Market Overview

| Study Period | 2021 - 2031 |

|---|---|

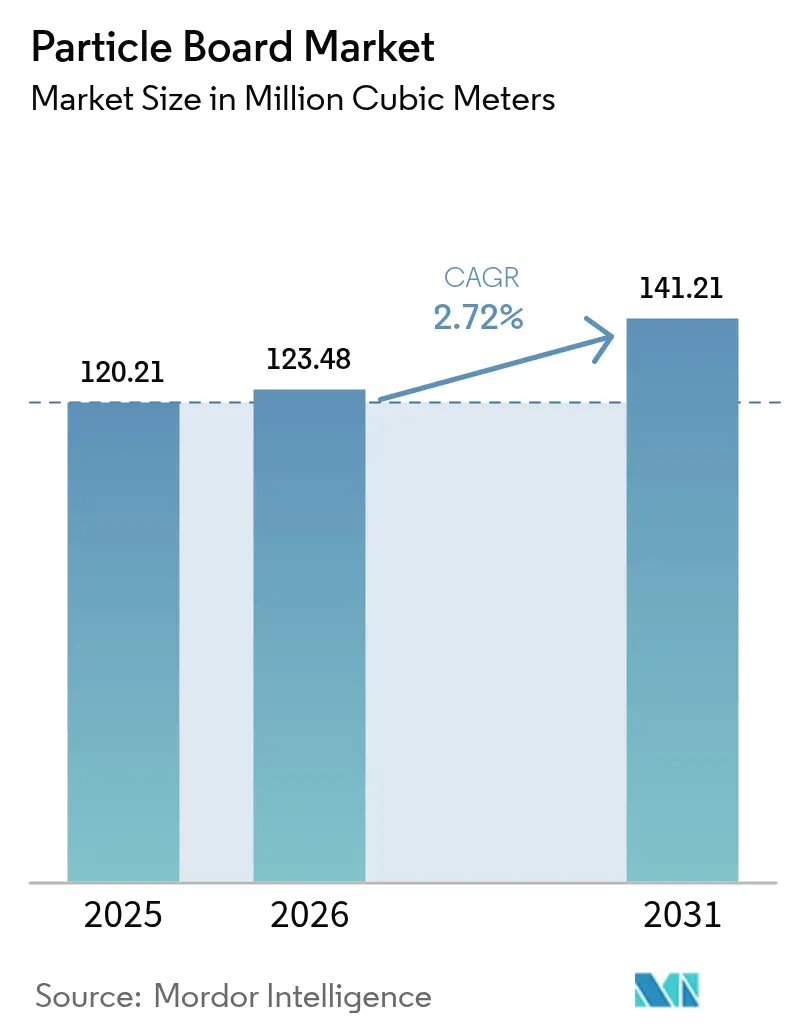

| Market Volume (2026) | 123.48 Million cubic meters |

| Market Volume (2031) | 141.21 Million cubic meters |

| Growth Rate (2026 - 2031) | 2.72% CAGR |

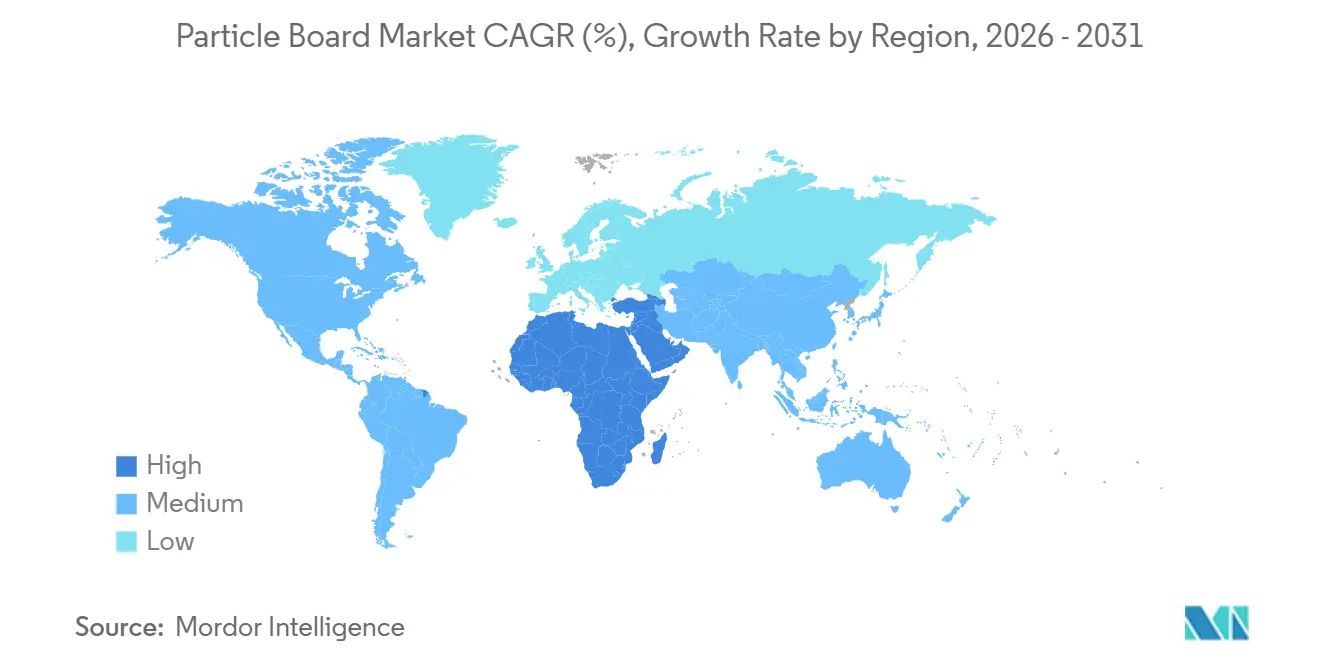

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Particle Board Market Analysis by ���ϲ�����

The Particle Board Market size is expected to increase from 120.21 million cubic meters in 2025 to 123.48 million cubic meters in 2026 and reach 141.21 million cubic meters by 2031, growing at a CAGR of 2.72% over 2026-2031. Capacity additions in China, together with persistent raw-material cost pressure and evolving trade regulations, are shaping a maturing supply base. Wood residue continued to dominate input streams, yet sugar-derived bagasse is capturing incremental share as decarbonization policies shift agricultural by-products into engineered panels. Ready-to-assemble furniture and modular kitchen demand from global retailers sustain core consumption, while low-formaldehyde standards in Europe and North America reward mills that invest in methylene diphenyl diisocyanate adhesive systems. Competitive intensity remains moderate because freight costs limit long-haul trade, and no producer controls more than 8% of global installed capacity, creating space for regional specialists to differentiate through moisture-resistant and non-wood grades.

Key Report Takeaways

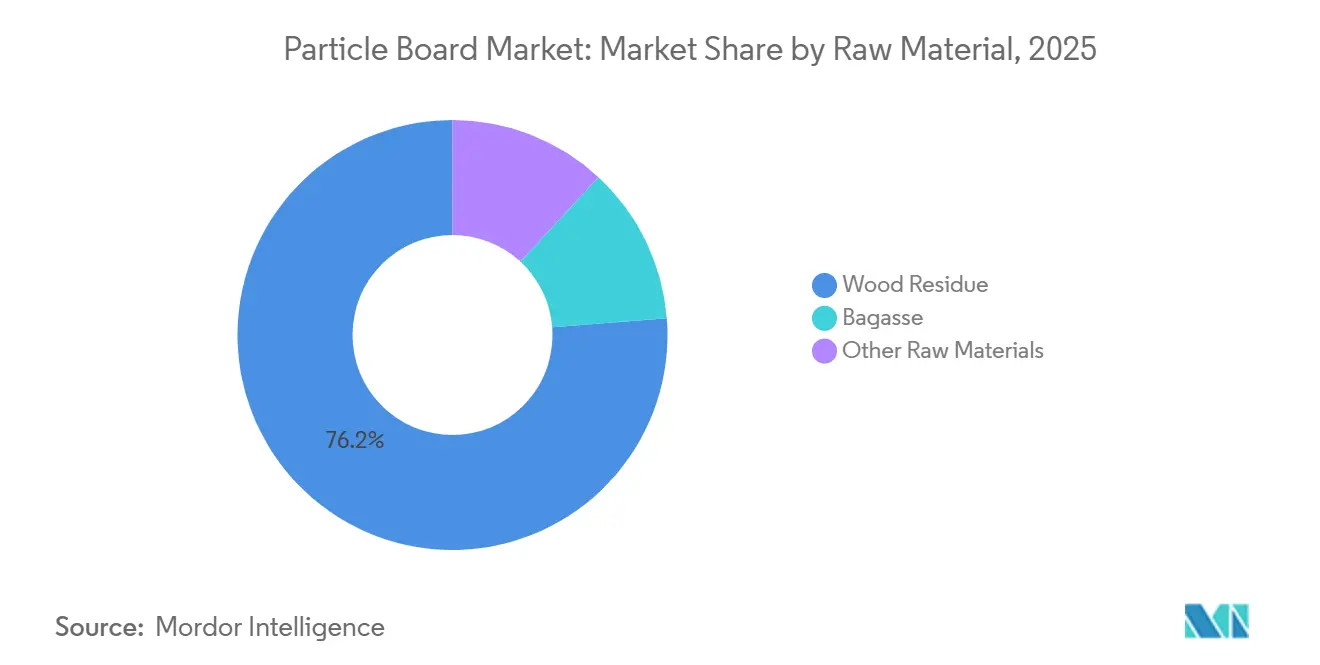

- By the raw material, wood residue captured 76.25% of the particle board market share in 2025, whereas bagasse is projected to advance at a 3.42% CAGR through 2031.

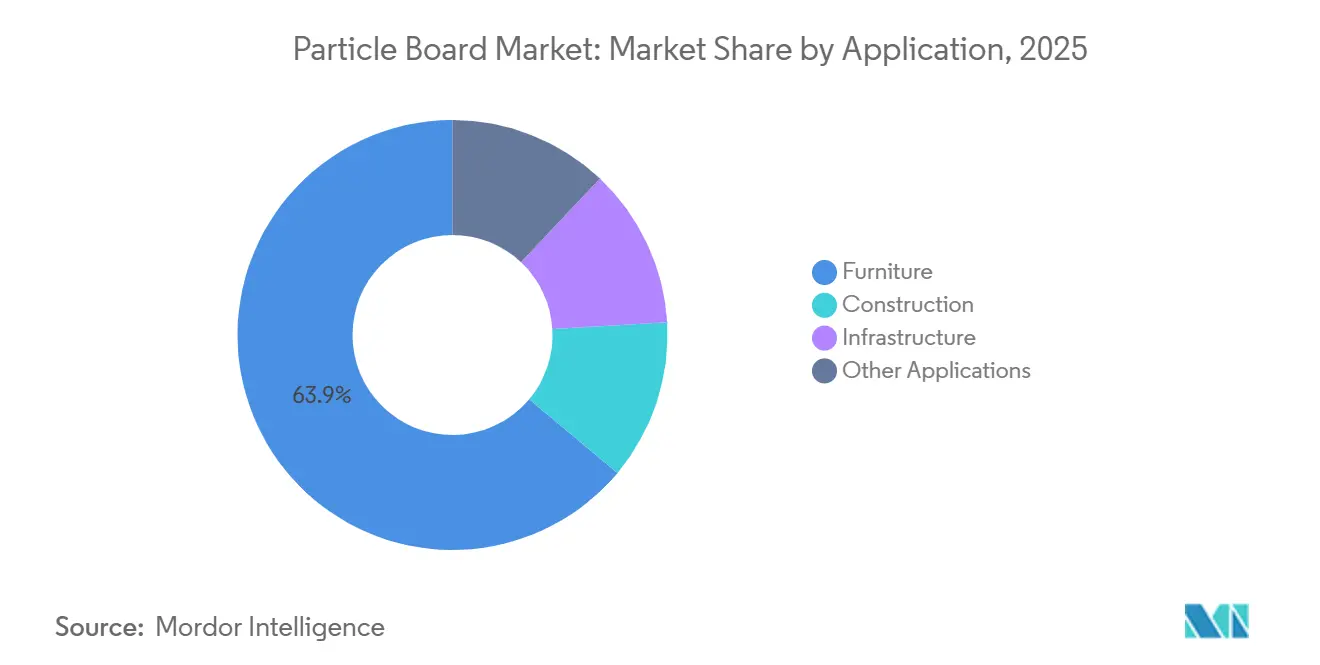

- By application, furniture led with 63.91% revenue share in 2025, while other applications are forecast to expand at a 3.66% CAGR to 2031.

- By geography, Asia-Pacific held 45.44% of the 2025 volume; the Middle-East and Africa recorded the fastest growth trajectory at 3.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Particle Board Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization in tier-2/3 Asian cities spurring affordable housing interiors | +0.8% | Asia-Pacific core (India, China, ASEAN), spill-over to South Asia | Medium term (2–4 years) |

| Cost advantage vs. MDF and plywood in non-load-bearing uses | +0.6% | Global, with highest uptake in price-sensitive markets (India, Southeast Asia, Middle East and Africa) | Short term (≤2 years) |

| Stringent low-formaldehyde rules boosting EU/NA import demand | +0.5% | North America and EU, indirect impact on certified Asian exporters | Long term (≥4 years) |

| Sugar-industry decarbonization freeing up bagasse feedstock | +0.3% | Brazil, India, Thailand, China (sugarcane-producing regions) | Long term (≥4 years) |

| AI-driven continuous-press optimization lifting yields and cut-offs | +0.4% | Global, led by Europe and North America, accelerating in China | Medium term (2–4 years) |

| Source: ���ϲ����� | |||

Rapid Urbanization in Tier-2/3 Asian Cities Spurring Affordable Housing Interiors

As second- and third-tier cities in India, China, and Southeast Asia witness a surge in migration, the demand for budget-friendly interior panels, tailored for apartments, is on the rise. India's Pradhan Mantri Awas Yojana is steering the affordable housing narrative, emphasizing particle board cabinetry and wardrobes[1]Ministry of Housing and Urban Affairs, “Pradhan Mantri Awas Yojana,” Government of India, pmaymis.gov.in. China's urbanization rate is expected to grow further, and provincial capitals are trailing coastal areas in furniture penetration. Vietnamese furniture exports, bolstered by manufacturers shifting from China and capitalizing on EU-Vietnam FTA tariff benefits, saw a significant year-on-year surge. This proximity not only slashes delivered costs compared to MDF but also fuels a cycle of local installations, hastening adoption in nearby urban areas.

Cost Advantage vs. MDF and Plywood in Non-Load-Bearing Uses

Particle board boasts a cost advantage over MDF and plywood, particularly in applications like carcass, shelving, and concealed surfaces. While MDF consumes more electricity for production, particle board's lower energy consumption translates to significant savings. In Vietnam, wage inflation has surged annually, prompting a shift in material choices for drawer bottoms and backs. Although plywood continues to dominate in high-load furniture applications, the introduction of larger-diameter screws, metal inserts, and adhesive-reinforced joints is gradually diminishing plywood's stronghold. This shift is particularly pronounced in markets with volatile currencies, where the price of imported plywood can fluctuate more rapidly than domestic panel costs.

Stringent Low-Formaldehyde Rules Boosting EU/NA Import Demand

In 2025, U.S. consumption outstripped domestic output, a gap that only accredited mills or importers can bridge. Meanwhile, in 2024, German buyers shelled out premiums for E0 panels. Capital-rich Asian manufacturers pivoted to melamine-urea-formaldehyde or MDI systems to stay competitive, while smaller mills opted for domestic markets with more lenient regulations. California's CARB Phase 2, the EPA's TSCA Title VI, and Europe's E0 voluntary regimes have set emission caps between 0.05 and 0.09 ppm, effectively dividing the supply base into certified and non-certified segments.

Sugar-Industry Decarbonization Freeing Up Bagasse Feedstock

In Brazil and India, efficient biomass cogeneration is unlocking millions of tons of bagasse each year. In 2024, Brazilian sugar operations produced bagasse, with a portion deemed surplus and directed towards engineered panels. Similarly, Indian mills, bolstered by an additional cogeneration capacity since 2020, found themselves with an oversupply. This surplus enabled panel producers to source feedstock at a significantly lower cost compared to their wood-residue counterparts. While bagasse panels incur additional resin costs, factoring in discounts on raw materials leads to notable net savings per cubic meter.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile resin and methanol prices squeezing producer margins | -0.5% | Global, most acute in Europe and North America where energy costs are highest | Short term (≤2 years) |

| EU Deforestation Regulation raising compliance costs for Asian mills | -0.3% | Asia-Pacific exporters (China, Indonesia, Vietnam, Malaysia) targeting EU markets | Medium term (2–4 years) |

| Moisture-related swelling limiting exterior applications | -0.2% | Global, particularly in humid climates (Southeast Asia, coastal regions, tropical markets) | Long term (≥4 years) |

| Source: ���ϲ����� | |||

Volatile Resin and Methanol Prices Squeezing Producer Margins

In mid-2024, Europe witnessed a surge in methanol spot quotes before retracting. This volatility pushed urea-formaldehyde prices higher and squeezed EBITDA margins at merchant mills. However, integrated firms like Georgia-Pacific managed to absorb the impact, thanks to their captive chemistry streams. With feedstock concentrated in China, the Middle East, and the U.S. Gulf, geopolitical risks loom large, hinting at an inherently unstable resin economic landscape.

EU Deforestation Regulation Raising Compliance Costs for Asian Mills

Starting December 2024, the EUDR mandates that all wood products entering Europe must verify their origin. This requirement could impose additional costs on mills lacking digital traceability platforms[2]European Commission, “Regulation on Deforestation-Free Products,” europa.eu. While Indonesian and Vietnamese exporters grapple with challenges due to a fragmented residue supply, the 25 largest producers in China are leveraging blockchain ledgers, not only to manage the new requirements but also to seize market share from those struggling.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Wood Residue Dominates, Bagasse Gains Traction

Wood residue delivered 76.25% of 2025 feedstock, confirming its entrenched logistical and process advantages. While the particle board market size for wood residue-based production is set to grow in tandem with the overall panel output, it will gradually yield a portion of its market share to bagasse, projected to grow at a 3.42% CAGR through 2031. Despite this growth, bagasse's global market penetration is expected to stay limited. This limitation arises as seasonal supply challenges compel mills to invest in covered storage and modify resin chemistry.

In India and Brazil, bagasse's adoption is driven by cost savings, with delivered prices significantly lower than wood residue on a dry-weight basis. In Germany and the Netherlands, recycled wood commands a notable share of the particle board market, bolstered by landfill-diversion mandates.

By Application: Furniture Anchors Demand, Infrastructure Niches Expand

Furniture absorbed 63.91% of the 2025 volume, validating the historic linkage between ready-to-assemble formats and the particle board market. While construction made up a significant share, "other applications" are projected to grow at a 3.66% CAGR during the forecast period. In 2024, railway interiors purchased a substantial amount of fire-retardant panels, with projections suggesting this could double by 2028.

Reinforcing feedstock recycling, circular initiatives are making waves; for instance, global circular hubs are reclaiming panels, leading to a reduction in raw-material costs. On the other hand, while automotive trunk liners present a limited opportunity due to the weight of particle boards conflicting with lightweighting goals, there's potential. With density optimization, additional demand could be realized by 2030.

Geography Analysis

Asia-Pacific represented 45.44% of 2025 consumption. China, boasting substantial installed capacity, faces a slowdown in local uptake due to weaknesses in its property sector. Meanwhile, India utilized resources in 2024, catering to both domestic furniture needs and export contracts. ASEAN nations are attracting production shifts from China, bolstered by trade agreements, whereas Japan grapples with dwindling demand due to its aging demographics.

Middle-East and Africa is the fastest-growing region at 3.71% CAGR to 2031. This growth is fueled by Saudi Vision 2030's investment in affordable housing fit-outs. Additionally, South Africa's residential growth in 2024 lends further credence to the region's expansion.

North America represented a notable portion of global volume in 2025. While U.S. housing starts bolstered cabinet demand, a significant supply gap looms, largely due to stringent CARB and EPA regulations. Europe, on the other hand, contributed a considerable share to the global volume, with production hubs in Germany, Poland, and Romania. However, early 2024 saw output curbed in these regions, primarily due to fluctuations in natural gas prices. South America accounted for a smaller share of the global market, with Brazilian mills actively seeking tariff protections against competitively priced imports from China.

Competitive Landscape

The particle board market is moderately fragmented. Scale players are deploying continuous-press automation and captive resin plants to secure cost leadership. Chinese mills installing blockchain traceability systems are positioned to seize share in EUDR-compliant channels. While certification regimes like FSC and ISO 14001 have become essential for entry into European and North American markets, many mills in Asia have yet to achieve these qualifications.

Particle Board Industry Leaders

Kronoplus Limited

ARAUCO

EGGER

West Fraser Timber Co.

Kastamonu Entegre

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Century Plyboards (India) Ltd commissioned India's largest particle board manufacturing facility in Therovy Kandigai near Chennai, Tamil Nadu, with an annual production capacity of 800 cubic metres. The facility aims to meet the increasing demand for engineered wood panels in domestic and international markets.

- November 2024: EGGER invested EUR 200 million (USD 214 million) in its Markt Bibart, Germany particleboard plant for processing recycled wood and producing laminated particleboard. The project features a Timberpak collection site for a consistent recycled wood supply, with initial construction phases underway.

Global Particle Board Market Report Scope

Particle board, also known as chipboard or low-density fiberboard (LDF), is an engineered product made from wood particles, such as sawdust, wood chips, or wood shavings, that are bonded together with a synthetic resin or other adhesive under heat and pressure. The resulting panel is dense, uniform, and relatively inexpensive compared to solid wood or plywood.

The particle board market is segmented by raw material, application, and geography. By raw material, the market is segmented into wood residue, bagasse, and other raw materials. By application, the market is segmented into furniture, construction, infrastructure, and other applications. The report also covers the market size and forecasts for the particle board market in 16 countries across major regions. For each segment, the market sizing and forecasts were made on the basis of volume (cubic metres).

By Raw Material

| Wood Residue |

| Bagasse |

| Other Raw Materials |

By Application

| Furniture |

| Construction |

| Infrastructure |

| Other Applications |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Raw Material | Wood Residue | |

| Bagasse | ||

| Other Raw Materials | ||

| By Application | Furniture | |

| Construction | ||

| Infrastructure | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast will global demand for particle board grow through 2031?

Volume is forecast to increase from 123.48 million cubic meters in 2026 to 141.21 million cubic meters by 2031, reflecting a 2.72% CAGR.

Which region is expected to expand the quickest?

The Middle East and Africa segment should register the fastest 3.71% CAGR due to Saudi infrastructure spending and South African housing growth.

What share of the particle board market comes from furniture uses?

Furniture commanded 63.91% of 2025 volume, maintaining its role as the primary demand engine.

Why is bagasse gaining relevance as a feedstock?

Surplus bagasse from decarbonizing sugar mills costs roughly half as much as wood residue and is growing at a 3.42% CAGR despite storage and resin-adjustment hurdles.

Page last updated on: