Pet Food Extrusion Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

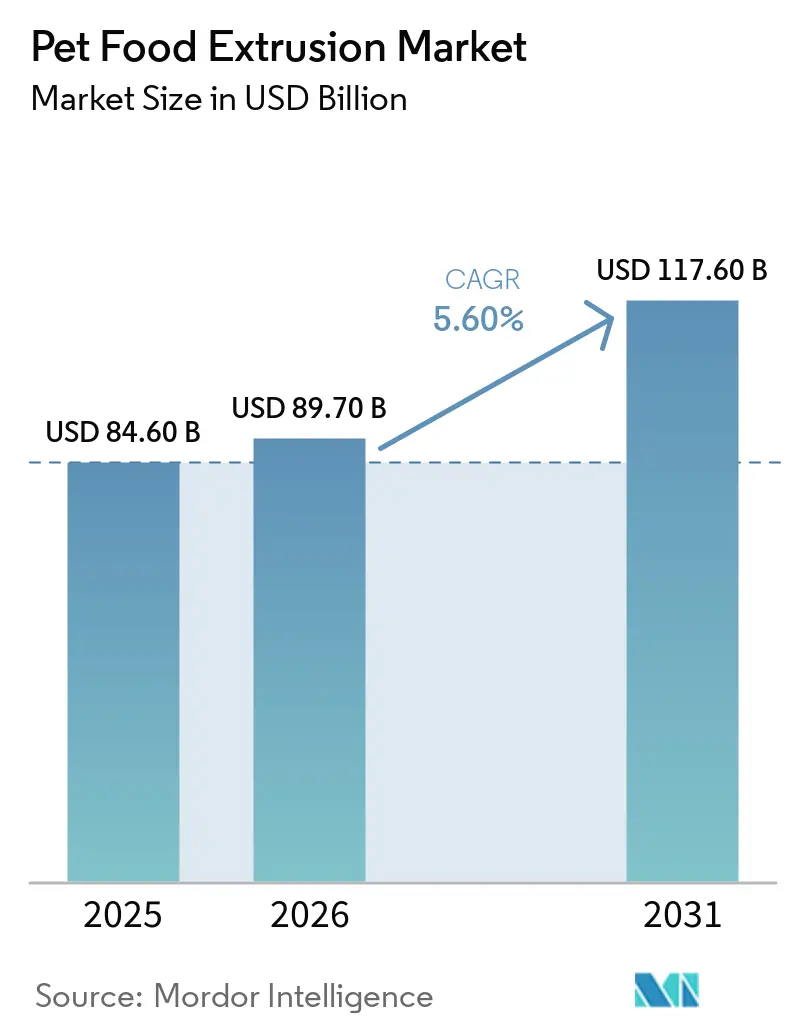

| Market Size (2026) | USD 89.70 Billion |

| Market Size (2031) | USD 117.60 Billion |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

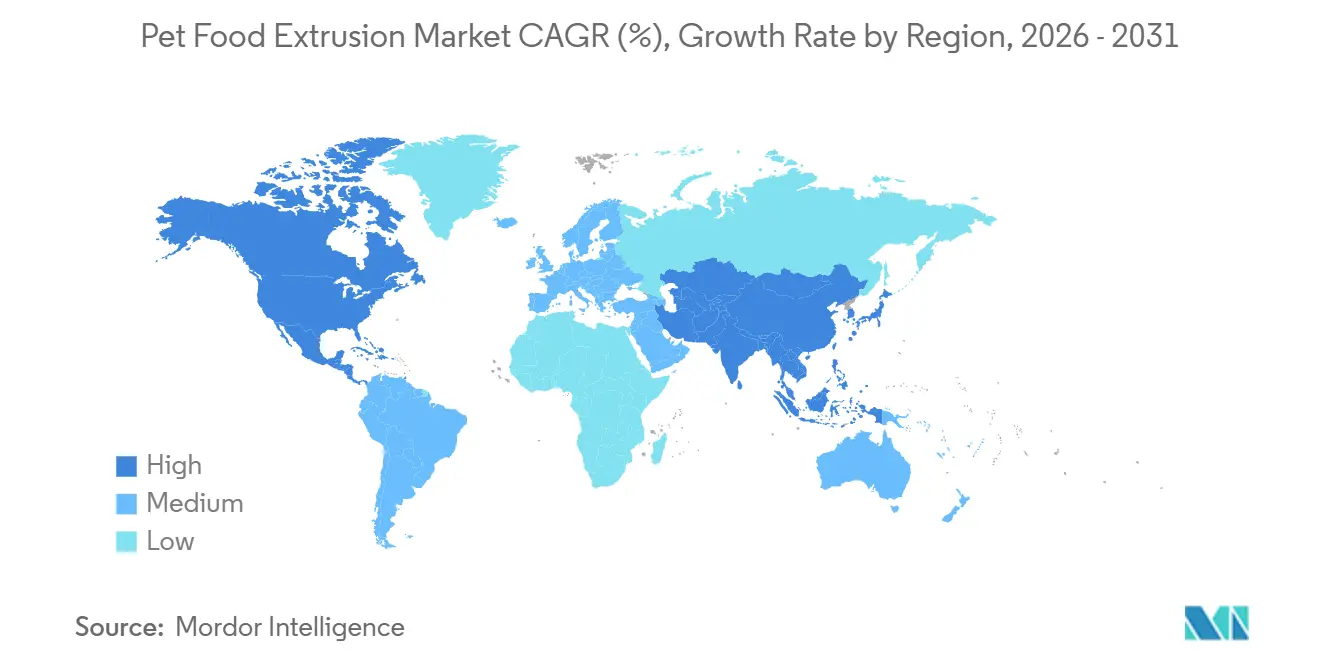

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Pet Food Extrusion Market Analysis by ���ϲ�����

The pet food extrusion market size was valued at USD 84.60 billion in 2025 and is projected to grow from USD 89.70 billion in 2026 to USD 117.60 billion by 2031, registering a CAGR of 5.60% between 2026 and 2031. This growth is driven by increasing pet humanization trends. According to America Pet Product Association, 41% of dog owners and 38% of cat owners in the United States opted for premium diets in 2024, an increase of 5% and 9% from the previous year. Producers are now prioritizing more than just output, as premium kibble, functional recipes, and therapeutic formats require tighter control, hygienic construction, and quicker recipe changeovers within the same production line. Competition in the pet food extrusion market is also evolving toward software-enabled services. Features such as process optimization, remote diagnostics, and overall equipment effectiveness (OEE) monitoring are helping suppliers maintain margins and generate recurring service revenue. However, ingredient inflation and the growing popularity of raw, freeze-dried, and fresh feeding formats are constraining the growth of standard kibble volumes. Despite these challenges, the market benefits from a diverse demand base across companion animals, aquatic species, and small mammals, which mitigates reliance on any single category or geographic region.

Key Report Takeaways

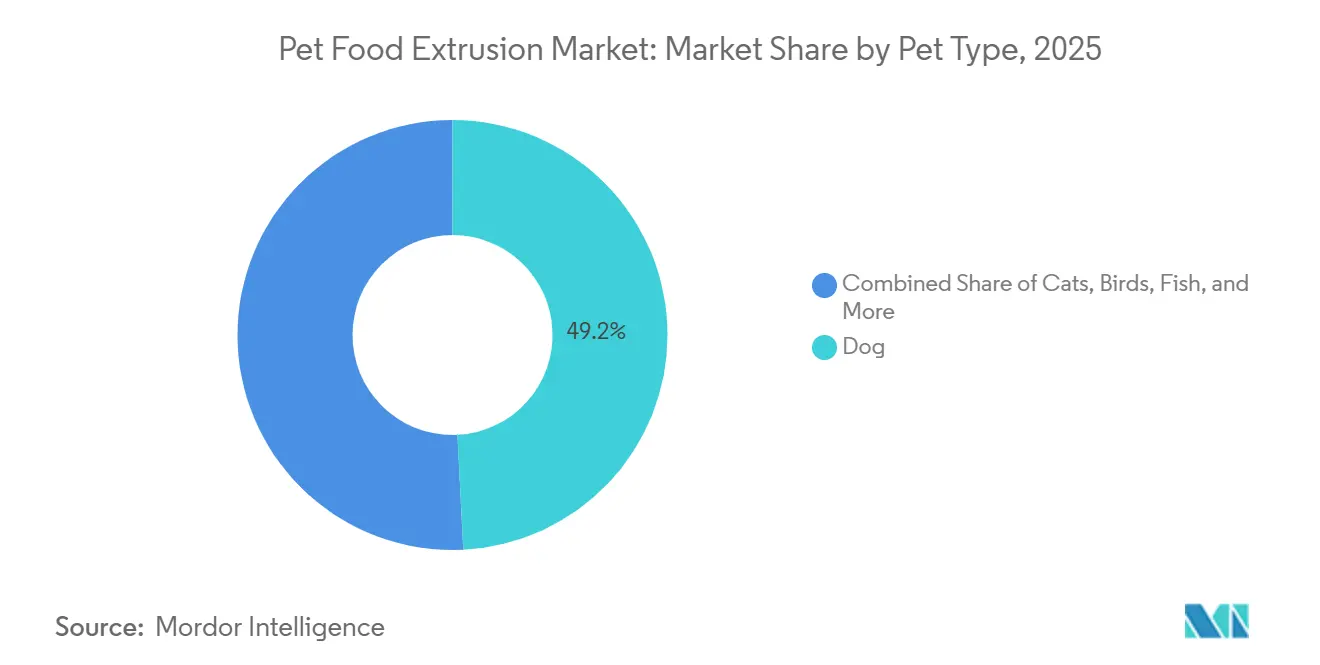

- By pet type, the pet food extrusion market share for the dog segment led with the largest 49.2% share in 2025, while the pet food extrusion market size for the cats segment is projected to grow at the fastest 6.1% CAGR from 2026 to 2031.

- By product form, the pet food extrusion market share for the dry kibble segment held the largest 62.3% market share in 2025, while the pet food extrusion market size for the treats and snacks segment is forecast to expand at the fastest 6.5% CAGR from 2026 to 2031.

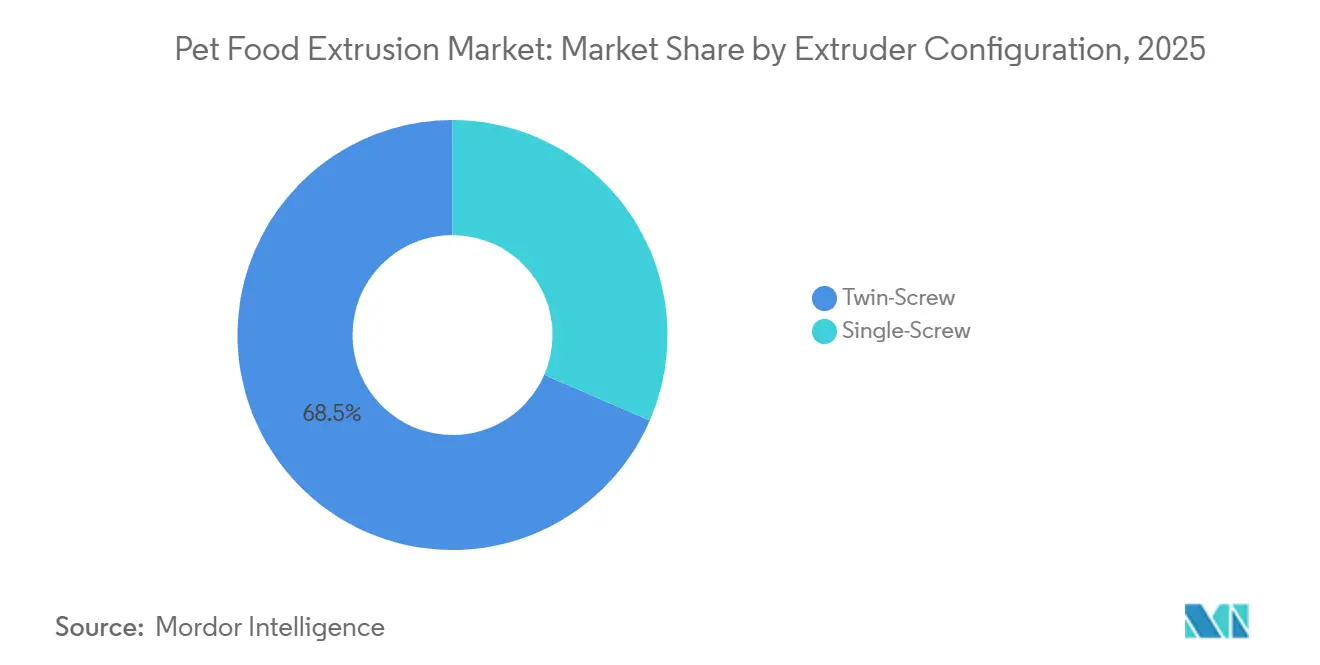

- By extruder configuration, twin-screw systems accounted for the largest 68.5% share in 2025 and also recorded the fastest projected CAGR at 6.6% from 2026 to 2031.

- By geography, North America held the largest 39.7% revenue share in 2025, while Asia-Pacific is forecast to expand at a 6.5% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pet Food Extrusion Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization driving higher-throughput extrusion investments | +1.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Veterinary and therapeutic diets requiring tighter process control | +0.9% | North America and Europe, with growing relevance in Asia-Pacific | Medium term (2-4 years) |

| Clean-label and highly digestible kibble demand | +0.7% | North America, Europe, and Australia | Short term (≤ 2 years) |

| Insect and alternative proteins widening formulation needs | +0.5% | Europe and Asia-Pacific, with spillover into North America | Long term (≥ 4 years) |

| Energy-efficient twin-screw and automation upgrades | +0.8% | Global, led by Europe and Asia-Pacific | Medium term (2-4 years) |

| Toll-extrusion demand from direct-to-consumer and emerging brands | +0.4% | North America and Europe | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Premiumization Driving Higher-Throughput Extrusion Investments

Premium pet nutrition remains a key factor driving both volume and value growth in the pet food extrusion market. According to the American Pet Products Association (APPA), pet food products containing prebiotics and probiotics experienced significant growth in 2024, with 13% of dog owners and 12% of cat owners in the United States purchasing these products. The APPA further reported an approximately 18% year-on-year increase in spending on functional pet food, with average consumer spending rising by about USD 8 compared to the previous year[1]Source: American Pet Products Association, “Research Insights on Premium & Functional Pet Foods,” americanpetproducts.org. This trend has prompted pet food manufacturers to enhance extrusion lines to enable more precise micro-ingredient dosing, improved die-pressure control, and higher fresh-meat inclusion levels compared to traditional kibble production. Consequently, production-line flexibility has gained importance, as manufacturers prioritize systems capable of transitioning between standard and premium recipes with minimal equipment adjustments.

Veterinary and Therapeutic Diets Requiring Tighter Process Control

Veterinary and therapeutic diets impose stricter requirements on the pet food extrusion market compared to standard dry food. These products demand more precise starch gelatinization, narrower protein denaturation ranges, and greater batch uniformity, as their production is often tied to specific nutritional outcomes. A study published in the Animals journal in 2025 on the safety and digestibility of a novel ingredient highlighted the importance of reproducible processing and adherence to Good Manufacturing Practices (GMP), which drive the need for systems capable of documenting and replicating exact operating conditions. In this segment of the pet food extrusion market, the use of programmable logic controller (PLC)-based monitoring and digital recordkeeping is becoming standard, as validation and traceability are as critical as production throughput. Additionally, producers in this segment achieve faster capital recovery due to the higher margins associated with therapeutic diets compared to commodity kibble.

Clean-Label and Highly Digestible Kibble Demand

The growing demand for clean-label and highly digestible products is increasing process complexity in the pet food extrusion market. Manufacturers are required to maintain stricter control over moisture, temperature, and ingredient stability during production. As reported by the National Metal and Materials Technology Center, Thailand, twin-screw extrusion and advanced steam-conditioning systems have successfully improved nutrient retention and digestibility by 2025. These technologies have also enabled cleaner formulations with reduced reliance on synthetic additives and preservatives.[2]Source: National Metal and Materials Technology Center Thailand, “Tech-Driven Excellence in Pet Food Processing and Extrusion,” foodfocusthailand.com. Additionally, limited-ingredient and hypoallergenic product lines necessitate stricter allergen management and more thorough equipment changeovers between production batches. Consequently, manufacturers are investing in hygienic extrusion systems, stainless-steel contact surfaces, and low-residue screw configurations to ensure stable commercial-scale production for premium pet food applications.

Insect and Alternative Proteins Widening Formulation Needs

The growth of insect and alternative proteins is introducing new technical challenges in the pet food extrusion market. According to researchers from Kansas State University, a study published in the Processes journal in 2025 reported that including black soldier fly larvae meal at a 30% inclusion rate led to expansion instability and irregular kibble shapes, attributed to its chitin content. Similarly, cricket flour reduced specific mechanical energy and led to a process surge due to its fat profile. These challenges imply that processors often require modifications such as different screw geometries, adjusted moisture settings, or additional upstream treatment steps to handle these ingredients at scale. Consequently, this is not merely a matter of substituting ingredients but involves a broader formulation scope, potentially necessitating additional capital investment and extended validation periods. Over time, this dynamic links the pet food extrusion market more closely to protein innovation rather than solely relying on volume growth in traditional kibble production.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Protein and cereal input volatility compressing processor margins | -0.9% | Global, strongest in North America and South America | Short term (≤ 2 years) |

| Cross-contamination and allergen segregation raising line capex | -0.5% | North America and Europe | Medium term (2-4 years) |

| Raw, freeze-dried, and air-dried diets competing with kibble | -0.7% | North America, Europe, and Australia | Long term (≥ 4 years) |

| Skilled extrusion labor shortages slowing ramp-up | -0.4% | North America and Europe | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Protein and Cereal Input Volatility Compressing Processor Margins

Volatility in protein and cereal inputs continues to be a significant restraint on the pet food extrusion market. The production of dry pet food relies heavily on grain meals, edible oils, and protein-based agricultural ingredients, all of which are subject to fluctuating pricing patterns. Sudden shifts in cereal and oilseed markets create procurement uncertainties and reduce visibility into operating margins for extrusion processors. Smaller and mid-sized manufacturers are particularly vulnerable, as they often depend on spot purchasing rather than long-term supply agreements. This margin pressure can lead to delays in investments for additional extrusion capacity, equipment upgrades, and production-line expansions. Even when consumer demand remains steady, unstable raw material costs frequently hinder capital spending decisions across commercial pet food processing operations.

Raw, Freeze-Dried, and Air-Dried Diets Competing with Kibble

Raw, freeze-dried, and air-dried products are limiting growth potential in certain segments of the pet food extrusion market. Freshpet, Inc. reported net sales exceeding USD 1.1 billion in fiscal year 2025, reflecting a 13% year-on-year increase, which highlights the rapid growth in demand for fresh-format pet food. While this trend does not eliminate the role of extrusion in the market, it constrains the growth of standard kibble volumes within overall pet food spending. Flexible production lines capable of manufacturing coated, semi-moist, and treat formats help mitigate this challenge, but the shift is altering the long-term demand composition in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Type: Dogs Hold Volume Leadership, Cats Propel Growth

The pet food extrusion market share for the dog segment accounted for the largest 49.2% in 2025. Dog nutrition continues to support the largest installed production base, as canine food products dominate industrial dry feed manufacturing and large-format kibble production globally. Standard dog food lines remain integral to equipment utilization, retrofit demand, and production-line replacement cycles. High-capacity systems are primarily designed for mainstream dog kibble and treat production in commercial pet food manufacturing facilities. Large integrated processors prioritize dog-focused production due to their ability to maintain consistent throughput utilization and achieve stronger economies of scale in mass-market pet food operations worldwide.

The pet food extrusion market size for the cats segment is projected to grow at the fastest 6.1% CAGR from 2026 to 2031. Cat nutrition is increasingly driving premiumization, as feline formulations require tighter process control, protein balancing, coating precision, and taurine supplementation compared to many dog food products. Additionally, smaller pet categories, including birds, fish, and small mammals, are creating specialized production opportunities. These categories demand unique density controls, die systems, and moisture-management configurations for floating feed, pelletized diets, and small-format extruded products within commercial pet food extrusion operations globally.

By Product Form: Dry Kibble Dominates, Treats Accelerate

The pet food extrusion market share for dry kibble held the largest 62.3% 2025. Dry kibble remains the primary production format because it offers longer shelf stability, easier transportation, and lower storage complexity than chilled or frozen pet food products. Standard kibble lines continue to represent the largest installed production capacity across global pet food processing facilities. Large integrated manufacturers rely heavily on dry food systems for high-volume throughput and operating efficiency. Dry kibble production also remains central to equipment replacement cycles, energy-efficiency upgrades, and modernization investments across commercial extrusion operations globally.

The pet food extrusion market size for treats and snacks is forecast to expand at the fastest 6.5% CAGR from 2026 to 2031. Premium treats and snacks are increasingly influencing investment decisions because processors seek flexible production systems capable of rapid product switching across shapes, textures, and coatings. Multi-format extrusion systems with faster die changes and shorter cleaning cycles are becoming more attractive for premium pet food manufacturing. Semi-moist products continue serving niche demand for enhanced palatability and differentiated texture profiles. Veterinary and therapeutic diets remain smaller in volume but require advanced segregation, micro-dosing, and validation systems that increase production complexity and equipment requirements.

By Extruder Configuration: Twin-Screw Lines Dominate Complex and Premium Applications

Twin-screw systems accounted for the largest 68.5% pet food extrusion market share in 2025. These systems remain dominant due to their superior process stability, particularly for high-fat, high-moisture, and protein-rich pet food formulations. They also offer greater product flexibility and consistency, especially for premium kibble and high-meat recipes. Pet food manufacturers increasingly prefer twin-screw technology as it enhances operational efficiency while maintaining throughput performance for complex formulations. Additionally, features such as energy efficiency, advanced moisture management, and tighter process control are driving the adoption of twin-screw configurations in modern commercial pet food production facilities worldwide.

Twin-screw systems also recorded the fastest projected CAGR at 6.6% from 2026 to 2031. Meanwhile, single-screw systems remain relevant in cost-sensitive regions and for standard kibble applications where simpler formulations dominate production. Manufacturers are enhancing single-screw technology with density-control systems and operational efficiency improvements to remain competitive against premium twin-screw installations. Budget-conscious processors in regions such as South America, Africa, and parts of Asia continue to favor single-screw systems due to their lower upfront investment requirements. The market reflects a dual structure, with twin-screw systems leading premium production and single-screw systems supporting economical, large-volume pet food manufacturing globally.

Geography Analysis

The pet food extrusion market share for North America held the largest 39.7% in 2025. The region remains a key production and consumption hub due to strong premiumization trends, advanced retail infrastructure, and a well-established manufacturing base. Investments in hygienic design, digital monitoring systems, and energy-efficient extrusion technologies further bolster the market. Major commercial manufacturers are focusing on retrofit programs and operational efficiency improvements at existing production facilities. Additionally, Canada and Mexico enhance the region's manufacturing capabilities through export-oriented dry food production and support for private-label pet food supply networks across North America.

The pet food extrusion market size for Asia-Pacific is forecast to expand at a 6.5% CAGR from 2026 to 2031. This growth is driven by increasing urbanization, rising premium pet ownership, and the expansion of organized retail across countries such as China, India, Southeast Asia, and Australia. Meanwhile, Europe maintains a significant manufacturing position, supported by stringent formulation standards, traceability requirements, and advanced processing capabilities. The region benefits from a dense production network and growing demand for premium, therapeutic, and alternative-protein pet food products. Investments in modern processing systems and hygienic extrusion infrastructure continue to drive global equipment demand within commercial pet food manufacturing operations.

South America, the Middle East, and Africa are smaller regional markets but are experiencing gradual growth due to increasing pet ownership and the expansion of modern retail channels. According to the Brazilian Institute of Geography and Statistics, Brazil’s pet sector generated BRL 75.4 billion (USD 12.7 billion) in revenue in 2024, with industrialized pet food contributing 54.1% of the total sector revenue, amounting to BRL 40.8 billion (USD 6.8 billion). Thailand continues to serve as a significant export-oriented manufacturing hub in the Asia-Pacific region. These regions are projected to drive future demand for flexible, mid-scale extrusion systems as commercial pet food production becomes more formalized and the adoption of premium products grows in developing consumer markets.

Competitive Landscape

The market remains moderately fragmented, with a limited number of full-line equipment suppliers leading major greenfield projects and commercial retrofit programs globally. Companies such as Bühler Holding AG, Andritz AG, Clextral S.A.S. (Legris Industries), Wenger Manufacturing, Inc. (JBT Marel), and Coperion GmbH (Hillenbrand, Inc.) hold strong competitive positions through their integrated processing solutions and extensive service networks. Competitive differentiation is increasingly driven by factors such as process reliability, energy efficiency, software integration, and the ability to combine upstream and downstream processing systems into complete production environments. Regional specialists continue to compete effectively by offering localized engineering support and application-specific customization capabilities.

Digitalization and automation are becoming critical competitive differentiators in the commercial extrusion equipment market. Suppliers are increasing investments in predictive maintenance, artificial intelligence-assisted process optimization, automated start-up systems, and browser-based production controls to enhance operating efficiency and minimize process variability. Manufacturers are shifting their focus toward integrated production ecosystems rather than standalone extrusion systems, as buyers prioritize simplified commissioning, centralized monitoring, and reduced downtime. Strategic consolidation is further strengthening full-line suppliers capable of integrating extrusion technology with cooking, coating, conveying, and packaging operations. Competitive positioning now increasingly depends on software capabilities, operational support depth, and long-term service relationships in addition to core extrusion equipment performance.

The competitive environment increasingly favors suppliers capable of integrating processing systems, digital controls, and application support within one coordinated platform. For instance, Bühler Holding AG introduced the Nutrex 7 Series extruder in May 2026, featuring browser-based controls, automated start-up functions, and reduced production waste capabilities[3]Source: Bühler Group, “Bühler Ushers in a New Era of Extrusion Systems with Nutrex 7 Series,” buhlergroup.com. Suppliers are also broadening their focus beyond standalone extruders to include conveying, forming, coating, and complete plant-integration systems. Global equipment manufacturers are targeting fast-growing mid-tier processors in Asia-Pacific and South America by offering localized engineering support, expanding regional service networks, and providing flexible mid-capacity production systems tailored for premium pet food applications.

Pet Food Extrusion Industry Leaders

Bühler Holding AG

Andritz AG

Clextral S.A.S. (Legris Industries)

Wenger Manufacturing, Inc. (JBT Marel)

Coperion GmbH (Hillenbrand, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Bühler Holding AG introduced the Nutrex 7 Series extrusion platform at Interpack 2026 in Düsseldorf. This platform includes AI-integrated, browser-based process control, a StepFlow automated start-up function that reduces waste by up to 30% per run, and hygienic design improvements that have achieved approximately a 50% reduction in cleaning time at pilot customer sites. This launch establishes Bühler Holding AG in the precision extrusion market, catering to premium and therapeutic pet food manufacturers.

- April 2026: CPM Holdings, Inc. installed a TwinTech extrusion system at Shengmeng's 5,136-square-meter facility in Hebei Province, China, signifying Shengmeng's entry into the pet food extrusion market. The system achieves approximately 5-10% lower energy consumption compared to traditional twin-screw systems by utilizing a permanent magnet synchronous motor. It is designed to meet the increasing demand for mid-tier kibble in China.

- November 2025: Andritz AG introduced the ExMax S1021 single-screw extruder at Victam Latam in São Paulo, Brazil. The extruder is equipped with the patented DensiFlex automatic density control system, ensuring consistent kibble expansion. It features a hygienic stainless-steel design and an energy-efficient drive system, catering to producers in the rapidly growing South American markets.

Global Pet Food Extrusion Market Report Scope

Pet food extrusion is a manufacturing process involving heat, pressure, and mechanical force to produce dry pet food products, including kibble, treats, and pellets. This process enhances digestibility, texture, shelf stability, and nutrient consistency, while supporting large-scale and efficient production of pet food. The pet food extrusion market report is segmented by pet type (dogs, cats, birds, fish, and small mammals), by product form (dry kibble, semi-moist, treats and snacks, and veterinary and therapeutic diets), by extruder configuration (single-screw and twin-screw), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). Market forecasts are provided in terms of value (USD).

| Dogs |

| Cats |

| Birds |

| Fish |

| Small Mammals |

| Dry Kibble |

| Semi-Moist |

| Treats and Snacks |

| Veterinary and Therapeutic Diets |

| Single-Screw |

| Twin-Screw |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Thailand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Pet Type | Dogs | |

| Cats | ||

| Birds | ||

| Fish | ||

| Small Mammals | ||

| By Product Form | Dry Kibble | |

| Semi-Moist | ||

| Treats and Snacks | ||

| Veterinary and Therapeutic Diets | ||

| By Extruder Configuration | Single-Screw | |

| Twin-Screw | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is driving growth in pet food extrusion through 2031?

Growth is being supported by premiumization, therapeutic diets, clean-label demand, and wider use of advanced twin-screw systems and the market size is projected to reach at USD 117.6 billion by 2031.

Which pet category creates the largest equipment demand?

Dogs remain the largest pet type, with a largest 49.2% market share in 2025.

Why are twin-screw extruders gaining share over single-screw systems?

Twin-screw units handle higher-fat and higher-moisture recipes more consistently, and they support better flexibility for premium and specialized formulations.

Which product form is growing fastest in processed pet food?

Treats and snacks are growing the fastest, with a 6.5% CAGR from 2026 to 2031.

Page last updated on: