Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

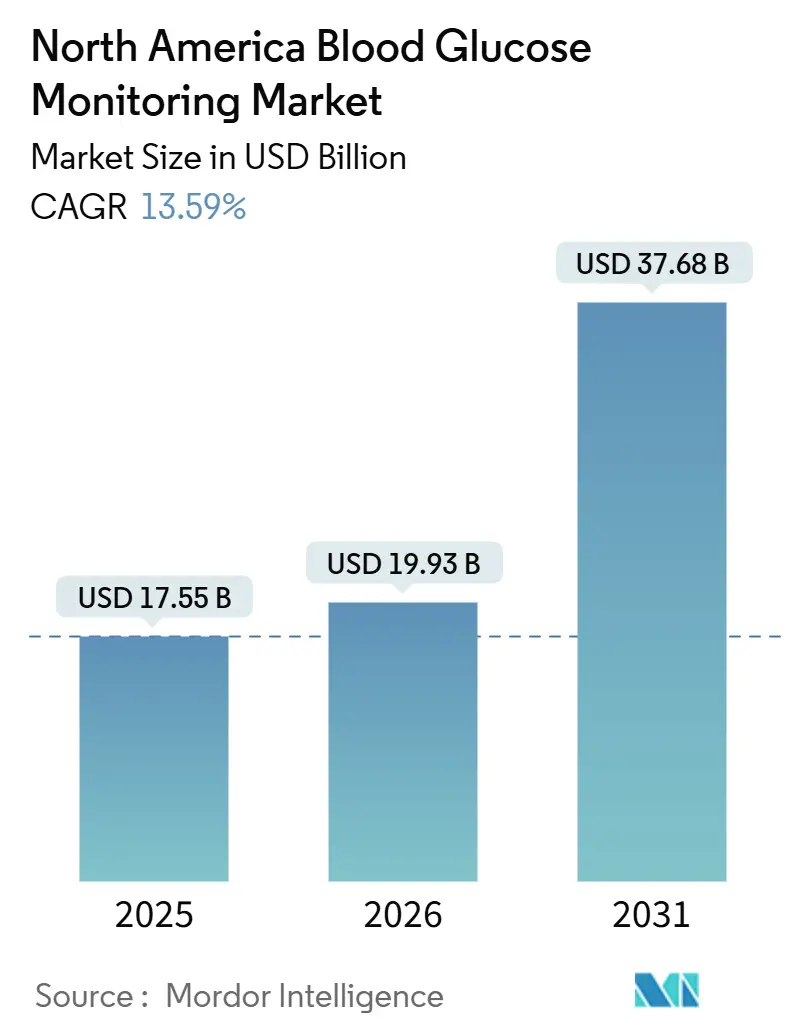

| Base Year Market Size (2025) | USD 17.55 Billion |

| Market Size (2026) | USD 19.93 Billion |

| Market Size (2031) | USD 37.68 Billion |

| Growth Rate (2026 - 2031) | 13.59% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

North America Blood Glucose Monitoring Market Analysis by ���ϲ�����

The North America Blood Glucose Monitoring Market size is projected to be USD 17.55 billion in 2025, USD 19.93 billion in 2026, and reach USD 37.68 billion by 2031, growing at a CAGR of 13.59% from 2026 to 2031.

Sensor reimbursement expansions, long-wear technology breakthroughs, and real-time data integration into artificial-intelligence diabetes platforms are compressing adoption timelines and shifting revenue away from legacy finger-stick meters. Expanded Medicare eligibility added 3.5 million potential continuous glucose monitoring (CGM) users in 2024, while over-the-counter (OTC) CGM entry has opened the retail channel to adults with type 2 diabetes who do not require prescriptions. Together, these policy and channel changes are catalyzing double-digit growth in the blood glucose monitoring market across North America.

Key Report Takeaways

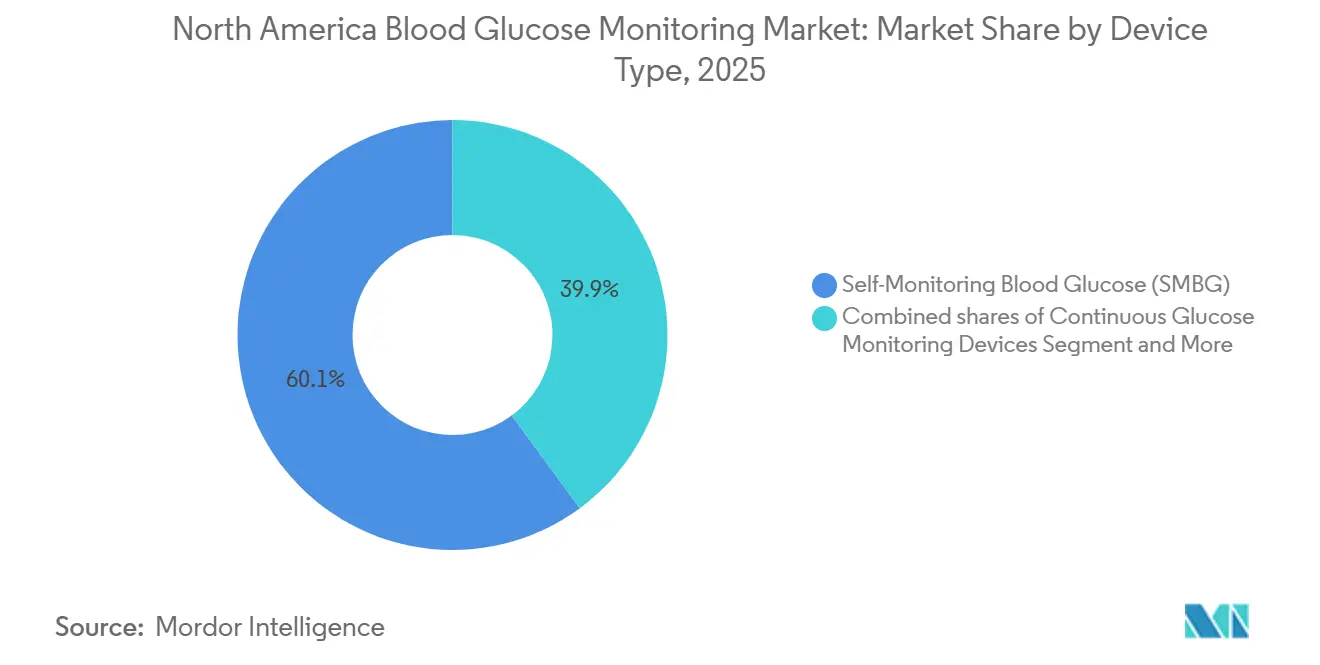

- By device, self-monitoring blood glucose (SMBG) devices led with 60.1% of the blood glucose monitoring market share in 2025, whereas CGM is projected to expand at 13.76% CAGR through 2031.

- By applications, diabetes-management applications accounted for 73.21% of the blood glucose monitoring market size in 2025, while health and wellness monitoring is forecast to grow at 14.78% between 2026 and 2031.

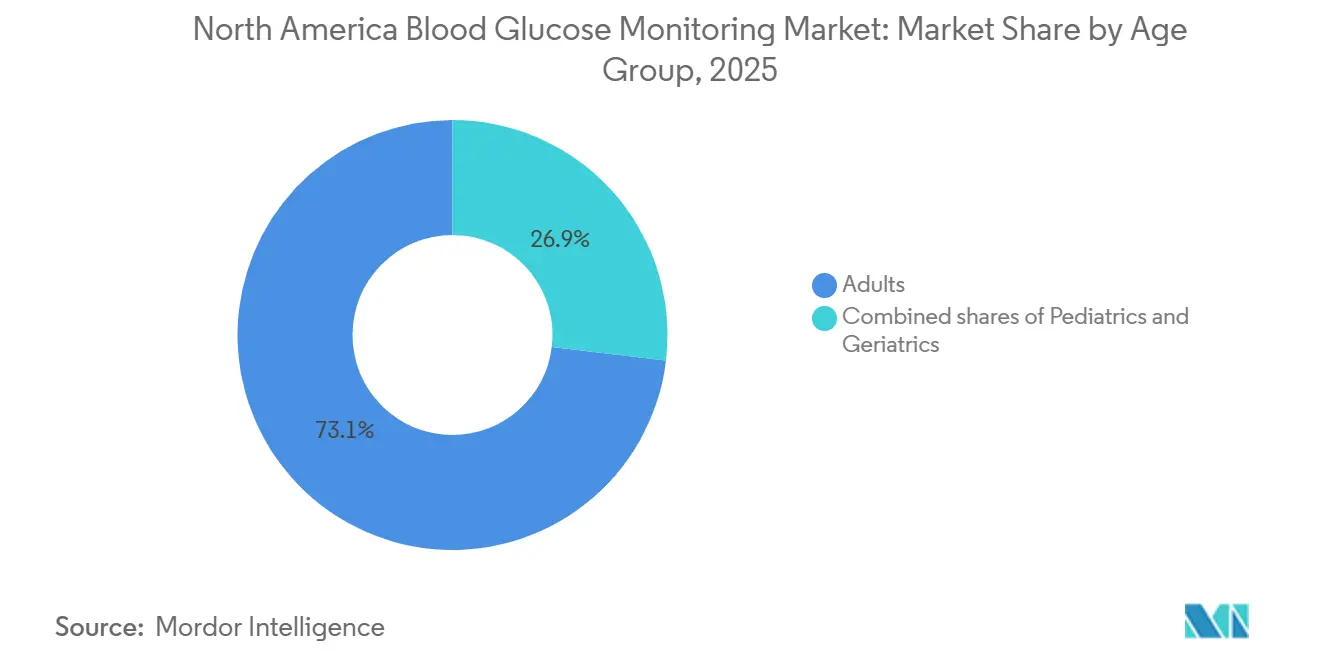

- By age group, adults represented 73.1% of users in 2025; the pediatric cohort is expected to grow at 15.6% CAGR through 2031.

- By test type, invasive test methods captured 61.65% share in 2025, whereas non-invasive systems are projected to post a 14.21% growth rate by 2031.

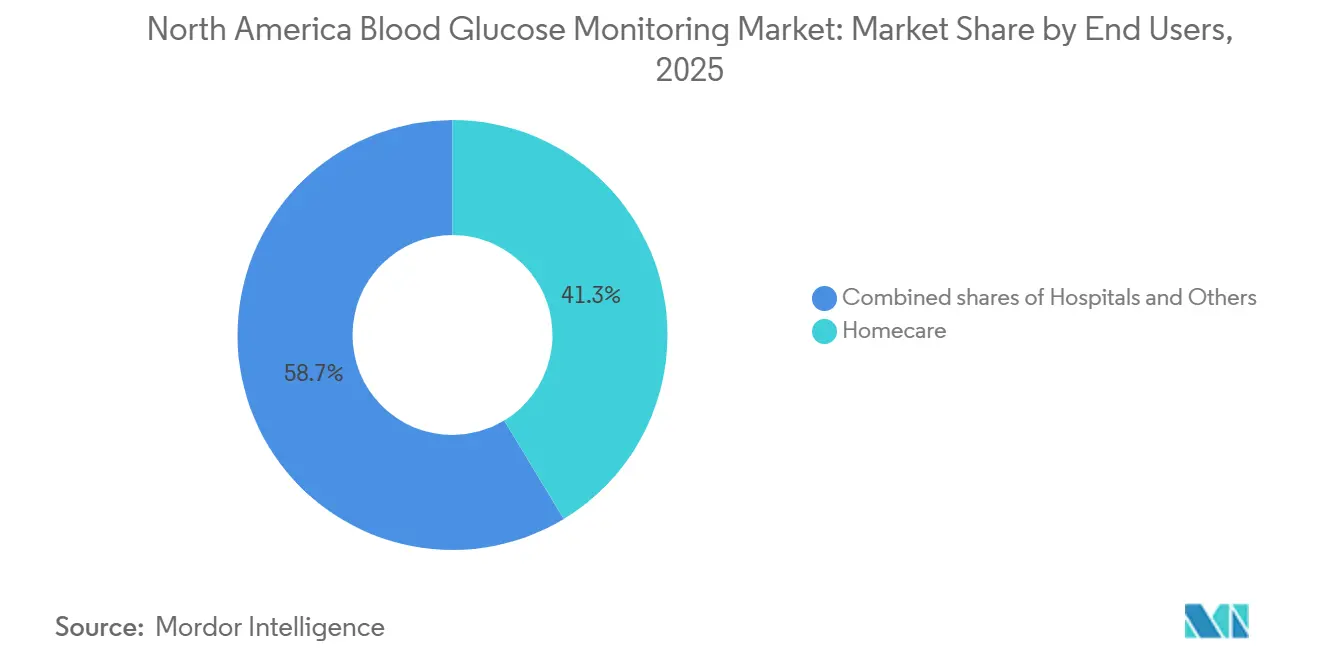

- By end users, homecare settings commanded 41.34% of 2025 revenue and are on a 15.11% expansion trajectory through 2031.

- By country, United States contributed 83.1% of regional value in 2025, while Mexico is poised to rise at 14.32% CAGR as public-sector procurement widens access.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Blood Glucose Monitoring Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Favorable Reimbursement Expansions (CMS, Private Payers) | +3.2% | United States, with spillover to Canadian provincial plans | Short term (≤ 2 years) |

| Technological Advances in Long-Wear CGM Sensors | +2.8% | North America, led by US FDA approvals and Canadian Health Canada clearances | Medium term (2-4 years) |

| Growing Type-2 Adoption of CGM Beyond Insulin Users | +2.5% | United States and Canada, early uptake in urban Mexico (Mexico City, Monterrey, Guadalajara) | Medium term (2-4 years) |

| Retail & OTC Channel Rollout for CGM Devices | +1.8% | United States, concentrated in CVS, Walgreens, and Walmart pharmacy networks | Short term (≤ 2 years) |

| Shift Toward Data-Driven, AI-Enabled Diabetes Platforms | +1.9% | United States and Canada, pilot programs in Mexico City and Monterrey | Long term (≥ 4 years) |

| Near-Shoring of Sensor Manufacturing Lowers Supply-Chain Risk | +1.2% | North America, with manufacturing hubs in Illinois, Arizona, and Monterrey | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Understand The Key Trends Shaping This Market

Download PDF

Favorable Reimbursement Expansions (CMS, Private Payers)

Medicare’s 2024 rule that broadened CGM coverage to non-intensive insulin users removed a historical barrier, doubling the eligible senior population to 5.3 million and driving a 47% prescription surge among Medicare Advantage members in 1H 2025. Commercial insurers mirrored the change and cut prior-authorization hurdles, enabling pharmacies to stock OTC CGMs nationwide. Accountable-care organizations are leveraging these benefits to trim emergency visits, accelerating revenue migration from SMBG to CGM and lifting overall blood glucose monitoring market momentum.

Technological Advances in Long-Wear CGM Sensors

Fourteen- and fifteen-day sensors such as FreeStyle Libre 3 and Dexcom G7 achieve mean absolute relative difference (MARD) scores below 8.5%, meeting insulin-dosing standards without finger-stick confirmation. Manufacturing gains from roll-to-roll electrode printing have trimmed unit costs by roughly 25% since 2024. Lower per-day monitoring costs make CGM price-competitive with multi-stick SMBG, stimulating hospital pilots and retail uptake across the blood glucose monitoring market.

Growing Type-2 Adoption of CGM Beyond Insulin Users

Updated ADA Standards now recommend CGM for adults who struggle to reach glycemic targets, independent of insulin intensity. Real-world data from Kaiser Permanente showed 0.8-point A1c reductions for non-insulin users versus 0.3 points with SMBG Self-insured employers have reacted by removing copays, betting that deferred insulin progression offsets program costs. These moves collectively expand the blood glucose monitoring market by attracting a previously underserved cohort.

Shift Toward Data-Driven, AI-Enabled Diabetes Platforms

Cloud analytics turn raw glucose streams into predictive insights. Dexcom Clarity’s 2025 release warns users up to 60 minutes before projected hypoglycemia. Abbott’s Libre data now feeds Tandem’s Control-IQ algorithm, allowing pumps to adjust basal rates every five minutes. FDA SaMD guidance imposes validation rigor, but ecosystem value outweighs compliance costs, underpinning the long-run expansion of the blood glucose monitoring market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Recurring Sensor & Strip Costs for Low-Income Users | -1.8% | United States, particularly rural areas and Medicaid-expansion states; Mexico's uninsured population | Short term (≤ 2 years) |

| Accuracy / Calibration Concerns in Extreme Glucose Ranges | -0.9% | North America, affecting all markets with focus on pediatric and geriatric populations | Medium term (2-4 years) |

| State-By-State Medicaid Coverage Disparities | -1.2% | United States, concentrated in non-expansion states (Texas, Florida, Georgia, Alabama) | Medium term (2-4 years) |

| Cyber-Security & Data-Privacy Compliance Costs (HIPAA, FDA) | -1.0% | United States and Canada, affecting all connected device manufacturers | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

High Recurring Sensor & Strip Costs for Low-Income Users

Uninsured and underinsured adults face list prices of USD 350 per month for CGM sensors and USD 60-150 for branded SMBG strips [1]Diabetes Patient Advocacy Coalition, “2025 Patient Cost Survey,” diabetespac.org. Cost burden leads to test rationing, raising risks of undetected hypo- and hyperglycemia. Although makers offer discount plans, enrollment caps leave many excluded, tempering near-term blood glucose monitoring market penetration in lower-income segments.

State-By-State Medicaid Coverage Disparities

Only 10 states provide unrestricted CGM access, whereas 22 restrict coverage to intensive insulin users [2]Kaiser Family Foundation, “Medicaid CGM Coverage Policies by State,” kff.org. Approval delays stretch to 90 days in Texas and Florida, depressing adoption rates among the 12 million Medicaid beneficiaries with diabetes in those jurisdictions. Fragmentation obliges suppliers to manage 50 reimbursement rules, inflating administrative overhead and dampening growth in the blood glucose monitoring market until policy harmonization materializes.

Segment Analysis

By Device Type: CGM Gains While SMBG Holds Volume

CGM revenue is set to eclipse SMBG despite SMBG's 60.1% blood glucose monitoring market share in 2025. CGM’s 13.76% growth rate reflects extended-wear sensors, OTC availability, and Medicare expansion. The blood glucose monitoring market size for CGM is projected to compound faster as cost-per-day falls and clinical accuracy rises [3]Abbott Laboratories, “Abbott Annual Report 2025,” abbott.com. SMBG remains entrenched in hospitals where point-of-care meters integrate with electronic health records, but even here, connected meters aim to mimic continuous data flow.

A bifurcated adoption pattern is emerging: majority of newly diagnosed type 1 children start on CGM within three months, yet elderly uptake lags due to interface complexity. Vendors are responding with simplified receivers and implantable six-month sensors, moderating attrition. Combined, these dynamics sustain a healthy pipeline for both premium CGM and value-focused SMBG devices inside the broader blood glucose monitoring market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Applications: Diabetes Management Dominates, Wellness Monitoring Emerges

Therapeutic diabetes management applications accounted for 73.21% of the 2025 value, underpinning the largest slice of the blood glucose monitoring market share. Closed-loop pumps, telehealth reviews, and population-health dashboards intensify data utilization, supporting a 14.78% forward growth path.

Wellness-oriented monitoring via subscription models such as Levels Health introduces CGM to fitness enthusiasts and pre-diabetics, growing awareness beyond clinical indications. Though still a modest slice of the blood glucose monitoring market size, lifestyle adoption contributes incremental sensor volume and could channel users into therapeutic pathways upon diagnosis.

By Age Group: Pediatric Surge, Adult Base

Adults maintained 73.1% share in 2025, reflecting type 2 prevalence. The pediatric segment, however, is projected to post 15.6% CAGR as school policies allow in-class monitoring and FDA labels extend to children as young as two. Manufacturers simplify insertion and enable caregiver viewing, improving adherence among minors.

Within geriatrics, CGM has limited penetration for those less than more than 75 years compared with high adoption among the 65-74 cohort. Skin fragility and smartphone literacy hurdles slow conversion, yet implantable options and simplified readers could unlock upside, sustaining incremental growth for the blood glucose monitoring market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Test Type: Invasive Dominates, Non-Invasive Gains Attention

Invasive modalities captured 61.65% share in 2025, but non-invasive prototypes such as Know Labs’ Bio-RFID are targeting FDA filings by 2026. If trials achieve sub-10% MARD, non-invasive wearables may widen the blood glucose monitoring market size by appealing to sensor-phobic users.

Optical methods still face pigmentation and hydration interference, keeping clinical clearance elusive. Nevertheless, USD 420 million in 2025 venture funding signals investor faith in eventual breakthrough. Meanwhile, invasive CGM continues refining chemistry and extending sensor life, reinforcing incumbent strength.

By End User: Homecare Dominates, Hospitals Modernize

Homecare held 41.34% of 2025 revenue thanks to telehealth incentives and new RPM billing codes that pay clinicians USD 64 for 20 minutes of monthly CGM data interpretation. Preference for virtual endocrinology visits underpins a 15.11% growth outlook.

Hospitals remain indispensable for acute care, relying on centralized meters that meet Joint Commission standards. Pilot studies at Johns Hopkins show significant hypoglycemia reduction with inpatient CGM, suggesting future penetration once the FDA approves dosing decisions in the ward. Long-term-care and correctional facilities represent smaller but specialized segments that demand rugged, easily auditable devices, rounding out opportunities in the blood glucose monitoring market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The United States anchors the blood glucose monitoring market with 83.1% of the 2025 value. Broad Medicare and commercial-payer coverage, combined with 37.3 million diagnosed diabetics, sustains scale advantages for suppliers. Manufacturing near-shoring is intensifying; Dexcom’s USD 150 million Arizona plant will supply U.S. and Canadian demand, reducing European shipment risk.

Canada benefits from province-funded CGM programs, yet inter-provincial policy disparities persist. Ontario and British Columbia reimburse type 2 intensive insulin users, but Quebec applies stringent A1c thresholds, delaying uptake and capping overall Canadian contribution to the blood glucose monitoring market.

Mexico is the fastest-growing geography at 14.32% CAGR through 2031, propelled by a national program that targets 500,000 CGM placements by 2028. Abbott’s Monterrey distribution hub cuts delivery lead times, while early private-insurer pilots in urban centers hint at nascent commercial demand. Despite lower per-capita spending, volume growth positions Mexico as a rising contributor to the North American blood glucose monitoring market.

Competitive Landscape

CGM revenue concentration is high: Abbott, Dexcom, and Medtronic command the majority of category sales, reflecting capital intensity and regulatory complexity. Abbott’s FreeStyle Libre franchise posted significant revenue in 2025 global sales, a significant portion of which is from North America. Dexcom’s installed base exceeded 2.5 million users, and its OTC Stelo aims for an additional 500,000 by end-2026. Medtronic’s Guardian 4 plus MiniMed 780G pump creates a closed-loop system that locks in consumable revenue.

SMBG remains fragmented with private-label strip brands and connected meters from Ascensia and LifeScan. Senseonics targets long-wear implantable CGM, addressing adherence pain points for seniors. Direct-to-consumer wellness platforms such as Levels Health spark cross-category awareness, potentially feeding future prescription growth. Patent filings emphasize sensor longevity and dual-analyte monitoring, foreshadowing continued innovation that will shape the blood glucose monitoring market trajectory.

North America Blood Glucose Monitoring Industry Leaders

Dexcom

Johnson & Johnson

F. Hoffmann-La Roche AG

Abbott Diabetes Care

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Dexcom unveiled a 15-day G7 sensor for U.S. adults, targeting mid-2026 retail availability.

- October 2025: OSR Holdings reached a binding agreement to acquire Woori IO Co., a company recognized for its non-invasive glucose-monitoring technology. The takeover will be completed through an all-share exchange.

- July 2025: Abbott brought its newest glucose-monitoring device, the FreeStyle Libre 3 Plus, to the Canadian market. The system uses the company’s smallest sensor so far, giving people with diabetes a lighter, less intrusive way to track their blood sugar.

North America Blood Glucose Monitoring Market Report Scope

As per the scope of the market, blood glucose monitoring is the fundamental process of measuring the concentration of glucose (sugar) in the blood, serving as a critical tool for managing diabetes and understanding metabolic health.

The North America blood glucose monitoring market is segmented by device, applications, age group, test type, end users, and geography. By device, the market is segmented into self-monitoring blood glucose devices, continuous glucose monitoring devices, and emerging non-invasive wearables. By applications, the market is segmented into bovine diabetes management, health and wellness monitoring, and others. By age group, the market is segmented into pediatrics, adults, and geriatrics. By test type, the market is segmented into invasive and non-invasive. By end users, the market is segmented into hospitals, homecare, and others. Geographically, the market is segmented across the United States, Canada, and Mexico. For each segment, the market size and forecast are provided in terms of value (USD).

By Device

| Self-Monitoring Blood Glucose Devices |

| Continuous Glucose Monitoring Devices |

| Emerging Non-Invasive Wearables |

By Applications

| Diabetes Management |

| Health and wellness monitoring |

| Other |

By Age Group

| Pediatrics |

| Adults |

| Geriatrics |

By Test Type

| Invesive |

| Non-Invasive |

By End User

| Hospitals |

| Homecare |

| Others |

By Country

| United States |

| Canada |

| Mexico |

| By Device | Self-Monitoring Blood Glucose Devices |

| Continuous Glucose Monitoring Devices | |

| Emerging Non-Invasive Wearables | |

| By Applications | Diabetes Management |

| Health and wellness monitoring | |

| Other | |

| By Age Group | Pediatrics |

| Adults | |

| Geriatrics | |

| By Test Type | Invesive |

| Non-Invasive | |

| By End User | Hospitals |

| Homecare | |

| Others | |

| By Country | United States |

| Canada | |

| Mexico |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the North America blood glucose monitoring market in 2031?

The blood glucose monitoring market is forecast to reach USD 37.68 billion by 2031.

Which device category is growing fastest across North America?

Continuous glucose monitoring systems are advancing at 13.76% CAGR through 2031, the highest among major categories.

How has Medicare policy affected CGM adoption?

CMS expanded eligibility in 2024, instantly doubling the addressable senior population and lifting CGM prescriptions by 47% among Medicare Advantage members in 2025

Which country in North America is showing the quickest market growth?

Mexico leads with a forecast 14.32% CAGR as its national diabetes program deploys CGM devices widely.