North America Healthy Snack Chips Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

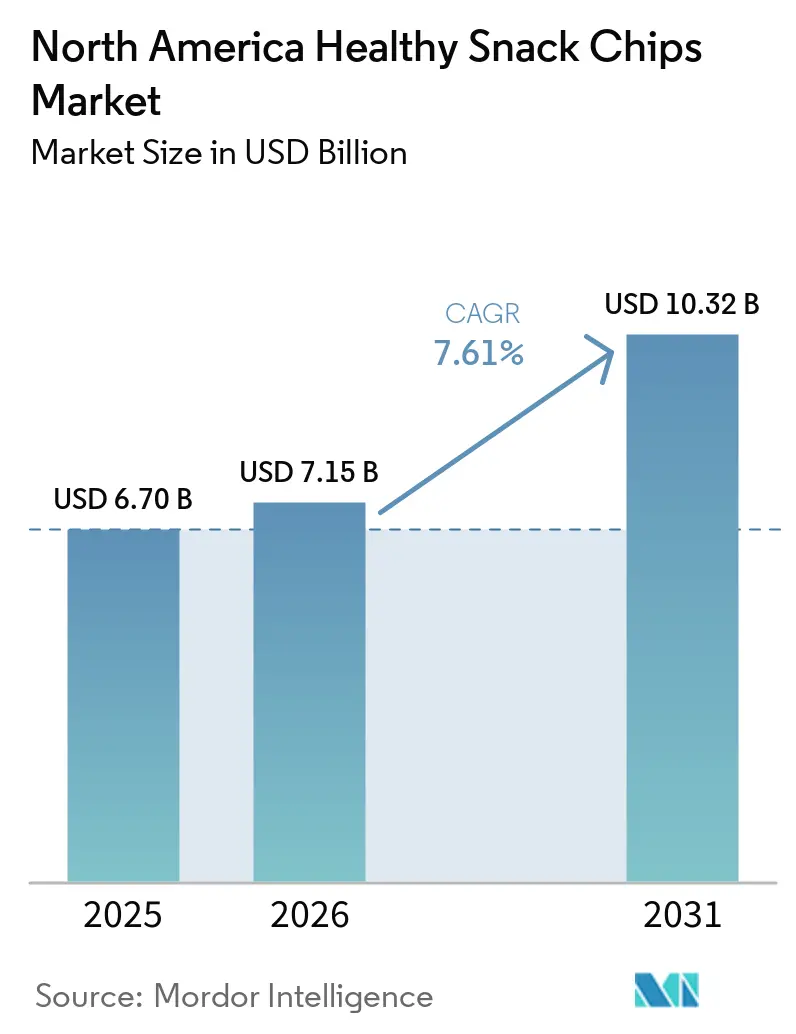

| Base Year Market Size (2025) | USD 6.70 Billion |

| Market Size (2026) | USD 7.15 Billion |

| Market Size (2031) | USD 10.32 Billion |

| Growth Rate (2026 - 2031) | 7.61% CAGR |

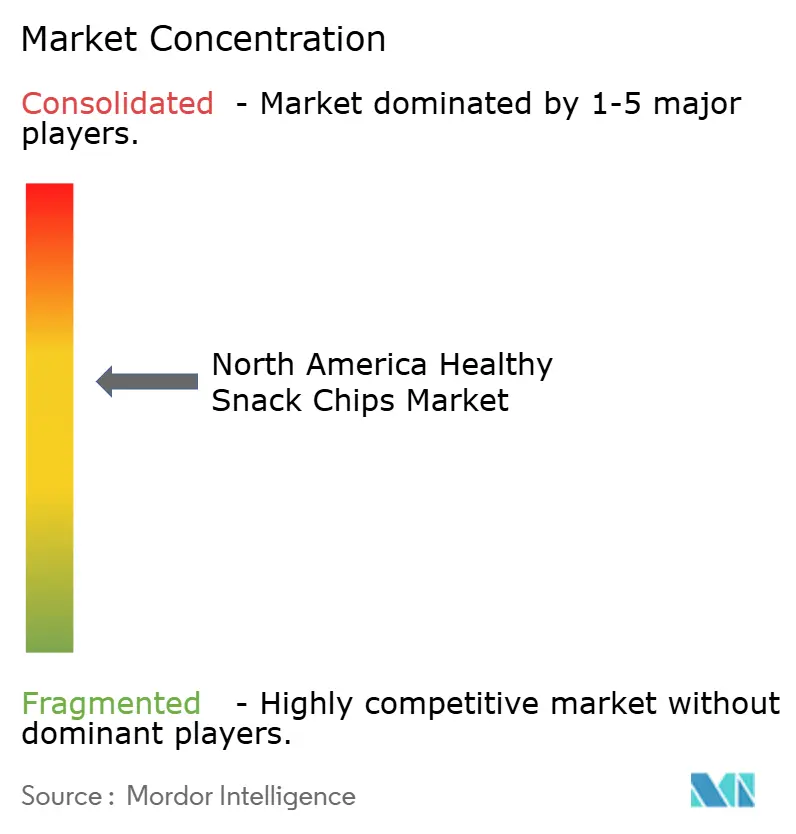

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

North America Healthy Snack Chips Market Analysis by ���ϲ�����

The North America healthy snack chips market size was valued at USD 6.70 billion in 2025 and estimated to grow from USD 7.15 billion in 2026 to reach USD 10.32 billion by 2031, at a CAGR of 7.61% during the forecast period (2026-2031). Rising focus on wellness and transparent ingredient sourcing is pushing snack chip manufacturers in North America to reformulate offerings with natural additives, whole-grain inputs, and added protein. Leading brands are reinforcing their core portfolios while also acquiring emerging niche players to maintain competitive positioning on retail shelves. At the same time, supply-side pressures such as climate-driven disruptions in raw materials, along with shifting consumer behavior influenced by appetite-suppressing treatments, are moderating overall volume expansion. The continued growth of online grocery platforms, accounting for a notable share of total food sales, has eased market entry for smaller and innovative brands. Regionally, Mexico is witnessing faster growth due to improving disposable incomes and increased spotlight on indigenous ingredients, while Canada’s market expansion is supported by strong demand for organic products and a growing e-commerce ecosystem.

Key Report Takeaways

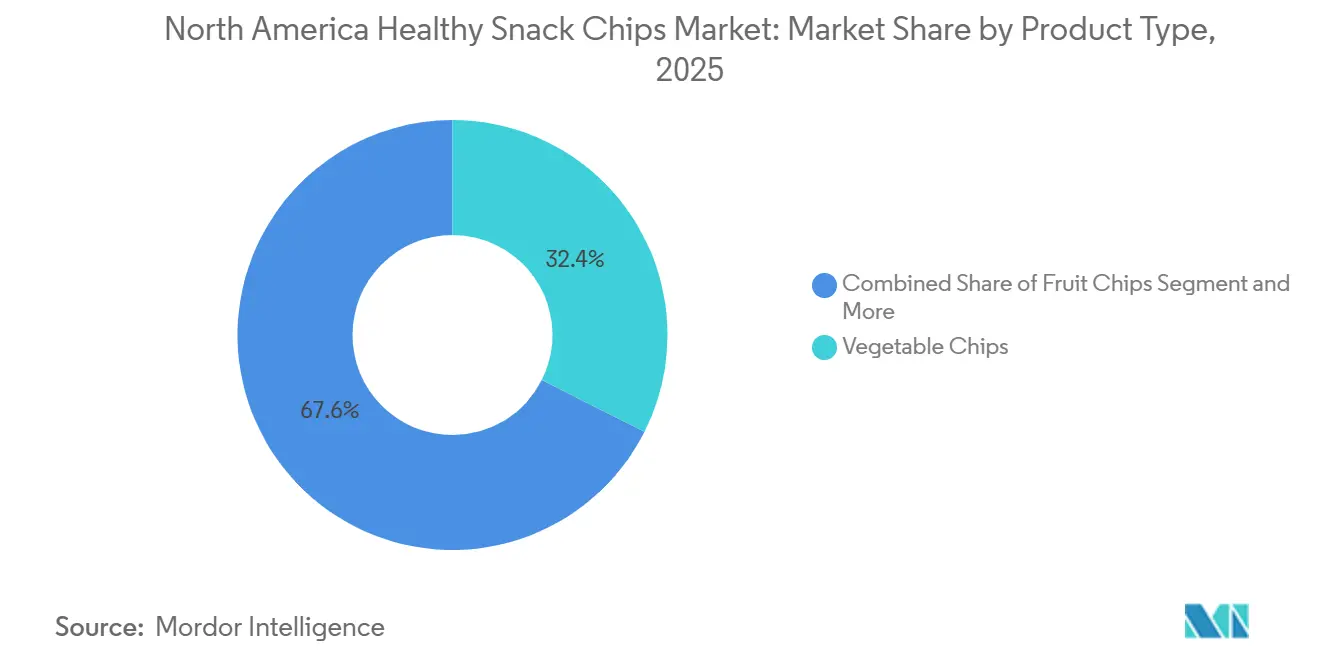

- By product type, vegetable chips led the 2025 sales with 32.43% of the market share, while protein-enhanced chips are projected to post the fastest growth at 9.86% CAGR through 2031.

- By ingredient source, plant-based formulations accounted for 78.65% of category revenue in 2025; animal-based options anchored by animal-based formulations are expanding at 8.21% CAGR.

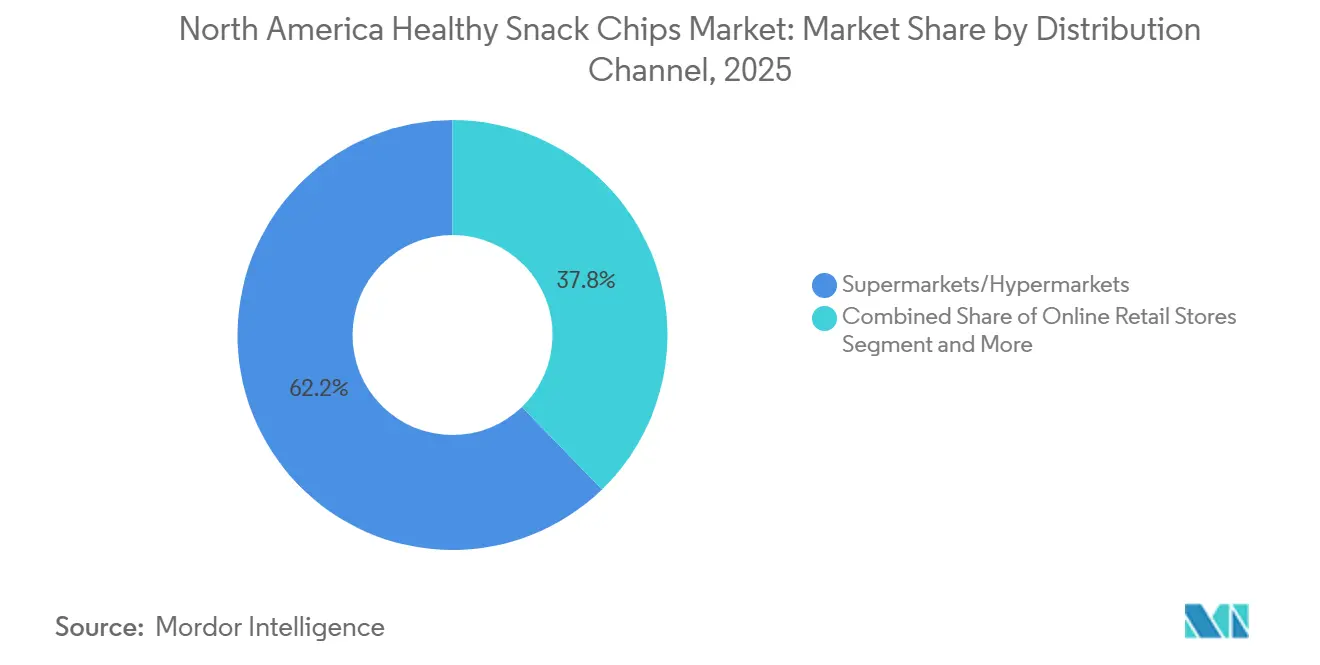

- By distribution channel, supermarkets/hypermarkets held 62.85% of 2025 sales, yet online retail is forecast to grow at 9.32% CAGR and is reshaping launch strategies for emerging brands.

- By geography, the United States captured 76.34% of 2025 value, whereas Mexico is poised for the highest geographic advance at 9.25% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Healthy Snack Chips Market Trends and Insights

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health awareness boosting demand for better-for-you snack chips | +1.20% | Regional, with strongest gains in United States and Canada | Medium term (2-4 years) |

| Growing preference for plant-based and gluten-free options | +1.00% | North America, with early adoption in urban United States markets and Mexico City | Medium term (2-4 years) |

| Increased focus on clean-label, natural ingredients | +0.90% | United States and Canada, spillover to Mexico premium segments | Short term (≤ 2 years) |

| Strong branding and marketing by key players to stand out | +0.80% | United States, with digital-first campaigns in Canada | Short term (≤ 2 years) |

| Shift toward healthier oil alternatives in formulations | +0.90% | United States and Canada, with pilot launches in Mexico | Medium term (2-4 years) |

| Demand for chips aligned with diets like keto, paleo, and intermittent fasting | +0.70% | United States, with niche growth in Canada | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising health awareness is boosting demand for better-for-you snack chips

With 82% of consumers prioritizing wellness and 75% recently purchasing natural or organic products, consumer health awareness has reached a tipping point. This heightened consciousness is also influencing spending behavior, as nearly 52% of consumers are willing to pay a premium for snack products aligned with specific dietary preferences and nutritional goals [1]Lesley Simeon, "Sustainability premium: 53% of consumers willing to pay 10% extra for sustainable food and drink", 2024, business.yougov.com. In the North America healthy snack chips market, demand is increasingly shifting toward chips formulated with plant-based ingredients, high protein content, lower sodium, and clean-label positioning. Younger consumers, particularly millennials and Gen Z, are actively replacing conventional fried snacks with functional and better-for-you alternatives that support fitness and lifestyle needs. Retailers and convenience chains are expanding shelf space for keto-friendly, vegan, gluten-free, and protein-enriched chip variants to capture evolving consumer preferences. Additionally, brands emphasizing authentic nutritional value, transparent ingredient sourcing, and functional health benefits are strengthening long-term market positioning and driving sustained category growth.

Growing preference for plant-based and gluten-free options

Plant-derived snack chips continue to gain strong traction across the North American healthy snack chips market, supported by rising demand for clean-label, nutrient-rich, and environmentally responsible food options. Consumers across the United States, Canada, and Mexico are increasingly shifting toward flexitarian eating habits, encouraging brands to introduce chips made from lentils, peas, cassava, nuts, and other vegetable-based ingredients. The growing preference for minimally processed snacks with natural colors, gluten-free claims, and non-GMO positioning is further accelerating innovation in the category. Regulatory support for naturally sourced ingredients and colors is also helping manufacturers strengthen plant-forward product appeal while reducing reliance on artificial additives. At the same time, healthier formulations featuring high protein, fiber enrichment, and functional ingredients are attracting wellness-focused consumers seeking guilt-free snacking alternatives. Although premium pricing remains a barrier for mass-market penetration, the expanding consumer base for sustainable and plant-based snacks is creating opportunities for brands to develop affordable products without compromising on taste or texture.

Increased focus on clean-label, natural ingredients

In the North America healthy snack chips market, clean-label transformation is increasingly becoming a core business requirement rather than a promotional strategy. PepsiCo plans to remove artificial ingredients from its Lay’s and Tostitos portfolios by the end of 2025, reflecting the region’s growing emphasis on transparent and healthier snack formulations [2]Snack Food & Wholesale Bakery, "PepsiCo snacks to be free from artificial colors by the end of 2025", 2025, www.snackandbakery.com. The company’s expansion of products free from artificial colors and flavors has already generated multi-billion-dollar revenues, highlighting strong consumer demand for better-for-you snacking options. Emerging brands are also reformulating products with nutrient-rich ingredients such as avocado oil and higher protein content to strengthen premium positioning and capture health-conscious consumers. Sustainability is further shaping innovation strategies, with manufacturers investing in eco-friendly packaging formats that reduce greenhouse gas emissions and align with retailer sustainability goals. Although these initiatives require significant investments in reformulation and R&D, they enable companies to command premium pricing, improve brand differentiation, and foster long-term consumer loyalty across the regional snack chips industry.

Strong branding and marketing by key players to stand out

In the North American healthy snack chips market, brands are increasingly strengthening promotional strategies to stand out in an intensely competitive environment. Utz Brands significantly increased advertising investments to accelerate organic sales growth, while emphasizing premiumization and brand visibility across retail shelves. WILDE Brands expanded its consumer outreach through experiential campaigns, including athletic-event sponsorships and in-store sampling, following strong investor backing. At the same time, private-label manufacturers are capitalizing on value-driven purchasing trends and “dupe” positioning, rapidly gaining traction among cost-conscious consumers. The expansion of online grocery and e-commerce snack distribution channels across the United States and Canada is further pushing brands to optimize digital engagement and influencer-led marketing initiatives. Rising customer acquisition costs are also encouraging companies to adopt data-driven and highly targeted promotional approaches to improve marketing efficiency and maximize return on investment.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-related disruptions impacting raw material consistency | -0.50% | United States (Idaho, Colorado, Nebraska), with spillover to Canada | Short term (≤ 2 years) |

| Evolving regulatory and labeling requirements | -0.30% | United States and Canada, with Mexico following | Medium term (2-4 years) |

| Rising competition from substitute healthy snack options | -0.40% | United States, with early signs in Canada and Mexico | Short term (≤ 2 years) |

| Workforce constraints in sourcing regions | -0.30% | United States (Red River Valley, Idaho), limited Canada impact | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Climate-related disruptions impacting raw material consistency

Climate variability and raw material supply fluctuations are intensifying cost pressures across the North American healthy snack chips market, particularly for specialty oils, seasonings, and clean-label ingredients sourced from a concentrated supplier network. Adverse weather events and geopolitical instability have disrupted the availability of key edible oils and agricultural inputs, resulting in sharp procurement cost spikes. According to the Food and Agriculture Organization (FAO) Food Price Index, the FAO Vegetable Oil Price Index averaged 138.2 points in 2024, reflecting a 9.4% increase over 2023 due to reduced global supply and ongoing supply chain disruptions [3]Food and Agriculture Organization, "FAO Price Index", 2024, grain-protrade.com. Premium ingredients such as organic, non-GMO, and sustainably certified components often command prices 2–3 times higher than conventional alternatives during supply shortages. Additionally, extended lead times and limited sourcing options for certified sustainable ingredients are complicating inventory planning for manufacturers. To mitigate these risks, companies are increasingly adopting multi-sourcing strategies, strengthening supplier partnerships, and investing in vertically integrated supply chains. However, persistent ingredient price volatility and logistics uncertainties continue to pressure operating margins across the market.

Evolving regulatory and labeling requirements

Evolving regulatory requirements across North America, including stricter front-of-pack labeling rules, sodium reduction targets, and anticipated updates to GRAS standards, are increasing compliance costs for healthy snack chip manufacturers. Companies are being compelled to invest in packaging redesigns, ingredient reformulation, and scientific validation to support health-related claims. These regulatory pressures are particularly challenging for smaller brands, which often lack the financial scale to absorb rising operational and certification expenses. As a result, some emerging players may streamline product portfolios or limit new product launches to maintain profitability. In addition, growing regulatory harmonization under regional trade agreements is encouraging greater alignment of food standards across the United States, Canada, and Mexico, requiring brands to adopt more coordinated product development strategies. Over the medium term, these compliance demands are expected to strengthen the competitive position of established companies with larger R&D, legal, and supply chain capabilities in the North America healthy snack chips market.

Segment Analysis

By Product Type: Protein-Enhanced Chips Drive Innovation

Vegetable chips accounted for 32.43% of the North America healthy snack chips market in 2025, supported by rising consumer preference for minimally processed, plant-based snacking alternatives. Products made from sweet potatoes, beets, kale, and other recognizable vegetables continue to gain traction due to their natural appeal, vibrant appearance, and perceived health benefits. Leading brands such as Terra and Sensible Portions have strengthened category penetration through broad flavor portfolios and strong retail visibility. The segment also benefits from growing clean-label demand, as consumers increasingly shift away from conventional potato chips toward snacks positioned around natural ingredients and wellness-focused claims.

Protein-enhanced chips are projected to register the fastest growth, advancing at a 9.86% CAGR through 2030 as consumers seek snacks that combine convenience with functional nutrition. The category is witnessing strong momentum among fitness-conscious, keto, and high-protein consumers looking for products that deliver satiety and nutritional value beyond traditional snacking. Companies such as WILDE Chips and Legendary Foods are expanding offerings with high-protein formulations derived from chicken, egg whites, and dairy-based ingredients, allowing brands to command premium pricing. Continued innovation in flavor, texture, and nutrient fortification is expected to further accelerate adoption across the North American market.

By Ingredient Source: Plant-Based Dominance Faces Animal-Based Challenge

Plant-based ingredients accounted for a dominant 78.65% share of the North American healthy snack chips market in 2025, supported by strong consumer preference for sustainable, clean-label, and minimally processed products. Brands are increasingly leveraging innovative plant-derived inputs such as legumes, seaweed, mushrooms, and upcycled vegetables to differentiate offerings while maintaining cost efficiency and broad consumer appeal. The segment continues to benefit from growing demand for organic and Non-GMO products, particularly across urban retail channels in the U.S. and Canada. In addition, manufacturers are introducing hybrid formulations and enhanced flavor technologies to improve texture, taste, and nutritional value, further strengthening plant-based leadership across the category.

Animal-based snack chips, although comparatively smaller in market share, are projected to expand at the fastest CAGR of 8.21% through 2030, driven by rising adoption of protein-rich and low-carbohydrate dietary lifestyles such as keto and paleo. Demand is particularly accelerating in premium snack segments, where consumers are seeking high-protein, functional alternatives with complete amino acid profiles. Products made from chicken, beef, and other animal proteins are gaining traction among fitness-focused consumers due to their perceived nutritional superiority and satiety benefits. Moreover, ongoing product innovation and wider retail penetration by companies offering meat-based chips are helping normalize the category and support its rapid market expansion.

By Distribution Channel: E-Commerce Disrupts Traditional Retail

Supermarkets and hypermarkets accounted for 62.85% of the North American healthy snack chips market in 2025, supported by extensive shelf visibility, strong in-store promotional activity, and high impulse purchase rates. These retail formats continue to benefit from established consumer shopping patterns and strategic category placements that encourage both product discovery and repeat purchases. Retailers are increasingly expanding their health-focused snack assortments, while private-label penetration and cross-merchandising initiatives are intensifying competition within the segment. The growing presence of clean-label, organic, and functional snack chips across mainstream grocery aisles further reinforces the channel’s dominance.

Online retail stores are projected to witness the fastest growth, registering a CAGR of 9.32% through 2030, driven by rising consumer preference for convenience, home delivery, and subscription-based purchasing models. E-commerce platforms are becoming key distribution channels for premium and niche healthy snack chip brands that require detailed product information, ingredient transparency, and targeted consumer engagement. Digital marketing strategies, direct-to-consumer expansion, and personalized promotions are further accelerating online sales momentum. Additionally, the increasing adoption of omnichannel retail strategies is enabling brands to strengthen customer retention and improve long-term revenue generation across the North American market.

Geography Analysis

The United States accounted for 76.34% of the North America healthy snack chips market in 2025, supported by strong consumer preference for premium and better-for-you snacking products, widespread retail penetration, and rapid innovation in protein-rich and clean-label offerings. Growing demand for functional chips aligned with keto, paleo, and high-protein diets continues to strengthen market maturity, while e-commerce platforms are enabling emerging healthy snack brands to expand their consumer reach. In addition, private-label expansion is intensifying competition, pushing established brands to differentiate through ingredient transparency, nutritional benefits, and premium positioning. Product innovation remains a key growth lever, highlighted by retail initiatives introducing healthier snack assortments tailored to evolving consumer preferences.

Mexico is projected to register the fastest growth in the North America healthy snack chips market, expanding at a CAGR of 9.25% through 2030. Rising health awareness, a growing middle-class population, and increasing demand for affordable healthier snacking alternatives are supporting market momentum. The country’s strong food processing industry and streamlined regional trade networks are improving supply-chain efficiency for snack manufacturers. Furthermore, growing interest in plant-based and vegetable-based chips is encouraging innovation in localized flavors and formulations tailored to regional taste preferences.

Canada continues to witness stable market expansion, driven by increasing consumer inclination toward organic, non-GMO, and minimally processed snack chips. The country benefits from well-developed retail infrastructure and strong alignment with clean-label regulations that emphasize ingredient transparency and product quality. Canadian consumers are demonstrating higher willingness to pay for premium and health-focused snack alternatives, encouraging brands to diversify their better-for-you portfolios. At the same time, specialty health retailers and online grocery platforms are improving product accessibility and supporting broader adoption of healthy snack chips across urban consumer groups. The broader North American region, including parts of Central America and the Caribbean, is also witnessing gradual demand growth supported by urbanization and increasing exposure to health-oriented food products.

Competitive Landscape

North America’s healthy snack chips industry remains moderately consolidated, with concentration estimated at 6 out of 10 as established food companies continue reshaping portfolios through health-oriented acquisitions and category expansion. Strategic deals such as Mars’ acquisition of Kellanova, PepsiCo’s purchase of Siete Foods, and The Hershey Company’s takeover of LesserEvil reflect growing emphasis on functional and clean-label snacking portfolios.

Competitive intensity is rising as private-label manufacturers strengthen shelf presence and pressure branded players to differentiate through premium ingredients, protein fortification, and lifestyle-focused positioning. Demand for keto-, paleo-, and protein-centric products continues to accelerate, encouraging brands to invest in personalized nutrition concepts, advanced formulation capabilities, and automated manufacturing technologies to improve speed and efficiency.

Innovation and transparency are becoming key competitive levers across the category. Companies are increasingly emphasizing sustainable packaging solutions, traceable sourcing, and clinically aligned nutrition claims to strengthen consumer trust. Emerging brands such as WILDE and Legendary Foods are gaining traction through high-protein differentiation, digital-first marketing, and strategic retail collaborations, highlighting how operational agility and targeted brand storytelling are reshaping market dynamics.

North America Healthy Snack Chips Industry Leaders

-

PepsiCo, Inc.

-

Utz Brands

-

Hain Celestial Group

-

Campbell Soup Co.

-

Siete Family Foods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Graza expanded its product portfolio with the relaunch of its popular olive oil potato chips, introducing it as a permanent offering in four upgraded flavors including Classic Sea Salt, Salt & Vinegar, Hot ’n Sweet, and Zesty Caesar. The chips are made using specially sourced yellow potatoes fried in 100% extra-virgin olive oil, delivering a lighter and crispier texture compared to the earlier limited-edition launch.

- February 2026: Ancient Crunch announced the retail expansion of its tallow-fried MASA tortilla chips and Vandy potato crisps across major grocery chains, including Whole Foods Market and Sprouts Farmers Market. The company also unveiled its upcoming “Golden Age Popcorn” line, further strengthening its clean-label snack portfolio focused on grass-fed beef tallow, organic ingredients, and seed oil-free formulations.

- March 2026: PepsiCo launched Smartfood FiberPop and SunChips Fiber snacks in the U.S., expanding its high-fiber better-for-you snack portfolio. The products target rising demand for functional and digestive-health-focused snacking options.

North America Healthy Snack Chips Market Report Scope

| Vegetable Chips |

| Fruit Chips |

| Legume and Pulse Chips |

| Grain and Seed Chips |

| Protein-Enhanced Chips |

| Sweet Potato Chips |

| Beef Chips |

| Other Product Types |

| Plant-Based |

| Animal-Based |

| Hybrid Blends |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Vegetable Chips |

| Fruit Chips | |

| Legume and Pulse Chips | |

| Grain and Seed Chips | |

| Protein-Enhanced Chips | |

| Sweet Potato Chips | |

| Beef Chips | |

| Other Product Types | |

| By Ingredient Source | Plant-Based |

| Animal-Based | |

| Hybrid Blends | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Country | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is the projected value of the North America healthy snack chips market by 2030?

The market is forecast to reach USD 9.6 billion by 2030, growing at a 7.48% CAGR.

Which product segment is expanding the quickest?

Protein-enhanced chips are posting a 10.97% CAGR and are the fastest-growing segment.

How significant is online retail for healthy snack chips in North America?

Online channels are expanding at a 13.48% CAGR, outpacing all other distribution formats.

Which major acquisitions signal strategic shifts toward healthier portfolios?

Mars-Kellanova, PepsiCo-Siete Foods, Hershey-LesserEvil, and Flowers Foods-Simple Mills all illustrate large players doubling down on better-for-you snacking

Page last updated on: