Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

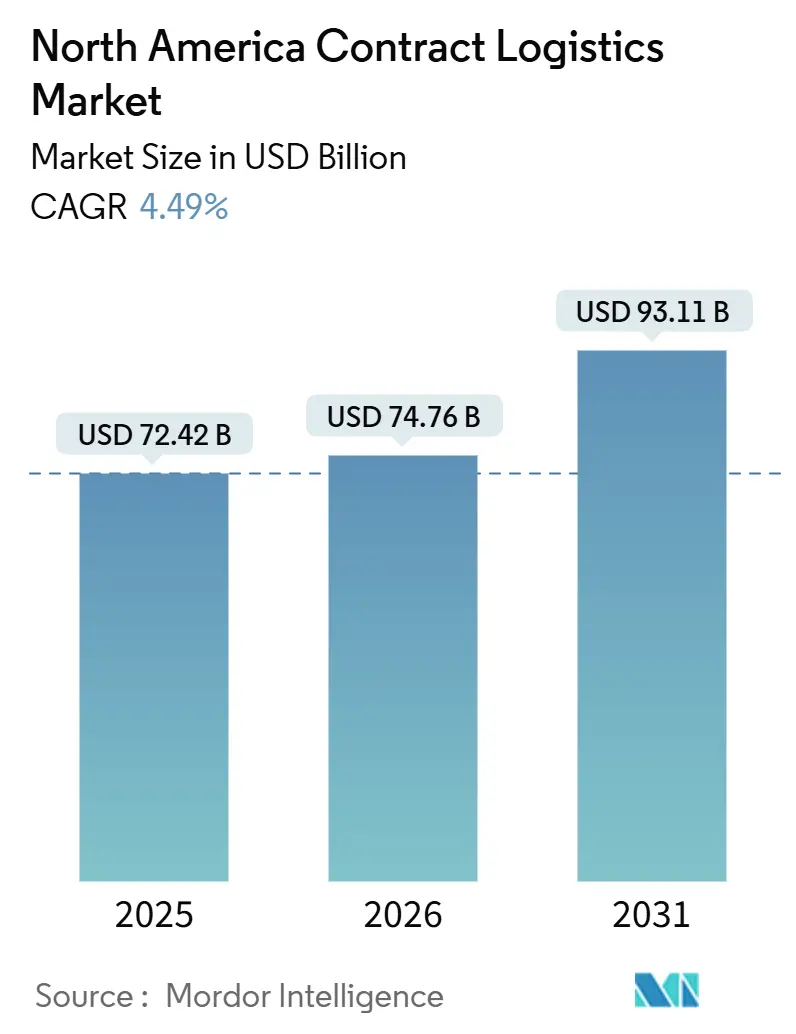

| Base Year Market Size (2025) | USD 72.42 Billion |

| Market Size (2026) | USD 74.76 Billion |

| Market Size (2031) | USD 93.11 Billion |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

North America Contract Logistics Market Analysis by ���ϲ�����

The North America contract logistics market size is projected to be USD 72.42 billion in 2025 and USD 74.76 billion in 2026, and reach USD 93.11 billion by 2031, growing at a CAGR of 4.49% from 2026 to 2031.

Automation retrofits, cold-chain investments, and urban micro-fulfillment hubs are changing cost structures and service models across the region. Providers are redirecting capital from greenfield projects to robotics upgrades in existing facilities, a move that limits exposure to land shortages in tier-1 metros. Specialized temperature-controlled capacity is expanding in response to biologics production and meal-kit adoption, while retailers are embedding compact, goods-to-person systems inside city limits to protect sub-one-day delivery promises. Cross-border corridors handling electric-vehicle battery materials and real-time visibility platforms that knit together multiple carriers are reinforcing the growth runway for the North America contract logistics market.

Key Report Takeaways

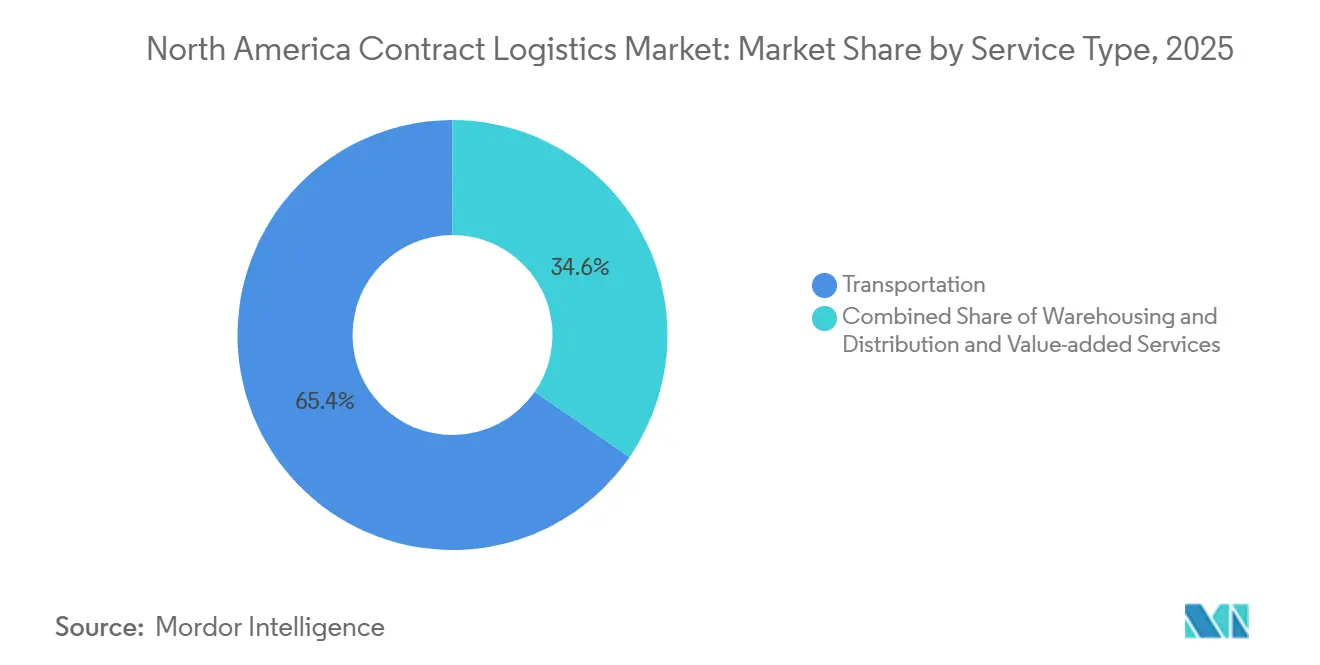

- By service type, transportation commanded 65.38% of the North America contract logistics market share in 2025, while value-added services are projected to post the fastest 5.90% CAGR through 2031.

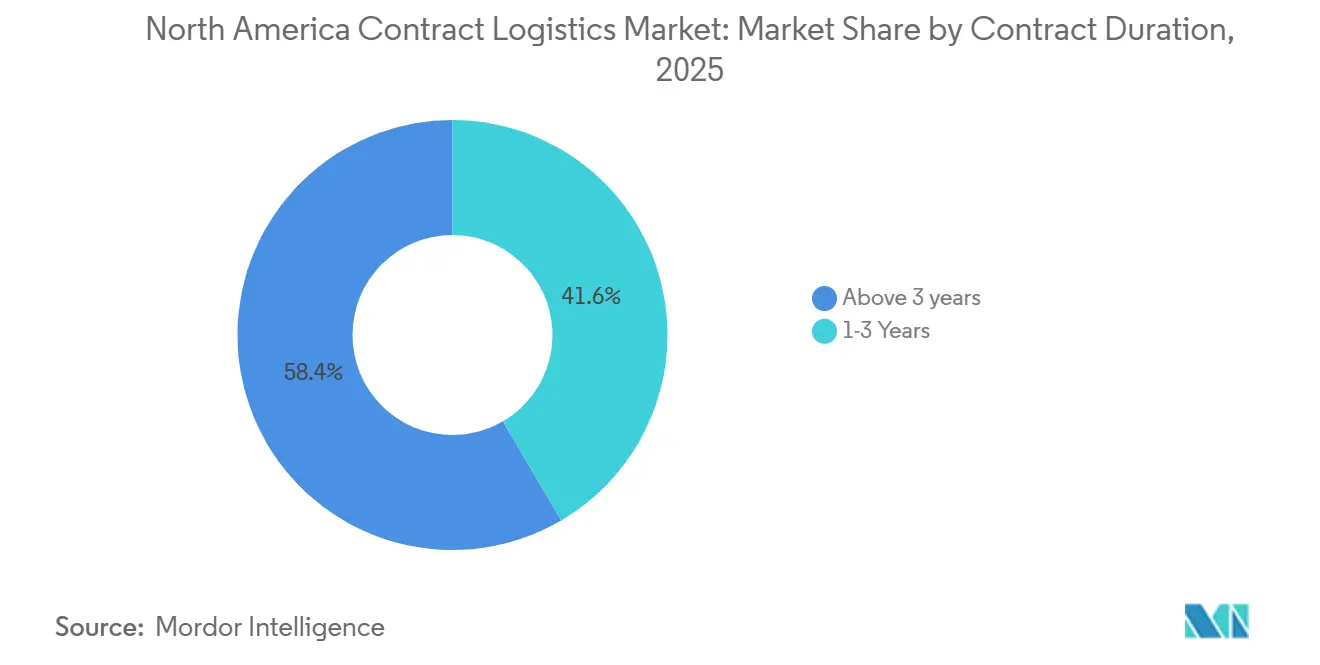

- By contract duration, agreements longer than three years held 58.44% of the North America contract logistics market size in 2025 and are forecast to expand at a 5.36% CAGR to 2031.

- By end-user industry, manufacturing and automotive together accounted for 31.20% of 2025 revenue, whereas healthcare and pharmaceuticals are advancing at a 6.05% CAGR through 2031.

- By country, the United States commanded 86.12% of the North America contract logistics market share in 2025, while Mexico is the fastest-growing country at a 5.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Contract Logistics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid automation-first retrofits in legacy DCs | +1.2% | United States industrial corridors, Ontario | Short term (≤ 2 years) |

| Cold-chain surge from biologics and meal-kit commerce | +0.9% | United States Northeast, California | Medium term (2-4 years) |

| Micro-fulfillment build-outs for sub-one-day delivery | +0.7% | Top United States and Canadian metros | Short term (≤ 2 years) |

| EV-battery materials trade corridors | +0.5% | Mexico-United States Southwest, Ontario-Michigan | Long term (≥ 4 years) |

| Real-time visibility and 4PL orchestration platforms | +0.6% | United States enterprise adopters | Medium term (2-4 years) |

| State-level tax credits in the United States South | +0.4% | Southeast and Texas Triangle | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rapid Automation-first Retrofits in Legacy DCs

Contract logistics providers are modernizing existing distribution centers with autonomous mobile robots and modular goods-to-person systems to sidestep land shortages and cut payback periods to 12-18 months. Cobots that assist with case picking now cost 30% less than in 2024, accelerating network-wide roll-outs. Retrofit projects typically lift productivity 35-40%, allowing providers to scale throughput for e-commerce peaks without the delays tied to new construction[1]“Battery Supply Chain Development 2025,” U.S. Department of Energy, energy.gov.

Cold-chain Surge from Biologics and Meal-kit Commerce

Biologics already constitute 35% of drug pipelines and demand temperatures as low as -80 °C, driving a USD 2.8 billion jump in cold-storage build-outs during 2025. Parallel demand stems from meal-kit services that require multi-zone facilities for frozen, chilled, and ambient goods. Dual-use warehouses that service both life-science and food customers are improving asset utilization while real-time tracking tools document chain-of-custody to satisfy stricter audits[2]“Tax Credits and Incentives 2025,” Georgia Department of Economic Development, georgia.org.

Micro-fulfillment Buildouts for Sub-one-day Delivery

Urban retailers opened 63% more micro-fulfillment centers in 2025, each spanning just 10,000-20,000 sq-ft but packing 3-4 times the pick density of manual operations. Last-mile costs typically fall 25-30% when orders originate from an urban hub rather than a suburban mega-site. Grocers are repurposing under-performing outlets into dark stores, gaining proximity to customers without competing for scarce industrial plots.

EV-battery Materials Trade Corridors

Lithium shipments from Mexico to United States cell plants rose by 127% in 2025, increasing demand for hazmat handling and nitrogen-purged containers. Cross-dock sites on both sides of the border reduced customs delays and stabilized high-volume flows. These improvements strengthened the EV-battery materials corridor. The contract logistics sector is projected to capture USD 4.2 billion in corridor spending by 2026. Growth is driven by rising cell-grade materials traffic and safety-compliant transport capacity.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute shortage of industrial real estate in tier-1 metros | -0.8% | United States coasts, Toronto, Vancouver | Short term (≤ 2 years) |

| Diesel-price volatility compressing margins | -0.5% | Long-haul corridors | Short term (≤ 2 years) |

| Heightened cross-border security protocols | -0.4% | Major United States gateways | Medium term (2-4 years) |

| Escalating liability insurance from "nuclear" verdicts | -0.6% | Litigation-prone United States states | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Acute Shortage of Industrial Real Estate in Tier-1 Metros

North America's Tier-1 logistics hubs face tight vacancy rates despite national oversupply. In 2025, Los Angeles had a 1.6% vacancy rate, while Toronto's York submarket and the City of Toronto recorded 1.7% and 2.1%, respectively. Small-bay, last-mile facilities in dense metros remain in high demand, with vacancy rates under 5%. This scarcity near major population centers, which drive 75% of logistics demand, forces operators into competitive infill markets[3]“Diesel Fuel Prices 2025,” U.S. Energy Information Administration, eia.gov.

Diesel-price Volatility Compressing Margins

Diesel-price volatility is impacting North American contract logistics, with 2025 pump prices fluctuating sharply due to geopolitical and supply-chain pressures. Rising diesel costs are tightening logistics budgets, with United States prices climbing year-over-year and squeezing margins. Providers face challenges in passing on these costs in a competitive market, leading to intensified margin compression. Pump price swings between USD 3.20 and USD 4.85 per gallon, and lagging fuel-surcharge formulas expose providers to unplanned cost spikes. Shippers capping surcharges shift more price risk onto providers, further eroding profitability[4]“Advanced Trade Analytics Platform 2025,” U.S. Customs and Border Protection, cbp.gov.

Segment Analysis

By Service Type: Automation Drives Value-Added Services Acceleration

Transportation held 65.38% of the North America contract logistics market share in 2025, anchored by road freight’s reach across the United States-Mexico lanes. Value-added services, however, will expand at a 5.90% CAGR, boosted by demand for postponement, kitting, and labeling work that trims clients’ inventory holding costs. The segment’s ascent shows how the North America contract logistics market size is shifting toward integrated solutions, not mere carriage or storage.

Automation underpins the upswing. Light-assembly cells, RFID print-and-apply lines, and camera-based quality checks shorten order-to-ship cycles while lifting accuracy above 99.9%. Providers that pair robotics with Six-Sigma practices are capturing premium rates and locking-in multi-year contracts. Rail and intermodal now challenge long-haul trucking on lanes above 750 miles, offering 20-30% savings with three-day service windows. Dedicated air charters shore up the spare-parts and pharma niches, reinforcing a multimodal fabric that keeps the North America contract logistics market resilient to one-mode disruptions.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Contract Duration: Long-Term Commitments Enable Infrastructure Investments

Longer agreements represented 58.44% of the North America contract logistics market size in 2025, and are estimated to grow at a 5.36% CAGR through 2031, mainly because multi-year visibility justifies capital-heavy automation and warehouse retrofits. Performance-based clauses tie fees to order accuracy and inventory turns, aligning incentives across the life of a contract.

Shorter 1-3-year deals still serve brands trialing new markets or coping with seasonality, yet the pandemic taught shippers that spot reliance risks capacity shocks. As a result, dual-sourcing strategies are emerging: a primary 3PL holds the bulk under a five-year term, while a challenger handles overflow to keep innovation pressure alive.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Healthcare Outpaces Traditional Manufacturing

Manufacturing and automotive retained 31.20% revenue in 2025 through sequencing and just-in-time models that depend on near-border warehousing. Even so, healthcare and pharmaceuticals are running ahead with a 6.05% CAGR, reflecting personalized medicine, specialty drug launches, and direct-to-patient deliveries, all of which need verified temperature control and serialized tracking.

Food and beverage users demand multi-zone storage that satisfies HACCP and lot-level traceability, whereas chemical shippers look for hazmat-trained crews and compliant storage. Retailers and e-commerce players insist on fast returns processing, another pocket where the North America contract logistics market continues to innovate through scalable reverse-logistics networks.

Geography Analysis

The United States accounted for roughly 86.12% of North America contract logistics market value in 2025, leveraging dense highway, rail, and air networks plus mature warehouse clusters around major consumer basins. Canada contributes principally via cross-border trade, with Ontario facilities feeding United States auto plants and British Columbia ports funneling Pacific imports. United States-Canada truck and rail lanes moved goods worth USD 761 billion in 2024.

Mexico is the fastest-growing geography with 5.81% CAGR for 2026-2031 as near-shoring draws electronics and auto parts plants south of the border. Bilateral trade with the United States hit USD 798 billion in 2024, and warehouse starts in Tijuana, Juarez, and Nuevo Laredo surged 67% during 2025. Providers are stitching CPKC rail corridors to run single-line service from Canadian ports through Midwestern hubs to Mexican factories, a spine that departs from coastal overloads.

Regionally, the United States Southeast and Texas Triangle absorbed 38% of new industrial builds in 2025. State incentives and labor pools lure capacity from the Northeast and Midwest, where land constraints and higher costs dilute ROI. Laredo processed USD 282 billion in truck freight during 2024, growing 8.2% per year as the Pacific-Southwest lane captures freight once routed by sea from Asia.

Competitive Landscape

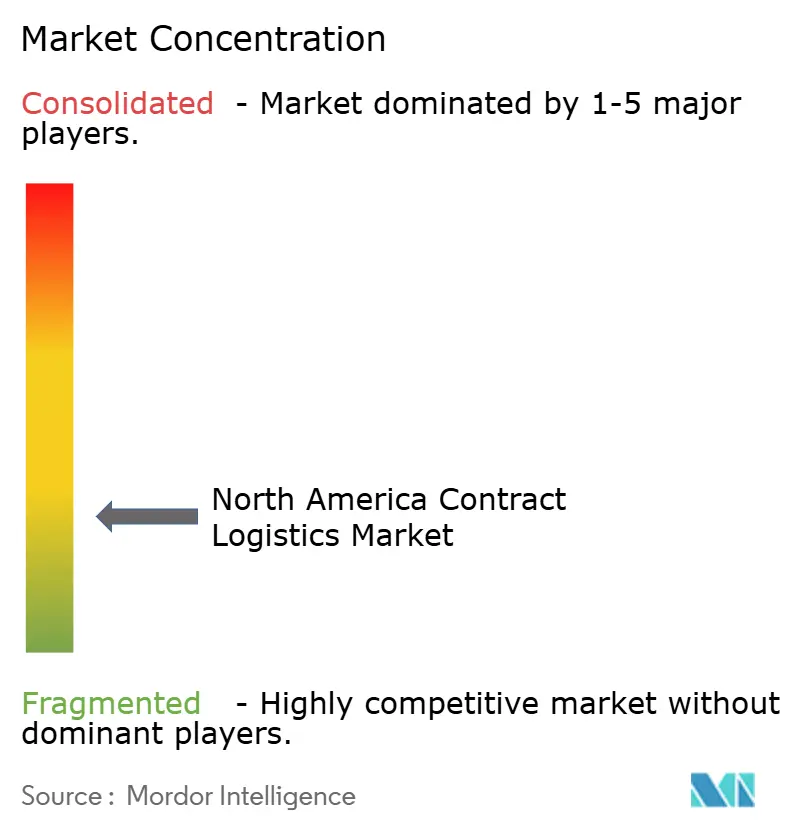

The North America contract logistics market shows low concentration. Global integrators DHL Supply Chain, UPS Supply Chain Solutions, and FedEx Supply Chain pair worldwide reach with advanced IT stacks, while regionals such as GXO Logistics, NFI Industries, and Penske Logistics win share through sector depth or flexible pricing. Technology is redrawing competitive lines: AI forecasting, AMR fleets, and blockchain traceability create sticky customer relationships and lift operating margins beyond the historic 4-6% range.

Vertical specialization is deepening. Providers chasing healthcare must validate cold-chain chambers to USP 1079 standards, a hurdle that discourages generalists. Automotive specialists refine sequencing and line-side delivery for electric-vehicle components. White-space opportunities in battery recycling, ultra-cold gene-therapy storage, and 4PL orchestration are spawning niche entrants. Meanwhile, the DSV-Schenker merger establishes a USD 50 billion revenue giant, pressuring mid-tier players to either consolidate or double-down on focus areas.

Scale still matters: network density lowers empty miles and supports hub automation, yet intimacy with customer SOPs can outgun size in heavily regulated niches. As a result, the North America contract logistics market balances global heavyweights with agile specialists, a structure likely to persist over the forecast horizon.

North America Contract Logistics Industry Leaders

DHL Group

Kuehne+Nagel

XPO, Inc.

United Parcel Service of America, Inc.

Ryder System, Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2026: DHL Supply Chain and RLCold agreed to build 5 million sq ft of multi-temp space, targeting United States food customers.

- October 2025: DHL launched the ReTurn Network, a multi-client platform for e-commerce returns across the United States.

- July 2025: Lineage announced an 82,000-sq-ft Louisville cold-store expansion, adding 10,300 pallet slots to its temperature-controlled network.

- May 2025: DHL Supply Chain bought IDS Fulfillment, enlarging its North America contract logistics market footprint among SMB merchants.

North America Contract Logistics Market Report Scope

By Service Type

| Transportation | Road |

| Rail | |

| Air | |

| Sea | |

| Warehousing and Distribution | |

| Value-added Services (Assembly, Labelling, Kitting) |

By Contract Duration

| 1-3 Years |

| Above 3 years |

By End-user Industry

| Manufacturing and Automotive |

| Food and Beverage |

| Retail and E-commerce |

| Healthcare and Pharmaceuticals |

| Chemicals |

| Other Industries |

By Country

| United States |

| Canada |

| Mexico |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea | ||

| Warehousing and Distribution | ||

| Value-added Services (Assembly, Labelling, Kitting) | ||

| By Contract Duration | 1-3 Years | |

| Above 3 years | ||

| By End-user Industry | Manufacturing and Automotive | |

| Food and Beverage | ||

| Retail and E-commerce | ||

| Healthcare and Pharmaceuticals | ||

| Chemicals | ||

| Other Industries | ||

| By Country | United States | |

| Canada | ||

| Mexico |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How fast is the North America contract logistics market expected to grow to 2031?

The market is forecast to rise from USD 74.76 billion in 2026 to USD 93.11 billion by 2031, reflecting a 4.49% CAGR.

Which service type contributes most to value today?

Transportation services account for 65.38% of 2025 revenue, fueled by road freight’s dominance on cross-border routes.

What is driving investment in value-added services?

Manufacturers are outsourcing kitting, labeling, and postponement tasks, enabling the segment to post a 5.90% CAGR through 2031.

Why is healthcare logistics growing faster than other industries?

Biologics, DSCSA serialization, and direct-to-patient deliveries require specialized cold-chain and compliance capabilities, propelling a 6.05% CAGR.

Which geography is expanding capacity the quickest?

Mexico leads growth as near-shoring boosts demand for cross-border warehousing; 2025 construction in major border cities rose 67%.

How are providers mitigating real-estate shortages in tier-1 U.S. metros?

They retrofit existing facilities with automation, pursue multi-story designs, and shift capacity to incentive-rich Southern states.