Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

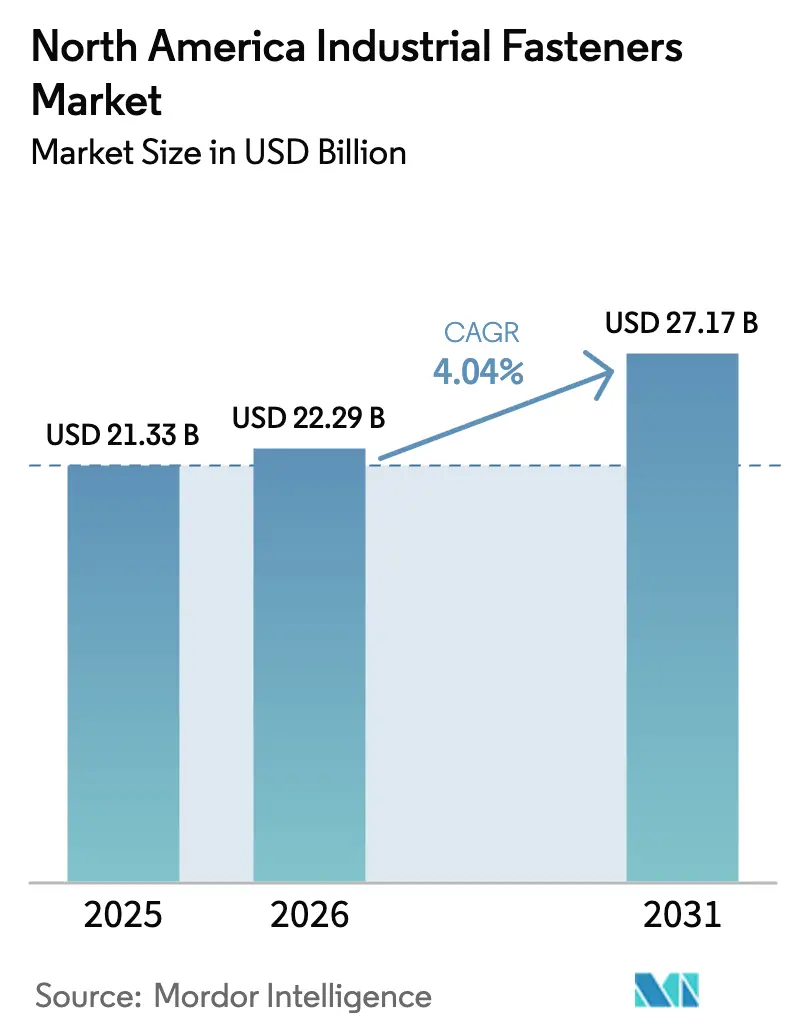

| Base Year Market Size (2025) | USD 21.33 Billion |

| Market Size (2026) | USD 22.29 Billion |

| Market Size (2031) | USD 27.17 Billion |

| Growth Rate (2026 - 2031) | 4.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

North America Industrial Fasteners Market Analysis by ���ϲ�����

The North America Industrial Fasteners Market size is projected to be USD 21.33 billion in 2025, USD 22.29 billion in 2026, and reach USD 27.17 billion by 2031, growing at a CAGR of 4.04% from 2026 to 2031.

Demand is shifting toward lighter, higher-performance products as electric vehicle and next-generation aircraft programs require aluminum, titanium, and composite fasteners that cut weight without sacrificing strength. Reshoring and Buy America rules are tightening local supply, prompting OEMs to lock in multi-year contracts while distributors install IoT vending to guarantee uptime. Environmental regulations banning hexavalent chromium elevate PTFE and zinc-nickel finishes, and raw-material volatility is encouraging inventory hedging among tier-two suppliers. Digital traceability, from QR codes to RFID, is becoming a baseline requirement rather than a premium feature.

Key Report Takeaways

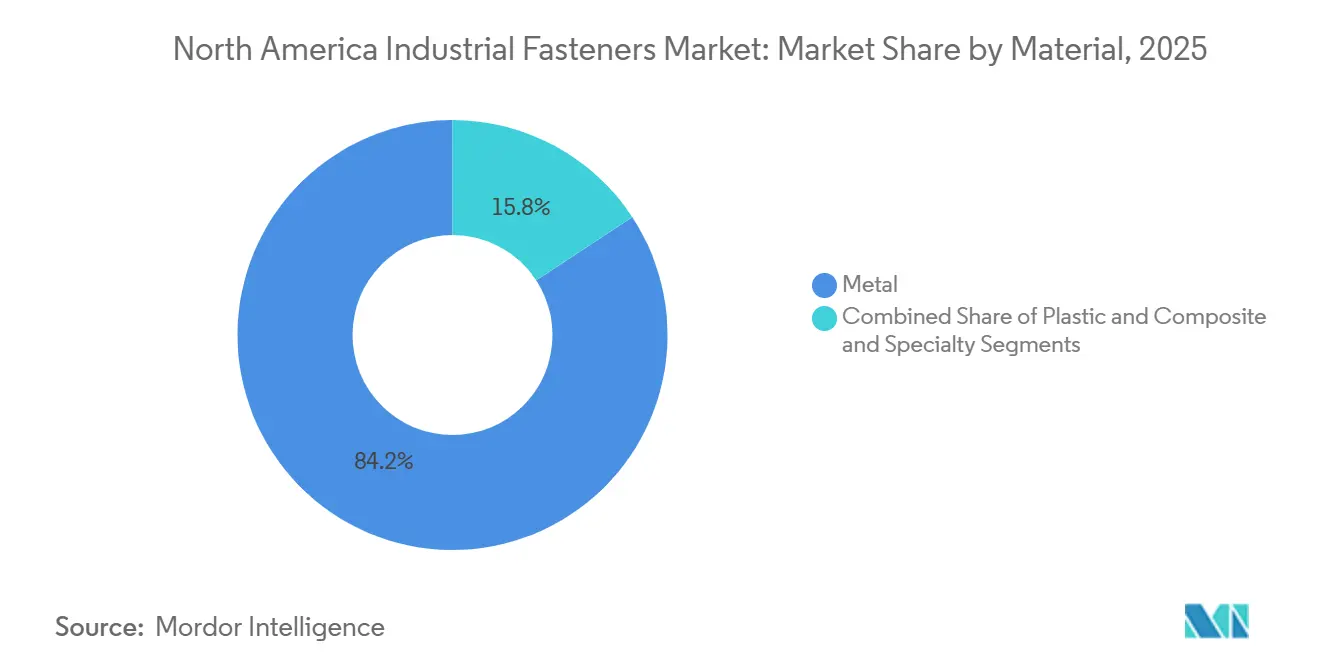

- By material, metal fasteners led with 84.23% of the North America industrial fasteners market share in 2025, while composite and specialty variants are forecast to advance at a 4.62% CAGR through 2031.

- By grade, standard products held a 67.13% share in 2025, whereas high-performance grades are projected to grow at a 4.49% CAGR over the same period.

- By product type, externally threaded fasteners captured 52.13% revenue share in 2025, and application-specific designs are poised for the fastest 4.87% CAGR to 2031.

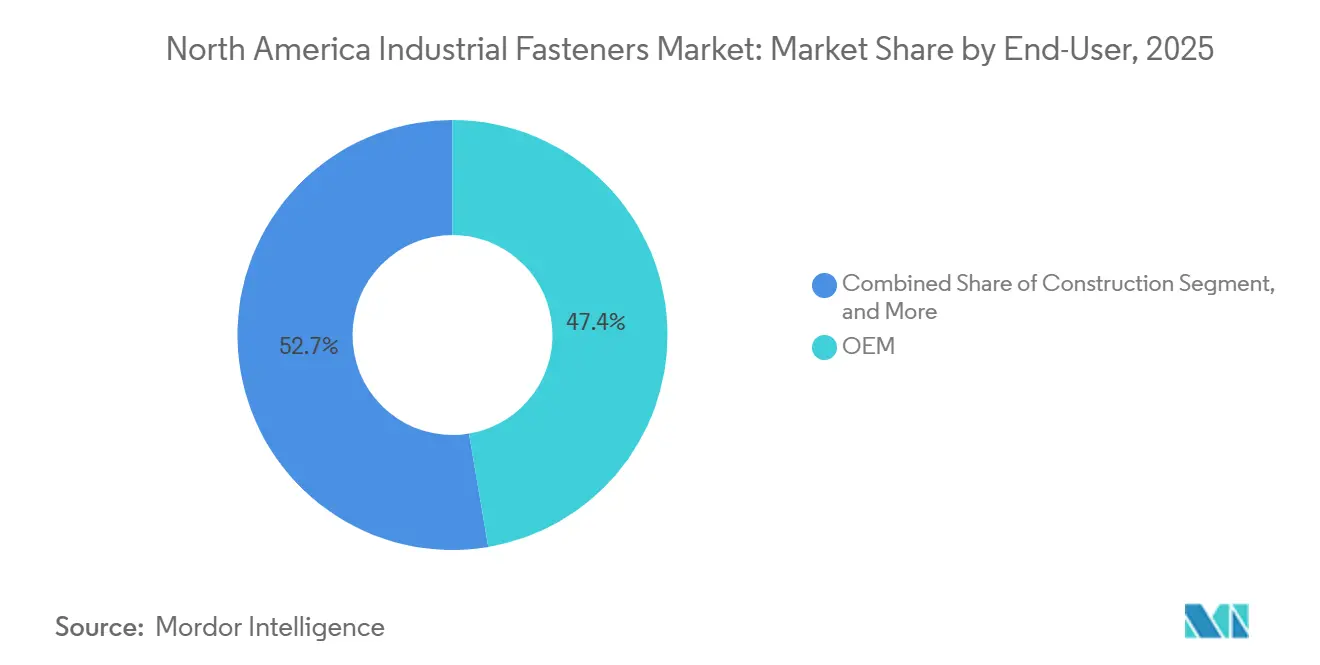

- By end-user application, the OEM segment accounted for 47.35% of the North America industrial fasteners market size in 2025 and is expanding at a 4.56% CAGR.

- By coating type, zinc-plated finishes dominated with a 39.02% share in 2025, yet PTFE and other specialty coatings are set to rise at a 4.91% CAGR through 2031.

- By geography, the United States accounted for 73.67% of 2025 demand, while Mexico is the fastest-growing market, with a 4.68% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Industrial Fasteners Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Automotive and Aerospace Manufacturing | +1.2% | United States and Mexico | Medium Term (2–4 Years) |

| Rapid Growth of North American EV Supply Chain | +0.9% | United States Core, Mexico Hubs | Short Term (≤2 Years) |

| Growth of the Construction Sector | +0.7% | United States and Canada | Medium Term (2–4 Years) |

| Advances in Corrosion-Resistant Coatings | +0.4% | Region-Wide | Long Term (≥4 Years) |

| Buy-American Acts Driving Local Sourcing | +0.5% | United States | Long Term (≥4 Years) |

| Digital Traceability and Smart-Fastener Initiatives | +0.3% | United States and Canada | Long Term (≥4 |

| Source: ���ϲ����� | |||

Understand The Key Trends Shaping This Market

Download PDF

Expansion Of Automotive and Aerospace Manufacturing

Ongoing multi-billion-dollar plant expansions by General Motors and Stellantis are translating into long-run orders for aluminum-compatible bolts and self-locking nuts that prevent galvanic corrosion inside battery packs. Hyundai is building the largest single automotive complex in U.S. history, an investment scheduled to come online in 2027 and consume roughly 150 million fasteners each year. Aerospace output is also climbing, with GE Aerospace adding turbine capacity in Ohio, which is boosting demand for nickel-based Inconel 718 screws capable of withstanding temperatures above 650 °C. Certified suppliers who can trace heat lots and meet NADCAP audit requirements have a competitive edge, pushing less-equipped rivals toward commodity niches. Collectively, these moves compress lead times for specialty parts and intensify local content requirements across the North America industrial fasteners market.

Rapid Growth Of North American EV Supply Chain

Battery gigafactories added 58 GWh of nameplate capacity in 2025, introducing demand for stainless-steel and aluminum fasteners engineered to ISO 16047 torque standards.[1]International Council on Clean Transportation, “North America Battery Manufacturing Capacity Report,” theicct.org Tesla’s Texas plant alone used about 80 million fasteners during the year, with M6 and M8 aluminum bolts topping the volume list. EV powertrains eliminate thousands of combustion-engine screws, yet battery enclosures, inverter housings, and motor mounts require vibration-resistant designs that survive intense thermal cycling. Argonne National Laboratory notes that forging capacity is struggling to keep pace with EV ramp-ups, stretching lead times for custom parts. Suppliers capable of drop-in design support and regional warehousing are therefore securing long-term volume commitments.

Growth Of The Construction Sector

Non-residential construction spending is trending 3.1% higher for 2025, led by data center builds that specify seismic-rated bolts and corrosion-proof coatings [2]American Institute of Architects, “Consensus Construction Forecast,” aia.org. Infrastructure funding under the Bipartisan Infrastructure Law is driving steady orders for hot-dip galvanized anchor bolts in highway and bridge projects. While single-family starts dipped amid high mortgage rates, multifamily and industrial projects offset the slowdown, providing mixed volume but richer margin profiles for fasteners meeting ASTM A325 and A490 specifications. The construction rebound supports stable baseline growth across the North America industrial fasteners market, especially for distributors with job-site vending programs that capitalize on just-in-time deliveries.

Advances In Corrosion-Resistant Coatings

The EPA’s ban on hexavalent chromium is accelerating migration toward trivalent alternatives, zinc-nickel alloy plating, and PTFE topcoats that meet 1,000-hour salt-spray tests without carcinogenic by-products. SAE research finds PTFE finishes cut installation torque by as much as 30%, reducing galling on stainless threads and trimming assembly times in aerospace production.[3]SAE International, “Study on PTFE Coating Performance in Aerospace Applications,” sae.org Automotive OEMs now mandate zinc-nickel coatings for underbody components exposed to de-icing salts, prompting plating shops to overhaul chemistry controls. Dorken’s Delta-Protekt solution is gaining share after demonstrating extended corrosion life while remaining compliant with new regulations. These shifts lift average selling prices and raise qualification barriers for offshore suppliers, reinforcing domestic share in the North America industrial fasteners market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Steel And Non-Ferrous Metal Prices | -0.8% | North America | Short Term (≤ 2 Years) |

| Rising Adoption Of Structural Adhesives | -0.6% | United States And Canada | Medium Term (2–4 Years) |

| Stringent Environmental Regulations On Plating | -0.4% | United States | Medium Term (2–4 Years) |

| Reshoring-Led Capacity Bottlenecks For Specials | -0.3% | United States | Short Term (≤ 2 Years) |

| Source: ���ϲ����� | |||

Rising Adoption Of Structural Adhesives

Henkel’s automotive adhesives unit grew 12% in 2025, displacing bolts in body-in-white assemblies where weight savings reach 12 kilograms per vehicle. Adhesives distribute load, reduce corrosion, and enhance NVH, motivating OEMs to redesign joint architectures. 3M acrylic foam tapes and Sika polyurethane systems now secure exterior trims and battery trays, trimming cycle times and tooling complexity. Serviceability concerns persist, so hybrid solutions pairing low-count fasteners with bonding agents are emerging. Fastener makers respond with screw-and-adhesive combos that cure in situ, but net demand pressure remains negative for basic hardware across the North America industrial fasteners industry.

Volatility In Steel And Non-Ferrous Metal Prices

Benchmark hot-rolled coil traded between USD 700 and USD 900 per ton in 2025, whipsawing annual contracts and squeezing margins for standard-grade fastener suppliers.[4]World Steel Association, “Global Crude Steel Production Statistics,” worldsteel.org Nickel touched USD 22,000 per ton, inflating stainless-steel costs just as EV battery demand accelerated, boosting nickel demand. Aluminum premiums remain elevated due to Section 232 tariffs, adding USD 400 per ton to domestic purchases. While larger distributors hedge and diversify sources, smaller fabricators lack liquidity for inventory carries, creating uneven supply reliability and occasional line stoppages for OEMs. Persistent price swings remain a headwind for the North America industrial fasteners market.

Segment Analysis

By Material – Metal Dominance Masks Specialty Gains

Metal fasteners accounted for 84.23% of 2025 revenue, underscoring their entrenched role in automotive crash structures, machinery housings, and steel-frame construction. Carbon steel meets most volume requirements thanks to favorable strength-to-cost ratios, while alloy and stainless grades serve higher-tensile or corrosive applications, such as underbody suspension points and chemical-processing equipment. Plastic clips and push-pins thrive in dashboards, white goods, and electronics where dielectric insulation or scratch avoidance matters more than high pull-out strength. Composite and specialty options, although niche, are expanding at a 4.62% CAGR as OEMs fight weight while guarding against galvanic corrosion between metals and carbon-fiber substrates.

Rapid shifts in product design are recasting bill-of-material choices. Airbus and Boeing have increased their composite fuselage share, driving the adoption of CFRP screws that match the thermal expansion of airframes and avoid galvanic couples. Titanium Grade 5 bolts, priced at more than USD 50 per kilogram, hold a secure position in jet engines and orthopedic implants where biocompatibility and 3:1 strength-to-weight superiority over stainless steel remain decisive. In the North America industrial fasteners market, PennEngineering’s self-clinching studs for thin aluminum casings reduced strip-out failures by 30%, demonstrating how process innovation can boost specialty penetration. PEEK screws, meanwhile, win spinal fixation work because they are radiolucent on post-op imaging, a clinical benefit that justifies a tenfold premium over 316L stainless alternatives.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Grade – High-Performance Segment Captures Premium Applications

Standard-grade bolts conforming to ASTM A307 and SAE Grade 2 delivered 67.13% of 2025 turnover, riding construction and MRO staples where cost and immediate availability outweigh deeper engineering metrics. These fasteners move through distribution hubs in pallet quantities, with branch managers optimized for line-item fill rate rather than tensile curve education. Price erosion remains an issue, so scale logistics and automated picking stand out as the only sustainable levers for margin defense in this layer of the North America industrial fasteners market.

High-performance grades are charting a 4.49% CAGR into 2031 by shadowing electrification, LNG projects, and advanced civil aircraft. Grade 8 carbon-alloy bolts, heat-treated to 150,000 psi tensile, populate agricultural sprayers and heavy haulers that encounter extreme torsion. Metric Grade 10.9 studs now anchor EV motor mounts because regenerative braking subjects joints to higher reversed-stress cycles than gasoline engines. Howmet’s USD 28 million Inconel 718 line widens the moat around nickel-based fasteners that hold turbine sections together above 650 °C. KAMAX’s proprietary post-quench temper raised fatigue life 25%, granting OEMs more warranty cushion and fetching 40% price premiums that buoy overall value captured within the North America industrial fasteners market.

By Product Type – Application-Specific Variants Lead Innovation

Externally threaded products, namely bolts, screws, and studs, generated 52.13% of 2025 revenue by spanning everything from drywall screws to aircraft-grade titanium bolts. Nuts, inserts, and other internally threaded pieces trail but mirror demand because every bolt needs a mate. Rivets, pins, and retaining rings round out non-threaded categories that support permanent or one-way assemblies in aerospace skins and consumer electronics. Yet the application-specific subset is growing the fastest, at 4.87%, as OEMs ask suppliers to consolidate sealing, vibration damping, and grounding into a single engineered part.

Innovation stories abound: PennEngineering’s broaching studs create their own internal mating surface, removing a tapping step and cutting assembly time by 18 seconds per EV battery tray. Simpson Manufacturing pairs laser-cut brackets with preinstalled nails, letting framers meet seismic codes without field calculations. Bossard is piloting sensor-embedded rivets that tally load cycles and feed data into predictive-maintenance dashboards, a design that commercial airlines are eyeing for real-time structural health. TriMas disclosed that engineered specials captured gross margins 12 points higher than catalog items, confirming that feature integration is the fastest path to profit uplift in the North America industrial fasteners market.

By End-User Application – OEM Segment Drives Specification Evolution

OEMs accounted for 47.35% of the North America industrial fasteners market in 2025 and will grow at a 4.56% CAGR as automakers, aircraft builders, and machinery firms pursue localized supply chains. Electric vehicles shed roughly 700 fasteners when engines and transmissions disappear, yet add new torque-critical joints in battery housings, inverters, and e-axles that demand narrow preload windows and conductive coatings for thermal pathways. A single commercial jet harbors more than 2 million fasteners, split across titanium, Inconel, and aluminum variants, each tagged to heat-lot certifications that raise unit economics to USD 15.

Heavy equipment and agricultural OEMs continue to specify Grade 8 or ASTM A490 bolts to tolerate shock loads and corrosive fertilizer exposure. MRO remains indispensable: Fastenal’s 100,000-strong vending fleet dispenses screws and washers on plant floors, logging pull data and auto-reordering to reduce line stoppages by 30%. Construction contractors purchase pallet loads of hot-dip galvanized rods for concrete anchor applications tied to the Bipartisan Infrastructure Law pipeline. Together, these demands cement OEMs as the bellwether while keeping aftermarket and site-build channels integral to volume stability across the North America industrial fasteners market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Coating And Finish – PTFE Variants Gain On Regulatory Tailwinds

Zinc plating, with a 39.02% share in 2025, remains relevant by offering sacrificial protection at a price accessible to most production budgets. Electro-plated layers between 5 µm and 25 µm serve indoor or moderate exposure, whereas hot-dip galvanized coatings above 50 µm endure roadside salt and marine spray but carry a 60% cost premium. Plain, uncoated steel maintains a niche in climate-controlled interiors and disposable fixtures where penny-pinching trumps performance considerations.

Specialty coatings, led by PTFE, zinc-nickel, and hybrid silane layers, are growing at 4.91% through 2031 because they straddle compliance, assembly, and lifecycle cost. PTFE finishes lower the required drive torque by as much as 30%, cutting battery-pack assembly time that would otherwise require powered tools to be calibrated every shift. Zinc-nickel formulations pass 1,000-hour salt-spray tests and meet OEM underbody rules without carcinogenic chromium, securing back-to-back approvals from multiple Detroit Three automakers in 2025. Nanoceramic topcoats for medical implants resist autoclave sterilization, preventing pitting and maintaining thread class after repeated cycles. By delivering extended field life and regulatory peace of mind, specialty finishes are a high-margin lever for suppliers entrenched in the North America industrial fasteners market.

Geography Analysis

The United States generated 73.67% of 2025 demand, fueled by aerospace clusters in Washington, Texas, and South Carolina and an automotive corridor stretching from Michigan through Tennessee to Georgia. Boeing programs alone absorbed roughly 400 million fasteners, while federally backed infrastructure poured USD 110 billion into road and bridge work that specified ASTM and AASHTO bolts. Fastenal, Wurth, and MSC Industrial Supply stock branch networks capable of next-day coverage, underpinning a service expectation that shapes buying patterns across the North America industrial fasteners market.

Mexico is on a 4.68% CAGR trajectory through 2031, leveraging USMCA content rules that encourage OEMs to localize stamping, battery, and sub-assembly lines south of the border. Guanajuato, Puebla, and Aguascalientes host vehicle plants from General Motors, Stellantis, and Volkswagen, each fostering ecosystems of tier-one fastener cold forgers. Aerospace primes now authorize Mexican vendors for titanium lugs and Inconel studs, using Hermosillo and Monterrey as logistics bridges into Arizona and Texas final-assembly plants.

Canada trails in share but remains strategically interlocked with U.S. supply chains. Ontario’s auto belt relies on timely shipments from Midwestern fastener makers, and Quebec’s aerospace scene around Montreal feeds Bombardier and Pratt and Whitney programs that consume AS9100-certified titanium screws. Exchange rate swings dictate cautious inventory holds, so distributors center stock near Toronto and Quebec City to shorten customs cycles. Overall, complementary growth across the three nations sustains regional output and innovation momentum for the North America industrial fasteners market.

Competitive Landscape

Roughly 45% of 2025 revenue accrued to the top 10 suppliers, indicating moderate fragmentation. No single company surpasses an 8% share, so competitive levers center on service models, certification scope, and engineered product breadth rather than price alone. Fastenal and Wurth embed over 100,000 vending machines that lock in MRO spend and provide real-time data, reducing customer stockouts by 40%. Manufacturers such as Illinois Tool Works cross-sell powertrain-specific fasteners through captive distribution networks, shielding margins from pure-play resellers.

Vertical integration is deepening: Howmet Aerospace forges titanium bar, machines close-tolerance screws, heat-treats them in-house, and validates through NADCAP labs, collapsing external lead time. Bossard leverages SmartBin weight sensors to trigger cloud-based replenishment orders, trimming on-site stock by one-third and freeing working capital for OEM users. Patent filings highlight corrosion-resistant coatings, self-locking geometries, and sensor integration, revealing where incremental value creation lies in the North America industrial fasteners market.

Specialists are exploiting profitable niches. ARaymond push-in clips replaced screws in door-panel programs, cutting 25 seconds per vehicle from line time. Optimas consolidates vendor-managed inventory for mid-tier OEMs lacking internal procurement scale, and TriMas secured AS9100 Rev D to bid on U.S. defense work. While barriers to entry remain moderate for commodity parts, aerospace and automotive accreditation standards create defensible moats, reinforcing the current moderate concentration dynamic.

North America Industrial Fasteners Industry Leaders

Illinois Tool Works Inc.

Howmet Aerospace Inc.

Stanley Black and Decker, Inc.

Würth Group

Fastenal Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2026: Howmet Aerospace confirmed a USD 35 million expansion in Torrance, California, to boost titanium and Inconel capacity for next-generation aircraft.

- November 2025: Illinois Tool Works recorded 8% organic growth in automotive fasteners after proprietary aluminum-safe coatings secured multiple EV contracts.

- September 2025: Stanley Black and Decker divested its industrial fastener distribution unit for USD 1.2 billion to concentrate on power-tool and storage lines.

- August 2025: Fastenal installed its 100,000th automated vending machine, citing 15% higher retention among vending accounts versus branch-only customers.

- June 2025: Wurth opened a 250,000 sq ft automated distribution hub in Dallas, cutting order-picking time 35%.

North America Industrial Fasteners Market Report Scope

The North America Industrial Fasteners Market Report is Segmented by Material (Metal, Plastic, Composite and Specialty), Grade (Standard, High-Performance), Product Type (Externally Threaded, Internally Threaded, Non-Threaded, Application-Specific/Specialty), End-User Application (OEM, MRO, Construction), Coating/Finish (Plain, Zinc-Plated, Hot-Dip Galvanized, PTFE and Specialty Coatings), and Geography (United States, Canada, Mexico). Market Forecasts are Provided in Terms of Value (USD).

By Material

| Metal |

| Plastic |

| Composite and Specialty |

By Grade

| Standard |

| High-Performance |

By Product Type

| Externally Threaded |

| Internally Threaded |

| Non-Threaded |

| Application-Specific/Specialty |

By End-User Application

| OEM | Motor Vehicles/Automotive | ICE Light Vehicles |

| ICE Medium and Heavy Trucks/Buses | ||

| Electric Vehicles | ||

| Aerospace | ||

| Machinery and Capital Goods | ||

| Electrical and Electronics | ||

| Fabricated Metals | ||

| Medical Equipment | ||

| Other OEM Applications | ||

| Maintenance, Repair and Operations (MRO) | ||

| Construction |

By Coating/Finish

| Plain (Uncoated) |

| Zinc-Plated |

| Hot-Dip Galvanized |

| PTFE and Specialty Coatings |

By Country

| United States |

| Canada |

| Mexico |

| By Material | Metal | ||

| Plastic | |||

| Composite and Specialty | |||

| By Grade | Standard | ||

| High-Performance | |||

| By Product Type | Externally Threaded | ||

| Internally Threaded | |||

| Non-Threaded | |||

| Application-Specific/Specialty | |||

| By End-User Application | OEM | Motor Vehicles/Automotive | ICE Light Vehicles |

| ICE Medium and Heavy Trucks/Buses | |||

| Electric Vehicles | |||

| Aerospace | |||

| Machinery and Capital Goods | |||

| Electrical and Electronics | |||

| Fabricated Metals | |||

| Medical Equipment | |||

| Other OEM Applications | |||

| Maintenance, Repair and Operations (MRO) | |||

| Construction | |||

| By Coating/Finish | Plain (Uncoated) | ||

| Zinc-Plated | |||

| Hot-Dip Galvanized | |||

| PTFE and Specialty Coatings | |||

| By Country | United States | ||

| Canada | |||

| Mexico | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected size of the North America industrial fasteners market by 2031?

The market is forecast to reach USD 27.17 billion.

Which material segment is growing the fastest?

Composite and specialty fasteners are expanding at a 4.62% CAGR through 2031.

Why are specialty coatings such as PTFE gaining share?

They provide superior corrosion protection and comply with EPA chromium bans while reducing installation torque by up to 30%.

Which country offers the highest growth rate in the region?

Mexico, with a forecast 4.68% CAGR, driven by expanding automotive and aerospace production.

How are distributors using technology to retain customers?

Firms like Fastenal deploy IoT-enabled vending machines that automate replenishment and improve retention by 15%.

What impact do structural adhesives have on mechanical fastener demand?

Adhesives replace some bolts in body-in-white assemblies, reducing vehicle weight, though hybrid joints still use fewer high-specification fasteners.