North America Luxury Appliances Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

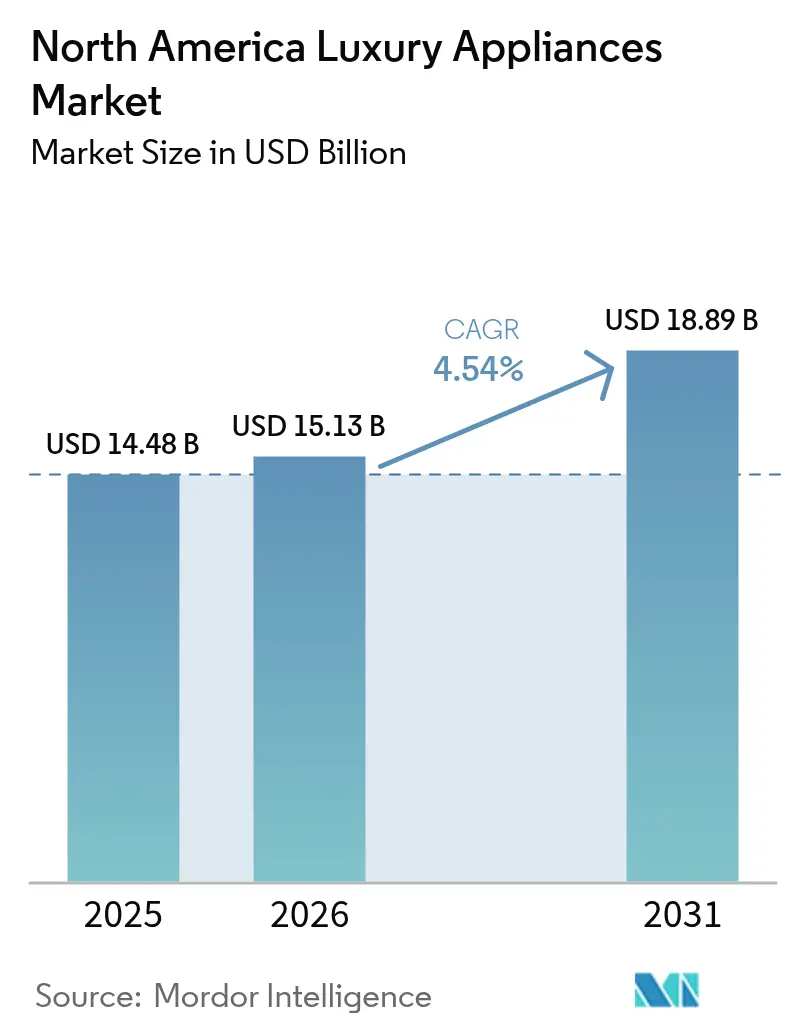

| Base Year Market Size (2025) | USD 14.48 Billion |

| Market Size (2026) | USD 15.13 Billion |

| Market Size (2031) | USD 18.89 Billion |

| Growth Rate (2026 - 2031) | 4.54% CAGR |

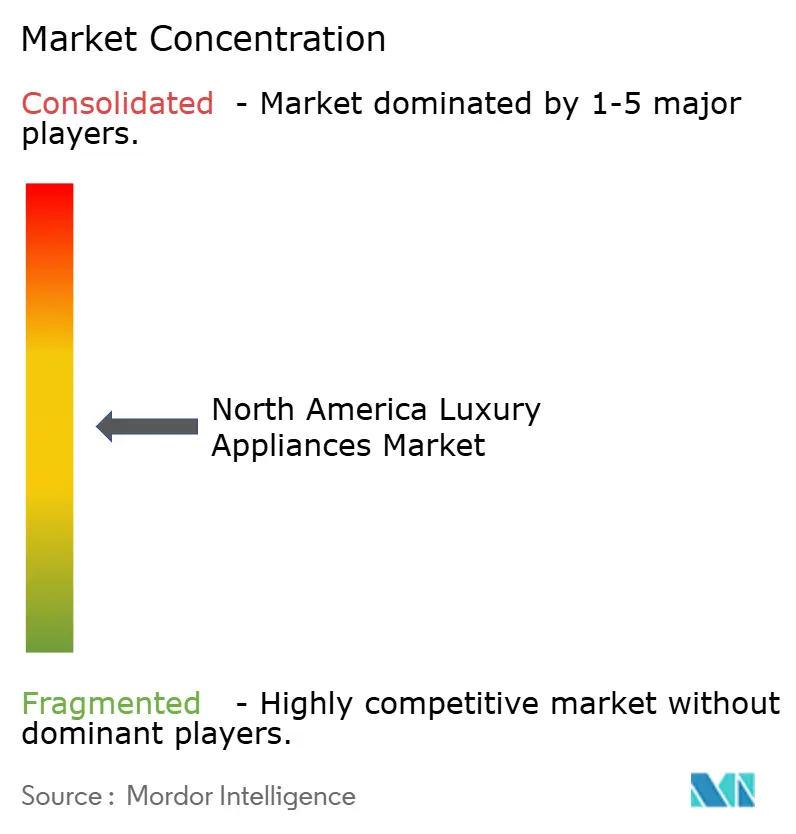

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

North America Luxury Appliances Market Analysis by ���ϲ�����

The North America luxury appliances market size is projected to expand from USD 14.48 billion in 2025 and USD 15.13 billion in 2026 to USD 18.89 billion by 2031, registering a CAGR of 4.54% between 2026 to 2031. Demand strength concentrates in refrigerators and other premium built-in kitchen suites as brands scale AI-enabled features, panel-ready designs, and integrated ecosystem controls across price tiers, which is lifting replacement intent among affluent renovators in key metro clusters. Policy incentives for electrification, particularly rebates that support induction cooking and heat-pump adoption, continue to stimulate premium electric upgrades in states with active program rollouts, which sustains momentum despite macro headwinds. United States affordability constraints and skilled-install bottlenecks remain the core friction points for built-in and induction adoption, although easing rate expectations and transaction-driven remodels help backfill demand for curated, high-spec kitchens. Competitive intensity is rising as incumbents and mass-premium players deploy conversational AI, computer vision, and predictive maintenance to elevate user experience, differentiating through both design customization and connected-service ecosystems that reduce ownership friction. Within the North American luxury appliances market, brands are also amplifying showroom experiences to guide complex purchase journeys while maintaining dealer partnerships that deliver white-glove installation and after-sales support in major United States and Canadian metros.

Key Report Takeaways

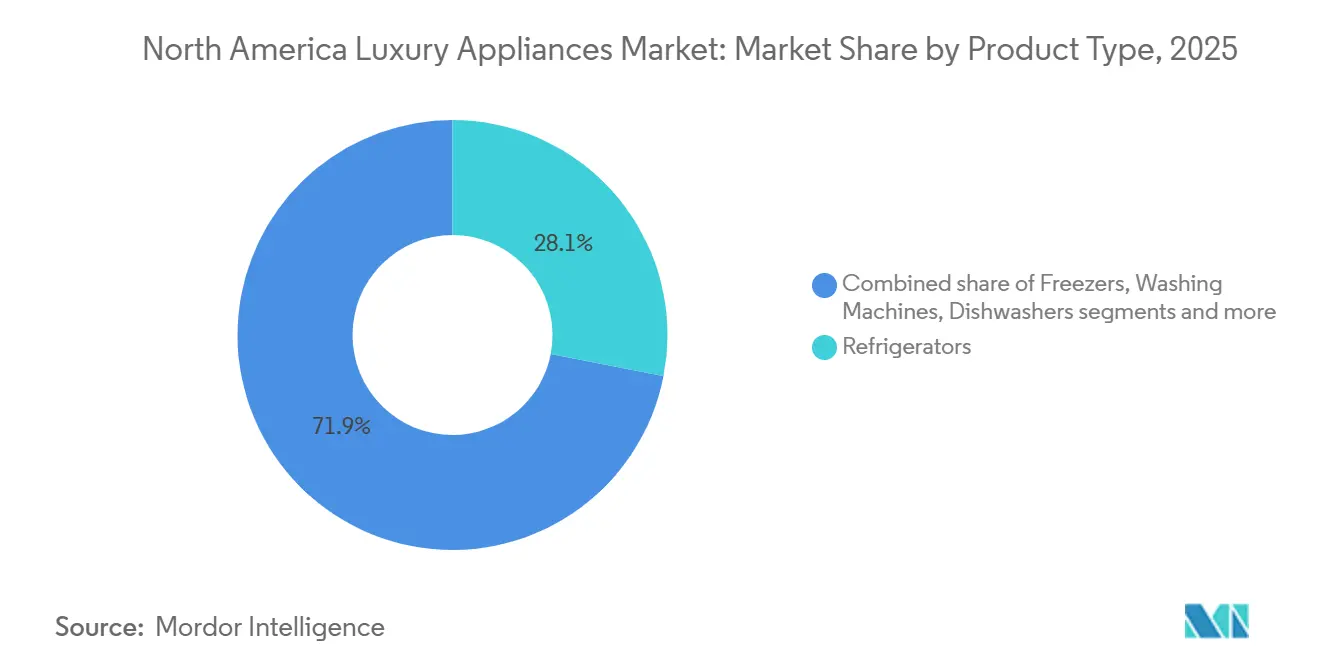

- By product type, refrigerators led the North American luxury appliances market with 28.06% revenue share in 2025, while dishwashers are projected to be the fastest growing at a 5.78% CAGR through 2031.

- By installation type, freestanding models held 83.61% of 2025 volume in the North American luxury appliances market, and built-in plus integrated units are forecast to grow at a 4.88% CAGR over 2026-2031.

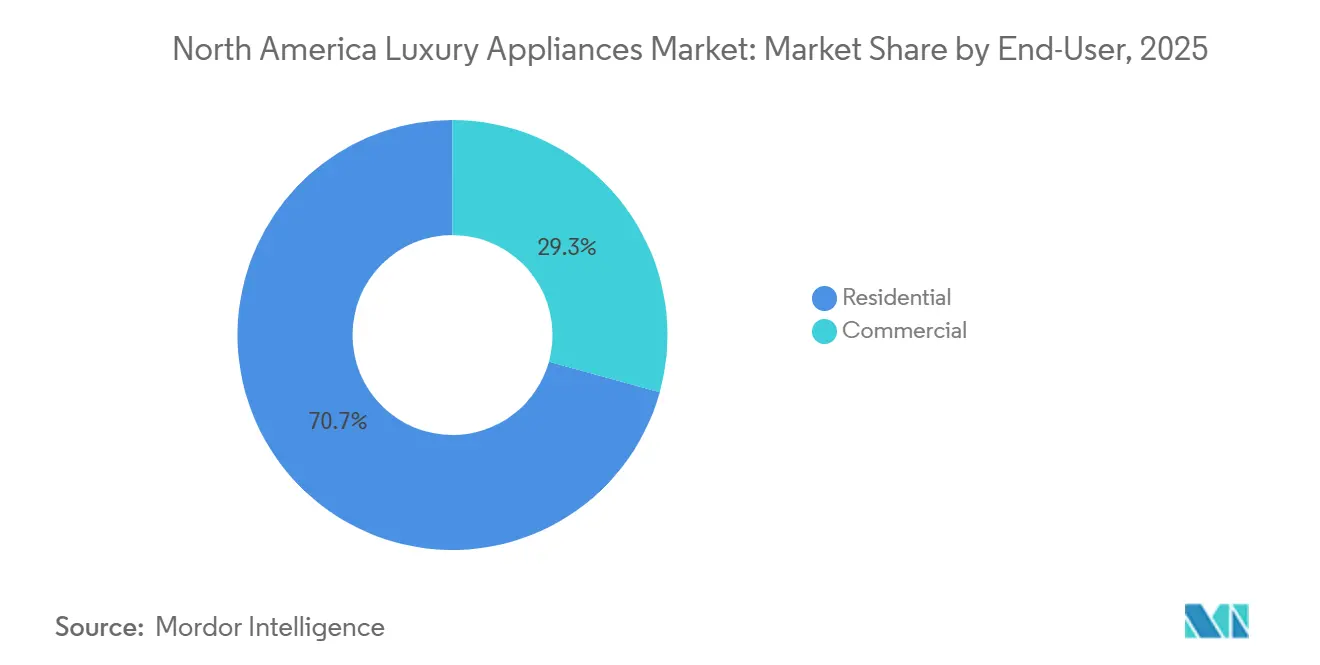

- By end-user, the North American luxury appliances market was led by residential with 70.71% of demand in 2025, while the commercial segment is projected to expand at a 5.62% CAGR through 2031.

- By distribution channel, B2C retail accounted for 75.73% of sales in 2025 within the North American luxury appliances market, and B2C retail is projected to grow at a 5.08% CAGR through 2031.

- By geography, the United States captured a 76.40% share in 2025 in the North American luxury appliances market, while Mexico is expected to be the fastest-growing at a 5.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Luxury Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and Smart, Design-Led Upgrades | +1.2% | Global, concentrated in U.S. coastal metros and Canadian urban centers | Medium term (2-4 years) |

| Built-In and Integrated Kitchens Expanding Attach Rates | +0.9% | North America, strongest in the U.S. and Canada, open-concept housing | Medium term (2-4 years) |

| Remodeling and Replacement Cycles Sustain Demand | +0.7% | United States and Canada, tied to housing turnover rates | Short term (≤ 2 years) |

| Accelerating Shift to Induction/Electrification | +1.1% | National, with early gains in California, New York, Pacific Northwest | Long term (≥ 4 years) |

| IRA-Linked Electrification Rebates Spur Premium Electric/Heat-Pump Adoption | +0.8% | United States, state-by-state rollout, strongest in California, New York, Colorado | Short term (≤ 2 years) |

| Outdoor Luxury Kitchens (Undercounter, Wine, Ice) Broaden Appliance Scope | +0.4% | Sunbelt states, California, Texas, Florida; spillover to Mexico resort markets | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Premiumization and Smart, Design-Led Upgrades

Manufacturers are embedding agentic AI, large language models, and computer vision into premium refrigerators, ovens, and cooktops to automate cooking workflows, personalize recipes, and enable conversational controls that elevate daily usability within the North American luxury appliances market. Samsung’s Bespoke AI portfolio previewed at CES 2026 integrates Google Gemini for natural voice interactions while expanding AI Vision food recognition that supports guided meal planning and healthier choices for time-constrained households[1]Communications Team, “CES 2026: A Home Companion Making Daily Life More Effortless,” Samsung Newsroom UK, news.samsung.com. LG’s tenth anniversary Signature lineup adds Gourmet AI with in-oven cameras that identify a broad range of dishes, and auto-select cooking modes, advancing hands-off precision that aligns with premium buyer expectations[2]Newsroom Staff, “LG Electronics Presents the Future of Luxury Home Living at KBIS 2026,” LG Newsroom Global, lg.com. Bosch Cook AI couples sensors with adaptive guidance across coordinated appliances, which supports consistent outcomes and reduces error rates during complex preparations in high-spec kitchens. Sub Zero’s Owner’s App recognition in 2026 highlights how proactive diagnostics and predictive maintenance now form part of the value proposition for luxury ownership, improving uptime and service experience. Design customization is deepening alongside intelligence, with brands showcasing panel-ready configurations, specialty finishes, and artisan collaborations that allow appliances to disappear into cabinetry or stand out as focal elements in the North American luxury appliances market.

Built-In and Integrated Kitchens Expanding Attach Rates

Open-plan residences and minimalist interiors prioritize visual continuity, which pushes demand toward panel-ready appliances that align flush with cabinetry and emphasize clean lines within the North American luxury appliances market. Brands are scaling integrated portfolios that minimize visible hardware, with premium ovens, cooktops, and refrigeration tailored for seamless installation and coordinated finish palettes favored by designers and custom builders. Induction platforms that incorporate ventilation into the cooktop surface help preserve open sightlines and support island‑centric layouts by removing the need for overhead hoods. Premium brands continue to extend panel‑ready options and modular configurations to accommodate varied cabinet standards, which reduces design tradeoffs and increases attach rates for coordinated suites. Luxury consumers increasingly expect a curated aesthetic and digital consistency across appliances, which encourages whole‑kitchen upgrades that blend finishes, handle treatments, and UI logic across ovens, dishwashers, and refrigeration in the North American luxury appliances market. This pairing of invisible design and intelligent orchestration is strengthening the case for built‑in adoption where installation capabilities and electrical capacity are available.

Remodeling and Replacement Cycles Sustain Demand

Transaction‑driven remodels, replacement of aging premium units, and the desire for cohesive suites sustain a steady activation base despite macro uncertainty in the North American luxury appliances market. Affordability pressures curbed move‑up transactions in 2025, but a one‑percentage‑point mortgage rate decline can expand the pool of qualifying households by millions, which supports a subsequent wave of kitchen refresh projects. New homeowners frequently replace builder‑grade packages early in occupancy, favoring panel‑ready, quiet, and smart‑enabled systems that fit open living concepts within the North American luxury appliances market. Premium brands that validate durability and long service life strengthen upgrade confidence by framing ownership as a multi‑decade investment. Rising intelligence, self‑diagnostics, and remote service capabilities also encourage replacements by reducing perceived hassle from complex installations and maintenance in the North American luxury appliances market. As showroom experiences highlight integrated ecosystems and curated finishes, consumers are motivated to pursue full‑suite adoption rather than incremental upgrades.

Energy-Efficiency Standards Favoring Premium Tech-Rich Models

Electrification incentives and consumer preference for precise, flameless cooking are advancing induction from early adopter status to mainstream consideration in the North American luxury appliances market. Premium introductions, including professional‑grade induction ranges and downdraft induction cooktops, deliver rapid response and fine‑grained control without gas‑line dependencies. Design‑integrated solutions that combine induction with surface ventilation support open‑concept kitchens by preserving clean sightlines and eliminating overhead hoods. Awards and industry recognition for induction leaders signal broadening consumer acceptance and performance credibility at the luxury tier. Infrastructure gaps remain a constraint because a large share of homes require 240‑volt circuits or panel upgrades for high‑wattage cooking, which lengthens project timelines and adds cost. Even with these hurdles, state and federal incentives, strong product roadmaps, and design point to rising induction penetration across premium remodels in the North American luxury appliances market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Price Points vs. Mainstream Alternatives | -0.6% | Broad North American middle-income segments | Short term (≤ 2 years) |

| Remodeling Growth Downshift (Rates, Macro) Tempers Upgrades | -0.8% | United States and Canada, correlated with Federal Reserve rate policy | Short term (≤ 2 years) |

| Skilled-Install and Electrical Upgrade Bottlenecks (Built-In/Induction) | -0.5% | National, acute in fast-growth metros (Austin, Phoenix, Charlotte) | Medium term (2-4 years) |

| Channel Conflict Risks in DTC vs. Dealer Ecosystems | -0.3% | United States and Canada, impacting brands with hybrid retail strategies | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

High Upfront Price Points vs. Mainstream Alternatives

Luxury suites and integrated installations carry significant premiums over mass premium offerings, which narrows the eligible buyer pool even when aspirational interest is high in the North American luxury appliances market. Affordability erosion compounds the challenge because middle-income households can access a smaller share of listed homes than they did pre-pandemic, which reduces discretionary budgets for elective kitchen upgrades. Brands counter price sensitivity by emphasizing longevity, energy efficiency, and service support to frame ownership as a long-term investment that enhances daily use and resale potential. Promotions and curated package discounts that bundle three or more appliances target conversion barriers for premium buyers who value finish consistency and connected features within the North American luxury appliances market. Feature parity from mass premium competitors intensifies trade-offs between price and performance, which pressures incumbents to justify premiums through heritage craftsmanship, panel-ready execution, and predictive service ecosystems. These dynamics collectively slow adoption among price-sensitive cohorts, while high-income households remain engaged through design-led, fully integrated projects in the North American luxury appliances market.

Remodeling Growth Downshift (Rates, Macro) Tempers Upgrades

Higher borrowing costs and a smaller pool of move-up transactions moderated the pace of kitchen remodels in 2025, which weighs on short-term premium-appliance demand in the North American luxury appliances market. Even so, the potential for rate relief expands qualification for millions of households, which tends to unlock resale inventory and subsequent kitchen refresh activity on a lag. Replacement-driven purchases continue because failure events do not track macro cycles and often prompt whole suite decisions when homeowners pursue integrated aesthetics and quieter operation within open plans. Showroom strategies that emphasize experiential vignettes, finish libraries, and live cooking demos help sustain intent despite caution around discretionary spending in the North American luxury appliances market. Manufacturers that pair premium intelligence with energy savings narratives align with homeowner priorities for comfort and total cost of ownership during periods of rate volatility. Over the forecast horizon, the mix shift toward advanced electric platforms and integrated suites should reassert growth as affordability headwinds ease in the North American luxury appliances market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Major Appliances Command Value, Dishwashers Accelerate

Refrigerators captured 28.06% of the North American luxury appliances market share in 2025, while dishwashers are projected to post a 5.78% CAGR through 2031 as consumers favor quiet, panel-ready units with advanced sensors and remote diagnostics. Within the North American luxury appliances market, brands are elevating large appliances with conversational controls, precision cooking, and predictive service that enhances day-to-day convenience in open-plan homes. Premium dishwashers and wall ovens with camera-based recognition and guided modes reduce trial and error, which resonates with busy households that value reliability and low noise. AI-assisted cooking and ecosystem orchestration across ovens, hoods, and ranges demonstrate how automation now complements craftsmanship to justify premium pricing. Refrigeration leadership remains anchored in food preservation, temperature precision, and flexible zones, while connected apps streamline maintenance and support. Small appliances play a growing supporting role as brands introduce design-forward accessories, including smart countertop devices that extend the experience beyond built-ins.

Premium oven lines that integrate cameras and machine guidance set expectations for consistent outcomes, while induction cooktops accelerate the shift away from gas through speed and fine-grained control in the North American luxury appliances market. Laundry platforms at the premium tier highlight quietness, fabric care, and energy efficiency, with models recognized for sustainability and performance across North America. Beverage and specialty refrigeration categories broaden attachment opportunities by complementing primary refrigeration with purpose-built storage and presentation. As brands layer intelligence and material refinement into major appliances, they extend design language and user interface consistency into adjunct categories to reinforce suite cohesion. This ecosystem view supports whole kitchen upgrades that leverage consistent finishes, handles, and digital controls, a pattern that strengthens mix and average selling price in the North American luxury appliances market.

By Installation Type: Freestanding Dominates, But Built-In Posts Superior Growth

Freestanding appliances represented 83.61% of 2025 volume, while built-in and integrated units are projected to expand at a 4.88% CAGR through 2031 as design-led projects prioritize flush installations and coordinated finishes within the North American luxury appliances market size. Integrated portfolios from leading brands address minimalist interiors with panel-ready options, concealed hardware, and aligned control logic that create seamless kitchen experiences. Induction innovations that incorporate downdraft ventilation simplify planning for island-centric layouts and remove overhead obstruction, which fits open concept preferences. Brands emphasize installation quality and certified service to ensure performance and longevity for built-in suites that require tight tolerances and tailored electrical capacity. As panel-ready offerings proliferate across refrigerators, dishwashers, and wall ovens, consumers are more likely to adopt full suites that align with cabinetry and trim details in the North American luxury appliances market.

Freestanding platforms maintain appeal where retrofit simplicity, mobility, or budget flexibility matters, and manufacturers continue to improve fit-and-finish to bridge to integrated aesthetics. Hybrid solutions and slimmer insulation profiles in premium columns reduce space demands while preserving capacity, which supports upgrade paths for remodels without full cabinet rework. Showrooms highlight side-by-side comparisons of freestanding versus integrated configurations to help buyers understand tradeoffs in service access, noise control, and visual continuity. Induction’s growth is additive for built-ins because flush cooktops with coordinated ovens simplify planning and elevate workflow in open kitchens within the North American luxury appliances market. Over the forecast window, built-in momentum should improve mix while freestanding volume sustains overall penetration in diverse North American housing stock.

By End-User: Residential Leads, Commercial Accelerates with Hotel Pipeline

Residential applications captured 70.71% of demand in 2025, while the commercial segment is projected to advance at a 5.62% CAGR through 2031 as boutique hospitality and mixed-use projects seek premium equipment that enhances guest experience within the North American luxury appliances market size. Residential buyers value quiet operation, panel-ready finishes, and smart features that reduce friction and improve outcomes in open plan spaces. Commercial buyers prioritize serviceability, uptime, and system integration that supports property management and staff workflows, which continues to influence premium engineering in consumer-facing lines. The ongoing shift toward induction and electric appliances aligns with decarbonization goals in both luxury homes and hospitality, which supports portfolio breadth across formats in the North American luxury appliances market. As newer residential owners replace builder-grade packages with integrated suites, they often adopt commercial-inspired performance features such as high-output burners, precise temperature control, and durable materials.

Premium outdoor and entertaining spaces add additional touchpoints for refrigeration and specialty appliances in both luxury homes and hospitality projects, broadening attachment opportunities. Hospitality programs increasingly display brand storytelling and finish coordination that mirror high-end residential showrooms, which narrows the experiential gap between property and home. Certification and compliance needs remain distinct in commercial settings, but consumer trends around quietness, intuitive controls, and connected diagnostics continue to influence specification. Retail and showroom strategies that present full suite vignettes help both residential and commercial buyers envision integrated solutions that meet performance and aesthetic objectives within the North American luxury appliances market. As design professionals coordinate multi-project portfolios, standardized premium platforms can streamline service across mixed residential and hospitality footprints.

By Distribution Channel: Retail Dominates, Yet DTC Conversion Lags

B2C retail captured 75.73% of 2025 volume and is projected to grow at a 5.08% CAGR through 2031, reflecting the central role of multi-brand showrooms and brand experience centers that facilitate specification, delivery, and installation for complex projects in the North American luxury appliances market. Manufacturers operate show spaces that immerse prospects in integrated suites while routing transactions to dealer partners, preserving consultative selling and white glove service. Direct e-commerce is expanding in content and configuration tools, but bulky logistics and installation needs keep physical retail central to the purchase journey in the North American luxury appliances market.

Category leaders sustain retail relevance by launching high-interest products with in-store prominence and coordinated marketing that educates consumers on advanced features. Hybrid distribution strategies that balance brand-owned touchpoints with authorized dealer ecosystems support channel health while providing consistent service outcomes. Over the forecast window, the North American luxury appliances market is expected to retain retail primacy even as digital experiences handle discovery, configuration, and service enrollment.

Geography Analysis

The United States held 76.40% of the 2025 value, while Mexico is projected to post the fastest growth at a 5.29% CAGR through 2031 as regional demand profiles diversify within the North American luxury appliances market. Canada sits between these trajectories with concentrated demand in major metros, where premium buyers favor integrated European and North American brands in design-led remodels. United States momentum in 2026 is shaped by affordability constraints and infrastructure readiness for electrification, with state-level incentives improving the case for electric upgrades in premium kitchens. Brands deploy showroom and service investments in gateway cities to guide buyers through built-in and induction decisions that hinge on design, performance, and electrical capacity in the North American luxury appliances market.

The United States remains the center of innovation for AI-enabled appliances, with multiple launches from top brands showcasing conversational interfaces, camera-assisted cooking, and predictive maintenance that align with premium buyer expectations. California’s IRA-linked rebates, with significant allocations progressing through reservations by early 2026, show how policy can accelerate premium electric upgrades at scale within the North American luxury appliances market. At the same time, many households need panel upgrades to enable high-wattage induction, which factors into planning timelines and project budgets. As rate dynamics evolve, expanded qualification can unlock resale activity and subsequent remodels, which benefits premium brands positioned with integrated suites and smart features.

Mexico’s role in the regional picture is rising with projected outperformance on growth from a low luxury base, while luxury penetration remains concentrated in select urban and resort markets in the North American luxury appliances market. Canadian demand mirrors the United States' preferences at a smaller scale, with heavy emphasis on integrated European design in high-income metros where open-plan renovations remain prevalent. Across all three markets, showroom experiences, certified installation, and post-sale service continue to shape brand choice, especially where electrical upgrades are needed for induction or panel capacity. The interplay of incentives, affordability, and infrastructure will guide the cadence of premium upgrades through 2031 within the North American luxury appliances market.

Competitive Landscape

The North American luxury appliances market features established leaders and fast-moving mass premium entrants, with competition focused on AI-enabled cooking, panel-ready integration, and predictive service that reduces ownership friction. BSH Home Appliances advances multi-brand strategies that cover accessible luxury through ultra premium, while continuing to invest in design-centric showrooms and product experiences across North America. Miele’s engineering and longevity positioning are backed by multi-year investments and steady revenue performance in 2025, which support premium pricing and brand equity. LG and Samsung emphasize LLM-powered interfaces and vision-assisted cooking that make connected experiences central to differentiation at the top of the market[3]Newsroom Staff, “LG Electronics Presents the Future of Luxury Home Living at KBIS 2026,” LG Newsroom Global, lg.com.

Strategic moves center on three vectors, including AI/IoT platforms, finish customization, and service ecosystems that anticipate maintenance needs in the North American luxury appliances market. BlueStar’s high output ranges and broad color library reinforce customization leadership, which resonates with designers who tailor finishes to millwork and metal accents. Electrolux and AEG highlight sustainability and intelligent guidance in premium launches, aligning with energy efficiency expectations in the luxury tier. GE Appliances’ multi-brand approach adds depth in smart ovens, dishwashers, and induction ranges, supported by continuous app innovation and retail partnerships that enhance category visibility. These moves concentrate differentiation around performance, integration, and aesthetics that address high-value use cases in the North American luxury appliances market.

R&D investment and IP depth remain critical, with top manufacturers reinforcing first-mover advantages through patents, standards development, and scalable platforms. Show presence at KBIS and IFA provides launch velocity for hero products across cooking, cooling, and cleaning, while experience centers in key metros deliver curated buyer journeys that support higher attach rates. As mass premium brands narrow feature gaps at lower price points, incumbents defend positioning through superior material quality, modular integration, and proactive service that simplifies ownership in the North American luxury appliances market. The net effect is a competitive field where brand equity, system intelligence, and execution quality drive share outcomes over the forecast period.

North America Luxury Appliances Industry Leaders

Sub-Zero Group

BSH Home Appliances

Miele & Cie.

Monogram (GE Appliances)

JennAir (Whirlpool)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: LG Electronics unveiled its tenth-anniversary Signature lineup at KBIS 2026, integrating conversational AI powered by large language model technology, Gourmet AI with in-oven cameras recognizing over 85 dishes, and expanding the portfolio to ten product categories across three design collections: Seamless, Iconic, and Tailored.

- February 2026: GE Appliances launched a comprehensive portfolio of 39 smart wall oven models across Monogram, GE Profile, and CAFÉ brands, featuring CookCam AI technology, 7-inch color LCD touchscreens, voice-command integration, and Bluetooth speakers on select units.

- February 2026: BlueStar relaunched its Platinum Series Gas Ranges with newly engineered ovens and proprietary X-8 burners featuring an 8-point sealed star shape, 152 precision-control heat ports, 25,000 BTUs for high-heat searing, and ultra-low 500 BTU simmer capability.

North America Luxury Appliances Market Report Scope

Luxury appliances are high-end appliances that are built for top performance. They provide consumers with both optimal functional and aesthetic value. They cost more than regular appliances for their state-of-art engineering.

The North American luxury appliances market can be segmented by product type, end-user, distribution channel, and geography. By product type, segments can be cooking and baking, cooling, cleaning, and other appliances. By end-user, segments can be commercial and residential. By distribution channel, segments can be multi-brand stores, Exclusive stores, E-commerce, and other distribution channels. By geography, segments can be divided into the USA and Canada. The report also offers a complete background analysis of the luxury appliances market, including the analysis and forecast of market size, market segments, industry trends, and growth drivers.

| Major Home Appliances | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Ovens (Incl. Combi & Microwave) | |

| Air Conditioners | |

| Other Major Home Appliances | |

| Small Home Appliances | Coffee Makers |

| Food Processors | |

| Grills & Roasters | |

| Electric Kettles | |

| Juicers & Blenders | |

| Air Fryers | |

| Vacuum Cleaners | |

| Electric Rice Cookers | |

| Toasters | |

| Countertop Ovens | |

| Other Small Home Appliances |

| Built-in / Integrated |

| Freestanding |

| Residential |

| Commercial |

| B2C / Retail | Multi-Brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B Channels/ Projects |

| United States |

| Canada |

| Mexico |

| By Product Type | Major Home Appliances | Refrigerators |

| Freezers | ||

| Washing Machines | ||

| Dishwashers | ||

| Ovens (Incl. Combi & Microwave) | ||

| Air Conditioners | ||

| Other Major Home Appliances | ||

| Small Home Appliances | Coffee Makers | |

| Food Processors | ||

| Grills & Roasters | ||

| Electric Kettles | ||

| Juicers & Blenders | ||

| Air Fryers | ||

| Vacuum Cleaners | ||

| Electric Rice Cookers | ||

| Toasters | ||

| Countertop Ovens | ||

| Other Small Home Appliances | ||

| By Installation Type | Built-in / Integrated | |

| Freestanding | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C / Retail | Multi-Brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B Channels/ Projects | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the size of the North American luxury appliances market in 2026 and its growth outlook?

The North American luxury appliances market size is USD 15.13 billion in 2026 and is projected to reach USD 18.89 billion by 2031 at a 4.54% CAGR.

Which product category leads and which is growing fastest in luxury appliances?

Refrigerators lead with 28.06% share in 2025, while dishwashers are the fastest-growing with a projected 5.78% CAGR through 2031.

How do installation types compare for premium kitchens in North America?

Freestanding models account for 83.61% of 2025 volume, but built-in and integrated units are projected to grow at a 4.88% CAGR through 2031 as flush, panel-ready designs gain favor.

Which channels are most important for buying luxury appliances?

B2C retail drives 75.73% of 2025 sales with a projected 5.08% CAGR through 2031, supported by showrooms and experience centers that handle complex specification and installation.

How do incentives affect premium electric and induction adoption?

United State and federal rebates under the Inflation Reduction Act lower upfront costs for eligible households, which supports faster adoption of induction cooking and heat pumps in premium remodels.

Page last updated on: