now post a 7.84% CAGR as returning OFWs and expats snap up five-year-old BMW and Lexus models at half their original sticker price. Dealers respond with white-glove showrooms, three-year warranties, and concierge after-sales support, nudging average selling prices higher.

Below-PHP 500 k cars remain entry points for rural buyers but suffer from limited financing and low-quality inventory. Fragmentation by price, therefore, intensifies, compelling lenders and insurers to create risk-based products for each tier.

Geography Analysis

Luzon commanded 69.40% of 2025 revenue, reflecting dense dealership grids, expressway infrastructure, and higher disposable incomes. Metro Manila alone accounted for a significant share of the Philippines' used-car market, yet saturation and rising ride-hailing adoption curb incremental growth. Provincial Luzon, particularly Calabarzon and Central Luzon, offsets this slowdown as new expressways catalyze suburban housing and car demand.

Visayas is the fastest-growing region at a 7.14% CAGR, anchored by Cebu’s diversified economy and Iloilo’s BPO boom. Improved port capacity and roll-on-roll-off ferry routes cut logistics costs, encouraging organized dealers to stock wider inventories and roll out certified programs. Buyers in Visayas emphasize after-sales coverage, making the region fertile ground for OEM-branded warranties.

Mindanao lags in absolute volume but shows catch-up momentum in Davao, Cagayan de Oro, and General Santos. Demand skews toward pickups and SUVs suited for agriculture and mining roads. While financing penetration is improving, it still trails the national average, limiting market depth. Political stability initiatives and infrastructure projects, however, could narrow the gap by late-decade.

Competitive Landscape

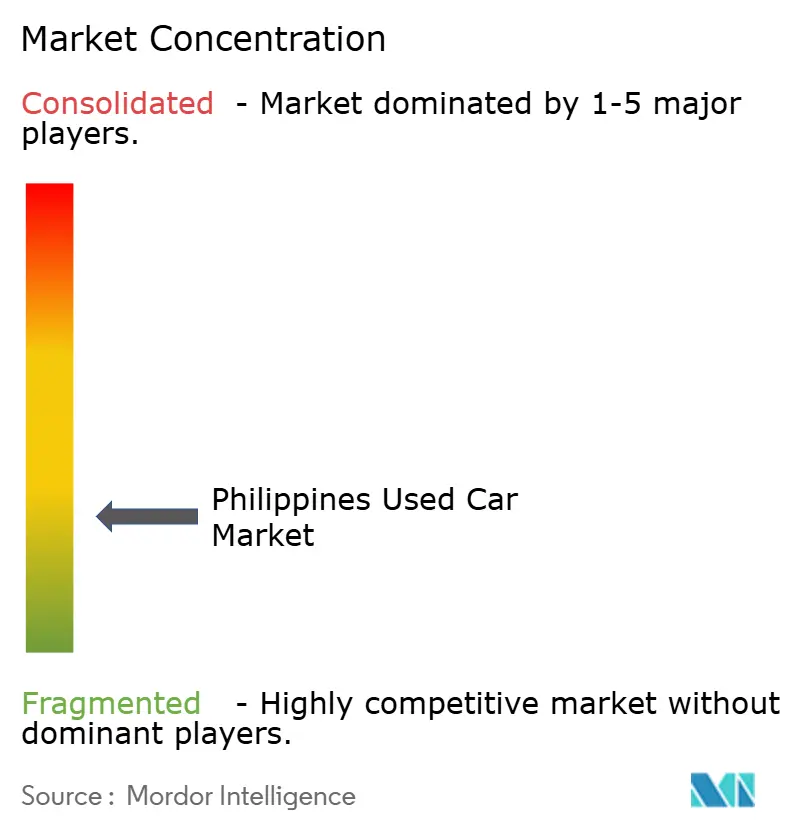

In the Philippines, the used car market is moderately concentrated. The top OEM-affiliated certified programs, along with leading e-commerce platforms, collectively account for a significant portion of the total sales value. Leading the charge is Toyota Motor Philippines, which boasts a widespread T-Sure network and offers competitive financing options for relatively newer units. Meanwhile, Hyundai HARI is trialing blockchain VIN ledgers to bolster buyer confidence, and Mitsubishi is leveraging its Subic reconditioning hub to capitalize on duty-free imports and supply inland showrooms [3]Mitsubishi Motors Philippines, “Diamond CPO Subic Facility,” mitsubishi-motors.com.ph.

In the digital arena, aggregators are racing against time and data. AutoDeal's AI engine offers price guidance almost instantly. On the other hand, Carmudi, backed by substantial funding, is embedding instant insurance quotes from Manulife. Carousell is venturing into peer-to-peer lending, enticing unbanked millennials with crowdsourced down payments that promise attractive returns.

Luxury niche players like PGA Cars Premium Used are making their mark by providing comprehensive vehicle checks and extended service packages for German brands. However, smaller provincial lots face the threat of marginalization unless they elevate their inventory vetting processes and forge partnerships with fintech lenders.

Philippines Used Car Industry Leaders

-

Carmudi

-

Carousell

-

Philkotse.com

-

Carmax

-

LausGroup

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Security Bank partnered with AutoDeal to enhance car financing options for Filipinos, integrating AutoDeal's extensive car listings with Security Bank's flexible loan options to create a seamless digital experience for car buyers amid significant growth in the auto loan market, with an 18.8% year-on-year increase in vehicle loans as of March 2025.

- July 2025: Two new Omoda & Jaecoo dealerships are opened, aiming to enhance the brand's presence in Luzon and Visayas. After their official launch in February 2025, Omoda & Jaecoo Motor Philippines Inc. is focused on building a strong nationwide presence through a strategic expansion plan.

Philippines Used Car Market Report Scope

Philippines used car market report is segmented by vendor type (organized and unorganized), vehicle type (hatchbacks, sedans, sport utility vehicles & multi-purpose vehicles, pickup trucks, and vans), fuel type (petrol, diesel, hybrid and electric, and others (CNG, LPG)), sales channel (online and offline), vehicle age (0 to 3 years, 4 to 6 years, 7 to 10 years, more than 10 years), price band (less than PHP 500 k, PHP 500 k to 1 million, and more than 1 million), and geography (Luzon, Visayas, and Mindanao). The market forecasts are provided in terms of value (USD) and volume (units).

By Vendor Type

| Organized |

| Unorganized |

By Vehicle Type

| Hatchbacks |

| Sedans |

| Sport Utility Vehicles and Multi-purpose Vehicles |

| Pickup Trucks |

| Vans |

By Fuel Type

| Petrol |

| Diesel |

| Hybrid and Electric |

| Others (CNG, LPG) |

By Sales Channel

| Online |

| Offline |

By Vehicle Age

| 0 to 3 Years |

| 4 to 6 Years |

| 7 to 10 Years |

| More than 10 Years |

By Price Band (PHP)

| Less than 500 k |

| 500 k to 1 million |

| More than 1 million |

By Geography

| Luzon |

| Visayas |

| Mindanao |

| By Vendor Type | Organized |

| Unorganized | |

| By Vehicle Type | Hatchbacks |

| Sedans | |

| Sport Utility Vehicles and Multi-purpose Vehicles | |

| Pickup Trucks | |

| Vans | |

| By Fuel Type | Petrol |

| Diesel | |

| Hybrid and Electric | |

| Others (CNG, LPG) | |

| By Sales Channel | Online |

| Offline | |

| By Vehicle Age | 0 to 3 Years |

| 4 to 6 Years | |

| 7 to 10 Years | |

| More than 10 Years | |

| By Price Band (PHP) | Less than 500 k |

| 500 k to 1 million | |

| More than 1 million | |

| By Geography | Luzon |

| Visayas | |

| Mindanao |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the Philippines used car market today and how fast is it growing?

It stood at USD 6.25 billion in 2026 and is set to reach USD 8.39 billion by 2031, reflecting a 6.06% CAGR.

Which sales channel is expanding quickest?

Online marketplaces post a 10.87% CAGR, although offline showrooms still close most deals.

What vehicle types dominate demand?

Sport utility vehicles and multi-purpose vehicles hold nearly half the market at 49.75% and post the strongest 8.21% CAGR because of flood resilience and family capacity.

How are hybrids and EVs performing?

They start from a small base but climb at an 11.32% CAGR, buoyed by CREATE MORE excise-tax exemptions and new charging stations.