Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

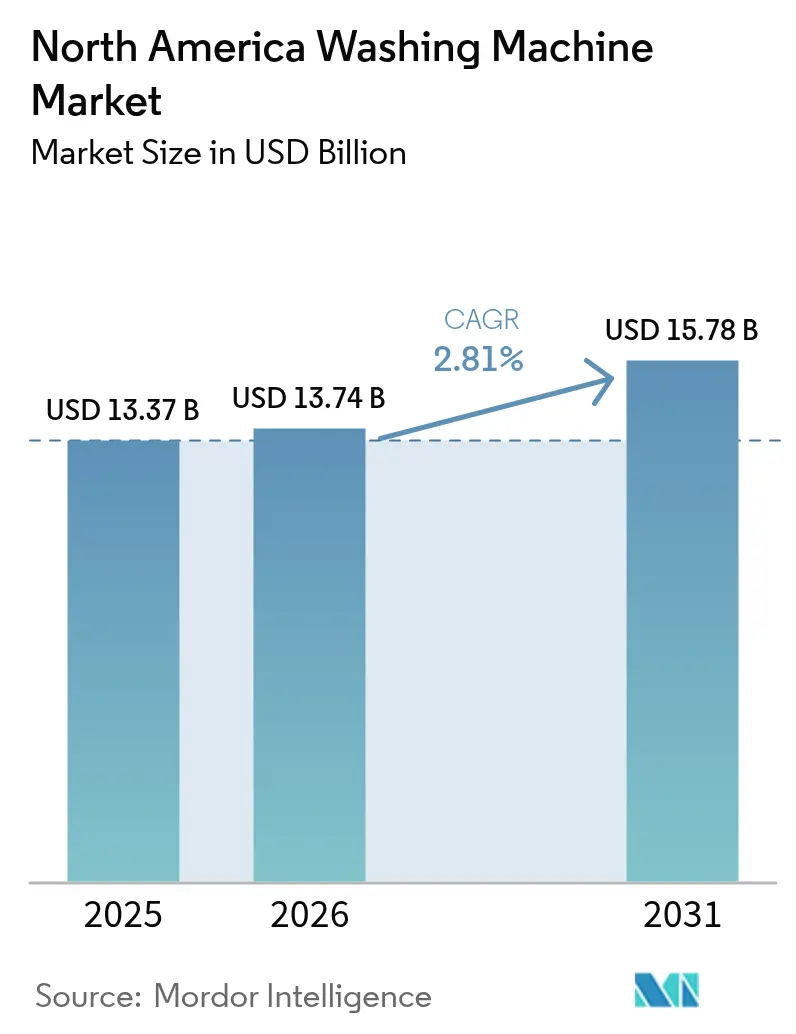

| Base Year Market Size (2025) | USD 13.37 Billion |

| Market Size (2026) | USD 13.74 Billion |

| Market Size (2031) | USD 15.78 Billion |

| Growth Rate (2026 - 2031) | 2.81% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

North America Washing Machine Market Analysis by ���ϲ�����

The North America washing machine market size is expected to increase from USD 13.37 billion in 2025 to USD 13.74 billion in 2026 and reach USD 15.78 billion by 2031, growing at a CAGR of 2.81% over 2026-2031. Replacement demand is intensifying as households prepare for the March 2028 federal efficiency standard, which will make many legacy units non-compliant and push upgrades earlier than planned[1]U.S. Department of Energy, “Home Energy Rebates and Residential Appliance Efficiency,” U.S. Department of Energy, energy.gov. Utility-funded incentives tied to the Inflation Reduction Act’s Home Energy Rebates are shortening payback periods and nudging buyers toward connected, heat-pump-ready models that carry mid-teens price premiums. Front-load penetration is advancing faster than the overall market as California’s Title 20 water rules favor low-Integrated Water Factor designs, while top-loaders retain a wide user base for mid-cycle add-ins and straightforward upkeep. Policy-driven cost volatility has also accelerated reshoring and automation, with leading manufacturers investing in United States plants and digital production systems to reduce lead times and labor-hours-per-unit. Online channels continue to scale on the back of richer pre-purchase tools and faster fulfillment, expanding much faster than stores as buyer journeys move from showrooms to apps.

Key Report Takeaways

- By product type, top-load machines led with 62.54% revenue share in 2025. Front-load units are projected to expand at a 3.81% CAGR through 2031.

- By capacity, 5–8 kg models accounted for a 48.21% share in 2025. Above-8 kg machines are projected to expand at a 4.34% CAGR through 2031.

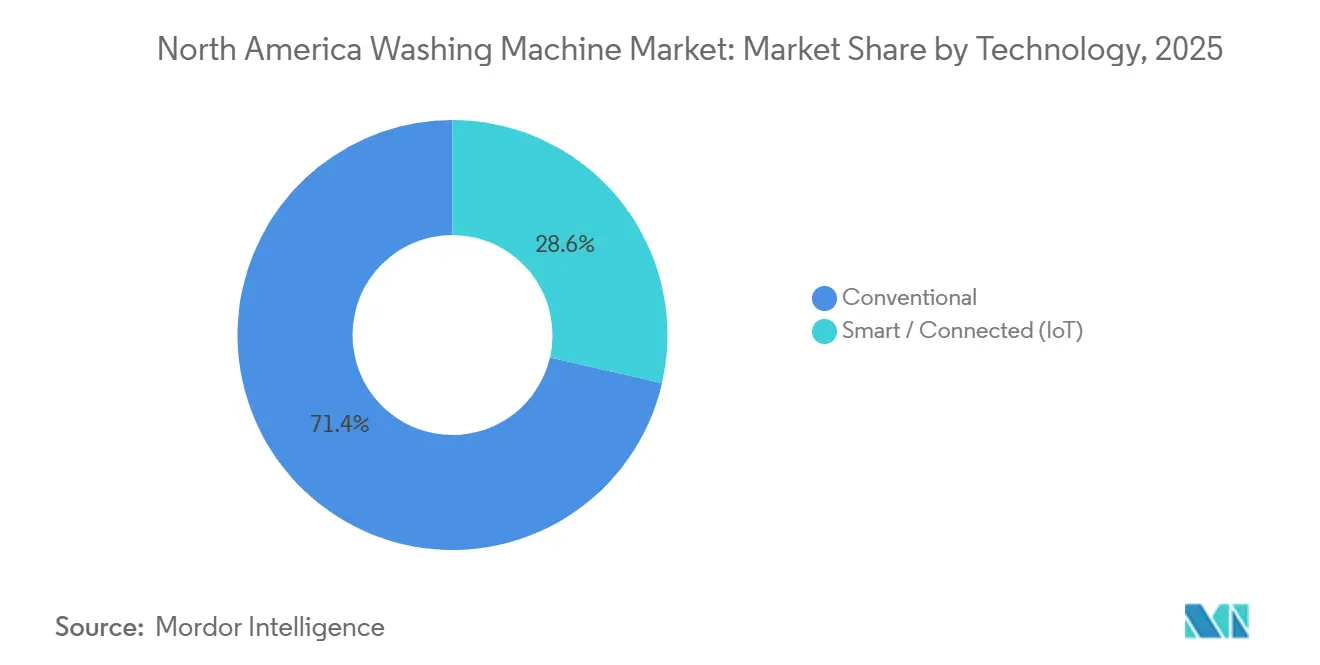

- By technology, conventional washers captured 71.40% share in 2025, and smart/connected (IoT) washers are projected to grow at a 3.90% CAGR through 2031.

- By end user, residential accounted for 80.53% of 2025 revenue. Commercial deployments are projected to expand to a 3.97 % CAGR through 2031.

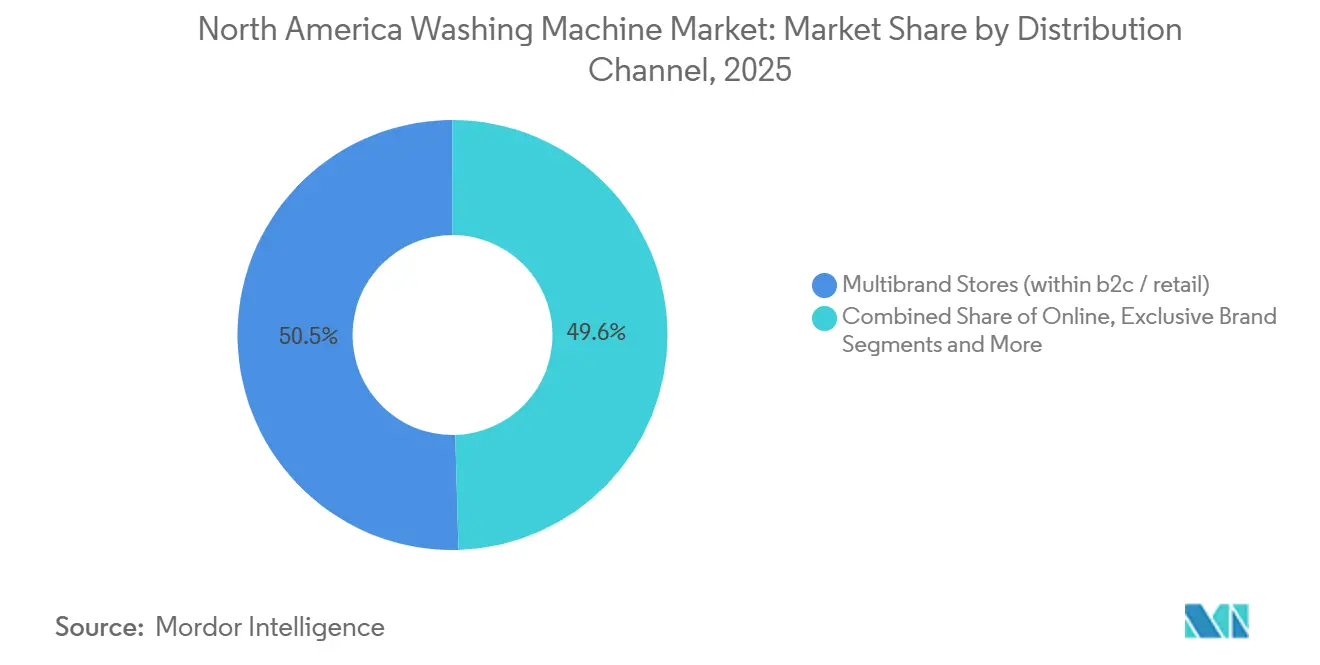

- By distribution channel, multibrand stores accounted for 50.45% of 2025 revenue. Online/digital (within b2c / retail) is projected to expand to a 5.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Washing Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Replacement-driven refresh cycles amid a high installed base | +1.2% | United States, Canada, Mexico | Medium term (2-4 years) |

| Energy and water efficiency mandates and utility rebates | +0.8% | California, Massachusetts, Washington, Oregon, Canada | Short term (≤ 2 years) |

| Smart home ecosystem adoption in laundry | +0.9% | United States metro areas, Canadian urban centers | Medium term (2-4 years) |

| Premiumization and migration to larger capacities | +0.6% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Multifamily building codes favor compact/ventless laundry | +0.5% | United States Sun Belt, Mountain West, Canadian cores | Medium term (2-4 years) |

| OEM nearshoring/reshoring is improving availability and lead times | +0.4% | Mexico, the United States, Kentucky, and Ohio | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Replacement-Driven Refresh Cycles Amid High Installed Base

A large installed base makes North America a replacement-led environment, and the March 2028 federal standard accelerates the timeline for households with older vertical-axis units that will not meet new energy and water thresholds. The compliance shift compresses upgrade cycles for cost-conscious owners who would otherwise defer purchases until failure, especially as non-compliant models face higher operating costs once utilities factor in tighter efficiency benchmarks. The savings gap is material because legacy top-loaders can consume far more energy and water per load compared with current ENERGY STAR front-load designs, a difference that compounds into meaningful annual utility savings for an average home. State-level incentives and utility rebates further pull upgrades forward by lowering out-of-pocket costs and enabling grid-integrated features that adjust cycles to off-peak periods for bill credits. As buyers refresh, they tend to trade up into mid-tier and premium models with inverter motors, AI load-sensing, and connected diagnostics to reduce lifetime ownership costs.

Energy and water efficiency mandates and utility rebates

The 2028 federal standard tightens Modified Energy Factor and Water Factor thresholds, which reshape assortments around compliant front-loaders and higher-spec top-load designs that meet stricter water-use caps[2]U.S. Department of Energy, “Energy Conservation Standards for Consumer Clothes Washers,” Federal Register, federalregister.gov. California’s Title 20 continues to favor low-Integrated Water Factor machines, pushing brands to invest in low-water drum geometries, recirculation pumps, and optimized rinsing to hit state thresholds while protecting cleaning performance. Manufacturers are reallocating engineering resources to accelerate efficiency improvements and fabric-care outcomes within the new limits, signaling a lasting portfolio tilt to water- and energy-optimized configurations. OEM AI features that modulate drum speeds by fabric type and soil load are also helping reduce water and energy use per cycle without sacrificing wash quality, a priority in drought-sensitive regions. Utilities are rewarding grid-interactive functionality with annual bill credits, which benefits connected washers that can schedule or delay starts to avoid peak periods. Canadian regulatory alignment with United States timelines reduces cross-border SKU fragmentation for brands operating in both markets and speeds the retirement of low-efficiency designs.

Smart Home Ecosystem Adoption in Laundry

Smart home ecosystem adoption drives connectivity premiums and aftermarket revenue. Interoperability advances like Matter 1.3 have removed app and ecosystem friction, enabling washers to coordinate with other home devices and energy systems through unified standards. Leading OEMs have committed to Matter-ready roadmaps, which support cross-device orchestration, such as delaying a wash while a paired water heater completes its drawing or shifting to off-peak utility windows. Predictive maintenance has emerged as a key benefit as platforms analyze vibration and water-draw patterns to flag bearing wear and other issues before failure, which reduces emergency service calls and enhances uptime for busy households. Commercial operators are extending these gains at scale through networked fleets that monitor cycles, error codes, and machine health, which optimizes preventive maintenance and asset allocation across locations. As module costs decline, connected features are cascading from flagship machines into mainstream models, improving the value equation for buyers who expect remote control, alerts, and app-based guidance as standard.

Premiumization and migration to larger capacities

Above-8 kg machines are growing faster than the overall market as large households and commercial operators consolidate loads to reduce water and energy use per kilogram washed. AI load-sensing allows larger drums to right-size water levels, which removes the historical penalty for running a big washer with a small load and encourages buyers to step up in capacity. Hygiene features such as steam cycles and targeted spray patterns have moved into mid-premium price bands, appealing to time-pressed users who prioritize thorough cleaning and shorter total cycle times[3]LG Electronics, “AI Direct Drive Technology Overview,” LG Electronics, lg.com. Premium combo units that sequence wash-to-dry in a single cabinet are gaining traction in space-constrained homes, where stackable pairs are not feasible or where venting is restricted. As these capabilities expand, capacity-led upgrades and premium feature bundles are likely to sustain higher average selling prices even as unit growth remains anchored in replacements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mature, Replacement-Heavy Demand Caps Unit Growth | -0.7% | United States, Canada | Long term (≥ 4 years) |

| Housing Market and Interest-Rate Sensitivity | -0.4% | United States, Canada | Medium term (2-4 years) |

| Tariffs/Trade Remedies Elevate Appliance Prices | -0.5% | United States, Canada | Short term (≤ 2 years) |

| Rising Repair Costs Extend Replacement Cycles | -0.3% | United States, Canada | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Tariffs and Trade Remedies Elevate Appliance Prices

Trade actions have raised the embedded cost of imported washers and subassemblies, including the June 2025 expansion of Section 232 coverage to steel-equivalent content within finished appliances[4]U.S. Department of Commerce, “Section 232 Steel Measures and Downstream Coverage,” U.S. Department of Commerce, commerce.gov. Per-unit landed costs rose for affected imports, which pressured entry-tier price points and prompted brands to accelerate United States production for select models to reduce duty exposure and ocean-freight uncertainty. Large manufacturers responded by committing new capital to North American lines and by installing advanced automation to offset labor-hours-per-unit and stabilize margins despite raw material inflation. These shifts help shorten lead times and reduce inventory risk but also require multi-year execution, which means pricing remains sensitive to input costs and policy changes in the near term. The combined effect steers the North America washing machine market toward a wider spread between premium and entry segments as cost pass-through varies by model mix and channel.

Mature, Replacement-Heavy Demand Caps Unit Growth

A high household penetration rate across the region keeps the sales base weighted to replacements, which inherently caps unit expansion even when macro conditions are favorable. Improved reliability from inverter and direct-drive motors extends ownership cycles, reducing the frequency of failure-driven purchases and aligning upgrades more closely with regulatory milestones and utility incentives. Smart diagnostics from leading platforms resolve a growing share of issues without an in-person visit, which further extends usable life for machines that might otherwise have been retired prematurely. Over time, OEMs offset slower unit velocity by raising average selling prices through capacity, fabric care, and connectivity features that compress cycle time and improve results for busy households. The result is steady revenue growth that outpaced units as buyers trade up within the North America washing machine market rather than expanding the installed base materially.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Agitator Familiarity Sustains Top-Load Dominance, While Front-Load Efficiency Gains

Top-load machines anchored 62.54% of revenue in 2025, reflecting user preference for mid-cycle add-ins, shorter cycles, and simpler maintenance. California’s Title 20 water-use standards and the federal 2028 rule are tilting assortments toward compliant designs, which benefits front-loaders with lower Integrated Water Factor profiles and encourages top-load reengineering for water efficiency. Many buyers still prefer the familiar ergonomics and user flow of vertical-axis washers for heavy, frequent loads, so brands emphasize anti-tangle agitation and stronger rinsing to preserve perceived cleaning power in lower-water formats. Smart features that automate detergent dosing, cycle selection, and off-peak scheduling are also lifting willingness to pay across both formats, since remote control and alerts reduce time costs in laundry routines. As this mix evolves, front-load units are growing at a 3.81% CAGR through 2031, outpacing the overall North America washing machine market as regulations and incentives support better water productivity at the household level.

The North America washing machine market continues to support both formats because value-seeking households often gravitate to top-loaders while premium and eco-focused segments move to front-loaders with advanced drum control and sensors. OEM platforms now sync washer starts with smart thermostats or water heaters to mitigate peak demand and capture grid incentives where available, which further differentiate connected front-load flagships. At the same time, new top-load designs that comply with tighter water factors offer a path to preserve a large legacy base without forcing a format switch for buyers focused on familiarity and unit price. Twin-tub and semi-automatic formats persist as niche solutions in select sub-regions but are ceding ground as fully automatic machines with inverter motors become more affordable. With policy tailwinds and ongoing product improvements, format choice is becoming less about sacrifice and more about a clear tradeoff between price, ergonomics, and connectivity within the North America washing machine market.

By Capacity: Mid-Tier 5–8 kg Balances Household Needs, While Jumbo Units Gain

Load consolidation models in the 5–8 kg band hold a 48.21% share in 2025, underlining their fit for three-to-four-person households that want one-load-per-week convenience without higher utility draw, while larger drums are winning with big families and commercial operators. AI-driven load-sensing is central to this balance because it right-sizes water and agitation even in bigger drums, which makes the step-up in capacity feel efficient rather than wasteful in everyday use. The appeal of jumbo drums is growing in homes that batch laundry to reclaim weekend time and in small businesses that care about water and labor savings per kilogram washed. North America washing machine market size for above-8 kg units is projected to expand to a 4.34% CAGR between 2026 and 2031 as multigenerational living and commercial refresh cycles support larger capacities in core assortments. Meanwhile, mid-capacity designs continue to dominate volume because they match the constraints and habits of most homes that want a balanced footprint, speed, and cost.

Premium feature migration strengthens this pattern across capacity tiers. Connected platforms suggest cycle presets based on fabric mixes and soil levels, which helps prevent overwashing and protects garments while keeping rinse quality predictable in larger drums. Hygiene add-ons such as steam or targeted spray patterns have moved beyond flagship models, reinforcing the sense that capacity upgrades also deliver better results and fewer rewash cycles when households are pressed for time. Combo units that finish wash-to-dry under a coordinated program are expanding options for condos and accessory dwelling units where a second laundry zone is not feasible. As these improvements standardize, the North America washing machine industry is likely to keep tilting toward higher-capacity drums in the USD 1,200–2,000 bracket, while mid-capacity remains the workhorse for mainstream budgets. The result is a durable two-track capacity mix that supports both value and premium growth paths in the North America washing machine market.

By Technology: Conventional Machines Sustain Growth Through Cost-Efficiency and Reliability, While Smart Penetration Faces Adoption Barriers

Conventional washing machines held 71.40% of revenue in 2025, and smart/connected (IoT) models are projected to grow at a 3.90% CAGR through 2031. Whirlpool’s Load & Go dispenser, which auto-doses detergent for 40 cycles without Wi-Fi, shows how convenience features can land at conventional price points and strengthen value perception for cost-focused buyers. Rural and suburban households, which represent 45% of United States residences, often lack consistent broadband at 25 Mbps or higher, so reliability and total cost of ownership take priority over connectivity, keeping conventional machines as the default outside major metros. On-device intelligence also bridges the gap, since models like Samsung’s April 2025 top-load launch optimize cycles locally and can cut energy use by 20% without an internet connection, which makes “conventional” feel smarter without adding subscription or app complexity.

Smart and connected washers are estimated to grow at a 3.90% CAGR through 2031, trailing conventional units due to cybersecurity concerns, app fragmentation, and price premiums that limit mass-market uptake. Matter 1.3 eased interoperability across major platforms in 2025, yet connectivity on its own remains a weaker purchase trigger than energy savings or proven care outcomes for most households. Utility incentives are starting to shift the math, since programs like National Grid’s ConnectedSolutions pay USD 25 to 75 per year for eligible demand-response enrollment, though participation remains below 12% in many qualifying zip codes. Commercial fleets show clearer returns because connectivity supports dynamic pricing and predictive maintenance at scale, with large networks shifting 12% of cycles to off-peak windows to capture bill credits and improve utilization.

By End User: Residential Anchors Volume, While Commercial Drives Feature-Rich Upgrades

Residential accounted for 80.53% of 2025 revenue, reflecting a very high installed base and replacement-heavy dynamics as owners cycle out aging units and upgrade in response to efficiency standards. The 2028 federal rule makes non-compliant models more expensive to operate, which nudges many households to move sooner to ENERGY STAR-grade machines with better water and energy profiles. This effect supports mid-tier and premium upgrades that offer inverter motors, enhanced rinsing, and basic connectivity without steep jumps in price, particularly in areas with stronger utility rebates. North America washing machine market size for commercial deployments is projected to expand at a 3.97% CAGR through 2031 as property managers and laundromat operators modernize fleets for lower total cost per cycle. Connected dashboards and machine-health analytics reduce downtime and enable dynamic pricing to shift demand off-peak in busy facilities.

Hospitality, healthcare, and multifamily operators are also pushing fabric-care and hygiene upgrades because faster, more consistent cycles free staff time and improve asset utilization. Commercial systems that aggregate cycle counts, errors, and revenue per machine allow portfolio-level optimization and planned maintenance that cuts emergency dispatches. In residential, smart diagnostics reduce service calls and keep older machines in circulation longer, which moderates unit growth but opens new avenues for OEM service and consumables revenue. The combination of compliance-driven refresh and feature-led trade-ups supports steady revenue expansion, even as volumes reflect a mature, replacement-oriented base. These demand contours will continue to shape assortments and price ladders across the North America washing machine market through 2031.

By Distribution Channel: Multibrand Stores Leverage Consultative Selling and Floor Demos, While Online Pure-Plays Exploit Price Transparency and Next-Day Delivery

Multibrand retailers remain the primary path to purchase in 2025, with 50.45%, because shoppers value side-by-side comparisons, live cycle demos, and BOPIS options that simplify fit checks and installation timing. These stores justify modest price premiums by bundling consultative selling with delivery, haul-away, and installation support that reduces post-purchase friction for complex laundry setups. Expanded distribution-center networks and tighter last-mile coordination have shortened delivery windows, which helps convert replacement purchases that are often time sensitive. In-store teams also guide value-focused shoppers to floor models and open-box units, clearing inventory while meeting budget targets without sacrificing core performance. Exclusive brand showrooms and experience centers reinforce premium positioning by demonstrating care outcomes and long-term ownership benefits in person, which supports higher ticket prices where hands-on proof matters. The coming 2028 federal efficiency standard and state-level rules increase the importance of in-person compliance guidance and installation verification, which favors brick-and-mortar for regulated markets that require clear documentation and setup confidence at the point of sale.

Online B2C channels are expanding at a 5.34% CAGR through 2031 as buyers lean on augmented-reality visualizers, fit-check tools, and fast financing workflows that streamline decisions and reduce returns linked to size or venting constraints. Prepurchase configurators and guided comparisons replicate key elements of the showroom experience, while transparent delivery windows and install add-ons make web checkout viable for more complex laundry rooms. OEM apps such as Samsung SmartThings add energy-cost projections and usage insights that strengthen online evaluations and help households plan around utility rates. Despite these gains, some buyers still prefer store-led journeys for installation-heavy projects, which keeps consultative retail relevant as a complement to digital research and ordering. On the professional side, commercial and multifamily operators often purchase through direct contracts that bundle equipment, maintenance, and consumables to maximize uptime and predictability over multi-year terms. As adoption matures, omnichannel paths dominate, with discovery and financing online and pickup or installation through stores, prompting equal investment in digital tooling and physical showrooms across the North America washing machine market.

Geography Analysis

The United States anchors the North America washing machine market with the largest installed base and a rising cadence of replacements tied to the 2028 federal efficiency standard. California’s Title 20 framework has been a major factor in the pivot toward lower water-use machines, reinforcing the shift to front-load designs and optimized top-loaders that meet state thresholds. Developers in Sun Belt metros are specifying in-unit laundry at higher rates to support rent premiums, which helps compact and ventless solutions gain ground in new-build multifamily projects. United States-based capacity investments by large brands are designed to reduce imported content, lower lead times, and bring cost control closer to home amid tariff and freight volatility. As connected features and grid incentives spread, United States buyers continue to migrate to models that coordinate with home energy systems and off-peak schedules.

Canada’s regulatory alignment with the United States timelines through Natural Resources Canada simplifies cross-border assortments and reduces the need for market-specific SKUs that fragment inventory. ENERGY STAR preferences remain high among Canadian buyers, who often prioritize cold-wash performance, winter-grade reliability, and compact, ventless dryer pairings in urban cores. Provinces with building-performance goals and municipal utility incentives are also shifting procurement toward connected washers that can participate in demand-response programs. As a result, connected mid-premium assortments are expanding in major metro areas, while mainstream households continue to favor dependable, efficient models with basic app functionality. This balance keeps Canada’s profile focused on premium efficiency, fabric care in cold-water cycles, and floorplan flexibility for condos and rental stock.

Mexico benefits from its central role in regional manufacturing, duty-free flows under USMCA, and rising domestic demand in growing metro areas that favor stackable or compact formats. Major OEMs operate plants in industrial hubs that serve both local buyers and export programs, which support rapid model refreshes and responsive inventory for the broader region. Space constraints in large cities support front-load and combo designs, while suburban expansion sustains value-oriented top-loaders that emphasize ease of use and reliability. As utility incentives and building codes evolve, connected features and filtration-ready designs are likely to expand in new residential projects and commercial laundries. Nearshoring continues to be a key advantage for time-to-market and cost control across the North America washing machine market.

Competitive Landscape

Scale and platform breadth define competition in the North America washing machine market, with Whirlpool, LG, Samsung, GE Appliances, and Electrolux leading on brand reach, R&D, and channel depth. Whirlpool emphasizes domestic manufacturing as a margin and agility anchor, citing high United States-content ratios that hedge tariff risk and enable faster model rollouts. GE Appliances is investing in a major Kentucky expansion that will consolidate front-load production, bring additional models under one roof, and cut ocean-freight exposure, along with long lead times. Korean brands compete with AI-driven fabric detection, ecosystem integrations, and user-experience features that justify mid-teens premiums in connected lineups. In commercial laundry, Alliance Laundry Systems builds on networked management and service ecosystems that deliver measurable uptime and revenue optimization at laundromats and in multifamily buildings.

Product roadmaps center on connectivity, grid readiness, and care outcomes. Matter 1.3 compatibility across leading brands has collapsed interoperability barriers, allowing washers to coordinate with home energy systems for bill credits and sustainability goals. Predictive maintenance is now a differentiator in both residential and commercial fleets, lowering emergency service calls and strengthening brand loyalty through proactive alerts and remote diagnostics. Feature bundles such as steam, targeted sprays, and refined drum geometries are broadening to mid-premium price bands, pulling adoption forward among time-stretched households. OEMs are also preparing for microfiber filtration and evolving water rules by designing filter-ready housing and retrofit paths that can adapt to future mandates without disrupting installed bases.

Capital deployment underscores a pivot to regional resilience. United States plant expansions and automation projects reduce labor-hours-per-unit, enable rapid compliance updates, and insulate product timelines from ocean-freight disruption. Manufacturers with robust North American footprints can localize designs for California and Canadian thresholds and iterate quickly on firmware and IoT integrations. As connected features become table stakes in mid-tier lineups, the basis of competition shifts to orchestration quality, diagnostic depth, and service ecosystems that extend usable life at lower cost. This dynamic reinforces the advantage for players with strong software, data, and field-service integration in the North America washing machine market.

North America Washing Machine Industry Leaders

Whirlpool Corporation

GE Appliances (a Haier company)

Electrolux Group (Frigidaire)

LG Electronics

Samsung Electronics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Whirlpool Corporation committed USD 300 million to expand its Clyde and Marion, Ohio, laundry plants, adding 400–600 jobs and increasing next-generation washer and dryer capacity by 25%.

- August 2025: GE Appliances unveiled a historic USD 3 billion, five-year plan to expand United States manufacturing, workforce, and communities across 11 domestic plants, targeting 1,000 new jobs in five states. The initiative includes modernizing production lines for air conditioning, water heating, and laundry, with advanced automation expected to increase output 30% while reducing labor-hours-per-unit.

- June 2025: GE Appliances announced a USD 490 million investment to establish a front-load washer manufacturing facility in Louisville, Kentucky, creating 800 new jobs and consolidating production of the GE Profile UltraFast Combo Washer/Dryer and over 15 washer models domestically. The new lines, slated to open in 2027, will incorporate automation, robotics, and in-house metal stamping to cut lead times from 45 days to under five days, positioning GE as the largest United States washer manufacturer.

- March 2025: Samsung Electronics launched a 27-inch Vented Combo washing machine tailored for the North American market, featuring AI Optiwash & Dry, an Auto Open Door, and an Easy Lint Clean filter. The model's extended soak times and vented drying method address multigenerational household needs.

North America Washing Machine Market Report Scope

A washing machine is an electronic home appliance that is used to wash various types of clothes without applying any physical effort. A complete background analysis of the North America Washing Machine Market, which includes an assessment of the emerging trends by segments and regional markets, significant changes in market dynamics, and market overview, is covered in the report.

The North America Washing Machine Market is segmented by product type, capacity, technology, end user, distribution channel, and geography. By product type, the market is divided into front-load, top-load, and twin-tub washing machines. The front load segment is further divided into with dryers and without dryers, while the top load segment is further categorized into with dryers and without dryers. By capacity, the market is categorized into below 5 kg, 5–8 kg, and above 8 kg. By technology, the market is segmented into conventional and smart/connected (IoT) washing machines. By end user, the market is divided into residential and commercial segments. By distribution channel, the market is segmented into B2C/retail and B2B/directly from manufacturers. The B2C/retail segment is further divided into multi-brand stores, exclusive brand outlets, online, and other distribution channels. Geographically, the market analysis covers the United States, Canada, and Mexico. The report provides market size and forecasts for the North America washing machine market in value (USD) across all the above segments.

By Product Type

| Front Load | With Dryers |

| Without Dryers | |

| Top Load | With Dryers |

| Without Dryers | |

| Twin Tub |

By Capacity

| Below 5 kg |

| 5 – 8 kg |

| Above 8 kg |

By Technology

| Conventional |

| Smart / Connected (IoT) |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C / Retail | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B / Directly from the Manufacturers |

By Geography

| United States |

| Canada |

| Mexico |

| By Product Type | Front Load | With Dryers |

| Without Dryers | ||

| Top Load | With Dryers | |

| Without Dryers | ||

| Twin Tub | ||

| By Capacity | Below 5 kg | |

| 5 – 8 kg | ||

| Above 8 kg | ||

| By Technology | Conventional | |

| Smart / Connected (IoT) | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C / Retail | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Directly from the Manufacturers | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the current size and projected growth of the North America washing machine market?

The North America washing machine market is projected to rise from USD 13.37 billion in 2025 to USD 15.78 billion by 2031 at a 2.8% CAGR.

How will the 2028 United States efficiency standard affect replacement demand?

The 2028 federal rule makes many older washers non-compliant, pulling forward replacements as owners seek compliant models with lower operating costs.

Which product format is growing fastest and why?

Front-load units are growing at a 3.81% CAGR due to water and energy advantages under state and federal efficiency rules, while top-loaders still lead on installed base.

What are the fastest-growing capacity tiers in North America?

Above-8 kg machines are expanding at a 4.34% CAGR as larger households and commercial operators consolidate loads to save time and resources.

How quickly are online channels growing for laundry appliances?

Online sales are projected to grow at an 5.34% CAGR through 2031 as AR tools, faster delivery, and easy financing streamline purchases.

What role do connected features play in purchasing decisions now?

Interoperability and predictive maintenance are becoming must-have features because they cut energy costs, prevent failures, and improve daily convenience.

Page last updated on: