Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

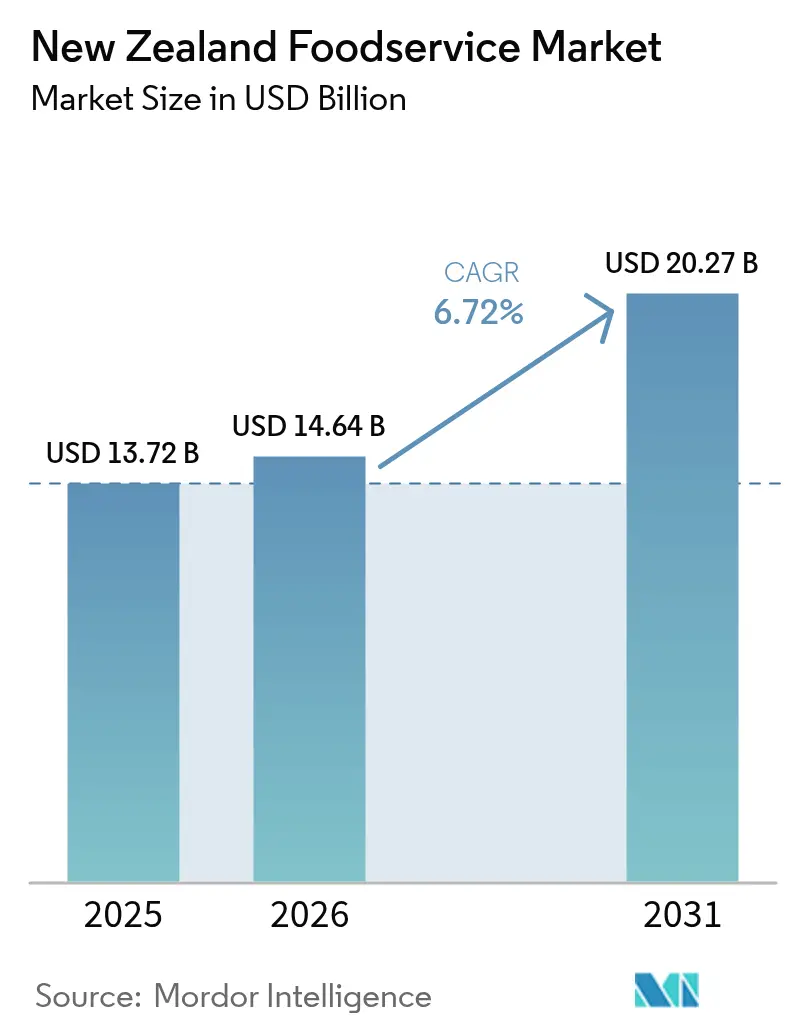

| Base Year Market Size (2025) | USD 13.72 Billion |

| Market Size (2026) | USD 14.64 Billion |

| Market Size (2031) | USD 20.27 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

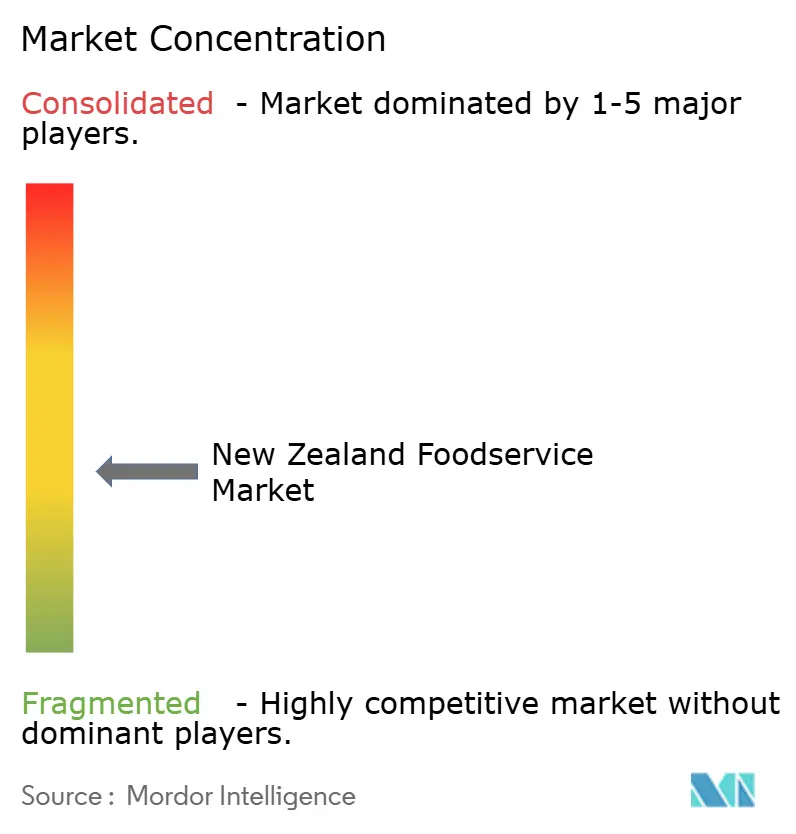

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

New Zealand Foodservice Market Analysis by ���ϲ�����

The New Zealand foodservice market size is projected to expand from USD 13.72 billion in 2025 and USD 14.64 billion in 2026 to USD 20.27 billion by 2031, registering a CAGR of 6.72% between 2026 to 2031. Demand is recovering on the back of resurgent tourism, a widening embrace of digital ordering, and consumers prioritizing convenience even as household budgets tighten. Chains are scaling faster than independents by leveraging franchise capital, data-driven menus, and supply-chain efficiencies, yet two-thirds of outlets remain owner-operated, preserving a vibrant entrepreneurial scene. Cloud kitchens continue to draw investment as operators seek lower fixed costs and hyper-local delivery reach. At the same time, experiential formats such as full-service restaurants benefit from pent-up social dining occasions, pointing to a bifurcated path where both low-touch and high-touch concepts coexist. Rising wage expectations, volatile food prices, and strict food-safety rules temper margins, encouraging automation pilots and collaborative purchasing among smaller operators.

Key Report Takeaways

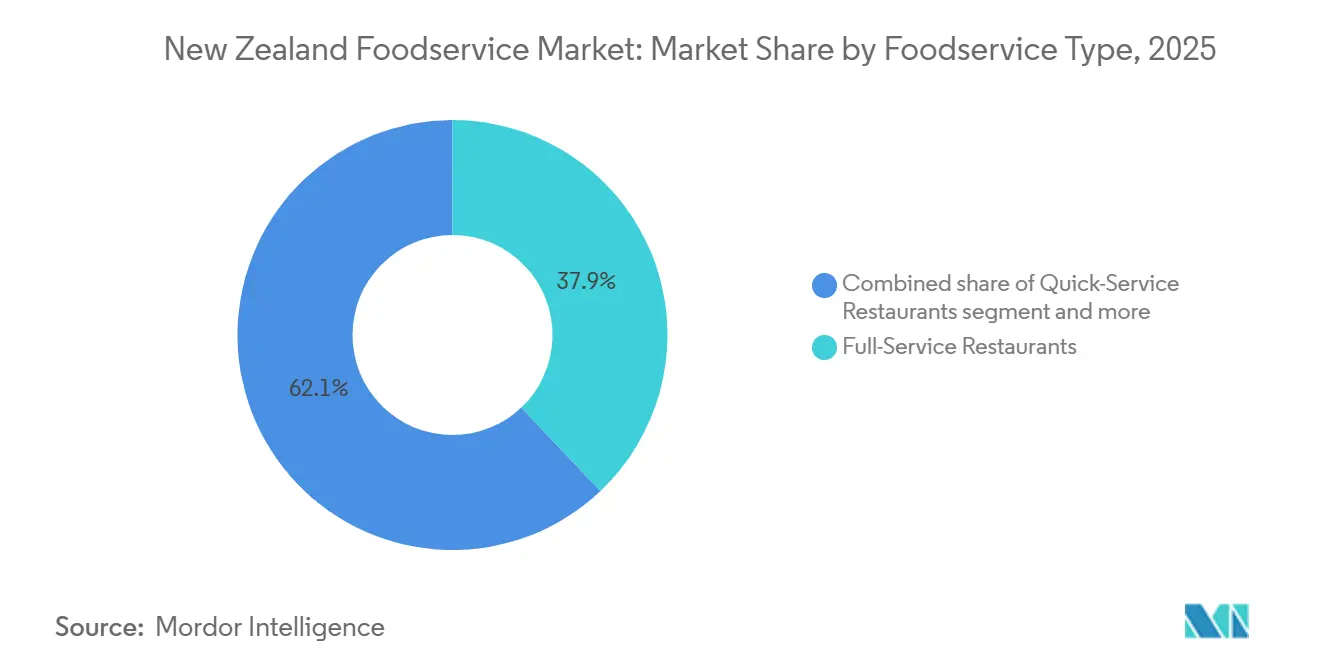

- By foodservice type, full-service restaurants led with 37.91% revenue share in 2025, while cloud kitchens are forecast to expand at an 8.34% CAGR through 2031.

- By outlet, independent operators accounted for 67.93% of the New Zealand foodservice market share in 2025, whereas chained outlets are growing at a 7.65% CAGR to 2031.

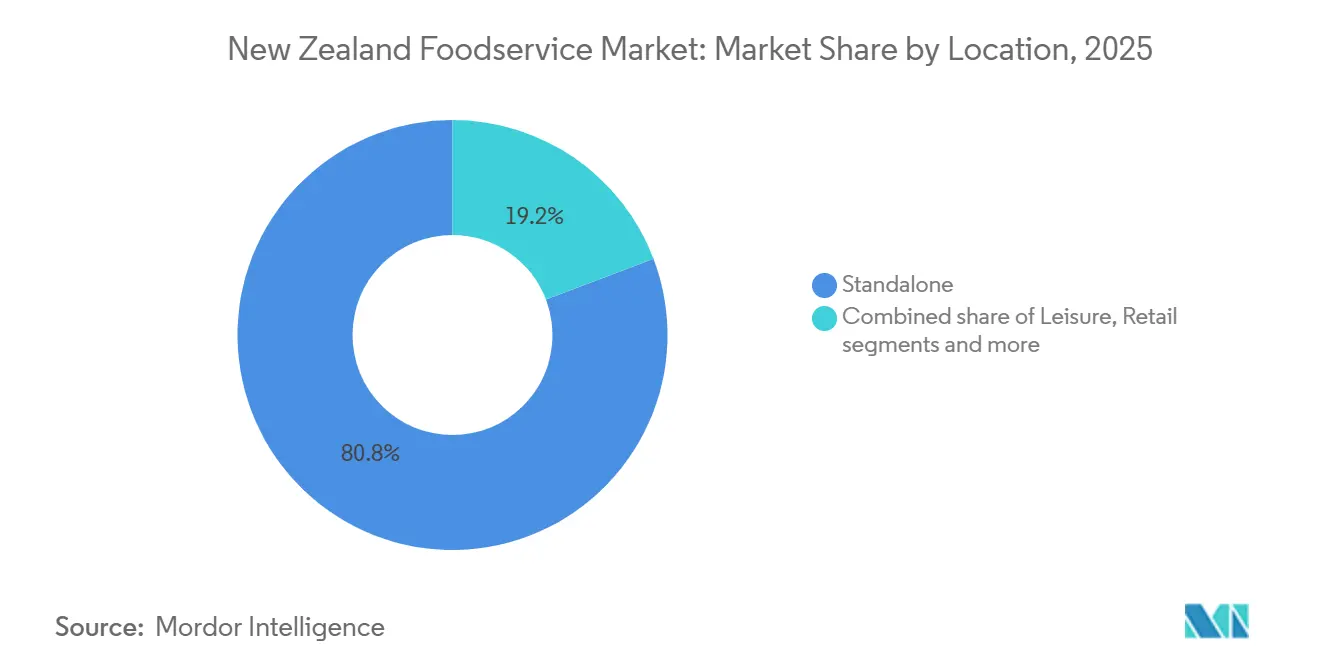

- By location, standalone sites captured 80.77% of outlets in 2025; leisure venues are projected to grow at an 8.27% CAGR through 2031.

- By cuisine, North American concepts held 41.10% share in 2025, but Asian cuisine is advancing at an 8.79% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

New Zealand Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in the tourism and hospitality market | +1.8% | National, concentrated in Auckland, Queenstown, Rotorua | Medium term (2-4 years) |

| Increasing consumer demand for convenience and dining out | +1.5% | National, urban centers leading | Short term (≤ 2 years) |

| Expansion of delivery services and digital ordering platforms | +1.2% | National, with rural penetration accelerating | Short term (≤ 2 years) |

| Transition to plant-based and health-focused menu options | +0.9% | National, Auckland and Wellington early adopters | Medium term (2-4 years) |

| Adoption of technology in restaurant operations | +0.7% | National, chains ahead of independents | Long term (≥ 4 years) |

| Emphasis on sustainability and local sourcing practices | +0.6% | National, compliance-driven in urban areas | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Growth in the tourism and hospitality market

Growth in tourism and hospitality is a significant factor driving demand within the foodservice market, as rising international arrivals directly increase footfall across hotels, cafés, quick-service restaurants, and casual dining outlets. Statistics New Zealand reported that overseas visitor arrivals reached 347,600 in November 2025, boosting occupancy rates and meal occasions in accommodation-linked foodservice formats [1]Source: Statistics New Zealand, "International Travel: November 2025," stats.govt.nz. This influx has elevated demand for premium breakfast options, grab-and-go meals, and experiential dining, particularly in key cities such as Auckland, Queenstown, and Christchurch. Hospitality operators are increasingly focusing on local sourcing, seasonal menus, and regional flavors to attract tourist spending and enhance destination experiences. Brands like BurgerFuel leverage high-traffic urban and airport locations to cater to international visitors seeking familiar yet locally adapted offerings. Similarly, café chains such as Coffee Club New Zealand capitalize on tourist-driven footfall in transport hubs and tourist precincts to drive sales of beverages and light meals. Hotels and resorts contribute by offering high-margin buffet concepts, room service, and curated dining experiences that extend visitor dwell time and spending. This interconnected growth across accommodation, travel retail, and dining formats strengthens overall foodservice activity, while inbound tourism recovery continues to support premiumization, menu innovation, and outlet expansion.

Increasing consumer demand for convenience and dining out

Consumer demand for convenience and dining out continues to drive growth in the foodservice market, supported by evolving lifestyles, extended working hours, and an increasing preference for ready-to-eat meals. According to the Restaurant Association of New Zealand (2024), households reported an average weekly expenditure of USD 162 on dining out, highlighting the shift of eating outside the home from an occasional indulgence to a routine behavior [2]Source: Restaurant Association of New Zealand, "2025 Consumer Dining Insights Report," restaurantnz.co.nz. This trend fuels demand across quick-service restaurants, cafés, and casual dining formats that emphasize speed, affordability, and consistent quality. The adoption of digital ordering, takeaway, and delivery platforms further accelerates this shift by simplifying access to foodservice options. Brands such as Hell Pizza capitalize on this trend with strong delivery penetration and menu offerings designed for convenience-driven consumption, while café chains like Columbus Coffee benefit from high-frequency breakfast and snack occasions aligned with on-the-go lifestyles. The interplay of time constraints and rising disposable incomes supports repeat visits and higher transaction volumes, encouraging menu simplification and operational efficiency across outlets. These dynamics collectively position convenience-focused dining out as a sustained structural growth driver in the foodservice market.

Expansion of delivery services and digital ordering platforms

The growth of delivery services and digital ordering platforms is reshaping the foodservice industry in New Zealand by extending restaurant reach beyond physical locations and increasing order frequency through at-home consumption. In 2024, Uber Eats expanded to 12 new locations across Aotearoa, demonstrating confidence in sustained demand and advancements in last-mile infrastructure. This expansion enables both independent outlets and chains to access suburban and regional consumers without significant investment in new stores. Similarly, DoorDash continued its rollout across secondary cities in 2025, including Te Puke, Tokoroa, Whakatane, Hawera, Feilding, Levin, Masterton, Ashburton, Oamaru, and Wanaka, intensifying competition and encouraging multi-platform ordering behavior. These platforms also support menu digitization, targeted promotions, and data-driven demand forecasting, enhancing operational efficiency for restaurants. Brands such as St Pierre’s Sushi have leveraged these developments to achieve higher lunchtime penetration and offer bundled delivery formats aligned with convenience-driven consumption. Furthermore, the integration of loyalty programs and app-based discounts reinforces repeat ordering behavior. This evolving digital ecosystem aligns consumer expectations for convenience with restaurant scalability, fundamentally transforming how foodservice demand is generated and fulfilled across the country.

Transition to plant-based and health-focused menu options

The transition to plant-based and health-focused menu options is driven by increasing wellness awareness, dietary diversification, and multicultural consumption patterns. Statistics New Zealand (2024) highlights the country’s diverse population mix, including European/Other (65.9%), Asian (20.1%), Māori (17.4%), Pacific (9%), Indian (7%), and Chinese (6%) communities, which supports broader acceptance of vegetarian, vegan, flexitarian, and lighter global cuisines [3]Source: Statistics New Zealand, "Asian Ethnic Population Projected to Increase," stats.govt.nz. This demographic diversity encourages restaurants to integrate plant-forward dishes, dairy alternatives, and clean-label ingredients into mainstream menus rather than limiting them to niche offerings. Additionally, the demand for functional foods, allergen-friendly options, and nutrient-dense meals is reshaping offerings across cafés and casual dining establishments. Brands such as Lord of the Fries New Zealand leverage fully plant-based menus within fast-casual formats to attract younger, urban consumers, while Wise Boys Burgers appeals to ethical eaters and flexitarians with vegan comfort food. These strategies address consumer expectations for taste and convenience while promoting inclusivity. The convergence of wellness priorities and cultural diversity is structurally expanding the penetration of plant-based options across the foodservice market in New Zealand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compliance with stringent food safety regulations | -0.5% | National, enforcement stricter in urban centers | Long term (≥ 4 years) |

| Volatility in supply chains and rising food inflation | -1.2% | National, rural areas face longer lead times | Short term (≤ 2 years) |

| High commercial rents in prime business locations | -0.8% | Auckland, Wellington, Christchurch CBD and premium retail zones | Medium term (2-4 years) |

| Labor shortages are posing challenges to growth | -1.0% | National, acute in tourism-dependent regions (Queenstown, Rotorua) | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Compliance with stringent food safety regulations

Stringent food safety regulations present a significant challenge for the foodservice industry in New Zealand, increasing operational complexity and compliance costs across restaurant formats. The regulatory framework has intensified with the introduction of mandatory allergen labeling protocols, effective February 25, 2024, which require menu audits, recipe standardization, and staff retraining. These requirements place a heavier burden on independent cafés and small operators with limited compliance infrastructure, slowing menu innovation and rollout timelines. Larger chains are better positioned to manage these demands, but still face increased documentation and verification costs across outlets. For example, McDonald’s New Zealand, as of November 2025, has invested in centralized allergen management systems to ensure consistency and regulatory compliance across its national menus. However, even established operators must frequently update digital and in-store disclosures to remain compliant. This compliance burden extends time-to-market for new products, raises back-end operational costs, and creates significant entry barriers for new entrants. Collectively, these factors limit agility and constrain margin expansion across the industry.

Volatility in supply chains and rising food inflation

Supply chain volatility and rising food inflation present significant challenges by increasing procurement uncertainty and compressing operator margins. Disruptions in imported ingredients, packaging materials, and freight logistics elevate input costs and undermine price stability for restaurants and foodservice distributors. These pressures force operators to either absorb cost increases or transfer them to consumers, potentially affecting demand in value-sensitive segments. Strategies such as menu rationalization and portion resizing are increasingly employed to manage cost fluctuations while preserving perceived value. Smaller independent outlets are particularly at risk due to limited supplier diversification and weaker bargaining power. In response, larger brands like Restaurant Brands New Zealand (KFC, Taco Bell) implement centralized sourcing, long-term supplier contracts, and menu engineering to safeguard margins. However, even scaled chains encounter pricing delays and operational strain during commodity price fluctuations, complicating forecasting, inventory planning, and promotional strategies. Collectively, rising food inflation and unstable supply chains constrain profitability and strategic flexibility across the foodservice market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: Cloud Kitchens Outpace Traditional Formats

Full-service restaurants are expected to account for 37.91% of the foodservice market share in 2025, supported by experiential dining, table service, and alcohol-led occasions that drive higher per-check averages and extended customer dwell times. These establishments benefit from the recovery of tourism and the growing preference for social dining, which sustains demand for premium menus and curated in-store experiences. To remain competitive against digitally native operators, many are retrofitting kitchens to meet off-premise demand. For example, SkyCity Restaurants Auckland leverages destination dining and beverage-led revenue streams while expanding takeaway and delivery-compatible menu options. This shift underscores the evolution of experiential dining beyond physical premises. As delivery demand increases, full-service formats are integrating cloud-style workflows to strengthen their omnichannel presence while maintaining high-margin dine-in occasions.

Cloud kitchens, with a projected CAGR of 8.34% through 2031, represent the fastest-growing foodservice format due to their asset-light models, rapid brand testing capabilities, and delivery-first infrastructure. These formats benefit from platform-driven demand and lower real estate costs but lack the experiential elements that build brand loyalty. Quick-service restaurants, such as Domino’s New Zealand, utilize drive-thru services and strong brand recognition but face margin pressures from third-party delivery commissions. Independently operated cafés and bars continue to encounter challenges related to labor intensity and limited scalability. In response, some cloud kitchen operators are testing dine-in pop-ups to enhance brand recognition and explore physical formats. These trends highlight a convergence between traditional and virtual foodservice models rather than a complete shift in the market.

By Outlet: Chains Gain Ground Through Franchise Acceleration

Independent outlets are expected to hold a 67.93% market share by 2025, reflecting the entrepreneurial culture and consumer demand for authentic, locally inspired dining experiences. These operators excel in customizing menus to regional preferences, exploring niche cuisines, and delivering personalized service that fosters customer loyalty. However, smaller operators face challenges such as scaling operations, ensuring consistent quality, and expanding marketing reach. Fidel’s Café in Wellington serves as an example of how independent businesses leverage local identity and uniqueness to attract repeat customers while maintaining strong community ties. To remain competitive, independent outlets must increasingly adopt digital ordering and delivery solutions to address evolving consumer expectations and the growing presence of chains.

Chained outlets are projected to grow at a compound annual growth rate (CAGR) of 7.65% through 2031, driven by franchise models that reduce capital investment and operational risks while enabling rapid market expansion. Franchising supports scalability by enhancing brand recognition, standardizing processes, and securing supplier agreements. Quick-service brands like Hell Pizza New Zealand demonstrate the effectiveness of this approach, combining national reach with local partnerships to ensure menu consistency and delivery efficiency. While chains focus on high-traffic urban and suburban areas, independents retain their niche and neighborhood presence, fostering a balanced foodservice ecosystem where innovation and accessibility coexist.

By Location: Leisure Venues Emerge as High-Margin Channels

Standalone outlets continue to play a significant role in the foodservice industry, projected to account for 80.77% of locations by 2025. These outlets benefit from cost efficiencies such as lower rent, convenient parking, and operational flexibility. Their format allows operators to innovate with menu offerings, expand delivery or drive-thru services, and cater to local and commuter traffic without the constraints of embedded commercial spaces. Brands like BurgerFuel leverage standalone sites to provide both dine-in and takeaway options while integrating delivery-only kitchens to enhance revenue streams. The rise of hybrid models underscores the importance of diversifying income sources to remain competitive, while sustainability initiatives, including certifications and eco-friendly practices, are becoming critical for differentiation.

Leisure venues, including shopping malls, sports stadiums, and entertainment complexes, are emerging as high-margin channels, with an anticipated CAGR of 8.27% through 2031. These venues benefit from steady foot traffic and extended operating hours. Retail outlets in malls capitalize on impulse purchases but face challenges such as rent escalations tied to turnover clauses. Travel hubs like Auckland Airport generate higher transaction values due to limited alternatives and time constraints. Operators in these venues are also addressing sustainability requirements, balancing compliance costs with opportunities for brand differentiation, as highlighted by the Ministry for Primary Industries’ environmental report. Together, these trends reflect strategic shifts in the foodservice landscape.

By Cuisine Type: Asian Flavors Ride Demographic Tailwinds

In 2025, North American cuisine held a 41.10% market share, led by brands such as McDonald's, KFC, Burger King, and Domino's. These companies deliver familiar comfort foods through efficient drive-thrus, app-based ordering, and value menus that resonate with diverse demographics in urban and suburban areas. Their emphasis on speed and consistency ensures that busy families, office workers, and tourists can rely on portable options like burgers, fried chicken, and pizzas without deviations in flavor or service quality. The scale of these brands supports aggressive promotions and loyalty programs, driving repeat visits, while shared supply chains help maintain competitive costs despite rising ingredient prices. These outlets often serve as key anchors in shopping centers and highways, indirectly supporting other cuisines by attracting foot traffic to mixed-use precincts. Their operational efficiency sets a benchmark for emerging segments aiming to establish a foothold in the market.

Asian cuisine is projected to grow at a compound annual growth rate (CAGR) of 8.79% through 2031, the fastest among all cuisine types. This growth is fueled by demographic shifts, with Stats NZ forecasting the Asian population to rise from 19% in 2023 to 33% by 2048. Demand for authentic ramen houses, sushi bars, and curry restaurants is increasing, with operators like Noodle Canteen adapting spice levels and portion sizes to local preferences while introducing fusion dishes. High-density areas such as Auckland and Christchurch are particularly conducive to scalable Asian dining concepts. Moreover, compliance with the Ministry for Primary Industries' Food Act 2014 enhances consumer trust through allergen labeling, enabling gluten-free and nut-free claims. By aligning population growth, regulatory compliance, and menu innovation, Asian cuisine is positioned for sustained high growth.

Geography Analysis

Significant regional differences characterize New Zealand's foodservice market, influenced by population density, tourism activity, and infrastructure investments. Auckland, with 1.8 million residents in 2024 and the nation’s busiest airport, is projected to lead national foodservice revenue in 2025. This leadership is driven by corporate dining, international tourism, and a diverse population supporting a variety of cuisines, including Asian, European, and Middle Eastern (Stats NZ). Restaurant Brands New Zealand’s KFC division, with half its outlets in Auckland, benefits from high foot traffic, dense delivery networks, and urban convenience. Additionally, Auckland’s scale supports premium, experience-focused offerings that integrate dine-in, takeaway, and delivery models to meet diverse consumer needs.

Infrastructure and redevelopment play a pivotal role in shaping foodservice dynamics in Wellington and Christchurch. Wellington’s market is anchored by government institutions and professional services, creating demand for lunch-centric cafés and full-service restaurants. The city’s predictable traffic patterns and repeat visitation favor smaller, high-frequency operators. Meanwhile, Christchurch faces challenges such as rising rents in prime retail areas, a lingering effect of the 2011 earthquake. However, the opening of the One New Zealand Stadium in April 2026, with over 200 annual events and 3,200 premium hospitality seats, is expected to create a high-margin, event-driven channel, benefiting operators capable of scaling for demand spikes.

Tourism-focused regions like Queenstown generate higher per-occasion spending from international visitors but face seasonal volatility between winter ski and summer low periods, complicating cash flow management. Regional towns such as Rotorua, Taupo, and Napier rely on domestic tourism and retiree populations, supporting independent cafés and family-style restaurants while limiting chain expansion opportunities. Delivery platforms like DoorDash expanded into rural towns, including Tokoroa, Oamaru, and Wānaka, during 2024–2025 to capture incremental volume. However, lower order density in these areas increases per-delivery costs and compresses margins, emphasizing the need for location-specific strategies across New Zealand’s foodservice ecosystem.

Competitive Landscape

The New Zealand foodservice market demonstrates moderate fragmentation, with independent operators outnumbering chains by a ratio of 2-to-1. However, chains capture a larger share of revenue due to their scale efficiencies, standardized operations, and strong brand recognition. This dynamic enables large players to dominate high-traffic urban areas, delivery platforms, and travel locations, while independent operators maintain strength in neighborhood dining and niche cuisines. Chains benefit from centralized procurement, marketing scale, and menu engineering, which help sustain margins despite rising costs. For instance, McDonald’s Corporation leverages drive-thru infrastructure and omnichannel ordering systems to convert foot traffic into high transaction volumes. This combination of outlet-level fragmentation and revenue concentration among scaled operators creates a hybrid competitive structure rather than a monopolized market.

Restaurant Brands New Zealand Ltd plays a significant role in the market by operating brands such as KFC, Pizza Hut, Taco Bell, and Carl’s Jr. The company employs a multi-brand strategy to optimize real estate use and supply chain efficiencies. This approach enables cross-brand learnings in areas such as delivery, value menus, and franchise development, reinforcing its dominance in the quick-service restaurant (QSR) segment. Similarly, Domino’s leverages digital-first ordering systems and a dense store network to enhance speed, consistency, and consumption frequency. These chains outperform independent operators in suburban and delivery-heavy areas, where convenience and price sensitivity are critical. However, independents remain competitive through menu innovation, community engagement, and experiential differentiation, sustaining moderate market concentration rather than consolidation-driven dominance.

BurgerFuel strengthens its market position through a premium fast-casual approach and strong local brand equity, appealing to urban consumers seeking unique burger offerings beyond global QSR formats. Starbucks capitalizes on international brand recognition and standardized café experiences to attract customers in commuter hubs, malls, and travel locations. Both global and domestic chains benefit from loyalty programs, consistent store designs, and digital integration, enabling them to drive repeat consumption more effectively than most independent operators. Despite this, independent cafés and restaurants continue to outnumber chains and play a vital role in shaping local dining culture, particularly in suburban and regional markets. This dual structure fosters competitive tension between the efficiency of scaled operators and the authenticity of independent establishments, leaving New Zealand’s foodservice market structurally fragmented but commercially skewed toward branded operators.

New Zealand Foodservice Industry Leaders

-

Restaurant Brands NZ Ltd

-

McDonald’s Corporation

-

Domino’s Pizza Inc

-

BurgerFuel Group Ltd

-

Starbucks Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Duck Donuts had entered into a master franchise agreement to expand into New Zealand. The US-based donut and coffee chain had collaborated with Martin and Anita van der Velden, former multi-unit franchisees of Bakers Delight, to establish its presence in the market. Duck Donuts operated alongside other US brands, Dunkin’ and Krispy Kreme, which had 19 and six stores in New Zealand, respectively.

- November 2024: Sushi Sushi announced plans to open 35 stores in New Zealand over the next 10 years after signing a deal with a new master franchisee. Stanley Greene, the first New Zealander to secure a master franchise agreement with Sushi Sushi, took over the existing Sushi Sushi Botany store and aimed to expand the network over the coming decade.

- November 2024: Ozone Coffee opened its newest café, Ozone Walker Street, in central Christchurch. Located at the former site of Ally & Sid, the café featured a selection of baked goods, small bites, and its signature freshly roasted, directly sourced specialty coffee.

- April 2024: Soul Origin opened its third restaurant in New Zealand at Auckland International Airport. The establishment provided fresh, healthy food options along with specialty coffee.

New Zealand Foodservice Market Report Scope

Foodservice defines those businesses, institutions, and companies responsible for any meal prepared outside the home. The scope of the New Zealand foodservice market includes segmenting food service providers in the country by type into full-service restaurants, quick-service restaurants, street stalls and kiosks, cafes and bars, and 100% home delivery restaurants. Further segmentation is done on the basis of foodservice structure into independent consumer foodservice and chained consumer foodservice. The report offers market size and forecasts in value (USD million) for all the above segments.

By Foodservice Type

| Full-Service Restaurants |

| Quick-Service Restaurants |

| Cloud Kitchens |

| Cafés and Bars |

By Outlet

| Chained Outlets |

| Independent Outlets |

By Location

| Standalone |

| Leisure |

| Retail |

| Lodging |

| Travel |

By Cuisine Type

| Asian |

| European |

| Latin American |

| Middle Eastern |

| North American |

| Other Cuisines |

| By Foodservice Type | Full-Service Restaurants |

| Quick-Service Restaurants | |

| Cloud Kitchens | |

| Cafés and Bars | |

| By Outlet | Chained Outlets |

| Independent Outlets | |

| By Location | Standalone |

| Leisure | |

| Retail | |

| Lodging | |

| Travel | |

| By Cuisine Type | Asian |

| European | |

| Latin American | |

| Middle Eastern | |

| North American | |

| Other Cuisines |

Key Questions Answered in the Report

How large will the New Zealand foodservice market be by 2031?

It is forecast to reach USD 20.27 billion by 2031 on a 6.72% CAGR trajectory.

Which segment is growing quickest within the sector?

Cloud kitchens lead with an 8.34% CAGR expected through 2031 as operators chase low-capital, delivery-first models.

Why are leisure venues attracting foodservice operators?

New stadiums and malls offer captive foot traffic and higher margins, prompting an 8.27% CAGR for leisure-located outlets.

What role do delivery platforms play in rural New Zealand?

Providers such as DoorDash expanded into towns like Tokoroa and Wānaka, albeit at higher per-delivery costs due to sparse order density.

Page last updated on: