Nonwoven Filtration Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

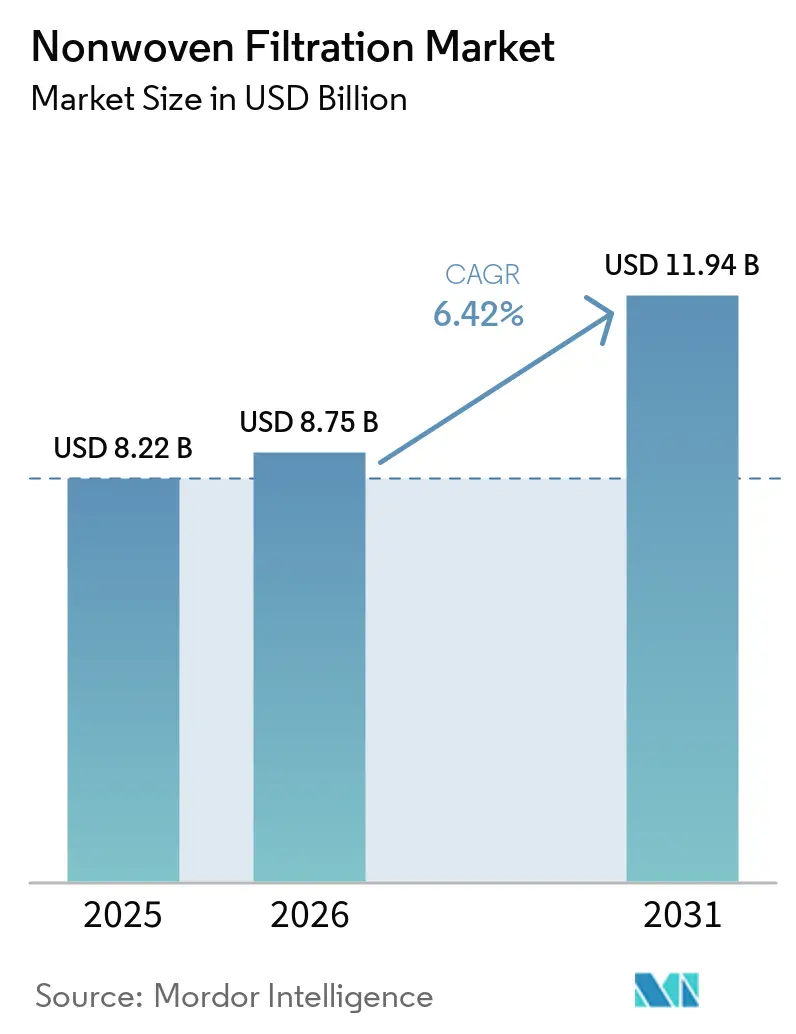

| Market Size (2026) | USD 8.75 Billion |

| Market Size (2031) | USD 11.94 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Nonwoven Filtration Market Analysis by ���ϲ�����

The Non-Woven Filtration Market size is expected to grow from USD 8.22 billion in 2025 to USD 8.75 billion in 2026 and is forecast to reach USD 11.94 billion by 2031 at 6.42% CAGR over 2026-2031. Heightened indoor-air-quality rules, rapid cleanroom buildouts in pharmaceutical and semiconductor sectors, and the emergence of battery-recycling plants that require sub-micron particle capture are converging to accelerate demand. Spunbond nonwoven dominates revenues in 2025, yet electro-spun is scaling fastest as data-center operators and hospital managers look for high-efficiency media with minimal pressure drop. Liquid filtration growth is outpacing air filtration as utilities tighten contaminant thresholds for wastewater reuse, while Asia-Pacific’s fab expansion and India’s new spunbond lines reinforce its position as the largest regional consumer. Competitive attention is shifting to PFAS-free binders, recyclable mono-material designs, and vertically integrated lines that reduce cost per square meter of qualified media.

Key Report Takeaways

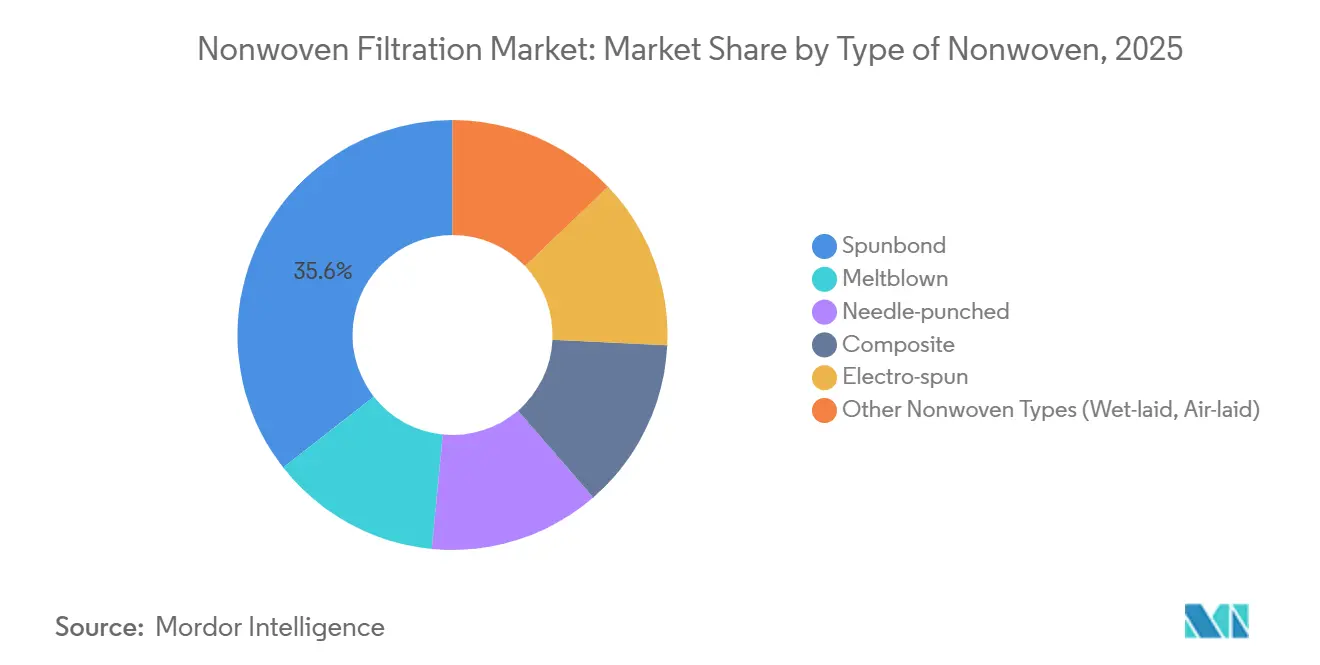

- By type of nonwoven, spunbond led with 35.57% of the nonwoven filtration market share in 2025, while electro-spun is projected to advance at a 6.79% CAGR through 2031.

- By filtration type, air filtration captured 50.22% of the nonwoven filtration market share in 2025; liquid filtration is projected to advance at a 6.90 CAGR through 2031.

- By application, water and waste-water treatment accounted for 27.78% of the nonwoven filtration market share in 2025, whereas healthcare and pharmaceuticals will expand at a 7.83% CAGR through 2031.

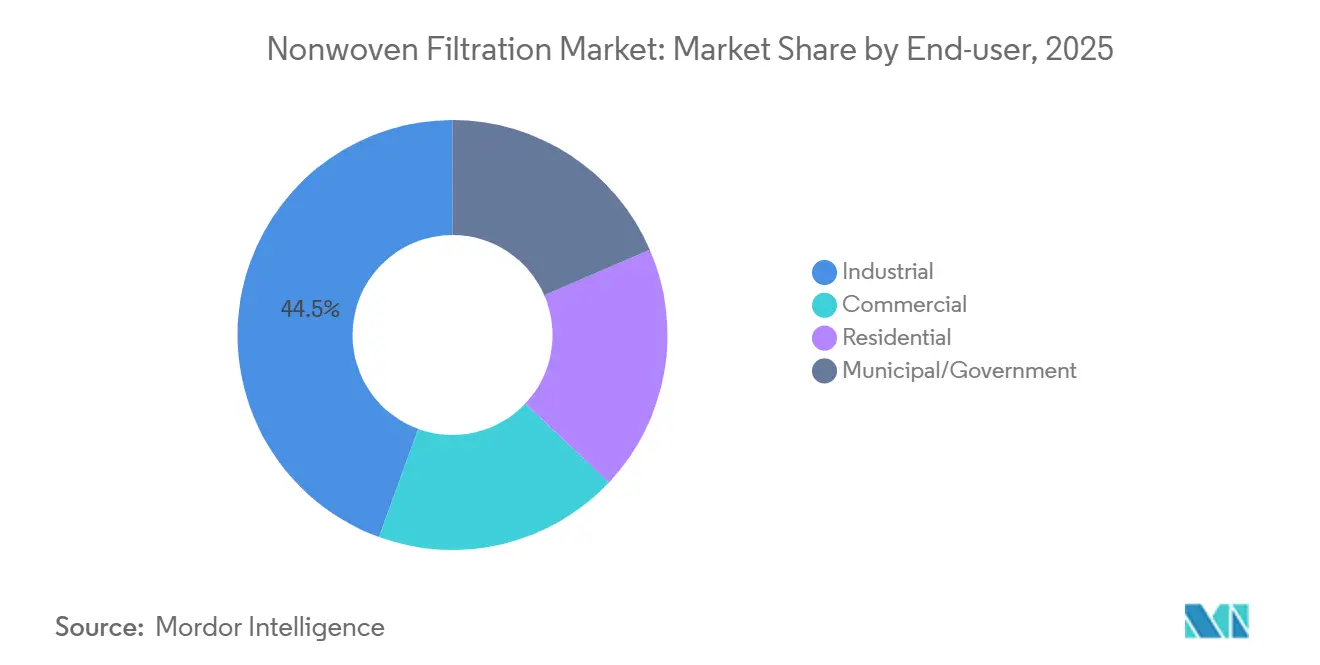

- By end-user, industrial held 44.45% of the nonwoven filtration market share in 2025, while residential is rising fastest at a 7.45% CAGR through 2031.

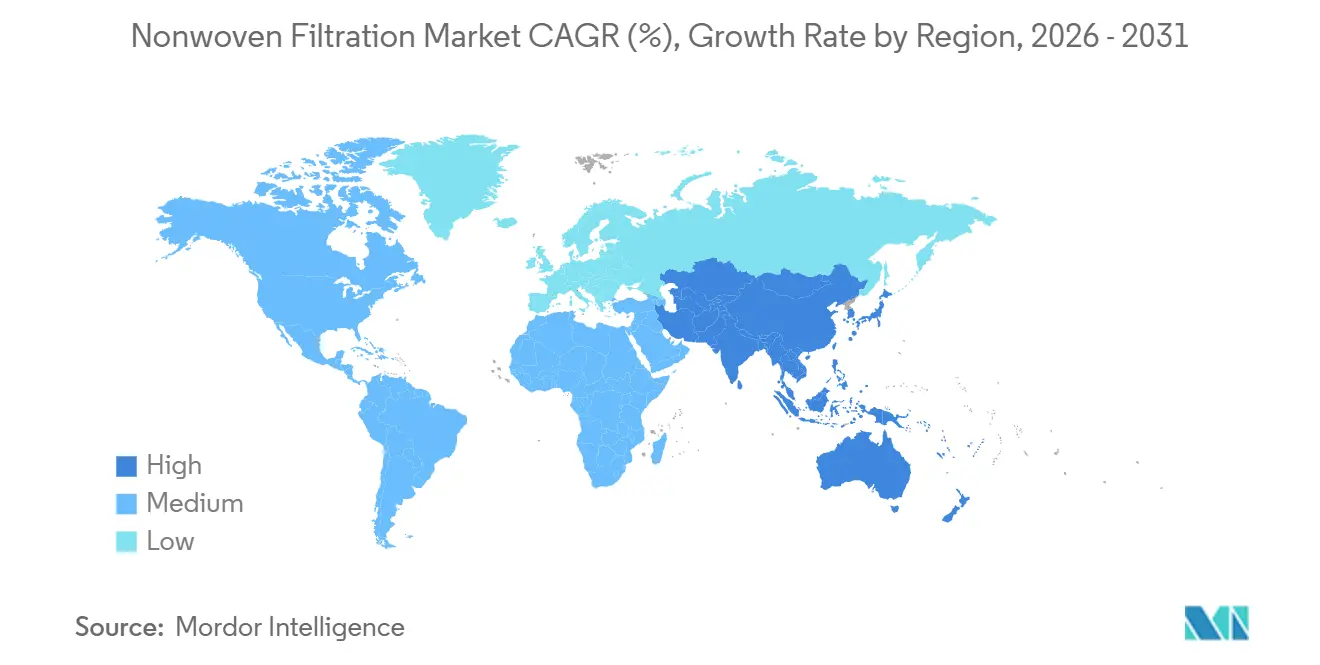

- By geography, Asia-Pacific commanded 39.97% of the nonwoven filtration market share in 2025 and is forecast to grow at a 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Nonwoven Filtration Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization boosting HVAC and IAQ demand | +1.8% | Asia-Pacific core, spill-over to Middle-East and Africa | Medium term (2–4 years) |

| Post-pandemic growth of healthcare and pharma cleanrooms | +1.5% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Data-center energy mandates for low-pressure drop filters | +1.2% | North America and Europe, emerging in Asia-Pacific | Medium term (2–4 years) |

| Battery-recycling plants needing fine-particle filtration | +0.9% | Asia-Pacific, North America | Long term (≥ 4 years) |

| Off-grid tourist desalination micro-filters | +0.4% | Middle-East and Africa, South America coastal zones | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rapid Urbanization Boosting HVAC and IAQ Demand

Revised ASHRAE 62.1 ventilation rates, adopted by several Asian and Middle-Eastern jurisdictions during 2025, now lock MERV 13 as the baseline for commercial sites, compelling building owners to replace legacy coarse filters more frequently[1]U.S. Department of Energy, “ASHRAE 62.1 Compliance Impacts,” energy.gov. Data-center operators, already consuming roughly 2% of global electricity in 2025, are standardizing on low-pressure-drop pleated nonwovens to temper fan-energy draw, favoring electrospun overlays on spunbond carriers. Utility-funded residential retrofit rebates across North America are accelerating replacement cycles to roughly three years, down from five. Embedded IoT pressure sensors in new housings allow predictive maintenance, rewarding vendors that guarantee linear pressure-rise curves under dust loading.

Post-Pandemic Growth of Healthcare and Pharma Cleanrooms

Global aseptic-fill capacity expanded 35% between 2024 and 2025 as mRNA vaccine lines and biosimilar suites came online. HEPA and ULPA filter installations in hospitals rose in parallel, embedding H14 terminal filters in operating theaters and intensive-care wards. In March 2026, MANN+HUMMEL opened a Level 7 cleanroom in Wilson, North Carolina, to validate pharma-grade media for OEM contracts. Strict particle-count limits from both U.S. FDA and EMA now mandate 0.2-micron absolute cartridges upstream of fill-finish modules, while continuous biologics manufacturing pushes single-use depth-filter demand that can run uninterrupted for longer campaigns.

Data-Center Energy Mandates for Low-Pressure-Drop Filters

Hyperscale contracts set power-usage effectiveness targets below 1.15, and fan energy can drop 20–30% once initial pressure falls under 0.3 inch water gauge. Electrospun nanofiber overlays achieve 99.97% PM0.3 efficiency with initial resistance around 0.25 inch, allowing service intervals of 12–15 months before hitting the 1-inch changeout threshold. Freudenberg’s micronAir neo, released March 2026, illustrates this design direction, pairing heterogeneous melt-blown structures with IoT sensors for real-time pressure tracking. Machine-learning airflow controls react to these sensors, creating a virtuous loop that privileges media with predictable dust-loading profiles.

Battery-Recycling Plants Needing Fine-Particle Filtration

Battery-recycling facilities processed roughly 180,000 metric tons of end-of-life cells in 2025, emitting sub-10-micron black-mass particulates rich in cobalt, nickel, and lithium. Conventional baghouses blind quickly, so recyclers specify composite nonwovens with hydrophobic and conductive fibers to tame static and resist chemical attack across pH 2–12. The EU Battery Regulation mandates 70% lithium recovery by 2030, catalyzing hydrometallurgical line builds that need staged filtration, nonwoven prefilters, 1-micron pleated cartridges, and 0.2-micron membranes for electrolyte polishing. Media suppliers able to validate chemical resistance at up to 80 °C and codify test protocols with recycler consortia secure long-term supply deals.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Disposal and recycling hurdles of composite media | -0.7% | Global, acute in Europe and North America | Medium term (2–4 years) |

| Regulatory focus on microfiber shedding | -0.5% | North America and Europe | Short term (≤ 2 years) |

| Capital scarcity for AI retrofits at SME converters | -0.4% | Global, concentrated in Asia-Pacific and South America | Medium term (2–4 years) |

| Source: ���ϲ����� | |||

Disposal and Recycling Hurdles of Composite Media

Activated-carbon laminated nonwovens cannot be economically separated in traditional recycling lines, and European cement kilns that accept spent filters charge USD 40–60 per metric ton in pretreatment fees. New melt-filtration reclaim systems achieve only 65–70% yield with multi-component webs, well below mono-material streams. Extended producer responsibility rules in France and Germany now force manufacturers to collect end-of-life filters, but rural logistics remain undeveloped, increasing landfill reliance. Lack of harmonized ISO or ASTM recyclability standards adds design uncertainty and compliance cost.

Regulatory Focus on Microfiber Shedding

The U.S. Fighting Fibers Act requires residential washing machines to capture particles ≤ 100 microns by 2030, spotlighting filter media as potential shed sources[2]U.S. Environmental Protection Agency, “Microplastics Roadmap 2025,” epa.gov. EU microplastic discharge rules, active since December 2025, cap industrial outflows at less than 1 mg/L, compelling process-water operators to certify filter integrity. A 2026 Particle and Fiber Toxicology study found cabin-facing sides of aged HVAC filters generate ultrafine fibers that triggered higher pulmonary inflammation in mice. Automotive OEMs now favor melt-blown media with narrow fiber-length distributions over staple-fiber needle-punched webs, squeezing legacy suppliers.

Segment Analysis

By Type of Nonwoven: Spunbond Anchors Revenue, Electro-spun Captures Premium

Spunbond nonwoven delivered 35.57% of 2025 revenue and underpins the largest revenue tier of the nonwoven filtration market. Electro-spun nonwoven, however, is projected to advance at a 6.79% CAGR through 2031.

Margin pressure on melt-blown lines built during the pandemic is prompting Asian firms to idle or repurpose capacity toward battery separators. Composite constructions that laminate spunbond backers with electrospun layers are narrowing the performance gap between HEPA and ULPA classes while preserving pleat stiffness. Breakthroughs that cut nanofiber diameters to 50–500 nm, demonstrated by HIFYBER and Espin Nanotech, let suppliers hit 99.97% PM0.3 efficiency at 30–40% lower pressure drop than conventional HEPA, strengthening the premium tier. Adoption of wet-laid synthetics with microfibers down to 0.04 dtex in reverse-osmosis support layers is another sign that specialty processes will coexist with high-output spunbond platforms.

By Filtration Type: Air Filtration Dominates, Liquid Filtration Surges on Reuse Mandates

Air filtration maintained a commanding 50.22% share of 2025 revenue in the nonwoven filtration market share landscape, yet liquid filtration is accelerating fastest at a 6.90% CAGR through 2031. Toray’s ultrafiltration launch in March 2025 and DuPont’s March 2026 nanofiltration upgrade illustrate vendor focus on lower energy and fouling profiles for municipal reuse projects.

Industrial processors upgrading cooling-tower loops and food and beverage plants phasing out PFAS now order multi-layer cartridge trains that pair spunbond prefilters with nanofiber polisher stages. Hybrid particulate-plus-molecular filters for semiconductor fabs blur classical air versus liquid boundaries by embedding gas-adsorption layers into nonwoven pleats. Consequently, vendors with cross-platform portfolios can upsell bundled solutions, raising average sales per installation in the nonwoven filtration market.

By Application: Water and Waste-water Treatment Leads, Healthcare and Pharmaceuticals Accelerates

Water and waste-water treatment delivered 27.78% of 2025 sales, the largest slice of the nonwoven filtration market size. Healthcare and pharmaceuticals, however, are expanding at a 7.83% CAGR through 2031.

Municipal utilities retrofit secondary-treatment plants with nonwoven membrane bioreactors to reclaim effluent for irrigation, trimming chemical dosing by 15% and energy by 10%. Hospitals and biologics manufacturers specify H14 HEPA ceiling modules and 0.2-micron sterile-filter cartridges. Automotive cabin-air premiumization and food and beverage allergen controls add incremental demand, but healthcare’s stricter compliance timelines underpin its superior growth curve within the nonwoven filtration market.

By End-user: Industrial Holds Share, Residential Surges

The industrial segment represented 44.45% of 2025 revenue, reflecting broad deployment across plant utilities, dust collection, and process protection. The residential segment is set to climb at a 7.45% CAGR through 2031, as North American and European codes embed MERV 13 filters into new construction.

Wildfire smoke events and public-health campaigns about PM2.5 risks have reframed filtration from a maintenance chore to a wellness investment. Direct-to-consumer purifier brands leverage e-commerce to sell replacement cartridges outside legacy HVAC distribution, increasing aftermarket frequency within the nonwoven filtration industry. Industrial buyers remain price-sensitive, but energy-linked total cost-of-ownership models help premium nonwoven suppliers defend margin.

Geography Analysis

Asia-Pacific held 39.97% of 2025 sales and is forecast to expand at a 7.12% CAGR through 2031. China’s semiconductor self-sufficiency drive funds new electrospinning and melt-blown lines, while India’s capacity surge to 18,740 tpa satisfies surging HVAC and cabin-filter demand.

North America and Europe form mature replacement markets, yet gain mid-single-digit lift from stricter PM2.5 and building-energy directives. Avgol’s USD 100 million North Carolina spunbond plant and MANN+HUMMEL’s Level 7 cleanroom demonstrate confidence in domestic capacity localization.

South America, and Middle-East and Africa contribute smaller revenues but see high-growth pockets in Brazilian water-treatment upgrades, Argentine lithium-mine dust control, Saudi cleanroom zones, and off-grid desalination micro-filters for tourism. Battery-recycling capacity, clustered in China, Europe, and North America, compels media suppliers to install regional tech-support labs, tightening service links across the nonwoven filtration market.

Competitive Landscape

The market exhibits low concentration with major players including 3M, KCWW, Freudenberg, Johns Manville, and Ahlstrom. Incumbents leverage in-house polymer compounding, pleating automation, and global test labs to meet ISO 29463 and EN 1822 certification at scale.

Emerging disruptors such as HIFYBER and Espin Nanotech introduce needleless electrospinning, lowering capital intensity and producing nanofiber rolls on demand. IoT-enabled differential-pressure sensors embedded in frames allow cloud analytics and predictive maintenance, creating service revenue streams.

Sustainability differentiation is widening: MANN+HUMMEL’s lignin-based filter launch in March 2025 demonstrates a pivot away from petroleum-derived binders, and Toray’s chemically resistant RO membrane, released in April 2026, targets circular-economy mandates. Vendors that align on PFAS-free chemistries and recyclability standards are best placed to capture future share.

Nonwoven Filtration Industry Leaders

Ahlstrom

Freudenberg SE

Johns Manville

3M

KCWW

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Ahlstrom introduced Ahlstrom PurXcel, a molecular filter media platform developed for clean air applications globally. It was manufactured in Turin, Italy, using advanced dry technology to provide cleaner and healthier air for the cabin and indoor environments.

- February 2024: Freudenberg SE launched the Filtura line, a 100% synthetic, wet-laid nonwoven material designed for high-performance industrial air and liquid filtration. Manufactured in Germany, these materials provided a sustainable and durable alternative to fiberglass.

Global Nonwoven Filtration Market Report Scope

Nonwoven filtration utilizes engineered fiber webs that are bonded mechanically, thermally, or chemically to provide efficient, cost-effective, and versatile solutions for air and liquid filtration, outperforming traditional woven materials. Major types, such as meltblown, spunbond, and needle felt, deliver high particle capture efficiency and are used in applications including HVAC systems, medical masks, and water treatment.

The Nonwoven Filtration Market is segmented into type of nonwoven, filtration type, application, end-user, and geography. By type of nonwoven, the market is segmented into spunbond, meltblown, needle-punched, composite, electro-spun, and other nonwoven types (wet-laid, air-laid). By filtration type, the market is segmented into air filtration, liquid filtration, and other types (gas, oil, blood). By application, the market is segmented into water and waste-water treatment, industrial (manufacturing, chemical, power), HVAC systems, automotive, healthcare and pharmaceuticals, food and beverage processing, electronics, and other applications (mining, pulp and paper). By end-user, the market is segmented into industrial, commercial, residential, and municipal/government. The report also covers the market size and forecasts for nonwoven filtration in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Spunbond |

| Meltblown |

| Needle-punched |

| Composite |

| Electro-spun |

| Other Nonwoven Types (Wet-laid, Air-laid) |

| Air Filtration |

| Liquid Filtration |

| Other Types (Gas, Oil, Blood) |

| Water and Waste-water Treatment |

| Industrial (Manufacturing, Chemical, Power) |

| HVAC Systems |

| Automotive |

| Healthcare and Pharmaceuticals |

| Food and Beverage Processing |

| Electronics |

| Other Applications (Mining, Pulp and Paper) |

| Industrial |

| Commercial |

| Residential |

| Municipal/Government |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type of Nonwoven | Spunbond | |

| Meltblown | ||

| Needle-punched | ||

| Composite | ||

| Electro-spun | ||

| Other Nonwoven Types (Wet-laid, Air-laid) | ||

| By Filtration Type | Air Filtration | |

| Liquid Filtration | ||

| Other Types (Gas, Oil, Blood) | ||

| By Application | Water and Waste-water Treatment | |

| Industrial (Manufacturing, Chemical, Power) | ||

| HVAC Systems | ||

| Automotive | ||

| Healthcare and Pharmaceuticals | ||

| Food and Beverage Processing | ||

| Electronics | ||

| Other Applications (Mining, Pulp and Paper) | ||

| By End-user | Industrial | |

| Commercial | ||

| Residential | ||

| Municipal/Government | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the nonwoven filtration market?

The nonwoven filtration market stands at USD 8.75 billion in 2026 and is forecast to reach USD 11.94 billion by 2031.

Which type of nonwoven is growing the fastest through 2031?

Electro-spun is advancing at a 6.79% CAGR through 2031.

Why is liquid filtration outpacing air filtration?

Utilities and processors are tightening contaminant thresholds for wastewater and process-water reuse, driving a 6.90% CAGR through 2031 in liquid filtration.

Which region is growing fastest through 2031?

Asia-Pacific is set to grow at a 7.12% CAGR through 2031.

Page last updated on: