Pet Wearable Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.56 Billion |

| Market Size (2031) | USD 7.23 Billion |

| Growth Rate (2026 - 2031) | 15.21% CAGR |

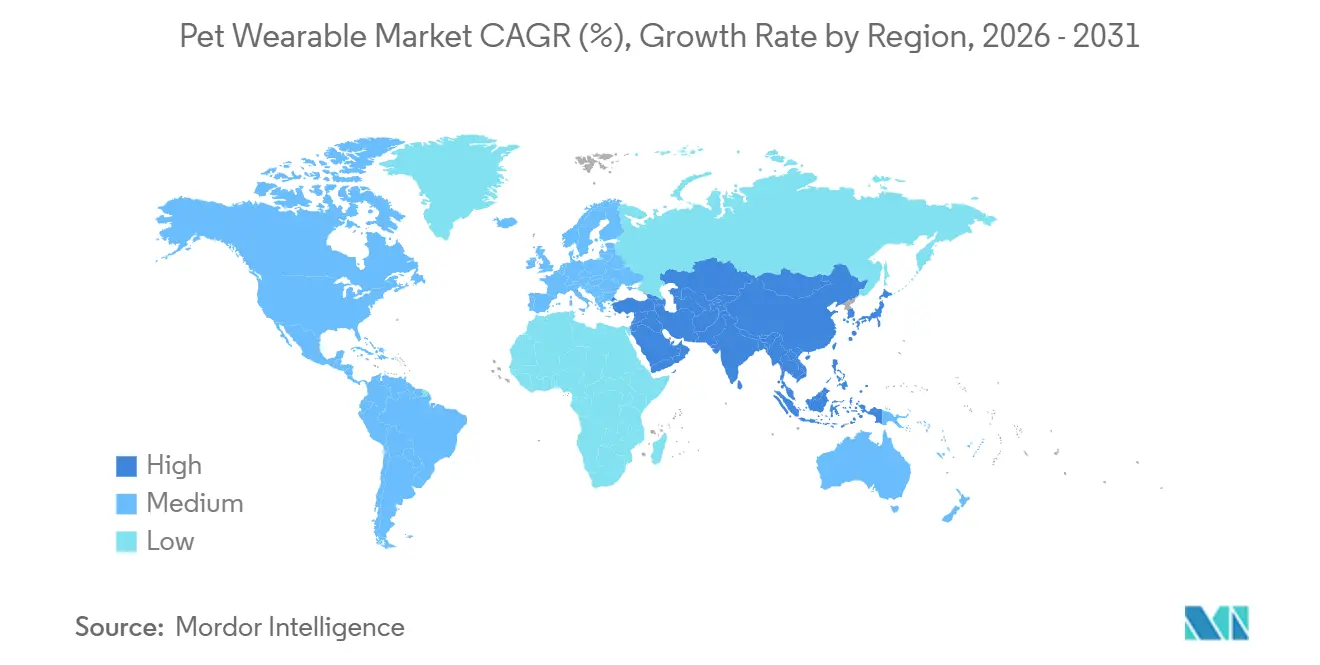

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

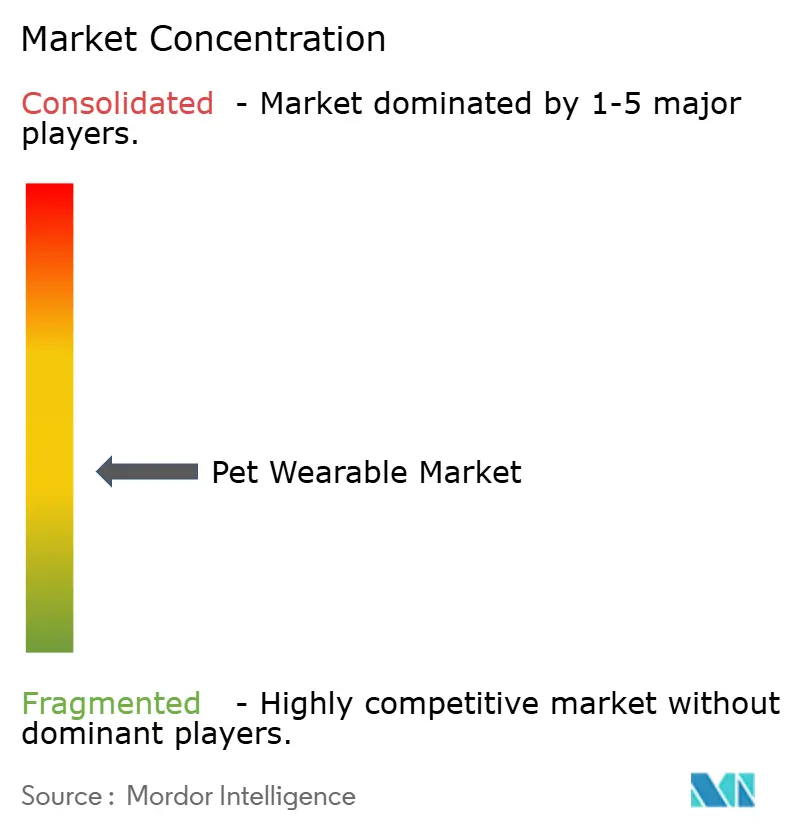

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Pet Wearable Market Analysis by ���ϲ�����

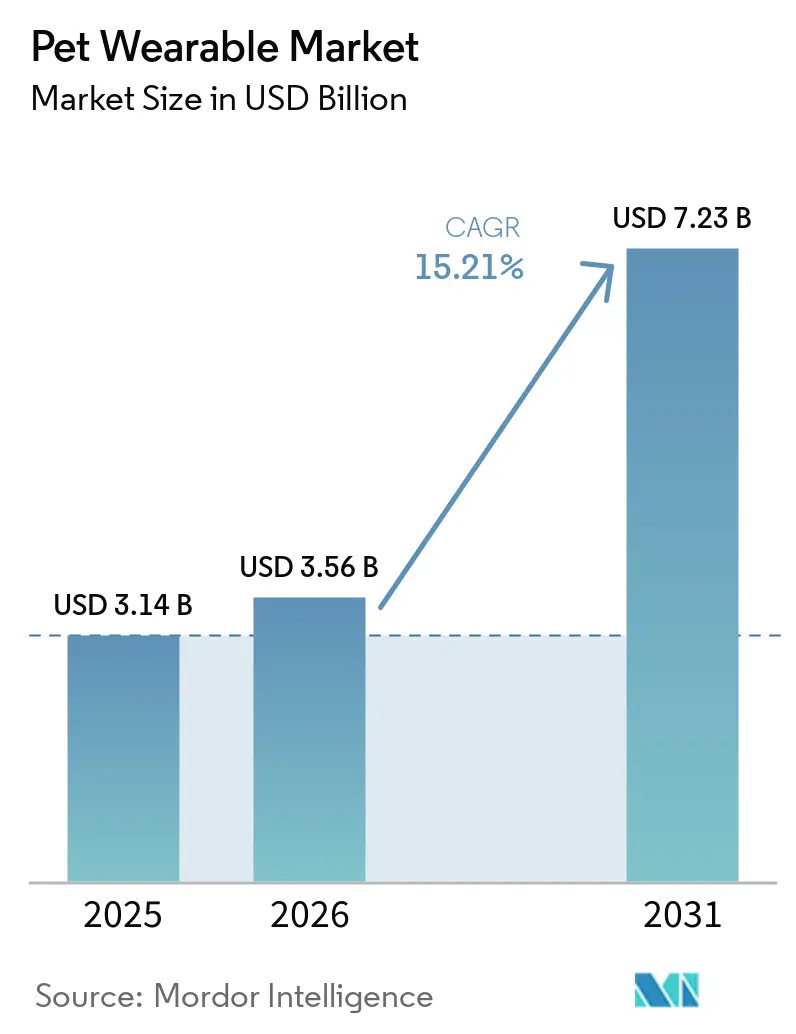

The Pet Wearable Market size is projected to expand from USD 3.14 billion in 2025 and USD 3.56 billion in 2026 to USD 7.23 billion by 2031, registering a CAGR of 15.21% between 2026 to 2031.

The pet wearable market is benefiting from a lasting shift in pet ownership, where Millennials and Gen Z treat pet care as part of daily lifestyle choices, and that is widening the base for connected monitoring devices as pet ownership rises further in the United States. Owners are also protecting pet spending better than many other household categories, which supports the pet wearable market because devices tied to safety and health are now closer to essential pet care than discretionary accessories. The pet wearable market is also moving away from simple hardware competition, as value is shifting toward software ecosystems, subscription services, and clinical data layers that can support remote care, chronic disease monitoring, and insurance-linked programs. At the same time, premium pricing, compliance burdens around location and biometric data, and the spread of inaccurate low-cost devices still limit faster adoption in more price-sensitive households and markets. Even with those constraints, the pet wearable market continues to show strong expansion because the largest demand pools now sit at the intersection of pet safety, preventive monitoring, and continuous owner engagement.

Key Report Takeaways

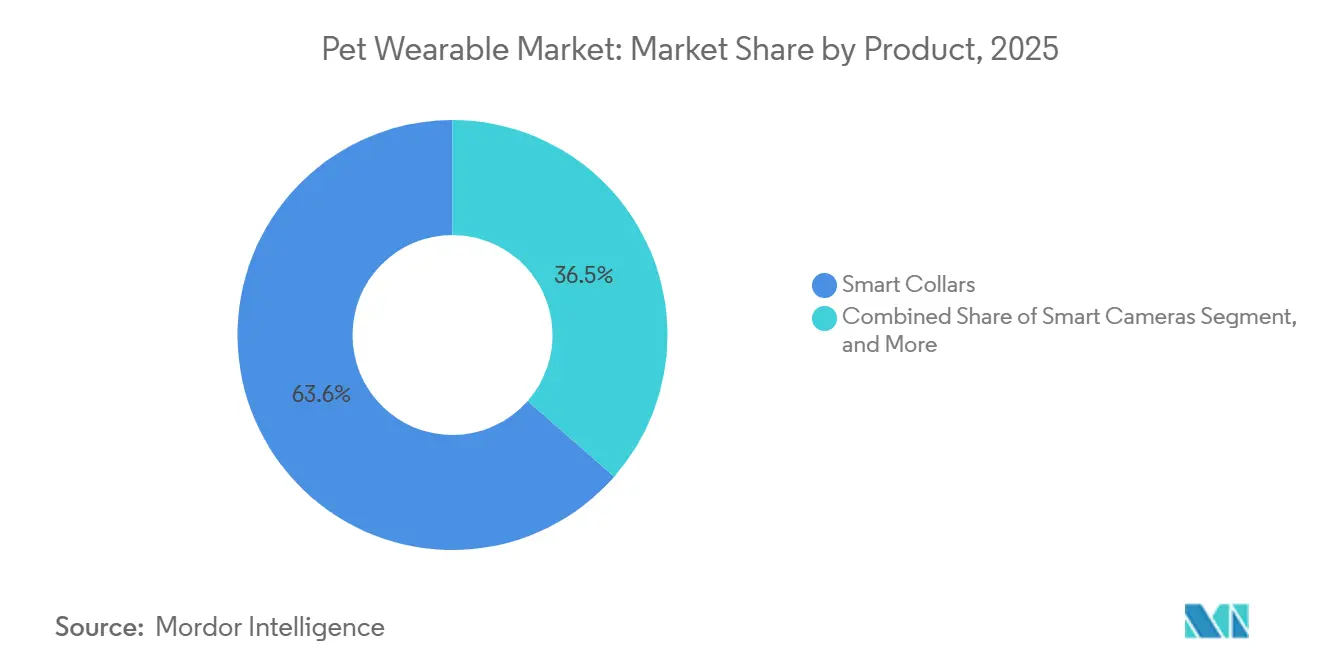

- By product type, smart collars led with 63.55% revenue share in 2025, while smart cameras are forecast to expand at a 15.89% CAGR through 2031.

- By connectivity mode, stand-alone GPS held 44.87% share in 2025, while hybrid multi-connectivity recorded the highest projected CAGR at 16.18% through 2031.

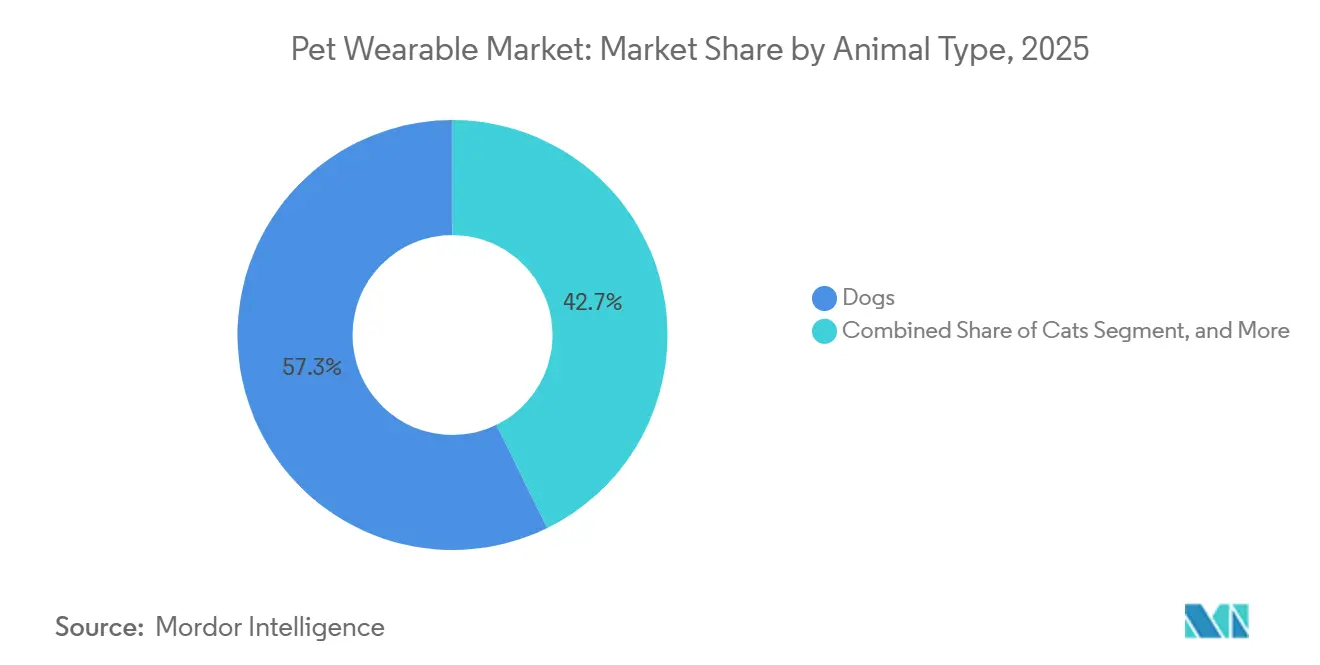

- By animal type, dogs accounted for 57.27% share in 2025 and also posted the fastest projected CAGR at 15.45% through 2031.

- By application, identification and tracking captured 50.23% share of the market in 2025, while medical diagnosis and treatment are advancing at a 16.83% CAGR through 2031.

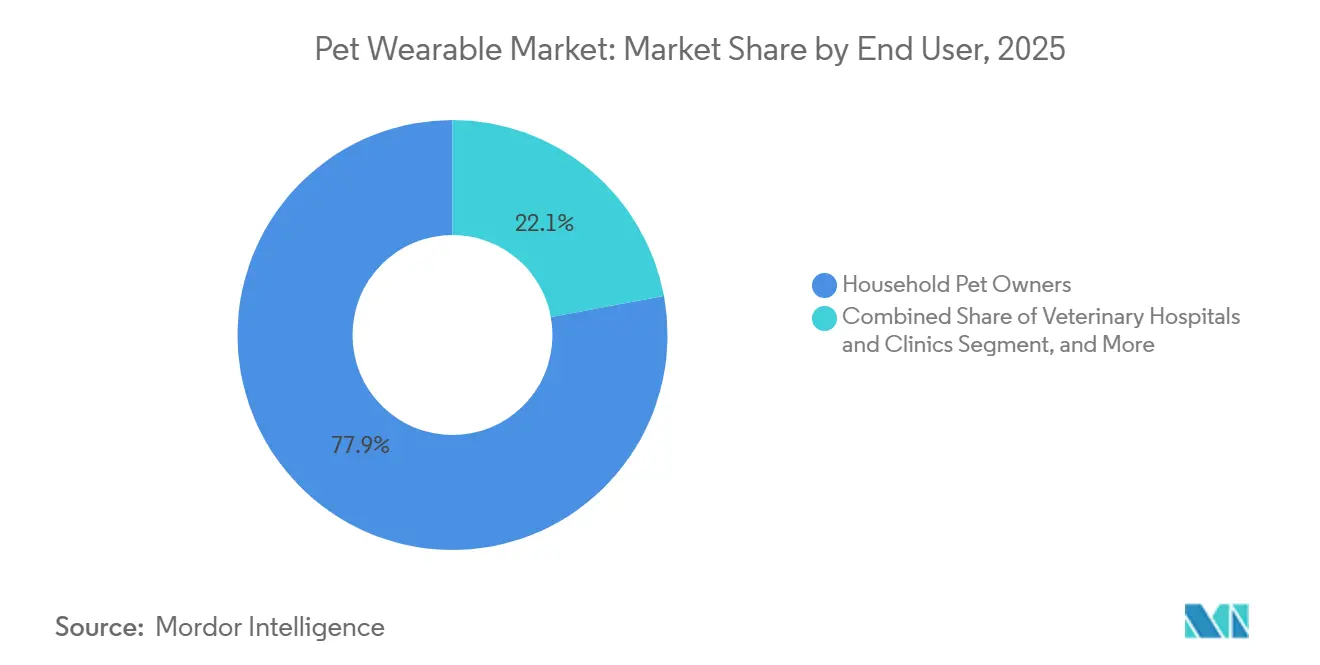

- By end user, household pet owners held 77.90% share in 2025, while veterinary hospitals and clinics are forecast to grow at a 17.28% CAGR through 2031.

- By geography, North America represented 41.88% share in 2025, while Asia-Pacific is projected to record the fastest CAGR at 17.62% through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pet Wearable Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Pet-Care Expenditure Fueling Market Growth | +3.5% | Global, with highest concentration in North America and Western Europe | Short term (≤ 2 years) |

| Preventive Health Monitoring and Chronic-Disease Screening | +2.8% | Global, early gains concentrated in North America, Germany, Japan | Medium term (2-4 years) |

| GPS Safety, Geofencing, and Lost-Pet Recovery Demand | +2.5% | Global, high relevance in North America, APAC urban centers, and South America | Short term (≤ 2 years) |

| IoT, AI, and Sensor Miniaturization | +2.3% | Global, manufacturing gains strongest in APAC, adoption gains in North America and EU | Long term (≥ 4 years) |

| Tele-Veterinary and Pet-Insurance Data Integration | +1.8% | North America and EU, with early spill-over to Australia and South Korea | Medium term (2-4 years) |

| Cat-Specific and Small-Pet Wearable Miniaturization | +1.2% | Global, fastest adoption in North America, Japan, and France | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Increasing Pet-Care Expenditure Fueling Market Growth

Elevated pet-care spending remains the broadest demand driver for the pet wearable market. The American Pet Products Association confirmed that the U.S. pet industry reached USD 158 billion in 2025 and is expected to move to USD 165 billion in 2026, which keeps the spending base large enough to support newer connected products.[1]American Pet Products Association, “U.S. Pet Industry Reaches USD 158 Billion in 2025, Poised for Continued Growth in 2026,” American Pet Products Association, americanpetproducts.org The more important shift is where that spending is going, because owners are placing more value on health-oriented and technology-enabled care than on basic discretionary items. That matters for the pet wearable market because devices linked to safety, monitoring, and wellness have a stronger case when households review spending priorities. APPA also showed that only 27% of pet owners planned to reduce pet spending over the next 12 months in 2025, which was well below the intended pullback in apparel and home goods, and that supports continued demand for higher-value pet solutions. The result is that brands positioned around pet health and prevention are better protected than those relying only on novelty or entertainment features.

Preventive Health Monitoring and Chronic-Disease Screening

Preventive monitoring is becoming one of the strongest structural supports for the pet wearable market. Invoxia’s Biotracker, designed for dogs at cardiac risk, reports 92% sensitivity in detecting atrial fibrillation and tracks resting breathing rate against thresholds aligned with ACVIM guidance, showing how wearables are moving closer to clinically relevant use cases.[2]Invoxia, “Invoxia Biotracker for Cavaliers & Small Dogs at Cardiac Risk,” Invoxia, invoxia.com PetPace pushed this direction further in September 2025 when it launched V3.0 of its AI smart collar with epilepsy episode monitoring for dogs, giving veterinarians and owners a more precise record for diagnosis and treatment planning. These launches matter because the pet wearable market is no longer driven only by pet recovery after escape or loss. Continuous monitoring creates a reason to keep the device active every day, which lifts retention and strengthens subscription revenue. Veterinary support also becomes a practical distribution advantage, because products with stronger clinical positioning are harder for less validated competitors to displace.

GPS Safety, Geofencing, and Lost-Pet Recovery Demand

Location recovery remains the most familiar purchase trigger in the pet wearable market. Halo Collar launched Halo Collar 5 in September 2025 with AlwaysOn GPS, 20 boundary and location updates per second, and AI-powered signal processing, while the device was positioned around protection for more than 200,000 dogs in the United States each day. Garmin strengthened the same use case earlier with Alpha LTE in North America, combining multi-GNSS tracking with smart switching between LTE and VHF networks for better coverage in mixed terrain.[3]Garmin, “Garmin Unveils Alpha LTE, Cellular-Based Dog Tracking Integration,” Garmin Newsroom, garmin.com These product moves show that recovery and geofencing still provide the clearest value proposition for first-time buyers. They also show that standalone location features are becoming easier to match across brands, which is pushing the pet wearable market toward added value in analytics, alerts, and connected services. As GPS becomes standard, revenue growth will depend more on what brands build on top of tracking than on tracking alone.

IoT, AI, and Sensor Miniaturization

Sensor miniaturization is widening the addressable user base for the pet wearable market. Fi launched the Series 3+ in June 2025 with AI-based detection of scratching, licking, barking, eating, and drinking at 80% accuracy, along with up to 3 months of battery life and waterproofing suited to daily use. Fi followed that in August 2025 with Fi Mini at 0.56 ounces, which made GPS and health tracking more practical for cats and dogs under 10 pounds. Smaller form factors matter because many pets, especially cats and smaller breeds, have traditionally fallen outside the comfortable use range of larger collar devices. The pet wearable market also benefits when multiple sensors can be placed on one compact platform, because that reduces the need for separate devices around one animal. Over time, this supports better household adoption and makes subscription retention more durable, since one device can cover more daily functions with less friction.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Upfront Device and Recurring Subscription Costs | -2.1% | Global, most pronounced in price-sensitive markets such as Latin America, MEA, and Southeast Asia | Short term (≤ 2 years) |

| Battery Life, Charging Frequency, and Outdoor Durability Constraints | -1.5% | Global, high relevance in APAC outdoor and rural use cases, and MEA | Medium term (2-4 years) |

| Data Privacy, Consent, and Interoperability Compliance Burden | -1.2% | EU, North America in CCPA-governed states, and Australia | Long term (≥ 4 years) |

| Counterfeit and Low-Accuracy Devices Undermining Owner Trust | -0.9% | APAC, mainly China and Southeast Asia, MEA, and South America | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Upfront Device and Recurring Subscription Costs

Pricing remains the most immediate barrier to broader household adoption in the pet wearable market. Premium AI-enabled smart collars still sit between USD 200 and USD 599, and recurring data plans can add another USD 96 to USD 360 each year. That total cost is manageable for upper-income owners in North America and Western Europe, but it remains difficult for many buyers in Latin America, Southeast Asia, and parts of the Middle East and Africa. The challenge is not only the hardware price, because mandatory subscriptions also make the long-term commitment harder to justify for first-time users. When a device is framed as a nice-to-have tracker instead of a health or safety tool, value-seeking households are far more likely to delay the purchase. Brands that cannot separate entry hardware from premium analytics will limit the scale potential of the pet wearable market in lower-income and high-growth geographies.

Data Privacy, Consent, and Interoperability Compliance Burden

Data governance is becoming a slower-moving but meaningful restraint for the pet wearable market. The European Data Protection Supervisor stated in Opinion 22/2024 that privacy-by-design, data minimization under GDPR Article 5, and clear consent mechanisms matter in connected systems involving traceability and sensitive data flows. That direction is important because pet wearables increasingly capture location, activity, and health-related data that may be shared across apps, insurers, and veterinary platforms. U.S. state rules around consumer data sharing add another layer of complexity when location and health information moves to third parties. The less visible cost falls on engineering teams, because products must work across borders while still meeting different privacy and interoperability requirements. This slows product cycles and narrows the speed advantage that smaller innovators might otherwise use against larger incumbents.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Collar Dominance Tested by Camera Momentum

Smart collars held 63.55% of the pet wearable market size in 2025, which shows that the collar remains the main platform for GPS, biometrics, and behavioral analytics. The segment leads because it sits on the animal throughout the day and can capture continuous data without adding extra friction for owners. That daily contact gives smart collars an advantage over more occasional or place-based devices such as cameras. Fi reinforced this segment in March 2026 with Fi Intelligence, an AI health companion that uses its canine dataset to deliver personalized insights and let owners upload veterinary records into one health profile. Health-specific wearables are also emerging as a more clinical layer inside the pet wearable industry, and PetPace Health 2.0 was named IoT Wearable Device of the Year in January 2025, which supported the shift toward medically oriented positioning.

Smart cameras are projected to grow at a 15.89% CAGR through 2031, making them the fastest-growing product line in the pet wearable market. Demand is tied to dual-income households that want remote visibility, interaction, and feeding support while away from home. The category is benefiting from lower hardware costs and the more common use of two-way audio and AI detection. At the same time, camera hardware is becoming easier to replicate, so the pet wearable market is likely to reward brands that connect cameras to broader health and alert ecosystems rather than selling them as isolated devices.

By Connectivity Mode: GPS Incumbency and the Hybrid Inflection

Stand-alone GPS accounted for 44.87% of the 2025 market, which reflects the continued importance of dependable tracking in outdoor and low-connectivity settings. This segment still serves hunters, ranchers, and trail users who value purpose-built reliability more than a broad feature stack. Garmin’s Alpha systems show why this remains durable, because the product family combines multi-GNSS reception with field-oriented coverage support for working and sporting dogs. Cellular and Wi-Fi modes remain more attractive for urban and suburban users who need seamless app access rather than rugged field performance. The pet wearable market still depends on GPS credibility because owners will tolerate fewer compromises in safety-related functions than in lifestyle features.

Hybrid multi-connectivity is forecast to expand at a 16.18% CAGR through 2031, which makes it the fastest-growing connectivity mode in the pet wearable market. The value of hybrid design is that it reduces dead zones by switching between satellite, LTE-M, Wi-Fi, and Bluetooth based on the environment and battery needs. That shift matters because pet movement often crosses indoor, outdoor, urban, and semi-rural settings in one normal day. Connectivity architecture is therefore becoming a true differentiator in the pet wearable industry, especially when smart switching improves battery life and reliability at the same time. Brands that own this firmware layer are less exposed to hardware commoditization than those competing only on a GPS chip or a radio module.

By Animal Type: Dogs Anchor Revenue While Feline Innovation Accelerates

Dogs held 57.27% of pet wearable market share in 2025 and are projected to grow at 15.45% CAGR through 2031, which keeps canine demand at the center of the category. Dogs remain the strongest revenue base because they spend more time outdoors, adapt more easily to wearables, and can carry larger batteries and broader sensor arrays. The segment is also expanding because AI health features continue to build on installed dog-focused hardware rather than starting from zero each cycle. APPA reported a 23% increase in cat ownership in 2024, with 49 million U.S. households owning a cat, and cat harness ownership rising 52% since 2018, which is gradually changing the accessory habits that support wearable adoption. That makes the pet wearable market more balanced over time, even though dogs still dominate current demand.

The cat segment is moving from a secondary use case toward a more defined product category. Tractive’s April 2026 launch of the CAT 6 Mini introduced a collar-integrated GPS and health-monitoring device designed for feline physiology, including resting heart rate and respiratory rate tracking against cat-specific baselines. Other companion animals remain a smaller opportunity, but APPA also reported 25% year-on-year growth in bird ownership in 2025, which supports a gradual long-term expansion into adjacent species as devices get smaller and lighter. The pet wearable market, therefore, still runs on dog-led scale today, while feline and small-pet innovation is becoming a more credible future growth path.

By Application: Tracking Dominates, Medical Diagnosis Reshapes the Value Ladder

Identification and tracking held 50.23% of the pet wearable market size in 2025, which confirms that safety remains the most common entry point for first-time device buyers. The core use case is simple and durable, because owners respond quickly to the fear of escape or loss. That recurring anxiety supports both replacement demand and subscription renewal even before health features are fully adopted. The pet wearable market is still anchored by this application because it solves an immediate problem across most geographies and income levels. It also gives brands a large installed base from which to introduce more advanced functions later.

Medical diagnosis and treatment are forecast to grow at a 16.83% CAGR through 2031, making it the fastest-rising application in the pet wearable market. PetPace deepened that shift in October 2025 when it partnered with Crucial Data Solutions to integrate real-time at-home animal health data from the PetPace collar into the TrialKit eClinical platform for decentralized veterinary research. Health and wellness monitoring remains a large adjacent use case, while behavior monitoring is also gaining medical relevance as collars detect scratching, licking, barking, eating, and drinking with increasing accuracy. Devices such as Tractive’s DOG 6 XL are pushing further into this space with scratch monitoring aimed at early signs of allergy or stress, which shows how the pet wearable market is moving from basic observation toward more actionable care signals.

By End User: Household Owners Drive Volume, Veterinary Channel Drives Growth

Household pet owners accounted for 77.90% of the market in 2025, which reflects the consumer-led origin of wearable adoption. This segment is supported by direct-to-consumer channels, bundle pricing, and recurring service plans that fit how most owners already shop for pet products. APPA also showed that pet spending held up better than many household categories in 2025, with only 27% of owners planning to reduce pet spending over the next 12 months. Other end users, such as shelters, boarding facilities, and research institutions, remain smaller in volume, but they still matter because institutional use can validate device quality for retail buyers. In the pet wearable industry, that validation effect can influence purchase confidence even when the direct revenue contribution is modest.

Veterinary hospitals and clinics are projected to expand at a 17.28% CAGR through 2031, making them the fastest-growing end-user group in the pet wearable market. Clinics are using wearable data more often for pre-visit review, chronic disease follow-up, and recovery tracking between appointments. ICE-Tech and Lupa partnered with Vetsure in April 2026 to embed pet insurance claims into veterinary workflows, linking wearable health metrics, telemedicine records, and insurance processing in one system while saving staff more than 1 hour each day. When clinicians adopt a platform, the pet wearable market gains a low-friction distribution channel because the veterinarian becomes part of the device recommendation path.

Geography Analysis

North America held 41.88% of the pet wearable market share in 2025, and the region remains the largest base for subscriptions, connected monitoring, and premium device adoption. The United States drove most of that position, with 95 million pet-owning households in 2025 and dog ownership reaching 71 million households, which was 4 million higher than in 2024. The region also benefits from strong mobile network coverage that supports LTE-M tracking and from a veterinary system that is more ready to use remote monitoring tools in normal care routines. Pet insurance adoption is helping as well because device-linked benefits make wearables easier to justify for health and safety use cases. Fi’s expansion path, which moved through Canada before broader rollout into the UK and EU in March 2026, shows that North America still functions as the main launch platform for international scale.

Europe is the second-largest region in the pet wearable market, with Germany standing out because buyers place strong value on technically reliable and certified devices. The UK, France, Spain, and Italy follow as important mid-tier markets where cat ownership trends, urban living, and rising insurance use are supporting device demand. Europe also has a clearer path toward insurer-linked adoption as reimbursement models begin to appear in pet care. At the same time, GDPR Article 5 data minimization and EDPS Opinion 22/2024 raise the design bar for connected products that handle location or health data, which makes privacy-ready development more important in this region.

Asia-Pacific is forecast to grow at a 17.62% CAGR through 2031, which makes it the fastest-expanding regional opportunity in the pet wearable market. China, India, and South Korea are the main growth engines because companion-animal ownership is increasing while urban living makes safety and monitoring more relevant. Japan and Australia are more established markets where clinical-grade devices can sustain pricing closer to North American levels. The Middle East and Africa remains earlier in adoption, with GCC countries led by the UAE and Saudi Arabia showing the strongest premium demand, while South Africa is the main sub-Saharan market. South America is led by Brazil, where the primary demand still centers on GPS-enabled tracking, and the rest of the region adds gradual growth as middle-class pet spending increases.

Competitive Landscape

The pet wearable market remains fragmented, and that keeps competitive intensity high across devices, services, and software layers. Tractive is the most globally scaled competitor by subscription footprint, with more than 1.4 million active users across 175 countries and a portfolio of over 200 patents in tracking, wearable technology, and pet health monitoring. The company also stated that annual recurring revenue surpassed EUR 100 million, or USD 108 million, in 2024, which points to the strength of its subscription-led model. Tractive’s July 2025 acquisition of Whistle from Mars Petcare removed a major U.S. competitor and added an established installed base, which shows how scale can be built faster through platform consolidation than through hardware launches alone. In the pet wearable market, that kind of move matters because recurring subscribers often carry more long-term value than one-time device sales.

PetPace occupies a different position in the pet wearable market because it competes through veterinary-grade data and clinical relevance rather than broad consumer reach. Its V3.0 collar, introduced in September 2025, added epilepsy episode monitoring and 24/7 telehealth integration, while its platform continues to emphasize AI and ML-driven health analysis. Garmin remains a strong specialist rather than a category-wide player, and its Alpha LTE platform shows how the company stays focused on working and sporting dogs that need reliable mixed-terrain tracking. This leaves room for specialists who solve one use case very well, even when they do not attempt to serve the full pet wearable market. Competitive success, therefore, depends on clear product focus as much as on raw brand scale.

There is still open space in 3 areas of the pet wearable market. Medically validated cat wearables remain early, mass-market GPS plus activity trackers below USD 50 are still limited in Latin America and Southeast Asia, and insurance-linked pricing models remain underdeveloped. Tractive’s CAT 6 Mini shows that cat-specific monitoring is advancing, but the segment still has far fewer validated products than the dog category. Software-led acquirers are also entering the space, and the March 2026 acquisition of Tractive by Bending Spoons suggests that recurring pet technology subscriptions are attracting broader platform interest. Even so, privacy compliance, clinical validation, and certification requirements still create barriers that give certified incumbents more protection than a simple unit-share view would suggest.

Pet Wearable Industry Leaders

Dogtra

Fitbark Inc.

Loc8tor Ltd.

Garmin Ltd

Tractive GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ICE-Tech and Lupa partnered to embed pet insurance claims into veterinary workflows for Vetsure, enabling claim initiation within the practice management system and eliminating third-party claims hubs, the integration is designed to save veterinary staff over 1 hour daily and cut revenue leakage by up to 10% via AI billing capture.

- April 2026: Tractive launched the DOG 6 XL and CAT 6 Mini, its next-generation health intelligence trackers, at MSRPs of USD 89 and USD 79 respectively. The CAT 6 Mini is the first collar-integrated GPS and health-monitoring device purpose-built for feline physiology, introducing vital sign monitoring with cat-specific baselines, the DOG 6 XL delivers up to 3x longer battery life alongside advanced scratch monitoring.

- March 2026: Fi launched Fi Intelligence, an AI health companion drawing on the world's largest proprietary canine behavioral dataset to provide personalized health insights and enable vet record integration for comprehensive health profiling.

- March 2026: Fi announced major international expansion into the UK and EU markets, introducing the Fi Series 3+ AI-powered dog collar into Germany, France, the Netherlands, and the UK with multi-language app support, following earlier expansions into Canada and Mexico.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the pet wearable market as connected collars, cameras, harnesses, vests, and smart tags worn by companion dogs, cats, and other household pets that employ GPS, RFID, sensors, cellular, Wi-Fi, or Bluetooth to deliver identification, location, activity, or physiological data to owners or veterinarians.

Scope exclusion: devices for livestock herd management, implantable microchips, and single-use RFID tags are outside the scope.

Segmentation Overview

- By Product Type

- Smart Collars

- Smart Cameras

- Smart Harnesses & Vests

- Smart Tags & Clip-on Trackers

- Health Monitoring Wearables

- By Connectivity Mode

- Stand-alone GPS

- Cellular-connected

- Wi-Fi-connected

- Hybrid Multi-connectivity

- Satellite-connected

- By Animal Type

- Dogs

- Cats

- Other Companion Animals

- By Application

- Identification & Tracking

- Health & Wellness Monitoring

- Medical Diagnosis & Treatment

- Behavior Monitoring & Control

- Safety, Security & Facilitation

- By End User

- Household Pet Owners

- Veterinary Hospitals & Clinics

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed veterinarians, specialty retailers, tele-health platform managers, and component vendors across North America, Europe, and Asia-Pacific.

Their guidance refined penetration rates, replacement cycles, connectivity preferences, and regional price bands, which were then triangulated with survey feedback from urban pet owners.

Desk Research

Mordor analysts begin with pet population and expenditure series from bodies such as the American Pet Products Association, FEDIAF, and Statistics Canada, then overlay customs shipments (HS 851762) and open clinical journals to size unit demand and benchmark average selling prices.

Patent analytics via Questel and 10-K filings reveal sensor trends and revenue splits, while paid libraries like D&B Hoovers and Dow Jones Factiva supply shipment clues and funding milestones.

The sources named are illustrative; many additional records supported data checks.

Market-Sizing & Forecasting

A top-down model converts national dog and cat counts into an addressable pool, applies validated penetration and multi-pet factors, and multiplies by median device ASPs.

Select bottom-up roll-ups of supplier shipments and sample e-commerce volumes check and adjust totals.

Key variables include pet ownership growth, smartphone penetration, average device life, e-ID regulations, component cost curves, and insurance enrollment.

Five-year forecasts employ multivariate regression blended with scenario analysis.

Data gaps in shipment logs are bridged through three-year moving averages anchored to audited disclosures.

Data Validation & Update Cycle

Outputs pass two analyst reviews against historical series and manufacturer filings; material variances trigger rapid re-contact with experts.

The model refreshes annually, with interim patches issued after events such as new regulatory mandates or major recalls, so clients receive the latest view at download.

Why Mordor's Pet Wearable Baseline Deserves Confidence

Published figures often diverge because providers choose differing product mixes, price bases, and refresh cadences. Mordor's disciplined scope alignment, dual-sourced variables, and yearly update cycle yield a balanced baseline for decision-makers.

Key gap drivers include: some studies bundle livestock trackers, others apply uniform uptake rates without field checks, and several convert revenues using static 2022 exchange rates, inflating or depressing totals versus our 2025 base.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.14 Billion (2025) | ���ϲ����� | - |

| USD 3.09 Billion (2024) | Global Consultancy A | Includes livestock wearables; ASPs based only on premium SKUs |

| USD 3.69 Billion (2024) | Industry Publisher B | Uniform 15% annual uptake, limited primary validation |

| USD 1.72 Billion (2024) | Regional Consultancy C | Excludes smart cameras and Wi-Fi-only tags; currency fixed at 2019 FX |

Taken together, the comparison shows Mordor's numbers sit between conservative and aggressive positions, traceable to transparent variables and repeatable steps that hold up under client scrutiny.

Key Questions Answered in the Report

What is the current size of the pet wearable sector?

The pet wearable market stood at USD 3.14 billion in 2025, reached USD 3.56 billion in 2026, and is projected to reach USD 7.23 billion by 2031 at a 15.21% CAGR.

Which product category leads demand for connected pet devices?

Smart collars led with 63.55% share in 2025 because they combine GPS, biometric sensing, and behavior analytics in one device.

Which region is growing the fastest for pet tracking and health devices?

Asia-Pacific is the fastest-growing region, with a projected 17.62% CAGR through 2031, driven by rising pet adoption, urbanization, and stronger mobile infrastructure.

Why are veterinary clinics becoming important buyers?

Veterinary hospitals and clinics are forecast to grow at a 17.28% CAGR because wearable data supports remote monitoring, baseline review before visits, and post-treatment follow-up.

What is the biggest barrier to wider adoption?

High upfront device prices and recurring subscriptions remain the most immediate obstacle, especially in price-sensitive markets where multi-year ownership costs are harder to justify.

Page last updated on: