Market Overview

| Study Period | 2020 - 2031 |

|---|---|

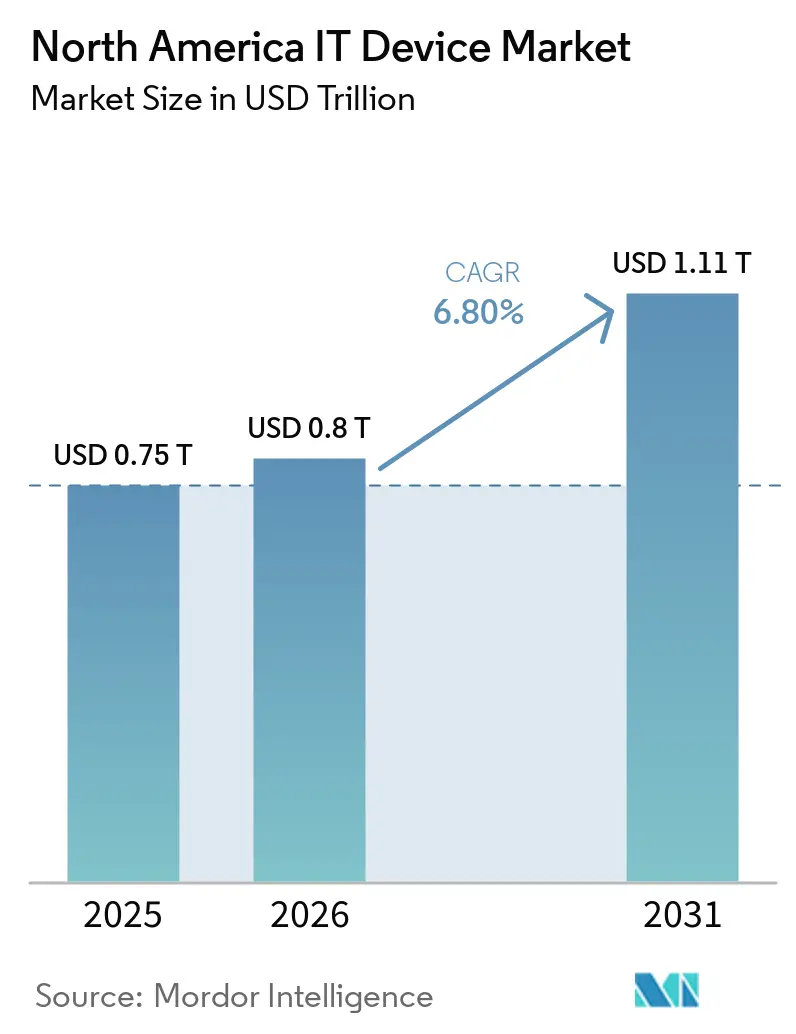

| Base Year Market Size (2025) | USD 0.75 Trillion |

| Market Size (2026) | USD 0.8 Trillion |

| Market Size (2031) | USD 1.11 Trillion |

| Growth Rate (2025 - 2030) | 6.80% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

North America IT Device Market Analysis by ���ϲ�����

The North America IT device market size is expected to increase from USD 801.85 billion in 2026 to reach USD 1,114.17 billion by 2031, growing at a CAGR of 6.8% over 2026-2031. Demand is shifting from the pandemic-era spike toward structural drivers, notably enterprise-wide hardware refreshes scheduled before Windows 10 support ended in October 2025, rapid 5G densification across major metro areas, and the mainstream roll-out of edge-AI chipsets inside laptops and desktops. Compressed replacement cycles mean technology buyers are advancing purchase decisions by 12-18 months, while wireless penetration is reshaping connectivity preferences in both consumer and commercial segments. The convergence of device and cloud analytics is also lifting attach rates for software subscriptions, boosting average revenue per user across smartphones, wearables, and PCs. Intensifying price competition in mid-tier phones is being partially offset by premium devices that bundle neural processors and exclusive services.

Key Report Takeaways

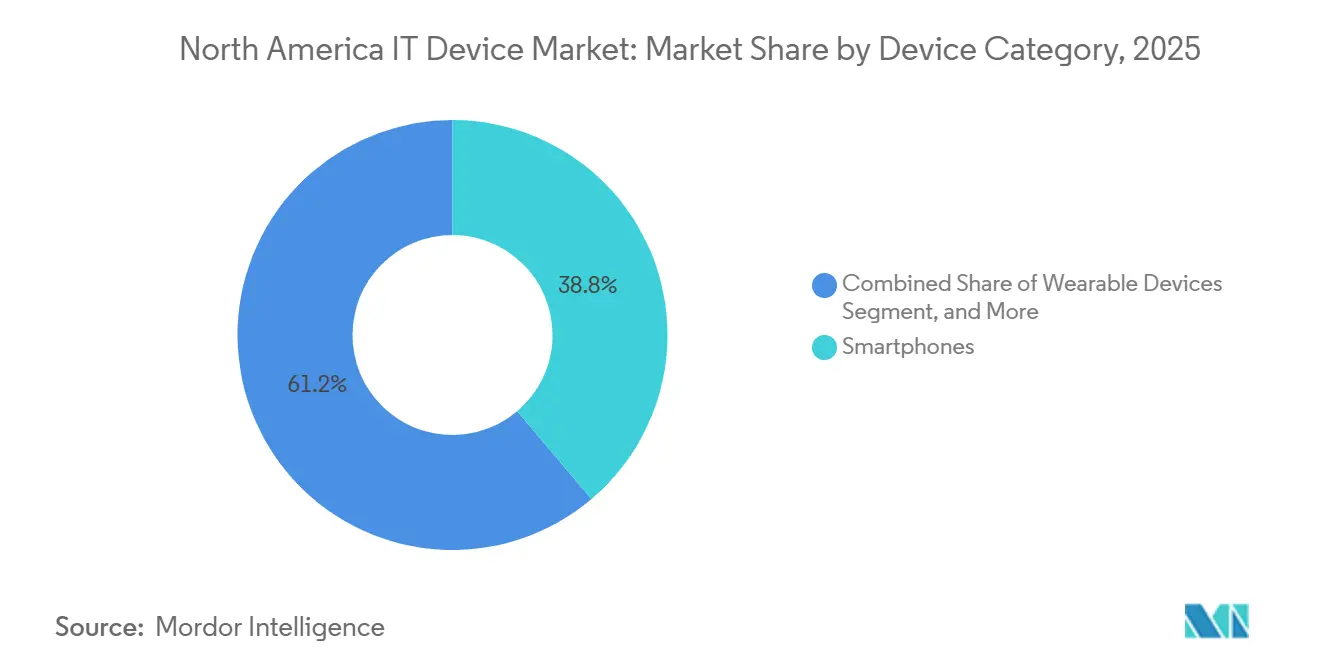

- By device category, smartphones led with 38.8% revenue share of the North America IT Device market in 2025, whereas wearables are forecast to advance at an 11.2% CAGR from 2026-2031.

- By end user, the consumer segment accounted for 46.3% of the North America IT Device market in 2025 value, while healthcare is projected to expand at a 10.6% CAGR through 2031.

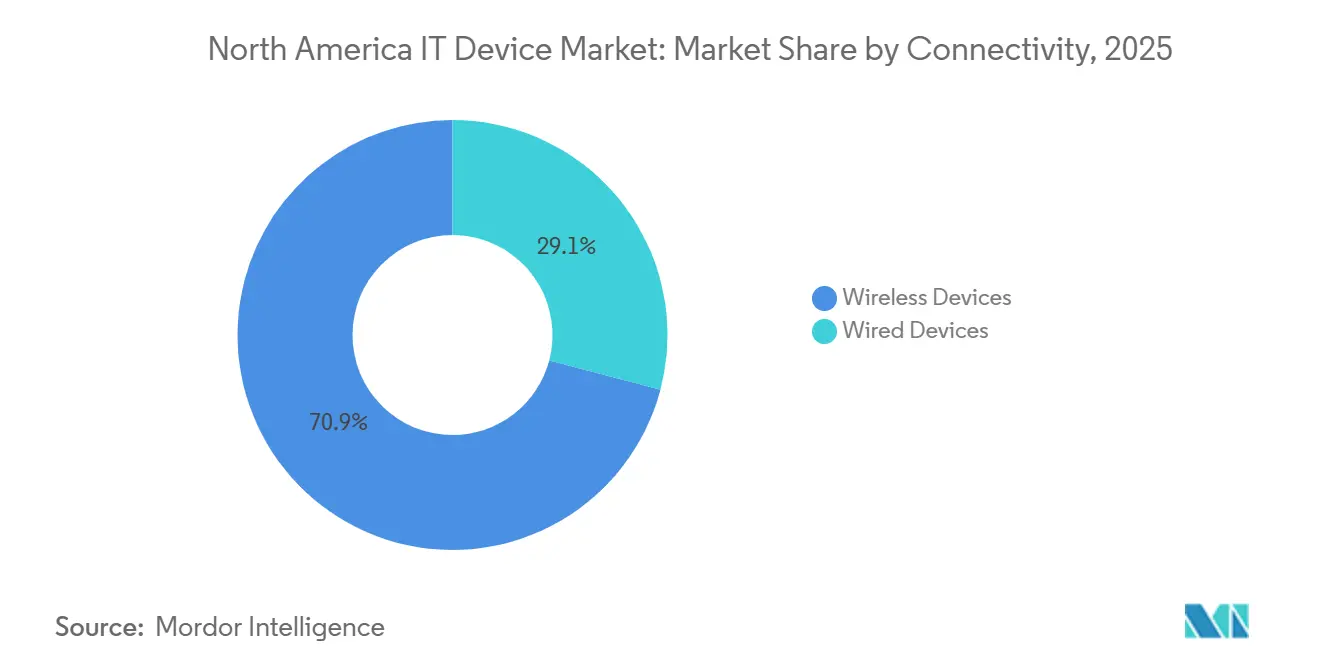

- By connectivity, wireless devices captured 70.9% of the North America IT Device market in 2025 revenue and are expected to grow at a 9.2% CAGR over 2026-2031.

- By distribution channel, online retail held 43.6% share of the North America IT Device market in 2025 and is set to increase at an 8.4% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America IT Device Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for Hybrid Work Hardware | +1.2% | United States, Canada | Medium term (2-4 years) |

| Enterprise-wide Device Refresh Post-Windows 10 | +1.5% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Accelerated 5G Roll-outs Fueling Upgrades | +1.0% | United States, Canada | Medium term (2-4 years) |

| Tax Incentives on Semiconductor Assembly | +0.6% | Mexico, spill-over to United States | Long term (≥ 4 years) |

| Growing Adoption of XR-ready Wearables | +0.8% | United States, early uptake in Canada | Medium term (2-4 years) |

| Edge-AI Integration into Laptops and PCs | +1.3% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Surging Demand for Hybrid Work Hardware

Hybrid work remains entrenched, propelling sustained purchases of laptops, monitors, and webcams beyond the pandemic spike. Best Buy disclosed that computing and mobile products generated 49% of domestic revenue in its third fiscal-quarter 2026 report, with comparable sales up 7.6% year-on-year. Dell Technologies and HP both emphasized growing commercial PC pipelines, underscoring condensed refresh cycles as enterprises step down from five-year to three-year replacement intervals.[1]Dell Technologies Inc., “Commercial PC Pipeline Commentary,” Dell Technologies, delltechnologies.com Demand is strongest in the United States and Canada, where remote work penetration tops 40% of knowledge workers, while Mexico lags because of infrastructure limits. The resulting uplift accelerates unit volumes across premium notebooks equipped with neural processing units, ensuring local AI inference and compliance with data-sovereignty mandates. Consequently, the North America IT device market benefits from higher average selling prices on commercial SKUs, partially offsetting softness in entry-level consumer PCs.

Enterprise-Wide Device Refresh Post-Windows 10 End-of-Life

Microsoft withdrew Windows 10 support on 14 October 2025, triggering the largest enterprise PC replacement cycle since the Windows 7 sunset. Volume-licensing agreements from HP and Dell now bundle Windows 11 Pro with Copilot+ PCs based on Qualcomm Snapdragon X Elite or Intel Core Ultra processors, each embedding dedicated AI engines.[2]HP Inc., “Windows 11 Pro and Copilot+ PC Bundles,” HP, hp.com Lenovo’s ThinkPad X1 Carbon Gen 13 exemplifies the trend, pairing Intel silicon with on-device transcription agents unveiled at CES 2025. Public-sector procurement in the United States, Canadian provinces, and Mexican subsidiaries is releasing deferred budgets to ensure cybersecurity compliance, concentrating the impact in 2026-2027. As a result, the North America IT device market is experiencing front-loaded demand that lifts near-term revenues but may elongate future cycles.

Accelerated 5G Roll-Outs Fueling Smartphone Upgrades

Mid-band spectrum deployments across 2.5 GHz and C-band frequencies have boosted 5G population coverage above 70% in the United States by end-2025. Samsung’s Galaxy Z Fold6 and Apple’s iPhone 16 series both integrate next-generation modems and satellite connectivity, encouraging consumers and enterprises to replace older handsets. Carrier installment plans tie device upgrades to unlimited 5G data, shortening the replacement cycle to below three years. Field-service industries such as utilities and logistics are leveraging low-latency links for augmented-reality workflows, magnifying enterprise uptake. Although Mexico trails by up to two years because of slower auctions, spill-over demand is expected once infrastructure matures, sustaining regional momentum for the North America IT device market.

Edge-AI Integration into Laptops and PCs

Neural processing units embedded in Qualcomm Snapdragon X Elite, Intel Core Ultra, and AMD Ryzen AI chips bring large language models on-device, enabling real-time video enhancement and privacy-preserving analytics. Microsoft’s Surface Laptop 7 and Surface Pro 11 deliver up to 45 TOPS of local inference capability, marketed as Copilot+ PCs that reduce cloud latency. Dell, HP, and Lenovo now feature similar silicon, appealing to enterprises governed by Canada’s Personal Information Protection and Electronic Documents Act and the European Union’s GDPR. This architecture shift raises bill-of-materials costs but differentiates premium PCs, lifting margins and further expanding the North America IT device market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Semiconductor Supply Imbalances | -0.9% | United States, Canada, Mexico | Medium term (2-4 years) |

| Inflation-driven Price Sensitivity | -0.7% | United States, Canada | Short term (≤ 2 years) |

| Tightened U.S-China Export Controls | -0.5% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Escalating e-waste Compliance Costs | -0.4% | United States, Canada | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Persistent Semiconductor Supply Imbalances

Structural shortages persist in high-bandwidth memory and advanced logic nodes despite easing headline constraints. Samsung announced DDR5 price hikes of up to 60% for 1Q 2025, citing tight supply linked to AI server demand. Micron echoed that memory scarcity will extend through 2027, diverting capacity away from consumer PCs. Export-control rules issued by the U.S. Bureau of Industry and Security in December 2024 and January 2025 further limit equipment access for Chinese fabs, stalling global wafer additions.[3]U.S. Bureau of Industry and Security, “Export Control Final Rules,” BIS, bis.doc.gov Resulting lead-time volatility complicates production planning for device makers across North America, trimming projected growth in the North America IT device market.

Inflation-Driven Price Sensitivity Among Consumers

Elevated inflation during 2024-2025 pressured discretionary electronics spending. The U.S. Bureau of Labor Statistics showed the consumer price index for televisions falling 8.2% year-on-year in December 2024, evidence of steep discounting.[4]U.S. Bureau of Labor Statistics, “Consumer Price Index December 2024,” BLS, bls.gov Adobe Analytics reported that U.S. online holiday electronics average order values slipped 2.1% despite higher unit volumes. As households prioritize essentials, manufacturers hold margins only in premium tiers with AI-centric features, compressing mid-range device profitability in the North America IT device market.

Segment Analysis

By Device Category: Wearables Outpace Smartphones in Growth Velocity

Wearables contributed a modest share in 2025 yet are projected to expand at a strong compound annual growth rate through 2031, making it the fastest-growing category among all IT device segments. Recent FDA guidance issued in early 2026 has eased regulatory barriers for low-risk health trackers, paving the way for accelerated adoption. Garmin’s Fenix 8, equipped with advanced features like ECG and SpO₂ sensors, caters to both athletes and first responders, addressing niche yet critical market needs. Additionally, continuous glucose monitors from companies such as Abbott, Medtronic, and Dexcom are integrating smartphone connectivity, creating deeper and more interconnected data ecosystems. These advancements highlight the growing importance of wearables in the broader IT device market, driven by innovation and regulatory support.

Smartphones, while remaining the largest segment of the North America IT device market, are experiencing a slowdown in growth as market penetration reaches saturation. In contrast, laptops and desktops are seeing incremental growth fueled by edge-AI upgrades, which enhance their functionality and appeal. Servers and storage devices are scaling up in density to meet the demands of AI workloads, as demonstrated by Seagate’s high-capacity 30-TB Exos M drives. Peripherals continue to benefit from sustained demand driven by hybrid work environments, while point-of-sale terminals and industrial handheld devices remain critical components of the "other devices" category. Collectively, these shifts underscore a broader market pivot toward data-generating hardware that supports recurring analytics services, reflecting the evolving needs of businesses and consumers alike.

By End User Industry: Healthcare Sector Leads Growth

Healthcare is forecast to post a 10.6% CAGR between 2026 and 2031, outstripping the consumer segment that nevertheless retains the largest share. Hospitals are increasingly deploying rugged tablets for bedside charting and wearable monitors for remote patient surveillance, ensuring seamless integration with electronic health records under HIPAA safeguards. The aging population and rising prevalence of chronic diseases in the United States and Canada are driving the demand for continuous monitoring solutions. Additionally, small and medium enterprises are opting for cost-effective laptops, while large enterprises are standardizing AI-ready PCs managed through zero-trust security consoles to enhance operational efficiency and data security.

Education continues to see steady demand for Chromebooks and iPads, supported by digital-learning grants from Canadian provinces. Government agencies in the United States leverage multi-year GSA schedules, while similar contracts in Canada are enabling the modernization of IT device fleets. The BFSI sector is refreshing workstations to support real-time fraud analytics, ensuring compliance and operational agility. Meanwhile, manufacturing and energy verticals are adopting ruggedized PCs designed for harsh environments, addressing specific operational needs. These trends collectively highlight the evolving demand dynamics within the North America IT device market, driven by sector-specific requirements and technological advancements.

By Connectivity: Wireless Devices Dominate

Wireless devices accounted for 70.9% of 2025 revenue and are projected to grow at a 9.2% CAGR, outpacing wired alternatives. Samsung’s Galaxy Z Fold6, equipped with the Snapdragon 8 Gen 3 chipset, delivers multi-gigabit 5G throughput, while Apple’s iPhone 16 introduces satellite SOS functionality, extending coverage into remote areas. The adoption of Wi-Fi 6E within corporate campuses is further displacing traditional Ethernet cabling. These advancements highlight the growing dominance of wireless devices in both consumer and enterprise markets. The increasing demand for seamless connectivity and enhanced mobility continues to drive the adoption of wireless technologies across various sectors.

Despite the rise of wireless devices, wired alternatives such as desktop PCs, servers, and USB-C docks remain critical for latency-sensitive workflows, including trading floors and other high-performance environments. These wired solutions provide the reliability and stability required for specific applications where even minor delays can have significant consequences. As carriers in the United States and Canada fulfill FCC and CRTC coverage mandates, rural and suburban adoption of wireless technologies is expanding. This shift is solidifying the primacy of wireless devices within the North America IT device market. However, wired solutions continue to serve niche but essential roles, ensuring a balanced ecosystem of IT devices.

By Distribution Channel: Online Retail Gains Share

Online retail held a 43.6% share in 2025 and is projected to grow at an 8.4% CAGR through 2031. Amazon’s North America segment reported USD 106.3 billion in revenue for Q3 2025, highlighting the platform's immense scale and dominance in the market. Best Buy’s omnichannel strategy, which integrates e-commerce with same-day in-store pickup, drove online sales to account for 31.8% of its domestic revenue. Additionally, direct-to-consumer portals from major vendors like Apple, Dell, and HP have complemented third-party marketplaces. These portals not only reduce channel margins but also provide vendors with greater control over their sales processes. The growing reliance on digital channels underscores the structural shift in consumer purchasing behavior within the North America IT device market.

While online retail continues to dominate, traditional big-box retailers, value-added resellers, and carrier stores still play a significant role in serving customers who prefer tactile experiences or financed purchases. These physical channels remain essential for certain consumer segments, particularly for high-value or complex IT devices. However, the incremental growth in the market is clearly leaning toward digital platforms, driven by convenience and broader product accessibility. This trend reflects the ongoing evolution of the North America IT device market, where digital channels are reshaping the competitive landscape while physical stores adapt to maintain relevance.

Geography Analysis

The United States anchors regional demand, propelled by the world’s largest installed enterprise base and aggressive 5G expansion. Federal and Fortune 500 refresh programs compressed by the Windows 10 sunset, combined with CHIPS Act incentives that redirect supply chains away from geopolitical risk. Environmental regulations, including the EPA battery take-back framework finalized in 2024, raise compliance costs but also spur recycled-device channels.

Canada’s market scales smaller but mirrors U.S. patterns, with provincial e-waste fees and government digital-infrastructure grants shaping purchasing. Public Services and Procurement Canada’s 2025-2026 plan emphasizes managed IT service bundles, encouraging lifecycle outsourcing. Rural broadband investments and AI compute grants fuel server and networking upgrades across universities and research labs, bolstering device demand albeit with cautious consumer spending.

Mexico delivers the highest growth rate, supported by federal tax incentives for semiconductor assembly, rising middle-class incomes, and nearshoring momentum aimed at the United States. Infrastructure gaps in power and water restrict rapid fab scaling, yet OEMs pursue dual-sourcing strategies to mitigate tariff and export-control exposure. Urban 5G deployments in Mexico City, Guadalajara, and Monterrey encourage smartphone and laptop adoption, while multinational manufacturing clusters deploy rugged tablets on shop floors. Successful workforce development and infrastructure build-outs remain prerequisites for Mexico to capture its full contribution to the North America IT device market.

Competitive Landscape

Smartphones, PCs, and tablets exhibit oligopolistic structures dominated by Apple, Samsung, Dell, HP, and Lenovo, each wielding scale economies and vertically integrated supply chains. Apple’s proprietary silicon, ecosystem lock-in, and high retention rates underpin premium pricing, allowing the company to maintain a stronghold in the premium segment. Samsung leverages in-house DRAM, NAND, and OLED production to cushion component volatility and ensure supply chain stability. Dell and HP focus on enterprise service contracts to differentiate themselves, while Lenovo undercuts competitors on price to capture a significant share in the SME space. These strategies highlight the competitive dynamics within the market, where innovation and operational efficiency play critical roles.

Storage rivals Seagate and Western Digital are racing to expand heat-assisted magnetic recording and 3D NAND capacity, which are essential to meet the growing demand for AI-driven data storage. Seagate’s advancements in storage technology exemplify efforts aimed at addressing the needs of data-intensive applications. Fragmented niches persist in wearables and peripherals, with companies like Garmin, Zebra, and Trimble carving out specialized markets. Garmin’s aviation-grade smartwatches cater to niche professional needs, Zebra’s rugged handhelds are designed for industrial use, and Trimble’s XR10 headset targets mixed-reality applications in specific verticals. These niches demonstrate how smaller players can thrive by addressing unique market demands.

Meta’s Quest 3S capitalizes on Microsoft’s HoloLens exit to target industrial mixed-reality workloads, positioning itself as a key player in this emerging segment. Meanwhile, Apple’s patent activity in neural processing units signals escalating competition for edge-AI leadership, as companies vie for dominance in next-generation technologies. Regulatory costs related to e-waste management, battery logistics, and data residency are increasingly favoring larger players with scale and resources to comply with stringent requirements. However, targeted innovation continues to enable smaller firms to establish defensible footholds, particularly in the North America IT device market, where adaptability and specialization remain critical for success.

North America IT Device Industry Leaders

Lenovo Group Limited

Apple Inc.

Samsung Electronics Co., Ltd.

HP Inc.

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Dell Technologies announced expansion of PC portfolio including revival of XPS lineup and introduction of more affordable devices to capture broader North American demand segments.

- January 2026: The FDA clarified that low-risk general-wellness wearables fall outside medical-device regulation, easing market entry for Garmin, Apple, and Samsung.

- February 2025: Seagate introduced its Exos M series 30-TB hard drives using the Mozaic 3+ platform, targeting hyperscale data centers.

- January 2025: Lenovo unveiled the ThinkPad X1 Carbon Gen 13 with Intel Core Ultra processors and integrated AI engines.

North America IT Device Market Report Scope

The North America IT Device Market refers to the market for physical computing and communication devices used by enterprises and consumers across the United States and Canada. It includes products such as personal computers (desktops and laptops), workstations, tablets, and peripheral devices that enable digital operations and connectivity. The market is driven by enterprise IT spending, device refresh cycles, hybrid work adoption, and advancements in computing technologies. It represents a mature, replacement-driven market with strong demand from corporate, government, and consumer segments.

The North America IT Device Market is Segmented by Device Category (Desktop PCs, Laptop PCs, Tablets, Smartphones, Servers and Storage Systems, Wearable Devices, Peripheral Devices, Other Device Categories), End User Industry (Consumer, Small and Medium Enterprises, Large Enterprises, Education Sector, Government and Public Sector, Healthcare Sector, Retail and E-Commerce, BFSI, Other End User Industries), Connectivity (Wired Devices, Wireless Devices), Distribution Channel (Online Retail, Offline Retail, Direct B2B Sales, Value-Added Resellers, Telecom Carrier Stores), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

By Device Category

| Desktop PCs |

| Laptop PCs |

| Tablets |

| Smartphones |

| Servers and Storage Systems |

| Wearable Devices |

| Peripheral Devices (Keyboards, Mice) |

| Other Device Categories |

By End User Industry

| Consumer |

| Small and Medium Enterprises |

| Large Enterprises |

| Education Sector |

| Government and Public Sector |

| Healthcare Sector |

| Retail and E-Commerce |

| BFSI |

| Other End User Industries |

By Connectivity

| Wired Devices |

| Wireless Devices |

By Distribution Channel

| Online Retail |

| Offline Retail |

| Direct B2B Sales |

| Value-Added Resellers |

| Telecom Carrier Stores |

By Country

| United States |

| Canada |

| Mexico |

| By Device Category | Desktop PCs |

| Laptop PCs | |

| Tablets | |

| Smartphones | |

| Servers and Storage Systems | |

| Wearable Devices | |

| Peripheral Devices (Keyboards, Mice) | |

| Other Device Categories | |

| By End User Industry | Consumer |

| Small and Medium Enterprises | |

| Large Enterprises | |

| Education Sector | |

| Government and Public Sector | |

| Healthcare Sector | |

| Retail and E-Commerce | |

| BFSI | |

| Other End User Industries | |

| By Connectivity | Wired Devices |

| Wireless Devices | |

| By Distribution Channel | Online Retail |

| Offline Retail | |

| Direct B2B Sales | |

| Value-Added Resellers | |

| Telecom Carrier Stores | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What growth is forecast for the North America IT device market between 2026 and 2031?

The market is projected to rise from USD 801.85 billion in 2026 to USD 1,114.17 billion by 2031, reflecting a 6.8% CAGR.

Which device category will grow the fastest through 2031?

Wearables are expected to post the highest CAGR at 11.2%, driven by enterprise XR use and FDA-clarified wellness rules.

How large is the wireless share of regional device revenue?

Wireless devices represented 70.9% of 2025 value and are forecast to grow at a 9.2% CAGR through 2031.

Why is healthcare the fastest-growing end-user segment?

Hospitals and clinics are adopting continuous monitoring wearables, rugged tablets, and AI-enabled diagnostics, producing a 10.6% CAGR.

Which sales channel is capturing incremental share?

Online retail, led by Amazon and direct-to-consumer OEM sites, held 43.6% share in 2025 and should expand at an 8.4% CAGR.

What is the main supply-side risk facing vendors?

Ongoing shortages in high-bandwidth memory and export-control restrictions on advanced nodes may reduce production flexibility.

Page last updated on: